Sample Category Title

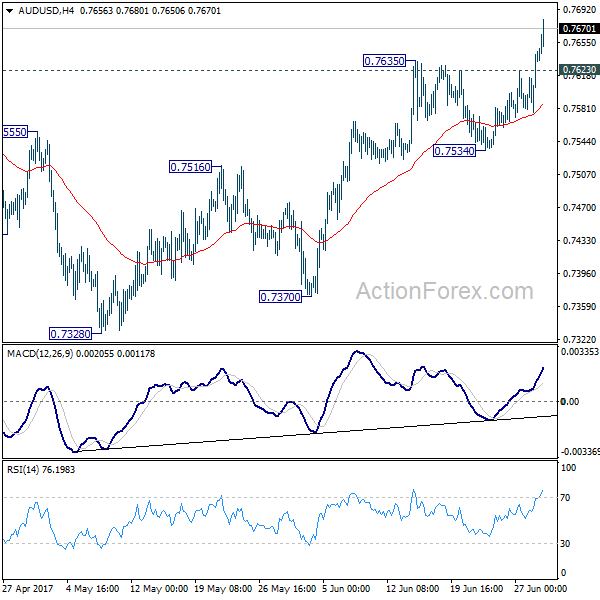

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7594; (P) 0.7619; (R1) 0.7662; More...

AUD/USD's rally finally resumed by taking out 0.7635 and reaches as high as 0.7680 so far. Intraday bias is back on the upside for 0.7748 resistance and above. At this point, there is no clear sign of medium term range breakout yet. Hence, we'd be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, below 0.7623 minor support will turn bias neutral and bring consolidations first. But near term outlook will remain bullish as long as 0.7534 support holds.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8116) and above.

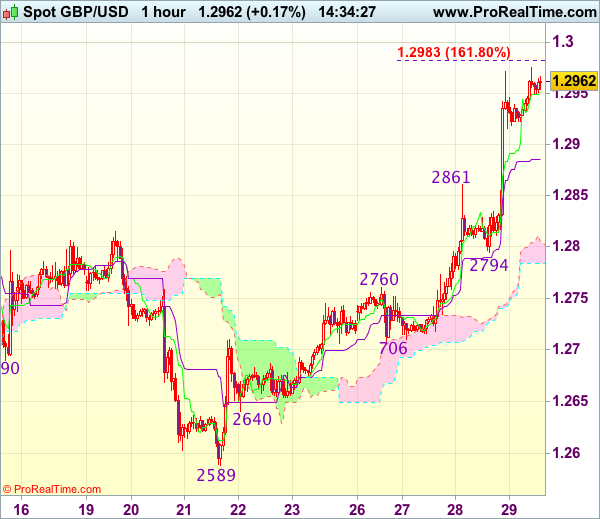

Trade Idea : GBP/USD – Buy at 1.2895

GBP/USD - 1.2977

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2964

Kijun-Sen level : 1.2895

Ichimoku cloud top : 1.2801

Ichimoku cloud bottom : 1.2784

Original strategy :

Buy at 1.2860, Target: 1.2970, Stop: 1.2825

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2895, Target: 1.2995, Stop: 1.2860

Position : -

Target : -

Stop : -

As cable has risen again after brief pullback, suggesting recent upmove is still in progress and may extend further gain to 1.3000 psychological resistance, however, loss of near term upward momentum should prevent sharp move beyond 1.3025-30 and reckon resistance at 1.3048 would hold on first testing, risk from there has increased for a retreat to take place later.

In view of this, we are looking to buy cable again on pullback as the Kijun-Sen (now at 1.2895) should limit downside. Below previous resistance at 1.2861 would defer and suggest a temporary top is formed instead, risk weakness to 1.2830-35 but support at 1.2794 should remain intact.

US Dollar Slips On Hawkish Comments From ECB And The BoE

The central banking chiefs from the European Central bank, the Bank of England and the Bank of Canada spoke yesterday. Surprising with hawkish comments, the US dollar slipped as the euro, the British pound and the Canadian dollar rose sharply.

Central bankers suggestions that reducing the stimulus program sent the respective yields falling while the currencies appreciated. The Canadian dollar also got a boost from rising oil prices following the EIA report.

BoE's Carney said that an interest rate hike was required noting that this would be discussedin the upcoming meetings. Meanwhile, the BoC Governor, Poloz said that the rate cuts in 2015 did their job and that the central bank will consider its options in terms of the excess capacity being used.

Looking ahead, the US final GDP numbers will be coming out today, but no major changes are expected, with GDP expected to remain steady at 1.2%.

EURUSD intraday analysis

EURUSD (1.1398): The EURUSD continued to the upside closing at 1.1376. The exchange rate briefly fell after rumors emerged from the ECB that Draghi's comments were misjudged. EURUSD fell to 1.1300 on the day before pulling back to close higher. In the near term, if the upside continues, EURUSD could be seen slipping back to 1.1357. This marks the resistance level high from August 2016. Establishing support here could signal further continuation. However, expect to see some weakness with the sideways range being formed at 1.1357 - 1.1300.

GBPUSD intraday analysis

GBPUSD (1.2954): The British pound rose steadily breaking past the 1.2800 resistance level. Any declines could be limited to this level which could now act as support. Price action is seen reaching towards 1.2970 minor resistance level from May this year. In the near term, GBPUSD could see a pullback that could potentially see price action test the support at 1.2800, as seen on the 4-hour chart. A breakout above 1.2976 will, however, require further upside in GBPUSD with the potential to reach out above 1.3000.

USDJPY intraday analysis

USDJPY (112.10): USDJPY managed to break past the resistance and yesterday's price action also closed above this level. However, the price action suggests that we could see some downside unless today's daily close is above the recent highs at 112.46. On the 4-hour chart, the bullish flag pattern remains in play. Following the initial target at 112.43, USDJPY will be seen testing the next main target level at 113.36.

Currencies: Euro Extends Post-Draghi Rally. Dollar Continues To Struggle

Sunrise Market Commentary

- Rates: German inflation numbers could test investors' resolve

The most interesting item on today's eco calendar are German inflation numbers. We see risks on the downside of expectations which could immediately test market's resolve in Draghi's contested comments. If the Bund isn't able to recover the neckline of the bearish double top formation (164.76), it would comfort our sell-on-upticks strategy. - Currencies: Euro extends post-Draghi rally. Dollar continues to struggle

Yesterday, EUR/USD showed sharp intraday swings, but in the end, the post-Draghi rally continued. At the same time, USD/JPY hardly profited from an intraday equity rebound. EUR/USD is setting new highs this morning. Will soft German CPI data, if they occur, be able to slow the euro rebound?

The Sunrise Headlines

- US equities rose on financial sector strength and tech rebound and closed with gains of 0.88% (S&P) and more (NASDAQ +1.43%). Positive sentiment extended into Asia trading but at a somewhat more moderate pace.

- Oil continued its six day rebound with Brent oil now at $47.5/barrel. Before talking about a sustained rise, we would like to see the Brent oil price breaking the technical $48.29/barrel level.

- For the first time since the start of the stress tests 7 years ago, US regulators are allowing all tested banks to pay out almost all their earnings to shareholders. This signals the regulators' confidence in the health of the financial system.

- UK Prime Minister May's minority administration won the first parliamentary test yesterday ahead of the final vote of her Queen's Speech later today. We expect May to win the final vote with help of the DUP party.

- The eco-calendar is quite light today with the third US GDP-reading and American jobless claims. In the EMU, EC confidence indicators will shed light on Eurozone sentiment and German CPI on inflation dynamics

Currencies: Euro Extends Post-Draghi Rally. Dollar Continues To Struggle

EUR/USD maintains post-Draghi gains

The Draghi comments from Tuesday still dominated EUR/USD trading yesterday. The pair extended its rally to the high 1.13 area early in the session. Market rumours suggesting that the ECB-president was misinterpreted caused a temporary correction. However, it was soon undone as BoE's Carney said that the BoE also considered a gradual tightening. EUR/USD closed session at 1.1378, within reach of the correction top. USD/JPY hovered mostly in the low 112 despite an intraday equity rebound.

Overnight, Asian equities go higher in the slipstream of WS. The dollar remains in the defensive. EUR/USD touched a new correction top north of 1.14. USD/JPY still doesn't profit from the broad equity rebound. The pair hovers in the 112.25 area. The Yuan continues its rebound against the dollar, trading at USD/CNY 6.78.

Today, the EC economic confidence should confirm the strong EMU recovery. German inflation is expected flat on the month and 1.3% Y/Y, down from 1.4% Y/Y in May. The June Italian inflation surprised on the downside 0.2% M/M decline). So, there are some downside risks. Even an expected outcome would confirm that inflation is cooling. Yesterday, rumours that Draghi's hawkish comments were misinterpreted, failed to stop the euro rebound. Will soft EMU inflation data be able to do the job? The final Q1 US GDP release is outdated. Initial claims stabilized at very low levels and no change is expected. Weekly 'noise probably won't change fortunes for the dollar. Fed Bullard speaks on monetary policy, but as he did so several times in recent days, no new info is expected.

Yesterday, the euro remained the 'by default' winner, despite attempts to downplay the Draghi comments. Soft Germany inflation data and ST overbought conditions might slow the euro rally. However, it is unlikely to cause a ST trend reversal. At the same time, sentiment on the USD remains fragile. The US dollar desperately needs good news (both on activity and price data) for markets to become again more confident on further Fed policy normalisation. We are neutral EUR/USD and look for a breather on the recent EUR/UJSD rally.

Yesterday's intraday price development in USD/JPY was again disappointing. Core yields more or less maintained Tuesday's increases and equities rebounded. Evens so, the pair hardly made any further headway. We remain cautious on USD/JPY longs.

Technical picture: Euro prevails. USD struggles

Early May, EUR/USD failed to break below the 1.0821/1.0778 support. Poor US data and US political upheaval propelled EUR/USD to a test of the 1.1300 area going into the FOMC decision, but the test was rejected. Earlier this week, a combination of hawkish ECB comments and negative US headlines pushed EUR/USD for an intensive test of the 1.1300/66 resistance are. The area is broken, if the break is confirmed, it would be a significant technical signal and open the way to the 1.1616/1.1714 LT correction tops. A return below 1.1220 (STMA) would be a first indication that the euro rally is easing. A drop below 1.1119 would call off the downward alert.

The USD/JPY rally ran into resistance in early May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair beyond a first minor resistance at 110.81. The pair regained the 112.13 correction top early this week, but there are no real follow-through gains , So, the break isn't confirmed yet. A break would improve the ST-picture. Even so, were remain cautious on further USD/JPY gains.

EUR/USD tends to break above the key 1.1300/66 resistance on Draghi comments

EUR/GBP

EUR/GBP: topside test rejected

Yesterday, it looked like sterling traders were heading for a calm session…. till late in the afternoon. Cable traded sideways in the lower half of 1.28. The price moves in EUR/GBP were primarily swings in the euro in the wake of Tuesday's Draghi comments. EUR/GBP traded at minor new highs in the 0.8870/80 area, but lost gradually a few ticks. Early afternoon, the pair tumbled to the low 0.88 on the rumours that Draghi was misinterpreted by markets. However, BoE's Carney changed the script again as he indicated that some tightening might be warranted if the growth/inflation trade-off lessens. Quite a big U-turn from recent comments of the BoE governor. Sterling jumped sharply higher. EUR/GBP closed the session at 0.8802. Cable rallied against a weak dollar and closed at 1.2926.

Today, the UK money supply and credit data will be published. A slightly easing is expected, but we doubt the data will change the debate on monetary policy. There will also be plenty of headliners on the vote on the program of the May minority government. However, markets will ponder the consequences from Carney's hawkish U-turn. The Carney comments will probably put a floor for the dollar short-term. However, we don't expected a protracted sterling rally anytime soon, especially not against the euro. We still look to buy EUR/GBP in case of more pronounced downticks

From a technical point of view, EUR/GBP set a minor top north of the 0.8854/66 resistance (2017 top), but a sustained break didn't occur. Yesterday's setback probably block further gains ST. A return below the 0.8655 correction low would indicate easing pressure on sterling. Such a break lower will be difficult. A EUR/GBP buy-on-dips approach remains favoured.

EUR/GBP: topside test rejected

Market Update – Asian Session: New Zealand Business Confidence Improves

Asia Mid-Session Market Update: Japan retail sales fall for the first time in 5 months; New Zealand Business Confidence improves

US Session Highlights

(US) MAY ADVANCE GOODS TRADE BALANCE: -$65.9BE V -$66.0BE

(US) MAY PRELIMINARY WHOLESALE INVENTORIES M/M: 0.3%E V 0.2%E

Pres Trump tweets: "The #AmazonWashingtonPost, sometimes referred to as the guardian of Amazon not paying internet taxes (which they should) is FAKE NEWS!"

(US) MAY PENDING HOME SALES M/M: -0.8% V +1.0%E; Y/Y: 0.5% V 0.5%E

(JP) BOJ Gov Kuroda: firms remain cautious on spending - comments in Portugal

(US) DOE CRUDE: +0.1M V -2.5ME; GASOLINE: -0.9M V -0.5ME; DISTILLATE: -0.2M V +0.5ME; total US production fell 1%

Fed did not object to the capital plans of all 34 bank holding companies participating in the Comprehensive Capital Analysis and Review (CCAR). Capital One is the only bank that will need to resubmit within six months, although its plan was not entirely rejected.

US markets on close: Dow +0.7%, S&P500 +0.9%, Nasdaq +1.4%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Utilities

Biggest gainers: SPLS +8.4%; ARNC +5.8%; TRIP +4.5%

Biggest losers: AAP -4.3%; ORLY -2.2%; FE -2.1%

At the close: VIX 10.0 (-1.0pts); Treasuries: 2-yr 1.35% (-2bps), 10-yr 2.22% (+2bps), 30-yr 2.77% (+3bps)

US movers afterhours

GEMP Announces top-line data from COBALT-1 Phase 2b clinical trial in HoFH patients ; +10.0% afterhours

PRGS Reports Q2 $0.42 v $0.37e, Rev $93.4M v $90.9Me; Guides Q3 $0.41-0.43 v $0.44e, Rev $93-96M v $97.6Me; +5.6% afterhours

COF Fed requires resubmission of its CCAR plan; Only US bank to require such; to maintain dividend at $0.40/shr (indicated yield 1.93%); to buy back $1.85B (4.5% of market cap); -1.3% afterhours

PIR Reports Q1 -$0.04 v -$0.05e, Rev $409.5M v $421Me; Guides Q2 -$0.08 to -$0.04 v -$0.03e, SSS flat to 2%, net sales growth flat y/y ; -10.8% afterhours

Politics

(BR) Brazil President Temer said to name Raquel Dodge as new top prosecutor; Temer’s residence subsequently attacked (Temer not inside) - US financial press

(US) Brendan Carr expected to be nominated to a position at the FCC by President Trump as soon as today - recode

Key economic data

(JP) JAPAN MAY RETAIL SALES M/M: -1.6% (first decline in 5 months) V -1.0%E; RETAIL TRADE Y/Y: 2.0% V 2.6%E

(JP) Japan May Loans & Discounts Corp y/y: 3.9% v 3.7% prior

(AU) AUSTRALIA MAY HIA NEW HOME SALES M/M: 1.1% (2nd straight increase and 6-month high) V 0.8% PRIOR

(AU) AUSTRALIA MAR-MAY SKILLED VACANCIES Q/Q: 1.5% V 2.1% PRIOR

(NZ) NEW ZEALAND JUNE ANZ BUSINESS CONFIDENCE: 24.8 (8-month high) V 14.9 PRIOR; ACTIVITY OUTLOOK 42.8 (3-year high) V 38.3 PRIOR

(KR) South Korea May Department Store Sales Y/Y: -1.9% v +0.5% prior; Discount Store Sales Y/Y: 1.6% v +2.3% prior

Speakers and Press

China

(CN) Former China State Administration of Foreign Exchange (SAFE) Official Guan Tao: China economy to stabilize in H2; Ease in capital outflow to result in a rise in FX reserves - press

(CN) China Vice Fin Min Zhu: Major economies should return to rate normalization

(CN) According to a large China insurance company, China regulators have signaled to insurers that they will relax restrictions on overseas investments in 2018

(CN) Moody's: China property sales are stronger in the lower tier cities

Japan

(JP) Japan 2016 tax Rev said to be lower y/y for the first time in 7 years - Kyodo

Korea

(KR) South Korea Pres Moon: Govt planning comprehensive job policy; Growth cannot become reality until peninsula has peace

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.5%, Hang Seng +0.9%, Shanghai Composite +0.3%, ASX200 +1.1%, Kospi +0.6%

Equity Futures: S&P500 +0.2%; Nasdaq +0.1%, Dax +0.1%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1375-1.1420; JPY 112.15-112.40; AUD 0.7580-0.7615; NZD 0.7260-0.7285

Aug Gold +0.3% at 1,253/oz; Aug Crude Oil +0.4% at $44.95/brl; Sept Copper +0.7% at $2.69/lb

iShares Silver Trust ETF daily holdings fall to 10,551 tonnes from 10,571 tonnes prior; first decline since June 20th

(CN) PBoC: To skip today's open market operation (OMO); 5th consecutive skip

(CN) PBOC SETS YUAN MID POINT AT 6.7940 V 6.8053 PRIOR (2-week high)

Asia equities notable movers

Australia

Prime Media (PRT) +5.8%; Raises FY17 guidance

Wesfarmers Ltd (WES) +0.4%; Said to be considering an industrial acquisition - Australian press

Vocus Group (VOC) -0.3%; KKR said to be losing interest in a takeover of Vocus - Australian

Japan

Honda (7267) +0.3%; Toyota (7203) +0.2%; Nissan (7201) +1.5%; May vehicle production

Obic Co (4684) +1.6%; may report Q1 op profit ¥7B, +15% y/y; Rev ¥15B, +10% y/y - Nikkei

Hong Kong

Tiangong International Company (826) +6.1%; Guides H1

Sparkle Roll Group (970) +3.4%; Reports FY17

Kingmaker Footwear Holdings (1170) +3.3%; Reports FY17

Ngai Shun Holdings (1246) -4.4%; Reports FY17

Suddenly, Central Bankers Turned Hawkish

Central bankers don't seem to have learnt from the former Fed Chair, Ben Bernanke, when he first mentioned the idea of tapering the amount of money being pumped into the economy in May 2013.

Back then, the news sent risk assets south, and the volatility index surged 63% in less than a month, while U.S. 10-year Treasury yields climbed 25%.

Both the ECB's Mario Draghi and the BoE's Mark Carney have now sent a message to investors from Sintra, Portugal, that the era of cheap money is close to an end. This time, the reaction was mainly felt in fixed income and currency markets.

Draghi's comments were intended to signal more confidence in the economic recovery and not an immediate call to withdraw stimulus; however, bonds were sold heavily, and the Euro marched above 1.14, a new 52-week high. Similarly, Carney's remarks sent the Pound to 1.2972, recovering all losses that stemmed from Theresa May's failure to win a majority vote in the recent snap elections, as he indicated the possibility of raising rates. I think going forward, central bankers will be more careful and cautious when passing on similar messages. In other words, they should be uninteresting not to disrupt financial markets.

Although I'm bullish on the Euro on the longer run, I think the market's reaction is a bit too exaggerated. I would rather wait for hard data to confirm the hawkish stance, especially on inflation, since the recent slide in oil prices may mean that inflation stays low for a prolonged period. If the Eurozone's headline and core CPI disappoints on Friday, there's a high chance that traders will book some profits.

Financial stocks are the biggest beneficiaries from the surging yields and the Fed's upbeat assessment on the U.S. banking sector. The biggest U.S. banks are now able to boost share buybacks and dividend payouts by almost 50% compared to 2016. This would likely lead to the continued rotation from bond proxies such as utilities to financials.

In commodity markets, gold recovered most of Monday's losses to trade above $1,250 as the U.S. currency continued to weaken against its major counterparts. Meanwhile, crude prices were higher on both sides of the Atlantic, despite U.S. inventories unexpectedly rising by 118,000 barrels last week. The supporting piece of news from EIA was the 100,000 barrel decline in production last week, but it's too early to jump to conclusions at this stage since this is likely to reverse in the weeks ahead.

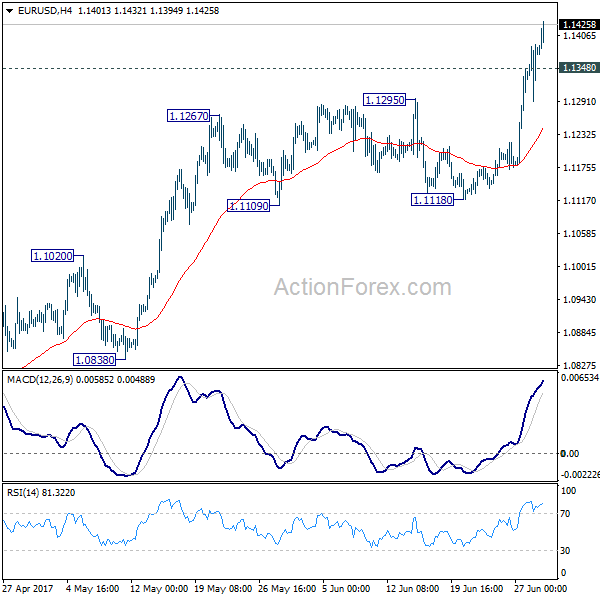

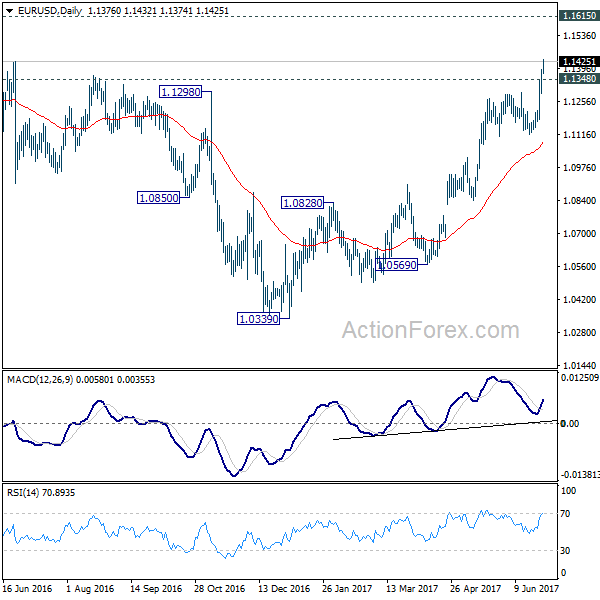

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1315; (P) 1.1352 (R1) 1.1414; More....

EUR/USD's rally resumed after brief retreat and reaches as high as 1.1432 so far. Intraday bias is back on the upside. Current rally from 1.0339 should target 1.1615 medium term resistance next. On the downside, below 1.1348 minor support will turn intraday bias neutral and bring retreat. But downside should be contained above 1.1118 support and bring rise resumption.

In the bigger picture, the break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition is seen in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

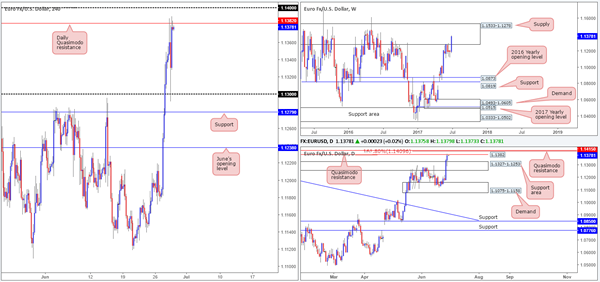

EUR/USD

In recent trading, the single currency gravitated north and found resistance around the daily Quasimodo formation pegged at 1.1382. This was a noted level to look for shorts due to this barrier being positioned within the walls of a weekly supply at 1.1533-1.1278. In addition to this, we liked the fact that the Quasimodo was (and still is) located just below a daily AB=CD 161.8% ext. at 1.1409 and the psychological band 1.14. Well done to any of our readers who managed to pin down a short from here. The move from 1.1382 provided at least 80 pips of profit and considering the stop-loss order should have been positioned at 1.1415 (33 pips), this would have been a worthwhile trade.

Moving forward, we can see that the unit is now back within striking distance of the aforementioned daily Quasimodo resistance. Selling from here again, of course, is a possibility, but not something we would advise. The main reason being is that the daily support area at 1.1327-1.1253 was tested yesterday and the sell orders from 1.1382 may be weak.

Our suggestions: The next area of interest for the desk is the daily Quasimodo resistance seen planted a little higher on the curve at 1.1415. Again, we know that this level is fresh, is positioned just above the daily AB=CD 161.8% ext. at 1.1409 and the psychological band 1.14, as well as still being located within the current weekly supply. To that end, we feel a bounce, at the very least, will be seen from 1.1415. Stops can be placed above the Quasimodo pattern’s apex at around 1.1430, and the first take-profit target will be the 1.1382 region: the previous daily Quasimodo pattern.

Data points to consider: German Prelim CPI. US Final GDP q/q figures, as well as the US weekly unemployment claims at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.1415 (stop loss: 1.1430).

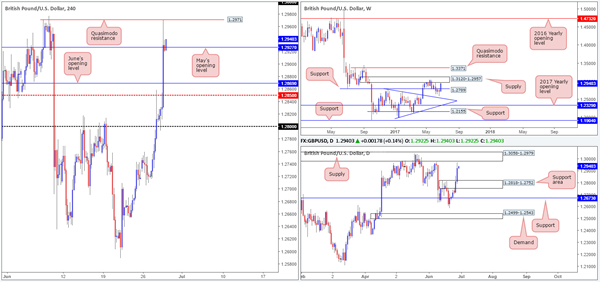

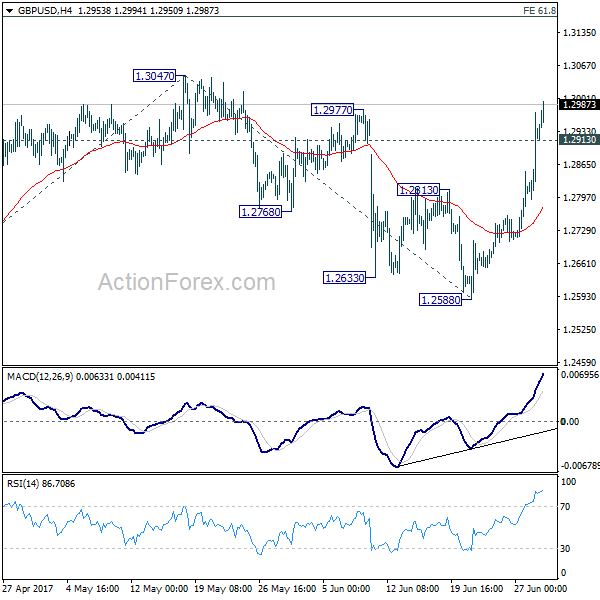

GBP/USD

In response to Mark Carney’s comments regarding monetary stimulus, the GBP/USD aggressively rose north. The H4 mid-level resistance at 1.2850 and June’s opening level at 1.2869 were consumed, which, as you can see, left price free to violently whipsaw through May’s opening level at 1.2927.

With H4 bulls looking strong just a few pips above May’s opening level right now, is this a good time to be thinking about buying this market? Let’s take a peek at what the higher timeframes are up to…

Weekly price recently shook hands with supply formed at 1.3120-1.2957. This area has already proven that it has some grit given that it held the unit lower in May. By the same token, daily action came within a cat’s whisker of clipping the underside of supply seen at 1.3058-1.2979. Considering that this area is positioned within the walls of the aforementioned weekly zone, this area is just as significant, in our opinion.

Our suggestions: Entering long therefore, despite H4 bulls demonstrating strength at the moment, is not something we would recommend. Instead, what we’re looking for is H4 price to retest the Quasimodo resistance at 1.2971 and hold firm. Should the reaction manage to produce a bearish candle, preferably a full-bodied candle, our team would consider selling, with an overall take-profit target being set around the top edge of the daily support area at 1.2818.

Data points to consider: US Final GDP q/q figures, as well as the US weekly unemployment claims at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.2971 region ([waiting for a reasonably sized H4 bear candle to form – preferably a full-bodied candle – following the retest is advised] stop loss: ideally beyond the candle’s wick).

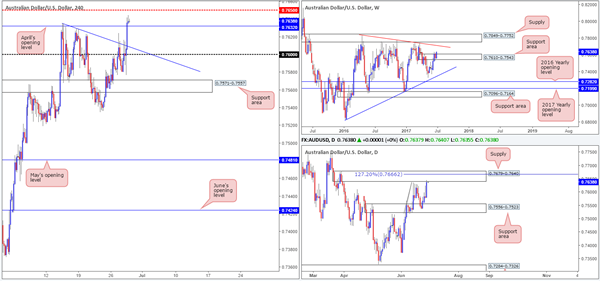

AUD/USD

Beginning from the top this morning, the weekly chart shows supply at 0.7610-0.7543, at least in our view, is now well and truly consumed. The next area of interest on this scale can be seen around the trendline resistance extended from the high 0.7835.

Despite the somewhat bullish tone being seen on the weekly chart at the moment, daily price is currently teasing the underside of a supply area coming in at 0.7679-0.7640. This area also happens to hold an AB=CD 127.2% ext. at 0.7666.

Looking over to the H4 chart, we can see that price is now hovering above April’s opening level coming in at 0.7632, and also just ahead of the H4 mid-level resistance barrier drawn from 0.7650. A few pips above this level is a H4 Quasimodo formation (not seen on the chart) seen at 0.7676.

Our suggestions: Buying this market, despite what the weekly timeframe is telling us, is not something we’d label as high probability right now given the current daily supply and nearby aforementioned H4 structures. Along similar lines, selling would also be a tad risky with the weekly support area seen in play at the moment. However, we do feel that should price connect with the H4 Quasimodo level at 0.7676, given that it is positioned within daily supply and nearby the daily 127.2% level, a bounce from here is highly likely. Ultimately though, you will want to get in here with a relatively tight stop here seeing as 0.7650 could halt selling and promote buying.

For us personally, we’re going to remain flat for now and watch how price action behaves during today’s segment before making any further judgment.

Data points to consider: US Final GDP q/q figures, as well as the US weekly unemployment claims at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Possible bounce from 0.7676.

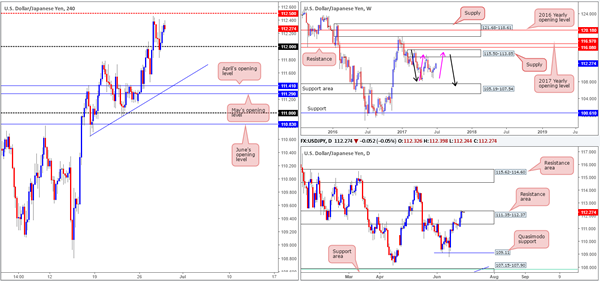

USD/JPY

Daily buyers remain keen in this market, despite price trading within the upper edge of a daily resistance area pegged at 111.35-112.37. In addition to this, weekly price shows room to advance up to supply pegged at 115.50-113.85, in the shape of a weekly AB=CD correction (see pink arrows).

However, buying right now, when H4 price is seen loitering beneath a mid-level resistance barrier at 112.50, is not something we would encourage. A break above 112.50, nevertheless, could inspire buyers to enter the market and bring price up to the 113 handle, and possibly the H4 resistance seen at 113.64.

Our suggestions: To prove buyer intent, a H4 close above 112.50 is needed. This – coupled with a retest and a lower-timeframe confirming signal (see the top of this report) would, in our book of technical setups, be enough to validate a long, targeting 113 as an initial take-profit zone.

Data points to consider: US Final GDP q/q figures, as well as the US weekly unemployment claims at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for H4 price to engulf 112.50 and then look to trade any retest seen thereafter ([waiting for a lower-timeframe buy signal to form following the retest is advised] stop loss: dependent on where one confirms this level).

- Sells: Flat (stop loss: N/A).

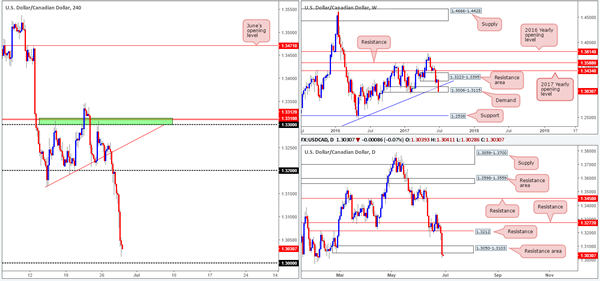

USD/CAD

For those who read Wednesday’s report you may recall our desk mentioning that a short position was taken from 1.3171, with a stop positioned at 1.3205. As you can see, the trade worked out beautifully and exceeded our expectations, given we took profit around the top edge of the weekly demand at 1.3115. Our reasoning behind this call was due to the space seen for price to move lower on the bigger picture, and also the fact that H4 price retested the underside of 1.32 and printed a reasonably sized full-bodied bearish candle.

Going forward, the pair is now seen within shouting distance of a large psychological band at 1.30. This level has held price higher on several occasions, with the most recent being seen in late January. While we agree that this level does hold promise, the bigger picture shows a nearby resistance area at 1.3050-1.3103.

Also of particular interest is that 1.30 is positioned just beneath weekly demand at 1.3006-1.3115. Therefore, stops from below this weekly zone could provide enough liquidity for the big boys to buy from 1.30 today.

Our suggestions: Personally, we really like 1.30 as a potential buy zone, if not only for the fact that it has held so beautifully in the past. However, that does not mean we would consider placing a pending buy order here! Waiting for the H4 candles to react and show buyer intent is, we believe, the safer route to take before pulling the trigger.

Data points to consider: US Final GDP q/q figures, as well as the US weekly unemployment claims at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: 1.30 region ([waiting for a reasonably sized H4 bull candle to form – preferably a full-bodied candle – following the retest is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (Stop loss: N/A).

USD/CHF

The picture being painted on the USD/CHF is an interesting one. Weekly price is, as we write, challenging the support level pegged at 0.9581. Down on the daily timeframe, we can see that yesterday’s candle retested the underside of a weekly resistance at 0.9639 and formed a rather conspicuous selling wick. The next downside target on this scale does not come into view until we reach 0.9546.

Swinging over to the H4 timeframe, the bulls are struggling to register any noteworthy movement around the 0.96 handle. Just as a reminder, below this number there is the weekly support level at 0.9581 and 35 pips below that is daily support at 0.9546.

Our suggestions: With stop-loss orders below 0.96 currently being filled, along with breakout sellers’ orders (this will likely provide liquidity for the big boys to buy); we believe a long trade from between 0.9546/0.9581 is high probability today. To be on the safe side though, we would only consider a buy from here in the event that a H4 bullish rotation candle takes shape in the form of a full or near-full-bodied candle. This will, for us, confirm buyer intent.

Data points to consider: US Final GDP q/q figures, as well as the US weekly unemployment claims at 1.30pm GMT+1

Levels to watch/live orders:

- Buys: 0.9546/0.9581 ([waiting for a reasonably sized H4 bull candle to form – preferably a full-bodied candle – following the retest is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

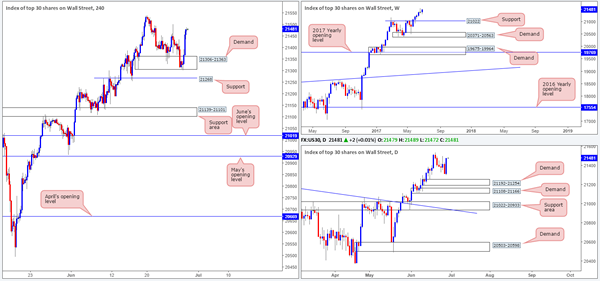

DOW 30

Unexpectedly, the H4 demand base coming in at 21306-21363 has held ground and rallied price, consequently painting a nice-looking daily bullish engulfing candle. For those who follow our analysis on a regular basis, you may recall that our desk is currently long from 21164. 50% of that position was quickly liquidated at 21234, with the remaining 50% left in the market to run since we intend on trailing this trend long term. The trailing stop was (and still is) positioned just beneath the said H4 demand zone at 21298, and thankfully was not triggered during yesterday’s trading.

Our suggestions: At the time of writing, there is not much else to hang our hat on. Of course, we would like to see the index continue advancing north and eventually register a fresh record high. From that point, we then have the freedom to move the trailing stop into further profits.

Data points to consider: US Final GDP q/q figures, as well as the US weekly unemployment claims at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: 21164 ([live] stop loss: 21298).

- Sells: Flat (stop loss: N/A).

GOLD

The H4 candles, as you can see, remain afloat above April’s opening level at 1248.0. As mentioned in Wednesday’s report, continual buying from here could see price connect with the green H4 area which we deem to be a sell zone. The reasons as to why are as follows:

H4 resistance at 1259.1.

Two H4 trendline resistances taken from lows of 1245.9/1252.9.

H4 50.0% retracement value at 1258.1 taken from the high 1281.1.

Located within the upper limits of a daily resistance area at 1247.7-1258.8.

Our suggestions: We believe that H4 price will likely test the above noted green H4 sell zone today. However, with little weekly connection seen around this area, there’s a chance that a fakeout could take shape. For that reason, we will only consider a sell from here valid if, and only if, a H4 bearish candle forms, preferably a full-bodied candle.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1259.1 region ([waiting for a reasonably sized H4 bear candle – preferably a full-bodied candle – to form before pulling the trigger is advised] stop loss: ideally beyond the candle’s wick).

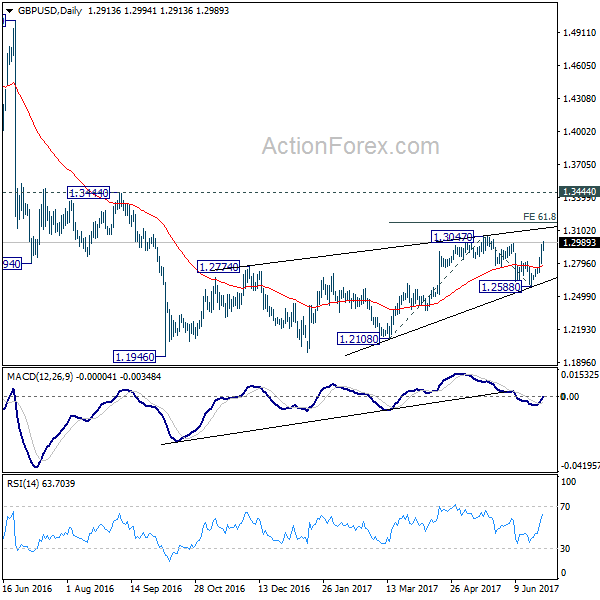

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2821; (P) 1.2896; (R1) 1.2998; More...

GBP/USD's rally continues to as high as 1.2994 so far and broke 1.2977 resistance. Intraday bias remains on the upside. Break of 1.3047 will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. On the downside, below 1.2913 minor support will turn bias neutral and bring retreat, before staging rally resumption.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. Pull back from 1.3047 has completed after failing to sustain below 1.2614 resistance turned support. It argues that the corrective pattern from 1.1946 is still in progress for another high above 1.3047. But still, outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes.

European Open Briefing: The US Dollar Weakened

Global Markets:

- Asian stock markets: Nikkei up 0.55 %, Shanghai Composite gained 0.20 %, Hang Seng rose 0.75 %, ASX 200 rallied 0.80 %

- Commodities: Gold at $1253 (+0.30 %), Silver at $16.83 (+0.60 %), WTI Oil at $44.95 (+0.50 %), Brent Oil at $47.70 (+0.35 %)

- Rates: US 10-year yield at 2.23, UK 10-year yield at 1.16, German 10-year yield at 0.37

News & Data

- Japan Retail Sales 2.0 % vs 2.6 % expected

- Australia HIA New Home Sales 1.1 % vs 0.8 % previous

- New Zealand ANZ Business Confidence 24.8 vs 14.9 previous

- New Zealand NBNZ Activity 42.8 % vs 38.3 % previous

- Dollar upended by rates reversal, stocks unfazed for now

Markets Update:

The US Dollar weakened across the board following hawkish comments from ECB President Draghi, Bank of England Governor Carney and Bank of Canada Governor Poloz. All of them were speaking at a panel organized by the ECB.

Draghi showed some caution, but noted that deflationary forces had been replaced by reflationary ones. EUR/USD declined sharply after ECB sources said that Draghi has been misinterpreted. However, the pair quickly recovered those losses and eventually broke above 1.14. In the short-term, EUR/USD looks a tad overbought, but the outlook remains positive.

BoE Governor Carney surprised markets with his hawkish comments, especially since he said last week that he doesn’t see the central bank hiking rates in the near-term. GBP/USD rallied to almost 1.2980. Heavy resistance is seen ahead of 1.30. Should the pair break above that level, a test of 1.31 is likely.

The Bank of Canada has also started to signal that a change in monetary policy might occur soon. USD/CAD has already been under a lot of pressure in the past weeks, and the recent optimistic comments increased that even more. The pair reached 1.3020 in Asia, and test of 1.30 support seems almost certain. Sub-1.30, support lies at 1.2960 and then at 1.2820.

Today, the main events will be German inflation data and US GDP numbers.

Upcoming Events:

- 10:00 BST – Euro Zone Consumer Confidence

- 13:00 BST – German CPI

- 13:30 BST – US GDP

- 13:30 BST – US Initial Jobless Claims

- 23:45 BST – New Zealand Building Consents