Sample Category Title

Trade Idea Wrap-up: GBP/USD – Sell at 1.2850

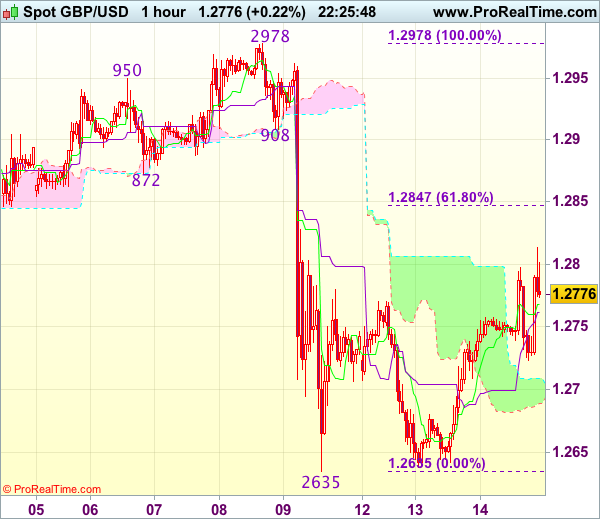

GBP/USD - 1.2772

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2768

Kijun-Sen level : 1.2761

Ichimoku cloud top : 1.2709

Ichimoku cloud bottom : 1.2689

Original strategy :

Sell at 1.2850, Target: 1.2750, Stop: 1.2885

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2850, Target: 1.2750, Stop: 1.2885

Position : -

Target : -

Stop : -

As the British pound has surged again after staged a strong rebound yesterday, suggesting further consolidation above last week’s low at 1.2635 would be seen and initial upside risk remains for gain to 1.2815-20, however, reckon 1.2845-50 (61.8% Fibonacci retracement of 1.2978-1.2635) would hold from here, bring retreat later, below 1.2720-25 would bring weakness to 1.2680-85 but break of latter level is needed to signal the rebound from 1.2635 has ended, then fall to 1.2650 would follow.

In view of this, we are looking to sell cable on recovery as 1.2845-50 should limit upside. Above 1.2870-80 would suggest recent decline has ended at 1.2635 instead, risk a stronger rebound to 1.2905-10 and possibly 1.2930 but price should falter well below resistance at 1.2978.

Trade Idea Wrap-up: EUR/USD – Buy at 1.1235

EUR/USD - 1.1278

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1247

Kijun-Sen level : 1.1244

Ichimoku cloud top : 1.1207

Ichimoku cloud bottom : 1.1199

Original strategy :

Buy at 1.1235, Target: 1.1335, Stop: 1.1200

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1235, Target: 1.1335, Stop: 1.1200

Position : -

Target : -

Stop : -

The single currency has rallied in US opening on dollar’s broad-based weakness and indicated resistance at 1.1285 was breached, adding credence to our bullish view that recent upmove has resumed, hence upside bias remains for further gain to previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 and later towards chart point at 1.1366.

In view of this, we are looking to turn long on pullback. Below 1.1195-00 would abort and prolong choppy trading below 1.1285, risk weakness to 1.1185, then towards said support at 1.1166 which is likely to hold from here.

CPI Inflation Softens Further Ahead of the FOMC Meeting

Missing expectations, headline and core CPI extended the recent deceleration of year-over-year trends. Today's softening performance may color today's FOMC policy statement and impact outlook projections.

Energy Weighs on the Headline

Following a 0.2 percent rise in April, the headline Consumer Price Index (CPI) missed expectations, slipping 0.1 percent in May - the second decline in three months. The primary driver of the headline's decline was a 2.7 percent contraction in energy prices, as a 6.4 percent drop in gasoline prices more than offset gains in electricity and natural gas (0.3 percent and 1.9 percent, respectively). Consumer food prices increased for the fifth consecutive month, up 0.2 percent.

Excluding food and energy, core CPI came in tamer than expected, rising just 0.1 percent on the month. Shelter costs increased 0.2 percent in May as the rent index and the index for owners' equivalent rent both advanced by a similar amount. This monthly performance was lower than that seen in April, but still keeps the year-over-year pace of shelter costs elevated above 3 percent. Several sectors within the core CPI contracted, tempering the aforementioned gains. Apparel dropped 0.8 percent, its third consecutive monthly decline, while airline fares, motor vehicles, communication and medical care services also posted lower readings. Medical care, education and recreation were all flat on the month.

Collectively, the trend of weakness in the core CPI continues. This is clearly evident in the three-month annualized pace which fell to a zero reading from 0.6 percent in April and a 3.0 percent pace in February. As seen in the middle chart, this deteriorating performance suggests that the annual pace of core CPI could continue to fall below its current two-year low of 1.7 percent in the coming months.

Still Enough for the Fed?

No doubt, the performance of consumer inflation has been soft relative to expectations at the start of the year. Year-over-year rates of headline and core CPI inflation have pulled back substantially in recent months, raising concerns over the likelihood of reaching the Fed's 2.0 percent target (note, the Fed's preferred measure of consumer inflation is the PCE deflator). Coming into today's CPI report and the June FOMC meeting, most Fed officials have characterized the softening inflation performance as "transitory." Interest will be high as to whether this assessment continues in the updated policy statement and with officials' inflation outlook. There is certainly now a higher probability that the Fed may include more dovish language in the policy statement over the current inflation performance as well as trim its inflation projections. A 25 bps federal funds rate hike is still expected at the conclusion of today's FOMC meeting, but clearly officials will be mindful of incoming inflation trends in the coming months before greater confidence can be made with second half of the year policy normalization plans.

Trade Idea Wrap-up: USD/JPY – Sell at 109.60

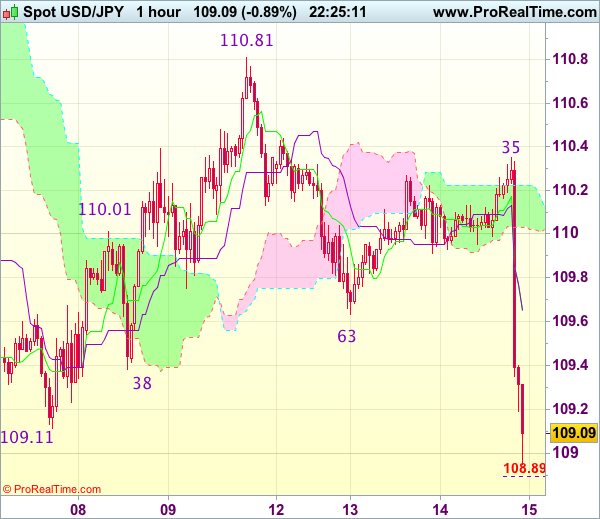

USD/JPY - 109.12

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 109.65

Kijun-Sen level : 109.65

Ichimoku cloud top : 110.22

Ichimoku cloud bottom : 110.03

Original strategy :

Sell at 109.70, Target: 108.70, Stop: 110.05

Position : -

Target : -

Stop : -

New strategy :

Sell at 109.60, Target: 108.60, Stop: 109.95

Position : -

Target : -

Stop : -

The greenback ran into renewed selling interest at 110.35 and has dropped sharply in NY morning, current breach of 109.63 and 109.38 support signal recent decline from 114.37 top has resumed an bearishness remains for this move to extend further weakness to 108.85-90 (1.236 times projection of 110.81-109.63 measuring from 110.35), however, near term oversold condition should limit downside to 108.40-45 (1.618 times projection) today and price should stay well above previous chart support at 108.13.

In view of this, we are looking to sell dollar on recovery as 109.63 (previous support turned resistance) should limit upside. Above 109.95-00 would defer and prolong consolidation but only break of resistance at 110.35 would signal an intra-day low is formed instead, bring another bounce to 110.50, then towards said resistance at 110.81.

Weak Retail Sales in May Explained by Low Gasoline Prices

Retail sales surprised in May by declining 0.3 percent with some of the decline coming from lower gasoline prices. However, the weakness was not circumscribed only to gasoline sales.

Retail Sales Hit Hard by Gasoline and Electronic Stores

Retail and food services sales for May declined 0.3 percent versus expectations of a flat reading after an increase of 0.4 percent in April, unrevised. Most of the decline came from a 2.4 percent drop in gasoline sales as gasoline prices decreased during the month. However, the May report was weak overall, which means that other sectors were not able to overcome the weakness in gasoline sales. The largest month-on-month drop was reported in electronics & appliances stores sales with a decline of 2.8 percent. However, this sector is much smaller than gasoline sales, which makes the decline less impactful on the overall retail sales number. Meanwhile, motor vehicles & part dealers' sales were down 0.2 percent after a strong, 0.5 percent increase in April.

Interestingly enough, clothing & clothing store sales, a sector that has been weak in the past several years, posted a growth rate of 0.3 percent after an increase of 0.2 percent in April. Sales of sporting goods, hobby, book and music stores were down 0.6 percent in the month after increasing 0.4 percent in April while sales at general merchandise stores were down 0.3 percent. Within this last sector, department stores sales were down 1.0 percent, continuing the trend we have seen over the last several years.

Bucking the weak trend in May were sales of non-store retailers increasing 0.8 percent after a strong 0.9 percent increase in April and furniture & home furniture stores, up 0.4 percent after a decline of 0.3 percent in April. Meanwhile, building material & garden equipment & supplies dealers' sales took a breather in May, as they remained flat after an increase of 0.6 percent in April.

The service side of the retail report, food services & drinking places, was also weak during the month, declining 0.1 percent after a decline of 0.2 percent in April. However, the goods cousin of this sector, food & beverage store sales, was up 0.1 percent in May. Meanwhile, health and personal care store sales were flat in May after increasing strongly, up 0.8 percent, in April.

Control Group Sales Flat in May

Although control group retail sales, which go directly into the calculation of GDP, were flat in May, they were revised up strongly in April, from an original print of 0.2 percent to an increase of 0.6 percent, which means that the second quarter of the year started on a relatively strong footing for personal consumption expenditures (PCE).

Furthermore, the fact that the retail report is in nominal terms while inflation has been slowing down considerably will help real numbers remain strong during the second quarter of the year. While this does not help retailers wanting more revenues, it will help real economic activity during the second quarter of the year.

Trade Idea: EUR/GBP – Buy at 0.8690

EUR/GBP - 0.8831

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Buy at 0.8750, Target: 0.8880, Stop: 0.8710

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8690, Target: 0.8880, Stop: 0.8650

Position : -

Target : -

Stop : -

Euro’s retreat after marginal rise to 0.8866 earlier this week suggests consolidation below this level would be seen and pullback to 0.8745-50 cannot be ruled out, however, reckon 0.8690-00 would attract renewed buying interest and bring another rise later, above said resistance would extend recent erratic upmove from 0.8304 low to 0.8880, then 0.8900, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000, bring retreat later this week.

In view of this, we are looking to buy euro on subsequent pullback but one should exit on such rise. Below 0.8680 would defer and risk test of 0.8650-55 support but break there is needed to signal top is formed instead, bring further fall to 0.8620, then 0.8600 which is likely to hold from here.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

EURUSD Approaching *TRUMP* Levels; Will EURUSD Fall or Become Stronger?

Traders welcome back for the US updates. We can see nice move up on EURUSD towards 1.13000 after some bad US data. It appears that euro may hit a new high here, but again there is an important "Trump Level" coming in at 1.13 from Nov 09 2016 when Trump won the US elections. Back then 1.13 played out an important role from where price fell sharply so it appears that it will be tested during another important event; FOMC because of a potential new change in rates. technically speaking a decline may follow after the FED today, especially if our new count will prove correct; an ending diagonal which remains valid as long as 1.1350 is not breached.

EURUSD,1H

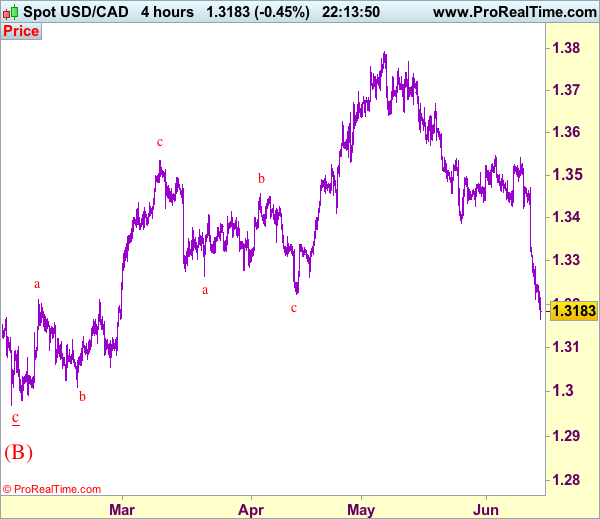

Trade Idea: USD/CAD – Sell at 1.3330

USD/CAD - 1.3182

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Sell at 1.3330, Target: 1.3130, Stop: 1.3390

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3330, Target: 1.3130, Stop: 1.3390

Position: -

Target: -

Stop:-

The greenback has remained under pressure after recent anticipated selloff, adding credence to our bearish view that top has been formed at 1.3794 earlier and downside bias remains for the decline from there to extend weakness to 1.3130-40, then towards 1.3100, however, near term oversold condition should limit downside today and reckon previous support at 1.3078 would remain intact, risk from there has increased for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell again on subsequent recovery as 1.3330-40 should limit upside. Above previous support at 1.3387 (now resistance) would defer and suggest low is possibly formed, bring a stronger rebound to 1.3420-25 but break there is needed to provide confirmation.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Poor US Data Put Dollar Under Pressure ahead of the Fed

- Treasuries rallied and the dollar weakened after data, showing US inflation cooled and retail sales contracted last month, signalled uneven economic growth as the Federal Reserve is set to deliver its latest rate decision. Stocks continued to stabilize after a two-day tech selloff, with European and emerging-market equities advancing.

- US inflation surprised on the downside. Headline CPI fell 0.1% M/M and eased to 1.9% Y/Y from February's peak of 2.7% Y/Y. Core CPI rose a tiny 0.1% M/M, but dropped to 1.7% Y/Y from 2.3% Y/Y in January. PCE inflation, the Fed's favourite inflation gauge which is generally lower than CPI, will probably also move further away from the 2% target.

- May headline retail sales dropped 0.3% M/M (vs 0% M/M expected). Car sales and gasoline were the culprits, as core retail sales were flat (vs. 0.3% M/M expected). April sales were revised higher to 0.5% M/M from 0.3% M/M. We saw a similar picture for the control group (important for GDP calculation), with a flat May figure which was compensated by a strong upward revision to 0.6% M/M in April.

- A fall of 0.4% in wage growth in the three months to April represented the biggest loss of real earnings for UK households since 2014. Wages are failing to pick up despite a robust labour market. Unemployment fell by 50,000 between February and April, leaving the jobless rate at a 42-yr low of 4.6%, and the number of people in work climbed 109,000 to a record 32 million.

- EMU industrial output grew in April (0.5% M/M) and employment rose in the first quarter of the year (0.4% Q/Q) to reach a record high, in fresh signs of healthy growth of the bloc's economy. In absolute terms, 154.8 million people were employed in EMU in Q1, surpassing the previous peak of Q1 2008.

- ECB Weidmann highlighted the risks of continuing extraordinarily expansive monetary policy for too long. According to Weidmann, sovereign bond purchases muddy the waters between monetary and fiscal policy. "This can lead to political pressure being exerted on the euro-system to maintain the very accommodative monetary policy for longer than appropriate from a price stability standpoint," Weidmann said

- The global oil glut is here to stay through 2017 as OPEC's efforts to restrain petroleum production have hit a wall in the US, the IEA said in its closely watched monthly oil report. The world's vast levels of stored oil, a proxy for the global oversupply, grew to 292 million barrels in April in industrialized nations, higher than the 5-yr average.

Rates

Softer US inflation and retail sales send bonds higher

Ahead of the FOMC decision, markets usually trade uneventful. Today's session was exceptional, due to the release of weak US eco, data. For the third month in a row, inflation surprised on the downside and declined. Headline and core inflation are dropping further below the 2% target, which suggests that the (core) PCE deflators, the Fed inflation targets, which are structurally lower than CPI, will drop too. Some governors already showed concern about the direction of inflation and these figures only add to the argument. The expected rate hike today will probably pass, but more of these figures clearly question the Fed's projected rate path and even the start of the balance sheet tapering which will normally be initiated later this year. The Bund auction was weak, but in line with recent average.

US Treasuries shot higher after the data, pushing yields substantially lower to key support. The monetary policy sensitive belly of the curve outperformed. In other markets, the dollar was heavily sold with main dollar supports under test. US (and European ) equities were higher ahead of the release, but are off the lows.

Later today, the FOMC renders its decisions. A 25 bps rate hike by the Fed is completely discounted, but markets' expectations about the continuation of the tightening cycle are extremely low (even lower after today's data releases). We expect the Fed to pencil in another rate hike this year and 3 hikes in 2018. The 2019 median forecast could be lowered slightly. Holding on to the blueprint of the rate path in combination with official communication about starting the BS run-off in H2 2017 should confirm last week's technical bottoming out on US yield markets (failed tests 5-y (1.69%), 10-yr (2.17%) and 30-yr (2.82%) and could start a new up-leg in yields. Of course today's data seam doubts about these expectations which we've put forward this morning. Yellen's comments today will be even more important than usual.

At the time of writing, the German yield curve flattened with yield changes ranging from +1.1 bp (2-yr) to -4 bps (30-yr). The belly of the US yield curve shifts about 7.5 bps higher and the wings 6 bps. Spread narrowing on EMU bond markets continued with Spain and Italy narrowing 4/5 bps at the 10-yr tenor versus Germany and Portugal even 10 bps.

Currencies

Poor US data put dollar under pressure ahead of the Fed

Today, major dollar cross rates initially held tight ranges. However, the USD-lethargy was brutally interrupted after weaker than expected US retail sales and CPI. USD/JPY dropped from the 110 area to the 109.30 area. EUR/USD trades in the 1.1275 area, nearing the key 1.1300/66 resistance. The currency market is clearly positioned for a soft Fed. Will the Fed go in the direction of the market?

Overnight, Asian equities traded mixed despite yesterday's WS rebound. China underperformed, despite Chinese data coming out close to expectations. USD/JPY held a tight range near 110. EUR/USD did go nowhere in the 1.12 area.

This morning in Europe, EUR/USD and USD/JPY stayed in a wait-and-see modus. EUR/USD was paralysed in the 1.12 area. USD/JPY profited slightly from a stronger equities, moving from the 110 to the 110.30 area.

In the US, usually investors are reluctant to react to data just hours before a Fed policy decision. However, both series again missed the consensus by a wide margin. The data added to uncertainty whether the Fed would be able to maintain its policy normalisation path. US yields nosedived and so did the dollar. EUR/USD jumped to the mid 1.1275 area. The recent top and the 1.1300/66 resistance are on the radar. USD/JPY slipped to the 109.25 area. The focus now turns the Fed policy decision, the dot plot and Yellen's press conference. The (FX) market is positioned for a soft Fed assessment. Our working hypothesis was that the Fed wouldn't give too much weight to recent softer data. In that scenario, the EUR/USD 1.1300/66 resistance looked quite tough. This hypothesis could be challenged if the market would hesitate about the Fed's normalisation campaign. USD/JPY and the trade-weighted dollar are also nearing important support levels.

Poor wage data halt sterling rebound (against the euro)

This morning, the yesterday's sterling rebound continued. EUR/GBP dropped to the 0.8766 area. Cable filled offers just below 1.28. The rebound was aborted by the publication of the UK labour data. The unemployment rate stabilized at 4.6%. Employment growth was slightly softer than expected but especially wage growth data posted again a big miss. Average weekly earnings declined from 2.3% Y/Y to 2.1% Y/Y (ex Bonus even from a downwardly revised 1.8% Y/Y to 1.7% Y/Y, 2.0% was expected). So, taking the May inflation jump into account, real earning are declining fast. The combination of high political and economic uncertainty and low wage inflation will probably will make the BoE prioritize growth over inflation when setting monetary policy. At the same time, UK PM May made no noticeable progress in finding support for its minority government. EUR/GBP reversed the early decline and returned to the 0.88 area. Cable dropped to 1.2725/40 area, but jumped back to the 1.28 area as the dollar was hammered after disappointing US data.

Slower-than-Expected US Inflation Won’t Affect the Fed’s Decision Later Today

Highlights:

- The all items index unexpectedly fell 0.1% in May to bring the year-over-year rate down to 1.9% from 2.2% in April.

- Energy price inflation moderated to 5.4% year-over-year as gasoline prices fell for the third time in four months.

- A 0.2% monthly rise in food prices provided some offset in May as that component continued to emerge from a period of deflation late last year.

- The year-over-year rate of inflation excluding food and energy fell to 1.7% from 1.9%, the slowest rate in more than two years.

- Core prices have been roughly flat over the last three months, the weakest streak since 2010. Falling goods prices and weaker-than-usual services inflation have both been factors.

- Some transitory factors have been at play, including a decline in the price of wireless phone services, though underlying inflation does appear to have moderated in recent months.

Our Take:

US inflation fell short of expectations for a third consecutive month in May. We don't see today's shortfall impacting the Fed's decision to raise rates this afternoon, a move that is universally expected and fully priced in by markets. But the recent moderation in inflation could lend a more dovish tone to Chair Yellen's press conference. Minutes of the Fed's May meeting indicated most participants "viewed the recent softer inflation data as primarily reflecting transitory factors". However, a further decline in core inflation and less upward pressure from energy prices should leave the Committee less comfortable with that view. Continued moderation in market-based measures of inflation expectations, now back at pre-election levels, could also have some bearing. Offsetting slower inflation is further tightening in labour market conditions that indicates limited slack in the economy and the potential for price pressure to pick up going forward. With that in mind, we expect the Fed will take the long view on inflation and continue to signal that a gradual withdrawal of accommodation is appropriate beyond today's move.