Sample Category Title

Inside the Forex Market: Searching for Black Swans?

What is a "Black Swan"?

The term was made popular by Finance professor Nassim Nicholas Taleb, who also writes for the Wall Street Journal and spent 21 years working on Wall Street as a quant trade developing computer models for investment banks. Taleb brought the term to popular attention in the aftermath of the financial crisis in his book "The Black Swan: The Impact of the Highly Improbable".

The term itself refers to an event which occurs well beyond the boundaries of what is typically expected and, therefore, represents a catastrophic surprise. The unexpected and random nature of black swan events makes them extremely difficult to predict. Given the difficult nature of anticipating these events, Taleb suggests it is important for people to always be aware that such dramatic events can happen and to focus on their risk management, protecting themselves.

(As an extra bit of info, the phrase comes from the belief in the Western world that all swans are white. This belief was based on the fact that these were the only ones accounted for until Willem de Vlamingh discovered black swans in Australia).

So, now you know what a Black Swan event is you're probably wondering what some of the most famous Black Swan events are; some of these you might have heard of and maybe some you haven't.

The Collapse of Long-Term Capital Management (LTCM)

In the late 90s, a 100 billion Dollar bond trading fund went pop and nearly took the entire financial system with it through their strategy of highly leveraged arbitrage trading. As the fund grew in size so too did the number of traders trying to piggy-back their strategy, and so the fund moved out of bond arbitrage and into equity arbitrage, swaps, volatility and global markets. Following severe losses during the Asian Financial Crisis, LTCM suffered a 14% loss - its biggest loss ever up till then.

Shortly after the Asian Financial Crisis, Russia defaulted on its sovereign debt which saw global markets plunging and triggered a $53 million one-day loss for LTCM. A few weeks later the fund was facing over $1 trillion in default risks. A default by the fund would have seen around 50 other counterparties (including investment bank UBS) defaulting also, and so the Fed and a conglomerate of Wall Street banks were forced to step in and bail them out.

The Global Financial Crisis

Ten years on from the collapse of LTCM the global financial system was once again rocked by the collapse of a major financial institution. In 2008, Wall Street giant Lehman Brothers filed for bankruptcy with a debt of $619 billion making it the largest bankruptcy filing in history. The bank was heavily involved in the sub-prime mortgage market and highly leveraged so as the credit crunch of 2007 took its toll the bank suffered enormous losses as mortgage delinquencies and foreclosures ripped through the mortgage market.

The US government worked to offer a $700 billion bailout package which failed to pass Congress and subsequently the bank officially went bankrupt. The market reaction was extreme with the FTSE 100 dropping 5% in a day and the Dow Jones shedding 2.5% while HBOS, which owns the UK's largest mortgage lender, suffered a 17.5% one-day loss. These declines came as central banks across the globe offered huge waves of funding to stabilise the market.

The Oil Crisis

In just a few months over 2014, the price of Oil plummeted from over $100 per barrel to just $50. US Crude Oil production has been surging for years jumping over 50% between 2011 and 2013, annually, from 2 billion barrels to 3 billion barrels. In 2014, Libya's oil production which had dropped to 250k barrels per day from around 1.8million barrels over April-June sharply rebounded to 900k barrels a day. The sharp increase in supply following the reopening of Libya's oil fields which had been closed for months during the civil war caused an acute shift in the supply-demand scale sending Oil cratering.

These are just a few of the many Black Swan events which have rocked markets. So, as these events are so unpredictable, what is the importance for you? The main takeaway here comes down to risk management. When trading, your capital is always at risk, and it is important to always be aware of the unmeasurable risk of such an event taking place. So, always make sure that you trade with a stop loss, this means that should such an event occur your account will be protected against any sudden moves.

What is Forex Trading?

There are some things that knock you for six when you hear them, and this is generally the case when one first encounters the foreign exchange markets, or 'forex' for short. Followed by the credit (debt) market (think US government bonds, notes and bills here), forex is the largest, most liquid market on the planet - an immense auction house which has a daily turnover of $5.1 trillion (according to the 2016 Triennial Central Bank Survey of FX and over-the-counter (OTC) derivatives markets). Forex is a globally decentralized marketplace, which simply means that there's no central exchange or physical location. It Operates around the clock five days a week, with the action beginning in Wellington, New Zealand and closing on Friday evening in New York, essentially allowing one to pick and choose when to trade.

Within this mammoth auction house, the forex market caters to investment managers, hedge funds, corporations, individual speculators/investors and international trade. For example, in order for a UK company to import baseball caps from the US, the Brits would have to exchange GBP for US dollars in order for the organisation to be able to complete the transaction.

The main participants, other than government central banks who probably have the most influence, are the large international banks, such as: Citi Bank and JP Morgan. These two organisations recorded the largest overall volume in the forex markets as of May 2016. Now that we have a brief understanding of what the forex market is, how much is traded/exchanged on a daily basis and who the main 'players' are, let's look at what forex trading is from an individual trader's perspective. If you've ever been on holiday to a foreign country, there's a good chance that you've already participated in the forex market, exchanging one's home currency for that of another.

The forex market is traded in pairs. The EUR/USD, the GBP/USD and the AUD/USD are all considered currency pairs. The 'base currency' is the first currency that appears in a currency pair quotation, the EUR, GBP and AUD (highlighted in bold) are all base currencies. The 'quote currency', or 'counter currency', is the second currency - the US dollar (underscored). So, when we look at the currency quotations provided by IC Market's market watch platform, one can see that in order to buy 1 unit of GBP, it will cost buyers $1.25181 at current market prices. The 'ask' tab represents the current price for buyers, and the 'bid' tab denotes the current price offered to sell.

In your forex trading career, you'll be dealing with a plethora of new terminology. A 'pip' is one of the more common terms you'll hear in the trading industry, which essentially means 'point in percentage' or 'price interest point'. IC Markets uses 4 decimal places to denote a one-pip movement. Using the market watch platform above, we can see that in order to buy 1 Euro, it'll cost $1.06950. Now, assuming that the market skips to $1.06960, price has just moved one pip higher. Conversely, should the unit decline in value to $1.06900, one is now able to purchase the 1 unit of Euro for 5 pips less than originally quoted ($1.06950-$1.06900). What is the very last number on the currency quotation then? This is called a 'pipette', which equals 1/10 of a pip. Therefore, if the EUR/USD quotation above moves to $1.06952 from the current price of $1.06950, we effectively have a 2-pipette advance.

The value of a pip, of course, depends on how a trader sizes his/her positions. This is where the use of leverage and risk management comes into play.

Leverage basically means having the ability to control a large sum of capital using very little of your own funds and borrowing the rest. By way of example, say one looks to trade a $100k position at leverage of 100:1, the broker will set aside $1k from your funds, thus allowing you to take on the larger position. IC Markets offer flexible leverage options ranging from 1:1 to 1:500, which is good news for conservative traders out there. As you can imagine, leverage is a double-edged sword. While high leverage could net one incredibly high gains, it can just as easily wipe you out, highlighting the need to correctly manage risk!

The difference between the bid/ask prices is called the 'spread'. This is another common term, which basically represents brokerage service costs. Looking at the GBP/USD quotation above, one can see that the spread or 'cost' to purchase 1 unit of GBP using IC Markets is around half a pip. The EUR/USD effectively has no spread at the time of writing - very tight indeed! The broader the spread the more expensive it is for one to trade, whereas the thinner the spread the cheaper it is. Liquid and frequently traded currency pairs usually offer a small bid/ask spread, while the more erratic, less traded pairs typically boast a larger bid/ask spread. In addition to this, spreads typically widen during high-impacting news events, such as the mighty US non-farm payrolls report generally released on the first Friday of each month. Technically speaking, spreads widen here due to lack of liquidity. Let's not forget that a spread is simply the difference between willing buyers and sellers. At times of high volatility, the difference becomes larger and thus the spread is equally increased.

How To Bounce Back From Trading Losses: 5 Lessons Learned

Trading is an interesting profession and has no peak as in other occupations. It is in fact an endless journey of discovery of oneself and trading itself. Trading for me at beginning was very tough not that I was not successful in other endeavours but i took it like every beginner thinking that it was easy. With this perception, i approached trading without a plan or proper trading education on how the market works. What do you expect? Your guess is as good as mind. It was a total disaster after taking many losses; i was almost psychologically blown a way. At this stage, two important things happened to me, my P&L was in the red and i was down emotionally.

My worst loss that stands out in all my losses was a trade i took (short EURUSD) in anticipation of French Referendum thinking that it would be in favour of the European Union but alas I got a margin call after the result was negative. Please do not ask me about a stop loss i did put a stop loss but i later removed it because i was so confident it was going to be a winning trade.Hey, can't you understand. I have been declaring losses so i thought this time around i would take a large position and cover all my losses. I was subsequently charged to court (trading), tried and found guilty (for losses).Punishment, six months without trading. While serving my term i embraced trading education especially technical analysis and trading psychology. So when I got a handle of certain strategies applying technical analysis and trading psychology i started trading again but not without losses but i followed my trading plan anyway and things improved especially when i became comfortable with losses as expenses in the business of trading.

Valuable Lessons/Tips

Never Trade Without A Trading Education-acquire proper trading education because the knowledge through trial and error in the market can be more expensive and time consuming than the normal trading education

Never Trade Without A Plan

Having a trading plan is a most in this business if you want to succeed. This plan most specify and predetermine your entries,exits,stop loss, position size and your psychology(your emotion at the time you click enter).There could be more you could have on your plan but the most important thing is that you must follow it, because when you follow your plan you have a chance of succeeding in trading. You may be tempted to say do I have to follow this damn plan everyday, just go to a near by Airport and observe what pilots do everyday; they follow their flight plan and check each one before taking off. He can as well say, i feel better flying without my plan today because I do it everytime.That you know my friend will be disastrous.

Do Not Be Smarter Than Your Emotion

What do traders do when they are tired? They wait for an opportunity instead of turning off their computers and call it a day they stay on waiting to initiate a position and when the trade turns out to be a loser they become angry adding to the tiredness.Hey,you know what, you can not win at trading if you are not in your right frame of mind. If you have problems with your spouse please do not trade, if you have a string of losses do not trade, take some time off and go over your losses until you know what went wrong before you can put on another trade. If any thing occupies your mind apart from the market and following your trading plan when you are ready to trade, do all you can to resolve it before you start trading for the day. If you cannot, go golfing.

Cut Your Losses Shut And Let Your Winners Run

This one sounds familiar,right.The professionals do exactly as is stated here but what do novice traders do? They do the opposite by letting their losses run and cutting their winners shut. In other words, they are patient with their losses and impatient with their winners thinking that their positions would come back. The hard truth is the market does not know whether you are winning or losing. It will go wherever it wants to go and do what it has been doing, which is moving up, down and sideways. It is now left to you to find opportunities within these up moves and down moves.

Becoming A Professional Trader Takes Time

This might sound funny. Do not ask any trader to tell you how many years it will take you to become a professional/experience trader. The truth is that real professional traders know that the education of a trader never ends. It is ongoing because market is not static, it changes so if you think you have acquired enough trading knowledge and market conditions change and you cannot cope with the changes you automatically become a learner. The fastest way to become a good trader is to learn from the professional traders (their strategies and how they apply them) taking into consideration your own psychological make up.

NZ Retail Softens | NZDUSD Considers Break of Monthly Pivot

At 4.5%, credit card retail sales remain elevated compared with some economies, yet the 1yr average suggests further weakness ahead. NZDUSD has failed to take the Feb highs and the odds of a retracement lower are quickly building.

Electronic card retail sales fell from 5.2% YoY to 4.5% YoY, a two-month low which has dragged the 12-month average down to 4.9%. The 1yr average better displays the cyclical tendency of retail spending, which peak in Q2 2016 and suggests we may continue to see downwards pressure on retail spending throughout 2017. The monthly read was steady at 0%, yet as this followed on from a -0.4% contraction in May which was the 3rd contraction in 4 months, further softness is yet to be revealed in the YoY read. Also, whilst -0.4% contraction may not sound too much, but by historical standards it is at the extreme of a -1 standard deviation.

However, where retail sales suggest further weakness from the consumer side, business survey's such as the PMI's continue to suggest support for the economy. Tomorrow we get to see if business PMI maintains positive outlook.

We have monitored NZDUSD over recent weeks to see if it could break above the 0.7375 high from February. Whilst we cannot rule out a break later this year, we now see potential for a pullback from current levels. Last week produced a dark cloud cover pattern which was also a marginally bearish outside week. The fact its high was below the Feb high is also another side of near-term weakness, as is the fact this occurred after touching the upper bollinger band. The 20 week DPO (detrended price oscillator) also moved lower after testing its own bollinger band.

To look at this from the US Dollar's perspective, the downside appears to have stopped for now and eyes will be on Yellen's testimony on Wednesday night for further clues of Fed tightening. As the USD remain unloved and possibly oversold over the near-term, we see potential for a bounce higher on DXY which may pile on the pressure on NZDUSD.

The impressive gains from the May low was fuelled by three main drivers; RBNZ becoming less dovish; A weaker USD; higher milk powder prices. It is therefor worth noting that some of this support has taken a side-step whilst NZDUSD has remain elevated. Milk prices stopped rising in June, RBNZ have not exactly turned into prominent hawks and, as mentioned, there is potential for a spike higher on US Dollar as markets continue to doubt Fed's ability to tighten.

NZDUSD appears to be considering a break of 0.7250 support. As this is also where the monthly pivot awaits, it may hold for a while longer yet but we also note a lower low and lower high has formed to suggest downside momentum is building.

We can use a sell-stop to catch a downside break with the view to target 0.719, and 07145 where the 38.2% retracement awaits.

GBPJPY – Backs Off Higher Prices, Vulnerable

GBPJPY - The cross continues to face upside pressure but could see pullback threats in the new week having continued to reject higher prices. On the downside, support comes in at the 146.00 level where a violation will aim at the 145.50 level. A break below here will target the 145.00 level followed by the 144.50 level. Conversely, resistance is seen at the 147.00 level followed by the 147.50 level. A cut through that level will set the stage for a move further higher towards the 148.00 level. Further out, resistance resides at the 148.50 level. All in all, GBPJPY looks to pullback further.

No Catalyst Overnight

No catalyst overnight

A lack of market agitators has led to a very parochial and lacklustre overnight session. However not too surprising as the market’s current driver, Fixed Income, walks a razor’s edge with the Bank of Canda ( BOC) and Yellen’s Humphrey-Hawkins testimony meeting head on in Wednesday’s NY session. So fixed income investors will likely take their lead from whether the Bank of Canada hikes rates and track cues from Fed Chair Yellen, more so if she taps the brakes on the FOMC hawkish lean.

After nearly a decade of loose monetary policy, Global central banks are looking to turn down the music at the global bond party that has raged on well past its expected shelf life. After a week of continued repricing yields higher in mature economies -a predictable feedback loop to hawkish policy guidance, that too may have run its course as the markets continue to grapple with the notion of higher interest in a low inflation world. Despite this growing sense of reality setting in, traders remain tied up in knots fearing inflationary data surprises could induce a secondary sell off.

After starting out with a bounce in their step in early Asia, yesterday equity investors found little direction overnight.After Asia caught up with the Wall Street Friday rally markets became rather directionless during the overnight sessions.

Commodity markets optimism continues to wane on revamped analysts warnings as WTI prices nudged higher with talk of production kerbs in Libya and Nigeria and a sign of shrinking U.S. stockpiles

The forex traders had a case of butterflies in the stomach ahead of upcoming BoC and Yellen risk which saw traded volumes drop well below last month’s average turnover; perhaps the tepid volumes are reflecting reduced summer positioning, a lack of interest or a bit of both. However, that tune will change as we move deeper into a potentially dangerous trading week.

Dr Yellen

Her testimony could be the least impactful risk of the week. It’s highly unlikely she will change her hawkish tone, and with the market in total data-dependent mode, traders will look past Fed speak and focus on both US CPI and the BOC announcement

US CPI

CPI data will be the key for the USD near-term direction. Despite the Hawks ruling the roost, it means little to traders without the inflationary impact kicking in. After three consecutive misses on CPI, the Fed’s ability to look past the transitory inflation factor will be tested on another downside inflationary wobble.

Bank of Canada

The markets completely fixated on this event and now pricing in over 90% probability of a hike in July and two full hikes by the end of 2017 implying an evolving tightening cycle Given this skew, a no rate hike could topple the apple carts and send both Fixed income and currency markets into a frenzy.The more likely scenario, however, is a one and done with the bank expressing some lingering downside economic concerns and a wave of USD-CAD profit taking ensues

Currency Markets

Price action on Monday was not too untypical of post NFP trade as traders tend to pick up the pieces after the weekend to digest the data.

EURO

Extremely quiet session lacking any central catalysts and with a slow week on the economic calendar traders will look to EDB rhetoric as the primary driver. Few convictions either way despite EU Bond markets trading a touch stronger with German and French 10-year yields falling 3bps

Japanese Yen

The first question I fielded this morning is why is USDJPY not trading higher given the Japan -US Bond differential back in vogue. First US bonds rallied a touch overnight, but I also suspect some short term optionality is in play.By all accounts with the BOJ and FED divergence still in the cards, we should be trading higher. However lingering regional geopolitical concerns ( North Korea) and domestic concerns about PM Abe’s continuity are weighing on Japanese investors as a drive for downside protection enters the psyche as local equity markets look ” toppish” . It appears these fears are tempering USDJPY upside despite the FED maintaining its tightening conviction, and BoJ its easing bias

USD/CAD Canadian Dollar Lower Ahead Of Central Bank Decision

The Canadian dollar started the week on the back foot as the USD recovered some ground during the Asian trading session touching session highs of 1.2932. Oil prices swung wildly in the past 24 hours ending in a net positive gain for the black stuff and helped the loonie reduce its daily losses ahead of Wednesday's widely anticipated interest rate decision by the Bank of Canada (BoC).

The Canadian dollar appreciated on Friday with the better than expected release of the Canadian jobs report. The economy added 45,500 jobs busting forecasts of 10,000 and forcing a drop in the unemployment rate to 6.5 percent. The American jobs report published at the same time usually takes the spotlight at it also showed a 223,000 job gain south of the border but the rising expectations of the BoC hike rates on its July 12 monetary policy meeting pushed the CAD over the USD.

The probability of a rate hike on Wednesday has gone up considerably since senior BoC policy makers started commenting on the effect of the two rate cuts in 2015 and the fiscal stimulus package launched in 2016. Money markets are pricing in a rate hike on July 12 and a follow up in the December monetary policy meeting to keep the gab between the Canadian benchmark rate and the Fed funds rate from diverging further.

The USD/CAD gained 0.068 percent on Monday. The currency pair is trading at 1.2886 as the USD enjoyed a recovery in the Asian and European session that sent the pair above the 1.29 price level. A modest recovery in oil prices above $44 per barrel helped the loonie end up back above 1.29.

Canadian jobs surprised to the upside with another strong gain. Canada added 45,000 jobs in June, although less full-time positions than in May but a strong showing that dropped the unemployment rate to 6.5 percent. The loonie appreciated after the release as it adds further speculation that the Bank of Canada (BoC) will hike rates on July 12 after several comments from senior central bank members. The Canadian central bank changed its tune on June 11 and started signalling an upcoming rate hike after the two rate cuts in 2015 and the government's fiscal stimulus seemed to have done their job. The BoC was not forecasted to hike rates until 2018 as there are still major question marks with oil prices and the NAFTA negotiations in the fall, but the pace of growth in the Canadian economy is giving the central bank the confidence to make a move sooner rather than later and keep up with the Federal Reserve.

The Bank of Canada (BoC) monetary policy meeting will be the highlight of the week. Central bank rhetoric in the developed economies has now taken hawkish tone as the European Central Bank (ECB), Bank of England (BoE) and the Bank of Japan (BOJ) have seen improvement in economic growth.

The BoC is ahead of the pack and slightly behind the pack as it carries no quantitative easing program to taper and its benchmark rate is 50 basis points. A 25 basis points in the next meeting would keep it close to the 100–125 basis points of the Fed funds rate.

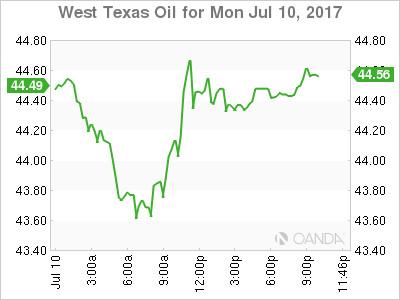

Oil rose 0.319 percent in the last 24 hours. West Texas Intermediate is trading at $44.40 after comments from Saudi Aramco CEO said on Monday that lack of new discoveries and a drop in investments will contusion global supply of oil. The market does not share the pessimistic view of the state run energy company with supply gaps anticipated to be filled by Brazil, Canada and the United States.

Oil rigs in the US have started to increase as shale operations take advantage of stable prices at current levels. The diplomatic disagreement between Qatar and other Arab nations leaves in question the unified front of the OPEC as Saudi Arabia's leadership in the group will be questioned. Weekly inventories regain their normal publication date with US crude stocks to be reported on Wednesday, July 12 at 10:30 am EDT.

Market events to watch this week:

Wednesday, July 12

4:30am GBP Average Earnings Index 3m/y

10:00am CAD BOC Monetary Policy Report

10:00am CAD BOC Rate Statement

10:00am USD Fed Chair Yellen Testifies

10:30am USD Crude Oil Inventories

11:15am CAD BOC Press Conference

Thursday, July 13

8:30am USD PPI m/m

8:30am USD Unemployment Claims

10:00am USD Fed Chair Yellen Testifies

Friday, July 14

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Gold Remains Under Pressure, Touches 4 Month Lows

Gold has shown some downward movement on Monday, but is unchanged on the day. In the North American session, spot gold is trading at $121.09 per ounce. Earlier in the day, gold prices dropped to a low of $1204, the metal's lowest level since mid-March. On the release front, there are no major events on the schedule.

Gold had a rough week, dropping 2.4 percent. The metal lost ground on Friday, as Nonfarm Payrolls rebounded in June, climbing to 222 thousand. This easily beat the estimate of 175 thousand and marked a 4-month high. At the same time, employment data was not all positive, as wage growth wage growth was unchanged at 0.2%, shy of the forecast of 0.3%. Weak wage growth has remained soft throughout the first half of 2017, despite a tight labor market. With wages remaining stagnant, inflation is also mired at low levels. The Fed has consistently said that it plans to raise interest rates for a third and final time in December. Last month, Fed Chair Janet Yellen shrugged off inflation worries, saying that she expected inflation was mired at lows levels due to temporary factors. However, the markets don't seem to be buying in, as the odds of a December hike have dropped to just 47%, according to the CME Group. The US economy slowed down in the first quarter, and there are signs that Q2 will also be soft. Consumer spending, which comprises two-thirds of US economic growth, remains soft. Another sore point in the economy is inflation, which remains below the Fed's target of 2%. If the economy doesn't show signs of stronger growth and higher inflation, the Fed might change its tune about a December rate, which would be good news for slumping gold prices.

Pound Steady After Ending Week on Losses

GBP/USD is showing limited movement in the Monday session. In North American trade, the pair is trading just under the 1.29 line. On the release front, there are no major events on the schedule.

The British economy has managed quite well since the Brexit vote in June 2016, but last week's PMIs may signal the much-feared economic downturn. PMIs in the manufacturing, construction and services sectors all pointed to slower growth in June, compared to the May readings. The double whammy of the British election and the start of Brexit talks with Europe have increased uncertainty and resulted in a decrease in new orders across the economy. The BoE is divided over whether to raise interest rates in the next few months, and the public disagreements between BoE policy makers over rate policy will not help investor confidence. The May government has a razor-thin majority, and must negotiate a divorce with an angry European Union that does not want to see other members opt to leave the club. The UK will release key employment numbers on Wednesday, with wage growth and unemployment claims expected to worsen in June.

The US wrapped up last week with key employment numbers, and the data was mixed. Nonfarm Payrolls rebounded in June, climbing to 222 thousand. This easily beat the estimate of 175 thousand and marked a 4-month high. However, wage growth remains soft, as Average Hourly Earnings was unchanged at 0.2%, shy of the forecast of 0.3%. Weak wage growth has remained soft throughout the first half of 2017, despite a tight labor market. With wages remaining stagnant, inflation is also mired at low levels. If inflation does not improve, the Federal Reserve may have second thoughts about a rate hike in December. Currently, the odds of an increase in December have dipped to 47%, as the markets clearly have their doubts that the Fed will press the rate trigger.

Dollar Pushes Above 114 on Weak Japanese Mfg. Report

USD/JPY has posted slight gains in Monday trading. In the North American session, the pair is trading just above the 114 level. On the release front, Japanese data started off the weak on a sour note. Core Machinery Orders declined 3.6%, well off the forecast of a 1.7% gain. Japan's current account surplus dropped to JPY 1.40 trillion, short of the estimate of JPY 1.63 trillion. There are no major events in the US.

Japan's economy has improved in 2017, buoyed by a stronger global economy. This has translated into increased demand for Japanese goods and this has boosted the manufacturing and export sectors. The Tankan Manufacturing Index jumped to 17 in the first quarter, its strongest showing since 2014. However, Core Machinery Orders is raising some concerns, as the indicator has posted two straight declines of 3.1% and 3.6%. We'll get a look at Preliminary Industrial Production on Friday. The indicator recorded a strong gain of 4.0% in April, but the markets are braced for a sharp downturn in June, with an estimate of -3.3%. If manufacturing indicators continue to miss expectations, the yen could continue to lose ground.

The US wrapped up last week with key employment numbers, and the data was mixed. Nonfarm Payrolls rebounded in June, climbing to 222 thousand. This easily beat the estimate of 175 thousand and marked a 4-month high. However, wage growth remains soft, as Average Hourly Earnings was unchanged at 0.2%, shy of the forecast of 0.3%. Weak wage growth has remained soft throughout the first half of 2017, despite a tight labor market. With wages remaining stagnant, inflation is also mired at low levels. If inflation does not improve, the Federal Reserve may have second thoughts about a rate hike in December. Currently, the odds of an increase in December have dipped to 47%, as the markets clearly have their doubts that the Fed will press the rate trigger.