Sample Category Title

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD continued its bullish momentum yesterday topped at 1.1658. The bias is bullish in nearest term testing 1.1712 (2015 high). Immediate support is seen around 1.1580. A clear break below that area could lead price to neutral zone in nearest term testing 1.1500 region but as long as stay above 1.1285 key support I remain bullish and any downside pullback should be seen as a good opportunity to buy. On the upside, a clear break and daily/weekly close above 1.1712 would expose 1.1870 – 1.2000 region next week.

GBPUSD

The GBPUSD had a bearish momentum yesterday bottomed at 1.2932. The bias remains bearish in nearest term as a part of the bearish scenario after formed a bearish pin bar at 1.3100 resistance area as you can see on my daily chart below. Note that the trend line support and 1.2935/00 area is a good support which need to be clearly broken to the downside to continue the bearish scenario testing 1.2810/00 area. Immediate resistance is seen around 1.3000 – 1.3030 region. A clear break above that area could lead price to neutral zone in nearest term retesting 1.3100 key resistance which need to be clearly broken to the upside to stop the bearish scenario and reactivate my bullish mode.

USDJPY

The USDJPY was volatile but indecisive yesterday. The bias is neutral in nearest term. Although we haven’t seen a nice and convincing bullish run, as long as stay above 111.45 key support, the bullish pin bar scenario should remain intact testing 112.75 area. A clear break and daily/weekly close above that area would expose 113.50 – 114.50 region next week. On the downside, a clear break and daily/weekly close below 111.45 would expose 110.25/00 region or lower. Overall I remain neutral.

USDCHF

The USDCHF attempted to push higher yesterday topped at 0.9618 but closed lower at 0.9513. We have a bearish pin bar (continuation) formation as you can see on my daily chart below suggests a potential bearish view after a rejection to move above 0.9620 resistance area. The bias is bearish in nearest term testing 0.9450 which remains a good place to buy with a tight stop loss as a clear break and daily/weekly close below that area would expose 0.9250 region next week. Immediate resistance is seen around 0.9550 followed by 0.9620.

ECB Calls For Patience, But Suggests It Will Provide Policy Signals In Autumn

- Draghi still keen to keep policy options open as far as possible

- Healthier activity suggests autumn announcement of reduction in policy support

- ECB confidence that inflation will head higher contrasts with latest Fed concerns

- Is today's FX market reaction to Draghi a form of 'taper tantrum'?

- Euro exchange rate could become a hot topic in holiday thinned markets

There was little expectation that the ECB would announce any major policy shift today, but there was some anticipation that it might move away from a commitment to step up its asset purchase programme if conditions were to weaken (it didn't alter this) and there was also the possibility that it would provide some clarity as to when and what actions might be taken to scale back its current 'very substantial degree of monetary accommodation' (Mr Draghi set out not to do this either).

In the event, Mr Draghi said little new. While he did promise the ECB would have 'significant discussions' on its policy stance in the autumn, his repeated calls for 'patience and persistence' suggest a strong desire to prevent the market from anticipating any early or dramatic policy shift from the ECB.

Unfortunately for Mr Draghi, even the not surprising suggestion that policy would be reviewed in the months ahead prompted FX markets to push the Euro higher against other major currencies. Given that Mr Draghi noted that the Euro's firmer tone of late 'received some attention' at today's Governing Council meeting, a further strengthening of the currency was probably not tintended outcome. There is little question that the ECB wants to give the current upswing in the Euro area more time to strengthen and spread. However, the main reason for Mr Draghi's caution today relates to persistently low inflation and the risk that a premature policy tightening or the market's anticipation of such a move would push inflation even further from target. Arguably, the most notable comment from today's press conference was the ECB president's assertion that 'the last thing the governing council wants is an unwarranted tightening of financial conditions that slows down or jeopardises the convergence of inflation' towards the ECB target.

Unfortunately for the ECB, even a relatively innocuous if upbeat assessment of the Euro area's economic prospects is likely to strengthen the Euro on FX markets, particularly on a day when the Bank of Japan downgraded its economic outlook and at a time when there is significant uncertainty about policymaking in the US- whether that relates to recent Federal Reserve concerns about below target inflation or broader issues such as Mr Trump's difficulties in pursuing his domestic legislative agenda. This meant that even though interest rate markets moved little in response to Mr Draghi's pronouncements, the Euro rose to its highest level against the US dollar in two and a half years.

There is little question that the ECB is increasingly confident about the persistence of the current momentum of activity in the Euro area. As the diagram below suggests, this simply reflects the current reality. If we exclude the early 2015 figures swollen by outsized and unrepresentative step-changes in Irish GDP, the current pace of growth is the strongest in six years.

Today's press statement recognises this and highlights 'a continued strengthening of the economic expansion in the euro area, which has been broadening across sectors and regions'. It goes on to refer to a global recovery that 'should increasingly lend support to trade and euro area exports'. Perhaps of greater significance, it adds to previously cited supports for consumer spending such as employment gains, an additional factor in the shape of 'increasing household wealth'.

We draw attention to the addition of a reference to wealth effects for a couple of related reasons. First of all, these wealth effects reflect strong and broadly gains in both house prices and equity markets that serve to reinforce Mr Draghi's contention that 'financial conditions remain broadly favourable'. Arguably, of greater significance for future policy considerations is that at some point such wealth effects could come to be seen as threatening from a financial stability perspective. This is not to suggest the ECB is currently concerned about these developments but they are clearly on its radar and may eventually encourage a desire to 'lean against the wind' by introducing a less expansionary policy stance.

If Mr Draghi was keen to emphasise the good news on economic activity, he was notably more restrained in relation to inflation but, here too, it could be argued that he was perhaps a little less dovish than might have been envisaged. The text of the ECB press statement emphasises that 'measures of underlying inflation remain overall at subdued levels' although the addition of the word levels might serve to acknowledge a slight pick-up in core inflation in recent months which is evident in the diagram above. Mr Draghi instead focussed on the current level of inflation, indicating that it 'is not where we want to be'. However, he also stated the belief that the factors holding back inflation 'will last for some time' but they're 'not permanent'. He further asserted that the ECB is confident that the inflation will reach its target in light of the strength of growth even if progress is gradual.

In terms of interest rate markets, the ECB's assessment of the inflation outlook is comforting as it implies the ECB can implement a reasonably slow and orderly pace of policy adjustment. Again, however, from an FX market perspective, the confidence with which Mr Draghi set out his expectations for modestly higher inflation stands in clear contrast to today's revised Bank of Japan projection that now sees its inflation target being hit during fiscal 2019 rather than 2018 as it envisaged three months ago.

It could also be argued that Mr Draghi's assessment is more confident in tone than several recent pronouncements from the US Federal Reserve that reflect a measure of surprise at a softer trend in US inflation of late. For these reasons, it is not entirely surprising that the exchange rate of the Euro has moved higher today although the scale of move likely owes something to holiday thinned trading conditions in FX markets.

How enduring today's currency moves prove to be and whether market interest rates follow may depend on how investors eventually assess Mr Draghi's indication that the ECB would have 'discussions in full' on the economic and inflation outlook as well and the implications for policy 'in the autumn' . In response to a persistent line of questioning, he refused to clarify whether this timeframe referred to the ECB governing council's next policy meeting on September 10th, nor would he provide any guidance on what specific policy options might be considered at that point. He repeatedly answered that the ECB had not discussed when or what the ECB might alter its current stance or even signal an intention to do so. Clearly, Mr Draghi is eager to keep all options open for now.

Our sense is that upcoming data are likely to confirm the increasing strength of the upswing in activity and may also suggest a tentative firming of inflation. In such circumstances, it could be expected that, at its September meeting, the ECB would signal an intention to taper, or in its language to 'recalibrate', its asset purchase programme and Mr Draghi could even provide some indications in this regard when he speaks at the high profile Federal Reserve Jackson Hole conference in late August. Of course, a more uncertain backdrop could push these announcements back to the following ECB governing council meeting on October 26th.

In the interim, however, the ECB is likely to pay even more attention to the performance of the Euro on FX markets. ECB research suggests that a 1% change in the currency alters inflation by about 0.1% in the opposite direction within twelve months and by about 0.3% over three years. This would threaten to push inflation further away from the ECB's target. Of course, the restraint offered by a higher exchange rate would be partly offset by the boost coming from stronger growth at present but, on balance, inflation would likely stay uncomfortably below the ECB's desired level.

More immediately, we have a strong sense that the ECB may be experiencing a bout of 'taper tantrums' today. However, unlike the US precedent in 2013, this is being seen in the potentially more volatile and more difficult to manage FX markets rather than in the bond market. Mr Draghi and his colleagues may not get the quiet summer they so clearly want.

ECB Review: QE Path Not Defined Yet But Slower Purchases Are Coming

The ECB kept unchanged policy rates, its QE programme, its forward guidance and QE easing bias. Hence, the ECB is still signalling its readiness to increase the size and/or duration of the QE purchases. The unchanged QE easing bias was perceived as dovish, as 47% of economists in a Bloomberg survey had expected the ECB to remove the reference to its readiness to increasing the size of the QE programme.

According to President Mario Draghi, the Governing Council was unanimous in setting no precise date for when to discuss changes to the QE programme but argued 'our discussion should take place in the autumn'. Additionally, Draghi said the ECB has not tasked its staff to look into QE options after December 2017. This suggests the ECB is not ready to make an announcement at the September meeting on how QE purchases will continue next year. We maintain our view that the ECB will continue its QE purchases but at a reduced pace of EUR40bn per month in H1 18 and now believe this will be announced at the October meeting (previously September).

Today's decisions from the ECB reflect its increased focus on the inflation outlook versus the economic recovery compared with what was communicated in Draghi's speech at the ECB forum in Sintra. First, Draghi did not repeat that in a situation where the economy continues to recover, a monetary policy tightening could be needed in order to keep the policy stance 'broadly unchanged'. Second, he reiterated that higher inflation is conditional on the monetary stimulus and that the ECB needs to be 'persistent and patient and prudent'.

On a more hawkish note, Draghi argued the financing conditions remain broadly supportive. This judgement was based on yields being low by historical standards, sovereign and corporate spreads being tighter and bank lending rates being at very supportive levels dominating the repricing of the exchange rate, which had received some attention among ECB members. That said, the ECB still has an eye on the conditions, as Draghi said a financial tightening was 'the last thing' the ECB needs.

It will be very interesting to see whether Draghi's main focus will be on his belief in the Phillips curve (i.e. the economic recovery will eventually lift wage inflation) at Jackson Hole when he is together with other global central bank governors. Given today's communication, this seems less likely, as he argued the ECB is waiting for more information (including the updated projections in September) but this could change ahead of Jackson Hole.

The euro generally gained during Draghi's press conference and EUR/USD still trades in overbought territory, in our view. Hence, we see risks skewed on the downside in the near term. In particular, we note that EUR/USD price actions contrast with European fixed income markets, where, for example, 2Y EUR swap interest rates fell back after the press conference, while EUR/USD remained higher. Our short-term financial models cannot fully explain the move higher in EUR/USD (given lower interest rates). Moreover, positioning and other short-term technical measures such as the RSI also indicate that the risk of correction lower in EUR/USD is high. However, we maintain the view that any dips in EUR/USD are likely to prove short-lived and, strategically, we still like to buy the cross on dips. Longer term, we still see the cross higher, targeting 1.18 in 12M. See FX Strategy: Healthcare failure lifts EUR/USD to overbought territory, 18 July.

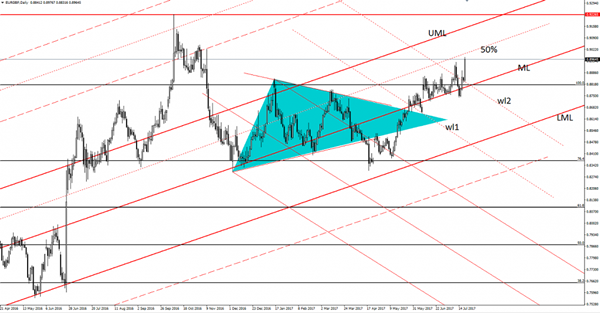

EUR/GBP Further Increase Expected, EUR/CHF Another Breakout Attempt, Brent Oil In The Buyers Territory

EUR/GBP further increase expected

The price increased significantly in the yesterday's session and climbed much above the 0.8948 previous high, should increase further because is trading inside the buyers territory. Has rallied aggressively after a false breakdown on Monday.

The Euro increased significantly versus all its rivals and could climb towards fresh new highs despite the dovish ECB. As you already know, the European Central Bank maintained the interest rate at the 0.00% historical minimum, but we may have another QE next year.

EUR/GBP jumped much higher after the false breakdown below the median line (ML) of the major ascending pitchfork, I've said in the previous analysis that will jump much higher if will stabilize above the 100% Fibonacci level and above the second warning line (wl2) of the minor descending pitchfork.

The next upside target will be at the 50% Fibonacci line (ascending dotted line), but most likely will approach the upper median line (UML) of the of the ascending pitchfork.

The Cable dropped also versus the USD even if the Retail Sales have increased by 0.6% in June, more versus the 0.4% estimate.

Price is strongly bullish on the short term, technically should approach also the 0.9226 static resistance, where he may find strong resistance again.

Could move sideways between the 0.9226 and the 76.4% retracement level in the upcoming months because I don't believe that will have enough energy to breakout from this range and to make a larger move.

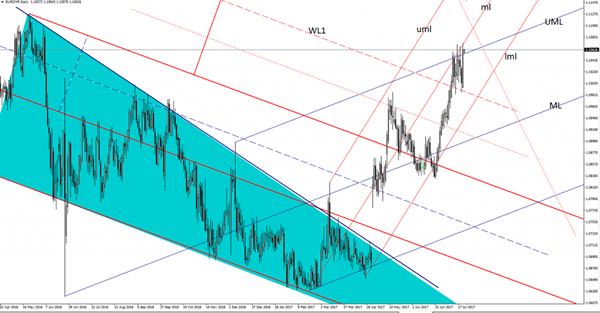

EUR/CHF another breakout attempt

Price increased sharply in the yesterday's session and erased the last day's losses, looks determined to reach new highs, but is facing a tough resistance on the Daily chart.

Maintains a bullish perspective on the Daily chart despite the last day's minor correction, will climb much higher is will stay above the 1.1050 psychological level.

Price jumped above the upper median line (UML) of the major ascending pitchfork, a valid breakout will signal a further increase. Only a false breakout will send the rate down again, the perspective remains bullish as long is trading within the minor ascending pitchfork's body because a breakdown will signal a broader drop.

Brent Oil in the buyers territory

Price slips lower after the aggressive breakout above the 50% retracement level, could come down to retest the static support (resistance turned in support). We may have a buying opportunity if will retest the 50% level, the next upside target will be at the sliding line (descending dotted line).

Yen Uninspired By The BOJ

Yen still sluggish post BOJ

We had some volatility on the USD/JPY today, has dropped in the morning and has touched some important support levels, remains to see in the upcoming days because a further Nikkei increase will send the Yen much lower versus all its rivals.

USD/JPY stays above the 111.90 level, even if the USDX is under massive selling pressure after the USDX’s drop. The greenback and the Yen have lost significant ground versus the other major currencies. As you already know, the BOJ keeps the policy unchanged, the BOJ Policy Rate remains steady at -0.10%, matching expectations.

The Yen has taken a hit also from the Japanese Trade Balance, which has dropped from 0.12T to 0.08T in the previous month, much below the 0.12T estimate, while the All Industries dropped by 0.9% in May, much versus the 0.8% estimate.

Aussie plunged on Australian data

The Australian dollar dropped significantly in the morning after the economic data was released, the Employment Change decreased from 38.0K to 14.0K, much below the 14.4K estimate, while the Unemployment Rate remains steady at 5.6% for the second month in June

The Aussie has managed to recover versus the USD in the second part of the day as the USDX plunged aggressively. AUD/USD maintains a bullish perspective on the Daily chart, could hit new highs if the US data will continue to disappoint in the upcoming days.

Euro rallies despite dovish ECB

The European currency has appreciated aggressively versus all its rivals in the afternoon, even if the European Central Bank has maintained the Minimum Bid Rate steady at 0.00%, matching expectations. Euro reached new highs versus the greenback, Yen, Cable and versus the Swiss Franc and could resume the upside movement in the upcoming period because the pairs are located in the buyer’s territory.

USD – the buyers have disappeared

The US dollar continues to drop despite the mixed US data, is going down after the speculation that the FED will delay another rate hike. The greenback wasn’t impressed by the Unemployment Claims impressive drop, have dropped from 248K to 233K in the previous month, much below the 245K estimate, the CB Leading Index increased by 0.6%, beating the 0.4% estimate, but wasn’t able to save the dollar from downside.

No Muss No Fuss

No Muss no fuss

While the ECB's guidance remains unchanged, the central bank lack of concern on the surging euro was a strong enough signal to send traders scrambling for top side EUR FX exposure.

So much frenzy in EUR FX at the moment; it's hard not to get carried away with the action.

But one thing that is crystal clear, Investors want to be long EUR and related proxies heading into the asset-purchase program (APP) taper which may be announced as early as the Jackson Hole 2017 Economic Symposium,(Aug. 24-26, 2017.).Circle Draghi's August 25th speech on the calendar as this will be a huge event so expect vol risk premium to ratchet higher as we near that date

But this move is not just about Draghi failing to express a currency view. The EUR kicked into high gear taking out 2016 high when news hit that Special Counsel Robert Mueller was looking into President Donald Trump's business transactions as part of the exploration into the Trump campaign's ties to Russia. This revelation is huge as just last week President Trump said that expanding the investigation beyond Russia would be out of bounds so with Muller broadening the Inquisition into Trump's business dealings, US political risk could move to whole new level as this foxtrot plays out.

Euro

Price action suggests US dollar selling remains the Flavour du Jour as investors were caught desperately short of euro. When it rains, it pours, so it seems for the beleaguered greenback these days which in the absence of critical primary economic data is unlikely to get a reprieve from the political lambasting the Trump administration is wearing.

Australian Dollar

The Euro is not the only game in town as the market sits tight awaiting an unblurred hawkish signal from RBA. After yesterday knee-jerk higher on last month's robust jobs performance with a +62k print in full-time employment, profit taking set in immediately as yield retraced in a blink of the eye.But I suspect Aussie longs were getting a severe case of the heebie jeebies ahead of the RBA member Guy Debelle's speech as he will be peppered with questions about the surging A$ and the market reaction to the RBA minutes

Two outcomes, Debelle does the Draghi shuffle and fails to discuss FX and policy in the same sentence, or he takes the opportunity to pare back recent moves in both yield and the currency. Either way, this could get exciting.

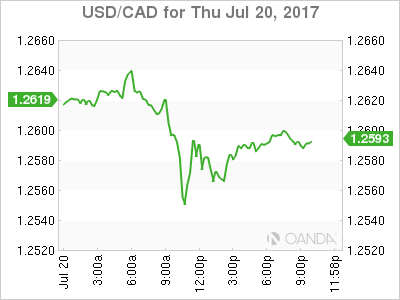

USD/CAD Canadian Dollar Higher On NAFTA Optimism

The Canadian dollar appreciated slightly on Thursday as comments from Mexican officials gave more details surrounding the upcoming NAFTA renegotiation talks. The loonie is higher despite a setback in oil prices. After three weeks of weekly US drawdowns energy prices lost close to 1 percent. Canadian data due on Friday could reverse the CAD rally with inflation and retail sales setbacks forecasted.

NAFTA Details Shared

Canadian and Mexican diplomats met on Wednesday to discuss their collective strategy ahead of the NAFTA first round of talks scheduled for August 16. Mexican sources revealed the plan is to hold seven rounds of talks in three week intervals. The aggressive schedule is designed to end negotiations before the Mexican presidential elections and the US midterm elections which could encumber trade talks. The Mexican ambassador to the United States has said that the possibility of the Trump administration could back out of the talks remains.

Bare US Economic Calendar

Lack of economic data in the US and the cloud of uncertainty around the Trump administration have impaired the US dollar. The U.S. Federal Reserve appears to be turning dovish after a hawkish start of the year with two rate hikes. Inflation remains weak but the central bank estimates it to be a “temporary” set back.

CAD Steady Ahead of Canadian Retail Sales and Inflation

The USD/CAD lost 0.131 in the last 24 hours. The currency pair is trading at 1.2575. The loonie is rising despite losses in energy prices as the US dollar weakness is the biggest trend in the market. The hawkish Bank of Canada (BoC) comments in June were followed by a rate hike in July and high probability of more to come before the end of the year. The CAD is closing the interest rate divergence with the USD as Canadian fundamentals have validated the actions of the central bank.

The next obstacle for the loonie will be the release of retail sales and consumer price index (CPI) data on Friday at 8:30 am EDT. The BoC faces a similar concern on soft inflation with other major central banks. Canadian inflation is expected to have slowed down by 0.1 percent last month. Retail sales are also estimated to have lost momentum by only gaining 0.3 percent and could be flat after removing the volatile auto sales.

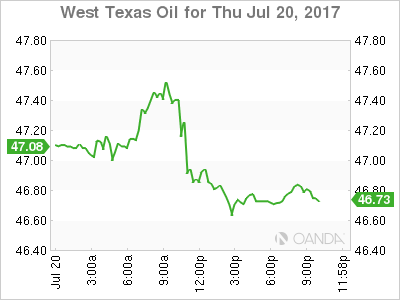

WTI Lower Ahead of Russia Summit

The price of energy lost 0.933 on Thursday. West Texas Intermediate was trading at $46.69 in anticipation of next week’s meeting between a select group of Organization of the Petroleum Exporting Countries (OPEC) and other major producers in Russia. The group will sit down to review compliance targets and there is a possibility for further measures or changes to the current agreement that runs until March of 2018.

The meeting between OPEC and Russia to discuss compliance later this month will open the door for the next steps for energy producers. A bigger cut in production after the agreed extension is in the cards, but there are some voice of dissent as current levels are causing distress for countries who depend on oil sales to balance their budget. Rising production in Nigeria and Libya as well as a higher rig count in the US have put downward pressure on energy prices despite the efforts of the OPEC and other major producers. Political infighting could fracture the OPEC with Saudi Arabia and Iran casting doubts on how unified the group will be going forward. Compliance with the production cut agreement has been stellar, but mostly on the efforts of Saudi Arabia, which could be entering a seasonal push for higher production along with comments from other OPEC members like Ecuador and Venezuela that want to increase production to balance their country’s budget.

Market events to watch this week:

Friday, July 21

8:30 am CAD CPI m/m

8:30 am CAD Core Retail Sales m/m

Gold Climbs To 3-Week High As ECB, BoJ Maintain Loose Policy

Gold has posted gains in the Thursday session. In the North American session, spot gold is trading at $1246.18, up 0.46% on the day. On the release front, the ECB and Bank of Japan both held the course with their ultra-loose monetary policy. In the US, the numbers were a mixed bag. Unemployment claims dropped to 233 thousand, marking a 9-week low. The news was not as positive on the manufacturing front, as the Philly Fed Manufacturing Index slowed down to 19.5, its weakest reading since November 2016.

Gold prices have moved higher after the European and Japanese central banks announced that they would continue their accommodative monetary policy. As well, the ECB and BoJ maintained the current policy of ultra-low interest rates, at 0.00% and 0.10% respectively. With the economies in the eurozone and Japan both showing improvement, their has been pressure on policymakers to reduce stimulus. However, inflation levels in the eurozone and Japan are well below the target of 2%, and the banks have reiterated that they will not taper asset-purchases until inflation levels move higher. The ECB is expected to revisit its monetary stance at its September meeting, and if policymakers decide to tighten monetary policy, gold prices could head lower.

President Trump hasn't done very well at learning how to tango with Congress, and this week's debacle on Capitol Hill could make the gap between Trump and Republican lawmakers even harder to bridge. Trump had vowed to replace Obamacare, but his health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility will take another hit if he's unable to do so. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.

Despite Draghi’s Best Efforts

The euro sent a powerful signal on Thursday as it surged to 23-month highs despite continued dovish rhetoric from Draghi. EUR was the top performer while sterling lagged. Politics are also back on the trading agenda. A new EUR trade & charts analysis was issued before the ECB press conference. Both the Arabic and English videos are posted below for subscribers.

Days like Thursday make it tough to explain currency moves but also make the underlying market dynamics clear. The ECB didn't make any meaningful changes to its statement. References to the size and duration of QE programs were unchanged and that initially sent the euro slightly lower.

Fast-forward to the press conference and a rally in the euro took hold that extended as high as 1.1658 from a low of 1.1479. Was it something Draghi said in the press conference? Hardly. He was clear the governing council was unanimous about no changes to forward guidance and he continued to preach patience.

At best there was some of the big picture optimism we warned about but it came in a small dose as he said that incoming information confirmed that the strengthening of the economy is broadening. That was balanced by a warning that underlying inflation had yet to show convincing signs of a pickup. His words were carefully chosen as to avoid any hawkish signals and a repeat of the Sintra speech fallout. He failed, nonetheless.

So while there was no clear catalyst for the gain, it is inevitable that QE will be curtailed further this year. The aggressive euro buying points to the underlying demand for EUR. It cruised through resistance at the 12-month high and finished the day with a strong bid. Ultimately, the market senses that a shift in Draghi's tone is inevitable and euro buyers have jumped into the race before the starting pistol.

At the same time, some of the EUR/USD strength Thursday also came from the other side of the trade. The US dollar sold off on a report that the Trump-Russia investigation had broadened to include his business deals. In the past, though, those type of politically-driven market moves have faded.

The Euro Surged Further

The Euro surged further after being initially pushed higher by remark from ECB chief Draghi that discussion should take place in the autumn, which heated his post-EB policy meeting speech, generally seen as usual dovish mantra.

Draghi said expecting inflation to rise only gradually and substantial degree of accommodation is still needed, similar wording to his speech three weeks ago.

Fresh boost for the single currency came from news about expanding Russia probe to Trump's business transactions which sent the dollar lower across the board.

The Euro enjoyed strong supports and spiked to the highest levels in over two years, hitting so far high at 1.1658.

The pair is riding on extended wave C of five-wave cycle from 1.1188 which dented its FE100% at 1.1643 and heading towards target at 1.1735 (Fibo 38.2% of 1.3992/1.0340 descend).

With daily indicators entering overbought zone, the pair may show hesitation ahead of 1.1735, with corrective easing expected on firmer bearish signals.

Tuesday's high at 1.1583 now acts as initial support, followed by rising daily Tenkan-sen which tracks the ascend for over three weeks, currently at 1.1514.

Res: 1.1658; 1.1700; 1.1735; 1.1800

Sup: 1.1600; 1.1583; 1.1556; 1.1514