Sample Category Title

Smoke There’s Fire

Smoke There's Fire

A unified Eurozone versus a US administration looking a little pained and discombobulated after yet another vexing Russia headline was the catalyst to send the EURO soaring.AS the political drama ‘of, by, and for the people” was unfolding but linking an unforeseen Russia-gate admission by Donald Trump, Jr and dovish Fedspeak was fire enough in to topple the greenback in thinly traded summer markets. How significant the latest Trump developments are to the broader market landscape is debatable, but one obvious take from overnight headlines was an unexpected policy shift from Patrick Harker, by failing to cement the markets call for a third 2017 rate hike.

Today's revelation that a series emails by Donald Trump Jr., confirming he was offered Russian government help for the Trump election campaign has sent US political risk to another level. Investors are once again questioning President's Trump's administration ability to pass through a pro-business agenda/attitude/stance to further stimulate the US economy, not to mention his sustainability to run the country.While the headlines are not impeachment worthy news, the market buzz does suggest the risk of impeachment proceedings is marginally higher than in the past.But each progressive revelation of the current administration's incompetence is wearing thin on investors psyche that even the most ardent conservative must now have second thoughts about their Nov ( 2016)election day decision. Needless to say what little support that remained for the strong-dollar theme this week quickly evaporated

On Fed speak while the market was waiting for Lael Brainard, a leaning dove, Fed Harker's unexpected WSJ interview 30 minutes after Jr's headlines suggesting the Feds remain in wait-and-see mode drove the final nail in the dollar's coffin during the overnight session.

Fed Chair Yellen's semi-annual monetary policy testimony will be the main event today, but given the Humphrey-Hawkins Testimony is very much a repeat of the latest FOMC minutes, and given the heightened US political risk the market is more focused on political headline risk in early APAC. Nonetheless, the market expects Yellen to frame the commencement of balance sheet normalising around a comparatively upbeat economic assessment, but even this tone is unlikely to shift the current dollar tide.

It didn't take much for the market to fold their cards on a long dollar trade this week which suggests this Fed-inspired move could have some legs and perhaps only a surprising shift in US CPI or Retail Sales data later in the week could stem the current tide.

G-10

As the headlines rolled in US yields fell by the minute pressuring the USD in G10. USDJPY toppled to 113.75, while EURUSD looked toward 1.1500 While Donald Trump, Jr.'s email release appeared to have started the move, I was Fedspeak l which drove the dollars short term demise home. With CPI around the corner and Harker suggesting that inflation will determine whether a third rate hike in 2017 is on the cards, speculative money suggests the view heading into this week's CPI is that of non-transitory.

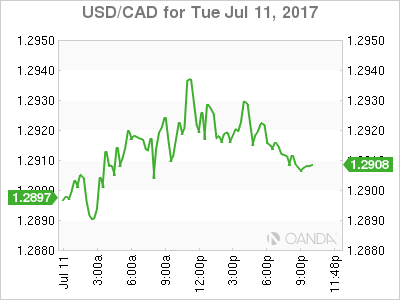

USD/CAD Canadian Dollar Lower Ahead Of Bank Of Canada Rate Decision

Strong growth and concerns for household debt trigger rate decision

The USD/CAD was trading above 1.34 in mid June when Bank of Canada (BoC) Deputy Governor Carolyn Wilkins delivered a speech to a business school crowd and started a swift recovery of the loonie that has the currency pair trading at 1.2927. The central bank cut rates twice in 2015 and has stayed in the sidelines since then, but it is now widely anticipated that the BoC will hike rates this year, with the July meeting firmly on the table.

The Bank of Canada (BoC) will release its rate statement on Wednesday, July 12 at 10:00 am EDT. The Canadian central bank joined the hawkish chorus in June taking the market by surprise and quickly pricing in a rate hike after repeated comments from senior BoC policy makers. The bond market is pricing in a rate hike of 25 basis points to leave the benchmark rate at 0.75 percent based on the remarks by the central bank Governor Stephen Poloz although some financial institutions remain unconvinced that the strong GDP growth does not warrant as a reduction in monetary stimulus. There will be a press conference at 11:15 am EDT where more details will be shared by the BoC Governor.

Fed Chair Janet Yellen will be giving her semiannual monetary policy report to the US House Financial Services Committee on Wednesday, July 12 at 10:00 am EDT and to the Senate Banking Committee on Thursday, July 13 at 10:00 am EDT. FOMC members will be speaking during the week reiterating the high probability of another rate hike and the imminent start of the central bank’s balance sheet reduction sooner rather than later.

The USD/CAD rose 0.288 percent in the last 24 hours. The currency is trading at 1.2916 ahead of the Bank of Canada (BoC) rate statement announcement on Wednesday. The loonie has lost some momentum as risk aversion triggered by the release of Donald Trump Jr’s emails have once again put political uncertainty in the US agenda. The bond market is pricing in a move by the BoC, but there are plenty of doubters amongst economists as evidenced by the Reuters poll published last week. Fourteen of 31 economists expect a rate hike on Wednesday. The quick change in stance from the BoC makes some question the timing but there is no denying that growth has been stronger than forecasted and the impact of falling oil prices has been contained.

Domestically there are concerns about the ballooning of household debt as cheap rates fuelled various real estate bubbles in the country. The move to a tighter monetary policy will be gradual although it could include a second rate hike before the end of the year if the economy continues to perform and other central banks continue to move towards the end of low rates.

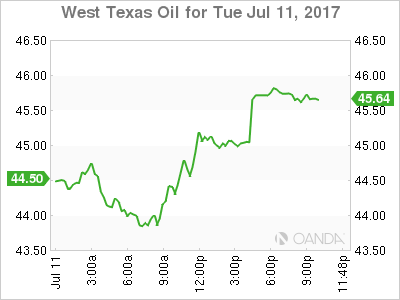

Oil rose 1.412 percent on Tuesday. The price of West Texas Intermediate is trading at $45.02 after forecasts for US production were lower and there is increasing talk about Nigeria and Libya after having resumed their full output will now have to participate in the production cut agreement.

US output has not grown at the same pace of the Organization of the Petroleum Exporting Countries (OPEC) agreed cuts with other producers forcing a reduction in forecasts for next year. Rigs in the US have been coming back online at a slower pace than expected and comments form Russia being open on further reducing output boosted crude prices.

The OPEC and other majors producers joined up in an attempt to lift oil prices from the floor by agreeing to cut production for 6 months in 2016 and adding a 9 month extension that will take the deal into 2018. The monitoring committee will meet in Russia on July 22 to discuss the state of affairs. Nigeria has been invited to attend in a move that could signal its inclusion into the production limit that it was previously exempt.

The release of the US weekly crude inventories will be followed by traders looking for more data on US production. The Energy Information Administration (EIA) will release the weekly report on Wednesday, at 10:30 am EDT. A 3.2 million barrel drawdown is expected to follow the 6.3 million barrel drop from the report published last week.

Market events to watch this week:

Wednesday, July 12

4:30am GBP Average Earnings Index 3m/y

10:00am CAD BOC Monetary Policy Report

10:00am CAD BOC Rate Statement

10:00am USD Fed Chair Yellen Testifies

10:30am USD Crude Oil Inventories

11:15am CAD BOC Press Conference

Thursday, July 13

8:30am USD PPI m/m

8:30am USD Unemployment Claims

10:00am USD Fed Chair Yellen Testifies

Friday, July 14

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Gold Subdued As Yellen Testifies On Capitol Hill

Gold is showing limited movement on Tuesday. In the North American session, spot gold is trading at $1214.30 per ounce. In economic news, JOLTS Jobs Openings dropped sharply to 5.67 million, well below the forecast of 5.98 million. In the US, Federal Reserve Chair Janet Yellen will testify before the House Financial Services Committee.

Although gold is having a quiet week, that could change after Janet Yellen’s testimony before a congressional committee. Janet Yellen is sure to be questioned on whether the Fed is still expecting to raise rates in the second half of the year. Despite repeated statements from Fed policymakers that a rate hike is likely in December, the markets are not as confident, even with last week’s strong Nonfarm Payrolls report. A rate increase in September is very unlikely, with the odds pegged at just 13%, according to the CME Group. As for December, the likelihood of a rate hike is 50%, so the markets will need plenty of convincing that the Fed plans to make a move. Investors will remain lukewarm about the chances of a rate hike unless growth and inflation numbers improve. The US economy slowed down in the first quarter, with GDP rising just 1.4%. Currently, inflation is well below the Fed’s target of 2%, and although Janet Yellen recently stated that the factors weighing on inflation were temporary, investors aren’t convinced. Another factor that has entered the equation is the Federal Reserve’s balance sheet. The Fed has outlined plans to reduce its bloated balance sheet, but has avoided providing any specifics. If the Fed started to lower the balance sheet in September, such a move would mark a vote of confidence in the economy and raise speculation of a rate hike to follow in December.

Gold prices are inversely linked to interest rate hikes, so recent developments involving central banks (aside from the Fed, which continues to talk about a December rate hike) could have a significant impact on the metal. At the recent ECB forum, the heads of the ECB and Bank of England made hawkish statements about tightening monetary policy, and the euro and pound reacted with sharp gains. As well, the Bank of Canada has sent out messages that it will raise rates, and the markets are expecting a quarter-point hike on Wednesday, which would mark the first rate increase in two years. The trend towards tighter policy should not be a complete surprise, as the global economy has been improving in recent months. The ECB and BoE have yet to make any rate moves, but the fact that policymakers are deliberating over tightening policy could lead to expectations in the markets of rate hikes, which in turn would send gold prices lower.

How to Build a Successful Expert Advisor

Automated day trading is probably one of the most exciting things for day traders in the forex community. It offers traders the option to build a mechanical trading system; one that doesn't require human intervention and one that can, of course, make money consistently.

Many traders at all levels often try to test different expert advisors. While there are some good working Forex EA's, it can be a difficult task initially. There are also inherent risks of using an expert advisor, the one that you don't know about.

Three steps to building your EA

In this article, we look at some ways traders can build or plan on how to use an EA.

Step 1

The first step is of course in having a strategy in mind. There needs to be a balance between mechanical rules and discretion. A discretionary based trading system can often be difficult (but not impossible) to code. The downside, of course, is the cost required to code, test and the subsequent iterations.

For traders, the most part of the time needs to be dedicated towards finding a trading strategy. Using the default set of technical indicators is a better option as it can reduce your cost of coding.

Secondly and more importantly, traders should really understand how the indicators work. Simply assuming that short-term and long-term moving average crossovers are bullish and bearish doesn't make sense.

Traders need to spend the time to see under what market conditions the indicators work.

It is also important to have a good money management strategy in mind. Do you want to trail your stops or do you want to take fixed profits? Asking these questions can help traders in the long run. This will incorporate sound principles into your overall strategy.

Step 2

Once the ground rules are in place, building an indicator is the next step. This customized indicator is the middle ground between manual trading and automated trading.

Based on your trading strategy, you can build an indicator that will signal buy and sell conditions on your chart. You can also incorporate take profit and stop levels if it comes to that.

This customized indicator will ensure that you can understand if there are any flaws in your trading system. Based on the strategy used, ensure that the customized indicator can also plot buy/sell signals on price history.

This can offer a quick visual back test that can point you to any potential downsides of your trading strategy that you need to be aware of.

If there are any mistakes, go back to step 1 and reconfigure the settings and apply these to the customized indicator.

It is important to also ensure that you do not fall into the trap of curve-fitting your strategy that will eventually become an expert advisor.

Step 3

Once you are convinced with the performance of step 2, the next step is to make a list, typically like an algorithm. While building the requirements, make sure to have lots of examples, including charts with detailed explanations.

The better your developer understands the requirements, the more robust your expert advisor will be.

Hiring a developer for your EA

Before hiring a developer ensure that you sign any confidentiality agreements about the strategy. Although one needs to realize that in an online world, there is no guarantee that your strategy will be kept secret.

Hiring individual developers is a better option than a company as there is less chance that the developer will tweak your code and re-sell it.

When giving requirements to the developer it is always in your best interests to have them put explanations in the code so that it is easy for the next developer, should you want to switch the developers at a later stage.

Looking for developers on the MQL5 market place or cTrader community can be the best ways to get started. Always make sure to look at the past work of the developer before committing.

In conclusion, designing your own EA is probably one of the most exciting things one can do. If you follow a mechanical trading system, chances are that you can convert that into an EA and exploit your strategy to the fullest.

Questions You Need To Ask Yourself Before You Enter A Trade

There are many different approaches to trading. From technical signals given by the indicators to the fundamentals that become the driving force in the asset or instrument. Put a few traders in a room and chances are that they will trade the same asset or instrument differently.

Despite the different approach to trading, there are some key questions that every trader should ask themselves and should be able to answer. Knowing the ins and outs of the instrument or asset that is being traded will put you in control of what you are doing.

If in doubt, ask these five questions in order to understand whether you are trading the asset or instrument in question knowing the details about it or whether you are merely trading with no clear details.

1. What is the asset doing?

This falls under the technical purview. When you are trading or want to trade a currency pair, the first question to ask is what is the asset or instrument doing? Is it going up or going down?

Where are the support and resistance levels? Is the market in a bullish or bearish trend?

Answering these questions will help you to get a better understanding of what the instrument is doing and how it is likely to behave.

From a trading perspective, this means that you will know when you are wrong in your bias and where to cut your losses.

2. What is driving the price?

Despite the fact that many day traders, especially in forex, tend to trade with technical analysis, it is important to know the fundamentals that are driving prices.

This means taking a look at the central bank speeches, interest rates, and the economic outlook.

Know the fundamental reasons will give you a broad idea of what other traders are looking at and thinking.

You can also use this knowledge later on while managing your trades to see if there is any shift in the bias.

This will ensure that your emotions are put in check, and more importantly you will know why you trade went to fill the take profit level or hit your stop loss.

3. What are other traders thinking?

The markets move on expectations. Price is always forward looking and continues to discount any new information. At times, the markets can get ahead of themselves. This is commonly found with diverging expectations between traders and central bank decisions.

At times you will also find this with the markets and economists extremely hawkish on an economic indicator only to find that the actual data was very disappointing.

A very good recent example of this can be the "Trump Trade." The markets rallied and continued to rally for a few months on. This rally came merely on traders' expectations that Trump's fiscal stimulus plans would help to boost inflation figures.

No sooner did the markets get a reality check only then did traders start adjusting their expectations accordingly.

4. What is your trading plan?

It goes without saying that trading without a plan can be disastrous as you will be caught in the crosswinds.

Times like this, due to lack of a plan, your emotions can begin to take control. This is when your money management and strategy can go for a toss.

From attempting to make money, you will soon switch to attempting to cut your losses.

But with emotions, this can be difficult, and as a result, you will end up taking a bigger hit. This could potentially put all your previous profits and trading capital at risk as well.

5. Why are you trading this particular asset or instrument?

The last but most important question to ask is why are you trading a particular asset or instrument.

In most cases, you will find the answer if you have already replied to the first four questions. Asking "why this instrument" can help you to form the full picture that combines both technical and fundamental analysis, as well as bringing in your trading strategy and plan.

Remember that trading requires a bit of discipline and a certain approach at all times.

It is important to have a disciplined approach to trading as it can always keep you grounded while also bringing some logic and objectivity to the markets that you want to trade.

How to Trade Using Oscillators

Using oscillators is very prominent in the world of trading, whether you are just beginning or have been trading professionally for years. Oscillators are based on math formulas and are categorized as inductive statistics. In forex, they make up a vital part of technical analysis since they are used to confirm market trends, signal when a trade is being overbought or oversold under extreme conditions, and also inform the trader when the market's movement is about to reverse due to loss of momentum.

Common Practice with Oscillators

Most types of oscillators swing close to the baseline, as they are rooted near the bottom of a price chart. The baseline -will undoubtedly vary depending on the oscillator and the mathematical calculation used. Common practice with oscillators is to use the zero line, but both 50 and 100 baselines tend to come up often.-

Basic Terms for Oscillators

Baseline Crossing

When the oscillator crosses the baseline, a buy or sell signal is generated. If you were to combine the oscillator with trend analysis, the signal's strength would be amplified. Therefore, signals that are triggered by intersecting the baseline should be in tandem with the prevailing direction of the trend.

Overbought/Oversold

Since some oscillators are bounded, they naturally come with both lower and upper borders. The most common boundaries are 0 and 100; that is to say, the tool oscillates on a range between 0 and a 100.

These bounded types of oscillators come with predefined overbought and oversold bounds.

Some of the most popular overbought and oversold bounds include 70/30 for RSI, 80/20 for Stochastics and 100/-100 for CCI.

If the oscillator goes above the overbought level (i.e. the upper bound), this indicates that the price has been trading at extremely high levels which means that opening a new long position would be quite risky.

Conversely, if the oscillator goes below the oversold level (i.e. the lower bound), this indicates that opening any new short positions may be too risky as prices are trading at extremely low levels.

Traders may stick to the above rules, except in the beginning stages of a new trend. Once a fresh trend arises, oscillators have a tendency to move into oversold and overbought spaces very fast, indicating that the trader may consider not to open new long or short positions. But in this case, that particular rule could be ignored.

Divergence

Another way of analysing oscillators is through divergence; a particularly valuable method, mainly when a trend has momentum and the oscillator has reached extreme levels. A divergence between the price and the oscillator is like a signal that the trend in question is nearing its end and either a reversal or a consolidation is highly probable. For instance, if the price is going in an upwards direction and forming higher tops and higher bottoms, but the oscillator does not form a higher top, then this is a so-called 'negative divergence warning' that a downside reversal is possible.--

On the other hand, if the price is on a downward track, forming lower tops and lower bottoms on its way, and the oscillator doesn't form a lower bottom, then this is a positive divergence signal that an upside reversal is likely.

In essence, divergence is an early-stage warning. It alerts the trader about a possible reversal before the actual reversal becomes visible. This is every trader's dream but it's important to remember that it is only a warning, not a guarantee and not a buy or sell signal! One must practice patience, and keep an eye on the price reversal before any new positions are opened. Never forget: price is the boss!

Conclusion

The majority of traders use oscillators. Their value is derived from the fact that they confirm trend directions, as well as signals for buy and/or sell opportunities. They also warn against extreme -price levels and alert the trader -when a current direction is nearing its end. Oscillators are also famous for giving traders a heads up about impending reversals before they even appear on the chart. Remember, oscillators should always be used together with price chart analysis. -

Range Trading Explained

Traders who are just beginning to get a handle on how the markets move, focus on the range pattern; one of the most popular price patterns in technical analysis. In a range, the price bounces from a lower horizontal line (support) and rebounds back down from an upper horizontal line (resistance). This creates a sideways or "trend-less" price movement, which is very appealing even for advanced traders, because when a trader looks at the range in hindsight or on paper, it looks like a very easy way to make money.

As long as this sideways price movement stays consistent, traders might potentially increase their profits by going long around the support area and short around the resistance area.

An experienced trader knows it's not enough to trade only when prices reach support and resistance lines, most of the time additional confirmation is needed. In this situation, reversal candlestick patterns can be very effective to help confirm movements, and it's something advanced traders will pay close attention to.

Here are some examples.

The Hammer

As a very popular bullish reversal candlestick, the hammer consists of a small body in two colours (black or white), and a lower shadow that's 2-3 times bigger than the body. The upper shadow is tiny or non-existent.

A hammer near the support line will signal a buy alert - a buy signal is triggered once the price exceeds the high of the candlestick. A protective stop-loss can be placed under the support line and similarly, a take profit order can be placed at the resistance level.

The Shooting Star

The shooting star is, in fact, an inverted hammer found near the top of the range by the resistance line. It's a small body (black or white) with an upper shadow that's 2-3 times the length of the body and has a lower shadow that's tiny, or non-existent.

Much like the hammer signals a buy alert, the shooting star signals a sell alert if it's detected near the resistance.

As soon as prices fall below the low of the candlestick, a sell signal is triggered. If the market moves in the opposite direction, a protective stop-loss can be placed above the resistance to protect capital.

The Bullish Harami

This pattern is made up of a long body of any colour, immediately followed by a small body of any colour. This second body needs to be small enough to be enclosed within the range of the longer, previous, body.

This Harami pattern is bullish if it's found near the lower part of the range, and if the price exceeds the high of the longer body, a buy signal is triggered. It would be wise to place a stop- loss below the support line, and take profit in the upper side of the range in order to protect your profits.

The Bearish Harami

If this same pattern is found near the resistance line, then it's called a bearish Harami and signals a sell alert. Similarly, if the price were to fall below the low of the longer body, then a sell signal is triggered.

A protective stop loss can be placed near the upper area of the range, while the take profit levels should be found near the lower end of the range.

Filtered Patterns

Overbought and oversold extremes can be identified using traditional indicators (Stochastics, for example) in an effort to improve the reliability of the candlestick patterns within a given range.

Stochastics, and other bounded indicators, oscillate between 0 and 100 levels. If it goes below 20, it's a typical sign of an oversold market and if it's above 80, it's a sign that the market is overbought.

Since reversal patterns are considered only when the market is overbought or oversold, these bounded indicators help to improve the pattern's predictability. For example, if one of the above-mentioned patterns is detected near the upper part of the range and the Stochastic indicator (specifically, %D) is above 80, the pattern becomes a more reliable prediction. Likewise, if a reversal pattern shows up closer to the support line, and the Stochastic indicator (%D) is already below 20, it is also considered a trustworthy signal.

It is important to note that reversal patterns should be ignored if they appear on either end of the two horizontal lines, while the Stochastic indicators are above 20 and below 80, as they are not dependable.

Whether you are a novice or an experienced trader, range trading can be a very useful method of analysis. With that said, even when price action makes a trade look profitable within the upper and lower boundaries of a range, traders should be cautious.

Range trading still maintains a level of risk because price is always unpredictable. It can go beyond the confines of the range at any given time and in any direction.

Using filters, like traditional bounded indicators, can enhance the reliability of reversal patterns in a given range. A common example of this, is combining the reversal candlestick patterns with Oscillators, when the market is overbought or oversold. If they're not confirmed by the Oscillator, identified reversals should not be taken seriously.

Taking Your First Live Forex Trade

From a psychological standpoint, taking trades on a demo account compared with trading in the live market are two completely different animals. Think tame house cat and wild lion! Regardless of how long one has successfully been trading on a demo account, pulling the trigger when hard-earned money is on the line is emotional for just about any trader.

So, when the big moment does eventually arrive to trade live funds, it is advisable to be as prepared and as organised as possible. Time and time again, traders enter live trading dosed high on excitement, which, for the most part, generally ends in tears. Remember, emotional trading breeds mistakes. One wrong error at this juncture may not only wipe out your account, but could also be extremely detrimental to your psychology before you've even begun!

Things you'll need to trade live:

- A brokerage account. With IC markets, you can Open an Live Account with as little as $200. That way, making your very first need not break the bank should you make a mistake.

- A trading plan. This should be easily accessible during your trading session. It should detail your method's rule, risk, money management etc.

- Capital.

- A clear head. No stress. No distractions.

- Position sizing calculator: Forex Calculators

- Economic calendar. We use both Forex Factory and Myfxbook.

- Strong internet connection. The last thing you want is your internet losing connection!

- Some chilled music in the background. This is an optional extra!!

Meet Susan

Instead of simply explaining what one can expect when taking their first live forex trade, we thought we'd take it a step further and actually sit side-by-side with a (hypothetical) friend of ours: Susan.

Susan was first introduced to the world of trading by accident. like most of us were in the beginning, she was sceptical and thought it was nothing more than gambling. However, after she read her first book she was eager to learn more.

Due to her full-time occupation as a teacher she trades part time, sticking to the H4 timeframe and above. For the past three years, Susan has committed herself to learning this business, reading several books, attending numerous webinars and testing out different methods on her demo platform. About a year into her study, she decided that trading price action was a good fit for her. Indicators just never felt right. Following another two years of testing (both forward and back testing), Susan believed she was ready to make the leap. As advised by numerous experienced traders on the forums she frequented, she started her live account with a relatively small amount: $5000.

So, without further ado, let's hand the reins over to Susan...

Her first trade

Limit buy order in place? Check. Stop-loss order set? Check. Take-profit target correctly positioned? Check. Any high-impacting economic events that can affect my trade? Check. Risk set at 1% of my account equity? Check.

I've completed this process at least a hundred times on demo and know my trading plan word-for-word, so why do I feel so uneasy! Have I entered into the live environment too early, am I missing something?

With a third coffee in hand (a coffee always makes things better), all I can do now is wait and watch price as it starts nearing my buy order. This is the boring part. When I traded demo dollars, I would simply read a book to kill the time. However, trading with real money and given that this is my first live trade, I feel totally unfocused on anything other than the market. As the time begins to drag, my mind, once again, drifts into self-doubt: 'You'll never cut it'. 'You're a teacher, not a trader'. 'Go and do something worthwhile with your time'...

To try and muzzle these thoughts, I leave the room and go outside. Feeling the sun on my face, and after a brief chat with my neighbour about his freshly-trimmed hedge, helps bring me back down to earth. A lot calmer, I return to my office to be greeted with the sound of a price alert (this means that the pair I am trading is currently three pips ahead of my entry). Instantly, my heart begins racing at twice its normal speed. It is like I have been injected with a double dose of adrenaline!

I quickly slam dunk myself into the chair and wheel myself in for a closer look. After two minutes of almost no movement, my order is filled and my first trade is underway. I take a deep breath to try and calm myself, as I attentively watch price fluctuate around the entry point. It's difficult to put in words my feelings right now. A part of me is thankful that the trade is finally in motion, while another part is apprehensive.

I pull up my profit/loss value, something I know I SHOULD NOT do (a golden rule in my trading plan), and watch the money seesaw between negative and positive. This only exacerbates the situation. My heart begins to thud against my chest again, only this time with double the intensity. Considering I am only risking $50 here, this is not something I expected.

After five minutes the market finally begins to move in my favour. A sigh of relief smothers over me like a warm blanket on a cold evening. I open my terminal to check the profit/loss value again and see green dollars. While pleasing to the eye, I have just broken the same rule I did ten minutes ago. With that, I believe another coffee is in order. Whilst waiting for the kettle to boil, I find myself imagining, or should I say wishing, that my trade has already hit take profit. It'd be wonderful to tell Greg (my husband) that my first trade was a success.

In closing...

Pausing the story here, we can see that Susan has managed to capture some raw emotion, which the majority of traders will feel once they make the switch from demo to live. With that being said though, as we can clearly see with Susan above, once you have your method tested and in place it's largely the psychological aspect one has to grapple with.

For a trader taking her first live trade, Susan has so far done remarkably well. A plan was in place, something that a lot of newbie traders either feel is not needed or simply do not know it's needed. There was no urge to ramp up the leverage. She also noted that there was no economic news on the horizon. This is important! In addition, she exhibited patience and did not try to jump in the market earlier than her pre-determined entry point.

Nevertheless, Susan had to deal with a string of negative thoughts. This can be destructive since retail trading is often a solitary practice. Each time you interact with the market you need to be 100%. There can be NO off days! During demo trading, one is calm and relatively objective. Once real money enters into the equation, things clearly change. Just look at how restless Susan became. It will take time for her to learn that she has absolutely no say on what direction price is heading. This is where thinking in probabilities helps. But again, this can take time to master.

It is said that trading is simple. It is us humans that make it complex. We firmly believe this to be true! Beginning to trade live is daunting. Try not to focus too much on the result, focus more on the process. Visualize yourself performing well! The majority of forex traders face mental roadblocks. By controlling risk, following your plan and keeping a cool head, you'll avoid many of the issues that cripple prospective traders.

Why Becoming an Independent Forex Trader is Appealing

The word 'Independent', or 'financially independent', is KEY here my fellow traders!

Like most folks, the thought of low-paying government pensions, working in your seventies and, just, well, working in general, usually brings a sour taste to one's mouth. A lot of people are often left thinking that there must be more to life than this! As a matter of a fact, according to the Telegraph UK, most people at work are miserable. Shocker!

Becoming financially independent is what most traders, and most people for that matter, strive for, hence the reason so many try their hand at trading. This is a business which requires no formal qualifications (assuming you're entering at retail level), can provide one an income, a pension and for some, millionaire status. There truly is no comparison!

Nevertheless, trading the forex market is not all sunshine and roses. There are downsides to this business which is also something we'll look to explore. But first, let's look at why becoming an independent forex trader is appealing...

Flexibility

- Working/trading from home is dreamy to say the least. No more rush hour morning commutes to the office or construction site! By and of itself, this is an immensely attractive aspect! With this being said though, some traders find it difficult to trade from home and need human interaction. One can overcome this by considering joining a trading arcade.

- Being your own boss. How many of us truly have great workplaces? A place where you feel respected and valued. An arrogant manager, or a company that makes you feel as though you're nothing more than a robot with a heartbeat kills motivation, and rarely allows one to reach their full potential! Being your own boss is therefore a huge plus to becoming a forex trader.

The idea of earning money while essentially not selling anything, having no boss, no clients to be worried about and no schedule, is extremely appealing.

Some take trading a step further and use the flexibility this wonderful business gives to travel the world like this young chap does here Forex Trading Nomad. Living by your own rules and not on someone else's schedule is, in our humble opinion, the epitome of TRUE independence.

Having a skill

- Like plumbers, electricians, doctors, dentists and lawyers, trading is a skill. A skill that enables one to essentially 'give back'.

- Having the ability to teach individuals how to become autonomous is better than any degree, in our opinion.

Learning how to handle one's finances is unfortunately not taught during school years, so It is no wonder so many are in debt right now. Educating others how to effectively trade their way to a better lifestyle and create a future that no job could ever do is a feeling that'd stay with you forever. No amount of money can compare. You've essentially handed over keys to a more sustainable brighter future.

Family time

This is the 'biggy'. How many times have you heard friends, relatives or colleagues say they wish they could spend more time with their family/children. Our guess is a lot! Let's be honest, society today is stressful. Rushing is the norm! Rush to get the kids to school, rush to get their dinner ready – life is just one big RUSH!

Becoming an independent forex trader is effectively a lifestyle. You set the rules/time by which you trade. Spending the best part of the weekday stuck in a prison-like office or at a dusty construction site surrounded by people you have little to no emotional connection with obviously limits your time you spend with family. This is especially true for people with children. Being there for them, especially when they're growing up, is something a lot of parents wish they could do.

Age

Trading requires no psychical effort. There's no lifting, no pushing (unless you consider 'clicking a mouse button' physical) and certainly no pulling. As long as you're well-balanced, have your vision and are able to move your arms/fingers, trading is something that can be done until the day you depart this mortal curl. What other job can honestly offer that, not many!

The downsides

- Often perceived as an easy way to riches, forex trading is actually one of the most challenging tasks one can undertake in life. Learning to trade forex is not something you'll achieve over a weekend, a month or even a year, despite what some insane gurus claim. It takes time, dedication and a truckload of will power to become proficient. A lot of traders are not prepared for this and therefore throw in the towel, hence the high failure rate. Think about it logically for a moment. How long does it take for the average doctor or lawyer to train, five years, ten? Why should trading be any different?

- Dependent on your style of trading it may require one to be at the screen for several hours each day. However, one still has the benefit of setting WHAT time one trades and is therefore needed be in front of the screens.

- The majority of people struggle not with the technical side of trading, it is usually the psychological component. Knowing thyself is crucial. The ability to take risks and stick to the rules you've set is easy in hindsight but incredibly difficult when hard-earned funds are bouncing up and down in front of you!

- There is so much information out there, it's difficult to know where to begin. This is where having a trusted mentor helps. To start, however, check out our beginners guide to technical analysis and also our forex trading 101 section. In addition to this, you may find it beneficial to follow along with our experienced analysts who scour the markets daily to find high-probability trading opportunities IC Markets Blog.

How to Use the ADX Indicator to Improve Your Trading?

The ADX or the Average Directional Index indicator is a handy tool that can help traders in a number of ways. For the most part, those who follow a trend trading strategy will discover that the ADX can be a useful addition.

While traders often end up using two or more indicators that basically gives the same information making them redundant, the ADX indicator in fact compliments any other trend based indicators.

In this article, we will look at how you can use the ADX indicator in your trading and more importantly how you can improve your trend trading strategies.

What is the ADX Indicator?

The ADX indicator is available for free on the MT4 trading platform. The indicator comprises of three variables. The +DI, -DI and the ADX line itself. Combined, all these three variables give information to the trader, informing when the trend is strong and also shows what the current trend is.

The ADX indicator is shown on the first chart below. Here, we use the standard setting of 14-periods.

ADX Indicator Example

You might notice that the level used for the ADX line is 25. This is quite subjective, and it is up to the trader. The ADX level shows when the trend is strong. Thus, when the ADX line is above 25, it indicates that the underlying trend will most likely continue.

In some cases, traders use the levels of 28 or even set a range of 25 - 28 as well. The above chart shows the ADX indicator for the EURUSD daily chart. Of course, the indicator can be applied to any time frame as well.

How to use the ADX indicator for trend trading?

There are two ways one can use the ADX indicator.

- Determine trends

- Determine the strength of the trends

Each of these two methods is outlined in more detail below.

Determining trends with ADX

To determine trends with the Average Directional Index, you can simply hide the ADX line. In this instance, the ADX indicator will only show you the +DI and -DI variables.

ADX Trend determination

In the above example, you can see how the +DI and -DI (along with price action) can signal the trends. The first instance shows the bearish trend, depicted by the -DI rising above the falling +DI. This also coincides with a breakdown of prices below the most recent higher low.

Although price action consolidates at this level, we can see the price falling a few pips below the level identified.

In the next example, you can see that major pivot high that was formed. After the pullback, price action broke past this level and surged higher. This bullish short-term uptrend was depicted by the +DI rising while the -DI was falling.

You can use a number of other indicators such as Bollinger bands or moving averages to act as an additional confirmation of the trend.

The trend determination using the ADX can help you to understand which way the markets are going. Combining with price action, you can expect to see sideways markets as well and stay away when the markets are flat.

Determine the strength of trends

You can also use the ADX to determine the strength of trends. In this example, you will have to use a price overlay indicator on the main chart. In the sub-chart, only the ADX line is used. This can be done by hiding the +DI and -DI levels in the indicator.

ADX Trend Strength

In determining the trend strength, traders can use moving averages on the main chart to understand the trend and use the ADX line to identify when the trend is strong. Because not all trends are powerful, the ADX line is a great way to determine when the trend strength is rising.

This typically coincides with a pullback in price to the moving average before price resumes its trend.

While the above two ways of using the ADX indicator might seem simple, they are in fact very powerful. The ADX indicator can help traders to stay out of the flat market which is where most of the money is lost.

By picking the price when the trend is the strongest, the ADX indicator can compliment any existing trend based trading strategy.