Sample Category Title

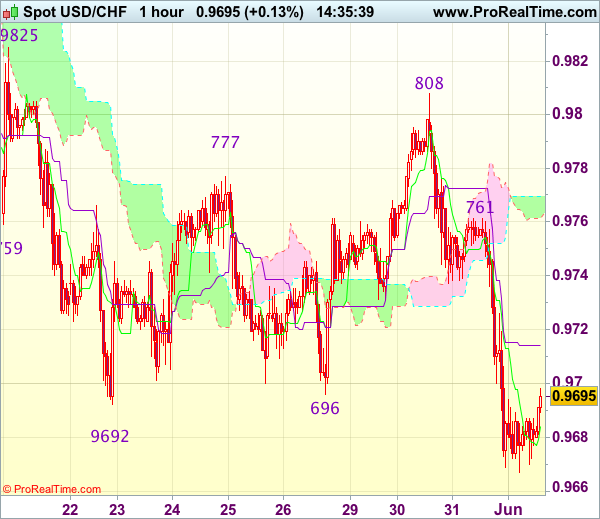

Trade Idea : USD/CHF – Target met and sell at 0.9720

USD/CHF - 0.9684

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9684

Kijun-Sen level : 0.9714

Ichimoku cloud top : 0.9770

Ichimoku cloud bottom : 0.9761

Original strategy :

Bought at 0.9700, met target at 0.9800

Position : - Long at 0.9700

Target : - 0.9800

Stop : -

New strategy :

Sell at 0.9720, Target: 0.9620, Stop: 0.9755

Position : -

Target : -

Stop : -

Although the greenback did stage the anticipated rebound to 0.9808 (our long position entered at 0.9700 met target at 0.9800), dollar ran into heavy selling pressure at 0.9808 earlier this week and has dropped sharply since, the subsequent breach of previous support at 0.9692 confirms recent decline has resumed and may extend further weakness to 0.9655-60, then 0.9630, however, near term oversold condition should prevent sharp fall below 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808), bring rebound later.

As we already took profit on our long position entered at 0.9700, we are looking to turn short on recovery as 0.9725-30 should limit upside and bring another decline. Only break of resistance at 0.9761 would abort and suggest a temporary low is possibly formed, risk test of said resistance at 0.9808 but only break there would provide confirmation.

Trade Idea : GBP/USD – Hold short entered at 1.2910

GBP/USD - 1.2854

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2865

Kijun-Sen level : 1.2845

Ichimoku cloud top : 1.2839

Ichimoku cloud bottom : 1.2833

Original strategy :

Sold at 1.2910, Target: 1.2810, Stop: 1.2945

Position : - Short at 1.2910

Target : - 1.2810

Stop : - 1.2945

New strategy :

Hold short entered at 1.2910, Target: 1.2810, Stop: 1.2900

Position : - Short at 1.2910

Target : - 1.2810

Stop : - 1.2900

Although sterling rebounded after falling marginally to 1.2769 yesterday, as price has retreated after meeting resistance at 1.2921, retaining our bearishness and as long as this level holds, consolidation with mild downside bias is seen for weakness to 1.2800-10, however, said support at 1.2769 should hold from here and bring another rebound later today or tomorrow.

In view of this, we are holding on to our short position entered at 1.2910. Above 12921-26 (said resistance and previous support) would defer and suggest low is formed instead, bring a stronger rebound to 1.2950 but upside should be limited to 1.2990-00.

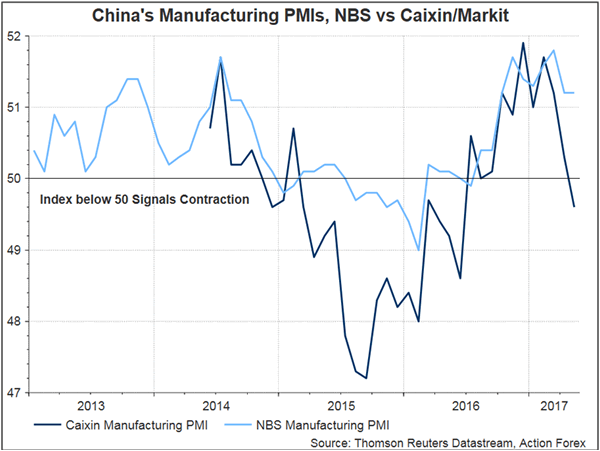

China’s Manufacturing Sector Contracted For First Time In Almost A Year

China's manufacturing activities contracted for the first time in 11 months, as Caixin/Markit's PMI index suggested. The report shows that the manufacturing PMI dropped -0.7 points to 49.6 in May (a reading below 50 signals contraction), compared with consensus of a milder drop to 50.1. While the sub-indices of output and new business remained in the expansionary territory, but both fell to their lowest levels since June last year. Meanwhile, the sub- indices of input costs and output prices drifted to the contractionary territory for the first time since June 2016 and February 2016, respectively. Meanwhile, the sub-index of stocks of purchases showed renewed decline. The rebound in the sub-index of stocks of finished goods suggested that companies stopped restocking as inventory levels increased.

Caixin Manufacturing PMI in Conflict with Official Data

Focusing on small- and medium-sized firms, the Caixin/Markit PMI report indicates quite rapid slowdown in activities in these companies. By contrast, the official PMI data by the National Bureau of Statistics saw a rebound in activities in small- and medium-sized firms. The official manufacturing index for small-sized firms rose for the third consecutive month to 51 in May while that for medium-sized firms rebounded to 51.3 in May, after moderating over the past 3 months.

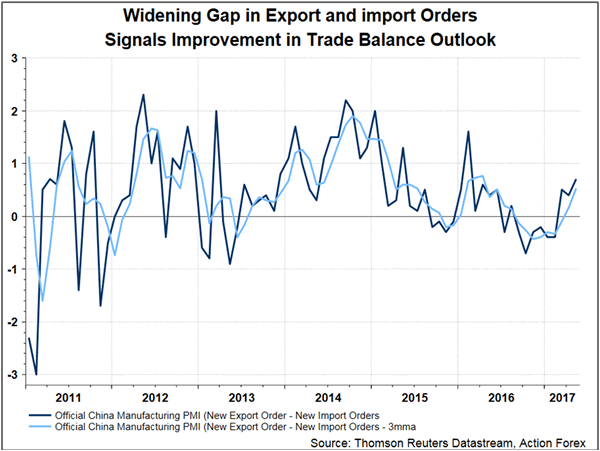

The official manufacturing PMI stayed unchanged at 51.2 for May, compared with consensus of 51. Besides the above-mentioned indices for small- and medium-sized firms, the official report also covers large corporations of which the index declined further to 51.2, from 52 in April. Despite the general belief that smaller companies should perform worse than larger companies due to the government tightening measures, the formers indeed benefited from the improved external demand, evidenced in the pickup in the export orders sub-index. The report also unveiled the widening gap between exports and imports, signaling stabilization in China's trade balance.

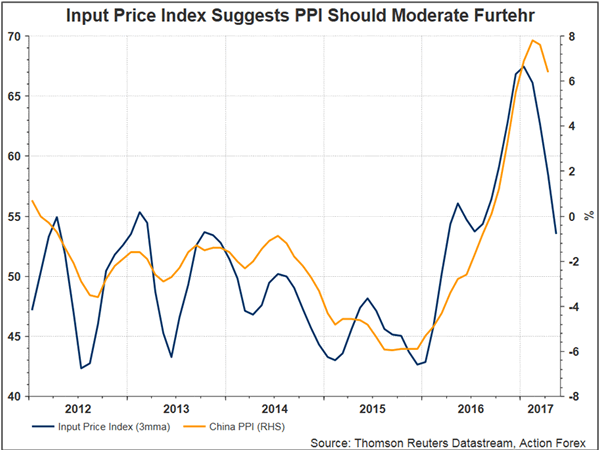

The input price index fell to 49.5 in May, marking the first sub-50 reading in 16 months, due to the decline in global commodity prices. We expect China's PPI would continue to moderate, probably falling to around 5%, in coming months.

The Non-manufacturing Sector

The official non-manufacturing PMI improved to 54.5 in May from 54 a month ago. the biggest growth driver for the month was the services PMI which gained +0.9 point to 53.5. The construction PMI slipped -1.2 points to 60.4 in May

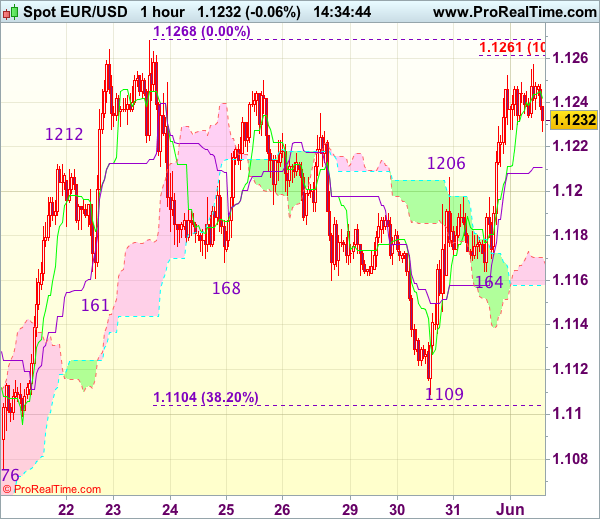

Trade Idea : EUR/USD – Buy at 1.1205

EUR/USD - 1.1236

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1242

Kijun-Sen level : 1.1211

Ichimoku cloud top : 1.1170

Ichimoku cloud bottom : 1.1158

Original strategy :

Buy at 1.1210, Target: 1.1310, Stop: 1.1175

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1205, Target: 1.1305, Stop: 1.1170

Position : -

Target : -

Stop : -

Although the single currency fell initially earlier this week, as euro found decent demand at 1.1109 and has rallied since, a retest of previous resistance at 1.1268 would be seen, break there would confirm early upmove has resumed and extend gain to another previous chart resistance at 1.1300, then towards 1.1340-45, however, near term overbought condition should limit upside to chart point at 1.1366, risk from there has increased for a retreat later.

In view of this, we are looking to buy euro on pullback as previous resistance at 1.1206 (now support) should limit downside and bring another rise later. Only below support at 1.1164 (yesterday’s low) would abort and suggest a temporary top is formed instead, risk weakness to 1.1140 but said support at 1.1109 should remain intact, bring rebound later.

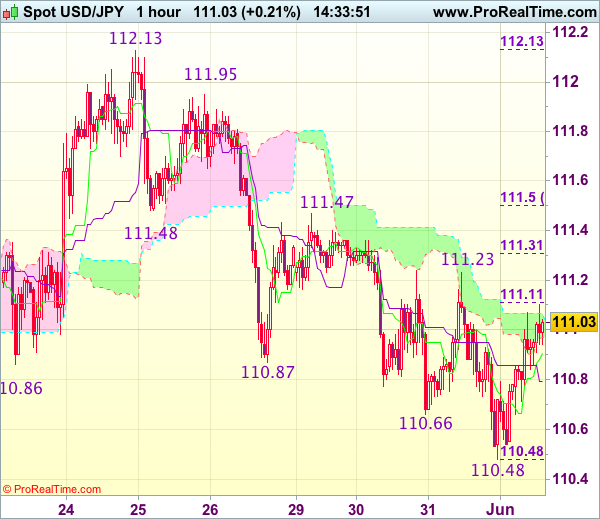

Trade Idea : USD/JPY – Stand aside

USD/JPY - 111.02

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.91

Kijun-Sen level : 110.79

Ichimoku cloud top : 111.07

Ichimoku cloud bottom : 110.97

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling to 110.48 yesterday, the subsequent rebound suggests consolidation above this level would be seen and test of resistance at 111.23-24 cannot be ruled out, however, break there is needed to signal low is formed, bring a stronger rebound to 111.47-50 (another previous resistance and 61.8% Fibonacci retracement of 112.13-110.48) but reckon upside would be limited and price should falter below resistance at 111.95.

On the downside, below 110.65-70 would bring retest of yesterday’s low at 110.48, break there would extend recent decline to another previous support at 110.24, break there would bring subsequent selloff to 110.00 which is likely to hold on first testing. As near term outlook is mixed, would be prudent to stand aside in the meantime.

EUR/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 03 May 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 3 May 2016

• Trend bias: Sideways

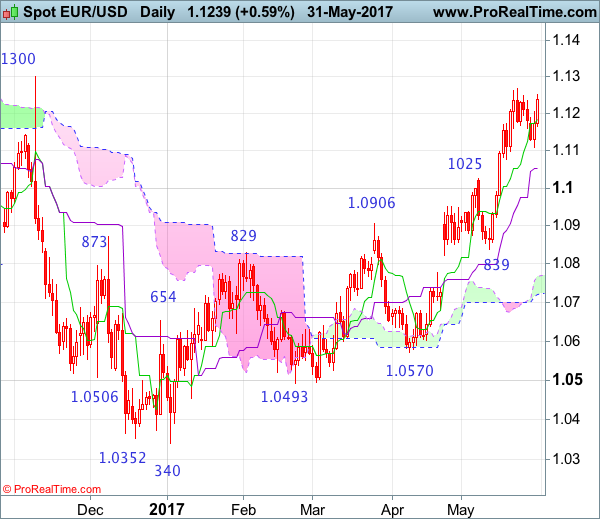

EUR/USD – 1.0946

Although the single currency retreated after rising to 1.1268, as euro did find renewed buying interest at 1.1109 earlier this week and has rebounded (we recommended in our previous update to buy at 1.1120 and a long position was entered), retaining our bullishness for recent upmove to resume after consolidation, above said resistance at 1.1268 would confirm the rise from 1.0340 low has resumed and extend further gain to previous resistance at 1.1300, then 1.1327, however, near term overbought condition should limit upside to previous chart resistance at 1.1366 but reckon 1.1440-50 would hold from here, risk from there is seen for a retreat later.

On the downside, whilst initial pullback to the Tenkan-Sen (now at 1.1184) cannot be ruled out, reckon downside would be limited sand said support at 1.1109 should remain intact, bring another rise later to aforesaid upside targets. A drop below said support at 1.1109 would defer and risk test of the Kijun-Sen (now at 1.1054) but only a daily close below there would defer and suggest a temporary top is possibly formed instead risk correction to 1.1025 (previous resistance now support), break there would add credence to this view, then correction to 1.0950-60 would follow, having said that, support at 1.0839 should remain intact.

Recommendation: Hold long entered at 1.1120 for 1.1320 with stop below 1.1105.

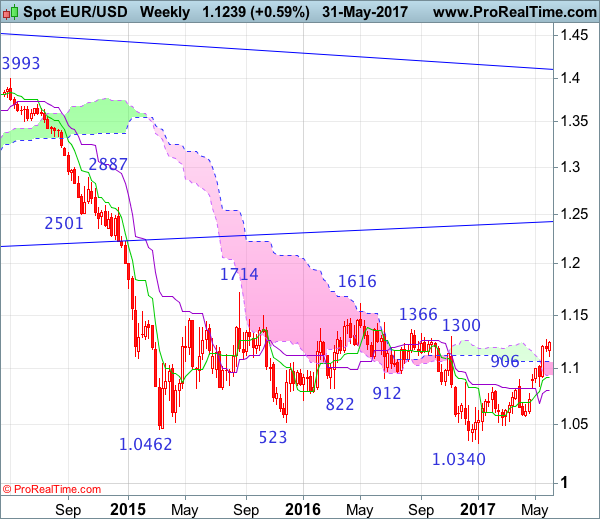

On the weekly chart, although euro slipped initially to 1.1109, renewed buying interest emerged there and the pair has rebounded since, retaining our bullishness for the erratic rise from 1.0340 low to bring a test of previous resistance at 1.1300, however, a break of another previous resistance at 1.1366 is needed to signal early downtrend has ended at 1.0340, bring further subsequent rise to 1.1428 but reckon 1.1500 would hold and price should falter well below another previous chart resistance at 1.1616.

On the downside, expect pullback to be limited to 1.1200-05 and bring another rise later to aforesaid upside targets. Below said support at 1.1109 would defer and risk weakness to the upper Kumo (now at 1.1067), then test of 1.1025 (previous resistance now support) but break there is needed to signal top is formed instead, bring further fall to 1.0965-70 but 1.0919-22 (current level of the Tenkan-Sen and previous support) should remain intact, price should stay well above another previous support at 1.0839, bring another rise later.

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Marubozu

• Time of formation: 14 Nov 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 15 Feb 2017

• Trend bias: Down

USD/JPY – 110.66

As dollar’s retreat from 112.13 has kept price under pressure, suggesting downside risk remains for a retest of previous support at 110.24, however, a break below there is needed to retain bearishness and confirm early decline from 114.37 has resumed and extend weakness to 110.00, then towards 109.59 support, having said that, loss of downward momentum should prevent sharp fall below minor support at 108.88 and price should stay well above recent low at 108.13, bring another rebound later.

On the upside, whilst recovery back to 111.00 and then 111.20-25 cannot be ruled out, reckon 111.45-50 would cap upside and bring another decline later to aforesaid downside targets. Above 111.95 would abort and bring another test of 112.13 resistance, break there would bring a stronger rebound to 112.45-50 (61.8% Fibonacci retracement of 113.85-110.24) and possibly towards 113.10-15 but upside should be limited to 113.85 and price should falter well below indicated resistance at 114.37.

Recommendation : Stand aside for this week

On the weekly chart, after trading narrowly last week (a doji was formed), this week’s retreat suggests downside risk remains for the fall from 114.37 to extend weakness to 110.24, below there would bring further decline to 109.59 support, however, a weekly close below there is needed to add credence to our view that the rebound from 108.13 has ended, bring subsequent weakness to 108.85-90 but said support at 108.13 should remain intact. In the event dollar drops below said support at 108.13, this would signal the fall from 118.66 top has resumed and extend weakness towards previous resistance at 107.49.

On the upside, expect recovery to be limited to 111.20 and 111.45-50 should hold, bring another decliner. Above previous resistance at 112.13 would defer and risk a stronger rebound to 112.45-50, then 112.70-75, break there would suggest the retreat from 114.37 has ended instead, bring test of 113.10-15, then towards the Kijun-Sen (now at 113.40) but break of 113.85 is needed to signal another leg of rebound from 110.24 is underway for a retest of 114.37 later. Looking ahead, only break of said resistance at 114.37 would extend the rise from 108.13 to 114.60-65 (61.8% Fibonacci retracement of 118.66-108.13), then towards resistance at 115.51 which is likely to hold from here.

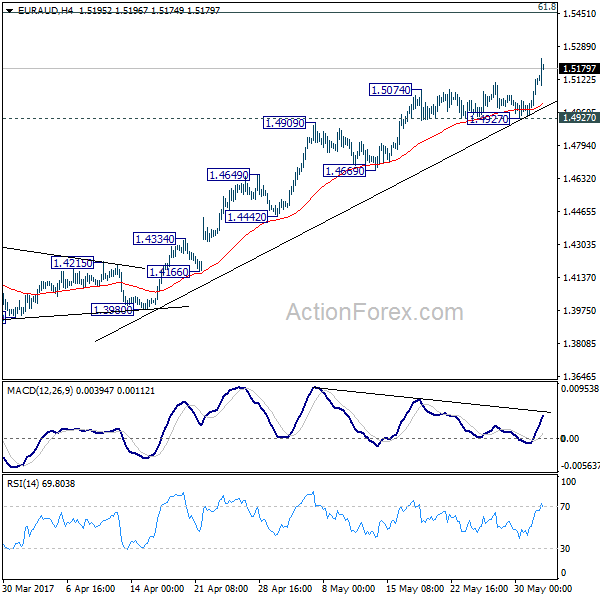

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5004; (P) 1.5067; (R1) 1.5191; More...

EUR/AUD's rally resumes today and surges to as high as 1.5226 so far. Intraday bias is back on the upside for next medium term fibonacci level at 1.5455. On the downside, break of 1.4927 is needed to signal short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. In any case, outlook will now stay cautiously bullish as long as 1.4669 support holds.

Australian Dollar Down as Private Capital Spending Missed, China PMI Dipped into Contraction

Australian dollar was given a brief boost by retail sales data in Asian session but quickly reversed. It's trading as the biggest loser so far for the day and the week. Retail sales rose 1.0% mom in April, above expectation of 0.3% mom. However, markets seem to be more sensitive to private capital expenditure, which rose a mere 0.3% in Q1, even worse than expectation of 0.5%. Meanwhile, China's private Caixin PMI manufacturing tumbled to 49.6 in May, down from 50.3 and missed expectation of 50.2. That's the first contraction reading in 11 months. Comparing with the official PMI, the Caixin one focuses more on SMEs and indicates that these companies could be under some pressure in May which might drag down the economy ahead.

Kiwi firms up mildly

New Zealand Dollar, on the other hand, is lifted mildly by as terms of trade index rose 5.1% qoq, in Q1, just slightly down from prior quarter's 5.8% qoq, and beat expectation of 3.9% qoq. The Kiwi was also supported by comments from RBNZ governor Graeme Wheeler earlier this week that risks to the financial system, domestically and from broad, have reduced. AUD/NZD extends the decline from March high at 1.1017 to as low as 1.0045 so far. It's clear that the corrective rebound from 1.0234 has completed with three waves up to 1.1017. Near term outlook will stay bearish as long as 1.0608 resistance holds, for 1.0323 support and then 1.0234 low.

BoJ Harada: No big long term losses on stimulus exit

BoJ board member Yutaka Harada addressed the concerns of stimulus exit and noted that the central bank won't suffer large long-term losses because of that. Harada said that it's "of course possible" that BoJ would register losses because it will "receive low interest rates while paying high interest rates". But such losses will be temporary. Instead, BoJ will "always make a profit in the long rung as it can buy high-yielding government bonds using cash and current account deposits that carry almost no cost." Regarding the economy, he pointed to the fall in unemployment rate to 2.8% and emphasized that "if this trend continues and the jobless rate falls further, there's no doubt prices will rise".

Released from Japan, capital spending rose 4.5% in Q1, above expectation of 3.9%. PMI manufacturing was finalized at 53.1 in May.

Fed's Beige Book affirmed June hike expectations

The upbeat Beige Book from Fed solidifies the case of a June rate hike. Fed fund futures are pricing in 91.2% chance of that. The reported suggested that most of the twelve Fed Districts reported a continued expansion in activity "at a modest or moderate pace", although Boston, Chicago and New York indicated some degrees of slowdown. Labour markets continued to tighten, with most Districts reporting shortages in a wide range of jobs. Despite continuing improvement in the employment condition, wage growth remained "modest to moderate". Overall, pricing pressures were reported to be little changed from the last report, with most Districts reporting "modest" increases.

Trump to announce decision on Paris accord

US President Donald Trump will announce his decision regarding the global pact to fight climate change at 1900 GMT today. It is reported that Trump will deliver his election promise and pull out from the accord. And that will leave US as one of the only three non-participant in the 195-nation agreement, with Syria and Nicaragua. Republican Mitt Romney expressed his disagreement and emphasized that the Paris agreement is "is not only about the climate: It is also about America remaining the global leader." Meanwhile, European Commission President Jean-Claude Juncker said that "the Americans can't just leave the climate protection agreement. Mr. Trump believes that because he doesn't know the details."

Also...

News regarding UK election next week will continue to influence the Pound. And for today, UK PMI manufacturing will also be watched. In European session, Eurozone PMI manufacturing final, Italian GDP, Swiss retail sales and SVME PMI, Swiss GDP will also be released. Later in US session, ISM manufacturing will be the main focus together with ADP employment. Jobless claims, non-farm productivity and construction spending will also be featured.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5004; (P) 1.5067; (R1) 1.5191; More...

EUR/AUD's rally resumes today and surges to as high as 1.5226 so far. Intraday bias is back on the upside for next medium term fibonacci level at 1.5455. On the downside, break of 1.4927 is needed to signal short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. In any case, outlook will now stay cautiously bullish as long as 1.4669 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q/Q Q1 | 5.10% | 3.90% | 5.70% | 5.80% |

| 23:50 | JPY | Capital Spending Q1 | 4.50% | 3.90% | 3.80% | |

| 0:30 | JPY | PMI Manufacturing May F | 53.1 | 52 | 52 | |

| 1:30 | AUD | Private Capital Expenditure Q1 | 0.30% | 0.50% | -2.10% | -1.00% |

| 1:30 | AUD | Retail Sales M/M Apr | 1.00% | 0.30% | -0.10% | -0.20% |

| 1:45 | CNY | Caixin PMI Manufacturing May | 49.6 | 50.2 | 50.3 | |

| 5:45 | CHF | GDP Q/Q Q1 | 0.50% | 0.10% | ||

| 6:00 | GBP | Nationwide House Prices M/M May | 0.20% | -0.40% | ||

| 7:15 | CHF | Retail Sales (Real) Y/Y Apr | 2.40% | 2.10% | ||

| 7:30 | CHF | SVME PMI May | 57.8 | 57.4 | ||

| 7:45 | EUR | Italy Manufacturing PMI May | 56.1 | 56.2 | ||

| 7:50 | EUR | France Manufacturing PMI May F | 54 | 54 | ||

| 7:55 | EUR | Germany Manufacturing PMI May F | 59.4 | 59.4 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI May F | 57 | 57 | ||

| 8:00 | EUR | Italian GDP Q/Q Q1 F | 0.20% | 0.20% | ||

| 8:30 | GBP | PMI Manufacturing May | 56.5 | 57.3 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y May | -42.90% | |||

| 12:15 | USD | ADP Employment Change May | 181K | 177K | ||

| 12:30 | USD | Non-Farm Productivity Q1 F | -0.60% | -0.60% | ||

| 12:30 | USD | Unit Labor Costs Q1 F | 3.00% | 3.00% | ||

| 12:30 | USD | Initial Jobless Claims (27 MAY) | 238K | 234K | ||

| 14:00 | USD | ISM Manufacturing May | 54.6 | 54.8 | ||

| 14:00 | USD | ISM Prices Paid May | 67 | 68.5 | ||

| 14:00 | USD | Construction Spending M/M Apr | 0.50% | -0.20% | ||

| 14:30 | USD | Natural Gas Storage | 75B | |||

| 15:00 | USD | Crude Oil Inventories | -4.4M |

Australia’s Manufacturing Sector Activity Slowed In May, Retail Sales Jumped The Most Since 2014 In April

For the 24 hours to 23:00 GMT, the AUD declined 0.44% against the USD and closed at 0.7425.

LME Copper prices rose 0.1% or $7.5/MT to $5615.5/MT. Aluminium prices declined 1.2% or $24.0/MT to $1919.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7391, with the AUD trading 0.46% lower against the USD from yesterday's close, following dismal Australian manufacturing data.

Overnight data revealed that Australia's AiG performance of manufacturing index declined to a level of 54.8 in May. In the previous month, the index had recorded a reading of 59.2.

On the other hand, the nation's seasonally adjusted retail sales climbed 1.0% on a monthly basis in April, advancing by the most in nearly three years and surpassing market expectations for an advance of 0.3%. In the previous month, retail sales had registered a revised drop of 0.2%.

Elsewhere, in China, Australia's largest trading partner, the Caixin/Markit manufacturing PMI index fell to a level of 49.6 in May, dropping into the contraction territory, compared to a level of 50.3 in the previous month. Market anticipation was for the PMI to drop to 50.1.

The pair is expected to find support at 0.7361, and a fall through could take it to the next support level of 0.7332. The pair is expected to find its first resistance at 0.7444, and a rise through could take it to the next resistance level of 0.7498.

Moving ahead, Australia's HIA new home sales data for April, set to be released overnight, will be eyed by traders.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.