Sample Category Title

The Loonie’s Long-Term Uptrend Is Now In Jeopardy

Key Points:

- An Elliot wave is becoming apparent in the wake of the recent rout.

- The breaking of the long-term trend line signals further losses are now likely.

- A near-term recovery is still expected

The USDCAD has been in free fall over the past few weeks in a move reminiscent of last year's remarkable downtrend. Indeed, selling pressure has now broken through even the long-term trend line that formed as the pair sought to recover from last year's collapse – a sign that downsides may have only just begun. However, before making a beeline for what could be a 10 month low, we may see a bit of buying pressure as a result of the overarching chart pattern.

Specifically, it is fast becoming clear that we may have an Elliot wave on our hands and that the most recent plunge lower represents the end of leg number 3. As a result, we would typically expect buying pressure to return shortly and a modest recovery to be seen. In this instance, such a move is made all the more likely by the sheer degree to which the pair has become oversold – as signalled by both the RSI and Stochastic oscillators – and the presence of a well-tested historical support level at 1.3011.

Nevertheless, this near-term bullish phase is likely to be short-lived and terminate at around the 1.3203 handle as the long-term bias remains highly bearish. More precisely, we forecast that the pair will move towards, and then rebound from, the old ascending trend line – due in no small part to numerous bearish technical indicators. In particular, the EMA bias and the Parabolic SAR readings are likely to be bearish even after the recovery. Moreover, the ADX will still be in strong trend territory if the upswing occurs in the forecasted time which could see added headwinds for the pair.

As for where we can expect the USDCAD to plunge to, the 1.2828 mark looks like our next notable level of historic support. Indeed, this price has seen a number of reversals occur when it has been challenged – both immediately prior to, and in the wake of, last year's massive upswing and subsequent downtrend. Furthermore, losses past this point will undermine the validity of the overall Elliot wave as it would make leg 5 longer than leg 3 which is typically a no-go.

Ultimately, we can't ignore the impact of the fundamental side of things but, luckily, the fundamental bias is somewhat in favour of further downsides. This is largely due to the prevailing view that the USD's ‘Trump Bump' is all but doomed, a view that has been driven home this week by further failures in the GOP's attempts at reforming healthcare. Nonetheless, watch out for any upsets that may come down the line – especially US rate hikes which could result in some volatility during the final leg of the Elliot wave

Is Crude Oil About To Mount A Reversal…In The Short Term?

Key Points:

- Short term technical time frame may be turning bullish.

- Fundamental over supply remains and is likely to impact medium term view.

- Watch for a short term break towards the $47.00 - $48.00 handle.

The past few weeks have proved relatively negative for crude oil as the commodity has continued to sink lower in the face of surprise inventory builds and ongoing concern about the current direction of prices. Subsequently, you might be forgiven for being tempted to take a short term bearish view on the commodity but we might just be setting up to see a sharply bullish move in the coming weeks.

Historically, crude oil prices are currently plumbing the depths of decline with WTI down around 12% so far for the month of June. In fact, we are literally looking at the longest string of declines since around 2015. However, there are some significant technical factors which now suggest that we could be about to see some significant upside moves in the coming weeks.

From the fundamental perspective, we are about to head into hurricane season in the Gulf of Mexico. Subsequently, the risk of rig disruption, due to incoming storms, is a relatively real prospect and this would impact production in the Gulf region. The typical storm season is normally between August- November but the first major hurricane of the year has already made landfall and impacted production.

In addition, the question of OPEC’s effectiveness remains a key concern within the global oil markets and there is some question as to the cartels ability to further restrict enough supply to impact prices by any measurable amount without damaging their respective member’s economies. This is an especially valid question given that U.S. shale oil producers continue to advance production whilst lowering their respective costs. Subsequently, it remains uncertain if OPEC can have much in the way of an impact on U.S. crude inventories.

However, the latest suggestion is that Saudi Arabia could indeed change the flow of exports away from the U.S. and artificially impact inventory figures. Unfortunately, this ignores the basic premise of the economics of Shale oil. Any measurable rally back towards the $50.00 handle is only going to bring with it increased domestic rig counts and additional production. Any such strategy would simply release further market share to the shale sector.

From the technical perspective, bullish pressure is starting to mount as price action appears to have failed on any meaningful decline below the rising trend line. In addition, the RSI Oscillator is now rising sharply away from oversold territory and price action is now rising, albeit on a short term basis. Subsequently, from the technical perspective, there are plenty of reasons to expect a big move higher in crude oil prices in the coming week.

Ultimately, the technical indicators are likely to win out in the short term and we are, subsequently, likely to see some resurgence in oil prices back towards the $48.00 handle. However, our bias changes over the medium term given the various fundamentals that are at play. In particular, the ongoing over supply issues are likely not going away any time soon so expect there to be plenty of further pain before rebalancing within the market is finally complete.

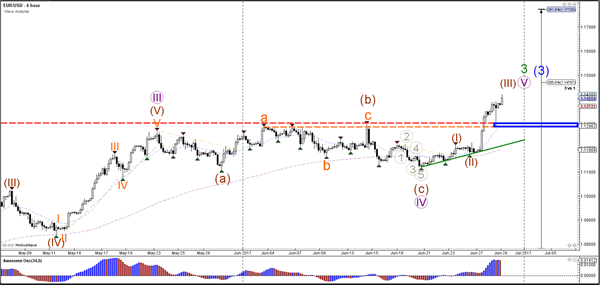

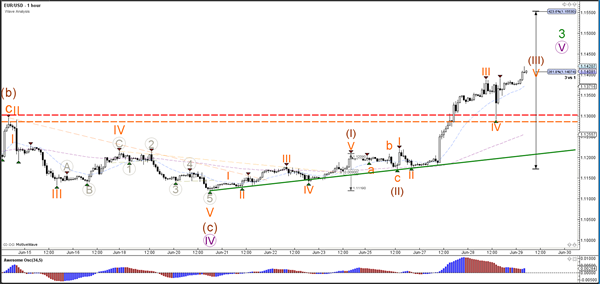

Daily Technical Analysis: EUR/USD Break, Pullback And Continuation Pattern Will Soon Test 1.15 Resistance

Currency pair EUR/USD

The EUR/USD used the key resistance at 1.13 (dotted lines) again but this time as a support level (blue box). As mentioned yesterday, the bullish continuation does not come as a surprise considering the potential wave 3s. Price is now above 1.14 and could be testing the 1.15 resistance soon which is the 200% Fibonacci level of wave 3

The EUR/USD indeed completed a light retracement for a wave 4 (orange) of a larger wave 3 (brown). Price is now moving towards the Fib targets of wave 3 vs 1.

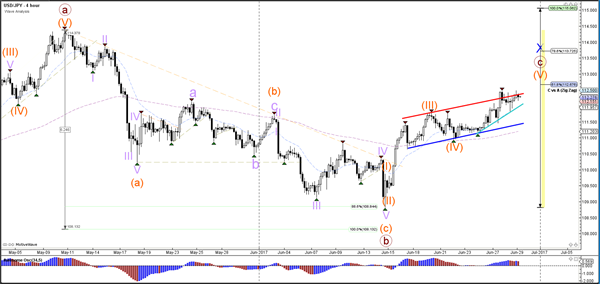

Currency pair USD/JPY

The USD/JPY is moving higher within a wave 5 (orange) of wave C (brown). A break above the top of the channel (red) could see price move towards the Fibonacci targets of wave C (brown).

The USD/JPY needs to break above the resistance trend line (red) before a bullish continuation is likely within wave 3 (grey). A break below support could indicate that the waves 5 (orange/purple) are completed.

Currency pair GBP/USD

The GBP/USD bullish breakout above the resistance trend line (dotted red) makes a bullish wave structure more likely than a bearish variant. The wave count is therefore showing a wave 3 (orange), which could either extend above the 261.8% Fibonacci target or retrace for a wave 4.

The GBP/USD will build a wave 4 and 5 (orange) once price completes the final wave 5 (grey) within wave 3 (orange).

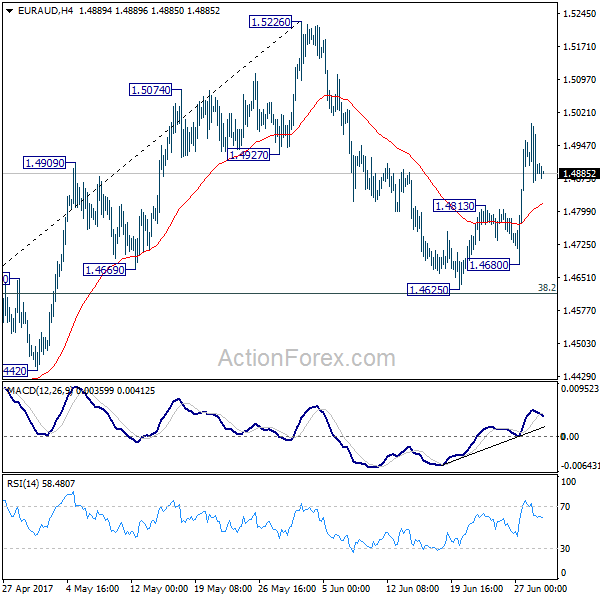

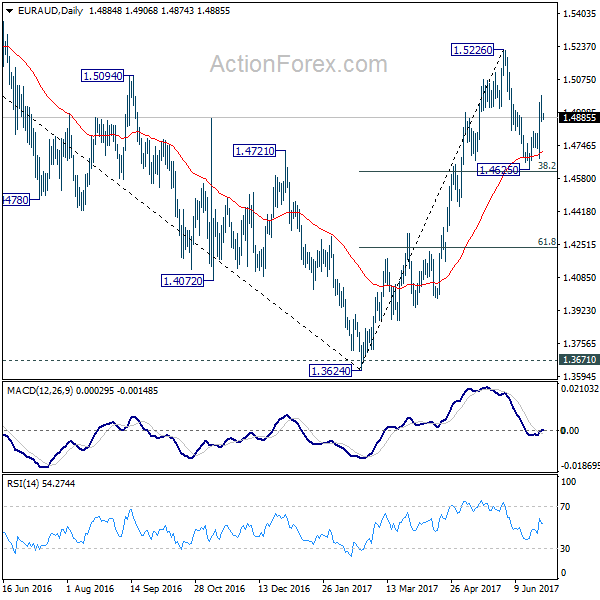

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4839; (P) 1.4918; (R1) 1.4971; More...

EUR/AUD lost some upside momentum a after hitting 1.4997. But intraday bias stays on the upside with 1.4813 minor support intact. As noted before, pull back from 1.5226 should have completed at 1.4625, ahead of 38.2% retracement of 1.3624 to 1.5226 at 1.4614. Further rally should be seen to retest 1.5226 next. On the downside, though, below 1.4813 resistance turned support will turn bias to the downside for 1.4625 again.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 would extend to 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. However, sustained break of 1.4669 support will dampen this bullish view. We'll assess the outlook later after looking at the structure and depth of the pull back.

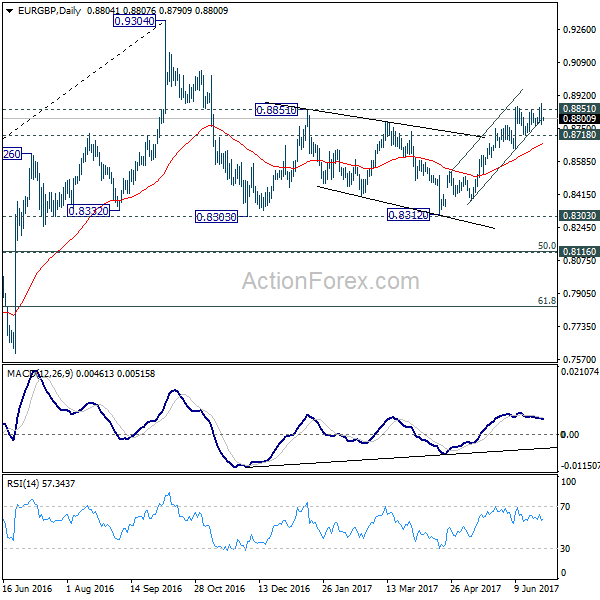

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8754; (P) 0.8817; (R1) 0.8862; More...

Intraday bias in EUR/GBP remains neutral for the moment as it's failing to take out 0.8851 resistance decisively. Yet, there is no confirmation of reversal yet. On the upside, break of 0.8879 and sustained trading above 0.8851 will pave the way to retest 0.9304 high. However, break of 0.8718 support will now indicate near term reversal and turn bias back to the downside for 0.8639 support and below.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after testing 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

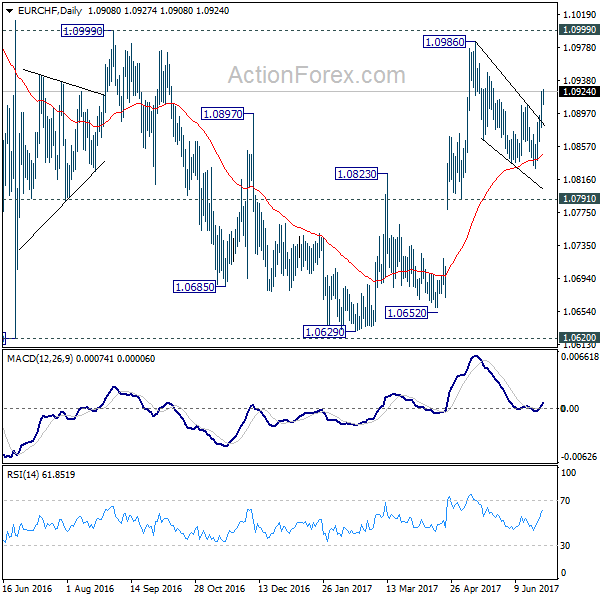

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0890; (P) 1.0908; (R1) 1.0934; More...

EUR/CHF's rebound from 1.0830 extended. The break of 1.0908 resistance suggests that the corrective pull back from 1.0986 has finally completed at 1.0830. Intraday bias is back on the upside for retesting 1.0986/0999 resistance zone first. On the downside, below 1.0880 minor support will dampen the bullish view again and turn bias neutral. In case of another fall, we'd still expect downside to be contained by 1.0791/0872 support zone to bring rebound.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

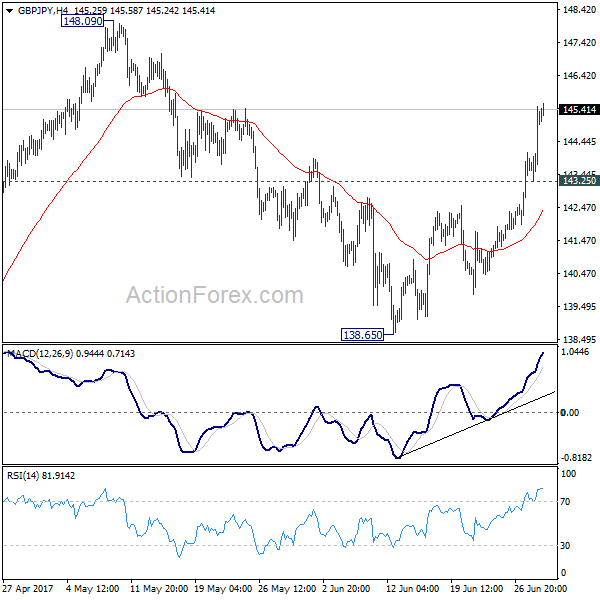

GBP/JPY Daily Outlook

Daily Pivots: (S1) 143.77; (P) 144.64; (R1) 146.03; More....

GBP/JPY reaches as high as 145.58 so far as rise from 138.65 extends. Intraday bias remains on the upside for 148.09/42 resistance zone. Decisive break there will resume whole rebound from 122.36 for key fibonacci level at 150.43. On the downside, below 143.256 minor support will turn bias neutral and bring retreat before staging another rally.

In the bigger picture, price actions from 148.42 are viewed as a consolidative pattern. And medium term rally from 122.36 is expected to resume later. Decisive break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case of another fall, we'd bee looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

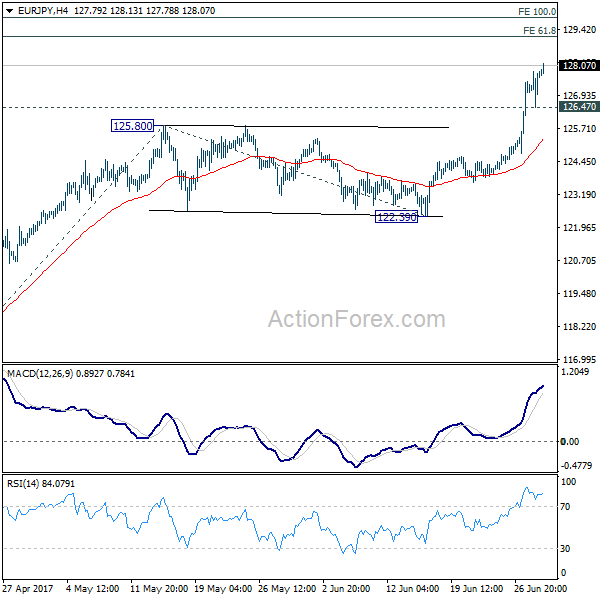

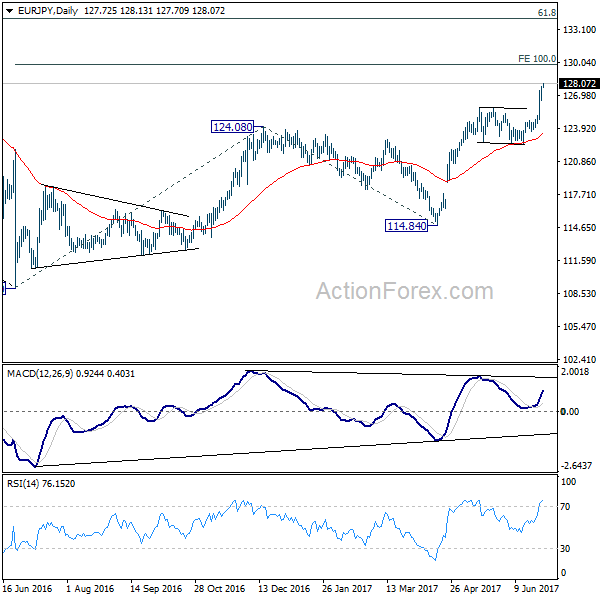

EUR/JPY Daily Outlook

Daily Pivots: (S1) 126.88; (P) 127.37; (R1) 128.27; More...

EUR/JPY's rally resumed after brief retreat and hits as high as 128.13 so far. Intraday bias is back on the upside. Current rise from 114.84 is expected to target 61.8% projection of 114.84 to 125.80 from 122.39 at 129.16 first next. That's also close to medium term projection level at 129.89. On the downside, below 126.47 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 should target 100% projection of 109.03 to 124.08 from 114.84 at 129.89 first. Break there will pave the way to 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will now remain bullish as long as 122.39 support holds.

British Pound and Canadian Dollar Soar on Rate Hike Expectations, Euro Rally Resumes after Jitters

Sterling and Canadian Dollar jumped sharply overnight as comments from BoE Governor Mark Carney and BoC Governor Poloz hinted at rate hikes ahead. Canadian Dollar is additional supported by the rebound in oil price, which sees WTI breaching 45 handle. Euro suffered some jitters on report that markets misjudged ECB President Mario Draghi's hawkish comments. But traders quickly turned to the bigger picture that ECB is, nonetheless, in a transition phase into stimulus removal. Euro remains the strongest major currency for the week, followed by Sterling and Canadian Dollar. On the other hand, the Japanese Yen is trading as the weakest as BoJ is expected to maintain stimulus. Dollar follows as markets are in doubt whether Fed will hike again in September.

BoE Carney: To debate rate hike in the coming months

BoE Governor Mark Carney said that "some removal of monetary stimulus is likely to become necessary if the trade-off facing the MPC continues to lessen and the policy decision accordingly becomes more conventional". And, as "spare capacity erodes", the "tolerance for above-target inflation falls". Carney said that the MPC will debate some of the issues "in the coming months". That's sharp turn from his own comments that "now it's not the time yet" for rate hike last week. And Carney is now more in-line with chief economist Andy Haldane that who noted that it would be "prudent" to begin removing accommodations "into the second half of the year".

Markets pricing in July hike after BoC Poloz comments

BoC Governor Stephen Poloz said that the rate cuts back in 2015 "have done their job" to counter the impact of falling oil price on the economy. And, the central bank is "approaching a new interest rate decision". He noted that for the decision "we need to be at least considering that whole situation now that the excess capacity is being used up steadily." He pointed out that regarding recovery momentum "the US obviously was way out in front. Canada some distance, perhaps as much as two years behind, given the oil shock. And then a little bit behind of course Europe." Markets took Poloz's comments as a signal that a rate hike in July 12 meeting is something that policymakers will consider. And, financial markets are pricing in over 50% chance for that.

Misjudged or not, ECB still on course to stimulus removal

Euro's rally started early this week on ECB President Mario Draghi's comment that "the threat of deflation is gone and reflationary forces are at play". There were then report yesterday saying that markets have misjudged. And, Draghi merely wanted to strike a balance between recognizing Eurozone's strength while maintaining that policy accommodation is still needed. But after all, the messages were still the same as what we pointed out before. Firstly, Draghi isn't concerned with the slowdown in inflation and judged that as "on the whole temporary". He is also optimistic on the outlook that "all the signs now point to a strengthening and broadening recovery in the euro area". So ECB is still on course to scale back monetary stimulus ahead. And September is still the time to debate and decide what to do after the current EUR 60b asset purchase program ends in December.

Markets doubtful on September Fed hike

On the other hand, news for US haven't been positive this week. In particular, markets are getting more impatient and doubtful on US President Donald Trump's ability to push through his economic agenda. Senate's delay of the healthcare vote was another sign of loss of political influence. IMF lowered US growth forecast after removing the "assumed fiscal stimulus" is another sign that analysts are giving up. Fed fund futures are pricing in less than 20% chance of a rate hike in September. It will now very much depend on the Q2 data to come out in July.

On the data front

Japan retail sales rose 2.0% yoy in May. New Zealand ANZ business confidence rose to 24.8 in June. Germany will release Gfk consumer confidence and CPI in European session. Eurozone confidence indicators will also be featured. UK will release mortgage approvals. From US, Q1 GDP final will be released with jobless claims.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 126.88; (P) 127.37; (R1) 128.27; More...

EUR/JPY's rally resumed after brief retreat and hits as high as 128.13 so far. Intraday bias is back on the upside. Current rise from 114.84 is expected to target 61.8% projection of 114.84 to 125.80 from 122.39 at 129.16 first next. That's also close to medium term projection level at 129.89. On the downside, below 126.47 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 should target 100% projection of 109.03 to 124.08 from 114.84 at 129.89 first. Break there will pave the way to 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will now remain bullish as long as 122.39 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y May | 2.00% | 2.80% | 3.20% | |

| 1:00 | NZD | ANZ Business Confidence Jun | 24.8 | 14.9 | ||

| 6:00 | EUR | German GfK Consumer Confidence Jul | 10.4 | 10.4 | ||

| 8:30 | GBP | Mortgage Approvals May | 64K | 65K | ||

| 9:00 | EUR | Eurozone Business Climate Indicator Jun | 0.93 | 0.9 | ||

| 9:00 | EUR | Eurozone Economic Confidence Jun | 109.5 | 109.2 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Jun | 2.8 | 2.8 | ||

| 9:00 | EUR | Eurozone Services Confidence Jun | 12.8 | 13 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Jun F | -1.3 | -1.3 | ||

| 12:00 | EUR | German CPI M/M Jun P | 0.00% | -0.20% | ||

| 12:00 | EUR | German CPI Y/Y Jun P | 1.40% | 1.50% | ||

| 12:30 | USD | GDP (Annualized) Q1 T | 1.20% | 1.20% | ||

| 12:30 | USD | GDP Price Index Q1 T | 2.20% | 2.20% | ||

| 12:30 | USD | Initial Jobless Claims (JUN 24) | 240K | 241K | ||

| 14:30 | USD | Natural Gas Storage | 61B |

Elliott Wave View: EURJPY Update 6.29.2017

Short term EURJPY Elliott Wave view suggests the decline to 122.35 on 6/15 low ended Intermediate wave (X). Rally from there is unfolding as an impulse Elliott Wave structure with extension where Minute wave ((i)) ended at 124.46 and Minute wave ((ii)) ended at 123.62. Minute wave ((iii)) ended at 127.84 and Minute wave ((iv)) at 126.46. Up from there pair has broken above the wave ((iii)) peak suggesting the next leg higher in Minute wave ((v)) has started already and after a short term pullback in Minutte wave (ii) pair should see more upside. We don’t like selling the pair.

EURJPY 1 Hour Elliott Wave Chart