Sample Category Title

Dollar Direction to be dictated by Climate

Thursday June 1: Five things the markets are talking about

Capital markets are currently experiencing a number of pressure points that are managing to keep investors on the toes.

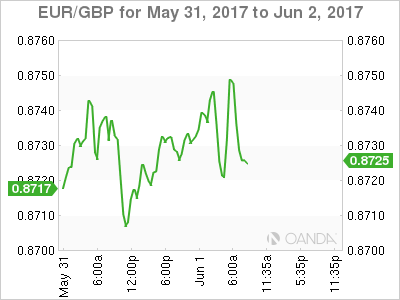

Sterling remains soft on investor fears that PM Theresa May could lose control of parliament in next week's U.K General Election (June 8). Yesterday's YouGov poll showed May could be well short of the number of seats needed to form a government, raising the prospect of political turmoil just as formal Brexit talks are about to begin.

In China, equities closed under pressure after a private survey - the Caixin manufacturing gauge - revealed that the country's manufacturing activity contracted last month for the first time in nearly a year. The results differed with yesterday's data that suggested growth remained relatively steady.

In the U.S, aside from Trump's administration being under FBI scrutiny, a decision by the President on whether the U.S will remain in the Paris agreement - global pact to fight climate change - will keep markets and investors on edge (3:00 pm EST).

At 10:00 am EST U.S manufacturing ISM data is expected to show it expanded at a robust pace last month (54.7).

1. Stocks mixed results

In Japan, the Nikkei snapped a four-day losing run (+1.1%) on upbeat data and a weaker yen (¥110.11). Indicators released overnight showed that corporate Japan picked up the pace of capital expenditures Q1. The broader Topix also traded in the black (+1.1%) after trading up +2.4% in May for its biggest monthly gain year-to-date.

In Singapore, the Straits Times Index climbed +0.5%, while down-under, the Aussies S&P/ASX 200 Index rose +0.2% after swinging between gains and losses amidst economic releases from China.

In Hong Kong, the Hang Seng Index climbed +0.5% after completing its fifth consecutive monthly gain.

In China, the Shanghai Composite Index slipped -0.5% percent, after a four-day rally on investor profit taking.

In Europe, indices are trading higher across the board with notable outperformance in Italy, and France. A number of softer corporate earnings and commodity and energy prices are providing slight pressure to the FTSE 100; however, a weaker pound is capping current losses at the moment.

In the U.S, stocks are expected to open in the black (+0.1%).

Indices: Stoxx50 +0.5% at 3573, FTSE +0.3% at 7545, DAX %+0.4 at 12670, CAC-40 +0.8% at 5325, IBEX-35 +0.1% at 10893, FTSE MIB +1.3% at 20993, SMI +0.6% at 9068, S&P 500 Futures +0.1%

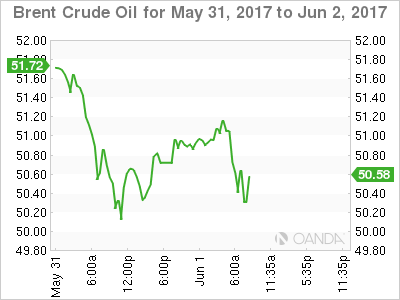

2. Oil rises on U.S stockpile draw, doubts over climate accord

Ahead of the U.S open, oil prices are rallying from yesterday's three-week low, mostly supported by expectations that the U.S could pull out of the Paris climate agreement and by yesterday's report that showed U.S stockpiles falling more than expected.

Note: Trump said he would announce at 3:00 pm EST his decision on the agreement.

Brent crude futures are up +58c, or +0.8%, at +$51.34 a barrel - on Wednesday, it fell -$1.53, or -3%, to close at +$50.31 a barrel.

Note: It was Brent's lowest close since May 10 and the contract dropped -2.7%in May, the third monthly decline.

U.S West Texas Intermediate is up +64c, or +0.8%, at +$48.96 a barrel - it dropped -$1.34, or -2.7%yesterday to settle at +$48.32 per barrel.

Note: It was the lowest close since May 12. The U.S benchmark also fell for a third month in May, declining -2%.

API data yesterday showed that crude inventories were down by -8.7m barrels at +513.2m in the week to May 26. The market was expecting a -2.5m drawdown.

Note: The U.S EIA report is due at 11:00 am EDT, delayed by a day because of the Memorial Day holiday this week.

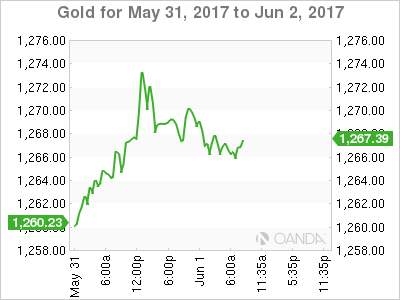

Gold has edged lower overnight (-0.2% at +$1,266.08 per ounce), but held near the five-week highs hit in the previous session, as expectations that the U.S. Federal Reserve will hike interest rates this month weighed on prices but geopolitical concerns provided some support.

3. Global yield curves little changed

U.S Treasuries have rallied this week on month-end buying adding to demand that has been building along with declining inflation expectations.

The yields on U.S 10's settled yesterday at +2.198%, and have backed up +1 bps ahead of the U.S open.

Data on Tuesday showed the Fed's preferred gauge of inflation - PCE - ticked up in April, but on an annual basis, remained stuck below the Fed's +2% target.

Elsewhere, benchmark yields in Australia backed up +1bps to +2.40%.

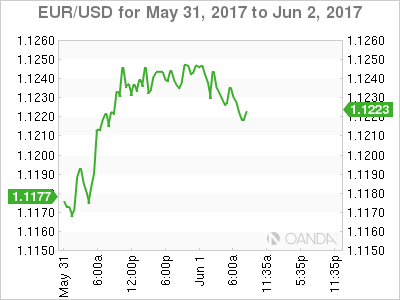

4. Dollar looking for direction

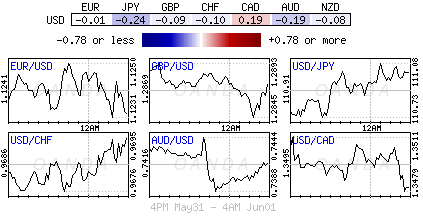

USD is trying to find its 'sea legs' in the first day of trading in a new month. The next couple of session will see various job-related data (today's ADP at 08:15 am EDT, and tomorrow's non-farm payroll (NFP) report at 08:30 am EDT) dictate the greenbacks rate differential direction.

Elsewhere, the EUR (€1.1227) continues to probe its seven month highs supported by the Bundesbank speak that the current eurozone outlook would suggest that the ECB should start to discuss "whether and when to change forward guidance."

Sterling (£1.2849) trades well under the psychological £1.29 handle as the currency continues to face headwinds ahead of next week's U.K Parliamentary election.

Note: More polls continue to showing PM May's Conservative in front, but her lead continues to dwindle.

Times/YouGov general election weekly poll: Conservatives +42% (-1pts), Labour 39% (+3pts)

Sun/SurveyMonkey general election poll: Conservative Party +44% (unchanged), Labour Party +38% (+2pts)

5. Eurozone Manufacturing PMI Unrevised

Data this morning shows that the manufacturing PMI for the eurozone was unrevised at 57.0 in May, up from 56.7 in April and in line with market expectations - (Beats: Germany, U.K, Spain, Russia, Hungary, Turkey; Misses: France, Italy, Sweden, Norway, Poland).

The measure points to robust growth in the sector, with businesses reporting that they added new workers at the fastest pace in the twenty-year history of the survey.

Digging deeper however, businesses raised their prices at the slowest pace in four-months, an indication that the stronger economic recovery may not lead to a sustained rise in inflationary pressures and would suggest that the ECB remains on the side line in the medium term.

DAX Edges Higher on Strong German, Eurozone Manufacturing Reports

The DAX index has posted small gains in the Thursday session. Currently, the DAX is trading at 12,656.25 points. On the release front, German and the Eurozone Manufacturing PMIs both indicated expansion. German Manufacturing PMI improved to 59.4, a shade under the estimate of 59.5. The Eurozone report rose to 57.0, matching the forecast. The US will release ISM Manufacturing PMI. Employment data is in the spotlight for the remainder of the week. Thursday's releases include ADP Nonfarm Payrolls and unemployment claims. On Friday, the US releases Nonfarm Employment Change, which is expected to drop to 186 thousand.

A solid and reliable German economy has been the backbone of an improved eurozone economy in 2017, but recent consumer spending data is raising concerns that the largest economy in the euro-area is slowing down. In April, retail sales declined 0.2%, compared to a forecast of +0.4%. This marked the third decline in 2017, and if there is further contraction in the second quarter, the eurozone economy could be in trouble. Although the German labor market remains strong, this has not translated into higher inflation, which declined 0.2% in May, after a flat reading of 0.0% in April.

The US labor market remains very strong, boasting an unemployment rate of just 4.4%. Despite healthy employment numbers, the US economy was unable to avert a slowdown in the first quarter of 2017, and it's questionable if we'll see improvement in the second quarter. Still, a rate hike from the Federal Reserve at the June 14 meeting remains very likely, with the odds of a 0.25% hike priced in at 89%. As for the second half of 2017, the likelihood of rate move is significantly lower. The odds for a September rate stand at just 26%, with the markets skeptical as to whether the Fed will make further moves this year if inflation remains below the Fed target. Political concerns are a serious worry, as the Trump administration is embroiled in scandals, with several congressional investigations probing into Trump's alleged connections with Russian politicians. A weakened White House raises doubts if Trump will be able to keep his election promises to lower taxes and cut government spending.

Daily Technical Analysis: EUR/JPY Cup With Handle Pattern Suggests Further Gains

The EUR/JPY has formed a cup with handle pattern (blue rectangle) and currently it is targeting D H4/ 100 % Fibonacci extension confluence. The POC zone serves as a strong support and possible now moment buyers could buy from the zone if we see a retracement into the POC zone. The POC 124.30-50 (EMA 89, trend line, handle top, ATR pivot, 61.8 Fib extension). EUR/JPY is targeting 124.98 and if we see a 1h breakout or 4h close above the level then 125.30 is possible.

USD/JPY Bulls Break Downtrend Line Resistance

US Pending home sales (YoY) released yesterday saw a 3.3% drop in April, from a 0.8% growth in March, marking the biggest drop since June 2014.

After the release of the data USD weakened across the board. USD/JPY hit a 2-week low of 110.47.

On Thursday, June 1st, in early European trading session, the USD/JPY bulls have regained momentum due to the rebound of USD.

On the 4-hourly chart the USD/JPY bulls have breached the near-term major downtrend line resistance, where another resistance level at 111.00 converges, indicating increased bullish momentum.

If the bulls can successfully hold above the level at 111.00 we will likely see USD/JPY continuing edging up.

The resistance level is at 111.20 followed by 111.40 and 111.70.

The support line is at 111.00 followed by 110.70 and 110.50.

The crucial US ISM manufacturing PMI for May will be released this afternoon at 15:00 BST with a market consensus 54.5 after the previous reading of 54.8.

It has remained above 50 since October 2016 but has experienced a falling trend over the past three months. Be aware that it will likely cause volatility for USD/JPY.

Sterling Offers Slight Recovery

- Sterling offers slight recovery

- Aussie data disappoints but Chinese data is worse

- Butter prices sharply higher

The Leader 'nearly all' the leaders debate yesterday didn't tell us much we didn't already know. Whether Theresa May's decision to stop the event will prove damaging is another thing. The BBC is clearly in love with Jeremy Corbyn and are trying hard not to make it too obvious (maybe Laura Kuenssberg could try harder) but the markets haven't really reacted much. Sterling is a tad stronger against the US Dollar, but remains subdued against the Euro; wallowing in the €1.14 area.

Sterling rose against the Australian Dollar after last night's data releases. Much stronger than expected Australian retail sales numbers showed a monthly rise in sales of 1.0% was more than three times the consensus forecast, but that was offset by the much weaker than forecast personal capital expenditure data and a poor release from China. Their Manufacturing Purchasing Managers' Index (PMI) was below the magic 50. That's the demarcation line between growth and contraction, so it has repercussions for the countries that supply China with its raw materials and that very definitely includes Australia. At the time of writing, we have not yet seen Australia's Commodity Index, but that too will impact the Aussie Dollar.

Today's data diary includes a smattering of manufacturing data from across the Eurozone, but nothing that spans the whole currency sharing bloc. The Eurozone Manufacturing PMI is looking good once more, at 57.0 for May, and employment across Europe in the sector growing rapidly.

UK data is limited to the Manufacturing PMI - posting another healthy growth figure of 56.7 - and a 10-year government bond auction. These are always interesting as a litmus test of the bond market's view of future interest rates.

US data is also dominated by manufacturing sector stuff, but we will also see the weekly Jobless Claims statistics and the Private Payroll data from ADP. I suspect these figures will be little more than a sideshow, because tomorrow brings the official employment report and that is still the first piece of data that covers the previous month. Whilst the Non-Farm Payroll count doesn't carry the same weight and excitement it did a decade ago, it is still a bellwether for the US economy.

And a lot of newswires are carrying the story that wholesale butter prices have soared since reports were published suggesting the belief that butter is bad for you is a myth. The story is slightly skewed, because butter prices slumped last year, so the recovery is from a very low level, but it does serve to highlight the ebb and flow of scientific opinion. It reminds me of the Woody Allen film, Sleeper, where, in the future, cabbage is bad for you, but smoking is encouraged for its health benefits. It could happen.

Oh - and stronger dairy prices are very good news for the Kiwi Dollar, so it will strengthen if this trend continues.

Late night in the office

Jenny the receptionist has worked late to finish a report and as she is packing up her things she sees the Chairman of the company standing in front of the shredder looking puzzled.

"Can I help you Mr Charterhouse?" she says.

"Oh can you Jenny? This is a highly confidential document. How do you work this thing?"

She puts down her handbag and walks across. "You just turn it on here and put the paper in there," she says.

"The Chairman does as she suggested and the turns to her. "Thanks Jenny. You're a lifesaver. Now how do I tell it I need three copies?"

Market Update – European Session: Global Market Updates

Notes/Observations

UK house prices fell for the 3rd month in a row (first time since 2009)

European Manufacturing PMI data mixed (Beats: Germany, UK, Spain, Russia, Hungary, Turkey; Misses: France, Italy, Sweden, Norway, Poland)

Swiss Q1 GDP misses expectations (QoQ: 0.3% v 0.5%

Overnight

Asia:

China May Caixin PMI Manufacturing registered its 1st contraction in 11 months (49.6 v 50.1e)

BoJ Harada: Current stimulus policy would be sufficient to achieve 2% inflation target; will withdraw stimulus when program succeeds

Europe:

ECB's Weidmann (Germany): Current outlook suggested ECB should start to discuss whether and when to change forward guidance. Believed that inflation would be higher even with reduced stimulus

ECB's Nowotny (Austria): possible that inflation rates will remain low in the long term; one could question whether current 2% ECB inflation target as still realistic. Before any rate changes, purchase of govt bonds will probable be cut as first step

Times/YouGov general election weekly poll: Conservatives 42% (-1pts), Labour 39% (+3pts)

(UK) Sun/SurveyMonkey general election poll: Conservative Party 44% (unch), Labour Party 38% (+2ppts)

Americas:

President Trump: I will be announcing my decision on Paris Accord, Thursday at 3:00 P.M E

Fed's Williams (moderate, non-voter): 3 rate increases for this year is base line view; 4 hikes possible if US economy strengthens Energy:

Weekly API Oil Inventories: Crude: -8.7M v -1.5M prior (biggest draw since Sept 2016)

Economic Data

(IE) Ireland May Manufacturing PMI: 55.9 v 55.0 prior (48 straight month of expansion)

(IN) India May Manufacturing PMI: 51.6 v 52.5 prior

(CH) Swiss Q1 GDP (miss) Q/Q: 0.3% v 0.5%e; Y/Y: 1.1% v 1.3%e

(UK) Nationwide House Price Index (miss)M/M: -0.2% v +0.2%e (3rd straight decline); Y/Y: 2.1% v 2.4%e

(RU) Russia May PMI Manufacturing PMI: 52.4 v 50.8e (10th month of expansion)

(FI) Finland Q1 GDP Q/Q: 1.2% v 1.0%e; Y/Y: 2.7% v 1.7%e

(SE) Sweden May Manufacturing PMI (miss): 58.8 v 62.4e

(NL) Netherlands May Manufacturing PMI: 57.6 v 57.8 prior

(NO) Norway May Manufacturing PMI: 54.3 v 55.0e

(HU) Hungary May Manufacturing PMI: 62.1 v 56.6e

(PL) Poland May Manufacturing PMI: 52.7 v 54.5e (30th month of expansion)

(TR) Turkey May Manufacturing PMI: 53.5 v 51.4e (3rd month of expansion)|

(ES) Spain May Manufacturing PMI (beat): 55.4 v 54.7e (43rd month of expansion)

(CZ) Czech May PMI Manufacturing: 56.4 v 57.9e (9th month of expansion)

(CH) Swiss May PMI Manufacturing: 55.6 v 57.8e

(IT) Italy May Manufacturing PMI (miss): 55.1 v 56.0e (9th month of expansion)

(FR) France May Final Manufacturing PMI (miss): 53.8 v 54.0e (confirmed 8th month of expansion)

(DE) Germany May Final Manufacturing PMI (beat): 59.5 v 59.4e (confirmed 30th month of expansion and highest since Apr 2011)

(EU) Euro Zone May Final Manufacturing PMI: 57.0e v 57.0 prelim (confirmed 46th straight month of growth and highest since April 2011

(GR) Greece May Manufacturing PMI: 49.6 v 48.2 prior(9th month of contraction)

(IT) Italy Q1 Final GDP (beat) Q/Q: 0.4% v 0.2%e; Y/Y: 1.4% v 0.8%e

(UK) May Manufacturing PMI (miss): 56.7 v 56.5e (10th month of expansion)

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.14B vs. €3.5-4.5B indicated range in 2021 and 2066 bonds

Sold €2.7B in new 0.05% 2021 SPGB; Avg yield: +0.021% v -0.142% prior, Bid-to-cover: 1.96x v 1.44x prior (under 1.15% July 2020 SPGB on May 18th 2017)

Sold €1.44B in 3.45% July 2066 SPGB; Yield: 3.249% v 2.688% prior; Bid-to-cover: 1.3x v 1.56x prior (Oct 20th 2016

(ES) Spain Debt Agency (Tesoro) sold €500M vs. €250-750M indicated range in 1.0% Nov 2030 I/L bond; Real Yield: 0.832% v 0.679% prior; Bid-to-cover: 3.26x v 1.76x prior

(FR) France Debt Agency (AFT) sold total €8.273B vs. €7.5-8.5B indicated range in 2027, 2032 and 2039 Oats

Sold €5.08B in 1.00% May 2027 Oat; Avg Yield: 0.72% v 0.81% prior; Bid-to-cover: 1.76x v 2.02x prior

Sold €1.72B in 5.75% Oct 2032 Oat; Avg Yield: 1.10% v 0.52% prior; Bid-to-cover: 1.86x v 1.49x prior

Sold €1.473B in1.75% 2039 green Oat; Avg Yield: 1.51% v 1.48% prior; Bid-to-cover: 1.87x v 1.92x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 +0.5% at 3573, FTSE +0.3% at 7545, DAX %+0.4 at 12670, CAC-40 +0.8% at 5325, IBEX-35 +0.1% at 10893, FTSE MIB +1.3% at 20993, SMI +0.6% at 9068, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes

European Indices trade higher across the board with notable outperformance in Italy, and France. In a busy morning for Macro news Germany, UK and Spain saw Manufactring PMI beat forecasts whilst Italy, Switzerland and France saw slight misses. On the corporate front UK traded First Group trades down over 5% following their FY results and recommendation not to pay a dividend, whilst shares of Inmarsat one of the leading risers following reports that Softbank is looking into the company, Johnson Matthey trades lower after missing on Rev. Looking head, earnings expected from Tech Data, Express and Dollar General out of the US.

Equities

Consumer discretionary[FirstGroup [FGP.UK] -6% (Earnings, Recommends no div), 888 [888.UK] -3.6% (O Shaked shares trust sell 40M shrs at 270p/shr), Watkins Jones [WJG.UK] -1.2% (Earnings)]

Materials: [Johnson Matthey [JMAT.UK] -0.9% (Earnings), Voestalpine [VOE.AT] +0.2% (Earnings)]

Financials: [Barclays [BARC.UK] -0.4% (Places 286M shares of BAGL)]

Telecom: [Inmarsat [ISAT.UK] +5.8% (Reports Softbank is interested)]

Healthcare: [Genfit [GNFT.FR +6% (Positive Outcome from the 1-year Pre-Planned Safety Review by the DSMB, in RESOLVE-IT Phase 3 Clinical Trial with Elafibranor)]

Speakers

German Chancellor Merkel: Germany and China jointly stand for free trade; cited concerns over global uncertainty. Both leaders supported WTO rules (**Note: comments alongside China Premier Li in Berlin)

Netherlands Fin Min Dijsselbloem: 2017 budget surplus revised lower from 0.5% to 0.2% citing need to spend €200M extra a year for education and more expenses for health care

Russia Econ Min Oreshkin: May CPI YoY reading seen around 3.9-4.0%. Inflation may slow below the year-end forecast of 3.8%. To see lower inflation and a smaller budget deficit if OPEC and non-OPEC oil producers agree to extend a production cut deal

Poland Dep Fin Min Skiba: Q2 GDP growth to be close Q1 levels (**Note: Q1 data beat expectations with YoY at 4.0%)

China Premier Li: Germany was China most important partner within the EU. China would stand by pledges tied to Paris accord on climate

Currencies

USD tried to find some steady legs as the month of June began as the greenback tried to solidify expectations of a rise in interest rates this month. The next few session will see various job-related data out of the US (ADP today, jobless claims on Thursday and Non-Farm payrolls on Friday).

EUR/USD probed its recent 7-month highs as the month began aided by German central bank speak that current outlook suggested ECB should start to discuss whether and when to change forward guidance. The Euro drifted off its best levels and was around 1.1230 area just ahead of the NY morning.

GBP/USD was holding just under the 1.29 area but faced headwinds ahead of next week's Parliamentary election. More polls showing Conservative in front but its lead dwindling a bit in most polls.

Fixed Income

Bund futures trade at 162.18 up 1 ticks, near the mid-point of this week's trading range as investors appear reluctant to swing bunds either direction. Resistance remains near the 162.81 level followed by 163.54. A break of the 161.65 support level could see lows target 159.96 followed by 157.50

Gilt futures trade at 128.71 lower by 10 ticks, following better than expected UK Manufacturing PMI data. Last week's rally took out both the 129.00 handle and the 129.14 April 18th high, but yesterday's decline was unable to hold that key region. Price finds key support at the 128.68 support level. An acceleration lower could test the 127.43 region. Resistance remains the noted 129.00/129.14 region, then 129.75 followed by 130.28.

Thursday's liquidity report showed Wednesday's excess liquidity fell to €1.623T a rise of €10.3B from €1.6127T prior. Use of the marginal lending facility rose to €177M from €148M prior.

Corporate issuance saw over $6.9B come to market via 3 issues headlined by Goldman Sachs $5B in an 3-part senior unsecured note offerings and William Partners $1.45B of senior notes due 2027

Looking Ahead

(RO) Romania May International Reserves: No est v $39.8B prior

(RU) Russia May Sovereign Wealth Fund Balances: Reserve Fund: No est v $16.3B prior; Wellbeing Fund: No est v $73.6B prior

(ZA) South Africa May Naamsa Vehicle Sales Y/Y: -0.4%e v -13.4% prior

(IT) Italy May Budget Balance: No est v -€5.2B prior

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

05:30 (UK) DMO to sell £2.5B in 1 25% 2027 Gilts;

06:00 (IE) Ireland May Live Registry Monthly Change: No est v -4.6K prior; Live Registry Level: No est v 266.6K prior

06:30 (ZA) South Africa Q1 Unemployment Rate: 27.0%e v 26.5% prior

06:45 (US) Daily Libor Fixing - 07:00 (CA) Canada Apr MLI Leading Indicator M/M: No est v 0.5% prior

07:00 (ZA) South Africa Apr Electricity Production Y/Y: No est v 2.7% prior; Electricity Consumption Y/Y: No est v 2.7% prior

07:30 (US) May Challenger Job Cuts: No est v 36.6K prior; Y/Y: No est v -42.9% prior

08:00 (BR) Brazil Q1 GDP Q/Q: +1.0%e v -0.9% prior; Y/Y: -0.5%e v -2.5% prior; GDP 4-quarters accumulated: -2.3%e v -3.6% prior

08:00 (BR) Brazil May Manufacturing: No est v 50.1 prior

08:00 (PL) Poland Central Bank (NBP) May Minutes

08:00 (CZ) Czech May Budget Balance (CZK): No est v 6.3B prior

08:00 (EU) EU's Moscovici speaks at Brussels Economic Forum

08:00 (IT) Italy Fin Min Padoan on panel at Brussels Economic Forum in Brussels

08:15 (US) May ADP Employment Change: +180Ke v +177K prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 238Ke v 234K prior;Continuing Claims: 1.92Me v 1.923M prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (RU) Russia Gold and Forex Reserve w/e May 26th: No est v $405.0B prior

09:30 (CA) Canada May Manufacturing PMI: No est v 55.9 prior

09:45 (US) May Final Markit Manufacturing PMI: 52.5e v 52.5 prelim

10:00 (US) May ISM Manufacturing: 54.6e v 54.8 prior; Prices Paid: 67.0e v 68.5 prior

10:00 (US) Apr Construction Spending M/M: +0.5%e v -0.2% prior

10:00 (BR) Brazil Apr CNI Capacity Utilization: No est v 77.1% prior

10:00 (MX) Mexico Apr Total Remittances: $2.3Be v $2.5B prior

10:00 (MX) Mexico Central Bank (Banxico) May Minutes

10:00 (MX) Mexico Central Bank Economist Survey

10:30 (US) Weekly EIA Natural Gas Inventories

10:30 (MX) Mexico May PMI Manufacturing: No est v 50.7 prior

11:00 (US) Weekly DOE Crude Oil Inventories

11:00 (BR) Brazil to sell LTN 2018, 2019 and 2020 Bills

11:00 (BR) Brazil to sell 2023 LFT

12:00 (IT) Italy May New Car Registrations Y/Y: No est v -4.6% prior

13:00 (MX) Mexico May IMEF Manufacturing Index: 46.0e v 45.0 prior; Non-Manufacturing Index: 48.0e v 47.2 prior

14:00 (BR) Brazil May Trade Balance: $7.5Be v $7.0B prior; Total Exports: $20.5Be v $17.7B prior; Total Imports: $12.9Be v $10.7B prior

15:00 (US) President Trump decision on Paris Climate agreement

Sterling Volatility Soars Ahead Of Election

British pound volatility has recently increased, not only because the general election is approaching, but also because some opinion polls suggest a hung parliament. The latest YouGov/ Time voting intention survey shows that support for the Conservatives declined markedly to 42% while the Labours gained +3 points to 39%. The 3-point lead by the Conservatives is the narrowest since PM Theresa May has called for the snap election in April. The Liberal Democrats hovered around single-digit, the UKIP remained on 4% and votes for other parties are at 8% (from 7%). Converting percentages to numbers, PM May's Conservative Party, while remaining the biggest party, might lose as much as 20 seats, down from 330 to 310, in the upcoming general election. If the election outcome results in a hung parliament, it would be the second time since 1974, and the seventh time since the beginning of the 20th century.

A hung parliament occurs when no party has won enough seats in a general election to have a majority in the House of Commons. If it really happens, Theresa May, the incumbent prime minister, would stay in office until it is decided who will attempt to form a new government. As the Cabinet Manual suggested, an incumbent government "is expected to resign if it becomes clear that it is unlikely to be able to command that confidence and there is a clear alternative".

Back in 2010, the general election resulted in a hung parliament as no party was able to get 326 seats (out of 650) needed for an overall majority. Winning 306 seats, the Conservative Party eventually had to form a coalition government with the Liberal Democratic Party with David Cameron and Nick Clegg being the Prime Minister and the Deputy Minister, respectively.

What if a Hung Parliament Occurs Again?

If YouGov's polling result materializes, Conservatives would win 310 seats, compared with 330, while Labors would gained +28 seats to 229. LibDem would get 10 seats while the SNP would get 50 seats. In this case, A Coservative-LibDem coalition would still be 6 seats short of majority. Meanwhile, a Labor-SNP coalition, resulting in 307 seats, would also not be workable. Ironically, while the Conservative-SNP coalition would work out in terms of the number of seats, it would unlikely be an appropriate option due to the fundamental conflicts, such as Brexit and Scottish independence, between the two parties.

Poll of Polls Suggests Conservatives Would Gain Overall Majority

Yet, polls of polls compiled by several agencies continue to project that Conservatives would win with overall majority, though it would not be a landslide victory as depicted in mid-April. In our opinion, it would be a disappointment to the market if Conservatives' seats shrink from 2015 or a Conservatives' majority is less than 50 seats, compared with expectation of over 100 seats shortly after the snap election was announced. Recall that PM May's intention to call for the snap election is to cement her mandate in negotiating the Brexit terms with the EU. Obviously, the size of the Conservative majority would affect the flexibility that PM May has in the negotiations

Euro Ticks Lower As German, Eurozone Mfg. PMIs Meet Expectations

The euro has posted small losses in the Thursday session. Currently, EUR/USD is trading at 1.1220. On the release front, German and the Eurozone Manufacturing PMIs both indicated expansion. German Manufacturing PMI improved to 59.4, a shade under the estimate of 59.5. The Eurozone report rose to 57.0, matching the forecast. The US will release ISM Manufacturing PMI. Employment data is in the spotlight for the remainder of the week. Thursday's releases include ADP Nonfarm Payrolls and unemployment claims. On Friday, we'll get a look at the official Nonfarm Employment Change, which is expected to drop to 186 thousand. The US will also release wage growth and the unemployment rate.

The markets were all ears on Monday as ECB President Mario Draghi testified before the EU parliamentary committee for economic affairs. Draghi acknowledged that the euro-area economy was improving, but said that inflation and wage growth remained weak, requiring the ECB to continue its asset-purchase program. The scheme is due to wind up in December, and stronger data had raised speculation that the central bank might revisit its monetary stance and perhaps taper the program at the June policy meeting. Draghi's message remains one of caution, and appears to be putting the markets on notice that any moves in June will likely be of a minor nature.

Is the German locomotive slowing down? As the eurozone's largest economy, a strong and reliable German economy has been instrumental in the eurozone's impressive improvement in the first quarter of 2017. However, the latest consumer spending numbers disappointed the markets. In April, retail sales declined 0.2%, compared to a forecast of +0.4%. This marked the third decline in 2017, and if there is further contraction in the second quarter, the eurozone economy could be in trouble. Although the German labor market remains strong, this has not translated into higher inflation, which declined 0.2% in May, after a flat reading of 0.0% in April.

The US economy expanded at an annual rate of 1.2% in the first quarter, according to its second estimate for GDP. This was considerably higher than the 0.7% gain which was reported in the first estimate in April. Still, this figure is the lowest in a year, and well off the 2.1% gain in Q4. Business spending remains weak, and although consumer confidence remains at high levels, consumer spending has not kept up, as retail sales was softer than expected in April. Will this lead to the Fed rethinking a June rate hike? The markets don't appear concerned, as the odds of a 0.25% rate hike have increased to 84%. At the same time, the likelihood of a rate hike in the second half of 2017 are low. The odds for a September rate are just 26%, with the markets unclear on whether the Fed will make further moves this year if inflation remains below the Fed target. Political uncertainty remains a serious concern, as the Trump administration is embroiled in scandals, with several congressional investigations probing into Trump's alleged connections with Russian politicians. A weakened White House raises doubts if Trump will be able to keep his election promises to lower taxes and cut government spending.

Sterling Gripped By Political Jitters

Investors avoided Sterling during trading on Thursday amid fears of UK Prime Minister Theresa May losing her grip onparliament afterBritain’s June 8 election. Recent polls indicatea potential scenario where Theresa May could be short of the seats requiredto form a government, which has sparked concerns of political instability prior to the Brexit negotiations. With the growing threat of a nightmare “hung parliament” scenario likely to weigh heavily on Sterling, further downside should be expected in the short to medium term.

Focusing on the macroeconomics, UK Manufacturing PMI fell less than expected in May, slightly easing some concerns over the UK economy. Although the firm PMI figure of 56.7 suggests that the manufacturing sector is building some momentum in the second quarter, Sterling bears were unaffected. The fact that short term gains on the GBPUSD were swiftly relinquished after the PMI report continues to highlight how UK politics and Brexit continue to dictate where Sterling trades with economic data almost becoming secondary.

Withthe UK election only a week away, investors will be paying very close attention to the polls, which should inject Sterling with explosive levels of volatility. With Brexit already having some undesirable impacts on the UK economy, the last thing investors need is a messy Brexit deal that will surely addto the current woes.

Technical traders may pay attention to how the GBPUSD reacts to the tough 1.2775 support level. A breakdown below 1.2775 should encourage a further depreciation lower towards 1.2600.

ADP NFP report in focus

The Greenback struggled to regain its charisma this week with prices sinking towards 97.00 on Wednesday following the mixed batch of economic data from the US which weighed on sentiment. Although there are high expectations over the Federal Reserve raising US interest rates in June, the longer-term hiking path remains clouded and as such, continues to pressure the Dollar.

Dollar weakness is likely to persist moving forward, especially when considering how bears are exploiting the uncertainty over Trump and ongoing political instability in Washington to attack prices ruthlessly. Investors may direct their attention towards the pending ADP NFP Report this afternoon which could provide some minor support for the Dollar if the data released exceeds estimates. From a technical standpoint, the Dollar Index remains heavily bearish on the daily charts. Repeated weakness below 97.00 should encourage a further decline towards 96.00.

Oil bears remain dominant

WTI Crude edged towards $49 on Thursday following reports of US Crude stockpiles extending declines, slightly easing oversupply concerns. Regardless of the recent gains, the lingering disappointment from last week’s OPEC meeting continues to haunt investor attraction towards oil with the upside limited. Sentiment remains firmly bearish towards oil and sellers are likely to exploit the fact that OPEC’s oil output in May rose despite constant talks of balancing the markets. Although OPEC and Non-OPEC members remain committed to bringing global oil inventories down to a five-year average, it remains a question of how US Shale reacts and benefits from OPEC’s actions. I remain bearish on WTI Crude moving forward and a breakdown below $48 should open a path towards $46.

Commodity spotlight – Gold

In times of uncertainty and periods of anxiety, Gold becomes a trader's popular choice which was seen on Wednesday when the metal lurched towards $1275. Although US rate hike expectations in June have slightly hindered the upside on Gold, short-term bulls are looking beyond this to propel prices higher. Although a positive ADP NFP Report this afternoon could expose the yellow metal to some downside pressure, bulls remain in control above $1260. From a technical standpoint, Gold needs to break above $1275 for the upside to continue.

Technical Outlook: AUDUSD Is Firmly In Red, Probes Below Strong Fibo Support At 0.7400

The Aussie dollar is in red for the second day and fell sharply on Thursday, pressured by weak data from China. Chinese Caixin Manufacturing PMI unexpectedly fell in to 49.6 in May, missing the forecast at 50.1 and previous month's 50.3 release.

Extension of bear-leg from 0.7475 (31 May high) cracked strong support at 0.7400 (Fibo 61.8% of 0.7328/0.7517 rally) with close below to signal further weakness.

Thursday's fresh bearish acceleration also completed Failure Swing pattern on daily chart which is seen as strong bearish signal.

Below 0.7400, next target lies at 0.7373 (Fibo 76.4% retracement), with extension towards key support at 0.7328 (09 May low/weekly cloud top) not ruled out.

Corrective upticks should be ideally capped by broken 20SMA at 0.7425, with next strong barrier at 0.7450 (daily Tenkan-sen).

Res: 0.7425, 0.7450, 0.7475, 0.7500

Sup: 0.7373, 0.7350, 0.7328, 0.7300