Sample Category Title

ADP Payrolls Set The Stage For A Stronger NFP Print

The U.S. dollar was bullish yesterday lifted by a stronger than expected private payrolls data. According to ADP/Moody's the private sector, hiring was robust with 253k jobs being added in May, beating estimates of 180k. The ISM's manufacturing PMI was largelystable, but data showed that wage pressures were building up.

This potentially builds up the possibility of a stronger payrolls data today. The market expectations for a rate hike by the Fed in June is all but confirmed and today's job numbers are most likely going to the prove the same.

The US Dollar Index snapped a two-day losing streak rising 0.3% on the day to close at 97.135. Technical resistance is seen at 97.50 which needs to be cleared to pave the way for further gains to the upside.

Besides the payrolls data, the UK's construction PMI is also due for release with data likely to show a weak print. This follows yesterday's manufacturing PMI which fell from 57.3 in April to 56.7 in May.

EURUSD intraday analysis

EURUSD (1.1216): The EURUSD closed bearish yesterday after testing the previous highs from last week at 1.1254. With prices, still above 1.1200, there is scope for the EURUSD to possibly push higher.

Any near-term gains are likely to see a test back to 1.1236 where resistance could be formed. But failure to breakout above 1.1236 will signal near-term declines towards 1.1100 at the very least. It is quite likely that EURUSD will remain broadly flat into next week's ECB monetary policy meeting.

GBPUSD intraday analysis

GBPUSD (1.2873):The British pound closed with a doji yesterday after price managed to continue rising following the bounce of 1.2800. We are watching the potential head and shoulders pattern that is likely to form.

A reversal is expected near 1.2937 or even at the current levels which will suggest the possible break down of 1.2800 support. This will give way for theprice to test 1.2600. However, most of the declines are likely to come by only next week, unless the markets react strongly to today's payrolls report.

XAUUSD intraday analysis

XAUUSD (1261.54): Gold prices continued to slip with price action yesterday currently trading below 1263.00 level of support and resistance. If price pulls back above 1263.00, expect another rally in gold that could see 1274.00 being tested firmly. In the near term, gold prices are likely to remain range bound within 1263 and 1274 with a breakout from this range likely to confirm the near-term continuation in prices. Below 1263, the next main support is at 1250, and above 1274, gold prices could be potentially eyeing the 1300 level.

Trade Idea: EUR/JPY – Buy at 124.20

EUR/JPY - 125.14

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

Original strategy:

Buy at 123.85, Target: 125.75, Stop: 123.25

Position: -

Target: -

Stop: -

New strategy :

Buy at 124.20, Target: 126.20, Stop: 123.60

Position: -

Target: -

Stop:-

As the single currency has maintained a firm undertone after staging a strong rebound from 123.16, consolidation with upside bias remains for gain towards strong resistance at 125.82, however, break there is needed to confirm recent upmove has resumed and extend headway to 126.20-30 and possibly 126.60-70 but reckon 127.00-10 would hold from here.

In view of this, we are looking to buy euro on pullback as 124.10-20 should limit downside and bring another rise later. Below 123.65-70 would defer and suggest the rebound from 123.16 has ended, bring another test of said support at 123.16 but only break there would abort and shift risk back to downside for test of previous support at 122.56 which is likely to hold from here due to broad consolidative outlook.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Stand aside

AUD/USD – 0.7382

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Exit long entered at 0.7405

Position: - Long at 0.7405

Target: -

Stop: -

New strategy :

Stand aside

Position: -

Target: -

Stop:-

As aussie has remained under pressure after meeting renewed selling interest at 0.7476, suggesting downside risk remains for the fall from 0.7518 to extend weakness to 0.7350, break there would add credence to our view that the rebound from 0.7329 has ended at 0.7518 last month, bring further fall towards this level. Only a drop below there would confirm recent decline has resumed and extend weakness to 0.7295-00 (76.4% retracement of 0.7158-0.7750).

In view of this, would be prudent to stand aside for now. above 0.7420-25 would bring another bounce to 0.7476 resistance but break there is needed to revive bullishness and signal the retreat from m0.7518 has ended, bring another rise towards this level first.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 16 Jan 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 18 Apr 2017

• Trend bias: Near term up

GBP/USD – 1.3003

Cable’s retreat late last week on profit-taking suggests a week of consolidation below recent high at 1.3048 would be seen and although price has rebounded from 1.2769, reckon upside would be limited to 1.2955-60 and 1.3000 should hold, bring another retreat later, below 1.2830 support would bring test of 1.2769 but break there is needed to signal a temporary top has been formed, bring retracement of recent upmove to 1.2700-10 and possibly towards the upper Kumo (now at 1.2669), having said that, reckon downside would be limited and previous resistance at 1.2616 would turn into support and contain dollar’s downside, bring rebound later.

On the upside, whilst initial recovery to 1.2955-65 cannot be ruled out, reckon resistance at 1.3015 would hold from here, bring another retreat later. Only a daily close above said resistance at 1.3015 would signal retreat from 1.3048 has ended, bring retest of this level later. Once this recent high at 1.3048 is penetrated, this would signal the upmove from 1.1986 low (Jan low) has resumed for retracement of early downtrend, hence further gain to 1.3050-60, then 1.3100 would be seen, however, loss of near term upward momentum should prevent sharp move beyond 1.3140-50 (38.2% Fibonacci retracement of 1.5018-1.1986) and reckon 1.3200 would hold.

Recommendation: Stand aside for this week.

On the weekly chart, as cable has retreated last week after meeting resistance at 1.3048, suggesting minor consolidation below this level would be seen and pullback to the Tenkan-Sen (now at 1.2707) cannot be ruled out, however, reckon 1.2665-70 would limit downside and bring another rise later, above 1.3015 would bring retest of 1.3048 but break there is needed to confirm recent upmove from 1.1986 low (2017 low) has resumed, bring retracement of early decline to 1.3090-00, then towards 1.3140-50 (38.2% Fibonacci retracement of 1.5018-1.1986) but price should falter well below 1.3200-10, risk from there is seen for a retreat to take place later.

On the downside, below 1.2830 would bring test of 1.2769 support, break there would bring correction to the Tenkan-Sen (now at 1.2707), however, downside should be limited to 1.2665-70 and bring another rise. Only below previous resistance at 1.2616 would abort and signal top is formed instead, bring weakness to 1.2550-60, however, still reckon downside would be limited and previous support at 1.2515 should remain intact.

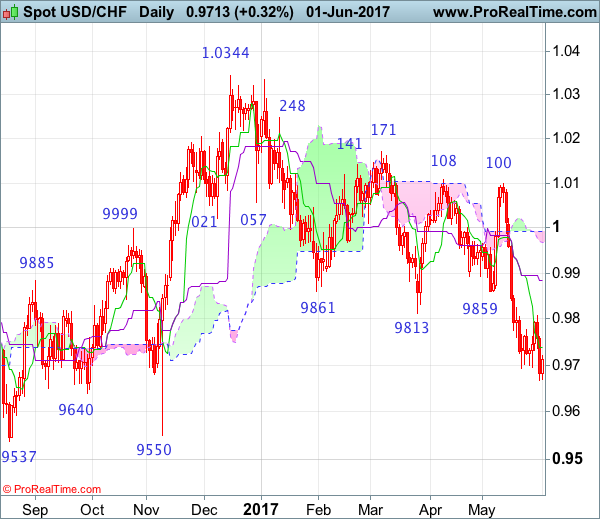

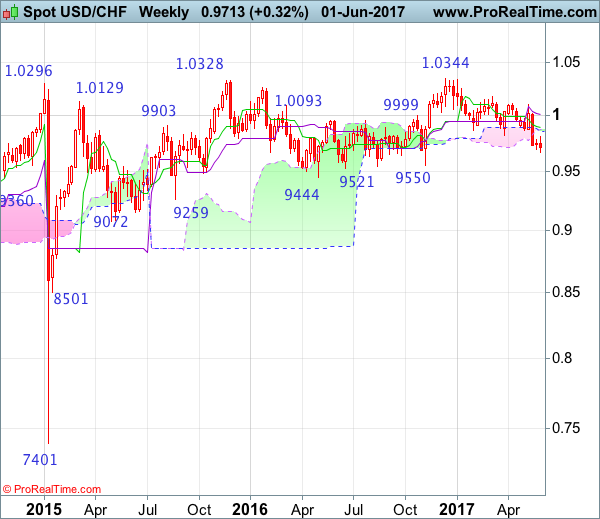

USD/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 7 Mar 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 9 May 2017

• Trend bias: Near term up

USD/CHF – 0.9708

The greenback only recovered to 0.9808 before dropping again, adding credence to our bearish view that early decline from 1.0344 top (2016 high) is still in progress and downside bias remains for further fall to 0.9650, then towards 0.9600, however, near term oversold condition should prevent sharp fall below 0.9550 support and price should stay above psychological level at 0.9500 support, bring rebound later.

On the upside, whilst initial recovery to the Tenkan-Sen (now at 0.9738), then towards said resistance at 0.9808 cannot be ruled out, reckon previous support at 0.9859 (now resistance) would limit upside and bring another decline later. Only a daily close above the Kijun-Sen (now at 0.9884) would defer and suggest a temporary low is formed, bring a stronger rebound to the lower Kumo (now at 0.9969) but price should falter below 1.0000 and bring another selloff.

Recommendation: Sell at 0.9855 for 0.9685 with stop above 0.9955

On the weekly chart, as the greenback has remained under pressure after forming a long black candlestick last month, adding credence to our bearish view that early erratic fall from 1.0344 top is still in progress, hence bearishness remains for this move to bring retracement of early upmove to 0.9600, then towards previous support at 0.9550, however, reckon downside would be limited to 0.9500 and another previous support at 0.9444 should remain intact, risk from there has increased for a strong rebound later.

On the upside, although initial recovery to 0.9808 resistance can not be ruled out, reckon 0.9850-60 would limit upside and bring another decline later. A weekly close above the Tenkan-Sen (now at 0.9888) would defer and risk a stronger rebound to 0.9940-50 but 1.0006-07 (current level of the Kijun-Sen and previous resistance) should limit upside and price should falter well below 1.0100, bring another decline later. Above 1.0100 would signal low is formed instead and suggest the aforesaid decline from 1.0344 has ended, bring test of 1.0171 resistance next.

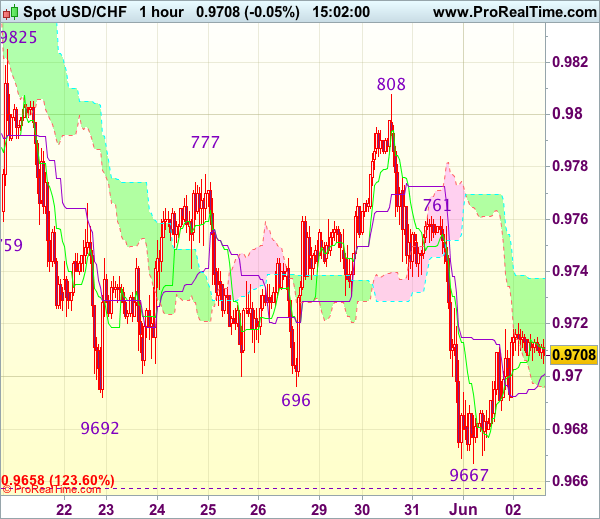

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9705

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9710

Kijun-Sen level : 0.9701

Ichimoku cloud top : 0.9738

Ichimoku cloud bottom : 0.9697

Original strategy :

Sell at 0.9740, Target: 0.9640, Stop: 0.9775

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback recovered after falling to 0.9667 yesterday, suggesting consolidation above this level would be seen and test of the upper Kumo (now at 0.9738) cannot be ruled out, however, break of resistance at 0.9761 is needed to signal low has indeed been formed at 0.9667, bring further gain to 0.9780 but resistance at 0.9808 should hold ahead of US opening.

On the downside, below said support at 0.9667 would signal recent decline has resumed and may extend further weakness to 0.9655-60, then 0.9630, however, oversold condition should prevent sharp fall below 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808), bring rebound later. As near term outlook is mixed, would be prudent to stand aside for now.

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.2860

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2877

Kijun-Sen level : 1.2873

Ichimoku cloud top : 1.2860

Ichimoku cloud bottom : 1.2845

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite rebounding to 1.2916 yesterday, as cable has retreated again after falling below indicated resistance at 1.2921, retaining our view that further consolidation would be seen and weakness to 1.2830 support cannot be ruled out, however, only break there would signal the rebound from 1.2769 has ended, bring further fall to 1.2800 but said support at 1.2769 should remain intact.

On the upside, above 1.2900 would bring another test of 1.2921-26 (resistance and previous support), however, break there is needed to signal low has been formed at 1.2769, bring further gain to 1.2940-45 (61.8% Fibonacci retracement of 1.3048-1.2769) and later towards 1.2970 but overbought condition should cap upside below 1.3000. As near term outlook is mixed, would be prudent to stand aside for now.

Currencies: Will Payrolls Trigger A USD Rebound?

Sunrise Market Commentary

- Rates: Decent payrolls sufficient to inflict losses on Treasuries?

Focus turns to US payrolls today. We expect net job growth, unemployment rate and average hourly earnings to be near consensus. Given market positioning, such outcome should be sufficient to trigger a reaction (lower US Treasuries) with the Fed on the brink of another rate hike (June 14) and preparing to taper its balance sheet (Q4 2017?). - Currencies: Will payrolls trigger a USD rebound?

The dollar performed mixed recently, but good data supported a bottoming out process yesterday. Today's payrolls might decide on the next USD move. Given the recent correction, we see room for a rebound if the payrolls don't surprise on the downside. Sterling also shows signs of bottoming out even as political uncertainty persists

The Sunrise Headlines

- US equities closed around 0.75% higher with new all-time highs for the S&P 500 and Nasdaq. Overnight, Asian stocks gain ground as well with Japan outperforming (>+1.5%) and China underperforming (-0.5%).

- President Trump said he will withdraw the US from the Paris climate accord in an effort to boost the nation's industry and independence, making a dramatic shift in policy despite intense lobbying from business leaders and close allies.

- The BoJ hit a new milestone as its balance sheet topped 500 trillion yen ($4.48 trillion), roughly the same size as that of the Federal Reserve, having more than tripled since it started aggressive stimulus in 2013.

- The pace of US car and light truck sales slowed in May for the third month in a row despite steep discounts, but investors bid up shares of General Motors and Ford after executives outlined plans to cut inventories.

- US crude supplies shrank for an eight week, falling by 6.43 million barrels as record refinery runs and exports pushed stockpiles lower, EIA data showed. Still, the drop was smaller than reported by the API and inventories are above the five-year seasonal high. Brent crude hovers just above $50/barrel.

- South Africa's government has avoided a second damaging credit rating cut from Fitch, but the ratings agency warned that the recent political upheaval is likely to further weaken the economy.

- Today's eco calendar contains US May payrolls, unemployment rate and average hourly earnings. Fed governors Harker and Kaplan are scheduled to speak.

Currencies: Will Payrolls Trigger A USD Rebound?

Payrolls to decide on USD comeback

Yesterday, the dollar started the session close to the recent lows against the euro and the yen. The EMU data were OK, but not strong enough to push EUR/USD to a new short-term correction top. Later in the session, the dollar even profited from a very strong ADP labour report and from an improving risk sentiment. President Trump announcing that the US is leaving the Paris climate agreement had no negative impact on the dollar or on global risk sentiment. EUR/USD closed the session at 1.1213 (from 1.1244). USD/JPY finished the day at 111.37 (from 110.78). The dollar bottomed out, but the gains remained modest.

Overnight, yesterday's US equity rally continued in Asia with Japanese indices taking the lead. There are plenty of headlines that the BOJ balance sheet hit the JPY 500 trillion milestone and that it is roughly nearing the same size as the Fed's. For now, this hardly weakens the yen. USD/JPY touched an intraday top in the 111.68 area but the decline of the yen remains very limited compared to equity performance. The CNH is correcting lower after recent steep gains as funding conditions are easing. EUR/USD (1.1220 area) is little changed from yesterday's close.

Today, there are no eco data with market moving potential in EMU. US central banks speakers (Harker, Kaplan) already gave their view recently. So the focus will be on the US payrolls report. The market expects a decent report with 182 000 net job growth in May. Yesterday's ADP report suggests that this is feasible, even as the labour market component in some confidence surveys eased of late. The unemployment rate is expected to be unchanged at 4.4%. Wage growth will be at least as important for markets/the dollar as payrolls growth. The consensus expects average hourly wage growth of 0.2% M/M and 2.6% Y/Y. This looks feasible.

What to expect for the dollar? Until yesterday, the USD performance was far from convincing. An outright miss/disappointment of the payrolls might put the dollar again under pressure with EUR/USD jumping beyond the 1.1268 area and USD/JPY drifting back lower in the 110 area. However, this is not our favoured scenario. After recent USD softness and given the low levels of US yields, an in line/slightly better than expected report might help a further USD bottoming-out process. An ongoing positive equity reaction might also be a slight additional USD positive. So, we look forward to seeing whether the payrolls are strong enough for a floor for the dollar

Technical picture

The USD/JPY rally ran into resistance in early May. A mini sell-off pushed the pair below the previous top (112.20), making the short-term picture negative. The pair regaining to 112.13 level would call off the short-term downside alert in this cross rate. As long as such a sustained rebreak hasn't occurred, the USD/JPY picture remains fragile and a return action lower in the 108.13/114.37 range remains possible.

Earlier May, EUR/USD failed to break below the 1.0821/1.0778 support (gap). Poor US data and political upheaval propelled EUR/USD north of the 1.1023 range top. The pair reached a short-term correction top at 1.1268. The correction top at 1.1300/1.1366 is next resistance. USD sentiment will have to be extremely negative to clear this hurdle short-term. So, a clean break of this won't be that easy. A return below 1.1023 would indicate that the upside momentum has eased. Will the payrolls be strong enough to do the job?

EUR/USD declines slightly of recent top. Will payrolls trigger a more pronounced correction

EUR/GBP

Sterling decline halts

UK elections remained the key driver for sterling trading yesterday. The UK manufacturing PMI declined less than expected from 57.00 to 56.7, indicating ongoing good growth in the sector. However the impact on sterling trading was negligible. In technical trade, EUR/GBP touched a minor short-term top in the 0.8755 area, but no sustained break occurred. Most election polls still indicated a lead for PM May's conservative party, but the lead is declining. After the recent substantial sterling losses, some consolidation seems to kick in. EUR/GBP closed the session at 0.8704 (from 0.8723). Cable finished the day little changed at 1.2882.

The UK construction PMI is expected to ease slightly from 53.1 to 52.6 today. We would be highly surprised to see the indicator having a lasting impact on sterling trading. The focus stays on the parliamentary elections as the campaign enters the final weekend. Political uncertainty remains high, but sterling yesterday entered some calmer waters. Markets apparently have adapted positions to this uncertainty (reducing sterling longs). At the same time, the basic market assumption remains that PM May will maintain a decent majority. Unless polls show a further erosion of the conservative lead, some sterling consolidation might kick in as quite some negative news should already be discounted after the recent sell-off. Next resistance comes in at EUR/GBP 0.8788. EUR/GBP 0.8655 is a first minor support. A sustained return below the EUR/GBP 0.86 alert would suggest that the worst is over for sterling.

EUR/GBP: most of the bad news discounted?

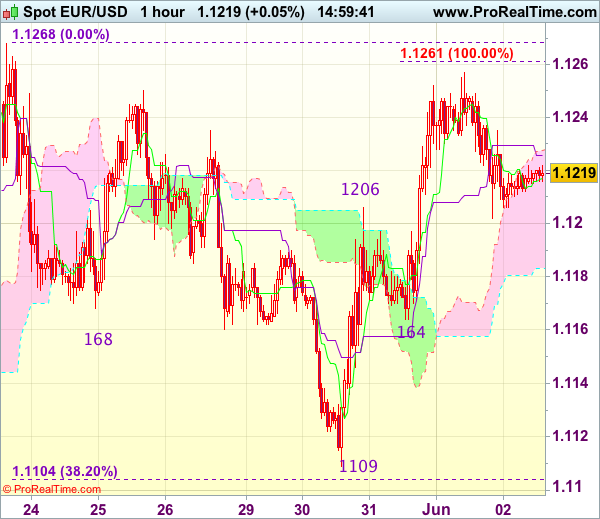

Trade Idea : EUR/USD – Hold long entered at 1.1205

EUR/USD - 1.1219

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1217

Kijun-Sen level : 1.1226

Ichimoku cloud top : 1.1228

Ichimoku cloud bottom : 1.1183

Original strategy :

Bought at 1.1205, Target: 1.1305, Stop: 1.1170

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1170

New strategy :

Hold long entered at 1.1205, Target: 1.1305, Stop: 1.1170

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1170

Although euro’s retreat after marginal rise to 1.1257 yesterday suggests consolidation below this level would be seen, reckon downside would be limited to 1.1195-00 and bring another rise later, above said resistance at 1.1257 would extend gain to previous resistance at 1.1268, break there would confirm early upmove has resumed and test of another previous chart resistance at 1.1300 would follow, above there would encourage for headway to 1.1340-45, however, overbought condition should limit upside to chart point at 1.1366.

In view of this, we are holding on to our long position entered at 1.1205. Only below support at 1.1164 would abort and suggest a temporary top is formed instead, risk weakness to 1.1140 but said support at 1.1109 should remain intact, bring rebound later.

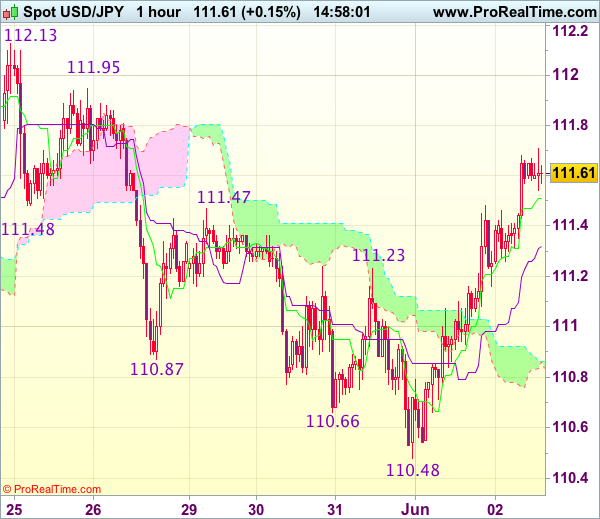

Trade Idea : USD/JPY – Buy at 111.20

USD/JPY - 111.62

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 111.53

Kijun-Sen level : 111.32

Ichimoku cloud top : 110.86

Ichimoku cloud bottom : 110.84

Original strategy :

Buy at 110.85, Target: 111.85, Stop: 110.50

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.20, Target: 112.20, Stop: 110.85

Position : -

Target : -

Stop : -

As the greenback has surged again after breaking indicated resistance at 111.23-24 yesterday, adding credence to our view that low has indeed been formed at 110.48 and mild upside bias remains for this move to extend gain to resistance at 112.13, however, break there is needed to bring a stronger retracement of early decline from 114.37 top to 112.45-50 (61.8% Fibonacci retracement of 113.85-110.24) first.

In view of this, we are looking to buy dollar on pullback as previous resistance at 111.23 should turn into support and contain dollar’s downside, bring another rebound later. Below 110.95-00 would defer and risk weakness to 110.65-70 but said support at 110.48 should remain intact.