Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9587; (P) 0.9652; (R1) 0.9686; More.....

Intraday bias in USD/CHF remains on the downside for the moment. Deeper decline could be seen through 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. But we'd start to look for bottoming signal again as it approaches 0.9443 key support level. On the upside, above 0.9718 minor resistance will turn intraday bias neutral first. But near term outlook will stay bearish as long as 0.9807 resistance holds.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.93; (P) 110.81; (R1) 111.31; More...

Intraday bias in USD/JPY remains neutral cautiously on the downside with focus on 110.23 support. Break there will resume the decline from 114.36. In such case, deeper fall should be seen to 108.12 and below. Whole decline from 118.65 is seen as a correction and is still in progress. We'll look for bottoming signal at 61.8% retracement of 98.97 to 118.65 at 106.48 as the correction extends. Meanwhile, above 111.70 will turn intraday bias back to the upside. But we'd expect strong resistance from 61.8% retracement of 114.36 to 110.23 at 112.78 to limit upside and bring fall resumption.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

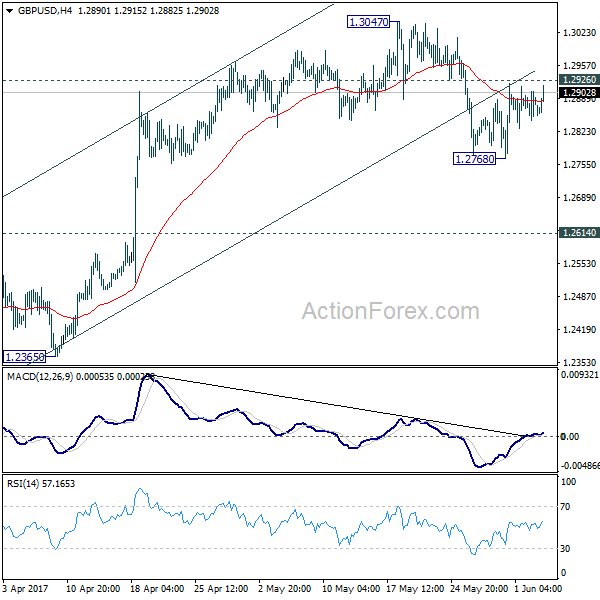

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2854; (P) 1.2879; (R1) 1.2913; More...

GBP/USD recovers again today but at this point it's staying below 1.2926 minor resistance. Intraday bias remains neutral and deeper fall is still in favor. Break of 1.2768 will turn bias to the downside for 1.2614 resistance turned support first. Break there should also indicate completion of whole consolidation pattern from 1.1946 and target a retest on this low. However, break of 1.2926 will turn focus back to 1.3047 instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

Sterling Recovers as Latest Poll Show Conservative Having 11 pt Lead

Sterling recovers mildly today as last Guardian/ICM poll showed that the Conservative is still having 11 pt lead over Labor ahead of Thursday's election. The poll showed that 45% of respondent would vote for Conservatives, unchanged from last week. Meanwhile, 34% would vote for Labour, up 1% from last week. FTSE continues it's negative correlation with Pound and trades mildly lower today, down -0.3% at the time of writing. Technically, 1.2925 minor resistance in GBP/USD and 0.8654 minor support in EUR/GBP will be watched for indication of strength in the Pound.

Looking at other poll results, according to a poll by Survation for The Mail on Sunday, support for Conservative dropped further to 40%, while that for Labour rose to 39%. That is, the Tories are only have a 1-point lead over Labour. On other hand other, a ComRes poll showed that support for Conservatives rose one to 47% and that for Labour also rose one 35%. In that case, Tories still maintained a 12-point lead. In the middle, Opinium poll for the Observer found that support for Conservatives was down 2 points to 43%, and that for Labour was up 2 to 37%. That was a 6-point lead.

Turnout pattern weighs on election results

However, according to an article by Patrick Sturgis and Will Jennings of University of Southampton these polls tend to be wrong with historical tendency to "over-state Labour support". One of the key factor is that support for Labour appears to be "soft" and they may change their mind before election day. Also, the turnout rate and pattern would have a huge impact on the actual results. Based on their model, the ever lead of Conservatives over Labour could be doubled from 5 to 10 pts after applying turnout weight.

UK PMI services missed

UK PMI services dropped sharply to 53.8 in May, down from 55.8 and below expectation of 55.0. Markit noted in the release it's seeing "a renewed slowdown in business activity growth across the UK service economy, following the four-month peak achieved in April." And, "optimism about the year ahead is running below the long-run average, weighed down principally by concerns over Brexit, political uncertainty and weaker spending by households".

Eurozone PMI services revised up

Eurozone PMI services was revised slightly up to 56.3 in May. Overall composite PMI was unchanged at 56.8. Markit noted that "the outlook for the Eurozone economy seems to be tilting to the upside, and it seems likely that we'll start to see many forecasters' expectations for 2017 growth revised higher." Also, "with the rate of job creation rising to one of the highest seen over the past decade, the recovery is also becoming more sustainable, as the improved labour market should feed through to higher consumer spending."

Also from Europe, Germany PMI services was revised up to 55.4 in May. France PMI services was revised down to 57.2 in May. Italy PMI services dropped to 55.1 in May.

China PMI services improved

China Caixin services PMI rose to 52.8 in May, up from 51.5, beat expectation of 51.4. Zhengsheng Zhong, director of Macroeconomic Analysis at CEBM Group noted that "the improvement in the services sector bolstered the Chinese economy in May." But he also warned that "the rapid deterioration in the manufacturing industry is worrying. We need to closely monitor whether the diverging trends in manufacturing and services will widen further." Released last week the Caixin PMI manufacturing dropped to 49.6, the first contraction reading in nearly a near.

RBA in upcoming Asian session

RBA will announce rate decision in the upcoming Asian session. The central bank is widely expected to keep the key interest rate unchanged at 1.50%. Most economists expect RBA to stand pat at least through 2017. But there are some who warned of the risk of a cut this year as the economy under performs RBA's forecast. AUD/NZD's fall from .1017 accelerated to as low as 1.0389 last week but rebounded from there since then. The corrective three wave structure of the rise from 1.0234 to 1.1017 suggests medium term bearishness. Hence we'd expect recovery to be limited by 1.0608 resistance to bring another fall through 1.0234. There is prospect of a test on 2015 low at 1.0016 in medium term.

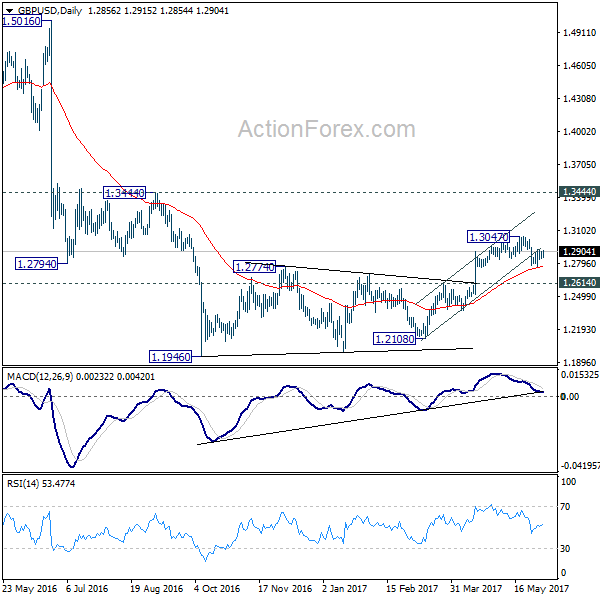

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2854; (P) 1.2879; (R1) 1.2913; More...

GBP/USD recovers again today but at this point it's staying below 1.2926 minor resistance. Intraday bias remains neutral and deeper fall is still in favor. Break of 1.2768 will turn bias to the downside for 1.2614 resistance turned support first. Break there should also indicate completion of whole consolidation pattern from 1.1946 and target a retest on this low. However, break of 1.2926 will turn focus back to 1.3047 instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | TD Securities Inflation M/M May | 0.00% | 0.50% | ||

| 01:00 | AUD | TD Securities Inflation Y/Y May | 2.80% | 2.60% | ||

| 01:45 | CNY | Caixin PMI Services May | 52.8 | 51.4 | 51.5 | |

| 07:45 | EUR | Italy Services PMI May | 55.1 | 55.3 | 56.2 | |

| 07:50 | EUR | France Services PMI May F | 57.2 | 58 | 58 | |

| 07:55 | EUR | Germany Services PMI May F | 55.4 | 55.2 | 55.2 | |

| 08:00 | EUR | Eurozone Services PMI May F | 56.3 | 56.2 | 56.2 | |

| 08:30 | GBP | Services PMI May | 53.8 | 55 | 55.8 | |

| 12:30 | USD | Non-Farm Productivity Q1 F | 0.00% | -0.20% | -0.60% | |

| 12:30 | USD | Unit Labor Costs Q1 F | 2.20% | 3.00% | 3.00% | |

| 14:00 | USD | ISM Non-Manufacturing Composite May | 57.1 | 57.5 | ||

| 14:00 | USD | Labor Market Conditions Index Change May | 3 | 3.5 | ||

| 14:00 | USD | Factory Orders Apr | -0.20% | 0.20% |

DAX Rises on Service PMIs in Holiday-Thinned Trade

The DAX index has started the trading week with gains. The index is closed on Monday, as German stock exchanges are closed for a holiday. The DAX closed on Friday at 12,822.84 points. On the release front, Eurozone and German Services PMIs continue to point to expansion. German Services PMI was unchanged in May, with a reading of 55.4, just above the forecast of 55.2 points. Eurozone Services PMI inched lower to 56.3, edging above the forecast of 56.2 points. On Tuesday, the Eurozone releases Sentix Investor Confidence and Retail Sales.

The DAX drifted for most of last week, but showed some life in the Friday session, posting strong gains of 1.25%. German stock markets took advantage of a weaker US dollar, which lost ground to the euro after soft US employment numbers on Friday. The markets were genuinely surprised at the Nonfarm Payrolls report. The economy produced just 131 thousand jobs, well short of the forecast of 181 thousand. Wage growth remains weak, and edged down from 0.3% to 0.2%. The unemployment rate dropped to 4.3%, but this reading can be largely explained by a decline in the participation rate. The disappointing employment reports are unlikely to alter the Fed's plan to raise rates next week, but policymakers will remain very cautious about additional rate hikes in the second half of the year.

Stock markets on both sides of the pond are keeping a close eye on the Federal Reserve, which holds its policy meeting on June 14. The odds of a rate hike have climbed to 96%, according to the CME Group, up from 88% just a week ago. Last week's dismal Nonfarm Payroll report has failed to put a dent in market confidence in a June rate hike. Traders should note that ahead of the March hike, the odds of a rate hike were also close to 100%, and the dollar actually lost ground after the Fed followed through with a quarter-point increase. Although an increase in interest rates would mark a vote of confidence in the US economy, the Fed continues to have concerns. Inflation remains stubbornly low, despite a labor market that remains close to capacity. Fed policy makers are also scratching their heads over soft consumer spending, which has not kept pace with high levels of consumer confidence. As for additional rate hikes in the second half of 2017, the markets are skeptical, with the odds of a September rate hike at just 26%.

USD/CAD Possible Retest of W H4/ D H5 Zone

As doubts grow of over-supply in the Oil market, its price continues to drift lower, putting pressure on the CAD, I expect this weakness of the CAD to be more prevalent than the USD weakness of recent. At this point we can see a slow bullish grind on intra day time frame towards W H4/D H5 confluence zone 1.3540-50. The POC zone (trend line, 50.0, D L3, Atr pivot, historical buyers) might spike the price up towards 1.3500, 1.3520 and if 1.3520 breaks towards 1.3550. The price is above W L3 and D L3 so the bulls are currently in control. The price should ideally stay above 1.3422 for bullish outcome.

UK in Focus as Election Nears

Bank holiday's across parts of Europe is contributing to relatively subdued trade at the start of the week, with a number of major events scheduled for the coming days also likely aiding this.

Polls over the weekend continue to suggest that Theresa May's lead is slipping, with another from YouGov suggesting that the Conservatives are set to lose their majority. Of course, different polls are still giving us a variety of outcomes, with some still pointing to a comfortable majority for the Conservatives, which appears to be the most market friendly scenario. The memory of 2015 when the Conservatives performed much better than expected may well be helping to support the pound, even as some surveys paint a worrying picture for Theresa May.

While the UK election is likely to be a dominant theme for markets this week, there will also be a focus on the ECB meeting, which is also due to take place on Thursday. There has been a lot of speculation about how and when the central bank will withdraw its stimulus, with some suggesting they may hint at further reductions either this week or in September. The economy is undoubtedly on a positive trajectory but as the PMI reports showed this morning, it is still unbalanced with Germany being a significant driver of it.

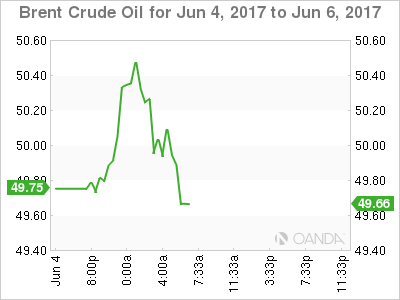

Oil has been boosted a little this morning by reports that Saudi Arabia, Egypt, UAE and Bahrain have severed diplomatic ties with Qatar, accusing the country of supporting terrorist organisations. Still, Brent and WTI crude continue to languish near last week's lows, with traders appearing to doubt whether the coordinated measures undertaken by OPEC and non-OPEC members will be enough to address the oil glut. Brent has traded back above $50 again this morning but continues to look vulnerable having broken below here on Friday.

Still to come today we've got a number of economic reports from the US including services PMIs from Markit and ISM, as well as factory orders, unit labour costs and productivity figures. Last week's jobs report hasn't filled people with confidence in the US economy, despite another drop in the unemployment rate, although this hasn't deterred people from believing they'll raise rates next week.

Geopolitics To Guide Dollar This Week

Geo-political risk is set to dominate capital markets this week; it will be supported by a handful of central bank monetary policy decisions.

In the Gulf, the Saudi's, Bahrain, the United Arab Emirates and Egypt said they are suspending all travel to and from Qatar, citing Qatar's support of 'terrorist groups aiming to destabilize the region.'

In the U.K, citizens are dealing with the outcome of the weekend's terrorist acts as the political parties enter the final three-days of the nation's election campaign. The British snap election will be held on Thursday, June 8. In France, the French election will take place in two-rounds beginning on June 11.

In the U.S, fired FBI Director James Comey is set to testify before the Senate Intelligence Committee on Thursday about his conversations with President Trump regarding suspicion of Russian interference in the 2016 election. His testimony is expected to drive further moves in equities and the dollar in a recurrence of market swings last month.

The RBA, RBI and the ECB announce their respective monetary policy decisions on June 6, 7 and 8 – all three central banks are expected to leave their policies unchanged, however, the market is looking for guidance on QE reduction from Draghi.

Germany will release its April data for both manufacturing orders and output, while Canada will report its labor force survey and key housing starts, both for May.

1. Global equities questioning growth

Friday's underwhelming non-farm payroll (NFP) is testing market bets on improving global growth that's helped drive the value of global equities this year.

In Japan, the Nikkei's share average barely changed overnight, keeping close to a 22-month high scaled last week as the yen's rise stalls (¥110.48), while the broader Topix index fell -0.1%. The gauge closed Friday at the highest point in two-years.

In Hong Kong, the Hang Seng fell -0.4%, while the Shanghai Composite Index slipped -0.5%.

Elsewhere in the region, the Malaysia's benchmark gained +0.6% and Indonesian stocks climbed +0.2%, while Taiwan's Taiex increased +0.7%.

With the Saudi-led alliance cutting diplomatic ties with Qatar, Doha's QE Index dropped -7.7%, the most in three-years. While in Dubai, the DFM General Index fell -1.3%.

Note: Germany, Switzerland and France all have a bank holiday.

In Europe, indices are trading slightly lower in light trade due to bank holidays. The market reaction to this weekends terror attacks in London is having little impact, although travel and leisure names seeing some downside pressure on the FTSE 100.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.3% at 3579, FTSE -0.2% at 7530, DAX Closed, CAC-40 -0.6% at 5312, IBEX-35 -0.5% at 10850, FTSE MIB -1.0% at 20724, SMI Closed, S&P 500 Futures -0.1%.

2. Oil prices gain as Saudi Arabia cuts ties with Qatar

Ahead of the U.S open, oil prices are better bid after top crude exporter Saudi Arabia and other neighbouring Arab states cut ties with Qatar – the market is worried that increased tension in the Middle East will disrupt supplies.

Saudi Arabia, the United Arab Emirates, Egypt and Bahrain closed all transport links with top 'liquefied natural gas and condensate shipper' Qatar, accusing it of 'supporting extremism and undermining regional stability.'

Brent crude prices are up +35c, or +0.7%, to +$50.30 a barrel, while U.S West Texas Intermediate (WTI) is at +$48.03 a barrel, up +37c.

Note: With a production capacity of about +600k bpd, Qatar's crude oil output is one of OPEC's smallest.

However, the market is focusing on tensions within OPEC, which could potentially impact any agreement to cut production in order to support global prices. Brent crude prices are still down about -7% from their open on May 25, when OPEC opted to extend last November's production cuts into 2018.

The market outlier that is having an impact on OPEC product cuts supporting prices is U.S oil production – The rise in production has been driven by a record 20th straight weekly climb in oil drilling, with the rig count climbing by 11 in the week to June 2, to 733, the most since April 2015.

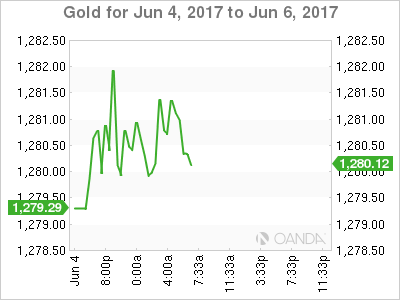

Gold is holding steady (+0.1% to +$1,280.90 per ounce) after hitting its highest in over six-weeks overnight, supported by Friday's disappointing U.S jobs data that appeared to dilute the prospects for an aggressive string of Fed interest rate hikes.

3. Yield curves remain flatter

U.S Treasury yields remain near the lowest level in seven months with last Friday's data on wage growth and hiring in the U.S labor market came in below expectations.

The report is unlikely to keep the Fed from raising rates in June (13-14), but the slow wage growth reinforces the view that stubbornly weak inflation could keep the Fed from raising rates again later in the year.

The yield on U.S 10-year Treasury notes has rallied less than +1 bps to +2.17%, after dropping -5 bps on Friday.

Elsewhere, the yield on Aussie 10-year government bonds have lost -2 bps to +2.39%. In the U.K, 10-year Gilt yields have climbed +2 bps to +1.06%.

4. Dollar seeks out direction

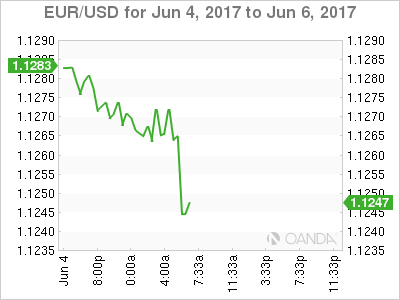

The 'mighty' USD has consolidated some of its recent losses after its declines following Friday's U.S jobs data. On Friday, the USD tested its lowest level across the board since November after non-farm payrolls underwhelmed – the markets seemed content to ignore that U.S unemployment rate (+4.3% vs. +4.4%) was its lowest level in 16-years.

The EUR (€1.1264) and GBP (£1.2888) trade slightly lower outright due to caution ahead of Thursday's ECB meeting and the U.K's general election. The single unit could gain again if the ECB speaks of plans to scale back monetary stimulus, but policymakers may be cautious of doing so given subdued core inflation.

In the U.K, sterling continues to be held captive by 'opinion polls' which point to waning support for the ruling Conservative party. Currently, the impact of weekend's terror attacks has been 'limited.'

Note: U.K election uncertainties have risen with some opinion polls seeing the Conservatives lead narrowing to only around +1-4% points ahead of Labour.

5. U.K May Services PMI Weaker Than Expected

Data this morning showed that the U.K's PMI for the dominant services sector came in weaker than expected in May, having hit a four-month high in April.

The measure fell to 53.8 from 55.8 the previous month and well below the expected 54.9 reading.

Digging deeper, IHS Markit said new orders grew more slowly, partly in response to a squeeze on household incomes as a result of a jump in inflation, and partly because some businesses have delayed making decisions ahead of the June 8 general election.

Despite the May dip, purchasing managers surveys more broadly point to a possible pickup in growth during Q2, to +0.5% from +0.2% in Q1.

Euro Dips Despite Solid German, Eurozone Services PMIs

The euro has ticked lower in the Monday session, as EUR/USD is currently trading at 1.1260. Traders can expect a quiet day from the pair, as German banks are closed for a holiday. In economic news, the German and Eurozone service sectors continue to expand.German Services PMI was unchanged in May, with a reading of 55.4, just above the forecast of 55.2 points. Eurozone Services PMI inched lower to 56.3, edging above the forecast of 56.2 points. In the US, today's key event is ISM Non-manufacturing PMI, which is expected to drop to 57.1 points.

The Federal Reserve holds its policy meeting on June 14, and the odds of a quarter-point increase continue to climb. The odds of a hike have climbed to 96%, according to the CME Group, up from 88% just a week ago. The markets have priced in a June move, and a dismal Nonfarm Payroll report has failed to put a dent in market confidence in a June rate hike. Traders should note that ahead of the March hike, the odds of a rate hike were also close to 100%, and the dollar actually lost ground after the Fed followed through with a quarter-point increase. An increase in interest rates represents a vote of confidence in the US economy, but the Fed continues to have some concerns. Inflation remains stubbornly low, despite a labor market that remains close to capacity. Fed policy makers are also scratching their heads over soft consumer spending, which has not kept pace with high levels of consumer confidence. As for additional rate hikes in the second half of 2017, the markets are skeptical, with the odds of a September rate hike at just 26%.

Technical Outlook: Aussie Extends Strong Recovery On Better Than Expected Chinese Data, Gulf Region Political Tensions

The Australian dollar extended strong recovery against its US counterpart, nearing 0.7500 on Monday.

Bullish acceleration was triggered on Friday on profit-taking and boosted by downbeat US NFP data which deflated the greenback. Strong bullish close on Friday that marked the biggest one-day gains since 15 Mar, left long bullish daily candle that underpinned fresh bulls.

Stronger than expected China's Service PMI data, released on Monday and rising geopolitical tensions in the Middle East sparked fresh acceleration higher that broke above former high at 0.7475 and cracked 0.7482 barrier (Fibo 76.4% of 0.7517/0.7369 downleg), shifting focus towards key barriers at 0.7517/22 (23 May peak/weekly cloud top), reinforced by 200SMA at 0.7527.

Daily indicators show room for extension higher, however, hesitation at these barriers could be anticipated.

Broken converged daily Tenkan-sen/Kijun-sen lines offer solid support at 0.7443 which is expected to hold corrective dips.

Res: 0.7500, 0.7520, 0.7535, 0.7573

Sup: 0.7460, 0.7443, 0.7420, 0.7400