Sample Category Title

Gold Analysis: Recovers After Crashing

After the sudden crash of the yellow metal, which occurred on Monday, the bullions price was recovering on Tuesday. The yellow metal traded rather flat, as it faced the resistance of the first weekly support level a the 1,246 mark. However, that resistance was broken and the bullion jumped to trade above the 1,250 mark. By looking at the technical aspects of the commodity price on the hourly chart, a prolonged recovery of the metal now seems unlikely. Every ascending chart of the bullion has been broken. Moreover, the metal faces the resistance of the various simple moving averages, the monthly pivot point at 1,253 and the weekly pivot point at 1,252.57. However, if these levels of resistance are broken, the pair might resume the surge.

Technical Outlook: GBPUSD – Near-Term Focus Shifted Higher While Daily Tenkan-Sen Holds

The pair rallied around 60 pips on Monday, bringing bulls back to play after four consecutive descending long-legged daily candles last week, which signaled hesitation of broader bulls ahead of daily cloud barrier. Thin daily cloud which twists on Tuesday continued to attract for fresh attacks and today's rally came just ticks ahead of it. Plethora of strong supports provided by daily MA's (which also made a multiple bull-crosses and contained last week's easing) continues to underpin the action for final break above daily cloud / 100 SMA pivots at 111.80 zone and further retracement of 114.36/108.80 descend. Corrective easing from today's high at 111.71 should ideally find support at 111.48 (Fibo 38.2% of today's 111.11/71 rally) with extended dips to be contained at 111.34 (hourly cloud top) to keep fresh near-term bulls in play.

Res: 111.71, 111.80, 112.00, 112.25

Sup: 111.57, 111.48, 111.34, 111.24

ECB President Mario Draghi Points To High Income Inequality, Defends Ultra Low Interest Rates

'Draghi pouring water on expectations of reducing monetary stimulus, that saw the euro then start to weaken.' - Douglas Borthwick, Chapdelaine Foreign Exchange

The European Central Bank President Mario Draghi reported on Tuesday that in order to overcome Europe's income inequality authorities should focus more on education, innovation and investment in human capital. According to the ECB President inequality in the Euro zone grew markedly since the last global financial crisis. Thus, governments should consider adopting policies aimed at redistributing wealth. According to data from Eurostat, the inequality level has increased sharply since the crisis in countries like France and Spain. The highest level of income inequality has been registered in Greece, Spain and Portugal. Apart from that, Mario Draghi said that ultra low interest rates helped to boost job creation, economic growth and benefit borrowers. Moreover, the ECB President said that a faster pace of monetary policy tightening would likely lead to a new wave of recession and boost income inequality in the region. Following these dovish comments, the US Dollar hit its one-month high against the Japanese Yen and rebounded sharply against the Euro, as the probability of a monetary policy stimulus reduction diminished.

Orders For US-Manufactured Durable Goods Drop 1.1% Last Month

'We see the core data as consistent with soft business investment in the second quarter.' - Blerina Uruci, Barclays

Orders for US-made durable goods dropped more than expected last month, pointing to a slowdown in the manufacturing sector. The Commerce Department reported on Monday that durable goods orders fell 1.1% in May, following the preceding month's downwardly revised drop of 0.8% and falling behind expectations for a 0.5% decline. In the meantime, core durable goods orders rose just 0.1% last month after dropping 0.5% in April, whereas analysts anticipated an increase of 0.4% during the reported month. Monday's data combined with the prior week's retail sales and inflation figures suggested that the economy failed to regain positive momentum in the June quarter despite the recent sharp drop in the jobless rate. Back in the Q1, the US economy expanded at an annualised 1.2% pace. Yesterday's data also showed that orders for machinery climbed 0.6%, while shipments dropped 0.3%. Orders for civilian aircraft dropped 11.7%, whereas orders for defence aircraft and parts plunged 30.8%. Orders for motor vehicles and parts advanced 1.2% last month.

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9726

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9724

Kijun-Sen level : 0.9713

Ichimoku cloud top : 0.9710

Ichimoku cloud bottom : 0.9696

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s retreat from 0.9738 to 0.9692, lack of follow through selling and the subsequent rebound suggest further choppy trading would be seen and another bounce to 0.9738-43 cannot be ruled out, however, only a firm break above there would revive bullishness and signal low is formed, bring test of 0.9766-71 resistance first. Once this resistance is penetrated, this would confirm recent rise from 0.9613 low has resumed for test of resistance at 0.9808, then towards another previous resistance at 0.9825.

On the downside, below said support at 0.9692 would suggest the rebound from 0.9676 (Friday’s low) has ended, bring another test of this level, break there would signal the erratic fall from 0.9771 top is still in progress for retracement of recent rise to 0.9660, however, as broad outlook remains consolidative, still reckon downside would be limited to 0.9641 support, risk from there is seen for another rise to take place later.

Nikkei Carves Out Swing Low | AUDJPY Pauses Below Key Resistance

The weaker Yen has benefitted the Nikkei which now appears on track for another leg higher towards the 20,400 targets. AUDJPY has since paused below a critical juncture yet we suspect the odds favour an eventual upside break.

The Nikkei printed a solid bull candle on Friday to suggest the low is in place, which leaves potential for the final leg up to our 20,400 targets. It has been helped higher by a weaker Yen and, if USDJPY goes on to hit the 114.38 target then the Nikkei could exceed the bullish target above 20,400. However, we are also slightly concerned that the bond market is not backing up the higher Nikkei, which is why we are conservatively bullish for another swing higher whilst also monitoring the development on a potential bearish wedge.

Friday's low also coincides with MR1 and the low of 3x Dojis. Therefore, we can use this area to aid with stop placement but to increase the potential reward/risk ratio we can consider a buy-limit within Friday's range.

We have included a potential bearish wedge but this is for illustrative purposes only; price need to remain contained perfectly within the red lines for the pattern to be valid, so we focus on the relationship between the swings instead. If this is a true bearish wedge, then each leg higher should be of less magnitude, so direct gain from here lowers the probability of the bearish wedge being confirmed. Moreover, to confirm the pattern we need to see a break of a prior swing combined with a higher low and, yet, we see neither. Therefor the near-term bias remains bullish and we will continue to monitor the potential wedge.

The 2yrs spread is testing the bearish trendline, so a bullish signal can be taken if it breaks to the upside over the coming sessions. We would feel more confident with Nikkei being near current highs if the spread it to move higher because presently, its failure to close the gap and support Nikkei undermines recent gains on the Stock index. Alternatively, if we are to see the spread move lower (and break the blue line) then this improves the odds of a bearish wedge of playing out.

The Australian Dollar is one of many currencies taking advantage of the weaker Yen. AUDJPY is fliting with a bearish resistance level and we suspect it odds of it breaking higher form here are strong. As Friday's candle particularly bullish, its likely we'll only see a minor pullback before it breaks higher. Therefor this is one of the rare occasions we'd consider entering before the break and using the 50% retracement of the bullish candle to aid with potentials entry or stop placement.

The zone between the 50% and 61.8% retracement of Friday's range also coincides with a swing low and swing high, making it an important level going forward. As prices have also stalled beneath the MR2 pivot as well as the bearish trendline, we think the odds of a move lower form here are relatively high, so we'll seek support to be found above the Fibonacci zone.

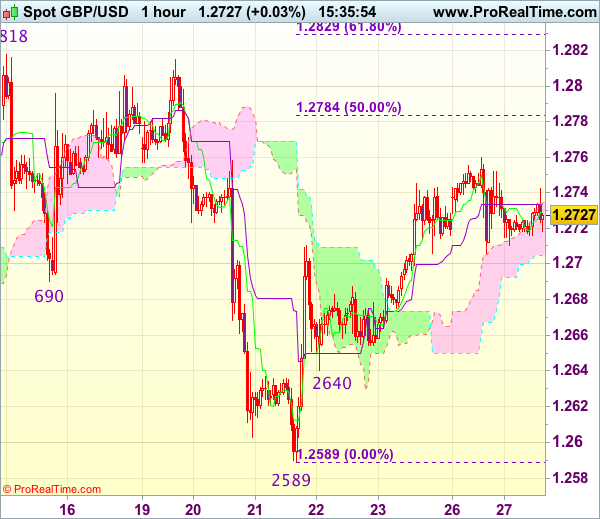

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.2730

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2729

Kijun-Sen level : 1.2733

Ichimoku cloud top : 1.2734

Ichimoku cloud bottom : 1.2705

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has retreated after rising to 1.2760, suggesting consolidation below this level would be seen, however, near term upside risk remains for the move from 1.2589 low to bring retracement of recent decline to 1.2780-85 (50% Fibonacci retracement of 1.2978-1.2589) but reckon upside would be limited to 1.2800 and price should falter below resistance at 1.2818, bring another selloff later.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below 1.2700-05 would bring weakness towards 1.2675-80 but break of latter level is needed to signal the rebound from 1.2589 has ended, bring further fall towards support at 1.2640 which is likely to hold on first testing.

EUR/USD Analysis: Continues To Surge

As it was expected the common European currency found support against the US Dollar, and the currency exchange rate continues on its set part higher. Moreover, during Monday's trading the pair managed to touch the 1.1220 mark. The Euro has set its eyes on the 1.1233 mark against the Buck, as that is the closest support level, which is likely to be reached. At that level the weekly R1 is located at. It is most likely that the 55-hour SMA, which helped the rate in its rebound on Monday, will push the pair higher until it reaches the mentioned resistance level. However, the weekly R1 might not be reached during Tuesday's trading, as the upper trend line of the short term ascending channel pattern still remains in the way of the pair above the 1.12 mark.

GBP/USD Analysis: Waits Fundamentals

On Monday, the expected upside potential up to the 1.2770 mark was halted by the monthly S1 at 1.2758 which intersected with the upper channel line. Subsequently, the price dropped down to the weekly PP at 1.2708 in response to fundamentals, but managed to recover some losses, thus returning above the 200-hour SMA. In this trading session, the Pound crossed the 55-hour SMA from below and continued a minor surge up to 1.2740. Technical indicators remain bullish, thus a continuous surge is likely to occur in the upcoming hours, setting either the aforementioned S1 or the 38.2% Fibo at 1.2770 as possible upside targets. In general, the pair is not expected to fall below the 200-hour SMA. Today, the economic calendar is full of important fundamental events, thus the rate should respond accordingly.

USD/JPY Analysis: Bearish In This Trading Session

Strong upside momentum guided USD/JPY for the whole trading session on Monday prior to reversing to the downside early on Tuesday. The US Dollar returned below the monthly PP at 111.80 and is expected to remain there, as bearish technical indicators suggest the prevalence of downside risks. From technical point of view, the pair broke the descending channel patter; thus a retracement down to the 111.30 mark, approximately, is likely to occur. There, the 200-hour SMA should support the rate, thus limiting further depreciation. The 55– and 100-hour SMAs in the 111.35/45 area may likewise halt the pair. The most important fundamentals scheduled for today are data on consumer confidence at 1400 GMT and Fed Yellen's speech at 17:00 GMT.