Sample Category Title

Euro Trading Higher, Ahead Of The Euro-Zone’s Industrial Production Data

For the 24 hours to 23:00 GMT, the EUR rose 0.65% against the USD and closed at 1.1470.

On the macro front, Italy's seasonally adjusted industrial production rebounded more-than-expected by 0.7% MoM in May, rising at its fastest pace in three months. Industrial production had fallen by a revised 0.5% in the prior month, while market participants had expected for a gain of 0.5%.

The greenback declined against its major peers, after the release of Donald Trump Jr.'s emails about a meeting with a Russian lawyer to obtain withering information on Hillary Clinton in last year's election campaign.

In the US, data indicated that the NFIB small business optimism index dropped to a level of 103.6 in June, more than market expectations for a fall to a level of 104.4 and compared to a reading of 104.5 in the previous month. Further, the nation's JOLTS job openings eased more-than-anticipated to a level of 5666.0K in May, compared to a revised reading of 5967.0K in the previous month, while investors had envisaged for a fall to a level of 5950.0K.

On the other hand, the seasonally adjusted final wholesale inventories rebounded more than initially anticipated by 0.4% in May, posting its largest gain in five months and compared to a gain of 0.3% recorded in the preliminary figures. In the prior month, wholesale inventories had recorded a revised drop of 0.4%.

Separately, the Federal Reserve (Fed) Governor, Lael Brainard, stated that the central bank would begin to unwind its balance sheet “soon” if the labour market continues to tighten and economy remains on the growth path. However, she expressed caution about further rate increases amid a slowdown in inflation.

On the other hand, the San Francisco Fed President, John Williams, downplayed recent slowdown in inflation and advocated for another interest rate hike this year.

In the Asian session, at GMT0300, the pair is trading at 1.1478, with the EUR trading 0.07% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1413, and a fall through could take it to the next support level of 1.1347. The pair is expected to find its first resistance at 1.1514, and a rise through could take it to the next resistance level of 1.1549.

Going ahead, investors will look forward to the Euro-zone's industrial production data for May, slated to release in a few hours. Moreover, market participants will closely monitor remarks by Federal Reserve (Fed) Chairwoman, Janet Yellen, to receive any guidance about the central bank's monetary policy trajectory.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Trading Slightly Lower, Ahead Of UK’s ILO Unemployment Rate Data

For the 24 hours to 23:00 GMT, the GBP declined 0.19% against the USD and closed at 1.2854.

In the Asian session, at GMT0300, the pair is trading at 1.2849, with the GBP trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.2811, and a fall through could take it to the next support level of 1.2773. The pair is expected to find its first resistance at 1.2907, and a rise through could take it to the next resistance level of 1.2965.

Looking forward, investors will closely monitor Britain's ILO unemployment rate as well as average weekly earnings data, for the three months to May, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.19% against the JPY and closed at 113.84.

In economic news, Japan's flash machine tool orders rose 31.1% in June. In the prior month, machine tool orders had advanced 24.5%.

In the Asian session, at GMT0300, the pair is trading at 113.47, with the USD trading 0.33% lower against the JPY from yesterday's close.

Earlier today, data indicated that the nation's tertiary industry index fell less-than-expected by 0.1% in May, compared to a revised advance of 1.4% in the prior month.

The pair is expected to find support at 113.10, and a fall through could take it to the next support level of 112.74. The pair is expected to find its first resistance at 114.16, and a rise through could take it to the next resistance level of 114.86.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Higher This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.25% against the CHF and closed at 0.9636.

In the Asian session, at GMT0300, the pair is trading at 0.9630, with the USD trading 0.06% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.9605, and a fall through could take it to the next support level of 0.9579. The pair is expected to find its first resistance at 0.9676, and a rise through could take it to the next resistance level of 0.9721.

With no economic releases in Switzerland today, investors will look forward to global macroeconomic factors for further direction.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s Housing Starts Rose More-Than-Expected In June

For the 24 hours to 23:00 GMT, the USD rose 0.18% against the CAD and closed at 1.2914.

Macroeconomic data showed that Canada's seasonally adjusted housing starts climbed to a level of 212.7K in June, compared to a revised reading of 194.6K in the previous month. Market expectation was for housing starts to rise to a level of 200.00 K.

In the Asian session, at GMT0300, the pair is trading at 1.2906, with the USD trading 0.06% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2879, and a fall through could take it to the next support level of 1.2853. The pair is expected to find its first resistance at 1.2938, and a rise through could take it to the next resistance level of 1.2971.

Ahead in the day, the Bank of Canada is scheduled to announce its interest rate decision and is widely expected to raise interest rate after strong signals from its key policymakers.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Market Update – Asian Session: BOJ Raises Purchases Of 3-5 Yr Bonds

Asia Summary

Equities markets remained mixed in the session. USD/JPY fell 0.4% and EUR/USD rose to the highest level since May of 2016 above $1.1480, as markets shift focus to US Fed Yellen’s testimony later today and the expected move from Bank of Canada on interest rates. Yellen is not expected to give any fresh insight, but markets remain wary after Brainard’s comments saying Fed should move cautiously on further rate increases to help boost inflation back to 2% target. Crude rose higher after API data has a larger than expected drawdown.The Bank of Japan (BOJ) raised purchases of 3-5 yr bonds to ¥330B from ¥300B and left others unchanged. JGB 10-yr rate held around 0.09%.

Chinese and Hong Kong banks rose again for the second day after the PBOC injected funds through OMO for the second day after an extended stretch of no action. Offshore yuan rose 0.2% to 6.7880. Financial press explored that the USD/CNY has settled lower than its daily fix in the last 25 of 29 trading days and the PBOC suspected intervention to prop up the yuan, and its inclusion of a "counter-cyclical" adjustment factor to the daily fix, hasn’t appeared to shift expectations with the currency’s weaker settlement continuing into July. In other Chinese press the Hong Kong China bond connect is being called a success.

Key economic data

(JP) JAPAN JUN PPI M/M: 0.0% V 0.0%E; Y/Y: 2.1% V 2.0%E

(AU) AUSTRALIA JUL WESTPAC CONSUMER CONFIDENCE INDEX: 96.6 V 96.2 PRIOR, M/M: +0.4% V -1.8% V -1.1% PRIOR (1st increase in 3 months, 8th consecutive month below 100)

(KR) South Korea Jun Unemployment Rate: 3.8% v 3.7%e

Speakers and Press

China

(CN) China's National Audit Office found improprieties in the 2015 financial statements of 18 out of 20 state enterprises investigated amid the government's anti-graft campaign - Nikkei

Japan

(JP) Bank of Japan (BOJ) raises purchases of 3-5 yr bonds to ¥330B from ¥300B; leaves others unchanged

Australia/New Zealand

(AU) ANZ analysts comment that Australia Q2 CPI will likely show that rates will remain on hold

Korea

(KR) South Korea presidential official: South Korea's new govt will seek both growth and fairer wealth distribution under the main theme of "good growth"

US

(US) Fed’s Mester (hawkish, non-voter): Reversing QE sooner rather than later is preferable

(US) Donald Trump Jr: Did not tell President Trump about his meeting with Russian lawyer last year - Fox interview

Asian Equity Indices/Futures (00:30ET)

Nikkei -0.6%, Hang Seng +0.9%, Shanghai Composite -0.2%, ASX200 0.8%, Kospi -0.1%

Equity Futures: S&P500 -0.1%; Nasdaq flat, Dax -0.1%, FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1487-1.1462; JPY 113.96-113.31; AUD 0.7664-0.7635; NZD 0.7240-0.7216

Aug Gold +0.4% at 1,219/oz; Aug Crude Oil +1.6% at $44.76/brl; Sept Copper +0.3% at $2.68/lb

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.7868 V 6.7983 PRIOR

(CN) PBoC injects combined CNY70B v CNY40B prior in 7-day and 14-day reverse repos

(CN) China MoF sells 2-yr bonds at 3.4552% and 5-yr bonds at 3.47%

Asia equities notable movers

Australia

Royal Wolf Holdings , RWH.AU Affirms received offer from GFC for A$1.83/shr (40.8% premium) in cash less the amount of the special dividend of A$0.0265; +38.5%

Adairs Ltd,ADH.AU Guides FY17 results at the upper end of range EPS A$0.11-0.13; EBIT A$30.5-31.0M (prior A$27-32M); Rev A$264.9M (prior A$255-265M); +34.7%

Hong Kong/China

Singamas Container Holdings, 716.HK Announces continued pledge of shares by controlling shareholder; -4%

China Vanke,000002.CN Denies press report that it signed contract with Xiongan area; +5.4%

Korea

Kolon Life Science, 102940.KR Receives approval to sell INVOSSA in South Korea; -10.8%

US Session Highlights

Investors tried to assess two speeches from Fed officials and the impact of evidence that Donald Trump Jr. made contact with purported Russian govt officials who sought to influence the 2016 campaign.

(UK) BoE Deputy Governor Ben Broadbent in a speech today made no mention about his views on interest rates, giving way to the interpretation he sees no need to make any changes anytime soon. The Pound dropped against all major currencies, reaching an 8-month low against the Euro at 0.8933, and against the US dollar the Pound lost nearly 100 pips from its day high, trading as low as 1.2829 at one point.

HCSG Reports Q2 $0.30 v $0.29e, Rev $470.9M v $423Me; +7.0% afterhours

US markets on close: Dow flat, S&P500 -0.1%, Nasdaq +0.3%, Russell +0.3%

Best Sector in S&P500: Energy

Worst Sector in S&P500: Financial

Biggest gainers: MU +2.9%; MNK +2.8%; WDC +2.8%

Biggest losers: KORS -7.4%; CMG -2.8%; TROW -2.5%

At the close: VIX 10.89 (-0.22pts); Treasuries: 2-yr 1.38% (0.9%), 10-yr 2.36% (-0.4%), 30-yr 2.92% (0.0%)

European Open Briefing: The Pound Recovered To 1.2860 Overnight

Global Markets:

- Asian stock markets: Nikkei down 0.65 %, Shanghai Composite gained 0.80 %, Hang Seng rose 0.75 %, ASX 200 lost 0.75 %

- Commodities: Gold at $1220 (+0.35%), Silver at $15.90 (+0.90%), WTI Oil at $45.78 (+1.65%), Brent Oil at $48.25 (+1.40%)

- Rates: US 10 year yield at 2.36, UK 10 Year yield at 1.28, German 10 year yield at 0.55

News & Data:

- Australia Westpac Consumer Confidence SA (M/M) Jul: 0.40% (Prev -1.80%)

- Australia Westpac Consumer Confidence Index Jul: 96.6 (Prev 96.20)

- Japan PPI (Y/Y) Jun: 2.10% (Est 2.0%, Prev 2.10%)

- Japan PPI (M/M) Jun: 0.00% (Est 0.00%, Prev 0.00%)

- South Korea Unemployment Rate SA Jun: 3.80% (Est 3.70%, Prev 3.60%)

- Australia Credit Card Purchases May: A$28.30 Bln (Prev A$22.90 Bln)

- Australia Credit Card Balances May: A$52.30 Bln (Prev A$52.00 Bln)

- PBoC Fixes USDCNY Reference Rate At 6.7868 (Prev 6.7983)

Markets Update:

The US Dollar retraced some of its recent gains after dovish comments from a Fed member, who said that the central bank needs to assess its rate hike path given the recent soft inflation data.

USDJPY fell from 114.60 to 113.30. Major support lies at 113, and it is important for USDJPY bulls that it holds. A break below would signal that the pair will test 112 soon.

The Pound recovered to 1.2860 overnight. The focus today will be on UK employment data. Better than expected numbers should push GBPUSD back above 1.29. However, given the political uncertainty, it is unlikely that the Pound will have a significant rally anytime soon.

CAD pairs will have high volatiliy today. The Bank of Canada will decide on interest rates at 1500 BST, and the market is expecting a rate hike. While that alone should support the Canadian Dollar only slightly, much will depend on the statement and the outlook of the central bank. A hawkish outlook would boost the CAD, and send the USDCAD in direction of 1.26. On the other side, if the BoC does not hike, we should see a large short squeeze in the USDCAD. A rally towards 1.31 would then seem likely.

Upcoming Events:

- 09:30 BST – UK Unemployment Rate

- 09:30 BST – UK Average Earnings

- 09:30 BST – UK Claimant Count Change

- 10:00 BST – Euro Zone Industrial Production

- 15:00 BST – Fed Chair Yellen testifies

- 15:00 BST – Bank of Canada Rate Decision

- 15:30 BST – US Crude Oil Inventories

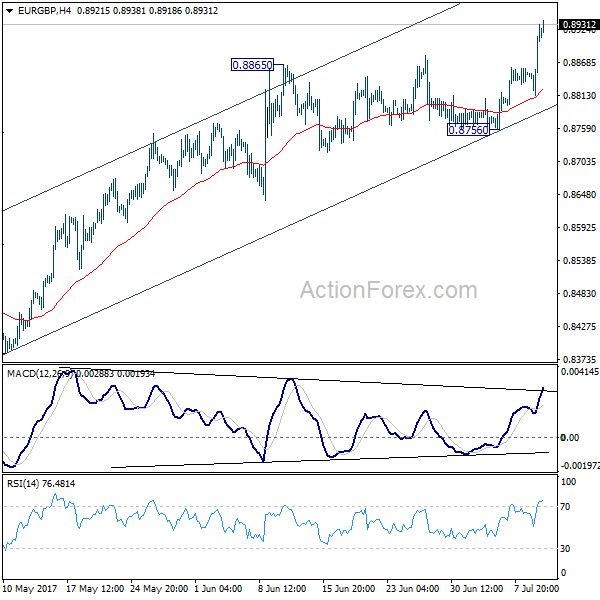

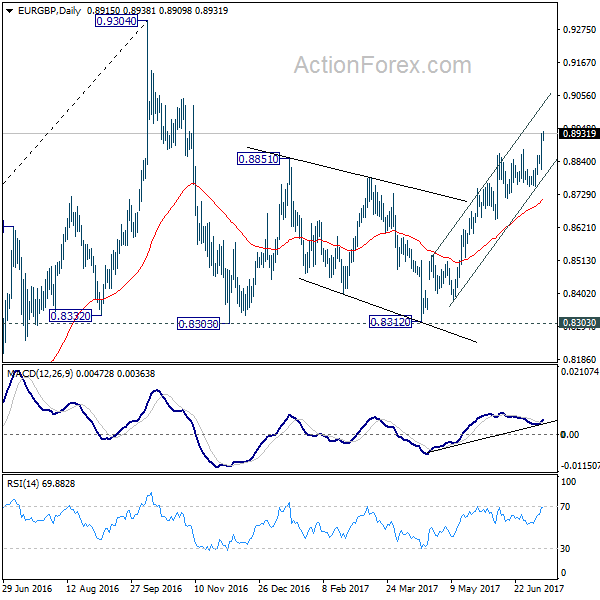

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8848; (P) 0.8890; (R1) 0.8966; More

EUR/GBP's strong break of 0.8879 resistance indicates that rise from 0.8312 has resumed. Intraday bias is back on the upside. Further rally would now be seen to retest 0.9304 high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to bring near term reversal. Nonetheless, for now, break of 0.8756 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

Dollar Weakens Broadly ahead of Fed Yellen Testimony, BoC to Hike Today

Euro surged broadly overnight, with the help from selloff in Sterling and then Dollar. Strength in the common currency carries on in Asia session today. Fed Governor Lael Brainard's cautious comments regarding rate hike is seen a a factor triggering the decline in the greenback. Fed chair Janet Yellen's testimony to Congress today will be the key to decide whether the greenback will suffer more selling. Meanwhile, Sterling tumbled as markets continued to price out a near term BoE hike. BoE Deputy Governor Ben Broadbent's lack of comments on interest rates was taken as a sign of neutral stance. Meanwhile, Canadian Dollar is staying in range against Dollar as markets are awaiting the highly anticipated BoC rate hike.

Technically, near term outlook in Dollar worsen mildly with EUR/USD taking out 1.1444 resistance firmly while USD/JPY was rejected from 114.36 key resistance. AUD/USD' s break of 0.7643 minor resistance today also suggests further upside to retest 0.7711 resistance. Meanwhile, EUR/GBP's break of 0.8879 resistance now suggests that recent rise from 0.8312 is resuming for 0.9304 high. GBP/JPY's break of 146.03 minor support also signals rejection from 148 handle again and near term reversal.

Fed Brainard: Not much to do to move rate to neutral level

Fed Governor Lael Brainard sounded cautious over further interest rate hike. She noted that "I will want to monitor inflation developments carefully, and to move cautiously on further increases in the federal funds rate, so as to help guide inflation back up around our symmetric target." And, "the neutral level of the federal funds rate is likely to remain close to zero in real terms over the medium term". She pointed out that "if that is the case, we would not have much more additional work to do on moving to a neutral stance." Nonetheless, she sounded more supportive to shrinking the balance sheet and said that "if the data continue to confirm a strong labor market and firming economic activity, I believe it would be appropriate soon to commence the gradual and predictable process of allowing the balance sheet to run off,"

Euro supported by ECB expectations

Euro surges as lifted by buying in EUR/GBP and against Dollar. The common currency is also firmly supported by expectation of ECB stimulus exit. It's generally expected that based on improving economic and inflation outlook, the central bank will announce some sort of tapering plan in September or October. Meanwhile, forward Eonia bank-to-bank rates are implying a 10 bp hike in ECB's -0.40% deposit rate by next July. Some economists noted that it's just a very sluggish tightening cycle that markets are pricing in. But it should still be noted that there wasn't such expectations a few months ago before the easing of political risks in Eurozone. Euro will continue to lend support from such expectations, in particular, if underlying inflation reading accelerates.

Australian consumer confidence improved

Australia Westpac consumer confidence snapped three months of decline and rose 0.4% in July. However, Westpac noted that "this is the eighth consecutive month where the Index has printed below 100 indicating that pessimists continue to outnumber optimists. The Index is not sending encouraging signals about the outlook for consumer spending." Meanwhile, they expect RBA to be on hold "throughout the remainder of 2017 and 2018". And, "a cautious consumer; a slowing housing market; and a weakening in the labour market with limited prospects of any boost to wages growth all point to another year of steady policy".

Canadian Dollar vulnerable on a neutral BoC hike

Canadian Dollar's place as the strongest major currency was overtaken by Euro ahead of the highly anticipated rate hike. BoC is generally expected to raise benchmark interest rate by 25bps to 0.75% today. Recent hawkish comments from BoC governor Stephen Poloz and solid economic data has already set the stage for it. But as we pointed out before, the Loonie could be vulnerable to a set back if BoC indicates that it's a one off move, rather than the start of a "cycle".

Judging from the price actions in EUR/CAD, a post BoC pull back in Canadian Dollar is a possible scenario. The decline in EUR/CAD from 1.5257 is so far having a corrective structure. It's also held above 1.4597 resistance turned support. A break of 1.4977 resistance will signal the completion of such decline and bring retest of 1.5257 high. And in that case, EUR/CAD could indeed be resuming the rally from 1.3782 towards 1.6103 high. On the other hand, firm break of 1.4597 will put 1.3782/4051 support zone into focus.

On the data front, Japan domestic CGPI rose 2.1% yoy in June. Australia Westpac consumer confidence rose 0.4% in July. UK job data will be the main focus in European session. Eurozone will release industrial production too.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8848; (P) 0.8890; (R1) 0.8966; More

EUR/GBP's strong break of 0.8879 resistance indicates that rise from 0.8312 has resumed. Intraday bias is back on the upside. Further rally would now be seen to retest 0.9304 high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to bring near term reversal. Nonetheless, for now, break of 0.8756 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Jun | 2.10% | 2.10% | 2.10% | |

| 0:30 | AUD | Westpac Consumer Confidence Jul | 0.40% | -1.80% | ||

| 4:30 | JPY | Tertiary Industry Index M/M May | -0.60% | 1.20% | ||

| 8:30 | GBP | Jobless Claims Change Jun | 10.4K | 7.3k | ||

| 8:30 | GBP | Claimant Count Rate Jun | 2.30% | |||

| 8:30 | GBP | ILO Unemployment Rate 3M May | 4.60% | 4.60% | ||

| 8:30 | GBP | Average Weekly Earnings 3M/Y May | 1.80% | 2.10% | ||

| 9:00 | EUR | Eurozone Industrial Production M/M May | 1.00% | 0.50% | ||

| 14:00 | CAD | BoC Rate Decision | 0.75% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | -6.3M | |||

| 15:15 | CAD | BoC Press Conference |

Elliott Wave View: NIFTY More Upside

Short term NIFTY Elliott Wave view suggests the pullback to 9449.06 low on 6/30 ended Intermediate wave (2). Up from there, rally is unfolding as an Elliott wave double three structure where Minute wave ((w)) ended at 9700.7 and Minute wave ((x)) ended at 9642.65. Wave ((y)) is in progress also as a double three structure where Minutte wave (w) ended at 9830.05.

Minutte wave (x) pullback ideally stays above 9642.65, but more importantly above 9449.06 for the next leg higher. While pivot at 9449.06 is intact, expect NIFTY to extend higher to 9894.8 – 9954.5 to complete Minor wave W and end cycle from 6/30 low. Afterwards, Index should pullback in Minor wave X in 3, 7, or 11 swing to correct cycle from 6/30 low before the rally resumes. We don’t like selling the Index.

NIFTY 1 hour Elliott Wave Chart