Sample Category Title

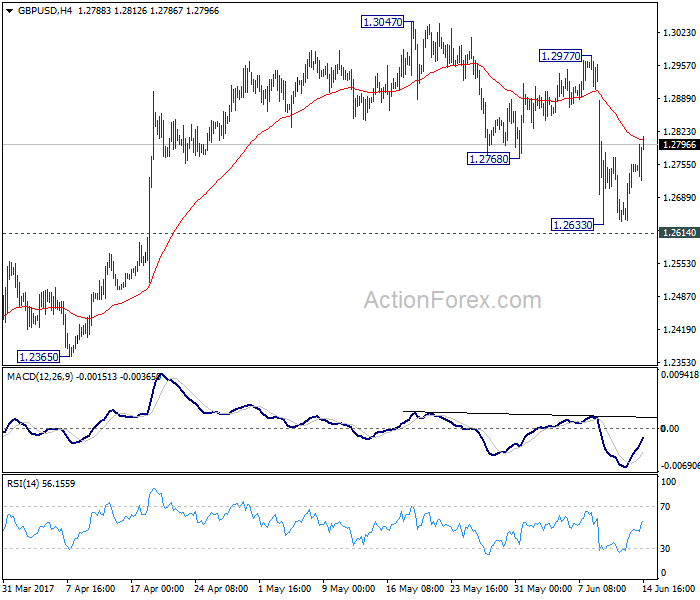

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2676; (P) 1.2716; (R1) 1.2791; More...

GBP/USD's rebound from 1.2633 continues today but still, intraday bias remains neutral first. Upside is expected to be limited below 1.2977 resistance to bring fall resumption. We continue to favor the case that consolidation pattern from 1.1946 has completed at 1.3047 already. Decisive break of 1.2614 resistance turned support would confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2977 will dampen our view and turn bias back to the upside for 1.3047 and above.

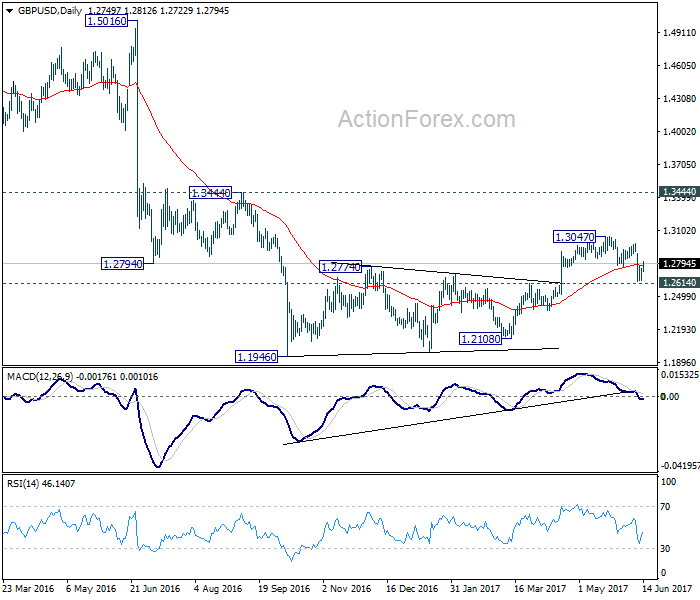

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

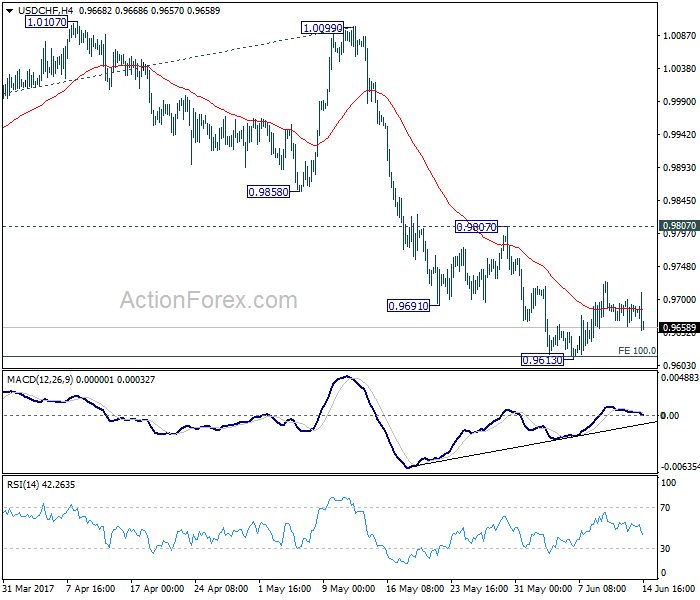

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9672; (P) 0.9683; (R1) 0.9697; More.....

USD/CHF weakens in early US session but stays above 0.9613. Intraday bias remains neutral first. As long as 0.9807 resistance holds, outlook remains cautiously bearish and deeper fall is expected. Break of 0.9613 will extend the whole decline from 1.0342 to 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

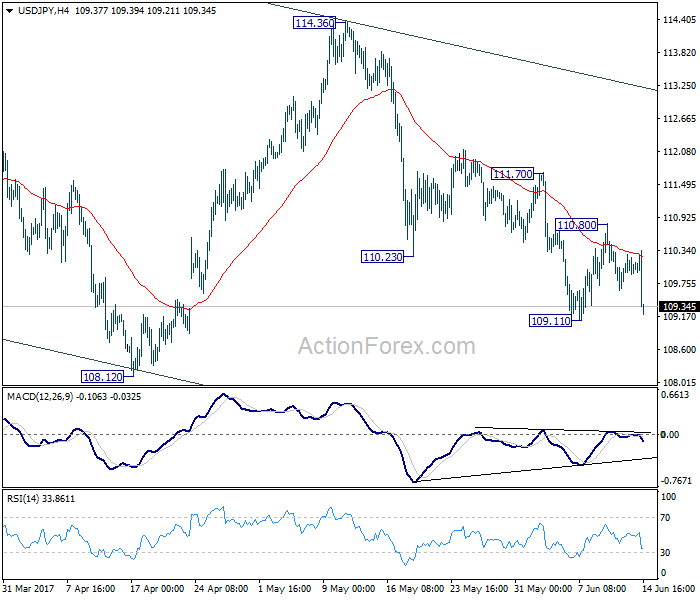

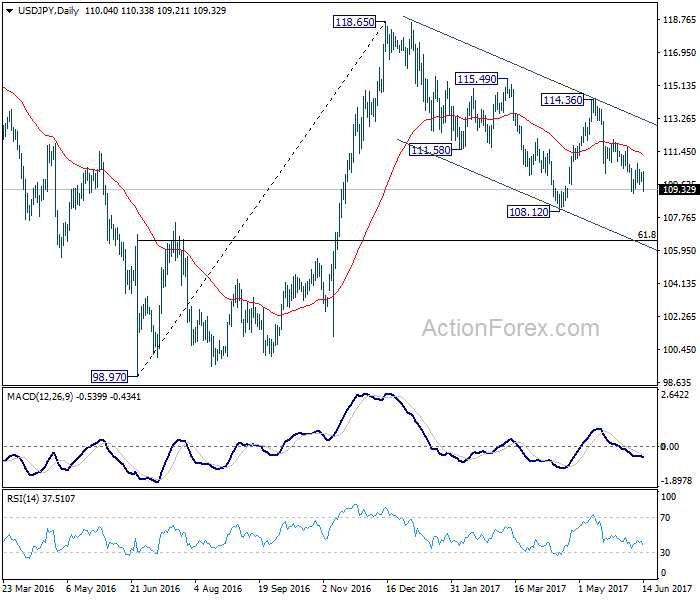

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.56; (P) 109.99; (R1) 110.37; More...

USD/JPY drops sharply in early US session but stays above 109.11 temporary low. Intraday bias remains neutral first. Near term outlook stays bearish with 111.70 resistance intact and further decline is expected. Break of 109.11 will resume the fall from 114.36 and target 108.12 low first. Break will extend the whole corrective fall from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. We will look for bottoming sign there. Meanwhile, break of 110.70 will indicate near term reversal and turn bias back to the upside for 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

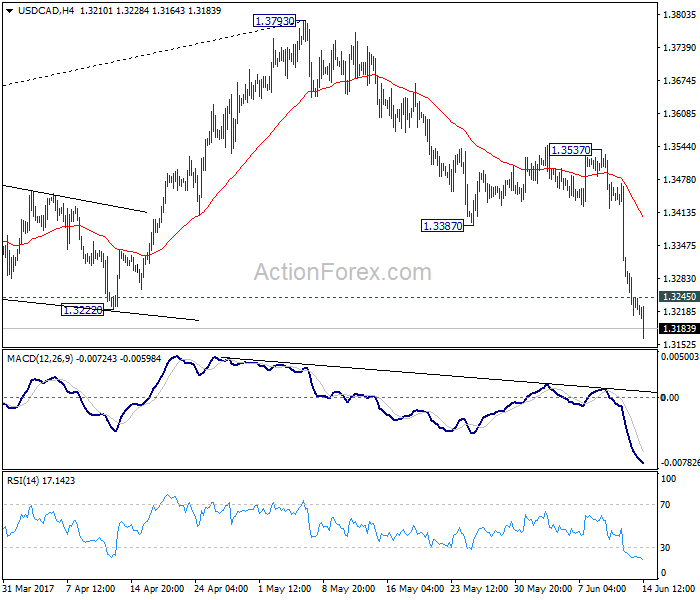

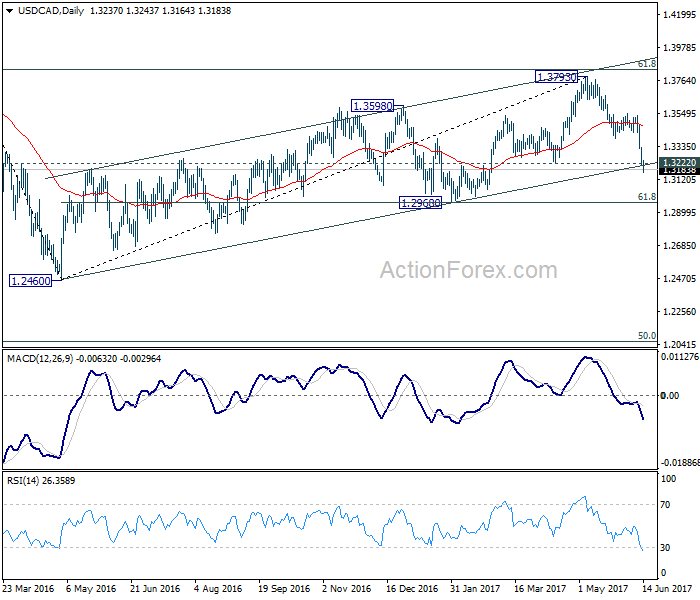

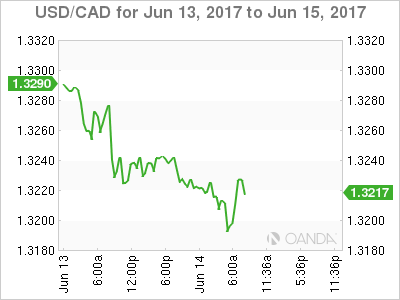

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3193; (P) 1.3259; (R1) 1.3306; More....

USD/CAD's decline continues today and reaches as low as 1.3164 so far. The strong break of 1.3222 support as well ass the medium term channel support affirms our bearish view. That is, corrective rise from 1.2460 has already completed at 1.3793. Intraday bias stays on the downside for next key level at 1.2968 (38.2% retracement of 1.2460 to 1.3793 at 1.2969). On the upside, above 1.3245 minor resistance will turn bias neutral and bring consolidations. But upside should be limited by 1.3387 support turned resistance and bring fall resumption.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.

Dollar Selloff Resumes after Poor CPI and Retail Sales, Vulnerable on FOMC Dovish Hike

Dollar is under some renewed selling pressure in early US session after poor economic data. Headline CPI dropped -0.1% mom, rose 1.9% yoy in May. The annual rate was notably slower than prior month's 2.2% and missed expectation of 2.0%. Core CPI rose 0.1% mom, 1.7% yoy. The annual rate was also slower than prior month's and expectation of 1.9% yoy. Headline retail sales dropped -0.3% in May, below expectation of 0.1%. Ex-auto sales dropped -0.3% versus expectation of 0.2%. The weakness against Canadian Dollar is particularly clear as USD/CAD is now clearing 1.3222 key near term support firmly. There is prospect of EUR/USD revisiting 1.1298 key resistance level even before FOMC announcement.

Talking about Fed, it's widely expected to raise federal funds rate by 25bps to 1.00-1.25% today. The base case for this year "was" that Fed will hike a total of three times, with another one in September, and then start shrinking its balance sheet in December. But there are doubts on whether the economy could withstand that recently. Today's set of data adds much to such worries. The new economic projections to be released today with the rate announcement are key to market expectations. That includes growth and inflation forecasts (with unemployment forecast a little less important), as well as the so called dot plot interest rate projections. In addition to that, the vote split will be closely watched to see how divided the committee is. Meanwhile, technically, we'd maintain the view that should EUR/USD takes out 1.13 handle decisively, selloff in Dollar will likely accelerate.

Former PM urges May on softer Brexit

In UK, former Prime Minister David Cameron urged Prime Minister Theresa May to "consult more widely with the other parties on how best we can achieve" success in the Brexit negotiation with EU. He noted there "will be pressure for a softer Brexit" and the parliament "deserves a say" on managing the Brexit process. Separately another former Prime Minster John Major said that "the concept of what we crudely call a hard Brexit is becoming increasingly unsustainable." And, "a hard Brexit was not endorsed by the electorate in this particular election." Theresa May said yesterday that the Brexit negotiation will formally start next week as scheduled.

Released from UK, claimant counts rose 7.3k in May, below expectation of 10.0k. ILO unemployment rate was unchanged at 4.6% in April. But average weekly earnings rose 2.1% 3moy, below expectation of 2.4% 3moy.

France and Germany open if UK changes mind

French President Emmanuel Macron said that the "doors remains open" if UK is to change their mind about Brexit. And it's "always open until the Brexit negotiations come to an end. But he emphasized that its a "a sovereign decision was taken by the British people and that is to come out of the European Union, and I very much respect the decisions taken by the people, be it by the French people or the British people." And, "once the negotiations have started we should be well aware that it'll be more difficult to move backwards." Comments of Macron echoed those of German Finance Minister Wolfgang Schaeuble that "if they want to change their decision, of course they would find open doors, but I think it's not very likely."

Released from Eurozone, industrial production rose 0.5% mom in April, employment grew 0.4% qoq in Q1. German CPI was finalized at 1.5% yoy in May.

IMF raised China growth forecasts but urged reforms

The International Monetary Fund raised its growth forecast for China to 6.7% this year, up from 6.6% in April. For the period from 2018 to 2020, IMF now projects China's growth to be averaged at 6.4% annually. That's also an upward revision from April forecast of average 6.2%. At the same time, IMF urged China to speed up actions on debt and reforms. The fund's First Deputy Managing Director David Lipton said in a statement that "while some near-term risks have receded, reform progress needs to accelerate to secure medium-term stability and address the risk that the current trajectory of the economy could eventually lead to a sharp adjustment. And, "it is critical to start now while growth is strong and buffers sufficient to ease the transition."

Released from China, industrial production rose 6.5% yoy in May, fixed assets investments rose 8.6% yoy, retail sales rose 10.7% yoy. Staying Asian Pacific, Japan industrial production was finalized at 4.0% mom in April. Australia Westpac consumer confidence dropped -1.8% in June. New Zealand current account balance turned into NZD 0.24b surplus in Q1.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3193; (P) 1.3259; (R1) 1.3306; More....

USD/CAD's decline continues today and reaches as low as 1.3164 so far. The strong break of 1.3222 support as well ass the medium term channel support affirms our bearish view. That is, corrective rise from 1.2460 has already completed at 1.3793. Intraday bias stays on the downside for next key level at 1.2968 (38.2% retracement of 1.2460 to 1.3793 at 1.2969). On the upside, above 1.3245 minor resistance will turn bias neutral and bring consolidations. But upside should be limited by 1.3387 support turned resistance and bring fall resumption.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account Balance Q1 | 0.24B | 1.00B | -2.34B | -2.42B |

| 00:30 | AUD | Westpac Consumer Confidence Jun | -1.80% | -1.10% | ||

| 02:00 | CNY | Retail Sales Y/Y May | 10.70% | 10.80% | 10.70% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y May | 8.60% | 8.80% | 8.90% | |

| 02:00 | CNY | Industrial Production Y/Y May | 6.50% | 6.50% | 6.50% | |

| 04:30 | JPY | Industrial Production M/M Apr F | 4.00% | 4.10% | 4.00% | |

| 04:30 | JPY | Capacity Utilization M/M Apr | 4.30% | -1.60% | ||

| 06:00 | EUR | German CPI M/M May F | -0.20% | -0.20% | -0.20% | |

| 06:00 | EUR | German CPI Y/Y May F | 1.50% | 1.50% | 1.50% | |

| 08:30 | GBP | Jobless Claims Change May | 7.3K | 10.0K | 19.4K | 22.0K |

| 08:30 | GBP | Claimant Count Rate May | 2.30% | 2.30% | ||

| 08:30 | GBP | ILO Unemployment Rate 3M Apr | 4.60% | 4.60% | 4.60% | |

| 08:30 | GBP | Average Weekly Earnings 3M/Y Apr | 2.10% | 2.40% | 2.40% | 2.30% |

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 0.50% | 0.50% | -0.10% | |

| 09:00 | EUR | Eurozone Employment Q/Q Q1 | 0.40% | 0.30% | 0.30% | |

| 12:30 | USD | CPI M/M May | -0.10% | 0.00% | 0.20% | |

| 12:30 | USD | CPI Y/Y May | 1.90% | 2.00% | 2.20% | |

| 12:30 | USD | CPI Core M/M May | 0.10% | 0.20% | 0.10% | |

| 12:30 | USD | CPI Core Y/Y May | 1.70% | 1.90% | 1.90% | |

| 12:30 | USD | Advance Retail Sales May | -0.30% | 0.10% | 0.40% | |

| 12:30 | USD | Retail Sales Less Autos May | -0.30% | 0.20% | 0.30% | |

| 14:00 | USD | Business Inventories Apr | 0.30% | 0.20% | ||

| 14:30 | USD | Crude Oil Inventories | 3.3M | |||

| 18:00 | USD | FOMC Rate Decision | 1.25% | 1.00% |

EURUSD: Sees Price Hesitation With Downside Bias

EURUSD: With the pair continuing to hesitate, a move lower on correction is envisaged. Resistance comes in at 1.1250 level with a cut through here opening the door for more upside towards the 1.1300 level. Further up, resistance lies at the 1.1350 level where a break will expose the 1.1400 level. Conversely, support lies at the 1.1150 level where a violation will aim at the 1.1100 level. A break of here will aim at the 1.1050 level. All in all, EURUSD faces further pullback threats in the days ahead.

DAX Jumps Ahead of Expected Fed Rate Hike

The DAX index has posted strong gains in the Wednesday session, and has climbed 0.97 percent. The index is currently at 12,892.50 points. On the release front, German Final CPI declined 0.2%, well off the forecast of a 0.5% gain. Employment Change climbed 0.4%, edging above the estimate of 0.3%. Eurozone Industrial Production climbed 0.5%, matching the estimate. There are a number of key events in the US, highlighted by the Federal Reserve rate announcement. As well, the US will release retail sales and CPI reports.

The markets are awaiting the Federal Reserve rate announcement later on Wednesday. The markets have priced in a rate hike at close to 100%, so it's a given that the Fed will increase rates by 25 basis points, to 1.25%. What is less clear, however, is what the Fed has planned in the second half of 2017. Analysts are expecting a "dovish hike", meaning that together with the rate increase, the Fed rate statement will be cautious in tone, and dovish regarding additional rate hikes. Earlier in the year, three rate hikes in 2017 seemed almost a given, but currently, the odds of a September move are just 28%. There are two items which could affect the movement of the dollar. First, the Fed Economic Projections will detail forecasts of inflation, growth and unemployment, and most importantly, the rate hike path. With the US economy performing better in the second quarter, there's a strong likelihood that the Fed will not moderate its rate hike projections,which is good news for the dollar. Secondly, the markets will be looking for details regarding its plan to lower the $4.2 trillion balance sheet. If the Fed outlines a plan to reduce its holding in H2, the dollar could respond positively. Another variable is the political paralysis which has engulfed Washington. With the Trump administration spending most of its energy on damage control, little progress is being made with regard to Trump's agenda of tax reform and major spending on infrastructure. The markets are becoming more skeptical about Trump's ability to work with Congress, and if this sentiment is shared by the Fed, it is likely to sound dovish regarding rate hikes in September or December.

Dollar to be Dot Plot Driven

Wednesday June 14: Five things the market is talking about

Soft U.S inflation data is raising market uncertainty about the Fed's policy plans for the rest of the year. Will Fed Chair Janet Yellen clarify their outlook this afternoon?

The Fed is widely expected to agree on an interest-rate increase today (2:00pm EDT) at the conclusion of its two-day meeting. U.S policy makers will probably also acknowledge recent inflation declines, while sticking to previous guidance for another hike before year-end and a first step towards unwinding its +$4.5T balance sheet.

Note: Fed officials have said for months they were discussing how to reduce the balance sheet, and last month outlined a proposed approach that would let increasing amounts of securities mature over time.

Any 'dot plot' downshift would definitely cast doubt on the Fed hiking three times in 2017.

Ahead of the U.S open, the 'mighty' dollar has weakened for a third consecutive day, Treasury prices have edged a tad higher and global equity markets are mixed.

Note: Bank of Japan (BoJ), Swiss National Bank (SNB) and Bank of England (BoE) are also scheduled to weigh in with policy decisions this week.

1. Global equities mixed performance

In Japan, stocks ended marginally lower in choppy trade overnight, as investors abstained from taking positions ahead of the Fed's rate announcement. The Nikkei share average fell -0.1%, while the broader Topix Index also closed down -0.1%.

Down-under, Australia's S&P/ASX 200 Index climbed +1.1% to its highest print since mid-May.

In China, the Shanghai Composite Index tumbled -0.8% and the CSI 300 Index dropped -1.3%, its biggest loss this year.

In Hong Kong, the Hang Seng Index pared losses, up +0.1%, while in South Korea the Kospi Index fell -0.1%.

In Europe, indices trade modestly higher following on from yesterday's rebound stateside. The French CAC is the out performer, whilst the FTSE MIB (Italy) again lags.

U.S stocks are expected to open little changed.

Indices: Stoxx50 +0.6% at 3578, FTSE +0.3% at 7527, DAX +0.4% at 12820, CAC-40 +0.9% at 5306, IBEX-35 +0.1% at 10896, FTSE MIB +0.1% at 21107, SMI +0.3% at 8897, S&P 500 Futures flat

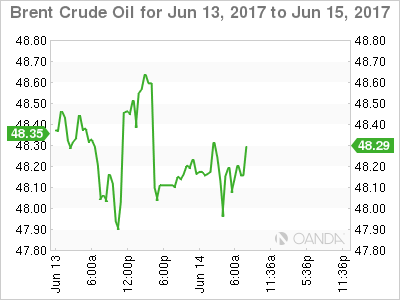

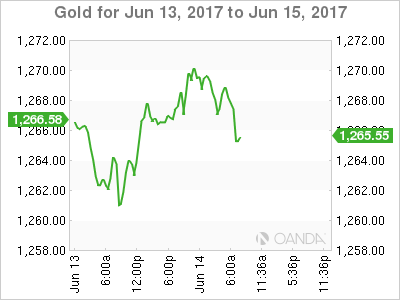

2. Oil prices fall as OPEC output, U.S crude stockpiles rise, gold unchanged

Ahead of the U.S open, oil prices are under pressure after industry data yesterday revealed a build in U.S crude stocks and OPEC reported a rise in its production despite a pledge to cut output.

Brent crude oil is down -45c a barrel at +$48.27, while U.S light crude (WTI) is -50c lower at +$45.96.

Note: Crude prices have fallen more than -10% since late May, pulled down by heavy global oversupply that has persisted despite a move led by OPEC to curb production.

Oil stocks are near record highs in some parts of the world, and producers that are not part of the OPEC deal are increasing output.

API data yesterday showed that U.S crude stocks rose by +2.8m barrels in the week to June 9 to +511.4m, compared with expectations for a decrease of -2.7m barrels.

According to BP data yesterday, global energy demand grew by +1% in 2016, a rate similar to the previous two years, but well below the 10-year average of +1.8%.

The market will take its cues from today EIA report at 10:30 am EDT.

Spot gold is little changed ahead of the Fed rate announcement (+0.1% at +$1,267.05 per ounce). Yesterday, the yellow metal touched its weakest price since June 2 at +$1,259.16.

3. Yields require Fed guidance

U.S equities continue to climb, yields have fallen (U.S 10's at +2.21%) and volatility remains low, despite recent Fed rate increases and plans for more.

Note: A Fed board whitepaper estimated that the expansion of Fed bond holdings since the crisis likely lowered the yield on the benchmark 10's by a percentage point from where it would otherwise have been. By 2023, the paper said, the yield would still be about -25 bps lower despite an anticipated shrinkage in the balance sheet.

The Fed's portfolio of assets has grown to +$4.5T from around +$800B before the crisis through a series of bond-buying programs aimed at lowering long-term interest rates. Allowing these assets to roll off is expected to push up long-term rates.

Market volatility has been well contained thus far, but is expected to pick up when fixed income dealers knows when the Fed will begin the process of reducing its balance sheet, the pace and the likely size of the balance sheet at the end.

Elsewhere, U.K, Germany and French benchmark yields all rose +1 bps, while the Aussie benchmark yield is little changed at +2.40%.

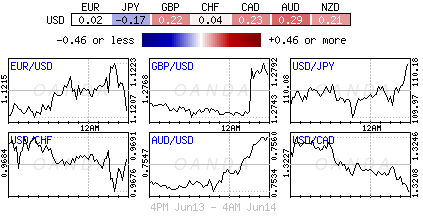

4. Dollar small under pressure

It comes as no surprise that the FX market is relatively steady ahead of the expected interest rate hike by the Fed.

The dollars next step will depend on what clues Ms. Yellen will serve up regarding the Feds policy for the rest of this year.

USD/CAD (C$1.3198) continues to trend lower, trading atop of its two-month lows following 'hawkish' comments from Bank of Canada's Deputy Governor Carolyn Wilkins Monday and Governor Poloz yesterday pointing out that the central bank may consider curtailing its accommodative monetary policy in view of the broadening economic growth.

GBP (£1.2745) is off its overnight highs, but is supported now that PM May seems to have secured the support of the DUP to form a working government. U.K wage data (see below) registered a lower reading for the second consecutive month hindered some of the pounds progress. Sterling 'bulls' believes that last week's snap election results have reduced the odds for a "hard" Brexit actually occurring is also supporting the pound. The Bank of England (BoE) rate announcement is due Thursday, no change is expected.

5. UK Real Wages Fall Again, China sales improve

Data this morning showed that the U.K. unemployment rate held steady in the three months to April, but regular wages adjusted for inflation fell on the year for the second consecutive month, suggesting accelerating inflation is squeezing British shoppers' wallets.

The unemployment rate stood at +4.6% - the lowest rate since mid-1975 - but real wages fell by -0.6% compared to the same period last year. Inflation stood at +2.9% in May, the fastest pace of price growth in nearly four-years.

In China, retail sales rose +10.7% y/y in May, in line with consensus, while industrial production was up +6.5% vs. an expected +6.4% gain.

GBPJPY Bearish Below 50-day Moving Average and Beneath Cloud

GBPJPY is in a downtrend since the May 10 high of 148.09, with prices falling in a descending channel and touching a low of 138.65 this week. The short-term bias turned more bearish after breaking below the 50-day moving average last week. The market is now holding below the base of the daily Ichimoku cloud, giving a bearish setup. Prices are also capped under the tenkan-sen line. Meanwhile, momentum studies are also bearish, since RSI is below 50 and MACD is below zero.

In the near-term, GBPJPY is finding support from the 200-day moving average at 138.87 and is finding resistance at 140.36 and has not recorded a daily close above it in the past two days. This level is the 61.8% Fibonacci retracement level of the upleg from 135.58 (April 17) to 148.09 (May 10).

The market is now at a critical point. If support at the 200-day moving average fails to hold, then there would be an accelerated decline towards the 135.58 (April 17). At this point, the market would have retraced all of the uptrend from 135.58 to 148.09, and a deeper decline would strengthen the bearish outlook for the medium-term picture.

A rise above the June 2 high of 143.93 (top of the cloud) is needed to shift momentum back to the upside to target resistance at the 23.6 Fibonacci at 145.14. A move above 147.00 would help bring a resumption of the April to May uptrend.

For now the short-term bias is bearish within the descending channel, while the medium-term picture is neutral since the beginning of the year.

Technical Outlook: Pound Falls To The Session Low On Profit-Taking, Disappointing UK Data

Recovery rally stays capped under daily cloud top where today’s extension of Tuesday’s strong bounce stalled. Profit-taking on two-day rally and disappointing data from UK pushed pound to the session low at 1.2724 and sidelined immediate risk of breaking above pivotal 1.2800 resistance zone.

Average earnings fell to 2.1% in April, missing the forecast at 2.4% and falling below downward-adjusted 2.3% numbers of March.

Stubbornly low wages underscore growing Brexit squeeze and are seen as a warning signal that may keep the pound under pressure, as unemployment rate stayed unchanged at 4.6%, the lowest since 1975.

Better than expected UK jobless claims that rose by 7.3K in May vs forecasted 20.3K, did not help much.

Weakness in the labour sector is also expected to affect BOE and keep central bank’s policy on hold for some time.

Bank of England is expected to keep interest rate unchanged at 0.25% on Thursday’s MPC meeting.

Daily technicals remain mixed, however, today’s rejection at daily cloud top and subsequent easing would keep the downside vulnerable. Extension below 1.2700 handle (Fibo 61.8% of Tue/Wed recovery) would further weaken near-term structure and expose key supports at 1.2640/35 zone.

Res: 1.2796, 1.2806, 1.2847, 1.2882

Sup: 1.2724, 1.2695, 1.2673, 1.2635