Sample Category Title

Japan’s Services Sector Growth Expanded In June

For the 24 hours to 23:00 GMT, the USD declined 0.24% against the JPY and closed at 113.10.

In the Asian session, at GMT0300, the pair is trading at 112.97, with the USD trading 0.11% lower against the JPY from yesterday's close.

Overnight data indicated that Japan's Nikkei services PMI rose to a level of 53.3 in June, compared to a level of 53.0 in the previous month.

The pair is expected to find support at 112.69, and a fall through could take it to the next support level of 112.40. The pair is expected to find its first resistance at 113.31, and a rise through could take it to the next resistance level of 113.64.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

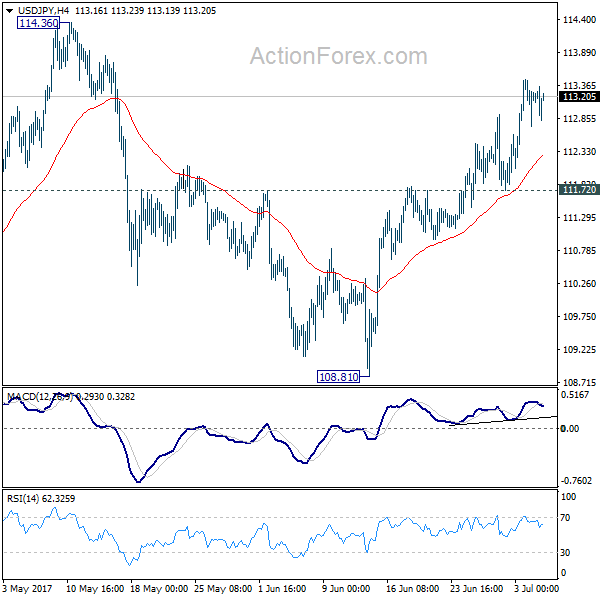

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.85; (P) 113.14; (R1) 113.57; More...

With 111.72 support intact, further rally is expected in USD/JPY for 114.36 resistance. Break there will confirm our bullish view that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65 next. However, break of 111.72 will indicate near term reversal and turn bias back to the downside for 108.81.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Swiss Franc Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.12% against the CHF and closed at 0.9647.

In the Asian session, at GMT0300, the pair is trading at 0.9644, with the USD trading marginally lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9624, and a fall through could take it to the next support level of 0.9604. The pair is expected to find its first resistance at 0.9662, and a rise through could take it to the next resistance level of 0.9680.

With no economic releases in Switzerland today, traders will look forward to global macroeconomic events for further direction.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canada’s Manufacturing Sector Activity Declined To A 4-Month Low In June

For the 24 hours to 23:00 GMT, the USD declined 0.52% against the CAD and closed at 1.2937.

On the macro front, Canada's Markit manufacturing PMI eased to a four-month low level of 54.7 in June, suggesting a slowdown in the nation's economic momentum. The PMI had registered a reading of 55.1 in the preceding month.

In the Asian session, at GMT0300, the pair is trading at 1.2936, with the USD trading slightly lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2895, and a fall through could take it to the next support level of 1.2853. The pair is expected to find its first resistance at 1.2996, and a rise through could take it to the next resistance level of 1.3055.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

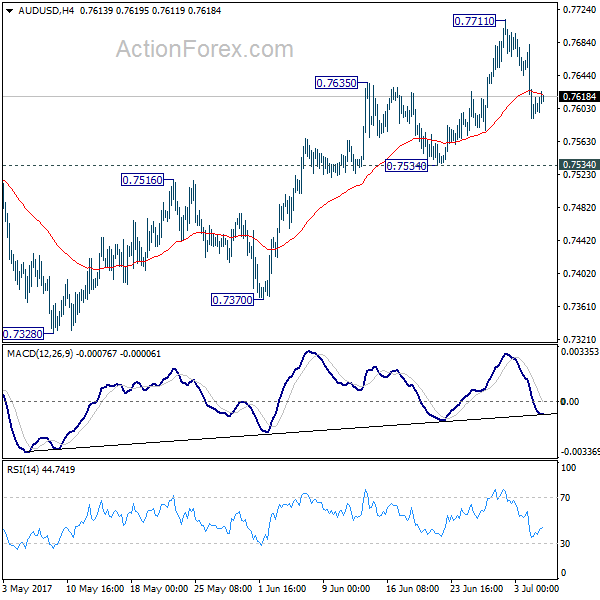

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7569; (P) 0.7626; (R1) 0.7660; More...

AUD/USD is staying in consolidation below 0.7711 and intraday bias remains neutral. With 0.7534 minor support intact, another rise is mildly in favor. Break of 0.7711 will target 0.7748 resistance and above. At this point, there is no clear sign of range breakout yet. Hence, we'd be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, break of 0.7534 will indicate near term reversal and turn bias back to the downside for 0.7370 support.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8096) and above.

Is Gold Making A Beeline For The 1180.00 Handle?

Key Points:

- The long-term trendline seems to be broken.

- A corrective ABC wave could be seen in the coming weeks.

- Losses could extend to the 1180.00 handle.

As a result of a breakout below its long-term trendline, gold has ostensibly confirmed recent fears that the metal's trajectory is going to be rather bearish moving ahead. Indeed, Monday's nearly 2% slip has cemented the bias of numerous technical readings that had been suggesting that the metal was in need of a corrective movement. However, exactly what form our corrective decline will take and how far losses will extend is up for debate and is worth taking a closer look at.

First and foremost, the sharp downturn and subsequent reversal tends to indicate that we are going to see an ABC wave over the coming weeks. As shown below, the historical reversal zone around the 1219.10 handle has struck again and looks as though it is going to remain intact – a sign that the ‘A' leg has completed. Of course, this means we are now moving into the second leg of the pattern which we expect to bring gold prices back to around the 1244.25 handle. This bias is reinforced by the fact that stochastics remain oversold and are in sore need of being relieved.

However, just because we are moving into a near-term uptrend doesn't mean we are necessarily going to see the metal make the required reversal to start the ‘C' leg of the pattern. This is where the old trend line comes back into the picture as it is likely to be a source of resistance moving forward. Importantly, this should limit upsides and force gold to retreat at that 1244.25 handle – marking the start of the final leg of the ABC wave.

Once the final leg is underway, the highly bearish EMA bias is likely to be felt once again and encourage the metal to move into a rather steep decline. Furthermore, the 100 day moving average will be providing substantial dynamic resistance as gold retreats which will limit chances of an intra-day sentiment swing disrupting the overall downtrend. Ultimately, this corrective structure should see the metal move back to around the 1180.00 mark – the lowest point in the first trough seen in during the recent uptrend.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2892; (P) 1.2953; (R1) 1.2994; More....

USD/CAD edges lower to 1.2911 as recent decline continues. Intraday bias stays on the downside. Sustained trading below 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969 will pave the way to retesting 1.2460 low. On the upside, above 1.3013 minor resistance will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 1.3164/3346 resistance zone first, before staying another fall .

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The second leg should have finished at 1.3793. Break of 1.2460 will extend such correction to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

Canadian Dollar Rises on Hawkish BoC again, Little Reaction to Korea Tensions

Dollar recovers this week but momentum isn't too strong so far. Indeed, the greenback is overwhelmed by the strength in Canadian Dollar, which follows high oil prices and hawkish BoC comments. Dollar is still holding well below near term resistance against Euro, Pound and even Aussie, and maintains bearishness. Meanwhile, Yen also tried to recover on news of geopolitical tensions in Korea but no follow through buying is seen. US markets will be back from holiday today with major focus on FOMC minutes. Sterling will look into PMI services for inspirations.

US and South Korea conducted missile drill

The US and South Korea jointly conducted a missile drill after North Korea's missile launch yesterday. Pentagon said that "together with the Republic of Korea, we conducted a combined exercise to show our precision fire capability." And the US Army said that's an exercise to counteract North Korea's "destabilizing and unlawful actions." Meanwhile, the US also confirmed that North Korea's claim that the one tested was an intercontinental ballistic missile. North Korea head Kim Jong-un said that the launch was a July 4 "gift" to the Trump administration. Forex markets' reaction to the news was rather muted. Also about US, Fed chair Janet Yellen was hospitalized over the weekend to treat a urinary tract infection while she was on holiday in London. Yellen was released on Monday and is returning to work as planned this week.

BoC Poloz reiterated hawkish comments

Bank of Canada Governor Stephen Poloz was interviewed by a German newspaper Handelsblatt. He said that while core inflation is "fair soft" recently, the central back has to look through the near term reading and anticipate the picture 18 to 24 months ahead. He said that "if we only watched inflation and reacted to inflation, we would never reach our inflation target, we'd always be two years behind in the reaction." Hence, "we have to look at the rest of our indicators in the models that predict inflation." He noted that output gap would close some time in first half of 2018 and inflation will then be well into an up trend. Thus, it's appropriate to start removing some of the monetary stimulus. Meanwhile, Poloz sounded unconcerned with recent volatility in oil price and said that the fall from around 50 to 40 was "not a big issue". Markets are pricing in over 50% chance of a 25bps rate hike by BoC to 0.75% on July 12 next week.

BoE hawks stay hawkish

There were three BoE policy makers who voted for a rate hike last month. Two of them maintained their hawkish stance as they spoke yesterday. Michael Saunders said that "households should prepare for interest rates to go higher at some point". But he noted that if rates do go up, "it will be in the context of the economy doing OK and unemployment being low and probably falling". Meanwhile, he is "reasonably confidence" that investments and exports would offset the slowdown in consumer spending. Ian McCafferty said in a newspaper interview that on the balance of monetary policy, "there is a need for change". And a rate hike would be "justified" and "the prudent thing to do at this stage".

ECB Praet called for patience

ECB chief economist and Executive Board member Peter Praet called for patience regarding stimulus exit as "inflation convergence needs more time to show through convincingly in the data". And he emphasized that "we need to be persistent, because the baseline scenario for future inflation remains crucially contingent on very easy financing conditions which, to a large extent, depend on the current accommodative monetary policy stance." Looking at the current outlook, Praet said that "measured inflation remains exceedingly volatile and metrics of underlying price pressures continue to be subdued. The entire distribution of inflation expectations still needs to shift a fair distance to the right."

ECB Governing Council member Ewald Nowotny also urged that a "steady hand" is needed for monetary policy. He said that "we again have a revival in investment, and together with the recovery of exports that's a significant reason for the clear upturn that we now see in Europe." Another Governing Council member Yves Mersch said that there will be "compositional discussion" on QE in ECB. And, the central bank will "in the not too distant future have to review the specific role of ABS in the context of the broader issue of QE beyond 2017."

In the economic calendar

UK BRC shop prices dropped -0.3% yoy in June. China Caixin PMI services dropped to 51.6 in June. UK PMI services will be the main focus in European session. Eurozone will release PMI services final and retail sales. Later in the day, US will release factory orders. But main focus will be on FOMC minutes. Markets will look into the discussions between policy makers. The key question will be whether Fed will hike again in September and start shrinking balance sheet in December. Or Fed will start cutting the balance sheet first and hike in December. Or, Fed will just do one of them this year.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2892; (P) 1.2953; (R1) 1.2994; More....

USD/CAD edges lower to 1.2911 as recent decline continues. Intraday bias stays on the downside. Sustained trading below 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969 will pave the way to retesting 1.2460 low. On the upside, above 1.3013 minor resistance will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 1.3164/3346 resistance zone first, before staying another fall .

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The second leg should have finished at 1.3793. Break of 1.2460 will extend such correction to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | -0.30% | -0.40% | ||

| 1:45 | CNY | Caixin PMI Services Jun | 51.6 | 52.9 | 52.8 | |

| 7:45 | EUR | Italy Services PMI Jun | 54.6 | 55.1 | ||

| 7:50 | EUR | France Services PMI Jun F | 55.3 | 55.3 | ||

| 7:55 | EUR | Germany Services PMI Jun F | 53.7 | 53.7 | ||

| 8:00 | EUR | Eurozone Services PMI Jun F | 54.7 | 54.7 | ||

| 8:30 | GBP | Services PMI Jun | 53.5 | 53.8 | ||

| 9:00 | EUR | Eurozone Retail Sales M/M May | 0.30% | 0.10% | ||

| 14:00 | USD | Factory Orders May | -0.50% | -0.20% | ||

| 18:00 | USD | FOMC Meeting Minutes |

Elliott Wave View: USDX Correction In Progress

Short term USDX (USD Index) Elliott Wave view suggests the rally to 97.88 high on 6/20 ended Intermediate wave (X). Decline from there is unfolding as an impulse Elliott Wave structure with extension and ended at 95.47 low on 6/29. This 5 wave move could be Minor wave A of an Elliott wave zigzag structure structure, where Minute wave ((i)) ended at 97.17 and Minute wave ((ii)) ended at 97.47. Minute wave ((iii)) ended at 96.15, Minute wave ((iv)) at 96.61 and Minute wave ((v)) of A ended at 95.47.

Minor wave B bounce is currently in progress to correct cycle from 6/20 peak. The subdivision of Minor wave B is unfolding as an Elliott wave zigzag structure. Minute wave ((a)) ended at 96.33 and near term, Minute wave ((b)) pullback is in progress to correct cycle from 6/29 low in 3, 7, or 11 swing before turning higher again. While the pullback stays above pivot at 6/29 low (95.47), USDX has scope to extend higher one more leg towards 96.66 – 96.95 area to end Minor wave ((c)) of B. Afterwards, while bounces stay below pivot at 6/20 high (97.88), expect USDX to resume lower again. We don’t like buying the proposed bounce.

USDX 1 Hour Elliott Wave Chart

Market Morning Briefing: Aussie Has Been Hurt By The RBA Maintaining Status Quo

STOCKS

Dow (21479.27, +0.61%) rose towards 21600 but came off sharply to close at lower levels. Immediate hurdle could be faced near 21600-21750 levels before targeting 22000 on the upside. Further upside could be limited just now and a sharp corrective fall is on the cards for the medium term. We need to be cautious near current levels.

Dax (12437.13, -0.31%) came off last week from important resistance near 13000 and could possibly come down to test 12000 in case it breaks below 12400. Movement looks bearish for the current week.

Shanghai (3191.94, +0.29%) continues to remain in the sideways consolidation mode as expected. Immediate resistance is seen near 3200 which seems to be holding quite well for now.

Nikkei (19928.79, -0.52%) is trading lower. There is some chance that it may test 19700 on the downside before again trying to move up towards 20250. On the weekly charts, the index is in a sideways consolidation mode within 19700-20250 levels.

Nifty (9613.30, -0.02%) tested 9650 yesterday but came down to close at 9613. While it manages to sustain above 9615-9625 levels, there could be some chances that it moves up towards 9700 in the next couple of sessions but at the same time it could also come off below 9600 just now. There is no directional clarity just now. We would like to wait and watch.

COMMODITIES

Gold (1222) is trading within the range of 1190-1230 and Silver (16.16) is within 15.80-16.50. On 27th June, we had clearly mentioned that 'If 1233 for gold and 16.45 for silver fail to hold for the current week then gradual selling for the target of 1195 and 15.93 can't be ruled as seller will take every bounce as a further opportunity for selling'. We will remain bearish on Bullion while gold and silver are trading below 1250 and 16.50 levels respectively.

No directional movement had been seen in Copper (2.68) as it is trading within the range of 266-2.78.If 2.66 holds then we might see 2.82 within few days of time. We will remain bullish on copper while it is trading above 2.55 levels.

Although Brent (49.56) and WTI (47.01) are trading near their resistances of 50 and 48.50 levels but this recent bounce hasn't affected their midterm bearishness much and we will remain bearish while Brent and WTI are trading within 54 and 51 regions respectively. We have U.S weekly crude oil inventory data tomorrow, which could be a decisive factor to determine the future course of action.

FOREX

All eyes will be on the Fed minutes from its Jun'17 policy meeting to find clues about the rate path in the coming months which may move Dollar tonight.

Neither Euro (1.1361) has declined below the support of 1.1320-1.1290 nor Dollar Index (96.13) has broken above the resistance of 96.50-65 to provide us the confirmation for the preferred scenario of continued Dollar strength in the coming days. Repeat - We expect Dollar to stage a turnaround to the upside soon but we are still waiting for confirmation. Till now, most of the majors are in a normal correction and further break of major supports are required before the downtrend can be confirmed.

Dollar Yen (112.96) is in a sideways corrective mode for the last 2 sessions but as long as the support of 112.60 holds, the chances of further upside to 114.30-115.00 remain open.

Pound (1.2938) has managed to stay above the support of 1.2880 so far, keeping the near term trend up so far and the possibilities of resuming the uptrend in the coming sessions open.

Aussie (0.7619) has been hurt by the RBA maintaining status quo and the upside momentum is gone. If the next support of 0.7580 holds, it may attempt a recovery but the bears may return at the higher levels.

Dollar Rupee (64.74) tried to rally above 64.90 but failed to sustain the upside momentum, as frequently seen in the recent days. It corrected to close below 64.80 but as long as the support of 64.60 holds, the chances of another rise to 64.90-65.00 remain open.

INTEREST RATES

The US yields have risen sharply since last week. The 5Yr (1.91%), 10Yr (2.32%) and the 30YR (2.84%) are all up from previous levels near 1.85%, 2.25% and 2.82% respectively. The 30Yr is heading towards resistance near 2.92% while the 10YR could rise to 2.4% before coming off again by the end of the week.

The German-Japan 10Yr (0.39%) is trading just below resistance levels and could come off sharply from there in the near term. this could indicate that the EUR/JPY (128.32) could also come off in the near term maybe towards 127 or even lower.

The German yields are rising and could face long term resistance above current levels. While the resistances hold, the yields could come off in the near term.