Sample Category Title

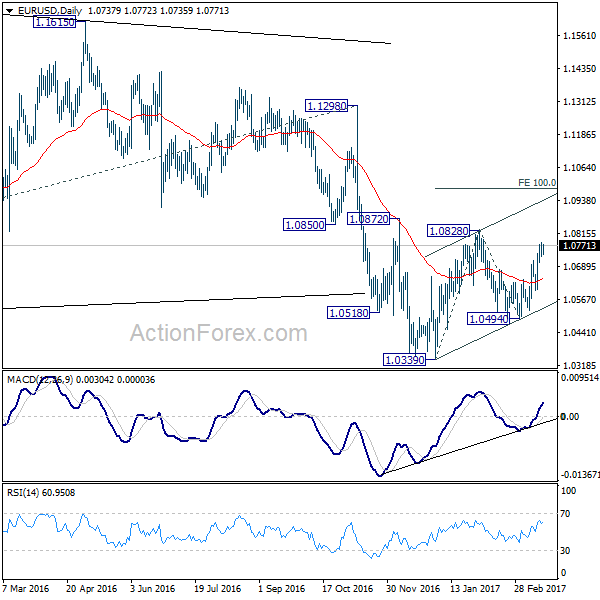

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0715; (P) 1.0748 (R1) 1.0770; More.....

With 1.0639 minor support intact, intraday bias in EUR/USD remains on the upside for 1.0828 resistance. Corrective rise from 1.0339 is still in progress and break of 1.0828 will target 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. Since such rise is viewed as a corrective move, we'd expect upside to be limited by 1.0983 to bring larger down trend resumption eventually. On the downside, break of 1.0639 minor support will turn bias back to the downside for 1.0494 support.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

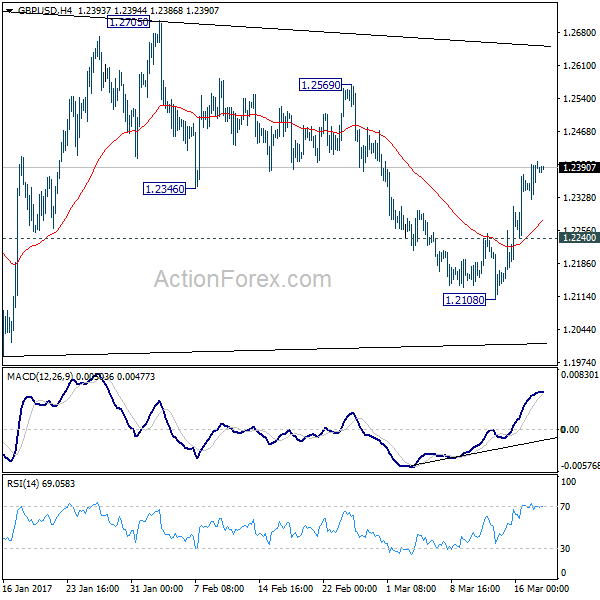

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2342; (P) 1.2373; (R1) 1.2423; More...

GBP/USD's rebound from 1.2108 is still in progress and intraday bias remains on the upside for 1.2569 resistance. Current development suggests that consolidation pattern from 1.1946 is extending with another rising leg. And the larger down trend is not ready to resume yet. Break of 1.2569 will target .2705/74 resistance zone next. At this point, we'd expect strong resistance from 1.2705/2774 to limit upside to extend the sideway pattern. Break of 1.2240 minor support will turn bias back to the downside for 1.2108 support. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

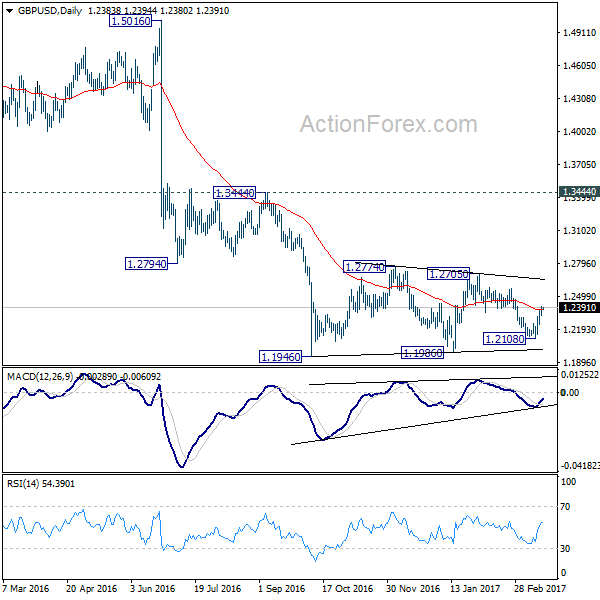

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

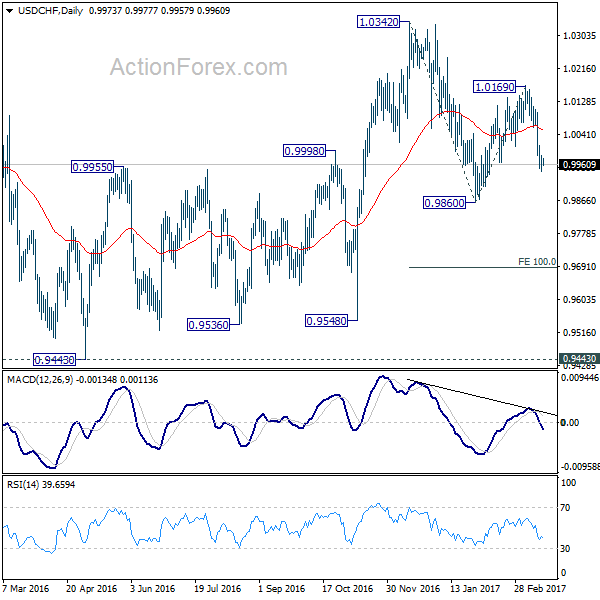

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9951; (P) 0.9969; (R1) 0.9995; More.....

With 1.0018 minor resistance intact, intraday bias remains downside in USD/CHF for 0.9860 support. Recovery from 0.9860 has completed at 1.0169 and whole decline from 1.0342 is likely resuming. Break of 0.9860 will target 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687. On the upside, above 1.0018 minor resistance will turn bias neutral. But outlook will now stay bearish as long as 1.0169 resistance holds.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

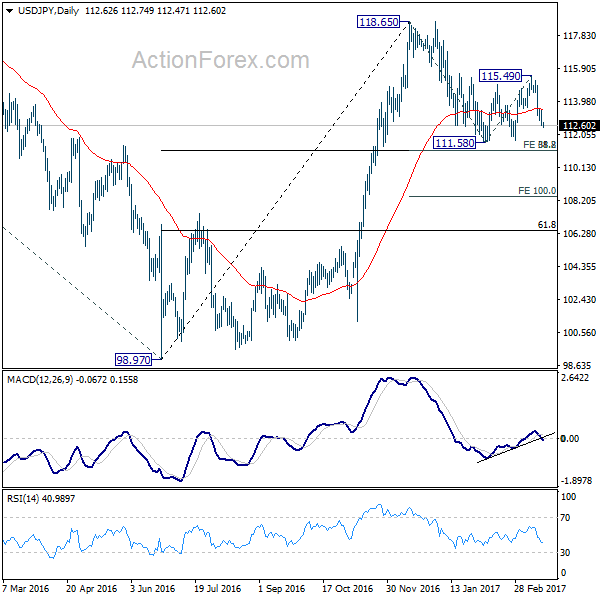

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.29; (P) 112.89; (R1) 113.22; More...

Intraday bias in USD/JPY remains on the downside for the moment as fall from 115.49 continues. As noted before, consolidation pattern from 111.58 has completed with three waves up to 115.49. And decline from 118.65 is likely resuming. Further fall should be seen through 111.58 to 111.12/13 cluster support. This level represents 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12 and 38.2% retracement of 98.97 to 118.65 at 111.13. At this point, we'd tentatively expect strong support from 111.12/13 cluster support to contain downside. On the upside, above 113.53 minor resistance will turn bias to the up for 115.49 resistance. However, sustained break of 111.12/13 will bring deeper decline to 100% projection of 118.65 to 111.58 from 115.49 at 108.42.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.19) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

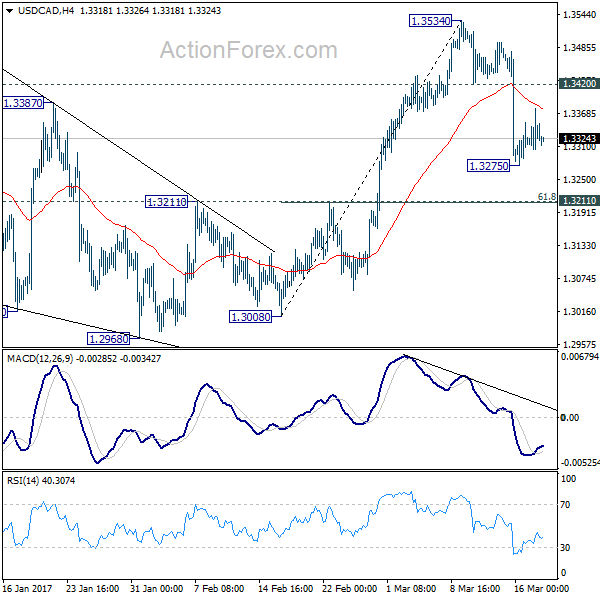

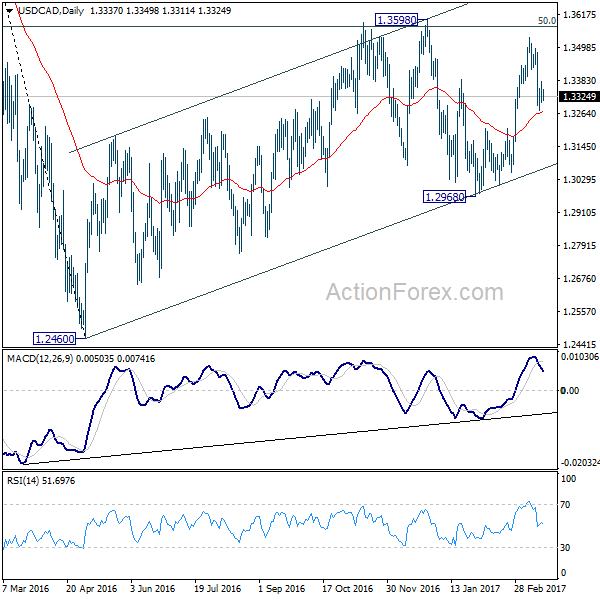

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3304; (P) 1.3341; (R1) 1.3379; More...

Intraday bias in USD/CAD remains neutral as it's staying in the consolidation from 1.3275 temporary low. Decline from 1.3534 might extend lower and below 1.3275 will turn bias to the downside. But such fall is still seen as a corrective pattern. Hence, we'd expect downside to be contained by 1.3211 cluster level (61.8% retracement of 1.3008 to 1.3534 at 1.3209) and bring rebound. On the upside, above 1.3420 minor resistance will indicate that the pull back is completed and turn bias back to the upside for 1.3534 resistance and then 1.3598. However, sustained break of 1.3211 will dampen this view and target 1.2968 key support level next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

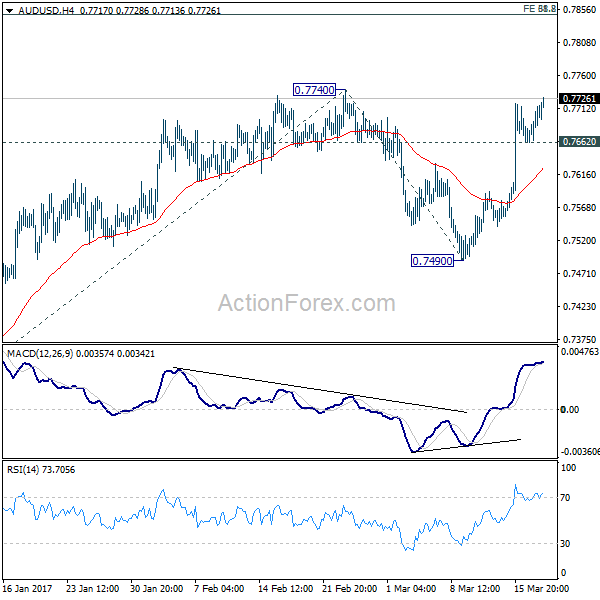

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7671; (P) 0.7694; (R1) 0.7725; More...

Intraday bias in AUD/USD remains on the upside as the rise from 0.7490 is extending to as high as 0.7728 so far. As noted before, the whole rally from 0.7158 is likely resuming. Break of 0.7740 resistance will confirm this case and target 61.8% projection of 0.7158 to 0.7740 from 0.7490 at 0.7850 next. That coincides with key long term retracement level at 0.7849. At this point, we'd expect strong resistance from 0.7849/50 to limit upside and bring reversal. On the downside, below 0.7662 minor support will turn bias neutral first. But break of 0.7490 is needed to indicate reversal. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8169) and above.

G20 Dropped Pledge Against Protectionism, Markets Shrugged Off

The financial markets have mixed, or probably just little reaction, to the outcome of the G20 meeting in Germany over the weekend. Markets in Australia, South Korea traded mildly lower. Meanwhile, stocks in Hong Kong jumped. Japan is on holiday today. In the currency markets, Sterling is paring back some of last week's gain while Dollar stays generally weak. On the other hand, commodity currencies are trading broadly higher as led by Kiwi and Aussie. In other markets, Gold breaches last week's high and is extending rebound to as high as 1235 so far. WTI crude oil dips back to 48.3 as last week's recovery failed below 50. While RBNZ will meet this week, the main focus will turn back to economic data in most countries.

G20 dropped pledge on protectionism and climate change

In the communique released by the G20 countries during the weekend, they dropped the pledged to "avoid all forms of protectionism." Instead, they toned down to a much tamer version of "working to strengthen the contribution of trade to our economies." This is seen as a response to the protectionist approach of US president Donald Trump's administration. Yet, Trump didn't get the pledge to ensure "fair" trade neither. Meanwhile G20 also dropped the pledge on climate change. Regarding global recovery, G20 noted that "the pace of growth is still weaker than desirable and downside risks for the global economy remain. We reaffirm our commitment to international economic and financial cooperation."

US Mnuchin: past communique not necessarily relevant

US trade secretary Steven Mnuchin described the meeting as "incredibly productive". And, he emphasized that "what was in the past communique is not necessarily relevant from my standpoint." He said that "I understand what the president's desire is and his policies and I negotiated from there." He also said that the US believes in "free trade" but "we want to re-examine certain agreements".

French FM Sapin: there was disagreement within the G-20 between a country and all the others.

On the other hand, EU Economic Affairs Commissioner Pierre Moscovici said that "it is not the best meeting we've had, but we avoided backtracking." He hoped that "the wording will be different" at the July G20 meeting in Hamburg. German finance minister Wolfgang Schaeuble tried to talk down the changes and said it's untrue that officials failed to find the common ground. And Schaeuble said that "it's completely clear we are not for protectionism. But it wasn't clear what one or another meant by that."

French finance minister Michel Sapin said that he regretted that the discussions "didn't end in a satisfactory manner." But he noted that "there wasn't a G-20 disagreement, there was disagreement within the G-20 between a country and all the others." Canadian finance minister Bill Morneau said that "the Americans were doing what any new administration would do -- they were looking at the language through their lens." And, "their lens is: how can trade benefit the U.S.? Everyone else has the same lens, but every other country has the advantage of being at the previous meeting."

NZD/USD heading higher ahead of RBNZ

New Zealand dollar is trading high ahead of RBNZ rate decision later in the week. The central bank is widely expected to keep the OCR unchanged at 1.75%. Technically, NZD/USD formed a short term bottom at 0.6888 and rebounded strongly. The development argues that price actions from 0.7484 are merely forming a consolidation pattern. And that is, medium term rise from 0.6102 low is not completed yet. Further rise would now be seen back to 0.7128 near term resistance first. Break will pave the way for at least a test on 0.7374/7484 resistance zone.

Looking ahead...

Released today, New Zealand Westpac consumer confidence dropped to 111.9 in Q1. UK Rightmove house price rose 1.3% in March. Germany will release PPI while Canada will release wholesale sales later today. For the week ahead, RBA and BoJ will release meeting minutes. UK CPI could be a market moving data considering the hawkish BoE minutes last week. New Zealand will also face the test from trade balance. Meanwhile, Euro traders will look into Friday's PMIs.

- Monday: German PPI; Canada wholesale sales

- Tuesday: Australia house price, RBA minutes; UK CPI; Canada retail sales

- Wednesday: BOJ minutes; Japan trade balance; US house price index, existing home sales

- Thursday: RBNZ rate decision; German Gfk consumer sentiment; ECB bulletin; US jobless claims, new home sales

- Friday; New Zealand trade balance; Eurozone PMIs; Canada CPI; US durable goods orders

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7671; (P) 0.7694; (R1) 0.7725; More...

Intraday bias in AUD/USD remains on the upside as the rise from 0.7490 is extending to as high as 0.7728 so far. As noted before, the whole rally from 0.7158 is likely resuming. Break of 0.7740 resistance will confirm this case and target 61.8% projection of 0.7158 to 0.7740 from 0.7490 at 0.7850 next. That coincides with key long term retracement level at 0.7849. At this point, we'd expect strong resistance from 0.7849/50 to limit upside and bring reversal. On the downside, below 0.7662 minor support will turn bias neutral first. But break of 0.7490 is needed to indicate reversal. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8169) and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | Westpac Consumer Confidence Q1 | 111.9 | 113.1 | ||

| 0:01 | GBP | Rightmove House Prices M/M Mar | 1.30% | 2.00% | ||

| 7:00 | EUR | German PPI M/M Feb | 0.40% | 0.70% | ||

| 7:00 | EUR | German PPI Y/Y Feb | 3.20% | 2.40% | ||

| 12:30 | CAD | Wholesale Sales M/M Jan | 0.40% | 0.70% |

OCR In Focus For An Indecisive Kiwi Dollar This Week

Key Points:

- Downtrend seems to have halted for now.

- Ranging phase now likely.

- RBNZ in focus in the week ahead.

The Kiwi Dollar finally began to stage a bit of a comeback last week which now begs the question, what's next for the embattled pair? To answer this, it's worth taking a quick look at what actually drove last week's price action and what the technical bias could have to say about the week to come.

Starting with the week that was, the Kiwi Dollar ended last week much where one would expect given the rather strong reaction to the Fed's decision to raise rates whilst also not offering a strong hawkish outlook moving ahead. However, things weren't all smooth sailing as things progressed and the NZ GDP figures came in at 2.7% y/y and 0.4% m/m, both of these being short of expectations. Initially, this saw the NZD slip back below the 0.70 handle before it found its footing again which had some worried that the FOMC gains would be short-lived. Luckily, the pair recouped these losses as the US Unemployment Claims put a dampener on USD sentiment as the week began to wind down.

As for the technical readings, the NZDUSD now has an overall bearish bias but a solid zone of support could help to limit losses and lead to a neutral week. Specifically, the 12, 20, and 100 day moving averages are in a highly bearish configuration which will be helping to encourage selling. Conversely, the pair has also peaked at a historical zone of resistance which could limit its ability to push higher. Meanwhile, the parabolic SAR has inverted to bullish and the current support has proven to be a robust low on multiple prior occasions.

As for the impending fundamental news, the key development to keep an eye on will be the RBNZ's announcement of the OCR. Currently, expectations are that the rate is held steady as the bank has proven reluctant to alter monetary policy. However, chances of a hike have been improving due to the admittedly slow, yet still notable, recovery of dairy prices. Moreover, the NZ government is coming under increasing pressure to cool off the red-hot housing market which could mean that Wheeler has a bit of a greenlight to follow the US example and tighten policy.

Ultimately, we should see the Kiwi Dollar range this week, likely, between the 0.6982 and 0.7047 levels. However, as mentioned above, don't discount the chances or a surprise breakout to the upside if the RBNZ decides to have a surprise rate hike. This being said, in the wake of last week, the central bank could be taking a rather cautious approach that might also be dependent on the GDT numbers released immediately before the OCR announcement.

European Open Briefing

Global Markets:

- Asian stock markets: Shanghai Composite gained 0.10 %, Hang Seng rose 0.65 %, ASX lost 0.55 %, Nikkei closed for holiday

- Commodities: Gold at $1234 (+0.35 %), Silver at $17.46 (+0.30 %), WTI Oil at $48.95 (-0.75 %), Brent Oil at $51.45 (-0.60 %)

- Rates: US 10-year yield at 2.50, UK 10-year yield at 1.25, German 10-year yield at 0.43

News & Data:

- UK Rightmove House Prices Mar MoM: 1.3% (Prior 2.0%)

- UK Rightmove House Prices Mar YoY: 2.3% (Prior 2.3%)

- PBoC Fixes USDCNY Reference Rate At 6.8998

- ECB's Visco: ECB should shorten break between QE exit and rate hike

- Asia stocks mixed, dollar slips as Fed continues to weigh – RTRS

- Oil prices drop on rise in U.S. drilling – RTRS

- Dollar on defensive for packed week of Fed speakers – RTRS

CFTC Positioning Data:

- EUR short 41K vs 59K short last week. Shorts trimmed by 18K

- GBP short 107K vs 81K short last week. Shorts increased by 26K

- JPY short 71K vs 54K short last week. Shorts increased by 17K

- CHF short 9K vs 10K short last week. Shorts trimmed by 1K

- CAD long 21K vs 29K long. Longs trimmed by 8K

- AUD long 43K vs 51K long. Longs trimmed by 8K

- NZD short 6K vs 4 short last week. Shorts increased by 2K

Markets Update:

Markets were quiet overnight amid a lack of events and a public holiday in Japan.

Most currencies rose against the US Dollar overnight. EUR/USD opened around 1.0735 and rose to a high of 1.0765 later in the session. GBP/USD almost made it to 1.24, but lacked momentum to extend the gain. Meanwhile, USD/JPY remains weak. The pair started around 112.75 at the open and fell to 112.50. A test of 111.50 support seems likely in the near-term.

AUD/USD rose from 0.7685 to 0.7725. Should it break above 0.7740, strong resistance lies at 0.7780. However, should 0.7780 be cleared as well, there is not much resistance left until 0.80. NZD followed the Australian Dollar higher, rising from 0.7010 to 0.7050.

Upcoming Events:

- 07:00 GMT – German PPI

- 12:30 GMT – Canadian Wholesale Sales

- 16:45 GMT – Bundesbank President Weidmann speaks

- 18:20 GMT – BoE Member Haldane speaks

The Week Ahead:

Tuesday, March 21st

- 00:30 GMT – RBA Meeting Minutes

- 09:30 GMT – UK CPI

- 10:00 GMT – BoE Governor Carney speaks

- 10:00 GMT – FOMC Member Dudley speaks

- 12:30 GMT – US Current Account

- 12:30 GMT – Canadian Retail Sales

- 16:00 GMT – FOMC Member George speaks

- 22:00 GMT – FOMC Member Mester speaks

- 23:50 GMT – Japanese Trade Balance

- 23:50 GMT – BoJ Meeting Minutes

Wednesday, March 22nd

- 01:40 GMT – RBA Assistant Governor Debelle speaks

- 09:00 GMT – Euro Zone Current Account

- 13:00 GMT – US House Price Index

- 14:00 GMT – US Existing Home Sales

- 14:30 GMT – US Crude Oil Inventories

- 20:00 GMT – RBNZ Rate Decision

- 20:00 GMT – RBNZ Rate Statement

Thursday, March 23rd

- 07:00 GMT – German Consumer Climate

- 09:00 GMT – ECB Economic Bulletin

- 09:30 GMT – UK Retail Sales

- 12:30 GMT – US Initial Jobless Claims

- 11:00 GMT – Fed Chair Yellen speaks

- 14:00 GMT – US New Home Sales

- 21:45 GMT – New Zealand Trade Balance

Friday, March 24st

- 07:45 GMT – French GDP

- 08:00 GMT – French Manufacturing PMI

- 08:00 GMT – French Services PMI

- 08:30 GMT – German Manufacturing PMI

- 08:30 GMT – German Services PMI

- 09:00 GMT – Euro Zone Manufacturing PMI

- 09:00 GMT – Euro Zone Services PMI

- 12:30 GMT – US Core Durable Goods Orders

- 12:30 GMT – Canadian CPI

- 13:05 GMT – FOMC Member Bullard speaks

- 13:45 GMT – US Manufacturing PMI

- 14:00 GMT – FOMC Member Dudley speaks

Weekly Technical Outlook And Review

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

Weekly gain/loss: + 68 pips

Weekly closing price: 1.0730

The EUR/USD enjoyed another relatively successful week, increasing its value by a further 70 pips and printing its third consecutive weekly bullish candle into the close. Despite this, there could be trouble ahead. Plotted in our field of vision right now is a nearby weekly resistance level pegged at 1.0819, shadowed closely by the 2016 yearly opening base line drawn from 1.0873. What’s also notable from a technical perspective is the potential weekly AB=CD bearish pattern (see black arrows) that terminates above the aforementioned weekly resistances at 1.0980.

Turning our attention to the daily candles, nevertheless, we can see that price came into contact with a bearish daily AB=CD (black arrows) 127.2% Fib ext. at 1.0770 on Friday. Leaving the daily trend resistance extended from the high 1.0873 unchallenged, price sold off and erased the majority of Thursday’s gains. As you can probably see though, there’s not much room left for the bears to stretch their legs here owing to the daily support area positioned just below at 1.0714-1.0683.

A quick recap of Friday’s sessions on the H4 chart shows that price hit the brakes and reversed from the H4 supply zone marked at 1.0797-1.0780. The US prelim UoM consumer sentiment survey, a notable market-moving event, was largely ignored. This, as far as we can see, helped the major close the week forming two back-to-back H4 selling wicks just ahead of a H4 demand area at 1.0705-1.0723. Also of particular interest here is the H4 demand is actually located around the top edge of the aforementioned daily support area, which also sits a few pips above the 1.07 handle and happens to merge nicely with a H4 trendline support taken form the high 1.0679.

Our suggestions: Based on the above points, our prime focus today will be on the current H4 demand area. Due to its surrounding confluence, additional support coming in from the daily picture and room seen to advance north on the weekly chart, there’s a healthy chance of a bounce being seen from the H4 base.

Whether or not this zone requires additional price confirmation before entry is obviously down to the individual trader. For us personally, we have decided to wait for a reasonably sized H4 bullish rotation candle to take shape before a long trade is executed for the simple reason that we do not favor getting stopped out on a fakeout down to 1.07!

Data points to consider: German Buba President Weidmann speaks at 4.45pm. FOMC member Evans speaks at 5.10pm and President Trump takes the stage at 11.30pm GMT.

Levels to watch/live orders:

- Buys: 1.0705-1.0723 ([waiting for a reasonably sized H4 bull candle to form is advised before pulling the trigger] stop loss: ideally beyond the confirming candle).

- Sells: Flat (stop loss: N/A).

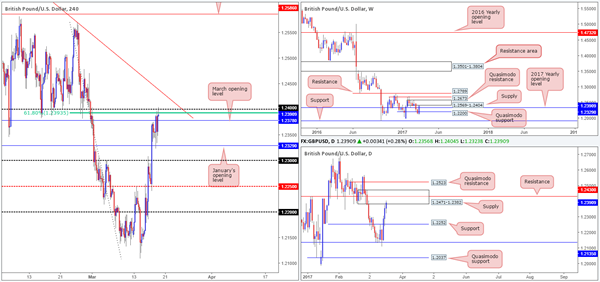

GBP/USD:

Weekly gain/loss: + 227 pips

Weekly closing price: 1.2390

Following a two-week slide, renewed buying interest came in from a low of 1.2109 last week. Not only did this momentum form a sizeable weekly bullish engulfing candle, it also lifted the pair above the 2017 yearly opening level at 1.2390. While this is considered bullish, it might be worth noting that weekly price also clipped the underside of a weekly supply area at 1.2569-1.2404.

In conjunction with the weekly timeframe, daily action shows that price shook hands with a daily supply zone at 1.2471-1.2382 going into the week’s end. Considering that this barrier holds a daily resistance line penciled in at 1.2430 and is planted within the boundaries of the above said weekly supply, the bulls may find it a challenge to break through here this week.

Swinging across to the H4 timeframe, we can see that cable settled for the week around the 1.24 handle which boasts additional resistance from the H4 61.8% Fib resistance at 1.2393 taken from the high 1.2569. Also noteworthy here is the closing candle: a H4 bearish selling wick. This – coupled with the aforementioned higher-timeframe structures currently in play could be enough to send the unit lower today/this week.

Our suggestions: While our team is firmly bearish this market right now, selling into March’s opening level at 1.2378 is not something we’d feel comfortable with. Should a H4 bearish close print beyond this monthly level, we would then be relatively content on shorting any retest seen to the underside of the 1.24/1.2378 region, targeting January’s opening line at 1.2390, followed closely by the 1.23 handle.

Data points to consider: FOMC member Evans speaks at 5.10pm and President Trump takes the stage at 11.30pm GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for price to engulf 1.2378 and then look to trade any retest seen thereafter (stop loss: ideally beyond 1.24).

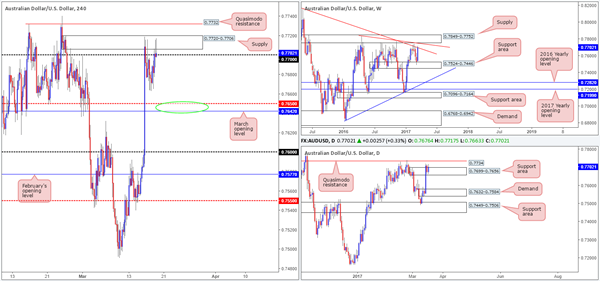

AUD/USD

Weekly gain/loss: + 168 pips

Weekly closing price: 0.7702

Recent trading on the weekly chart shows that price aggressively extended the prior week’s (minor) bounce from the weekly support area seen at 0.7524-0.7446. Consequent to this, the weekly candle reconnected with a weekly trendline resistance stretched from the high 0.8163 and closed the week in strong fashion. In the event that this weekly line is violated, the next upside area to have an eyeball on this week can be seen at 0.7849-0.7752: a weekly supply zone that fuses nicely with another, albeit smaller, weekly trendline resistance taken from the high 0.7835.

Over on the daily chart, the daily supply zone at 0.7699-0.7656 was consumed during Wednesday’s advance and is, as you can see, now being used as a support area. Should the bulls continue to defend this neighborhood; traders’ crosshairs will likely be fixed on the daily Quasimodo resistance coming in at 0.7734.

During the course of Friday’s segment on the H4 chart, the commodity-linked currency retested the H4 supply zone visible at 0.7720-0.7706. Although the H4 supply remained defensive, the H4 candles managed to hold above the 0.77 handle into the week’s end. While there’s still a possibility of a bounce being seen from the nearby 0.7642/0.7650 area (green circle – March opening line and H4 mid-way support), we have a keen interest in the H4 Quasimodo resistance seen beyond the current H4 supply at 0.7732.

Our suggestions: 0.7732 converges closely with a daily Quasimodo resistance line at 0.7734, and is also positioned nearby the weekly supply at 0.7849-0.7752 mentioned above. As highlighted in Friday’s report, we would, dependent on the time of day, likely look to enter aggressively here at 0.7732 and place stops above the H4 (Quasimodo apex) high at 0.7740 (0.7742).

Data points to consider: FOMC member Evans speaks at 5.10pm and President Trump takes the stage at 11.30pm GMT.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.7732 (Stop loss: 0.7742).

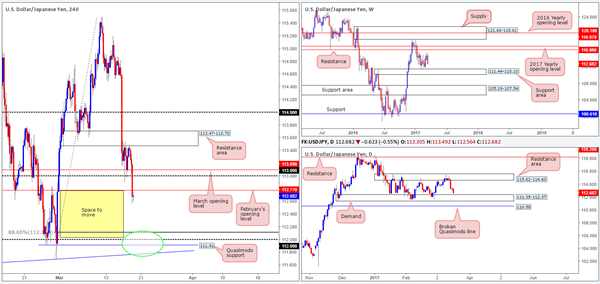

USD/JPY

Weekly gain/loss: – 209 pips

Weekly closing price: 112.68

A healthy bout of selling was seen in the market last week, erasing the prior week’s gains and breaking a two-week bullish phase. Providing that the bears can continue to stamp in their authority here, we see no reason why the weekly support area at 111.44-110.10 will not come into play.

Since mid-January, the daily candles have been consolidating between a daily resistance area coming in at 115.62-114.60 and a daily demand formed at 111.35-112.37 (positioned around the upper edge of the aforementioned weekly support area). A sustained move beyond the top edge of this range could lead to a rally north up to the daily resistance registered at 118.20. Conversely, a push below the lower edge of the daily consolidation may force the unit to challenge the nearby daily broken Quasimodo line at 110.58.

In the early hours of Friday’s London morning segment, the US dollar resumed its decline against the Japanese yen. After chomping through March’s opening base at 113.09, the 113.00 handle and eventually February’s opening line at 112.77, the pair concluded trade forming a H4 indecision candle at 112.68. Despite space being seen for the H4 candles to continue selling off down to around the 112.00 vicinity, we have to remain cognizant of the current daily demand pictured at 111.35-112.37.

Our suggestions: With the top edge of the daily demand coming in at 112.37, shorting from the underside of Feb’s opening line at 112.77 is not impossible, but difficult in regards to space. One has 40 pips of room to play with here. As such, we feel the better route to take today/this week is instead of looking to grab 30 or so pips from a short here, look to wait and see if the H4 candles can test 112 (green circle) for longs. There are a number of technical aspects that support a buy from this angle:

The H4 88.6 retracement value seen at 112.11.

The H4 Quasimodo support at 111.91.

A H4 trendline support taken from the low 111.59.

All of the above is positioned within the current daily demand, which, as we also mentioned above, is located around the top edge of a weekly support area.

Given the above points, a long from 112 is far more appealing to us. Seeing as how the H4 buy zone (111.75/112.11) is rather large, nevertheless, a reasonably sized H4 bullish candle is required to be seen before we pull the trigger.

Data points to consider: FOMC member Evans speaks at 5.10pm and President Trump takes the stage at 11.30pm GMT.

Levels to watch/live orders:

- Buys: 111.75/112.11 ([waiting for a reasonably sized H4 bull candle to form is advised before pulling the trigger] stop loss: ideally beyond the confirming candle).

- Sells: Flat (stop loss: N/A).