Sample Category Title

USD/JPY Analysis: Trades Near Two-Month High

Following the hourly surge on Friday morning, the US Dollar lost its strong upside momentum against the Yen and continued to trade with moderate gains. Contrary to expectations, the monthly R1 did not provide enough resistance to hinder or halt the pair. Thus, the rate has approached a two-month high at 114.34, suggesting that this level could finally reverse the Greenback to the downside. Technical oscillators may likewise reach the overbought area in this session, adding some ground to the aforementioned scenario. Nevertheless, there is still some upside potential until the upper channel boundary circa 114.60. In case bears are to prevail, the 55– or 100-hour SMAs located at 113.60 and 113.42 on Monday morning may be considered the bottom limit today.

GBP/USD Analysis: Recovers Losses On Monday

Despite technical indicators being bullish on Friday morning, GBP/USD plunged 98 pips within couple of hours mid-session. The most significant downfall resulted from weak UK data released at 0830GMT. This move pushed technical indicators in the strongly bullish and oversold territory. The rate, however, was halted at the 55- day SMA near the 1.2875 mark prior to making a U-turn. The Pound has started to recover some losses and is expected to continue doing so in this trading session, as the pair has formed a minor falling wedge that should lead it to the upper boundary of this pattern circa 1.2930. The Sterling may likewise trade sideways, given the lack of strong market movers scheduled for today. By and large, a possible trading range is likely to be 1.2883/1.2930.

EUR/USD Analysis: Trades Near 1.14 Mark

The common European currency bounced off a long term descending channel’s resistance line against the US Dollar. As a result of the following decline the pair has recently passed the support of a medium term ascending channel. However, the decline might not continue. The reason for that is the fact that the area from 1.1395 to 1.1374 is full of support levels. All of the hourly SMAs, which are used by Dukascopy Bank analysts are located in that region. In addition, the weekly PP is stationed at 1.1388 mark together with the 23.60% Fibonacci retracement level. Due to that reason it can be expected that the currency pair will find support and not continue the decline right away. However, in accordance with the larger scale pattern the Euro should depreciate against the US Dollar

British Manufacturing Production Fell Unexpectedly In May

'This morning's data paint a rather bleak picture for the U.K. economy and underline the challenges lying ahead.' - Kay Daniel Neufeld, Centre for Economics and Business Research.

Output in the UK manufacturing industry dropped unexpectedly over the month in May, suggesting that the country's economic growth continued to weaken. The Office for National Statistics reported on Friday that manufacturing production fell 0.2% in the observed month, compared with April's 0.2% increase. Meanwhile, analysts anticipated British manufacturing production to expand 0.5%. The report showed two main contributors to the decline, with car production registering a 4.4% fall, the steepest since February 2016, while energy sector fell 0.8% amid lower gas supply. On a yearly basis, total production dropped 0.2% with downward trends in two of the four main sectors. Experts suggested that a high degree of uncertainty about the future of the UK and the European Union's trade relationship weighed on the country's manufacturing industry. Moreover, weaker-than-expected figures added to expectations for a more modest Britain's economic expansion in the Q2, following the first quarter's 0.2% increase, the lowest among the G7 countries.

US Non-Farm Employment Improves Significantly In June

'The continued vitality in the U.S. labor market means that the Fed is on track to begin shrinking its balance sheet in September and to raise rates again in December.' – Nariman Behravesh, IHS Markit

US private companies showed a stronger-than-expected job growth in June, indicating that the labour market continued strengthening further. The official Labour Department's report showed that the country's private sector added 222K jobs last month, surpassing market expectations for a modest increase of around 175K in June. Meanwhile, May's figure was revised up to 152K from 138K registered previously. The US non-farm payrolls increase, the second largest within this year, was supported by strong gains in government, healthcare, restaurants as well as business and professional services sectors, the Labour Department revealed. Notwithstanding job growth acceleration, the unemployment rate was slightly higher, at 4.4%, suggesting that more people were left without job. In addition, the report showed that average hourly earnings rose modestly, jumping 0.2% over the month of June, with 2.5% yearly increase in wages. Analysts believed that weak productivity was curbing wages, while some of them were optimistic over the tightening labour, expecting it to spur wage growth at a faster pace.

Canadian Labour Market Adds 45.3K Positions In June

'We had held on to our October forecast for a Bank of Canada rate hike, but concede that's likely to end up off the mark, as today's jobs numbers cement the case for the central bankers to raise rates in the coming week.' - Avery Shenfeld, CIBC

Canadian employment rose more than expected last month, setting stage for the Bank of Canada to make an interest rate hike. Statistics Canada reported on Friday that the Canadian economy created 45.3K jobs in June, following the preceding month's 54.5K gain and surpassing analysts' expectations for an 11.5K increase. The report showed that employment growth was mainly supported by faster part-time job creation, with 37.1K positions added last month, compared with an 8K rise in full time jobs. Meanwhile, the unemployment rate dropped to 6.5%, while analysts expected to see an unchanged reading of 6.6%. In regional terms, the largest job creation was registered in British Columbia and Quebec, where unemployment rate remained at 6%, the lowest level since 1976. Strong data provided some confidence for the Bank of Canada to raise interest rates this week. Moreover, some analysts anticipate the next rate hike in October 2017 to reverse two rate cuts made in 2015, which helped the Canadian economy to confront the effects of the slump in oil prices.

JPY Set To Weaken, USD Trendless Amid Lacklustre Jobs Report

Mixed jobs report failed to set new trend

On Friday, the US jobs report showed that the pace of job creation bounced back in June and addressed investors' concerns after a worrying slump in May. The US economy added 222k nonfarm jobs in June compared to an upwardly revised figure of 152k in the previous month. However, the lack of consistent wage pressure scaled down the market's optimism. Average hourly earnings grew 2.5%y/y in June (versus 2.6% expected) compared to a downwardly revised number of 2.4% in May.

June's inflation figures are due for released on Friday and according to the latest survey, headline inflation is expected to have eased to 1.7%y/y from 1.9% in the previous month amid falling energy prices. The core measure is expected to remain stable at 1.7%.

After printing at 0.5%y/y in May, real average weekly earnings will also be released on Friday. The indicator started the year in negative territory, contracting 0.6% and 0.5% in January and February, respectively, before bouncing back to 0.6% in April, highlighting the Fed's sensitive work. Indeed, the solid pace of hiring failed to translate into higher nominal wage for Americans, while looking at the adjusted measure for inflation, the picture is even darker as since last August real wage growth have been slowing down significantly. We suspect the Fed wants to see a solid recovery in real wage before accelerating the pace of tightening. This is indeed the guarantee of a solid job market that could stand tighter monetary conditions.

The greenback was little changed after Friday's jobs report. The dollar rose 0.22% against the Japanese yen and 0.12% against the Canadian dollar. Investors were looking for a new driver. They will have to wait another round as the report didn't allow to reduce the level of uncertainty.

Yen set to weaken on continued Fed normalization path

That is a good news for the Bank of Japan, investors are estimating the likelihood of another US rate hike much higher which is driving the yen currency lower. The US ZIRP (zero-interest rate policy) seems to approach to an end. The rate differential between the US yields should then increase.

The spread between US 10-Y and Japan 10-Y is now widening. The US is now whistling the end of the free money era and Japan which has been struggling to fight against deflation may now have a unique occasion to see its inflation running back again.

For the time being, Japan fundamentals data are still on the soft side. This morning May machine orders declined by 3.6% m/m after the fall of 3.1% in April. The USDJPY is now monitoring its highest level in a year and we believe that in the absence of geopolitical uncertainties, the JPY should further weaken. The summer promises to be quiet for the BoJ.

EURGBP In Neutral Phase, Risk To Upside With Rising Upper Bollinger Band

EURGBP is neutral in the short-term. The pair has been trading sideways since early June after making a substantial recovery from the April low of 0.8346. The sideways Bollinger band on the 4-hour chart is indicative of a trendless market.

After rising towards the upper Bollinger band and peaking just outside the line, prices made a corrective move lower. Meanwhile, the RSI reached overbought levels just above 70 on the 4-hour chart when the market hit a high of 0.8860 on July 7. The indicator is now flat, suggesting consolidation in the near term.

Support levels are located at key Fibonacci retracement levels of the rise from 0.8755 to 0.8860. The first support comes in at the 23.6% Fibonacci at 0.8835. Below this, further support lies at 0.8820, defined by the 38.2% Fibonacci. From here, the 50% Fibonacci at 0.8807 is the next target. The 61.8% Fibonacci at 0.8795 is located around the lower end of the recent trading range.

Should upside momentum pick up, EURGBP could see a re-test of the 0.8860 high and a break above it would open the way towards the June 28 high of 0.8880. Such a move would shift the short-term neutral bias to a bullish one, extending the recent uptrend that started from the April low of 0.8346.

Overall, the medium-term outlook is neutral to bullish as the upper Bollinger band is rising.

Dollar Continues To Strengthen, Euro Steady, Commodities Pressured

As the Asian markets were coming to a close, the dollar continued gaining against the yen following a strong boost on Friday. In the meantime, the yen was also weakened by soft data releases, reaching a near two-month low against the dollar. The euro was steady against the dollar while the pound gained ground, to ease some of the Friday's weakness.

The dollar continued building on Friday's gains against the yen during today's Asian session. Today's speech by Bank of Japan Governor Haruhiko Kuroda reiterated the bank's policy to maintain its current accommodating monetary policy. This along with worse-than-expected data releases out of Japan further weakened the yen, pushing it to a near two-month low. Both Japanese current account and machinery orders came in well below expectations. Dollar/yen opened at 113.88 and continued trending higher to last trade at 114.22 as the Asian trading session was coming to a close.

The dollar index, a broad measure of the greenback's strength, firmed up during the Asian session to last trade at 96.072.

The euro was steady against the greenback during the Asian session. Euro/dollar opened at 1.1397 and was last trading at 1.1399 as the European trading session was about to start. The euro didn't get much boost from the weekend interviews by two members of the European Central Bank. In a TV interview for Bloomberg, Bank of France Governor Francois Villeroy de Galhau called for a decision on adaptation of the intensity of the ECB monetary policy in autumn. This may signal a potential absence of clues during the last policy meeting before summer holidays on July 20. ECB Chief Economist Peter Praet, speaking in a newspaper interview released the same day, insisted that “we still need a long period of accommodative policy.”

Sterling edged higher during today's session, easing some of Friday's losses. Pound/dollar opened at 1.2881 and was last trading at 1.2886. In the absence of data releases out of the UK, the current political situation around the latest Brexit developments could have been commanding much of the forex trading around the pound as of today. The UK will release key labor data such as June unemployment and average earnings for May on Wednesday, which could dictate much of sterling's volatility. In the meantime, two Bank of England members will speak on Tuesday, potentially giving more insight into the bank's latest thinking.

The Canadian dollar edged lower today after a strong rally on Friday amid figures pointing to an improving labor market. The upbeat data also adds to speculation that the Bank of Canada could start tightening monetary policy as soon as this week during its planned policy meeting.

Looking at commodities, oil prices continued to fall, inching lower during the Asian trading hours. WTI was last trading at $44.20 a barrel, while Brent was at $46.65. The oil price have been under pressure for four consecutive days.

Gold also continued to decline as the dollar strengthened. The precious metal was last trading at $1,206.31 an ounce, its lowest since mid-March.

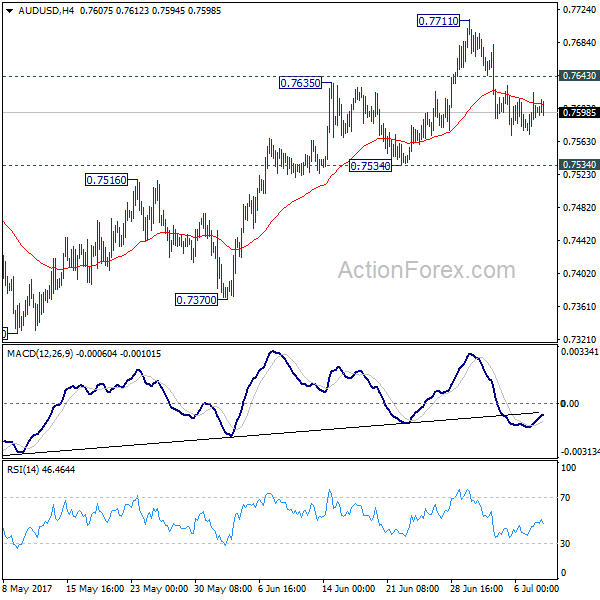

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7574; (P) 0.7598; (R1) 0.7625; More...

Intraday bias in AUD/USD remains neutral for the moment. With 0.7534 support intact, another rise is in favor. Above 0.7643 minor resistance will bring retest of 0.7711. Break will extend the rally from 0.7328 to 0.7748 resistance and above. At this point, there is no clear sign of range breakout yet. Hence, we'd be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, break of 0.7534 will indicate near term reversal and turn bias back to the downside for 0.7370 support.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8082) and above.