Sample Category Title

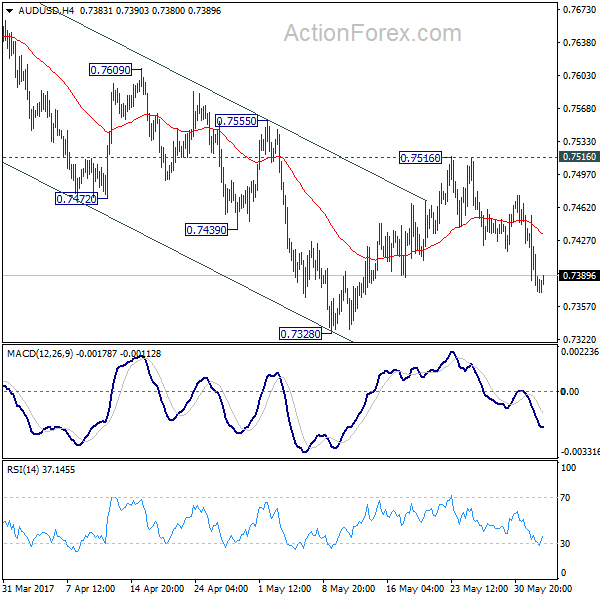

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7347; (P) 0.7400; (R1) 0.7429; More...

Intraday bias in AUD/USD remains mildly on the downside for 0.7328 support. Recovery from 0.7328 should have completed at 0.7516 after failing to sustain above 55 day EMA. Break of 0.7328 will resume whole fall from 0.7748 to 0.7144/7158 support zone. On the upside, break of 0.7516 resistance will indicate near term reversal and turn bias back to the upside.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

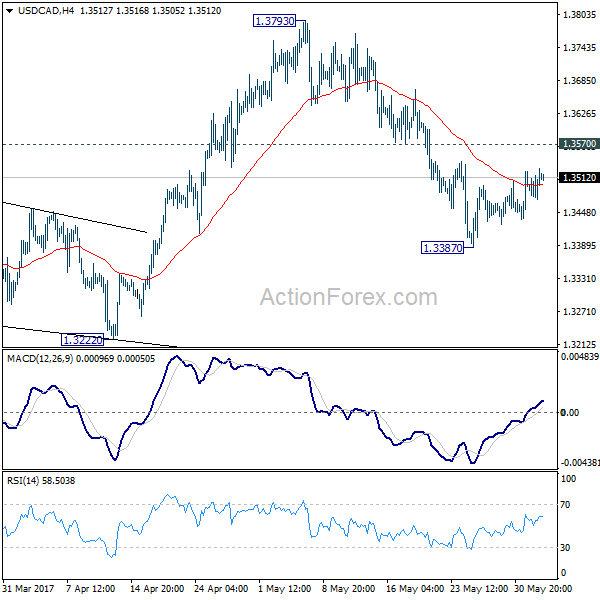

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3482; (P) 1.3505; (R1) 1.3538; More....

USD/CAD's consolidation from 1.3387 is still in progress and outlook is unchanged. Intraday bias remains neutral first. Upside of recovery is expected to be limited by 1.3570 resistance to bring another decline. At this point, we're still favoring the case that rise from 1.2968 has completed. And the larger rise from 1.2460 could have finished too. Below 1.3387 will target 1.3222 support first. Break of 1.3222 will affirm our bearish view and target 1.2968 key support level for confirmation. However, break of 1.3570 will turn focus back to 1.3793 high instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and could have completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

DOW, S&P, NASDAQ Surged to Records on NFP Optimism, Dollar Stays Mixed

Major US indices surged to new record high overnight as boosted by solid ADP job data. Positive sentiments also carry on in Asian session. DOW gained 135.53 pts, or 0.65% to close at 2114.18, a record close even if it's slightly short of record intraday high at 21169.11. S&P 500 rose 18.26 pts, or 0.76% to close at 2430.06. NASDAQ rose 48.31 pts or 0.78% to close at 6264.83. Both were also record close. Nikkei follows in Asia and is trading up 1.4% at the time of writing, at 20140. That's also the first time Nikkei tops 20000 handle since December 2015. Elsewhere, 10 year yield closed up 0.021 at 2.217 but was way off session high at 2.239. Gold struggled to find follow through buying above 1270 again and is back at 1262. WTI crude oil stays soft at around 48.

In the currency markets, Sterling stabilized this week and is trading mildly higher against all other major currencies. In particular, the rebound in GBP/JPY, more thanks to weakness in Yen, suggests short term bottoming at 141.43. But the Pound could stay vulnerable as the election on June 8 approaches. Euro follows as the second strongest major currency for the week on expectation that ECB will tweak its language to the hawkish side in June meeting. Aussie and Loonie are trading as the weakest ones for the week so far, followed by Dollar. The greenback will look into today's non-farm payroll report.

A solid NFP expected with focus on wage

The markets are expecting NFP to show 185k growth in May. Unemployment rate is expected to be unchanged at 4.4%. Average hourly earnings are expected to rise 0.2% mom. Looking at other related data, the "rip-roaring" ADP report suggests that is upside potential in today's NFP. ADP private jobs grew 253k in May, well above expectation of 181k. Four week moving average of initial claims dropped to 238k in the week ended May 27, down from 243k four weeks ago. Continuing claims stayed below 2m handle for all of the May data released so far. Employment component of ISM manufacturing rose slightly to 53.5, up from 52.0. Conference board consumer confidence dropped for the second month to 117.9 in May but the three month average stayed at the highest level since 2001. Overall, there is much prospect of a strong NFP report today. The focus would be on whether such healthy growth in job markets could push up wages.

Trump announced withdrawal from Paris climate accord

Some attributed the surge in stocks to US President Donald Trump's announce to withdraw from the Paris accord on climate change. But we would like to point out that such a move should be well priced in as Trump is just delivering his election promise. And, based on the reactions from European leaders during and after Trump's visit to Europe, it was already clear that the withdrawal was a decision made. So, we'd maintain our view that the surge in stocks was mainly due to optimism on the US economy.

Trump announced US is withdrawing from the Paris climate pact yesterday and said that "we are getting out, but we will start to negotiate and we will see if we can make a deal, and if we can, that's great." Environmentalist reacted to the announcement with anger as many could easily predict. But there were also business leaders who expressed disagreement to the move. Tesla CEO Elon Musk tweeted that his is leaving the presidential councils and warned that "leaving Paris is not goof for America or the world:". Walt Disney CE Robert Iger also resigned from presidential council over the withdrawal, "as a matter or principle". Goldman Sachs CEO Lloyd Blankfein tweeted for the first time ever that the decision was a "setback for the environment and for the US's leadership position in the world".

Elsewhere...

Japan monetary base rose 19.4% yoy in May. Consumer confidence will be released in Asian session. UK will release construction PMI in European session while Eurozone PPI will be featured US and Canada will release trade balance today too. Meanwhile, the main focus is of course on US non-farm payroll.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3482; (P) 1.3505; (R1) 1.3538; More....

USD/CAD's consolidation from 1.3387 is still in progress and outlook is unchanged. Intraday bias remains neutral first. Upside of recovery is expected to be limited by 1.3570 resistance to bring another decline. At this point, we're still favoring the case that rise from 1.2968 has completed. And the larger rise from 1.2460 could have finished too. Below 1.3387 will target 1.3222 support first. Break of 1.3222 will affirm our bearish view and target 1.2968 key support level for confirmation. However, break of 1.3570 will turn focus back to 1.3793 high instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and could have completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y May | 19.40% | 19.60% | 19.80% | |

| 5:00 | JPY | Consumer Confidence May | 43.5 | 43.2 | ||

| 8:30 | GBP | Construction PMI May | 52.6 | 53.1 | ||

| 9:00 | EUR | Eurozone PPI M/M Apr | 0.20% | -0.30% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Apr | 4.50% | 3.90% | ||

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 0.40% | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Apr | 0.0B | -0.1B | ||

| 12:30 | USD | Trade Balance Apr | -45.5B | -43.7B | ||

| 12:30 | USD | Change in Non-farm Payrolls May | 185K | 211K | ||

| 12:30 | USD | Unemployment Rate May | 4.40% | 4.40% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | 0.20% | 0.30% |

Market Morning Briefing: Aussie (0.7386) Remains Weak

STOCKS

Most of the stock indices are looking bullish for the coming week.

Dow (21144.18, +0.65%) has risen sharply and has come up to re-test previous high of 21170, also an important near term resistance. A break on the upside is needed to turn further bullish in the near to medium term.

Immediate support is seen near 12600 on Dax (12664.92, +0.40%). While that holds, a rise towards 12800 seems possible in the coming sessions.

Shanghai (3088.54, -0.45%) is trading lower and could test levels near 3050 before again bouncing back towards 3100-3150 over the next week. Overall ranged movement in the 3050-3150 region is possible in the next couple of weeks.

Nikkei (20139.31, +1.41%) has moved up sharply breaking above the 20000 resistance and while the rise sustains there is scope of rising towards 20500-21000 in the coming sessions. Near term looks bullish.

Nifty (9616.10, -0.05%) closed a little lower yesterday. We could possibly see a rise back towards 9650-9660 today. A small dip towards 9500 is possible next week before it resumes its upward rally towards 9700-9800.

COMMODITIES

Gold (1262.97) is struggling near the resistance zone of 1275-85 but the bears need a break below 1255-50 to confirm a fresh decline towards 1230 levels.

Silver (17.20) resolved the contraction phase to the downside but the support of 17.00 is holding so far. Similar to Gold, Silver requires a break below this immediate support of 17.00 for a confirmation of the downtrend.

Copper (2.57) has been consolidating in the range of 2.55-60 for the last few sessions. As discussed previously, it remains bearish below the short term channel resistance near 2.62/65 and the chances of a decline to 2.45-40 remains open but it could be prudent to be prepared for a sudden turnaround to the upside in the medium term.

Brent (50.41) is yet to show our expected recovery as it wanders just above our target/support of 50.00. A break below 50.00 may negate the chances of an immediate recovery and open up further downside towards 48.30. In that case, WTI (48.12) may test 47.00 to the downside and even lower levels below 46 may be on the cards.

FOREX

Dollar Index (97.21) has recovered some of the losses made in the previous 2 sessions on the back of better than expected American private hiring data but the resistance of 97.40-50 may limit the bounce after the US Job data release tonight.

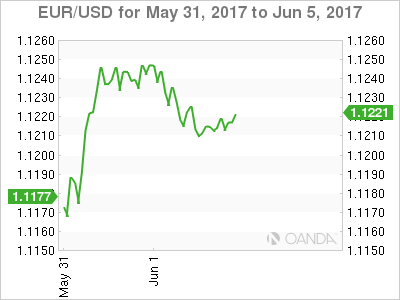

Euro (1.1217) is in a minor pause after the sharp rally earlier in the week and may resume the uptrend soon for 1.1300.

Dollar Yen (111.61) is rising towards the higher end of its near term range of 110-112 but the resistance near 112.00 is expected to hold for the week. Repeat, it’s better to wait for a breakout as any attempt to gauge any directional clue from these oscillations may turn out to be deceiving.

As discussed yesterday, the chance of a prolonged phase of sideways consolidation of Pound (1.2874) in the broader range of 1.2750-1.3000 is strengthening every day and this phase may well extend to the next week.

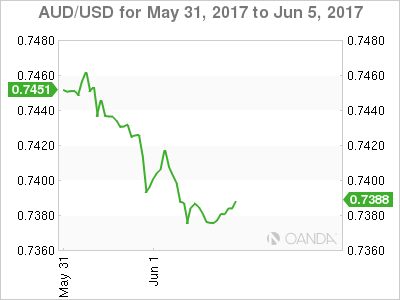

Aussie (0.7386) remains weak and a failure to end the week above 0.74 may push it down to 0.7325 next week.

Dollar Rupee (64.50) to remain within 64.40-64.60 this week. A break on either side is needed to get some directional clarity.

INTEREST RATES

The US yields are mixed. The shorter term yields of 2YR and 5Yr are trading slightly higher today while the longer term 10YR (2.22%) and the 30Yr (2.87%) yields are stable.

The UK-US 10YR (2.16%) is headed lower and has enough scope on the downside. We could possible see a short bounce from 2.0% in the next week.

The UK yields have bounced back from immediate support levels as expected and could now move up in the coming sessions. The 5Yr (0.507%), 10YR (1.061%) and the 20YR (1.618%) are trading higher today.

The Japan yields have risen but could remain ranged in the near term. The 10Yr (0.06%) has risen the most among the other tenure yields and could be headed towards 0.08-0.10% in the near term.

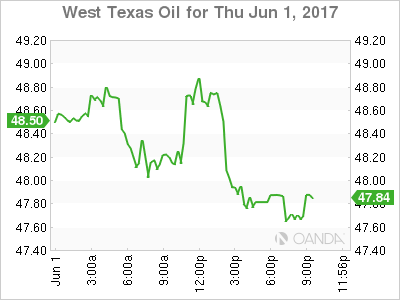

Oil Prices Poised For Further Losses

Key Points:

- Oil's technicals are looking rather grim.

- The commodity seems to be shrugging off fundamental developments.

- The $45 handle could now be in the crosshairs for the bulls.

Oil prices could be in trouble moving forward as they seem to have shrugged off both renewed commitments from OPEC and a 6.43M barrel draw in US inventories. This could be, in part, a result of the technical bias which is looking fairly dour going ahead. Indeed, current readings are suggesting that we could see the commodity retreats to the $45 mark within a fairly short timeframe.

More precisely, whilst we are currently seeing oil hover above a robust support level at 47.70, there is growing evidence to suggest further losses are now warranted. For one thing, we can see that the 12 and 20 day moving averages have just completed a bearish crossover and the overall EMA bias is now in highly bearish. Furthermore, the MACD and signal line have also experienced a crossover – a sign that oil prices are predisposed to a tumble in the coming days.

If we take a closer look at a number of other technical indicators, the story remains largely consistent with the EMA bias. Notably, the Parabolic SAR is still well and truly above price action and is, therefore, signalling that a continuation of the downtrend is likely to occur. Moreover, a decline back to the downside of the bearish channel would be in line with the regression trend analysis which continues to suggest downside risks are abundant.

Speaking of the channel, the structure highlighted in the above chart represents a near-term cap on downsides but we may see a reversal prior to an actual challenge to the lower constraint. Specifically, the $45 handle should hold as a support zone given that there is a historical zone of support around this price. Additionally, both stochastics and RSI would be deeply oversold around this price if oil tumbles at its current pace which will be worth keeping in mind.

Ultimately, the future isn't looking too buoyant for oil prices and it's only likely to get worse unless OPEC members can pull something major out of their collective hats. However, do keep an eye on the North American rig count data as, if the uptick in active rigs begins to slow, this could help to give some credence to OPEC's cuts – potentially saving the embattled commodity from sinking much further.

It’s All About The Wages

It's all about the wages

The Dollar is opening an on slightly better footing this morning in part due to a big May ADP print ( +253) and more robust ISM manufacturing data, and as traders trim short USD positions ahead of tonight's Key NFP data. While the market took solace in the solid ADP prints, investors are mindful that this evening's absolute jobs number will influence USD sentiment much less than the wages component. It's all about the wages as the AHE will be a key metric the for Fed Watchers.

But wise not to get too complacent on the headline print as the 50K Delta over/under could significantly shift rate hike expectation probabilities beyond June.Given the recent string of middling US economic data, the greater risk would be for a downside miss given the current negative dollar view. Whereas it would likely take a daily double on both the Headline and AHE for the Greenback to convincingly break out of its current funk No question, with the major Trump Tax themes growing dimmer by the day, it's going to take a substantial jolt of the data to shake this dollar doldrums

The Dow, S&P and Nasdaq all galloped to record highs as equity investors were fired up by the ADP report. After a string of weak to middling economic data this past week, the large print has eased investor angst that the US economy is running out of steam and now appear more upbeat heading into tonight's NFP

The roller coaster affectionately dubbed 'Oil Patch' is heading lower again. After making it's way up the lift hill on significant US inventories draw we're back on the dive drop as the old familiar themes come to the fore.The supply glut continues to weigh on near-term sentiment, despite the decline in US inventories, while the prospects of shale output production are rising weights substantially on future prices.

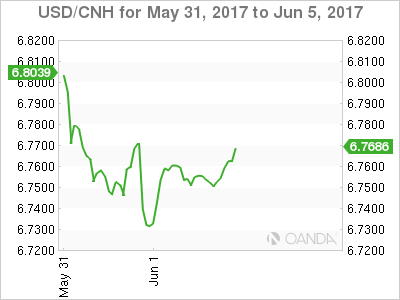

Chinese Yuan

A follow up to yesterday's major CNH headlines: Finally, a reprieve from the severe Tom Next funding crisis as the three-day carry fell from 300 to 85 in London. And predictably the USDCNH bounced above 6.75 after plummeting to 6.7250 in Asia. While the Pboc has made their views loud and clear, but as the funding crisis abates, I suspect the markets will sheepishly test the water probing every so slightly higher to challenge the Pboc's resolve.But after getting spanked this week, I believe the aggressive Yuan bears will either go into hibernation or take to the sidelines licking their wounds for the foreseeable future.

Pre CNY fixing: USDCNH trading 6.7570

Australian Dollar

AUD is finally caving and was hammered mercilessly thanks to China's Caixin manufacturing PMI slipping into dreaded contraction zone and plummeting iron ore prices.

The commodity bloc is receiving little support from oil prices which have fallen over a dollar per barrel this morning, and with Iron Ore prices having trouble finding a bid anywhere, we could be setting up for a purposeful move lower for the Aussie

The heaviness in iron ore was difficult to side step as it's incredibly challenging for the Government to overcome budgetary shortfalls created by these sharp drops. And the outlook doesn't look any rosier with the tepid China PMI data raising concerns about manufacturing sector demand while the growing stockpiles are a burden to supply.

Despite the growing list of Aussie negatives, we're likely in a holding pattern for the day after failing to take out .7365 level overnight.The proximity of NFP suggests the next move will be dollar driven, so traders may either opt to sell at better levels post NFP or jump on the waggon if the greenback returns to favour post data. But with high level of USD risk entering the week's end, dealers preference to express their negative AUD bias is more likely on the crosses with the EURAUD the current market favourite

Next week focus will pivot to domestic concerns as the RBA board meeting, and Q1 GDP will hog the limelight. While no change in interest rates is expected at next week's RBA meeting, the markets will key on the RBA's post-meeting statement. But unless the RBA alters their steady as she goes, that too will most likely be a non-event and traders will turn their focus back to external drivers.

EURO

The monthly end portfolio rebalancing supply of dollars along with some hawkish ECB rhetoric has helped the EURO sentiment into weeks end. And while the current landscape suggests the short-term market is long and want's to get more extended on dips the increasingly likely Italian elections in September/October has thrown a monkey wrench in the works, and probably tempered some expectation for a near-term shift in ECB policy. But none the less the EURUSD should continue to grind higher based on solid EU economic data alone, and if it can break through the large supply of Euro's currently on offer through 1.1250-65 region, a break of 1.1300 is all but a done deal.

Hard to make too much of a meal of this morning price action, it's notably quiet but not untypical of pre NFP trading conditions.

USD Higher Ahead Of NFP

Dollar Rebounds After Strong Private Job Gains

The US dollar is higher against major pairs on Thursday after the ADP added 253,000 jobs in May beating expectations of a 181,000 gain. The Institute for Supply Management (ISM) released the manufacturing index showing a slight gain in April overall holding steady and sending a positive signal on the US manufacturing sector. The dollar has struggled for most of the week until finally getting some traction from positive economic indicators. Traders will look to the U.S. non farm payrolls (NFP) released on Friday, June 2 at 8:30 am EDT for more guidance on the currency.

The Memorial Day holiday on Monday compress the data releases and Thursday in particular was busy. The positive ADP gains were balanced against a larger than expected weekly unemployment claims in the US. 248,000 individuals filed for unemployment insurance last week, analysts were anticipating 239,000. US crude oil inventories had a big weekly drawdown of 6.4 million barrels beating the forecast of 2.7 million. Gasoline inventories also fell by 2.9 million barrels and only distillates showed a small buildup of 400,000 barrels.

Federal speakers continue to support the idea of two or more interest rate hikes this year. On Thursday it was Fed Governor Jerome Powell to speak on behalf of further tightening and to throw some numbers on the final size of the central bank’s balance sheet ($2.5 – $3 trillion). The U.S. Federal Reserve is expected to raise interest rates after the meeting on June 14 ends. The market is pricing a 95.8 percent probability of the benchmark US rate to be in the 100 to 125 basis point range. With the June rate hike almost a foregone conclusion more data is needed to figure out if the Fed will hike another time before the end of the year.

The EUR/USD lost 0.225 percent in the last 24 hours. The single pair is trading at 1.1208 after the strong ADP private payrolls report came in stronger than expected. The 248,000 gain is margin the fastest pace in private employment since 2014. The ADP has set higher expectations for the U.S. non farm payrolls (NFP) report to be published Friday. The US Jobs monthly report is the biggest indicator in the market. Solid fundamental data has helped the USD regain the momentum it has lost this year as Political turmoil has swamped the Trump Administration.

The dollar was an early beneficiary of the President’s plan to boost growth through tax reform and infrastructure spending, but those plans were derailed by prioritizing other policies that used up a lot of political capital from the White House, and still did not end up in anything concrete. The current Russian connection investigations could potentially further delay tax reform who is now not expected to be put to congress until August. The NAFTA negotiations will start around then as well and is uncertain what strategy will the Trump administration will employ, or if they will have enough time to craft one ahead of the trilateral negotiations.

Ending the week on a high with strong data will boost the USD which has suffered from political uncertainty. Political risk is on the rise on a global scale as the snap election in the UK and the parliamentary elections in France are entering their final stages.

The price of oil gained 1.244 percent on Thursday. West Texas Intermediate is trading at $48.76 after the larger than expected drawdown of weekly US inventories. WTI came close to breaking above the $49 but remains close as the battle between the Organization of the Petroleum Exporting Countries (OPEC) with their production cut agreement and the US shale industry with ramping supplies have keep the price of energy within a range despite volatility.

Market events to watch this week:

Friday, Jun 2

4:30 am GBP Construction PMI

8:30 am CAD Trade Balance

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

Swiss Q1 GDP: Slow and Steady Growth

While Swiss Q1 GDP undershot the consensus forecast, the underlying details are not as weak as the headline figure suggests. Continued muted growth will not likely spur inflationary pressures in the foreseeable future.

Setting up for Potential Rebound in Q2

Data released this morning revealed that real GDP in Switzerland grew 0.3 percent in Q1 (1.1 percent annualized), undershooting the consensus expectation which called for 0.5 percent growth. Despite the miss, Q1 growth was the strongest since Q2-2016. A breakdown of Swiss output into its underlying demand components shows mixed results in the first quarter.

Household consumption was notably weak, growing just 0.1 percent in Q1. However, a slowdown in personal consumption growth could have been expected given its 0.9 percent increase the previous quarter. Government spending increased 0.4 percent to mark its twelfth consecutive quarter of expansion. Business investment in equipment and software increased a strong 1.7 percent on the quarter while construction investment edged up 0.4 percent.

Moreover, exports (excluding valuables) jumped 3.9 percent on the quarter, following a 3.5 percent pullback in Q4-2016. Likewise, exports of services grew 3.2 percent. Prior to this quarter, Swiss export growth had been lackluster, reflecting slow economic growth in many of Switzerland's trading partners as well as the appreciation of the Swiss franc. As economies in the Eurozone begin to gain momentum, as we expect, Swiss export growth should remain positive. On the other hand, real appreciation of the Swiss franc in recent years has eroded the price competitiveness of goods and services produced in Switzerland relative to goods and services produced in other countries, which could serve as a headwind for export growth moving forward. Moreover, nominal inventories declined 1.7 percent, and it appears that real inventories are weighing on overall growth. However, the current drag of inventories on topline growth provides the potential for a bounce back in coming quarters.

Inflationary Pressures Relatively Absent

Consumer price inflation in Switzerland emerged from negative territory in January for the first time in over two years. The core CPI followed suit in March, however both price measures remain dangerously close to slipping back into negative territory. The aforementioned appreciation of the franc has put downward pressure on inflation via lower import prices. The Swiss National Bank (SNB) has adopted extraordinary policies in recent years in an effort to bring about higher prices on a sustained basis. Between mid- 2011 and late 2014 the SNB held its target rate for 3-month Swiss franc LIBOR at 0 percent. In January of 2015, the SNB cut rates deeper into negative territory by reducing its target for 3-month Swiss franc LIBOR to -0.75 percent. Although inflation has recently been positive, the SNB likely will maintain negative rates for the foreseeable future.

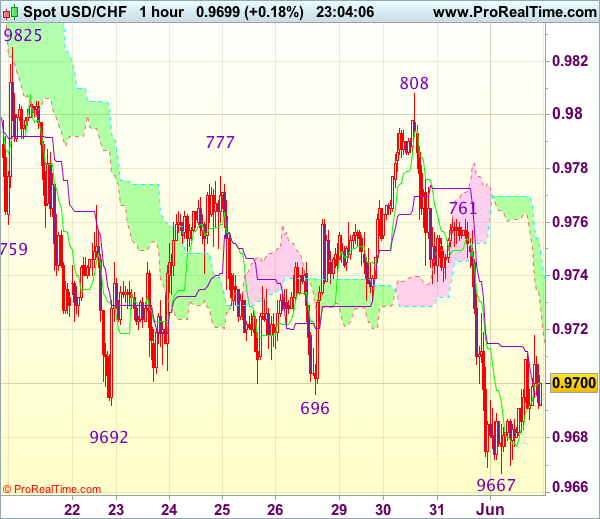

Trade Idea Wrap-up: USD/CHF – Sell at 0.9740

USD/CHF - 0.9707

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9701

Kijun-Sen level : 0.9693

Ichimoku cloud top : 0.9749

Ichimoku cloud bottom : 0.9729

Original strategy :

Sell at 0.9740, Target: 0.9640, Stop: 0.9775

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9740, Target: 0.9640, Stop: 0.9775

Position : -

Target : -

Stop : -

Although the greenback did stage the anticipated rebound to 0.9808, dollar ran into heavy selling pressure at 0.9808 earlier this week and has dropped sharply since, the subsequent breach of previous support at 0.9692 confirms recent decline has resumed and may extend further weakness to 0.9655-60, then 0.9630, however, near term oversold condition should prevent sharp fall below 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808), bring rebound later.

In view of this, we are looking to turn short on recovery as 0.9735-40 should limit upside and bring another decline. Only break of resistance at 0.9761 would abort and suggest a temporary low is possibly formed, risk test of said resistance at 0.9808 but only break there would provide confirmation.

ISM: Continued Growth Signals, Rising Prices

The ISM manufacturing index rose to 54.9 in May compared to 54.8 in April. Expansion remains the signal as production, new orders and employment remain in growth mode. Rising input costs will pressure profits.

May Signals Expansion, Factory Activity Still Solid

Consistent with several regional purchasing managers (Chicago, Philadelphia) indices released over the past few weeks, growth in the manufacturing sector continues to improve. The May ISM came in at 54.9 (top graph). When we examine the graph, we witness how much intracycle volatility is characteristic of manufacturing sentiment, so ups and downs are endemic to this survey. We estimate industrial production up 2.0-2.5 percent in the second half of 2017.

The production index came in at 57.1 and is now slightly above its twelve-month average. Moreover, the pipeline for activity remains positive as new orders were up at 59.5. Strength in new orders (middle graph) stems, in part, from the improved global backdrop. Fourteen sectors reported a gain in orders including paper, primary metals and machinery. Export orders came in at 57.5, with 11 industries reporting growth including textiles, wood and paper. While not seasonally adjusted, the index indicates continued gains in exports.

The employment index came in at 53.5 with 11 industries reporting job gains to include furniture, electrical equipment and appliances. Manufacturing hiring remains on the upswing, with the employment index up near the highs since mid-2011. The index indicates another solid gain is in store for manufacturing payrolls in May.

Supplier Deliveries Indicate Further Economic Gains

The supplier delivery index remained above breakeven indicating slower deliveries - a positive for growth. Slower deliveries are associated with incoming orders above the pace of outgoing deliveries. These backlogs signal pent-up production for the future. Eleven industries reported slower supplier deliveries in May including plastics, furniture and electrical equipment.

Input Inflation Pressures Mounting: Challenge for Profits

Price pressures continue to mount in the manufacturing sector. Prices paid, bottom graph, came in at 60.5 in May with 15 of the 18 sectors reporting higher prices paid. Among those paying higher prices include electrical equipment, appliances, apparel and furniture.

Commodities were up in price, including aluminum, corrugated boxes, steel and steel tubing. Capacitors and electronic components remain in short supply.

Our outlook for producer prices remains at 2 percent plus for 2017 compared to 0.4 percent for 2016 and an outright drop in prices in 2015. Rising input prices and rising interest rates will combine to put pressure on many firms' profit outlooks going forward. We estimate pre-tax profit growth at 3.4 percent in 2017.