Sample Category Title

False Breakout Could Be About To Send Gold Reeling

Key Points:

- Price action produces a false breakout.

- 60 EMA dynamic support is looming.

- Watch for a break lower in the coming week towards the $1230 an ounce mark.

The past six months have proved relatively positive for gold as the metal has continued to make headway over a cooling U.S. Domestic economy. However, the past few days have proved relatively illuminating for the metal with a false breakout occurring above the trend line likely signalling a sharp pullback could be ahead. Subsequently, it remains to be seen if Gold can retain its bullishness or whether a rout is, potentially, in progress.

It's always the case that the retail money chases the high and the last few days, in precious metals, have largely proved that adage. As the large banks and financial institutions have been clamouring to get out of their positions, and have become largely net short via gold miners and derivatives, the retail trader has blundered into a bear trap.

This effect is quite clearly seen on the daily chart with the false breakout above the short term declining trending line. As momentum started to stall, and the smart money exited their positions, Gold saw plenty of spurious volume as retail traders sought to position long on the breakout. Unfortunately, the move stalled near the $1296.09 mark and we are left with price action now slipping steadily lower.

Subsequently, we are now left with the question of where to next for the precious metal given that markets have taken a relatively negative tone following, not only the false breakout, but also the FOMC decision. A quick technical analysis of the metal suggests that we could be in for some further falls given the fact that the RSI Oscillator remains within neutral territory and steadily trending lower. Additionally, price action is closing in on the 60 Day EMA and a break of this level could see a decline as deep as $1230 an ounce.

However, given the U.S. Fed's recent commitment to economic tightening Gold could fundamentally be facing a much deeper fall. In fact, if the central bank follows through on their forward guidance to continue hiking rates, whilst tapering their balance sheet, we could see a deleterious decline that takes price action all the way to the bottom of the supporting trend line around $1140 an ounce.

Ultimately, the metal's near term trend is clearly negative but it just remains to be seen whether Gold experiences a soft or a hard landing. In the short term, at least, we are likely to see a fall back towards $1230 an ounce over the next few weeks. Any further declines will require some fundamental variables to change and that remains at the behest of the Federal Reserve.

CHFJPY Looking To Rebound

Key Points:

- A reversal is looking likely in the coming sessions.

- Support being generated by the 100 day EMA.

- Also keep half an eye on the BoJ.

The CHFJPY has been having some fairly reliable reversals over the past few weeks and it looks about ready to make yet another one. Nevertheless, the sheer momentum of the recent sell-off does bring into question whether or not the pair can make a recovery this time around. As a result of this, we might need to take a closer look at the technicals to try and establish a bias for the days ahead.

First and foremost, it's fairly obvious that the CHFJPY has recently entered a ranging phase that has kept the pair oscillating between the 115.08 and 112.42 levels. Currently, price action is at the lower extreme of this range – usually a sure sign that we can expect to see the bulls get back into the driving seat in the coming sessions. However, can we be sure that support will hold this time around? Indeed, the 12 and 20 day EMA's have just had a bearish crossover and the parabolic SAR is signalling that a downtrend is underway.

Fortunately, a closer inspection of the technicals reveals that we have good reason to suspect that a reversal is on its way in the near future. For one thing, unlike its shorter period counterparts, the 100 day moving average is still quite bullish. As shown, it is not only beneath the 12 and 20 day lines but it is also supplying dynamic resistance around that 112.42 handle. Given that this price is also the 38.2% Fibonacci retracement, a breakout would be highly irregular.

Regardless, minimised downside risks do not necessarily mean that we are about to see a solid uptrend take place. Instead, the argument for some buying pressure stems from the stochastics and the Bollinger bands. Starting with the stochastics, these are clearly in oversold territory and will need to be relieved going forward – potentially leading to some decent gains. However, it's really the Bollinger bands that indicate that a sizable recovery is required as price action should be trying to move back to the basis line imminently.

Ultimately, keep an eye on this pair as there is definitely some potential for a rally moving ahead which could extend all the way up to the 115.08 handle. This being said, monitor the fundamental side of things on Friday as the BoJ could be making waves, thereby disrupting technical forecasts.

BoE Should Look Beyond Temporary Inflation

- BoE should remain on hold despite inflation rising well beyond target;

- Fed signals another hike this year but markets aren't buying it;

- Strong Australian jobs report aids further gains in AUDUSD.

The UK will be back in focus again on Thursday as the Bank of England announces its latest monetary policy decision, amid all the political chaos following last week's snap election result, and we'll also get retail sales numbers for May.

The timing of the latest monetary policy decision from the BoE couldn't be much worse, as the country prepares to start Brexit negotiations without a stable government following the surprising snap election result. To make matters worse for policy makers, this comes as inflation has hit 2.9%, higher than what it anticipated would be the peak only a month ago.

While policy makers claimed after the last meeting that they would only need little upside news on growth or inflation to consider voting for tighter policy, I would be extremely surprised to see them act at this moment in time. The huge amount of economic uncertainty paired with the temporary drivers of inflation and lower growth prospects is surely a good enough reason to look through the current spike in prices. Should they not look beyond this and even signal a possible hike in the near-term, it would catch markets completely off guard which could provide a significant boost to sterling.

The Federal Reserve finds itself in a far more privileged position, albeit still not an ideal one, with growth prospects much better, the economy in better shape and inflation at a level that allows for tighter policy without necessitating the need for it. The FOMC raised interest rates for a second time this year on Wednesday – as was fully expected and priced in – and signalled an intention to do so again this year while laying out plans to begin reducing the size of its balance sheet.

Traders appear unconvinced by the possibility of another rate hike this year, despite what the Fed indicated, with the implied probability of one by December standing at below 50%. Investors appear concerned about the slowing pace of inflation but this doesn't seem to bother policy makers, who revised down their projection for this year to 1.6%, from 1.9% previously, while maintaining their forecasts of 2% for 2018 and 2019.

A strong jobs report boosted the Australian dollar overnight, as stronger gains in employment – boosted entirely by full time roles – brought the unemployment rate back to a four year low, while participation rose to its highest in almost a year.

Still to come today there's plenty of economic data being released, including retail sales from the UK, which are expected to have softened again in May following the Easter holiday driven spike in April. We'll also get plenty of numbers from the US this afternoon including jobless claims, Philly Fed manufacturing index and industrial production.

Daily Technical Analysis: EUR/USD Challenges 1.13 But Reverses With US Rate Hike

Currency pair EUR/USD

The EUR/USD challenged the key 1.13 resistance zone (red line) after weak inflation figures in the US were released yesterday. Despite the recent weakness in inflation levels, the US interest rates did increase from 1% to 1.25% later in the day which sparked a renewed US Dollar rally and hence a decline in the EUR/USD.

The EUR/USD is currently caught in between strong support and resistance and would need to break (arrows) these levels before a potential trend could start.

The EUR/USD wave 4 (blue) becomes unlikely if price manages to break above the 61.8% Fib level.

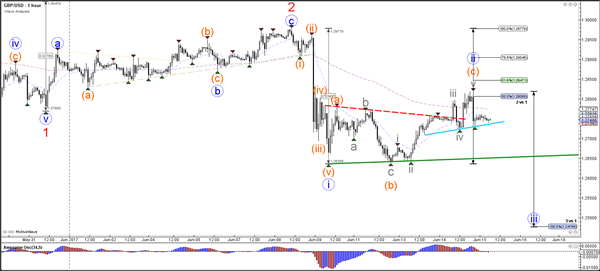

Currency pair GBP/USD

The GBP/USD has retraced to the 50% Fibonacci level of wave 2 (blue) via an ABC zigzag (orange). A bearish breakout (red arrows) could confirm wave 3 (red). The GBP/USD wave 2 is invalidated if price breaks (green arrows) above the 100% Fibonacci level.

The GBP/USD needs to break below support (blue/green) to confirm a potential wave 3 (blue). The Fibonacci levels of wave 2 (blue) could act as resistance.

Currency pair USD/JPY

The USD/JPY broke the support trend line (dotted blue) which has reopened the correction within wave B (brown). Price has reached the 88.6% Fibonacci level which is the last Fibonacci level of this wave B and a major bounce (green arrows) or break (red arrows) zone.

The USD/JPY needs to break above resistance (red) for a potential bullish trend or break below support (green) for a potential bearish trend.

Australian Unemployment Rate Hits Lowest Level Since 2013 In May

For the 24 hours to 23:00 GMT, the AUD rose 0.74% against the USD and closed at 0.7592.

LME Copper prices rose 0.5% or $25.5/MT to $5684.5/MT. Aluminium prices rose 0.5% or $9.5/MT to $1886.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7613, with the AUD trading 0.28% higher against the USD from yesterday's close, following an upbeat Australian jobs report.

Early morning data showed that Australia's seasonally adjusted unemployment rate unexpectedly eased to 5.5% in May, dropping to its lowest level in four years, driven by a rebound in fulltime positions. Markets expected unemployment rate to remain steady at 5.7%. Additionally, the number of people employed climbed by 42.0K in May, following a revised gain of 46.1K in the prior month, whereas investors had envisaged for a rise of 10.0K.

On the other hand, the nation's consumer inflation expectations dropped to 3.6% in June, compared to a reading of 4.0% in the previous month.

The pair is expected to find support at 0.7552, and a fall through could take it to the next support level of 0.7491. The pair is expected to find its first resistance at 0.7655, and a rise through could take it to the next resistance level of 0.7697.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Industrial Output Rose For The Second Consecutive Month In April

For the 24 hours to 23:00 GMT, the EUR slightly rose against the USD and closed at 1.1212.

On the macro front, the Euro-zone's seasonally adjusted industrial production advanced for the second straight month, after it rose 0.5% on a monthly basis in April, meeting market expectations and following a revised gain of 0.2% in the previous month.

Separately, Germany's final consumer price index (CPI) climbed 1.5% YoY in May, rising at its weakest pace in six months and confirming the flash estimate. The CPI had advanced 2.0% in the prior month.

The US Dollar clawed back some of its losses against a basket of currencies, after the Federal Reserve (Fed) raised interest rates for the second time this year and painted a rosier picture of the US economy.

The Fed, at its latest monetary policy meeting, raised its benchmark interest rate by a quarter percentage point to a target range of 1.00% to 1.25%, citing continued US economic growth and job market strength. Additionally, it indicated plans to pare back its $4.5 trillion balance sheet this year if the economy evolves as the central bank expects. In a post-meeting statement, the Fed judged that the recent weakness in economic data is temporary and maintained the outlook for one more rate hike this year but did not shed light on the timing of the rate hike.

Meanwhile, in its latest quarterly economic forecasts report, the central bank stuck to its outlook of three interest rate hikes in 2018. Moreover, policymakers slightly raised their economic growth forecast for this year to 2.1% but kept the estimates for 2018 and 2019 unchanged at 2.1% and 1.9% respectively. Inflation is expected to be at 1.7% by the end of this year, down from the 1.9% previously forecast.

Prior to the Fed interest rate decision, the greenback declined against its major peers, after the US inflation and retail sales data surprised with an unexpected drop.

The US CPI unexpectedly eased 0.1% on a monthly basis in May, suggesting that inflationary pressures in the world's largest economy are moderating. The CPI had registered a rise of 0.2% in the prior month, while markets expected it to record a flat reading. Further, the nation's advance retail sales surprisingly declined 0.3% MoM in May, defying market consensus for a flat reading. Advance retail sales had recorded a rise of 0.4% in the previous month. Further, the nation's business inventories fell 0.2% in April, at par with market expectations. In the previous month, business inventories had advanced 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.1218, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.1175, and a fall through could take it to the next support level of 1.1133. The pair is expected to find its first resistance at 1.1278, and a rise through could take it to the next resistance level of 1.1339.

Going ahead, market participants will keep a close watch on the Euro-zone's trade balance for April, slated to release in a few hours. Moreover, the US initial jobless claims, industrial as well as manufacturing production for May and NAHB housing market index for June, set to release later in the day, will keep investors on their toes.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

UK’s ILO Unemployment Rate Remained Steady At A 42-Year Low Level In The Three Months Through April

For the 24 hours to 23:00 GMT, the GBP rose 0.06% against the USD and closed at 1.2760, after UK's ILO unemployment rate remained steady at a 42-year low level of 4.6% in the three months ended April, meeting market expectations. However, the nation's average earnings including bonus advanced less-than-expected by 2.1% on an annual basis in the February-April 2017 period, rising at its slowest pace since February 2016, intensifying concerns about the outlook for consumers as inflation accelerates to a four-year high level. Markets anticipated average earnings to gain 2.4%, following a revised rise of 2.3% in the January-March 2017 period.

In the Asian session, at GMT0300, the pair is trading at 1.2747, with the GBP trading 0.1% lower against the USD from yesterday's close.

The pair is expected to find support at 1.2708, and a fall through could take it to the next support level of 1.2669. The pair is expected to find its first resistance at 1.2802, and a rise through could take it to the next resistance level of 1.2857.

Looking ahead, the Bank of England's (BoE) interest rate decision, due in a few hours, would possibly remain a low-key affair as the central bank is unlikely to be hawkish amid heightened political and economic uncertainty.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Japanese Yen Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.65% against the JPY and closed at 109.35.

In the Asian session, at GMT0300, the pair is trading at 109.56, with the USD trading 0.19% higher against the JPY from yesterday’s close.

The pair is expected to find support at 108.81, and a fall through could take it to the next support level of 108.07. The pair is expected to find its first resistance at 110.32, and a rise through could take it to the next resistance level of 111.09.

Moving ahead, traders would anxiously await the Bank of Japan’s (BoJ) monetary policy decision, scheduled tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Swiss Franc Trading A Tad Higher, Ahead Of SNB’s Interest Rate Decision

For the 24 hours to 23:00 GMT, the USD rose 0.26% against the CHF and closed at 0.9713.

In the Asian session, at GMT0300, the pair is trading at 0.9712, with the USD trading slightly lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9657, and a fall through could take it to the next support level of 0.9601. The pair is expected to find its first resistance at 0.9752, and a rise through could take it to the next resistance level of 0.9791.

Ahead in the day, investors will await the announcement of Swiss National Bank's (SNB) interest rate decision.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading Lower, Ahead Of Canada’s Existing Home Sales Data

For the 24 hours to 23:00 GMT, the USD traded flat against the CAD and closed at 1.3235.

On the data front, Canada's Teranet/National Bank house price index recorded a rise of 2.2% MoM in May. In the prior month, the index had climbed 1.2%.

In the Asian session, at GMT0300, the pair is trading at 1.3244, with the USD trading 0.07% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3182, and a fall through could take it to the next support level of 1.3121. The pair is expected to find its first resistance at 1.3288, and a rise through could take it to the next resistance level of 1.3333.

Looking ahead, Canada's existing home sales data for May, slated to release later in the day, will be on investors' radar.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.