Sample Category Title

Trade Idea Wrap-up: GBP/USD – Target met and buy at 1.2860

GBP/USD - 1.2926

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2883

Kijun-Sen level : 1.2865

Ichimoku cloud top : 1.2747

Ichimoku cloud bottom : 1.2743

Original strategy :

Bought at 1.2845, met target at 1.2945

Position : - Long at 1.2845

Target : - 1.2945

Stop : -

New strategy :

Buy at 1.2860, Target: 1.2970, Stop: 1.2825

Position : -

Target : -

Stop : -

As cable did rally after breaking resistance at 1.2861 (now support) on active cross-buying in sterling, adding credence to our bullish view that recent upmove from 1.2589 low is still in progress and may extend further gain to 1.2980-85 (1.618 times projection of 1.2589-1.2760 measuring from 1.2706), then towards psychological resistance at 1.3000, however, reckon upside would be limited to 1.3025-30 and price should falter below 1.3050 today.

In view of this, we are looking to buy cable again on pullback as previous resistance at 1.2861 should limit downside. Below 1.2830-35 would defer and suggest an intra-day top is formed instead, risk weakness towards support at 1.2794 but 1.2760 (previous resistance turned support) should remain intact.

Trade Idea Wrap-up: EUR/USD – Buy at 1.1275

EUR/USD - 1.1357

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1342

Kijun-Sen level : 1.1333

Ichimoku cloud top : 1.1242

Ichimoku cloud bottom : 1.1234

Original strategy :

Buy at 1.1280, Target: 1.1395, Stop: 1.1245

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1275, Target: 1.1395, Stop: 1.1240

Position : -

Target : -

Stop : -

The single currency retreated after rising to 1.1389-91, suggesting consolidation below this level would be seen and pullback to 1.1275-80 cannot be ruled out, however, reckon the upper Kumo (now at 1.1242) would hold and bring another rise later, above said resistance at 1.1389-91 would extend recent upmove to 1.1400-05 (61.8% projection of 1.0839-1.1296 measuring from 1.1119), then towards 1.1430 but overbought condition should prevent sharp move beyond 1.1450-60 and price should falter below 1.1500.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1275-80 should limit downside. Below 1.1245-50 would defer and risk test of previous resistance at 1.1220 but break there is needed to confirm top is formed instead, bring correction towards 1.1180-85 later.

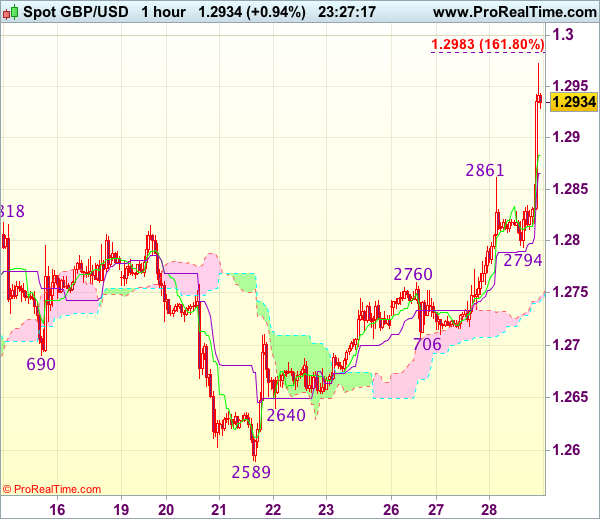

Sterling Surged after BoE’s Governor Carney

Sterling surged after BoE's governor Carney, speaking at European Central Bank conference in Portugal, said Bank of England is likely to raise interest rates as the British economy comes closer to operating at full capacity and will debate this in the coming months.

Pound eventually broke above thick daily close in fresh bullish acceleration and came close to pre-UK election high at 1.2977, posted on 08 June. Fresh bulls are also looking for retest of psychological 1.3000 barrier, after mid-May probes above were short-lived and stalled at 1.3047.

Renewed near-term bullish sentiment is reinforced technical studies which are entering full bullish setup on daily chart and supportive for further advance.

Also, close above daily cloud will be strong bullish signal.

However, hesitation on approach to strong resistance zone between 1.2977 and 1.3047 could be anticipated, with rising daily cloud expected to ideally contain.

Extended pullback should find support above converged 30/55SMA at 1.2836.

Res: 1.2977; 1.3000; 1.3047; 1.3125

Sup: 1.2900; 1.2863; 1.2836; 1.2800

Trade Idea Wrap-up: USD/JPY – Buy at 111.70

USD/JPY - 112.14

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.13

Kijun-Sen level : 112.15

Ichimoku cloud top : 111.73

Ichimoku cloud bottom : 111.61

Original strategy :

Buy at 111.80, Target: 112.80, Stop: 111.45

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.70, Target: 112.70, Stop: 111.35

Position : -

Target : -

Stop : -

The greenback has maintained a firm undertone after this week’s rally on active cross-selling in yen, adding credence to our bullishness and signal the rise from 108.82 low is still in progress, hence further gain to 112.75–80 (61.8% projection of 108.82-111.79 measuring from 110.95) would be seen, however, loss of momentum should limit upside and price should falter below 113.00-10 today, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 111.70-80 should limit downside. Below minor support at 111.46 would defer and suggest top is possibly formed, risk weakness to 111.10-15, break there would confirm, then test of support at 110.95 would follow.

Sterling Jumps on Carney U-turn

- Trading in most markets remained very volatile as investors pondered the impact of yesterday's 'hawkish' comments from ECB's Draghi. Rumours that the ECB president was misinterpreted caused an temporary reversal in yields and the euro, but the jury is still out where this move will end. European equities declined early this morning but reversed part of the early losses, currently trading with losses of less than 0.5%. US equities are in better shape and regain part of yesterday's loss in volatile trade.

- Italy's CPI fell by 0.2 % M/M in June. Today's preliminary reading marks a pullback from the revised 0.1% decline in May. On the year, prices rose by 1.2%, down from the 1.6% rise in May. Food and energy were the main reasons for the decline.

- Macron's cabinet will approve a broad outline of changes to the labour code and asks parliament for the authority to negotiate the details over the summer with unions and business groups. The government plans to introduce the new code in September by decree, to avoid getting tangled up in a long parliamentary debate.

- The UK's housing market regained some momentum in June, according to Nationwide's latest house price survey. This uptick was not enough to stop quarterly price growth slowing markedly. Average prices in Q2 were 2.8% higher than the same period last year, compared to 4.1% growth in Q1. London and the south-east suffered most.

- Britain's markets' watchdog announced radical changes to the country's asset management industry, seeking to improve transparency and value for money for customers. The proposed change is met with resistance from the industry, which is already under pressure because of Brexit and cheaper index-tracking funds stealing market share.

Rates

Draghi's comments contested

Mr. Draghi's comments yesterday continued to dominated markets and media, resulting in a volatile sideways oriented morning session. The Bund set a new low at 162.78, but traded sideways afterwards. The Bund spiked higher in the afternoon after sources stated that markets had misinterpreted Draghi's remarks yesterday. Investors didn't buy into the move after which return action occurred. Comments by BoE governor Carney, who said that the BoE may need to remove stimulus as slack erodes, helped reversing the core bond gains. A similar, but opposite, move occurred in EUR/USD.

The ECB might have been flabbergasted by yesterday's sharp reaction to Mario Draghi's comments, as it runs against the suggested prudent gradual turn. If the euro and yields surge significantly higher while equities fall, it tightens financial conditions even without any ECB action and makes the central bank's turn superfluous. We think Mario Draghi prepared a cautious turn in policy and the ECB now tries to control the sharp market reaction.

In a daily perspective, German yields fell between 0.5 (10-yr) and 2.5 (2-yr) bps, erasing a small part of yesterday's increase. The US yield curve steepened with yield changes ranging between -1.2 bps (2-yr) and +2.1 bps (30-yr). On the intra-EMU bond markets, yield spreads versus Germany narrow up to 2 bps with Spain (-6 bps) and Portugal (-7 bps) outperforming. The narrowing occurred mainly between the Bloomberg article was published.

The second tier data releases didn't impact trading in a lasting way, but nicely describe the current economic situation. On the activity side, French consumer confidence boomed, while M3 lending data confirmed a steady recovery of lending activity. On the other hand, Italian inflation (June) and German import prices (May) were down on the month, declined on a yearly basis and printed below expectations. The US trade deficit was near expectations and inventories above consensus.

Currencies

Draghi comments continue to spook EUR/USD

Yesterday's Draghi comments remained the dominant factor for EUR/USD trading. The pair extended yesterday's rally this morning, moving to the high 1.13 area. Market comments/rumours that the ECB-president was misinterpreted caused an intraday setback causing EUR/USD to trade in the 1.1360 area again. USD/JPY hovers around 112 on conflicting influences.

This morning, Asian equities traded with modest losses as the US Tech sell-off weighed. At the same time, yields remained under upward pressure. The oil rebound struggled. EUR/USD held near the rally highs in the mid 1.13 area. USD/JPY tried to sustain north of 112, but the momentum eased as correction of equities tended to support the yen.

There were few EMU eco-data with market-moving potential. FX traders continued to adapt positions to yesterday's developments (Draghi comments, delay US healthcare vote, Yellen comments…). Initially, European markets followed yesterday's trends in the US. European equities corrected further south, but the euro extended its Draghi-induced rebound. European yields held close to the recent highs, but the interest rate differentials between the dollar and the euro didn't narrow anymore. Still, EUR/USD touched a new correction top in the 1.1388 area. USD/JPY initially traded in the 112.40 area but gradually ceded ground as equity sentiment weighed.

At the onset of the US session, markets were wrong-footed by comments indicating that the ECB considered the market having misjudged yesterday's Draghi comments. The rumours triggered a sharp setback. European yields and the euro tumbled. EUR/USD filled bids below the 1.13 mark. Equities rebounded, reversing most of the intraday losses. EUR/USD staged a cautious rebound this afternoon, but the move accelerated as BoE's Carney also indicated that some removal of policy stimulation might be warranted. EUR/USD trades currently in the 1.1350/60 area in volatile trade.

USD/JPY showed no clear reaction as the intraday rebound in equities and the decline in core yields kept each other in balance. USD/JPY trades currently in the low 112.20 area. We are a bit surprised by the sharp reaction of the euro on what is currently nothing more than 'rumours'. We keep monitoring the speeches from the ECB in Portugal.

Sterling jumps on Carney U-turn

It was a calm session for GBP trading…. for most of the day. Cable held a sideways range in the lower half of the 1.28 big figure. BoE's Cunliffe indicated that the BoE had time to consider whether a rate hike is appropriated. His comments confirm the rift within the BoE, but the market reaction was limited. The price moves in EUR/GBP were in the first place driven by the swings in the euro in the wake of yesterday's Draghi comments. EUR/GBP traded in the 0.8870/80 area early this morning, but gradually lost a few ticks as sentiment on risk turned less negative. Early afternoon, the pair tumbled to the low 0.88 on the rumours that Draghi was misinterpreted by markets.

At the time of writing a new plot for sterling trading is popping up as BoE's Carney indicated that some tightening might be warranted if the growth/inflation trade-off lessens. Quite a big U-turn from recent comments of the BoE governor. Sterling is jumping sharply higher. Cable is currently trading north of 1.29 and EUR/GBP has returned below the 0.88 handle.

Trade Idea: EUR/GBP – Exit long entered at 0.8800

EUR/GBP - 0.8780

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Bought at 0.8800, Target: 0.8900, Stop: 0.8760

Position : - Long at 0.8800

Target : - 0.8900

Stop : - 0.8760

New strategy :

Exit long entered at 0.8800,

Position : - Long at 0.8800

Target : -

Stop : -

Despite intra-day brief rise to 0.8882, lack of follow through buying on break of previous resistance at 0.8866 and current sharp retreat suggest top is possibly formed and downside risk has increased for test of 0.8763 support, break there would add credence to this view, bring retracement of recent upmove to 0.8730-35, however, still reckon downside would be limited to 0.8719 support.

In view of this, would be prudent to exit long entered at 0.8800 and stand aside for now. Above 0.8845-50 would bring a retest of 0.8882 but break there is needed to signal recent upmove from 0.8304 low has once again resumed and extend further gain to 0.8900-10, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

The Euro Fell Across the Board after ECB Said that Markets Misread the Comments

The Euro fell across the board after ECB said that markets misread the comments from President Draghi on Tuesday which sent the single currency to one-year high. Draghi intended to prepare markets for decision on stimulus later this year but not making firm commitment as markets understood his message. The Euro fell to session low at 1.1291 after hitting fresh one-year high against the greenback at 1.1388 earlier today, with dip being contained by 4-hr Tenkan-sen. The price bounced quickly above 1.1300 handle which now acts as strong support, averting immediate danger seen on sustained break below 1.1300 support. The move is for now seen as extended consolidation before fresh extension higher and attack at next targets at 1.1414/28, with daily close above 1.1300 needed to confirm scenario. However, overbought slow stochastic on daily chart warns of deeper correction which may extend towards 1.1250 (converged ascending daily Tenkan-sen/Kijun-sen lines) possibly to 1.1215 (20SMA) in extension, on close below 1.1300 handle. Shape of today's daily candle after closing will be also in focus for further signals.

Res: 1.1388; 1.1400; 1.1414; 1.1428

Sup: 1.1320; 1.1391; 1.1250; 1.1215

Trade Idea: USD/CAD – Target met and sell at 1.3170

USD/CAD - 1.3088

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Sold at 1.3295, met target at 1.3130

Position: - Short at 1.3295

Target: - 1.3130

Stop: -

New strategy :

Sell at 1.3170, Target: 1.3020, Stop: 1.3230

Position: - Short at 1.3295

Target: - 1.3130

Stop:- 1.3265

Current anticipated selloff has justified our bearish view for recent decline to resume and our short position entered at 1.3295 met indicated downside target at 1.3130 (with 165 points profit), as price has remained under pressure, adding credence to our downside bias for the decline from 1.3794 top to extend further fall to 1.3020-30, then test of psychological support at 1.3000, however, near term oversold condition should limit downside to 1.2940-50 today, risk from there has increased for a rebound later.

As we have taken profit on our short position entered at 1.3295, would not chase this fall here and we are looking to reinstate short on recovery as previous support at 1.3165 should turn into resistance and limit upside. Above 1.3210-15 would defer and risk rebound to 1.3260-65 but only break there would abort and signal a temporary low is formed instead, then test of resistance at 1.3308 would follow.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

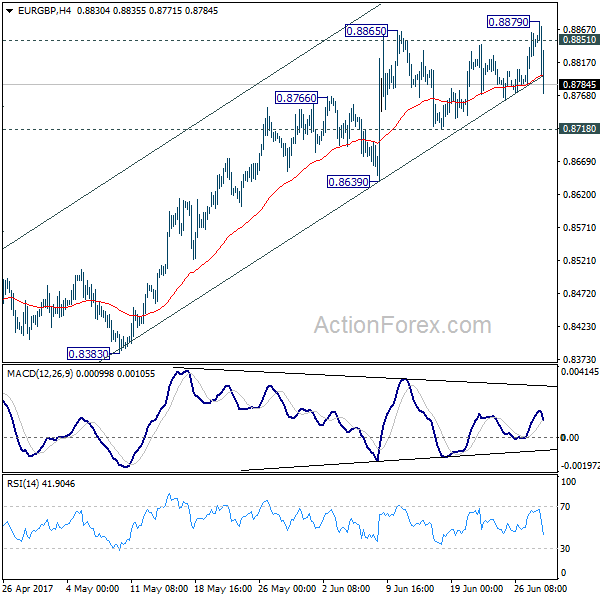

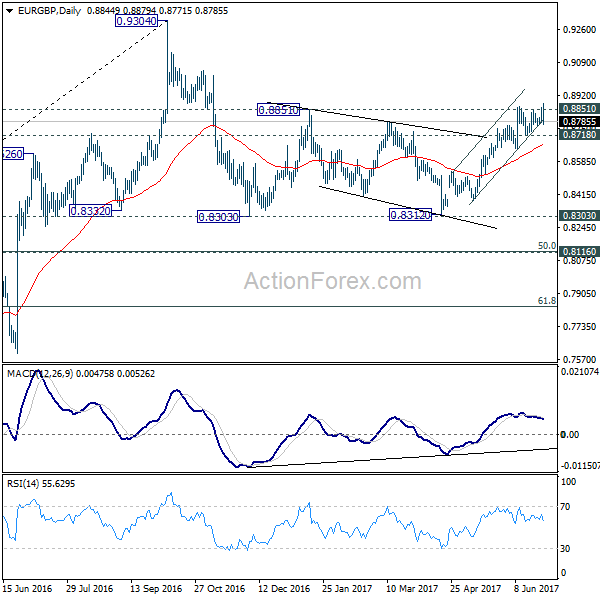

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8800; (P) 0.8831; (R1) 0.8879; More...

EUR/GBP edged higher to 0.8879 earlier today but failed to sustain above 0.8851 resistance and retreated sharply again. Intraday bias is turned neutral first. Further rise is still expected as long as 0.8718 support holds. Break of 0.8879 and sustained trading above 0.8851 will pave the way to retest 0.9304 high. However, break of 0.8718 support will now indicate near term reversal and turn bias back to the downside for 0.8639 support and below.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after testing 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

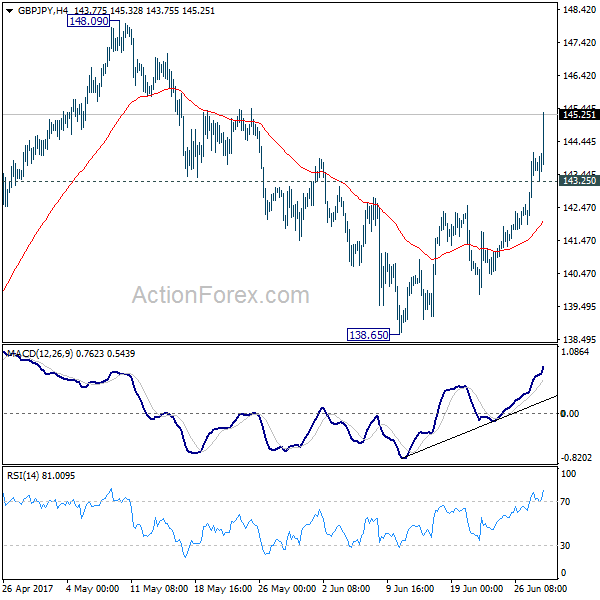

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.53; (P) 143.36; (R1) 144.78; More....

GBP/JPY surges to as high as 145.29 so far and intraday bias remains on the upside for 148.09/42 resistance zone. Decisive break there will resume whole rebound from 122.36 for key fibonacci level at 150.43. On the downside, below 143.256 minor support will turn bias neutral and bring retreat before staging another rise.

In the bigger picture, price actions from 148.42 are viewed as a sideway pattern. And medium term rally from 122.36 is expected to resume later. Decisive break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case of another fall, we'd bee looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.