Sample Category Title

What is Leverage and How Does it Work in the Forex Market?

'What you don't know can't hurt you'.

This widely used idiom may apply to some things in life, but certainly NOT when it comes to leverage! Quite literally, the MORE you know the BETTER!

What is leverage?

Leverage essentially means having the ability to control a large sum of capital using very little of your own funds and borrowing the rest. When you buy a house on credit i.e. a mortgage, for example, you are actually trading with leverage. Say you put a 25% down payment of $50,000 on a house worth $200,000, you are effectively using leverage here!

Leverage in the forex market is rather straightforward. For every $1 in your account you can control $X amount where X is greater than 1. For instance, 100:1 leverage means you control $100 for each $1 in your account. If you have $1,000 in your account this means that you can control $100,000 in positions.

The leverage achievable in the forex market, nonetheless, is immense in comparison to other markets. In the stock market, for example, the majority of leveraged accounts allows you to borrow at a 2:1 ratio i.e. a $10,000 deposit allows you to control $20,000. In forex, leverage of 500:1 is possible!

How does one use leverage?

This is always best explained using an example:

Terry the investor believes the EUR will strengthen against the US dollar in the coming months. He calculates his position size and wants to take a $100k position at (one standard lot) in the EUR/USD market at leverage of 100:1. Terry's current account balance stands at $10,000. The broker, assuming that the margin rate is 1%, would set aside $1,000 from the account (1% of 100,000 is 1000), thus leaving Terry with a usable free margin of $9000.

Why is there a margin rate and what the heck is free usable margin?

In a margin account, the broker uses the $1,000 as security. If Terry's position worsens or his losses exceed $9,000, the account will be trading at the margin level ($1,000). If this occurs, the broker will issue the dreaded margin call.

Free usable margin is the amount of account equity that is not currently being used to maintain the open position. Essentially, it is the amount available in the account to open additional positions, and the amount that the current position can move against Terry before receiving a margin call.

As you can see, margin is not a fee nor is it a transaction cost. If you buy on margin you're, in essence, borrowing money from your broker to trade. The deposit is considered margin which is required in order to use leverage.

Margin requirements differ from broker to broker. IC Markets offer very reasonable margin rates as low as 0.2% on most FX pairs, as well as flexible leverage options ranging from 1:1 to 1:500. With margin rates set at 0.2%, instead of $1000 margin being required as we saw in Terry's trade example above, the amount needed would have been $200 - quite a difference!

How much leverage should I use?

This is a common question and it really depends on the risk taken on a trade. Let's assume that you have a $5000 account and you risk 2% on each trade.

Let's also assume that you want to buy the EUR/USD at 1.1256, and have a stop set at 1.1246: a 10-pip stop loss. To trade this position, one would be required to enter using one standard lot, or $100,000. That's twenty times your account size you're trading there. However, by correctly sizing your position, you only have 2% of your account equity at risk even though you have a $100k position in the market.

Let's take this a step further and assume you wanted to risk 10% of your account on the same trade discussed above. This would equate to $500 of risk. To trade with a 10-pip stop, you'd then need to input five standard lots, or $500,000. Now, you're trading at leverage of 100:1 - 100 times your account size, but only risking 10%.

For beginner traders, we would strongly advise respecting leverage as it truly is a double-edged sword. Trade small to begin with and please RESPECT leverage!

Identifying Trends: A Beginners’ Guide

In the early stages of trading, the identification of a trend emerges as a compass to the markets. We have all heard the phrases "the trend is your friend", "never go against the trend" and "trade with the trend". But, what is a trend and why is it so important? A trend is simply the prevailing direction of the market. It is the direction that future prices will most likely follow. So, the early identification of the trend is imperative in trading the financial markets. Whether it's going up, down or sideways, has to be determined before entering the market. Many trading systems have been developed with precise rules on when to open a trading position, exit a losing trade and of course lock potential profits. Trend identification is one of the cornerstones of successful trading

Tops and Bottoms

A common way of detecting a trend is by visual inspection. Spotting consecutive higher tops and higher bottoms will indicate an uptrend, while consecutive lower tops and lower bottoms will indicate a downtrend. Equal tops and equal bottoms will define a sideways, trendless market. Even though identification of tops and bottoms looks very easy in hindsight, traders, especially beginners, sometimes find it difficult to find prevailing trends, it does take some practice. Another common way of identifying a trend on the price chart, is by attaching technical tools designed to spot the direction of the market. Indicators and oscillators fall in this category which are based on statistical concepts like inductive statistics.

Using trading tools like indicators and oscillators, is a popular way for identifying a prevailing trend. There are many such tools, which may confuse traders who are just getting acquainted with them, so we will focus on the three most popular trend-identifying indicators.

Moving Average

A very popular tool for traders is the Moving Average. It is an indicator that focuses on a series of averages. It is a very simple tool; when prices cross above the Moving Average curving line, an uptrend is expected. When prices pass below the Moving Average line, a downtrend is usually formed because there are more sellers than buyers influencing the price.

MACD

A Moving Average Convergence Divergence indicator, or MACD for short, shows the difference between two exponential moving averages (i.e. MA's that place special emphasis on the most recent prices). Once the equilibrium line (the zero) is crossed, the start of a new trend is signaled - just like with any other oscillator. A positive MACD reading implies an uptrend while a negative MACD reading signifies that prices have been falling- the typical feature of a downtrend.

Momentum

This indicator measures the rate at which prices change. In other words, how quickly the price increases or decreases. In the case of Momentum, the equilibrium line is at 100. A new uptrend begins when prices are seen to accelerate and the oscillator crosses over the equilibrium line - this would be a positive signal. The opposite is true when prices decelerate and Momentum passes below the equilibrium. In that case, it's a negative signal that shows a downtrend.

Validation

The confluence of all three indicators (i.e. Moving Average, MACD and Momentum) in the same direction, increases the probability of the market moving in the predefined direction. As a result, when all three indicators signal the same trend, traders tend to be more confident with their analysis which in turn, makes their trading more disciplined.

Five Simple Trading Lessons from Hell’s Kitchen

Hell's Kitchen, one of Chef Gordon Ramsay's many reality TV shows is quite an entertaining show to watch. Chefs face off to win a grand prize of running their own restaurants at the end. However, the path to success isn't easy as the contestants are truly put to hell. From having to deal with their peers to putting their differences aside and working as a team, Hell's Kitchen simply draws the viewer into it.

However, this article isn't a review about Hell's Kitchen, but rather the lessons a viewer can take away from it. From a trading perspective, there are quite some interesting nuggets of wisdom that can truly help you to become a better a trader. Here are the five biggest lessons that stand out however.

1. Never lose focus

Starting from the first episode to the end, a common recurring theme in Hell's Kitchen is the fact that contents that are the most focused and have their eyes fixed on the prize are the ones who often end up on the tops. There is a bit of luck involved too. But isn't that the case anywhere?

For traders, staying focused on their goals is what determines the best from the rest. There are ups and downs, but that doesn't mean you have to give up because you hit a losing streak.

In Hell's Kitchen, some of the top chefs hit rock bottom, often coming close to being eliminated. However, some of them manage to bounce back simply through sheer determination and focus to come out on the tops.

2. Preparation is important

The main event in every episode of Hell's Kitchen is the grand service that is put out. This is often a time of high pressure and shows Gordon Ramsay at his very best, swearing at the contestants and going nuts. It is a recurring theme to find contestants either running out of ingredients or failing to have a backup plan. It does sound a bit familiar in the trading world doesn't it?

In the heat of trading, the stress a trader goes through is no different. However, the preparation that one needs to do ahead of trading is very important. Do you take time out to analyze the charts or understand the main driving themes for the day? Do you really have a plan of attack?

Always prepare yourself before you start trading. Get to know the markets and what's driving them

3. Constant learning

Another impressive feat from the Hell's Kitchen winners is the fact that it is not your education or your experience that matters. There have been winners on the show who were not even professional chefs to begin with. What they lack as experience or education is made up by the zeal to learn and improve on their weaknesses.

For traders, this is a very important lesson. Learning doesn't necessarily mean having to buy tons of books and read through them all. Lessons can be found anywhere. From a losing trade to a winning trade, you only need to know where to look. Some of the most successful traders often ensure that they always learn something from a losing trade and most importantly, ensure that they don't repeat it again.

The constant loop of feedback and learning ensures that you overcome your weakness over time.

4. Strategize

Every episode of Hell's Kitchen concludes with a best performer of the evening having to put up two contestants on the hot seat for elimination. Quite often you will come across contestants being put up for elimination in a strategic way. Eliminating the biggest competitor and moving one step closer to the goal. While this works, there are also instances where the strategy backfires, such as the competition being put up for elimination quite early on.

An important lesson for traders is strategy and timing. You can have a great strategy, but if you miss out on the timing it can backfire. A great example is where you find a nice reversal candlestick pattern on the charts and you execute it. However, pullbacks can be frustrating. Without correct timing to execute your strategy you could end up under water for quite a while.

While strategy is important, timing also plays a crucial role when it comes to your trading plan

5. Consistency is key!

Finally, a recurring theme among the winners of Hell's Kitchen is their consistency to keep up their performance and standards. There are many contestants on Hell's Kitchen who start with a bang but soon fizzle out under pressure. Likewise, there are contestants who start off weak but manage to rise to the challenge only to peak out and get eliminated. Staying consistent is one of the key aspects for trading as well. Almost any trader at some point has had a winning trade, but if you are not consistent in your trading chances are that you will simply peak out at some point. Consistency is not about having a winning streak; it is all about how well you can trade according to your plan.

For traders, consistency plays a big role in the longer term success of your trading. The better you are at consistently churning out winners, the more the chances of you staying in the trading game for the long term.

Elliott Wave Analysis: Complex Correction On GBPUSD Points Higher

GBPUSD made a sharp drop in the past couple of trading sessions, which we now see it as final wave C of B). Ideally current drop represents the final piece of a complex correction, that may find support near the Fibonacci ratio of 50.0 and from there turn higher. A five wave rally and a breach of 1.2984 level would later then suggest a bullish continuation.

GBPUSD, 1H

Weak Data Fails to Dent US Dollar; Sterling Weakens Near 10-day Low

The dollar ignored a weaker-than-expected US JOLTs report and rose higher against the yen as the European session was coming to a close. The greenback gained against most of its major counterparts, with the dollar index rising a tenth of a percent to 96.125. Oil reversed from its earlier gains.

The JOLTS report showed the number of job openings in the US fell to 5.666 million in May from a downwardly revised 5.967 million in the previous month and fell short of expectations (5.950 million). The dollar weakened against the yen briefly upon the release of the figures, but was quick to recover and rose even higher. Dollar/yen was last trading at 114.40. Greenback traders are eyeing Janet Yellen's two-day testimony in Congress on monetary policy starting tomorrow.

In the absence of important data releases out of the eurozone, the euro has been steady for the past two days. Euro/dollar was last trading at 1.1417.

Deputy BoE Governor Ben Broadbent avoided to address the topic of the next interest rate hike, but did warn on the negative impact the UK economy may face amid Brexit and less trade. Broadbent also said UK incomes would suffer from a likely fall in services exports to the EU. Many traders interpreted his views as being dovish, prompting sterling to soften to near 10-day lows against the US dollar. Pound/dollar was last trading at 1.2842.

The oil-linked Canadian dollar reacted negatively to the bearish reports on oil and followed crude oil prices lower. This meant the USD/CAD pair rose for the day to last trade at 1.2911. The loonie got some support from the upbeat housing data released during European session, however the gains were short-lived.

Canadian housing starts rose in June with the stand-alone seasonally-adjusted annual rate (SAAR) at 212,695 from a revised 195,000 the previous month and above expectations of a figure close to 200k. This could be a positive signal for the Bank of Canada ahead of its policy meeting tomorrow. Stronger housing starts means higher supply and could cap prices. Rising house prices have been one of the key topics monitored by the BoC.

Oil supply glut is keeping oil medium-term outlook weak, prompting major banks to start downgrading price forecasts. Oil prices reversed early daily gains and were trending downward as the European session was about to end. WTI was last trading at $44.27 a barrel while Brent was at $46.74.

Gold wasn't relieved from the pressure either, with the dollar further strengthening in the late European session, the precious metal weakened further to last trade at $1,208.58 an ounce.

Yen Dips to 4-Month Lows, Japanese PPI Next

USD/JPY has posted gains in the Tuesday session. In the North American session, the pair is trading at 114.50, its highest level since March. On the release front, Japanese Preliminary Machine Tool Orders climbed to 31.1%. Later in the day, Japan releases PPI, which is expected to remain at 2.1%. In the US, JOLTS Jobs Openings dropped sharply to 5.67 million, well below the forecast of 5.98 million. On Wednesday, Federal Reserve Chair Janet Yellen will testify before the House Financial Services Committee. The markets will be listening closely, looking for clues regarding interest rate policy.

Japan's economy has improved in 2017, buoyed by a stronger global economy. This has translated into increased demand for Japanese goods and this has boosted the manufacturing and export sectors. The Tankan Manufacturing Index jumped to 17 in the first quarter, its strongest showing since 2014. On Tuesday, Preliminary Machine Tool Orders improved in June to 31.1%, up from 24.4% a month earlier. We'll get a look at Preliminary Industrial Production on Friday. The indicator recorded a strong gain of 4.0% in April, but the markets are braced for a sharp downturn in June, with an estimate of -3.3%.

The Federal Reserve has all but promised another rate hike in 2017, and Fed Chair Janet Yellen is sure to be questioned on whether the Fed is still expecting to raise rates in the second half of the year. The markets are not showing much confidence in a rate move, despite a strong Nonfarm Payrolls report last week. A rate increase in September is very unlikely, with the odds pegged at just 13%, according to the CME Group. As for December, the likelihood of a rate hike is 50%, so the markets will need plenty of convincing that the Fed plans to make a move. What factors will raise the odds of a rate increase? First, second quarter growth will have to improve, after a weak performance in the first quarter, in which GDP rose just 1.4%. Second, stronger inflation levels would boost speculation of a rate hike. Currently, inflation is well below the Fed's target of 2%, and although Janet Yellen recently stated that the factors weighing on inflation were temporary, investors aren't convinced. Third, the Fed has outlined plans to reduce its bloated balance sheet, but has avoided providing any specifics. If the Fed started to lower the balance sheet in September, such a move would mark a vote of confidence in the economy and raise speculation of a rate hike to follow in December.

Your Trading Plan Is Essential

What is the first thing that you do when you want something with an intense desire? When you want it so bad you can taste it? When you can feel the desire in your bones? When you're driven by a desire that leaves you hungry for it? With this kind of emotionally passionate focus, you automatically begin to think about "how" you can get it. In other words you begin to plan. The "how" or "plan" charts the way to achieving the desired item...no matter what it is and no matter how small or large. Planning is essential to the process of achievement and without it you would come as close to accomplishing the goal as you would if you were to be blindfolded and spun around and given a bow and arrow to hit a bullseye 100 yards away. Trading requires planning at both the macro level (the big picture) and the micro level (the small picture or plan for every trade).

Now, many of you reading this article are trading without a plan. That's very unfortunate ... for you! If you don't have a macro trade plan and you are trading then you are "out-of-sequence" in your trading process. Your success as a trader depends on a number of items that include market knowledge, a set of rules, money management and risk management, and self-discipline to explicitly follow these trading necessities. Your plan would include all of these elements and others to construct a vehicle that is designed for getting the results you want. Without a macro stock trading plan you lack the "big picture," the overview map that holds the "how" you would proceed. Furthermore, what are you telling yourself to justify not having a macro trade plan? Here are some examples:

I have no idea how to write one,

I don't consider it necessary,

It's boring and time consuming,

Successful traders don't have plans

I have a mental plan.

Of course, there are all types of excuses, but the bottom line is that they are excuses, and they are standing between you and setting yourself up for getting effective trading results.

Let's take a look at some of the essentials that would go into your macro trade plan.

- Create a cover sheet with the name of your business and this will establish the intention of treating your trading like the real business that it is. Your cover sheet and name may seem inconsequential, but having an emotionally focused label is powerful.

- Establish your purpose for trading, the compelling reason why you want to trade. You'll want to tie this to the what-matters-most in your life in order to "harness" the passionate energy associated with it. Things like family, friends, personal freedom, and those things you're "hungry" for. Answer the questions: I want to learn to trade because... My primary objective of learning to trade is... These objectives are important to me because... I believe I can achieve my goals because...

- Identify your trading style in order to help you define your risk management strategy and the tools you'll use to trade. Answer these questions: My trading style is... I have chosen this style because...

- One of the toughest obstacles in trading is not the market, but rather the trader, him or herself. A simple personality profile questionnaire will help you determine your strengths, weaknesses, how you handle losses and your expectations. There are many resources available on the web to help you evaluate your personality. Then answer these questions: My greatest strength is... My greatest weakness is... Potential problem areas are...

- Goals should be set to help you evaluate your progress, and give you a target for which to aim. These goals should be both mechanical data (direct and indirect information related to the markets) and internal data (mental and emotional) goals. An example of a mechanical data goal would be to beat the S&P 500 index in returns over a 12 month period. An example of an internal data goal would be to read 1 book every 2 months to sharpen your trading knowledge.

- Identify the markets you want to trade; that is, those markets that your personality resonates with. Also, determine the details of these markets for instance, Forex because you live on the West Coast and you're a night owl and you particularly like the British Pound vs. the Japanese Yen pair. Finish these sentences: I will trade the following instruments... I am trading these instruments because... My trading times will be as follows...

- Make sure that your technology is up to date, free of bugs and with an IT (information technology) person on call in case your computer goes down. Trading online demands a powerful and reliable system. Ensure that you have one and that it is backed up. Additionally, get a strong internet provider...cable preferably. Going further you'll want a trading platform that you trust both for data streams and for accurate fills.

- Effective routines lead to good habits. Create a routine for the beginning, middle and end of your trading session; i.e., pre-market routines for both mechanical data (research, news, zones, time frames, indicators) and internal data (meditation, taking your emotional temperature, and lowering stress levels in order to be focused and ready for the trading trenches.)

- Gauging your risk is critically important at all times. Categorize what you can control and determine how you will manage it. For example, having limits on every trade you enter. The prime directive is to protect your capital at all times. Limits such as having a max number of shares/lots/contracts per trade; having a max loss per trade; and identifying a max loss per day are very important. Complete these sentences: I will gauge my risk on each trade by... I will risk only _____ on any one trade... My daily stop loss will be... Once my stop is reached, I will...

- Have your protocols (strategies, procedures, setups and entry rules) spelled out. Many strategies exist for trading, and every one does something different. What will your approach be? What tools will you use when you trade (mechanical/internal)? Complete the following phrases: My primary reason for entering into a trade will be... My secondary reason for entering into a trade will be... My ideal setup would be...

- Your review process is just as important as what you put into your macro trade plan. Weekly, monthly, quarterly and yearly reviews would not be too much. Remember it's a living document meaning that it evolves as you do and you'll want to have an intimate relationship with it. It is your trusted vehicle for taking you and your A-Game to success. Ask yourself these questions:

What securities are you trading more consistently?

What indicators work best for you?

Are you adhering to your stop loss plan?

Are you achieving your trading goals?

What times do you trade best?

What is your optimal share size?

Yes, planning is of paramount importance and if you put the time in to construct a good macro trade plan you will have laid out your road map to getting the results that you want. If you haven't written your plan yet or if it is not a strong model, then stop trading and do it now. Your success is too important to trade by default; i.e., just doing what you feel without a plan...you want to design your path and include everything that you'll need for that journey. Remember success is where preparation meets opportunity.

Myths of Fear and Greed in FX

For the subject of this week's article, I thought that I would take the time to explore the thought process behind most trading decisions we make during our FX speculating. As you may already know if you have read previous articles written by myself or my colleagues, we all drive home the importance of formulating and then following a detailed and actionable written trade plan, so as to remove any underlying emotions from the decision making process and thus enforce ongoing discipline in our trading activities. The less the trade becomes about us and more about our rules and plan, the more we have steered ourselves towards achieving success in the markets on a consistent basis. The plan tells us what to do, as opposed to us looking at a chart and guessing what we should do.

Controlling our emotions during our trading is perhaps the toughest obstacle we face in making our goals a reality. Every single time a candle on the charts moves up or down, we can be easily tempted to click the buy or sell button on a whim, without any real reason to be entering at all! In the early stages of my trading education, I remember reading that candlesticks and trend on a price chart are nothing more than simply a representation of people's emotions when they buy and sell. Rising prices are an illustration of greed in the markets and when prices are falling, we are seeing the picture of fear taking over. Greed causes prices to rally and fear causes them to fall…or so they say. After teaching students worldwide with Online Trading Academy both in the classroom and during the ongoing virtual environment of our online graduate Extended Learning Track program and obviously through my own experiences as a trader for pushing eight years, I have started to look at the emotions of fear and greed in a slightly different light. Let me explain.

One of the most powerful aspects of Online Trading Academy's Core Strategy, is that helps our students to change their mindset of the how markets work and gets them thinking like the groups who know how make the most money in the markets, mainly the Institutions. The difference between the way most retail traders think and act when they place trades and how some of the biggest banks and funds act when they trade, is hugely different. Think about this for a second: when a fund manager places an order to enter the market to take a position, do you think that they are worried about losing the trade and how it will make them feel? Or do you think that they find it easy to pull the trigger because firstly their superior has already given them their risk parameters and secondly because the money at risk is not actually theirs? To the fund manager, taking the trade is nothing more than their job and, like any other job, they need to get on with it on a daily basis.

On the other hand, let's think about the retail trader sitting at home and taking the same trade but with a much smaller size. Even if they were taking the trade at the same time and in the same direction as the fund manager, do you think that there is a possibility that their thoughts may be a little different than the fund manager's? For most retail traders I would say absolutely, and why might you ask? Well for a start the retail trader is trading with their own money, not somebody else's money, which will automatically have a different dynamic in itself, meaning that whatever the outcome of the trade, it will directly impact the retail trader. Secondly, the retail trader has no guarantee of an income at the end of the month, unlike the fund manager or trader who works for an institution. This person will no doubt still earn at the end of the month as long as they follow their instructions and trade plan as outlined to them by their superiors.

I have come to understand that the completely different environments in which retail and institutional traders operate, dictate clearly the challenges that can be faced for most retail speculators out there. I do not believe that the emotions of fear and greed work the same way for the small trader, as they do with the larger trader. In fact, I would go as far as to suggest that greed does not even become a factor in the potential success of the retail trader because if you ask most people who want to trade for themselves what they want more than anything else in their trading, they will normally say, consistency. They just want to be able achieve their goals with low risk trades and slowly build upon this. It does not become about greed at all. It is the fear which tends to be the biggest challenge of all.

It is fear which stops us from taking a solid setup in the markets because we have been on a losing streak, only to see it work out well and the opportunity missed. It is fear which causes us to not follow the trading plan to the hilt and make irrational changes all the time because the odd trade fails to work. It is fear which causes us to get out of a trade far too early with a small profit because we are scared to hold on in case it becomes another loser and it is fear which makes us search over and over again for the perfect strategy which does not exist, simply because we think there is always something out there we are missing out on or don't know about. Fear my friends, is the biggest hurdle any retail trader has to face and will hold you back more than anything else ever will. Recognize that fear needs to be controlled with a plan and discipline. Once the consistency comes, then the fears will subside over time. Oh, and for those of you who were wondering what I feel about greed's place in the market, well that is an easy one. Just ask yourself a quick question: Why do people become greedy? Because they are fearful there will never be enough…

Canada Housing Starts Bounce Back in June

- Housing starts rose to 213k units in June (on a seasonally adjusted annualized basis), recouping most of the ground lost over the last two months. This pushed the six-month moving average close to a 5-year high of 215k units.

- Gains were widespread during the month with both single-detached (+10%) and multi-unit (+9%) starts rising.

- Regionally, strength stemmed largely from Ontario (+24k) and Quebec (+8k), while Newfoundland and Labrador and PEI also recorded increases during the month. Ontario more than erased the losses sustained in May. On the flipside, starts declined in B.C. (-9k) and the Prairies (-6k), with Alberta and Manitoba accounting for the bulk of the Prairie losses.

Key Implications

- The bounce back in housing starts in June puts the second quarter pace of homebuilding at 204k units – a decline of roughly 8% relative to the first quarter. As such, homebuilding activity will detract from growth during the quarter. Having said that, the overall economy remains on track to expand by close to 3% during Q2.

- While we see no harm in the Bank of Canada waiting until October to hike rates, there is a very real possibility that the first rate hike in seven years will come as early as tomorrow. Should the rate hiking cycle be brought forward, Canada's housing market is likely to be slightly weaker than we currently expect. The impact of higher rates – be it now or later this year – will be most pronounced in regions where affordability is the lowest – such as Vancouver and Toronto.

- The GTA housing market is still adjusting to the Ontario Fair Housing Plan which appears to be having the desired effect of cooling the market, with sales and price growth slowing. While starts did pause in May, the rebound in June suggests that the impact on new home construction may not be as long-lasting. Indeed, while the province's housing starts are unlikely to return to the highs seen early this year, we expect them to hold near current levels going forward.

- For the country as a whole, homebuilding activity is expected slow modestly over the remainder of the year, but remain close to the 200K mark for the foreseeable future.

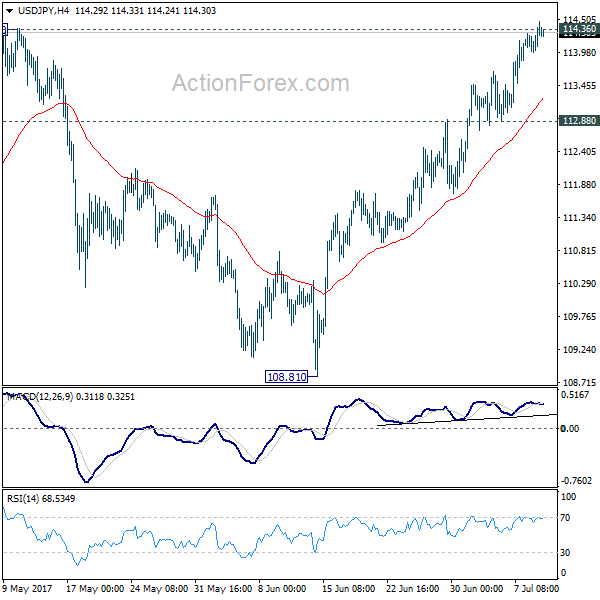

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.83; (P) 114.06; (R1) 114.26; More...

Intraday bias in USD/JPY remains on the upside with focus on 114.36 resistance. Decisive break of 114.36 resistance will confirm our bullish view that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65. On the downside, break of 112.88 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.