Sample Category Title

ECB Stands Pat; Dovish Draghi Fails to Dent Bullish Euro

The European Central Bank maintained its highly accommodative monetary policy stance at the end of its two-day meeting today, confounding expectations that it would take another baby step towards exiting from its stimulus program.

As widely expected, the ECB held its key rates and pace of asset purchases unchanged. However, following the small tweaks to the forward guidance seen at previous meetings this year, many analysts were anticipating the ECB to make further modifications to its statement by dropping its easing bias. But the ECB disappointed as it maintained its pledge that "the Governing Council stands ready to increase the programme in terms of size and/or duration".

The euro initially fell after the announcement, slipping to an intra-day low of 1.1478 against the US dollar. However, the single currency soon reversed higher after President Mario Draghi began his press conference where he repeated his recent upbeat assessment of the Eurozone economy. His remarks on inflation were not as positive and his overall tone was surprisingly dovish, but traders shrugged off Draghi's comments to drive the euro towards Tuesday's 14-month high, hitting 1.1573 dollars after the press conference ended.

Last month, Draghi had used an ECB forum in Sintra, Portugal, to signal that as the Eurozone economy improves, policy adjustment would be necessary. However, at today's press conference, Draghi was far from suggesting that policy tightening was forthcoming and instead emphasized the need to be patient.

"We need to be persistent and patient because we aren't there yet" stressed the ECB head, before adding that the Governing Council hasn't even decided on an exact date when they will begin the discussion of stimulus withdrawal. Draghi said, "We also were unanimous in communicating no change to the forward guidance and also we were unanimous in setting no precise date for when to discuss changes in the future – in other words, we simply said that our discussions should take place in the autumn".

The lack of confirmation that the September meeting would be used to announce the possible start of tapering was an unexpected development and suggests any decision could be pushed back till October. Draghi also reiterated that a substantial degree of monetary accommodation was still needed despite the "robust" recovery, as wages and underlying inflation remain subdued.

The ECB's latest stance opens the prospect that a full exit from the bond buying program is a long way off and that the central bank is in no hurry to abandon its easy monetary policy. However, looking at the reaction in forex markets, investors appear less convinced, with some analysts interpreting Draghi's words as an attempt to portray any future reduction in the size of asset purchases as mere policy adjustment rather than tapering.

Euro Rallies Despite Dovish Draghi; Sterling Weakens Despite Upbeat Retail Sales

The euro rallied to a near 14-month high against the dollar during the European session following ECB President Mario Draghi's speech at a news conference today. Sterling was briefly lifted against the US currency, but gave up on gains and was down on the day as the US session started. During the end of the session, forex markets reacted significantly on the back of just released news regarding Trump's links with Russia. The dollar index was down 0.60% at 94.22.

The euro had initially slipped to a two-day low against the greenback following the release of the ECB policy decision, which was kept the same. However, the eurozone currency rose towards a 14-month peak against the dollar after ECB President Mario Draghi said policymakers would discuss possible changes to its bond-buying scheme in the autumn. While Draghi said no date had been set for discussing any changes to the program, investors believed discussions in the autumn would lead to monetary tightening next year. The euro rose to as high as $1.1575 as Draghi spoke, near the 14-month highs of $1.1583 from earlier in the week and being up almost half a percent on the day. The next key event euro traders will be closely monitoring in hope for more clues is the Fed symposium in Jackson Hole (late August) at which Mario Draghi will speak this year.

The euro rallied further on the back of news that the special council is "examining a broad range of transactions involving Trump's businesses". Dollar/yen fell to 111.78 while euro/dollar rose to above the 1.16 level to last trade at 1.1630, its 23-month high, as the US session was underway.

Warm weather lured UK shoppers to splash during June, mostly on clothing that led the retail sales higher. The figure for June beat expectations to rise 0.6% month-on-month, above the 0.2% forecasted expansion and the 1.2% decline recorded in the previous month. The year-on-year number was also higher than expected and increased 2.9% versus the forecasted 2.5%. However, an official comment from UK's Trade Minister Liam Fox saying that the country could get by without a Brexit trade deal casted a cloud over the pound. This scenario, if true, could deter business activity as predicted by economists. Sterling rose against the dollar after the upbeat UK retail sales report today. Pound/dollar rose to 1.3017 immediately post the release, though it lost ground later in the session to last trade at 1.2991.

The two important economic data releases out of the US gave a mixed picture of the economy. The figure for initial jobless claims portrayed a positive image by coming in below expectations. The number of people seeking unemployment benefits fell to 233K for the week ending July 15, the lowest level in nearly five months. The figure is below the upwardly revised number for the prior week (248K). However, the Philadelphia Fed Manufacturing index for July disappointed by falling to 19.5, the lowest level since November 2016 and far below the expected level of 24 and the prior month's 27.6. The dollar rose slightly immediately after the data release, however it fell soon after. The US currency was last trading at 111.78 yen as the US session started.

Oil prices continued gaining during the European session with Brent reaching an intra-day high of $50.19 a barrel, above the key $50 level. Brent was last trading just another that level, while WTI was at $47.44, up 0.7% on the day.

Even though gold prices rose in the pre-US session on dollar weakness, it wasn't enough to offset earlier losses. The precious metal was last trading at $1,238.58 an ounce.

Pound Dips Below 1.30, UK Retail Sales Beat Estimate

GBP/USD has posted slight losses in the Thursday session. In North American trade, the pair is trading at 1.2990, down 0.25% on the day. In economic news, British Retail Sales posted a gain of 0.6%, above the forecast of 0.4%. US numbers were mixed. Unemployment claims dropped to 233 thousand, marking a 9-week low. On a sour note, the Philly Fed Manufacturing Index slowed down to 19.5, its weakest reading since November 2016. On Friday, the UK releases Public Sector Net Borrowing.

There was relief in the markets as British retail sales rebounded in June. After two sharp declines in the past three months, the key indicator rebounded with a respectable gain of 0.6%. Warm weather was a key factor in the gain, as a warm June translated into stronger clothing sales. Despite the solid June release, British consumers have plenty to worry about. The reality of Brexit has arrived, as British and EU teams have sat down to negotiate a divorce which promises to be extremely complex. Inflation is at higher clip than wage growth, meaning the consumer has less purchasing power. Finally, the weak pound (a key factor behind high inflation) has meant that imports have become more expensive.

British CPI has been picking up speed in recent months, but the indicator slowed to 2.6% in June, down from 2.9% in May. This was considerably lower than the estimate of 2.9% and the first time in 2017 that inflation levels have not increased from the previous reading. The soft data eases the pressure on the BoE to raise rates in order to curb high inflation levels. Policymakers at the BoE have been at odds over raising rates – even though inflation is high, the economy has been showing signs of weakness, raising concerns that the economy does not need higher interest rates. On Tuesday, BoE Governor Mark Carney said that the main factor behind high inflation was the fall in the pound, which has dropped sharply since the Brexit vote in June 2016. The BoE hold its next policy meeting on August 4, and analysts expect the policymakers to hold the benchmark rate at 0.25%, where it has been pegged since August 2016.

Brexit negotiators from Britain and the European Union met in Brussels earlier this week, marking the start of substantive negotiations on Britain's exit from the EU. After weeks of "discussions about what to discuss", the UK agreed to the European demand that the negotiations would focus on the rights of EU citizens in the UK and Britain's bill for leaving the EU, before entering talks on a new trade agreement. Britain has presented its position on guaranteed rights for EU citizens living in the UK, but EU negotiators have said that this offer doesn't go far enough. The EU has handed Britain an exit bill of EUR 69 billion, and although the May government has agreed that it owes funds to Brussels, it certainly will counter with a much lower figure. With significant gaps between the parties on both of these issues, the negotiations promise to be difficult. Another complication is internal dissent within the May government, with senior officials at odds over a 'transition period' for Britain after leaving Brexit. Finance Minister Philip Hammond has suggested a transition period of two years, but Brexit Secretary David Davis has said he wants the UK completely out of the single market when Brexit negotiations terminate in March 2019.

Soft Draghi Not Soft Enough to Hurt the Euro

- European equities started the day on a strong footing, supported by constructive earnings and dipped only temporarily during the ECB press conference. Daily gains of the Euro Stoxx 50 hover around 0.50%. American markets also opened in positive territory but gains are more limited than in Europe.

- Unsurprisingly, the ECB left its policy rate unchanged and maintains the pace of bond purchases. ECB present Draghi maintained a soft assessment. He acknowledged that the euro's strength "received some attention" and said a sudden change in financing conditions would be "the last thing the governing council wants". He also said "financing conditions remain broadly supportive to secure a sustained return of inflation rates towards our inflation aim".

- UK June Retail Sales June surprised to the upside, helped by warm weather conditions and early timing of the Muslim festival of Eid. Retail sales excluding auto fuel rose 0.9% M/M (3.0% Y/Y) while only a 0.5% rise was expected (2.5%). In the previous month, retail sales had declined by 1.5%.

- The weekly initial jobless claims in the US came in better than expected at 233K while 245k was expected, confirming healthy labour market conditions.

- The Philadelphia Fed's headline General Business Activity index declined more than 8 points from 27.6 in June to 19.5 in July. Consensus expected a smaller decline to 23. The number however still points to solid expansion. The survey also showed that price pressures moderated but price expectations for the six months to come rose.

- EU and UK negotiators ended their four-day round of talks today with little common ground found on the role of the European Court of Justice, the divorce bill or the Irish soft border. The clock is ticking on Brexit but talks on the free-trade agreement have to wait until "sufficient progress" has been made on the above mentioned issues.

Rates

Soft Draghi cannot really convince bond markets

Global core bonds moved up and down after the release of the ECB statement and during the press conference, but couldn't choose a firm direction. The statement was dovish, as the decision was unchanged from June, including the easing bias on the APP (asset purchase programme ,see below). The text of the statement was virtually unchanged and during the press conference Mario Draghi held a dovish tenure. The ECB doesn't want an unwarranted tightening of financial conditions and will eventually react if condition do tighten (easing bias). He was optimistic on the growth outlook, but doesn't see any tangible signs of a sustained upturn of underlying inflation. He said the general council was unanimously in its decision, including in having no precise date for when to decide on policy changes. The council left that deliberately open. The Committees were not charged with technical preparations for the implementation of the APP after end 2017 and he even suggested that the final discussion would not necessarily happen in September. It might be later. Despite this dovish performance, Bunds couldn't really catch a sustained bid.

The ECB kept, as expected, both its rates (repo: 0%, depo:-0.40%) and its guidance on rates unchanged. It expects rates to remain at the present level for an extended period of time and well past the horizon of the asset purchases. The ECB also confirmed the $60B/month asset purchases till at least the end of December 2017 and, contrary to about halve of the forecasters, it also kept its guidance on this point intact. "If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase our asset purchase programme in terms of size and/or duration."

At the time of writing, German yields fell very modestly by 0.5 (2-yr) to 2.1 bps (5-yr). The 30-year yield rose 0.4 bp. Changes on the US yield curve were limited too and range between flat (2-yr) to -2.2 bps (30-yr). On intra-EMU bond markets, peripherals benefitted from the Draghi comments. 10-yr yield spread changes versus Germany ranged from -4 bps (Portugal) to -7 bps (Italy/Spain).

Currencies

Soft Draghi not soft enough to hurt the euro

Today, the focus for global FX trading was on the ECB policy decision. The ECB left its policy unchanged, kept its commitment to extend asset purchases if needed and didn't commit on the timing of a policy reassessment. Despite this soft ECB communication, the euro rebounded during the press conference as the ECB president wasn't very worried on the recent rise of the euro. EUR/USD currently trades in the 1.1550 area. USD/JPY is little changed in the low 112 area.

The BoJ kept its policy unchanged overnight, as expected. The yen weakened slightly on the prospect that the BoJ will lag the Fed and the ECB on its way to policy normalisation. USD/JPY returned north of 112. However, changes were negligible. EUR/USD drifted lower toward the 1.15 mark as investors took partial profit on the recent rally ahead of the ECB decision.

During the morning session, trading in the major dollar cross-rate developed in wait-and-see modus as investors looked forward to the ECB policy decision and press conference.

The ECB, as expected, left its policy unchanged. The euro dropped temporary below the 1.15 mark as the ECB maintained its language that it stands ready to increase asset purchases in size and duration if the economy worsens. Sentiment changed however during Draghi's press conference. On a question regarding recent euro strength, the ECB president said that the euro repricing received some attention in the meeting but at the same time said that financing conditions remain broadly supportive. The 'objective' message from the ECB president was little changed from recent soft ECB communication but the market apparently expected that he would be more worried about the recent rise of the euro and the rise in EMU yields. This 'feeling' propelled the euro higher in the 1.15 area. EUR/USD currently trades in the 1.1555 area. The US eco data were mixed with the claims lower/better than expected and the Philly Fed index softer than expected, but the data hardly had any impact on the dollar. The fall-out from the ECB press conference had little impact on USD/JPY. The pair still trades in the low 112 area. Conclusion: the ECB president was soft, but not soft enough to weaken the euro. A decline of EUR/USD clearly needs support for a stronger dollar too.

Lack of progress in Brexit-talks weighs on sterling

Today, Brexit-noise rather than the retail sales data unexpectedly dominated the price action in sterling. UK trade secretary Fox in an interview repeated that the UK will try to secure a deal, but that it can survive without a deal. Comments from negotiators from both sides were more balanced, but couldn't hide deep differences on key issues at the end of this week's negotiations. EUR/GBP started a gradual rebound of the intraday lows in the 0.8835 area. The UK June retail sales (0.6% M/M and 2.% Y/Y) rebounded more than expected, but were not able to reverse the negative sterling sentiment. EUR/GBP soon resumed its intraday rebound to the high 0.88 area. Cable also lost about a full big figure and dropped to the 1.2950 area. This afternoon, the rebound of EUR/USD during the ECB press conference also filtered through into the major sterling cross-rates. EUR/GBP trades north of 0.89 again. Cable regained some ground in lockstep with EUR/USD and trades in the 1.2970 area.

EURUSD Rallied to Fresh 14-Month High as Draghi Promised QE Discussions in Autumn

ECB left interest rates and the QE program unchanged in July. The members also decided to keep the QE reference in the forward guidance. The central bank indicated it would continue buying assets in the market for some time and President Mario Draghi admitted that "inflation is not where we want it to be, nor where it should be" and "that's why a substantial degree of accommodative monetary policy is still needed". The single currency plunged after the dovish statement. However, it reversed to gains and jumped to a fresh 14-month high against USD after Draghi indicated that QE discussion would begin in autumn.

The central bank kept the main refi rate, the marginal lending rate and the deposit rate unchanged at 0%, 0.25% and -0.4% respectively. The central bank also affirmed that the QE program would be maintained at the monthly pace of 60B euro, which is "intended to run until the end of December 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim".

At the press conference, Draghi acknowledged that the economy is experiencing "a robust recovery where we only have to wait for wages and prices to follow course". He added that "while the ongoing economic expansion provides confidence that inflation will gradually glide toward levels in line with the inflation aim, it has yet to translate into stronger inflation dynamic" and "a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to gradually build up".

In the accompanying statement, ECB reiterated that "if the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase our asset purchase programme in terms of size and/or duration". A few weeks ago, Mario unveiled that the members had discussed over the possibility of removing the forward guidance of expanding and extending QE purchases, triggering market speculations that they would do so in July.

While leaving the policies and statement unchanged, Drahi promised QE discussions to begin in autumn. However, he refused to comment whether it means the September 7 meeting.

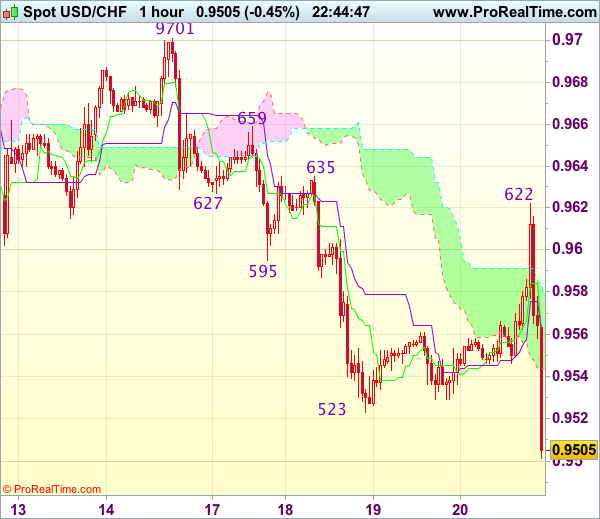

Trade Idea Wrap-up: USD/CHF – Sell at 0.9555

USD/CHF - 0.9500

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9558

Kijun-Sen level : 0.9558

Ichimoku cloud top : 0.9579

Ichimoku cloud bottom : 0.9544

New strategy :

Sell at 0.9555, target: 0.9455, Stop: 0.9590

Position : -

Target : -

Stop : -

Although the greenback staged a strong rebound to 0.9622, renewed selling interest emerged there and dollar has dropped again from there, confirming recent decline has resumed and bearishness remains for further weakness to 0.9490, then towards 0.9460, however, near term oversold condition should prevent sharp fall below previous support at 0.9440-44, risk from there is seen for a rebound later.

In view of this, we are looking to sell dollar on recovery as the Kijun-Sen (now at 0.9558) should limit upside and bring another decline. Above the upper Kumo (now at 0.9579) would suggest an intra-day low is formed, bring a stronger rebound towards resistance at 0.9622 which is likely to hold from here.

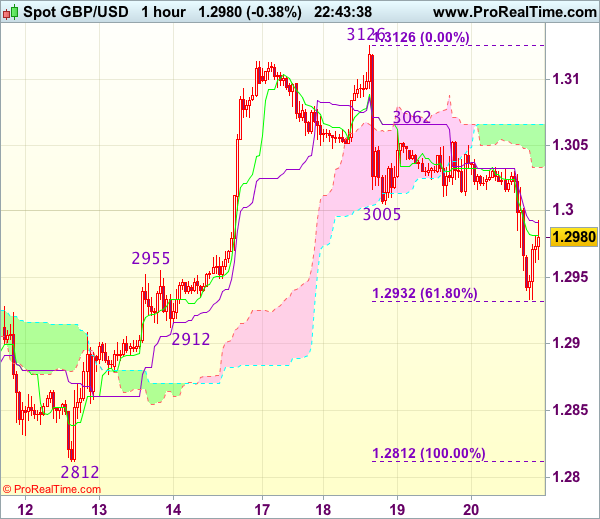

Trade Idea Wrap-up: GBP/USD – Sell at 1.3030

GBP/USD - 1.2979

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2982

Kijun-Sen level : 1.2992

Ichimoku cloud top : 1.3066

Ichimoku cloud bottom : 1.3033

Original strategy :

Sell at 1.3010, Target: 1.2915, Stop: 1.3045

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3030, Target: 1.2930, Stop: 1.3065

Position : -

Target : -

Stop : -

Cable has dropped after breaking support at 1.3005, suggesting top has been formed at 1.3126, hence consolidation with mild downside bias is seen for weakness to 1.3930-32 (61.8% Fibonacci retracement of 1.2812-1.3126), then test of previous support at 1.2912, however, break of latter level is needed to retain bearishness and extend the fall from 1.3126 top to 1.2880-85 first.

In view of this, we are looking to sell cable on recovery as the lower Kumo (now at 1.3033) should limit upside. Only break of resistance at 1.3062 would abort and signal an intra-day low is formed instead, bring a stronger rebound towards 1.3090-00 but resistance at 1.3126 should remain intact.

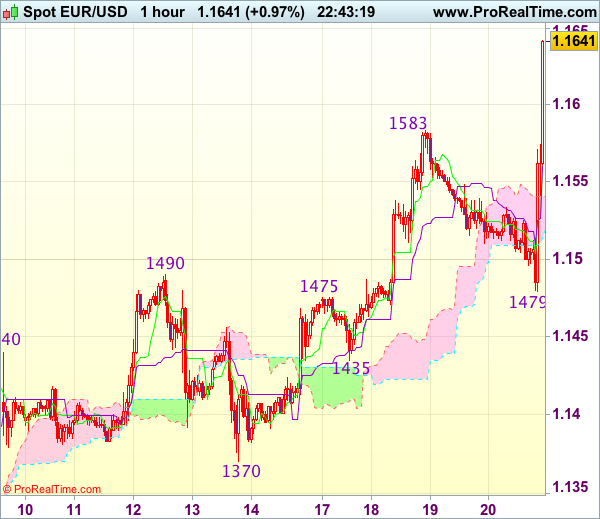

Trade Idea Wrap-up: EUR/USD – Buy at 1.1580

EUR/USD - 1.1641

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1569

Kijun-Sen level : 1.1569

Ichimoku cloud top : 1.1540

Ichimoku cloud bottom : 1.1514

Original strategy :

Buy at 1.1540, Target: 1.1640, Stop: 1.1505

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1580, Target: 1.1680, Stop: 1.1545

Position : -

Target : -

Stop : -

The single currency only slipped to 1.1479 (just missed our long entry at 1.1475) before finding renewed buying interest and current rally above said resistance at 1.1583 confirms recent upmove has resumed and bullishness remains for further gain to 1.1680, then towards previous chart resistance at 1.1714, however, break there is needed to retain bullishness for the rise from 1.0340 low to extend further headway towards 1.1750.

In view of this, we are looking to buy euro on dips but at a higher level as previous resistance at 1.1583 should limit downside. Below the upper Kumo (now at 1.1540) would abort and suggest an intra-day top is formed, bring correction to 1.1510-15 but said support at 1.1479 should remain intact.

Trade Idea Wrap-up: USD/JPY – Exit long entered at 111.80

USD/JPY - 111.80

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.07

Kijun-Sen level : 111.99

Ichimoku cloud top : 112.23

Ichimoku cloud bottom : 111.91

Original strategy :

Bought at 111.80, Target: 112.80, Stop: 111.45

Position : - Long at 111.80

Target : - 112.80

Stop : - 111.45

New strategy :

Exit long entered at 111.80,

Position : - Long at 111.80

Target : -

Stop : -

Current sharp retreat on dollar’s broad-based weakness signals an intra-day top has been formed at 112.42 and downside risk remains for retest of yesterday’s low at 111.55, break there would confirm recent decline from 114.50 top has resumed and extend further weakness to 111.20-25, however, reckon 111.00 would hold from here due to near term oversold condition, bring rebound later.

In view of this, would be prudent to exit long entered at 111.80 and stand aside for now. Above 112.20-25 would prolong consolidation and bring another bounce to 112.42, break there would signal a temporary low is formed, bring a stronger rebound to resistance at 112.87.

Elliott Wave Analysis: GBPUSD Looking Lower

GBPUSD is making a sharp three wave move to the downside, which can be an indication that wave C) found a top at the 1.3126 level. If that is the case, then we will ideally see a five wave move develop to the downside and a breach below the bearish 1.28.11 level.

GBPUSD, 1H