Sample Category Title

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

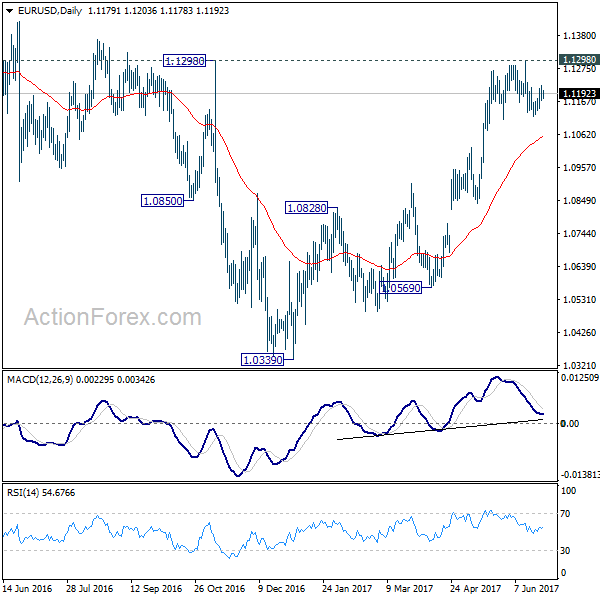

EURUSD

The EURUSD was indecisive yesterday. The bias is neutral in nearest term. The pair has been consolidating between 1.1285 – 1.1118 range area in the last two weeks and we need a clear break from the range area to see clearer direction. Overall I still prefer a bullish scenario but need a clear break above 1.1285 to continue the bullish scenario targeting 1.1350 – 1.1425 area. On the downside, 1.1080 area remains a key support and good place to buy with tight stop loss as a clear break below that area would interrupt the bullish scenario testing 1.0900 and the major trend line support as you can see on my H4 chart below.

GBPUSD

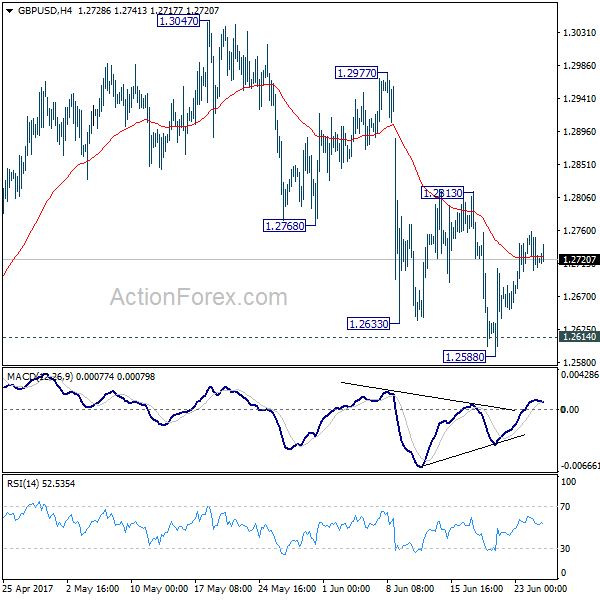

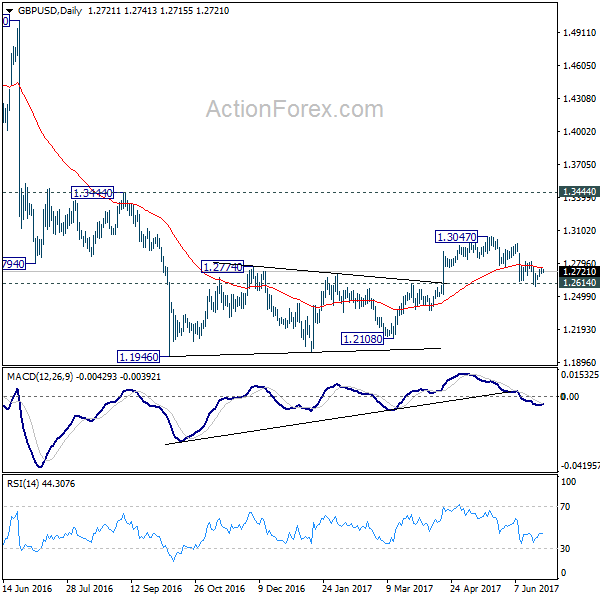

The GBPUSD was indecisive yesterday. The bias is neutral in nearest term. Immediate resistance is seen around 1.2759 (yesterday’s high). A clear break above that area could trigger further bullish pressure testing 1.2815 which remains a good place to sell with a tight stop loss as a clear break and daily close above that area would expose 1.3000 – 1.3050 region. Immediate support is seen around 1.2705. A clear break below that area could trigger further bearish pressure testing 1.2675 but key support remains at 1.2635 which need to be clearly broken to the downside to continue the double top bearish scenario targeting 1.2500 region. Overall I remain neutral.

USDJPY

The USDJPY had a bullish momentum yesterday topped at 111.94 and hit 112.07 earlier today in Asian session. The bias is bullish in nearest term testing 113.00 area. Immediate support is seen around 111.60. A clear break below that area could lead price to neutral zone in nearest term testing 111.15 area but as long as stay above 110.65 price is still in a bullish phase after broke above the trend line resistance as you can see on my H4 chart below. Overall I remain neutral.

USDCHF

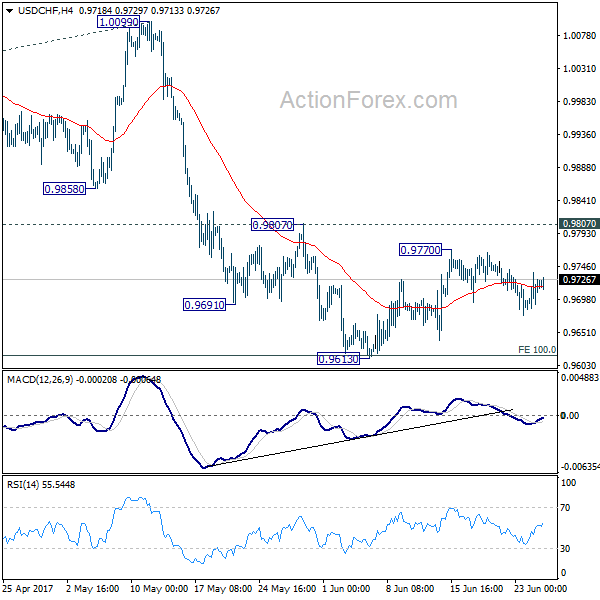

The USDCHF had a bullish momentum yesterday topped at 0.9738. The bias is bullish in nearest term testing 0.9765 – 0.9815 area which remains a good place to sell with a tight stop loss. Immediate support is seen around 0.9695. A clear break below that area could lead price to neutral zone in nearest term testing 0.9650 area. On the upside, a clear break above 0.9815 would end the bearish outlook testing 0.9900 or higher.

EUR/GBP: Sterling Rebounds Temporary On BoE Comments, But The 0.8854/66 Resistance Stays Within Reach

The US dollar was trading mixed yesterday, and there was some weakness as the latest durable goods orders data showed a 1.1% decline, which was more than expected. Core durable goods orders rose 0.1%, slower than the estimated 0.4% increase. The decline in the headline durable goods orders was the biggest drop in nearly 9-months.

Gold prices posted a sharp decline yesterday, falling to intraday lows of $1235.99 before stabilizing. The decline in gold prices was attributed to an erroneous sell order which pushed gold prices lower.

The economic calendar today is packed with speeches from various central bank officials. This includes ECB President Mario Draghi, BoE Governor, Mark Carney and later in the day, FOMC members Harker and Kashkari along with the Fed Chair Janet Yellen are expected to speak.

EURUSD intraday analysis

EURUSD (1.1180): The EURUSD was rather muted with price action staying firmly above the 1.1129 support level. The strong intraday consolidation seen above this level and 1.1200 is indicative of a possible breakout in the near term. Above 1.1200, further gains could be expected, but the risk of rising past 1.1200 could signal a move towards the support level at 1.1129, followed by a decline to 1.1018. EURUSD is currently carving out the head and shoulders pattern with the neckline support at 1.1129 that will be key. The current gains in prices could form the right shoulder following which we could expect some strong declines.

GBPUSD intraday analysis

GBPUSD (1.2726): The British pound closed with a doji candlestick pattern yesterday following the strong rally off the 1.2600 support level. Resistance is seen at 1.2800 - 1.2780 which could be tested in the near term. Failure to break past this resistance level could put GBPUSD back on track for near-term losses. On the 4-hour chart, if we expect to see a rally in prices, then GBPUSD could be seen pushing lower near 1.2800. The evolving inverse head and shoulders pattern here suggests some near-term upside in prices. Watch for a reversal near 1.2688 after establishing resistance at 1.2800. This would mark the right shoulder in GBPUSD with the minimum upside target coming in at 1.3200 at the very least.

USDJPY intraday analysis

USDJPY (111.88): The USDJPY managed to break past the resistance level at 111.61 by yesterday's close. However, the price action is not very convincing at this resistance level, and this could probably result in some near-term declines. On the 4-hour chart, USDJPY is trading within the resistance zone of 112.00 - 111.70 following the bullish break out from the flag pattern. Near-term declines could be held at 111.70, but a break down below this level could invalidate the bull flag pattern. The next lower support is seen at 110.70.

Currencies: Dollar Still Awaiting A Trigger For A Directional Move

Sunrise Market Commentary

- Rates: More of the same or surprise from Yellen?

Today's wildcard is Fed chairwoman Yellen's speech. Will she holds on to the FOMC's communication line from the June statement, downplaying the recent setback in eco data, if she touches on monetary policy? We think so given the low amount of eco data published since. That should prevent more US Treasuries gains ahead of key eco data (PCE on Friday). - Currencies: Dollar ‘resilient' despite disappointing US data

The dollar easily reversed an intraday setback after poor US durable orders. However, EUR/USD and USD/JPY are still locked in tight ranges. The focus for USD trading is on US consumer confidence and on a speech of Fed's Yellen today. If Yellen confirms the Fed normalization path, it should protect the USD downside, but sustained USD gains need better data

The Sunrise Headlines

- US equities closed flat (S&P/Dow) to lower (NASDAQ). Asian markets follow WS and trade mixed. Brent oil tries to move further up, but little headway is made overnight.($/barrel).

- Brazilian president Temer is charged with corruption by the chief prosecutor. This unprecedented development may put the president on trial, if 2/3 of the chamber of deputies approve to proceed.

- The US Supreme Court cleared much of President Trump's travel ban to take effect this week and agreed to hear arguments in the fall, giving the president at least partial vindication for his claims of closing the nation's borders.

- Barnier, the EU chief negotiator, rejected May's offer to protect work and residency rights for its citizens living in Britain and asks Britain go further.

- The US Senate's health care bill would increase the number of uninsured Americans by 22 million by 2026, the Congressional Budget Office said. The report came as Republicans released a slightly revised version of the legislation.

- China's industrial profits rose 16.7% in May from a year earlier as global demand improved, helping to fill companies' order books.

- With little data on the eco-calendar, investors will focus on Yellen, Carney and the ECB's forum for policy clues. We also have Italy, Germany and US selling bonds today and June US consumer and Richmond manufacturing confidence coming out.

Currencies: Dollar Still Awaiting A Trigger For A Directional Move

Will Yellen help the dollar?

On Monday, the dollar initially profited from positive risk sentiment. The US currency temporary reversed the intraday gains on disappointing US durable orders, but showed resilience afterwardst. Especially USD/JPY erased the post data weakness amid talk of new carry trades funded in yen. The pair closed the session at 111.86 (from 111.28). EUR/USD finished the day at 1.1182.

This morning, Asian equities trade narrowly mixed. USD/JPY trades in the high 111 area, but a test of the 112.13 resistance didn't occur yet. EUR/USD hovers in the high 1.11 area. Yesterday's comments from ECB's Draghi defending the low rate policy maybe prevented further euro gains. Basically, the recent sideways trading persists. Commodity currencies like the CAD, the AUD and the kiwi dollar remain well bid. The latter continues its recent outperformance despite a smaller May trade surplus.

US Consumer confidence and Yellen in focus

In the US, consumer confidence (Conference board) and the Richmond Fed manufacturing index will be published. Consumer confidence is expected to ease slightly, but another negative surprise may add to lingering uncertainty on the Fed rate hike path. That should be USD negative. However, the dollar easily resisted a poor durable goods report yesterday. The market might be cautious to place big bets ahead of a speech of Fed's Yellen in London (CET 19.00). If she addresses monetary policy, we expect her to confirm to Fed communication after the June FOMC decision. This might help to protect the downside of the dollar, but we don't expect a big USD rebound. For that the happen, US data have to improve. Headlines from the ECB forum in Portugal are a wildcard. In a daily perspective, we expect EUR/USD trading to remain technical in nature ahead of Yellen. We also keep an eye at the USD/JPY price action. We are a bid surprised by recent ‘relative dollar strength' even as core yields stay low. For now, we remain cautious on further USD/JPY-gains as long as US eco data remain mediocre and as long as the dollar receives no additional interest rate support

Technical picture: USD still confined to tight ranges

Early May, EUR/USD failed to break below the 1.0821/1.0778 support (gap). Poor US data and US political upheaval propelled EUR/USD north of the 1.1023 range top. The pair tested the 1.1300 area going into the FOMC decision, but the test was rejected. The Trump top/correction top at 1.1300/1.1366 proved to be a solid resistance. USD sentiment will have to become really negative to clear this hurdle. EUR/USD 1.1110 is a first minor support. A return below 1.1023 would indicate that the upside momentum has eased.

The USD/JPY rally ran into resistance in early May. A mini sell-off mid-May made the short-term picture negative, driving the pair further down in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair beyond a first minor resistance at 110.81. A break beyond the 112.13 correction top would improve the ST-picture. The day-to-day sentiment improved of late, but we remain cautious to forecast a U-turn.

EUR/USD: test of 1.1300/66 resistance rejected, but correction is modest. First support at 1.1110 holds

EUR/GBP

EUR/GBP locked near 0.88

Yesterday, the conservative party reached a deal with the DUP of Northern Ireland to support the minority government of PM May. The deal applies for the life of the current parliament (till 2022).Amongst others, it contains £1bln extra funding for northern Ireland. Sterling gained temporary a few ticks after the announcement, but the reaction was negligible. EUR/GBP closed the session at 0.8789. Cable finished the day at 1.2723.

Today, the CBI retail data will be published. A modest decline is expected. The CBI data are interesting but have rarely a lasting impact on GBP-trading. Even so, we look for the market reaction in case of better than expected data as the debate on a rate hike in the BoE intensifies. BoE governor Carney will give a press conference after the publication of the Financial stability report. This is not the forum for an in extenso debate on monetary policy, but the BoE governor can make some sidesteps. If anything, his assessment might be slightly negative for sterling. Headlines from the Brexit negotiations remain a wildcard. The EU apparently holds a rather tough stance which is a tentative sterling negative.

From a technical point of view, EUR/GBP extensively tested the 0.8854 area (2017 top), but a real break didn't occur. The BoE debate on a rate hike caused some volatility recently. In the end, the 0.8854/66 resistance remains within reach. A break would open the way to the 0.90 area. A return below the 0.8655 correction low would indicate easing pressure on sterling. Such a break lower will be difficult. A EUR/GBP buy-on-dips approach remains favoured

EUR/GBP: sterling rebounds temporary on BoE comments, but the 0.8854/66 resistance stays within reach

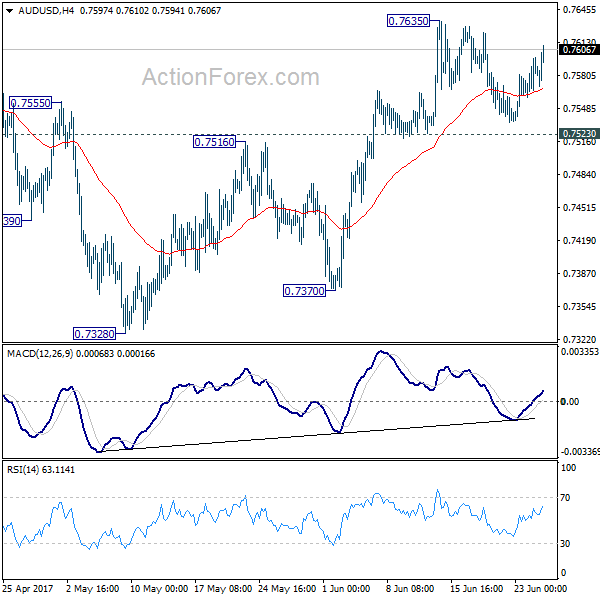

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7564; (P) 0.7581; (R1) 0.7603; More....

Intraday bias in AUD/USD remains neutral at this point. With 0.7523 intact, further rise is expected. Break of 0.7635 will extend the rise from 0.7328 to 0.7748 resistance and above. At this point, there is no clear sign of range breakout yet. Hence, we'd be cautious on topping again as it approaches medium term fibonacci level at 0.7849. Meanwhile, break of 0.7523 will argue that rebound from 0.7328 is possibly completed. In that case, intraday bias will be turned back to the downside for 0.7370 support.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8116) and above.

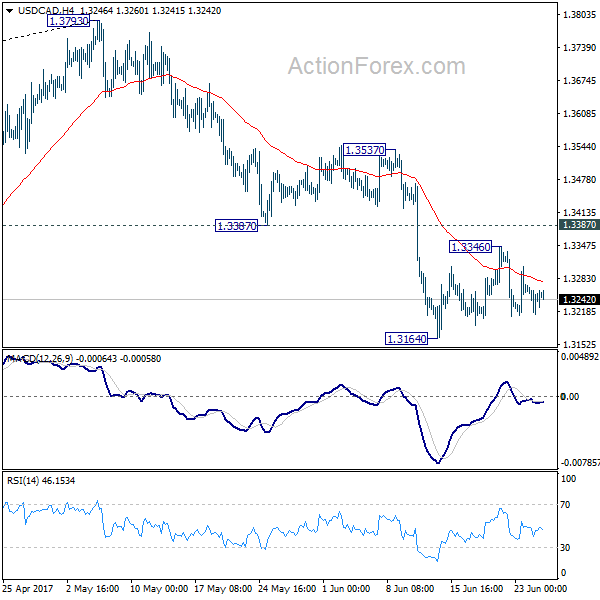

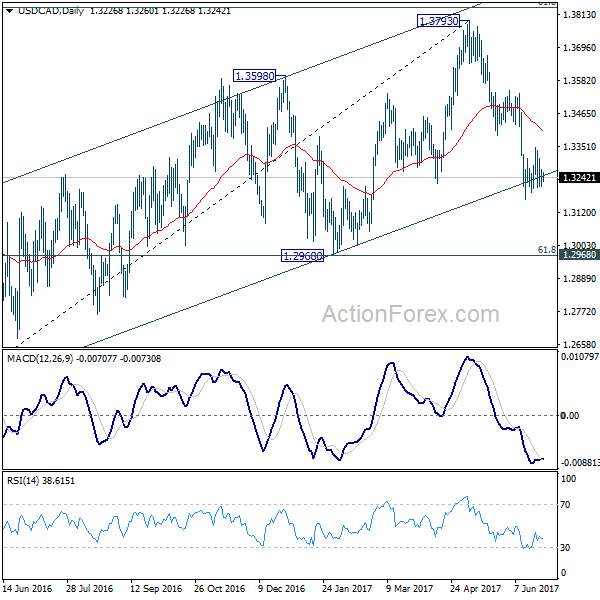

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3216; (P) 1.3243; (R1) 1.3273; More....

USD/CAD's consolidation from 1.3614 is still unfolding and intraday bias stays neutral. In case of another recovery, upside should be limited by 1.3387 support turned resistance to bring fall resumption. As noted before, corrective rise from 1.2460 has completed at 1.3793 already. Below 1.3164 will extend the decline from 1.3793 to 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969. However, firm break of 1.3387 will dampen our view and turn focus back to 1.3537 resistance next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.

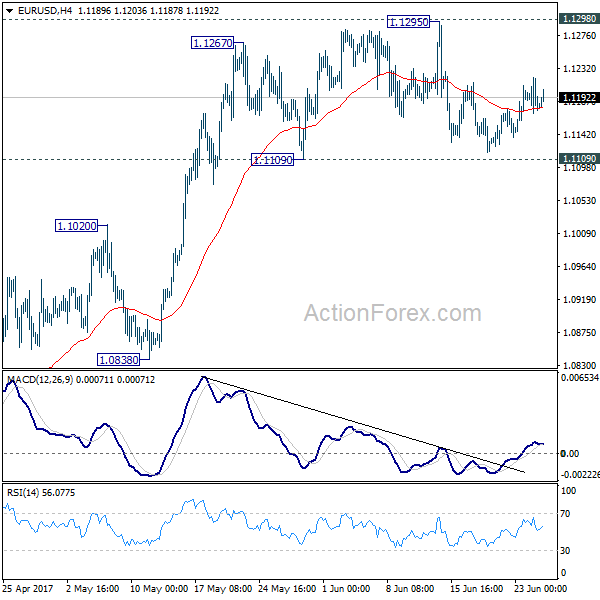

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1162; (P) 1.1190 (R1) 1.1210; More....

Intraday bias in EUR/USD remains neutral for the moment as it's still bounded in range of 1.1109/1295. With 1.1109 support intact, there is no indication of reversal yet. Decisive break of 1.1298 key resistance will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0941). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Elliott Wave Trade Ideas Performance Update

6 positions were entered last week with total loss of 115 points and the positions are listed below.

16 Jun : GBP/USD - Short at 1.2750, exited at 1.2810 (- 60 points)

20 Jun : GBP/JPY - Long at 141.50, exited at 141.55 (+ 5 points)

21 Jun : AUD/USD - Long at 0.7595,

21 Jun : EUR/JPY - Long at 123.80,

22 Jun : GBP/USD - Short at 1.2675, exited at 1.2735 (- 60 points)

23 Jun : USD/CAD - Short at 1.3295,

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 60 -65 -60

Jun + 1 + 10 +20 -120 +205

Jul

Aug

Sep

Oct

Nov

Dec

Y-T-D + 136 - 232 +127 +298 -185 +190

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2698; (P) 1.2728; (R1) 1.2752; More...

No change in GBP/USD's outlook as it's bounded in range of 1.2588/2813. Intraday bias stays neutral for the moment. With 1.2813 resistance intact, deeper decline is expected. Sustained break of 1.2614 resistance turned support will confirm our bearish view that consolidation pattern from 1.1946 has completed. In that case, deeper fall should be seen back to retest 1.1946 low. However, break of 1.2813 resistance will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed at 1.3047 after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9690; (P) 0.9714; (R1) 0.9748; More.....

No change in USD/CHF's outlook as the consolidation pattern from 0.9613 is still extending. Intraday bias stays neutral and another rise cannot be ruled out. But after all, near term outlook remains bearish as long as 0.9807 resistance holds. Break of 0.9613 will resume the decline from 1.0342 and target 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. On the upside, firm break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

Market Update – Asian Session: China Premier Li Upbeat On Economic Prospects Amid Another Double-Digit Industrial Profit Growth

US Session Highlights

(US) Fed’s Dudley (dove, FOMC voter): Fed's taken very measured and careful approach to shrinking bond portfolio

(US) MAY PRELIMINARY DURABLE GOODS ORDERS: -1.1% V -0.6E (the largest drop in six months); DURABLES EX TRANSPORTATION: 0.1% V +0.4%E

(US) May Chicago Fed National Activity Index: -0.26 v +0.49 prior

(US) JUNE DALLAS FED MANUFACTURING ACTIVITY: 15.0 V 16.0E

Stocks opened the week on a positive note, spurred by a rally in Europe, as two Italian banks were saved from bankruptcy with public money and Nestle hit a new all-time high, gaining 4% on the day. Technology stocks fell out of favor, down 0.3%. Best performing sectors in the S&P were Utilities and Financials, gaining 0.8% and 0.5% respectively.

US markets on close: Dow +0.1%, S&P500 flat, Nasdaq -0.3%

Best Sector in S&P500: Utilities

Worst Sector in S&P500: Technology

Biggest gainers: FE +4.1%; EQT +3.8%; CVS +3.5%

Biggest losers: FTR -6.6%; ARNC -6.0%; QRVO -5.1%

At the close: VIX 9.9 (-0.1pts); Treasuries: 2-yr 1.36% (+1bps), 10-yr 2.14% (-1bps), 30-yr 2.70% (-2bps)

Politics

(US) Sen Collins (R-ME) to vote NO on motion to proceed on healthcare legislation - tweet

(US) CBO scores Senate Republican healthcare bill: 22 million more people uninsured by 2026

(BR) Brazil Prosecutor General Janot confirms to proceed with corruption charges against President Temer - Brazil press

Key economic data

(CN) CHINA MAY INDUSTRIAL PROFITS Y/Y: 16.7% V 14.0% PRIOR; YTD 22.7% V 24.4% PRIOR

(NZ) NEW ZEALAND MAY TRADE BALANCE (NZD): 103M (3rd straight surplus) V 419ME; 12-MONTH YTD: -3.75B V -3.39BE

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 111.8 v 112.4 prior

Asia Session Notable Observations

China Premier Li spoke at World Economic Forum, pleding to maintain policy settings amid steady growth expectations in Q2; Unemployment seen at 4.9%.

China profit growth accelerates to 16.7% from 14.0%, while Liabilities growth slows to 6.5% from 6.7% in May.

New Zealand posts 3rd straight trade surplus; Exports in line with estimates and Imports higher than expected; Shipments of Dairy spike over 40% y/y to NZ$1.2

Brazil Prosecutor confirms proceeding with corruption charges against Pres Temer.

White House notes signs of Syria preparing another chemical attack, warns Assad will pay heavy price if he proceeds.

Speakers and Press

China

(CN) China Premier Li: Economy maintaining steady growth and improving in Q2; To keep proactive fiscal policy and prudent monetary policy - World Economic Forum comments

(CN) PBOC said to be in talks with MoF on asset management tax plan

(CN) China May Lottery Sales CNY37.7B, +8.9% y/y

Japan

(JP) Japan Fin Min Aso: Takata bankruptcy may impact jobless rate; Will work with METI to gauge impact - press

(JP) Japan ruling Liberal Democratic Party lawmaker Shigeru Ishiba: Japan must keep its 2020 primary balance target; faith in currency is extremely important

(JP) Japan Q1 Household Assets ¥1,809T, +2.7% y/y

Korea

(KR) South Korea Pres Moon: Extra budget will help economy get back to 3% GDP growth - press

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.3%, Hang Seng +0.1%, Shanghai Composite -0.1%, ASX200 -0.1%, Kospi +0.3%

Equity Futures: S&P500 flat; Nasdaq +0.1%, Dax flat, FTSE100 flat

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1180-1.1195; JPY 111.80-112.10; AUD 0.7575-0.7605; NZD 0.7275-0.7300

Aug Gold flat at 1,246/oz; Aug Crude Oil +0.3% at $43.50/brl; July Copper -0.2% at $2.63/lb

SPDR Gold Trust ETF daily holdings rise 2.7 tonnes to 853.7 tonnes

Morgan Stanley lowers Q3 Iron Ore price forecast by 23% to $50/ton - press

(CN) PBOC SETS YUAN MID POINT AT 6.8292 V 6.8220 PRIOR; Weakest Yuan fix since May 31st

(CN) PBoC: To skip today's open market operation (OMO); 3rd straight skip

(JP) Japan MoF sells ¥1.77T v ¥2.2T indicated in 2-yr 0.1% JGBs; Avg yield: -0.103% v -0.162% prior; bid to cover: 6.79x v 5.06x prior

(AU) Australia (AOFM) sells A$150M in 2.5% 2030 indexed bonds; avg yield 0.6562%

Asia equities notable movers

Australia

QBE Insurance (QBE) +1.3%; Exec: Seeing higher claims in emerging markets - press

Blackmores Limited (BKL) -3.9%; CEO Christine Holgate to resign

Metcash (MTS) -4.1%; Cut at Credit Suisse

Japan

Nissan (7201) +0.7%; Targets 8% global market share as part of its next mid-term plan - press

Mitsubishi Motor (7211) +1.4%; Guides FY19 global vehicle production at least 1.5M units, +40% from last FY

Nikon (7731) +0.7%; Said to increase display device output for camera and TV products - Nikkei

Hong Kong

China Southern (1055) -3.5%; To raise up to $1.9B in share sale

Pioneer Global Group (224) +13.4%; Reports FY17 (HK$) Net loss 67.6M v loss 67.7M y/y; Rev 295.0M v 258.7M y/y

Bosideng International Holdings limited (3998) +5.1%; Reports FY (CNY) net 391.8M v 280.9M y/y, Rev 6.82B v 5.79B y/y