Sample Category Title

Elliott Wave View: EURJPY Short Term Pullback

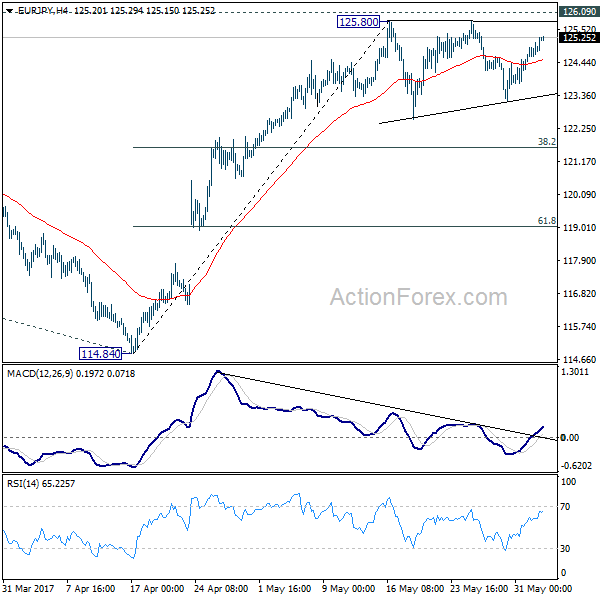

Short Term EURJPY Elliott Wave view suggests the rally from 4/16 low is unfolding as a double three Elliott Wave structure. Up from 4/16 (114.8) low, Intermediate wave (W) ended at 125.81 and Intermediate wave (X) ended at 122.53. A break above 125.81 however is still needed to add conviction that the next leg higher has started.

From 122.53 low, the rally is also unfolding as a double three Elliott Wave structure. Minute wave ((w)) ended at 125.8 and Minute wave ((x)) ended at 123.11. Near term, cycle from 5/30 low (123.11) is mature and expected to end soon. This cycle from 5/30 low is unfolding as a Flat Elliott Wave structure and expected to end with Minutte wave (w) at 125.5 – 125.7 area. Once Minutte wave (w) is over, expect pair to pullback in Minutte wave (x). The pullback should unfold in 3, 7, or 11 swing and while the pullback stays above 123.11, pair should extend higher. If pair breaks below 123.11, then pair is likely doing a double correction from 5/16 peak. This suggests pair can open extension lower to 121.6 – 122.25 area in case of a double correction. From this area, buyers should appear again for an extension higher or at least a 3 waves bounce. We do not like selling the proposed move to the downside and expect dips to find buyers in 3, 7, or 11 swing.

EURJPY Elliott Wave 1 Hour Chart

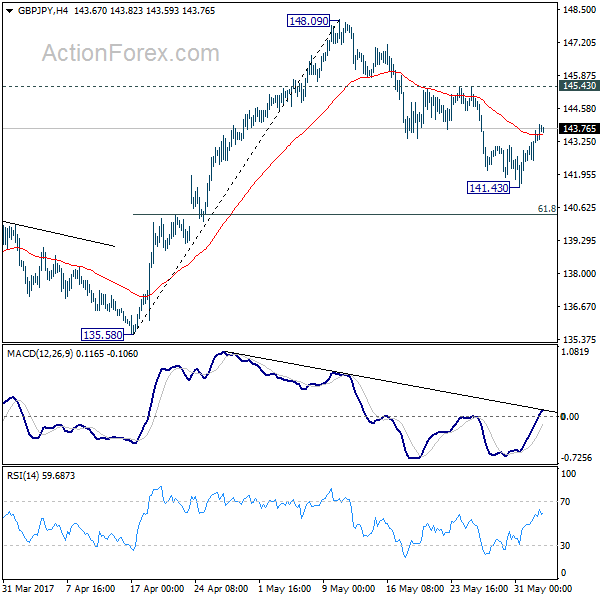

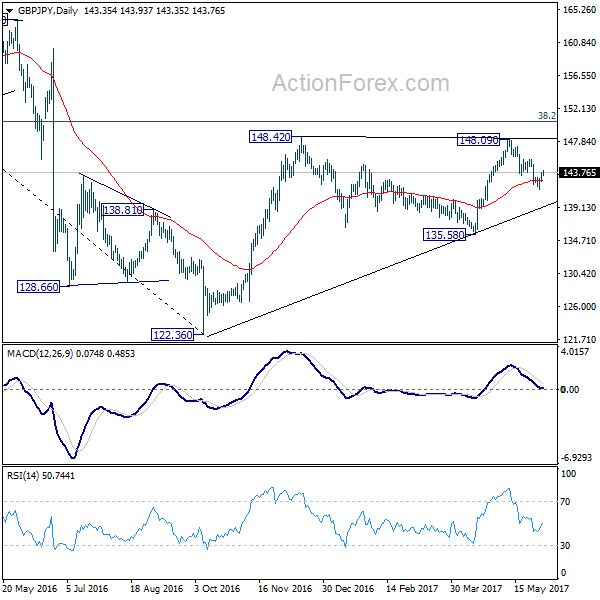

GBP/JPY Daily Outlook

Daily Pivots: (S1) 142.70; (P) 143.20; (R1) 143.90; More....

Break of 141.3.36 minor resistance suggests short term bottoming at 141.43, on bullish convergence condition in 4 hours MACD. And, the pull back from 148.09 could have completed too. Intraday bias is turned back to the upside for 145.43 resistance first. Decisive break there should confirm this bullish case. And also, in that case, whole rally from 122.36 could be resuming through 148.42 resistance to long term fibonacci level at 150.42.

In the bigger picture, rise from 122.36 medium term bottom is still expected to extend to of 195.86 to 122.36 at 150.42. And decisive break there could pave the way to 61.8% retracement at 167.78. However, as the cross is starting to lose upside momentum, rejection below 150.42 and break of 135.58 support will indicate reversal and bring deeper fall back to retest 122.36 instead.

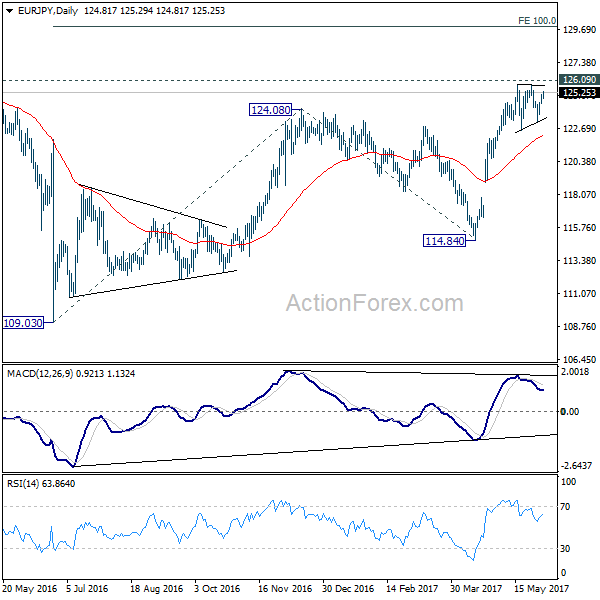

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.53; (P) 124.80; (R1) 125.14; More...

Intraday bias in EUR/JPY remains neutral as the consolidation from 125.80 continues. Deeper fall cannot be ruled out down we'd expect downside to be contained by by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Nonetheless, firm break of 121.61 will dampen our bullish view and bring deeper fall to 61.8% retracement at 119.02.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

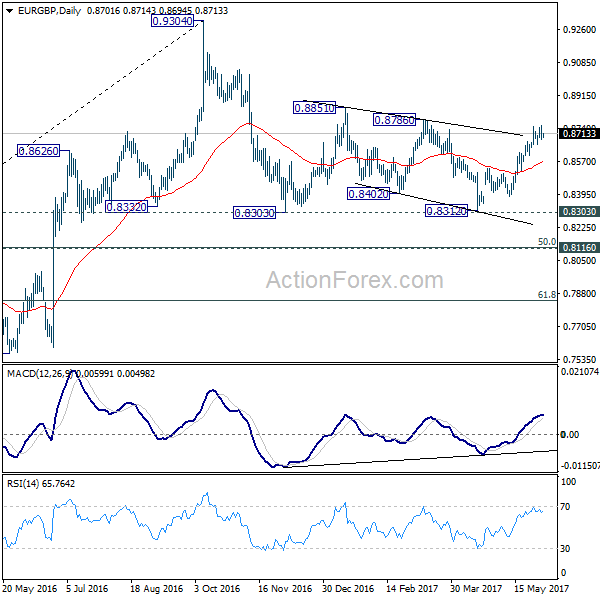

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8673; (P) 0.8714; (R1) 0.8744; More...

Despite breaching 0.8750 to 0.8754, EUR/GBP quickly retreated back to established range. Intraday bias stays neutral first as the consolidation from 0.8750 could extend. Near term outlook will remain mildly bullish as long as 0.8602 support holds and further rally is expected. Above 0.8750 will target 0.8786 resistance first. Break of 0.8786 would pave the wave for retesting 0.9304 high. Break of 0.8602, however, will argue that the rebound from 0.9312 has completed and turn bias back to the downside for 0.8529.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after taking 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

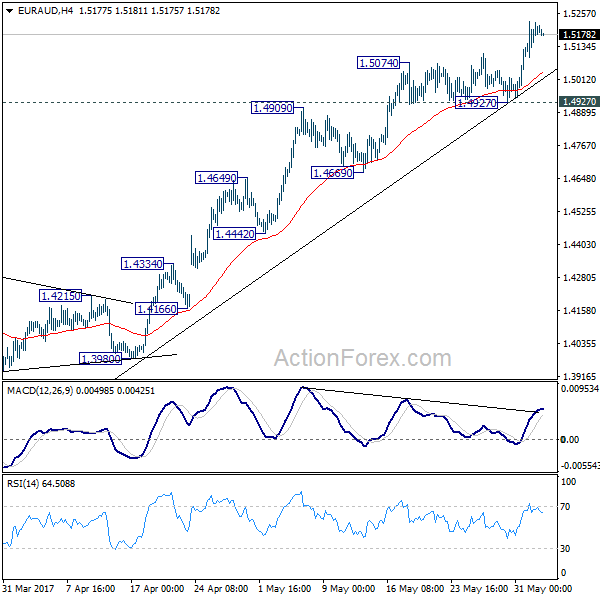

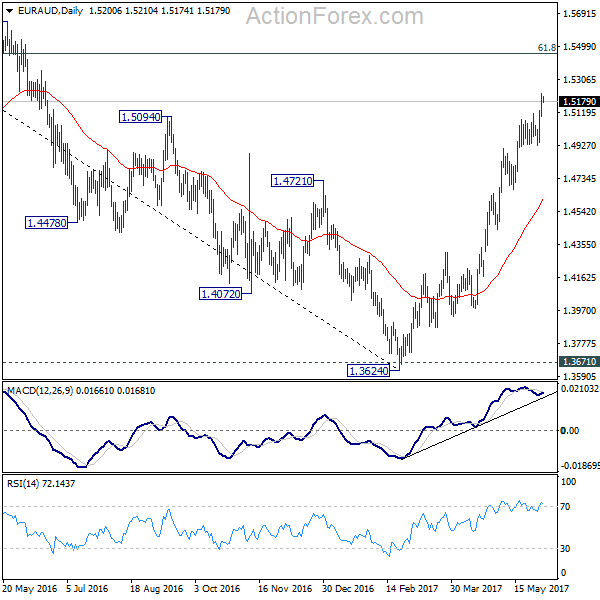

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5121; (P) 1.5174; (R1) 1.5253; More...

Intraday bias in EUR/AUD remains on the upside for the moment. Current rise from 1.3624 is expected to target r next medium term fibonacci level at 1.5455. On the downside, break of 1.4927 is needed to signal short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. In any case, outlook will now stay cautiously bullish as long as 1.4669 support holds.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0875; (P) 1.0888; (R1) 1.0906; More...

No change in EUR/CHF's outlook as consolidation from 1.0986 continues. Intraday bias stays neutral for the moment. Deeper fall cannot be ruled out. But downside should be contained by 1.0791/0872 support zone to bring rise resumption. As noted before, the consolidative pattern from 1.1198 should be completed. Firm break of 1.0999 resistance will pave the way for a retest on 1.1198 high.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

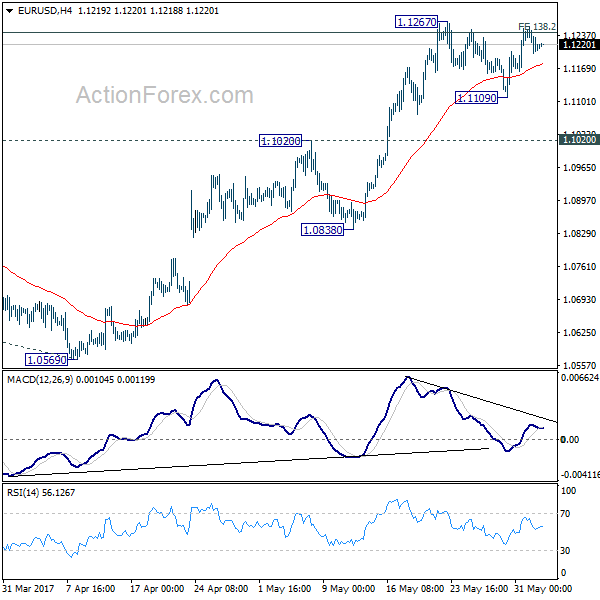

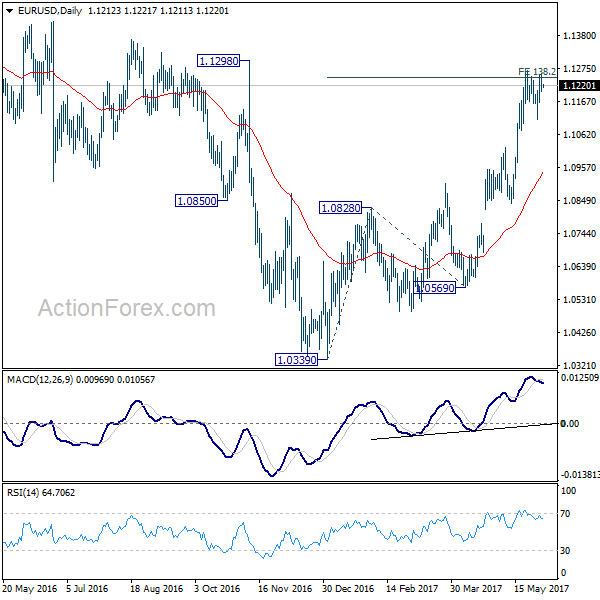

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1189; (P) 1.1223 (R1) 1.1244; More....

Intraday bias in EUR/USD remains neutral for the moment. On the upside, break of 1.1267 will resume recent rise. Decisive break of 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) resistance zone will carry larger bullish implication and target 1.1615 resistance next. In case consolidation from 1.1267 extends with another fall, further rise will remain in favor as long as 1.1020 support holds. But, break of 1.1020 will indicate rejection from 1.1245/98 and turn bias to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

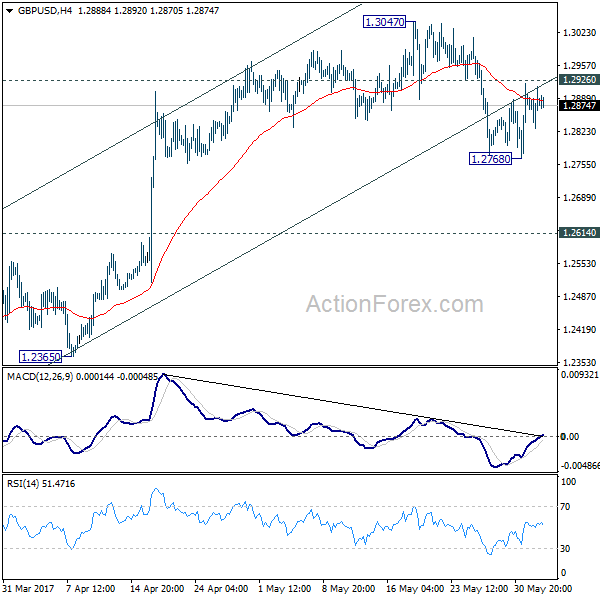

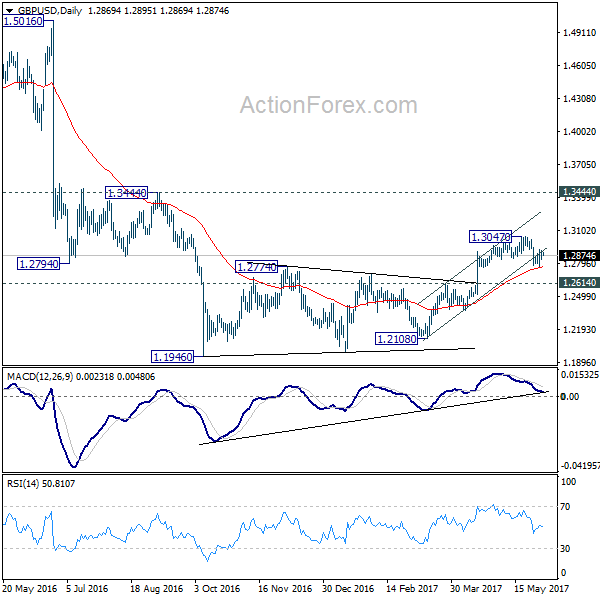

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2833; (P) 1.2874; (R1) 1.2919; More...

Intraday bias in GBP/USD remains neutral first. With 1.2926 minor resistance intact, deeper fall is still in favor. We're holding on to view that rise from 1.2108 is completed. Below 1.2768 will target 1.2614 resistance turned support next. Break there should also indicate completion of whole consolidation pattern from 1.1946 and target a retest on this low. Meanwhile, above 1.2926 minor resistance will turn focus back to 1.3047 high instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

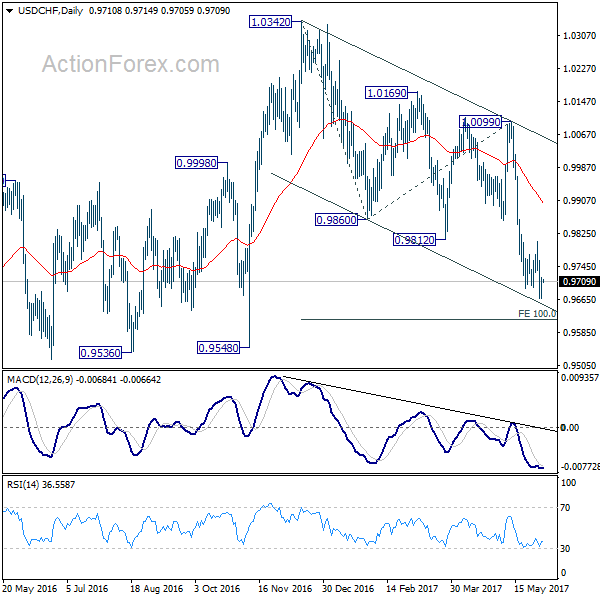

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9678; (P) 0.9699; (R1) 0.9734; More.....

Further decline is still expected in USD/CHF with 0.9807 resistance intact. Current fall from 1.0342 should target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there. Meanwhile, break of 0.9807 will be the first sign of near term reversal. In such case, intraday bias will be turned back to the upside for 0.9860 support turned resistance for confirmation.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

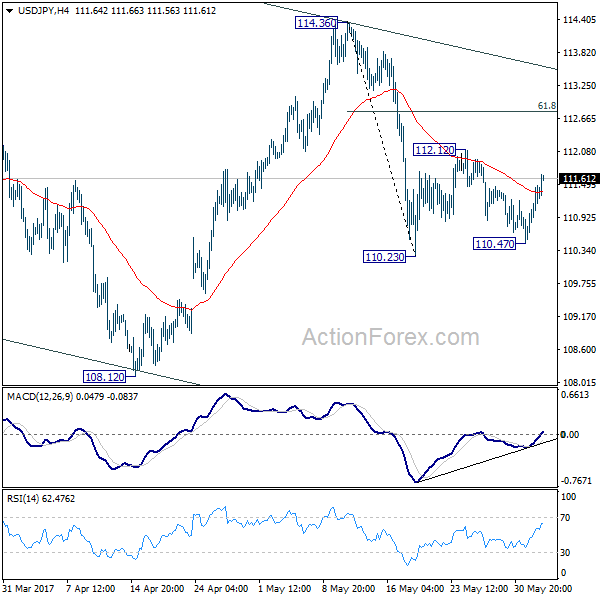

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.83; (P) 111.15; (R1) 111.69; More...

USD/JPY's consolidation from 110.23 is extending with another rise and intraday bias stays neutral first. Break of 112.12 might be seen but upside should be limited by 61.8% retracement of 114.36 to 110.23 at 112.78 to bring fall resumption. Below 110.23 will turn bias to the downside and will likely resume the fall from 118.65 through 108.12 low. At fall from 118.65 is seen as a correction, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48. However, sustained break of 112.78 will turn focus back to 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.