Sample Category Title

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8918

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency has risen again after finding support at 0.8829, suggesting near term upside risk remains and gain to resistance at 0.8950 cannot be ruled out, however, beak there is needed to retain bullishness and confirm recent upmove has resumed for headway to 0.8975-80, then towards psychological resistance at 0.9000 which is likely to hold from here due to near term overbought condition.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 0.8865-70 would bring test of said support at 0.8829 but break there is needed to prolong consolidation below said resistance at 0.8950 and bring another corrective fall to 0.8780-85, then towards previous support at 0.8743 which is likely to hold from here.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Markets Not Buying What Draghi Has to Sell

There may have been no hints at tapering in September in today's ECB statement or in Mario Draghi's press conference but traders certainly found reason to drive the euro higher, something the ECB President was clearly trying to avoid.

I don't think Draghi could have possibly adopted a more dovish stance at the press conference without suggesting that tapering will not happen later this year. Rather than discuss the possibility of tapering, Draghi was determined to avoid laying the foundations for such a move and instead insist that asset purchases could rise or be extended, a clear attempt to avoid the taper tantrum that the Federal Reserve was forced to contend with four years ago.

What we learned from today's meeting though was that the ECB probably doesn't have anything to worry about. The market is already working off the assumption that the ECB will gradually phase out bond buying, with the program likely ending by the end of next year, possibly even the third quarter. This was made clear when the euro rallied despite the repeated insistence from Draghi that tapering wasn't discussed and further analysis will be done in the Autumn, in other words when the ECB next meets in September and has access to the latest macro-economic projections.

Perhaps it's time for the ECB to focus less on the intraday movements in the single currency and more on being transparent on its intentions because as it is, they're fooling nobody and the market reaction today suggests they're suffering credibility damage along the way.

None of this is to say that traders believe the ECB is on a pre-set course. The Fed wasn't either despite it's clear intentions to phase out its QE program and other central banks won't be when they begin normalising monetary policy. Changes in the data could force the ECB to change course but it seems that the central bank is more concerned with managing the currency than guiding traders.

Trade Idea: USD/CAD – Sell at 1.2765

USD/CAD - 1.2600

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway with wave iii ended at 1.4690, wave v of C may bring one more marginal rise probably in 2018

Trend: Near term down

Original strategy :

Sell at 1.2765, Target: 1.2565, Stop: 1.2825

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2765, Target: 1.2565, Stop: 1.2825

Position: -

Target: -

Stop:-

The greenback has remained under pressure, suggesting recent downtrend is still in progress, adding credence to our bearish view and we took the count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii still in progress, hence bearishness remains for this fall to extend weakness to 1.2550-60, then towards 1.2500-10, however, oversold condition should prevent sharp fall below 1.2440-50, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell the pair again on recovery as 1.2760-70 should limit upside. Above 1.2800-10 would defer and risk a stronger rebound to 1.2850-60 but only break of latter level would signal a temporary low is formed instead, bring retracement of recent decline to 1.2900-10, then 1.2940-50, however, price should falter below 1.3000 and the greenback shall head south again from there.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

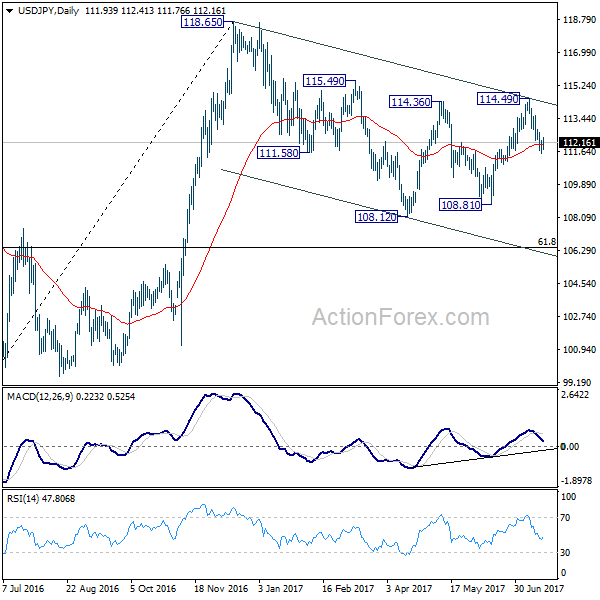

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.58; (P) 111.90; (R1) 112.26; More...

A temporary low is in place at 111.54 and intraday bias is turned neutral first. Some consolidation could be seen but another fall is expected as long as 112.85 resistance holds. Below 111.54 will target 108.81 low. Break there will extend the whole correction from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.85 will turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

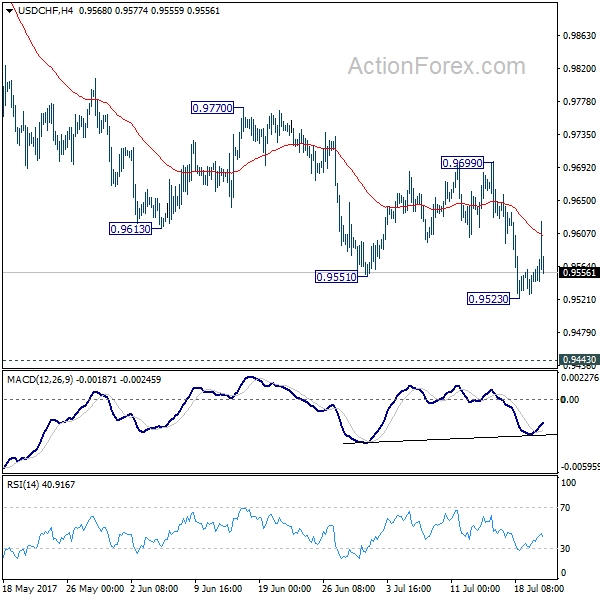

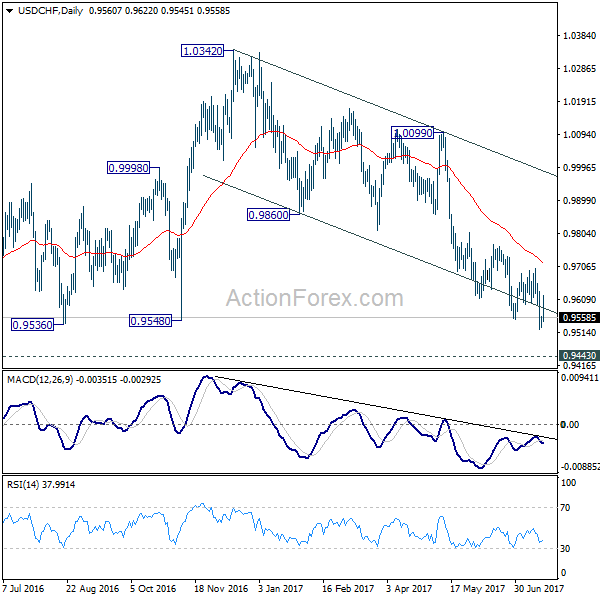

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9535; (P) 0.9548; (R1) 0.9567; More...

Some volatility is seen in USD/CHF today but it's, after all, staying in range of 0.9523/9699. Intraday bias remains neutral for consolidative trading. Upside of recovery should be limited well below 0.9699 resistance and bring fall resumption. Break of 0.9523 will extend the decline from 1.0342 and target 0.9443 key support level next. At this point, we'd expect strong support from there to bring rebound.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

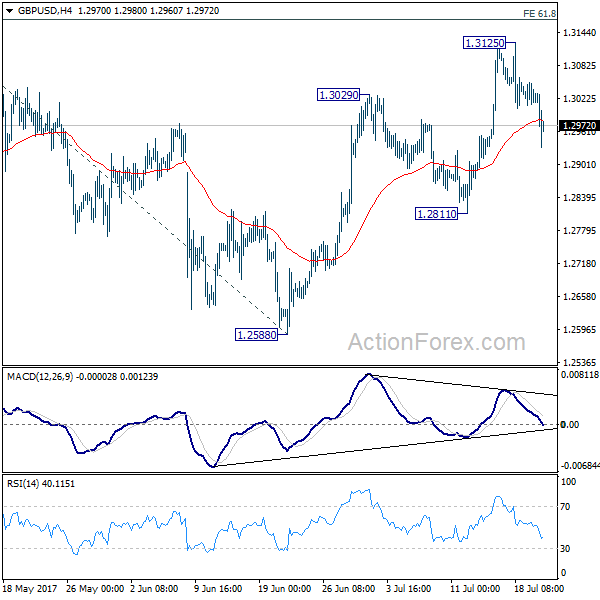

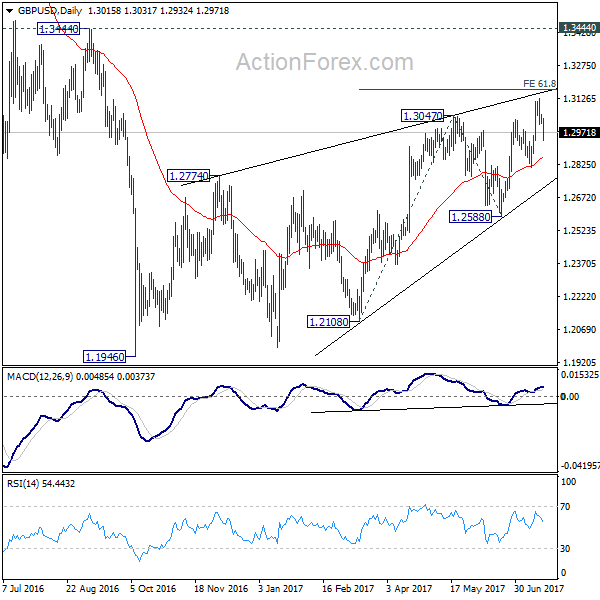

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3005; (P) 1.3028; (R1) 1.3047; More...

GBP/USD's pull back from 1.3125 extends lower today but it's staying well above 1.2811 support. Intraday bias remains neutral and another rise is still in favor. Break of 1.3125 will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. Overall, choppy rebound from 1.1946 is seen as a corrective pattern, hence, we'd be cautious on strong resistance from 1.3168 to limit upside. But firm break of 1.3168 will bring further rise towards 1.3444 key resistance. Meanwhile, break of 1.2811 support will be the first sign of reversal and will turn bias to the downside to target 1.2588 key support next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

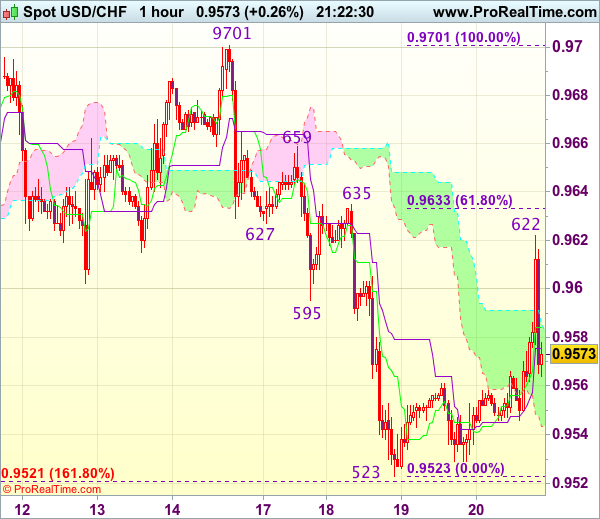

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9566

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback staged a strong rebound to 0.9622, the subsequent quick retreat after faltering below indicated resistance at 0.9635 suggests further choppy trading would be seen and weakness to 0.9540-45 cannot be ruled out, however, break of support at 0.9523 is needed to confirm recent decline has resumed for weakness to 0.9500, then towards 0.9475-80 later.

On the upside, above 0.9600 would bring another test of 0.9622 but only break of said resistance at 0.9635 would confirm low is formed instead, bring a stronger rebound to resistance at 0.9659 which is likely to hold on first testing. As near term outlook is mixed, would be prudent to stand aside for now.

ECB’s Mario Draghi Words Lose its Magic

Prudent and patience remains the theme

The big news out of the European Central Bank (ECB) so far this morning is that it is keeping the window open for more QE.

The ECB said it "could increase QE in size, duration if the outlook worsens," when many expected that language to be removed from its statement.

Press Comments:

Draghi

- Information Confirms Strengthening Econ Expansion

- Risks to Growth Outlook Broadly Balanced

- Economic Expansion Not Yet Translated to Stronger Inflation

- Headline Inflation Dampened by Energy

- Underlying Inflation Still Subdued

- Very Substantial Degree of Accommodation Still Needed

- Stand Ready to Increase Asset Purchases If Needed

- Data Point to Solid Broad-Based Growth in Period Ahead

- Private Consumption Supported by Employment Gains

- Global Recovery Should Support Exports

- Growth Prospects Dampened by Slow Pace of Structural Reforms

- Current Positive Momentum Increases Chances of Stronger Upswing

- Downside Risks Primarily from Global Factors Still Exist

- Headline Inflation at Current Levels in Coming Months

- Measures of Underlying Inflation Still Low

- Private Sector Loan Recovery Is Proceeding

- Pass Through of Policy Measures Support Borrowing Conditions

- Need Substantial Step Up of Structural Reforms

- No Convincing Sign of Pick Up in Underlying Inflation

- We Need to Be Persistent and Patient, 'We Aren't There Yet'

- We Were Unanimous in Communicating No Change to Guidance

- We Were Unanimous in Setting No Precise Date on When to Discuss Changes

- Our Discussions Should Take Place in the Autumn

- Financing Conditions Broadly Supportive for Achieving Inflation Goal

- Re-pricing of Exchange Rates Has Received Some Attention

- We Are Confident It Will Get There, But It's Not There Yet

- Will Stay in Market for Long Time

- Serious Progress in Greece in Last Several Months

Net result: The market does not see Mario Draghi as "dovish" enough in the press conference, which is sending the EUR higher – last trades up +0.4% versus the U.S. dollar at €1.1561

Draghi is now expected to use the Jackson Hole Federal Reserve conference in August (24-26) to prepare the ground for a bond-buying program tapering announcement in September. Why? The ECB wants to keep the market guessing for another month so that it could manage expectations better.

Yen Dips as BoJ Pushes Back Inflation Target

USD/JPY has posted slight gains in Thursday trading. In the North American session, the pair is trading at 112.12, up 0.15% on the day. On the release front, the Bank of Japan maintained rates at 0.00%, but extended the timeline for its inflation target. In the US, indicators were mixed. Unemployment claims dropped to 233 thousand, marking a 9-week low. As well, the Philly Fed Manufacturing Index slowed down to 19.5, its weakest reading since November 2016.

There were no surprises from the Bank of Japan, which maintained its ultra-loose monetary policy. The bank kept interest rates at 0.00%, and maintained its inflation target at 2.0%. However, in light of persistently low inflation levels, the BoJ extended the timeline for the inflation target by one year, saying it expected inflation to reach 2% by fiscal year 2020. The BoJ has kept in place its inflation timeframe of 2% since 2013, and has had to postpone it six times, as the bank's radical asset-purchase program has failed to end deflation. BoJ Governor Haruhiko Kuroda has insisted that the inflation target is feasible, and blamed low inflation on external factors, such as low oil prices. The bank was more upbeat in its economic forecast than in June, but with the bank stubbornly clinging to its inflation target, the markets don't expect any withdrawal of stimulus until 2018 at the earliest.

It's been another brutal week for the Trump administration, which is sorely in need of a legislative victory in Capitol Hill. One of Trump's flagship projects has been replacing Obamacare, but that goal may have been dashed this week. Trump's health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility and popularity will take another hit if he's unable to produce. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.

Trade Idea Update: GBP/USD – Sell at 1.3010

GBP/USD - 1.2975

Original strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3010, Target: 1.2915, Stop: 1.3045

Position : -

Target : -

Stop : -

Cable has dropped after breaking support at 1.3005, suggesting top has been formed at 1.3126, hence consolidation with mild downside bias is seen for weakness to 1.3930-32 (61.8% Fibonacci retracement of 1.2812-1.3126), then test of previous support at 1.2912, however, break of latter level is needed to retain bearishness and extend the fall from 1.3126 top to 1.2880-85 first.

In view of this, we are looking to sell cable on recovery but at a lower level as 1.3005-10 should limit upside. Only break of resistance at 1.3062 would abort and signal an intra-day low is formed instead, bring a stronger rebound towards 1.3090-00 but resistance at 1.3126 should remain intact.