Sample Category Title

Hot First Quarter Growth Marks a Canadian GDP ‘Three-Peat’

The Canadian economy roared ahead in the first quarter of the year, expanding 3.7% q/q annualized. Including price effects, nominal GDP growth was an impressive 8.9%.

Consumers were the star of the show as household spending rose 4.3% on the back of robust durables spending (+9.9%). It seemed that Canadians still can't shake their debt habit, as nominal household expenditures outpaced disposable income growth, resulting in a 1 percentage point drop in the household savings rate (to 4.3%).

The positive story was not confined to consumers. Business investment rebounded significantly (+10.3%) on strength in machinery and equipment investment (+25.3%), while investment in intellectual property products rose 6.3% supported by an eye-popping 67.1% rise in mineral exploration. On the residential investment side of things, a 15.7% gain in activity marked the strongest performance since 2012 on the back of strong construction activity and a significant increase in resale activity.

Net trade was a modest drag on growth as exports were effectively flat (-0.3%) and imports gained sharply (+13.7%), as the impacts of earlier one-offs worked their way out of the data. Of course, imports must go somewhere, and in the first quarter, they appear to have largely made their way into inventories, which rose $14.9 billion, adding 3.6 percentage points to first quarter growth.

The 0.5% expansion of monthly GDP in March was also encouraging, providing a healthy starting point for the second quarter. The goods-producing side of the economy led the way (+0.9%) on strong gains in utilities and manufacturing (both +1.6%). The service sector expanded at a still healthy 0.3% monthly pace, with gains in retail trade (+1.0%), finance and insurance (+0.8%), and wholesale trade (+0.7%) leading the way. Encouragingly, on an industry basis, the Canadian economy continues to demonstrate a breadth of expansion: 80% of Canadian industries, representing approximately 90% of output expanded in March, the best performance since May 2014.

Key Implications

Wasn't it America that was supposed to be made great again? And yet boring old Canada was a first quarter pace of growth that more than tripled what was seen for the U.S. Moreover, although helped by a post-wildfire recovery, the 2016Q3 to 2017Q1 'three-peat' marked the fastest three-quarter string of growth since the post-crisis recovery in early 2010. Beneath the surface however, there are reasons to expect a less exciting pace of expansion going forward.

To begin with, there is already evidence that key housing markets are beginning to cool off, suggesting that the robust pace of first quarter growth is not likely to be seen again any time soon. At the same time, the environment for business investment should remain supportive, but elevated uncertainty is likely to cap the pace of growth. Finally, consumers are likely to keep their wallets open, helped by past gains in housing wealth. But, it is again unlikely that the pace of first quarter growth, particularly for durable goods spending, can be maintained, and the credit-fueled nature of recent spending growth remains concerning.

It is not all bad news however - strong March figures provide a solid start to the second quarter, setting the Canadian economy up another quarter of well above-trend growth.

For the Bank of Canada, despite the March GDP figures, concerns about the durability of growth and still soft consumer price inflation will likely result in continued near-term caution. That said, we remain of the view that growth is likely to moderate but remain above-trend, supported by a continuation of the broad based growth trend that has emerged in recent months. This broad-based growth, alongside nascent inflationary pressures, should set the stage for the beginning of a gradual tightening cycle early next year.

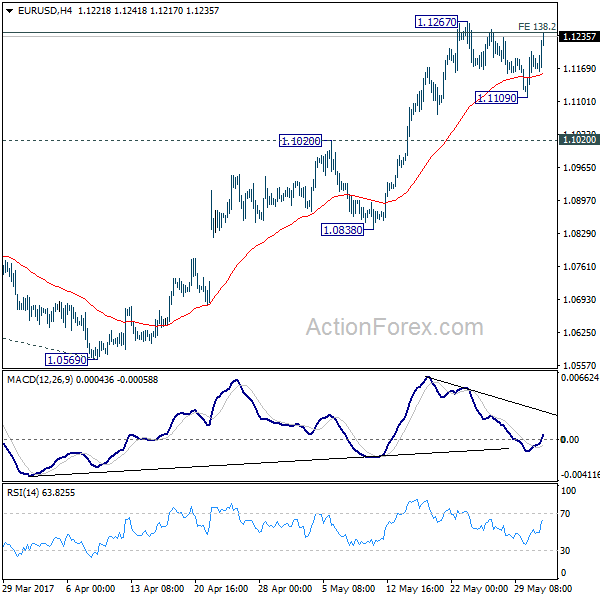

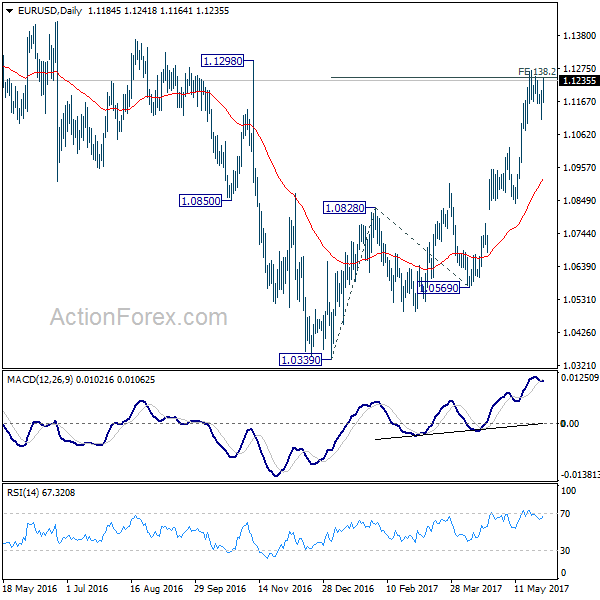

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1127; (P) 1.1166 (R1) 1.1223; More....

EUR/USD rebounds strongly today but it's stays below 1.1267 so far. And intraday bias stays neutral first. Nonetheless, pull back from 1.1267 could be completed at 1.1109 already. Break of 1.1267 will resume recent rise. Decisive break of 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) resistance zone will carry larger bullish implication and target 1.1615 resistance next. In case consolidation from 1.1267 extends with another fall, further rise will remain in favor as long as 1.1020 support holds. But, break of 1.1020 will indicate rejection from 1.1245/98 and turn bias to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

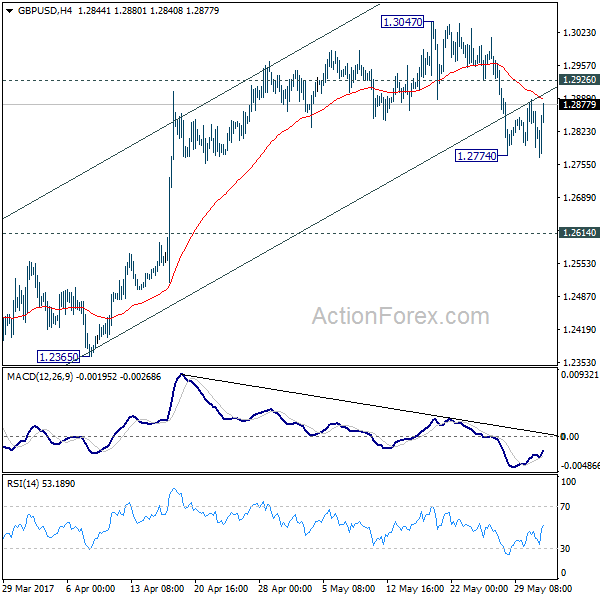

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2804; (P) 1.2846; (R1) 1.2898; More...

Despite breaching 1.2774 temporary low, GBP/USD quickly recovered and intraday bias stays neutral first. We're holding on to view that rise from 1.2108 is completed. Hence, upside of current recovery should be limited by 1.2926 minor resistance and bring another decline. Below 1.2774 will target 1.2614 resistance turned support next. Break there should also indicate completion of whole consolidation pattern from 1.1946 and target a retest on this low. Meanwhile, above 1.2926 minor resistance will turn focus back to 1.3047 high instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.56; (P) 110.93; (R1) 111.22; More...

With 111.46 minor resistance intact, intraday bias in USD/JPY remains mildly on the downside for 110.23 support. Break will resume the fall from 114.36 to 108.12 and below. Note again that decline from 118.65 is seen as a correction. In that bearish case, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48. On the upside, above 111.46 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

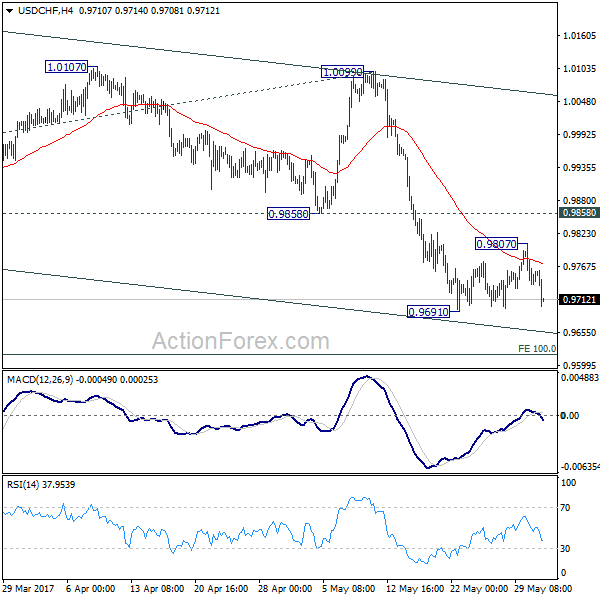

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9718; (P) 0.9763; (R1) 0.9789; More.....

USD/CHF drops sharply today but it's staying above 0.9691 temporary low. Intraday bias stays neutral first. Consolidation from 0.9691 could have completed at 0.9807 already. Break of 0.9691 will resume recent fall from 1.0342 to 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there. In case of another rise as the consolidation extends, upside should be limited by 0.9858 support turned resistance and bring fall resumption.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

Euro Shrugs off CPI Miss, Resuming Recent Rise against Dollar and Pound

Euro shrugs off lower than expected Eurozone inflation reading and strengthens against Dollar and Sterling today. EUR/USD is heading back to 1.1267 resistance while USD/CHF is heading back to 0.9691 support. Both currency could be set to resume recent rally against the greenback. Eurozone CPI slowed to 1.4% yoy in May, down from 1.9% yoy and missed expectation of 1.5% yoy. Eurozone core CPI slowed to 0.9% yoy, down from 1.2% yoy and missed expectation of 1.0% yoy. Also from Eurozone, Germany unemployment dropped -9k in May, fewer than expectation of -14k. Unemployment rate dropped to 5.7%. German retail sales dropped -0.2% mom in April.

The Euro remains supported by expectation that ECB policymakers would start discussing stimulus exit in the June meeting. There might be a hawkish twist and President Mario Draghi's press conference. But even if not, ECB should be starting to pave the way to announce something in September. The current asset purchase program will end in December and ECB should prepare the markets for what's after that in by latest September.

Italian Central Bank Governor Visco: Leaving euro won't solve Italy's problems

In Italy, central bank governor Ignazio Visco said that "it is an illusion to think that Italy's economic problems could be solved more readily outside Economic and Monetary Union." And he emphasize that leaving the Euro would not heal the "structural defects" of Italian economy, not "lower interest expenses and not "magically lower our debt level". He warned that "on the contrary, it would generate serious risks of instability". Instead, he urged Italy to work on brining down its huge public debt, which is at around 132% of GDP and the second highest in Eurozone after Greece. Visco emphasized that "an appreciable and lasting decline in the debt-to-GDP ratio must commence without delay."

Some volatility is seen in Euro this week on news that Italy could be close to an early election. With major parties converging to a deal on a new electoral law, an early election might take place in coming months, probably synchronizing that of German's in September. The euro reacted negatively and declined to the lowest level in more than a week before rebound. The 10-year Italian-German yield spread soared to almost the highest level in a month on concerns that the rapidly-rising Five Star Movement, the populist, euro-skeptic political party, could eventually become part of the coalition in Italy and destabilize European Union again. More in Political Uncertainty Re-Emerges in Europe, Euro Volatility Spikes.

Sterling weighed down by prospect of hung government

Sterling is so far the weakest major currency today, next to Aussie. The British Pound is pressured as a new poll indicates that Prime Minister Theresa May's Conservative could fall short of an overall majority in the upcoming election on June 8. According to a new modelling by YouGov for the Times, it predicts that the Conservative would get 310 seat in the parliament, down from the prior 330 seat. On the other hand, Labour would get 257 seats, up from prior 229 seat. As the required majority is 326 seats, it now means that a hung parliament is a realistic possibility.

Released from UK, mortgage approvals dropped to 65k in April. M4 money supply rose 1.2% mom in April. Gfk consumer confidence rose to -5 in May, BRC shop price dropped -0.4% yoy. Also from Europe, Swiss UBS consumption indicator rose to 1.48 in April.

Canada GDP beats expectation, but impact offset by oil weakness

Canada GDP rose 0.5% mom in March, up from prior month's 0.0% mom and beat expectation of 0.3% mom. In annualized term, GDP growth accelerated to 3.7% qoq in Q1, up from prior quarter's 2.7% but missed expectation of 3.9%. USD/CAD stays in tight range above 1.3387 today as consolidations continue. The positive effect from GDP data was offset by falling oil price. WTI crude oil is trading down -2.5% at 48.4 at the time of writing and looks set to take on 48 handle soon. Meanwhile, Dollar will look into Chicago PMI, pending home sales and Fed's Beige Book report later today.

China PMIs show stabilizing in the slowdown

In China, the National Bureau of Statistics PMI manufacturing, the official one, was unchanged at 51.2 in May. While that stayed at the lowest level in six months, it was above expectation of 51.0. Looking at the details, new orders was unchanged at 52.3, export orders rose 0.1 to 50.7. Production dropped to 53.4, down from 53.8. Employment rose to 49.4 from 49.2. Input price dropped to 49.5 from 51.8. Output prices dropped to 47.6 from 48.7. The official PMI services rose to 54.5, up from 54.0. Overall, the set of data at least showed no further deterioration in growth momentum. Nonetheless, the picture will still be closely monitored by economists in the coming months. The impact from Moody's downgrade of China's credit ratings for the first time in nearly 30 years is yet to be seen. Elsewhere, Japan industrial production rose 4.0% mom in April. Housing starts rose 1.9% yoy in April.

New Zealand businesses upbeat

New Zealand ANZ business confidence rose to 14.9 in May, up from 11.0. ANZ noted that "the economy's excellent adventure continues". And, "firms are upbeat, and prepared to hire and invest. That's an economic expansion that is still going full steam. Survey indicators are elevated but not stratospheric, consistent with the economy evolving into a mature stage of the expansion; we're growing nicely off a good base, as opposed to lifting rapidly off a low level."

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9718; (P) 0.9763; (R1) 0.9789; More.....

USD/CHF drops sharply today but it's staying above 0.9691 temporary low. Intraday bias stays neutral first. Consolidation from 0.9691 could have completed at 0.9807 already. Break of 0.9691 will resume recent fall from 1.0342 to 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there. In case of another rise as the consolidation extends, upside should be limited by 0.9858 support turned resistance and bring fall resumption.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence May | -5 | -8 | -7 | |

| 23:01 | GBP | BRC Shop Price Index Y/Y May | -0.40% | -0.30% | -0.50% | |

| 23:50 | JPY | Industrial Production M/M Apr P | 4.00% | 4.10% | -1.90% | |

| 01:00 | NZD | ANZ Business Confidence May | 14.9 | 11 | ||

| 01:00 | CNY | Manufacturing PMI May | 51.2 | 51 | 51.2 | |

| 01:00 | CNY | Non-manufacturing PMI May | 54.5 | 54 | ||

| 05:00 | JPY | Housing Starts Y/Y Apr | 1.90% | -1.50% | 0.20% | |

| 06:00 | EUR | German Retail Sales M/M Apr | -0.20% | 0.40% | 0.10% | 0.20% |

| 06:00 | CHF | UBS Consumption Indicator Apr | 1.48 | 1.5 | 1.44 | |

| 07:55 | EUR | German Unemployment Change May | -9K | -14k | -15k | |

| 07:55 | EUR | German Unemployment Rate May | 5.70% | 5.70% | 5.80% | |

| 08:30 | GBP | Mortgage Approvals Apr | 65K | 66K | 67K | 66K |

| 08:30 | GBP | M4 Money Supply M/M Apr | 1.20% | 0.40% | 0.30% | |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 9.30% | 9.40% | 9.50% | |

| 09:00 | EUR | Eurozone CPI Estimate Y/Y May | 1.40% | 1.50% | 1.90% | |

| 09:00 | EUR | Eurozone CPI - Core Y/Y May A | 0.90% | 1.00% | 1.20% | |

| 12:30 | CAD | GDP M/M Mar | 0.50% | 0.30% | 0.00% | |

| 13:45 | USD | Chicago PMI May | 57 | 58.3 | ||

| 14:00 | USD | Pending Home Sales M/M Apr | 0.60% | -0.80% | ||

| 18:00 | USD | Fed Beige Book |

British Pound Slips on YouGov Poll

- Sterling slips on YouGov poll

- Euro strengthens as data improves

- Improved Chinese data benefits AUD and NZD

- Canadian economic growth forecast for an uptick

Sterling dropped a little yesterday when a YouGov poll suggested that the Tory party could fall short of a majority on June 8th. This is further proof that the markets are keen for a decisive victory to aid the strength of Britain's negotiating hand in the Brexit discussions. The EU has published a very detailed document outlining just how much Britain needs to fund when we leave the EU. I love a provocative opening negotiating stance, don't you? Other than mortgage lending figures, there is nowt in the UK data diary today, so, once again, the Pound will be wafted around by political speculation. Currently, the GBP-EUR rate is in the €1.14 area and the GBP-USD rate is around $1.28.

We get a couple of interesting stats from the Eurozone today. The unemployment rate may have eased to 9.4%. That's still appalling, but any improvement is welcome. We will also see the Eurozone inflation rate, which is forecast to have dipped, oddly enough. With energy prices rising, balanced against a strengthening Euro, maybe the forecasters have got their sums right, but there is scope for a mismatch between the fact and the forecast.

And the Euro-USD rate is also susceptible to volatility today with the Eurozone data and, from the US side, the Chicago Purchasing Managers' Index (PMI) and the release of the Federal Reserve's Beige Book. That regional view of the US economy can produce changes in sentiment as far as the Fed members are concerned, hence its ability to affect exchange rates.

Last night brought the Chinese Manufacturing Sentiment Index, which was better than forecast, and that has strengthened the currencies of China's supplier nations. Those include Australia and New Zealand. The Aussie and Kiwi Dollars are both stronger this morning and the forecast for Australia's Manufacturing PMI, due out overnight tonight, is positive. So further Aussie Dollar strength before tomorrow morning is a real possibility.

The Canadian Dollar also benefits if China – one of the big global users of raw materials – sees improvement in its economy. This afternoon brings Canada's economic growth data. Rising growth is forecast; an annualised 2.9% compared to the previous 2.5%. That will be good news for the Canadian Dollar, which is already a little stronger this morning. Those who need to buy CAD in the short term may decide to trade early.

Have a great Wednesday… or is it Tuesday? Bank holidays always throw my head-calendar out of whack.

At the psychologist's office

A guy goes in to see a psychologist. He sits on the couch and says, "The problem is that I can't seem to make any friends. Can you help me fatso?"

GOLD – Hesitates But Still Retains Upside Bias

GOLD - The commodity continues to hold on to its upside pressure short term though hesitating on Tuesday. On the downside, support comes in at the 1,250.00 level where a break will turn attention to the 1,240.00 level. Further down, a cut through here will open the door for a move lower towards the 1,230.00 level. Below here if seen could trigger further downside pressure targeting the 1,220.00 level. Conversely, resistance resides at the 1,270.00 level where a break will aim at the 1,280.00 level. A turn above there will expose the 1,290.00 level. Further out, resistance stands at the 1,300.00 level. All in all, GOLD looks to strengthen further despite price hesitation

GBP Under Pressure After Latest Poll

- GBP Slips as Conservative Majority Wiped Out in Latest YouGov Poll;

- Panelbase Poll Claims Otherwise Offering Some Reprieve For GBP;

- EUR Higher as Eurozone Unemployment Falls to Eight Year Low;

- Fed Speakers and US Data Still to Come Today.

US futures are pointing to a flat open on Wednesday, similar to what we've seen already in Europe, with focus remaining on the UK election as the June 8 vote nears.

Sterling has been under pressure once again on Wednesday and continues to show its vulnerability to the polls as the election nears. While there has been plenty of evidence of the polls being wrong in the past – most notably during the last election campaign in 2015 – it's hard to ignore the collapse in Theresa May's lead over recent weeks. The latest YouGov poll suggests that not only has the Conservative majority been slashed compared to only a couple of weeks ago, it's disappeared altogether which has triggered further weakness in the pound.

With momentum being very much against the Conservatives, the pound may remain very vulnerable as we near the 8 June vote. The uncertainty that a hung parliament would bring is clearly far from ideal when the country is due to begin Brexit negotiations only 11 days later and this may be contributing to the moves in the currency. Should the pound break below 1.2750 against the dollar, it could trigger further downside for the pair, with 1.27 offering possible support but 1.26 being the next key level.

Interestingly, a poll released later in the morning from Panelbase suggested the Conservative lead still remains very much intact. In fact, it claims it's been increased compared to two weeks ago, up to 15 points. Under the circumstances, it's no wonder that people continue to question the reliability of these polls. While the pound has recovered some lost ground following the release, the polls generally do seem to suggest that May's lead in slipping which could ensure it remains vulnerable to downside moves.

We had some mixed data from the eurozone this morning, with unemployment falling to its lowest level in eight years and further than was expected. The inflation release on the other hand was slightly disappointing, with core inflation falling back to 1%, as expected, but headline inflation falling a little more to 1.4%, from 1.9% previously. This is well below the ECBs target of below but close to 2% but after a brief period of choppiness, the euro appears to have shrugged off the inflation number in favour of the better labour market figures. While the gains aren't substantial, the euro is trading back around 1.12 against the dollar, which has being something of a ceiling for the pair over the course of this week. Still to come today we've got some data from the US, including pending home sales and the Chicago PMI. We'll also hear from two Fed policy makers – Robert Kaplan and John Williams – with only two weeks to go until its next meeting. As it stands, markets are pricing in almost an 87% chance of a rate hike in two weeks but only a 42% chance of another one this year. That would explain the weakness we've seen in the dollar despite June appearing to have never been in doubt.

Sterling Spikes Lower After Poll Predicts Hung Parliament

The British pound tumbled overnight, following the release of an election opinion poll by YouGov, which projected the Conservative party to fall short of a majority in Parliament by 16 seats (326 needed for majority). Such an outcome would imply a “hung parliament”, meaning that the Conservatives would need to form a coalition with another party, or govern with a minority. In both of these scenarios, Theresa May would likely have less domestic support than previously and as a result, her hand in the Brexit negotiations may be weaker.

Even though one should not take the results of a single poll for granted, we have to note that over the past few weeks, the gap between Conservatives and Labour has been steadily narrowing in almost all polls. So, even though this one showed a potentially extreme outcome with the Conservative party not being able to even establish a majority, most other polls confirm the story that Labour is slowly but surely catching up. If new polls show that this trend continues heading into Election Day next week, we would expect the British pound to remain under pressure, on speculation that this race may actually be closer than previously anticipated.

GBP/USD was trading marginally above the 1.2850 support (now turned into resistance) hurdle ahead of the release of the poll. The pair then dropped below that hurdle to hit support a few pips above the 1.2770 (S1) zone. Should new polls indicate that the Conservative - Labour gap continues to narrow over the next week, we would expect the bears to retake control at some point and push the price lower. A clear break below 1.2770 (S1) could pave the way for the next support at 1.2700 (S2).

Euro lifted by another media report about the ECB

The euro came under renewed buying interest yesterday, following a Reuters report that the ECB is set to upgrade its language about growth at the June meeting, and that the Governing Council will discuss whether to drop some aspects of its forward guidance that stimulus can be increased in the future if needed. We share the view for a more optimistic tone on growth. Policymakers could acknowledge that the risks surrounding the outlook for growth are no longer tilted to the downside but are instead “broadly balanced”, considering that growth-related data are very strong and that forward-looking indicators like the PMIs suggest this will likely continue.

However, we think it is far too early for the ECB to alter its forward guidance, by removing the signals that the QE program can be expanded and that rates could be lowered further in the future if needed. Even though policymakers could indeed discuss this prospect, we do not expect an actual decision next week. Such a rapid change in language could be over-interpreted by investors as a preliminary hint to tapering, which could result in a sharp appreciation of the euro as well as a spike higher in euro-area bond yields. What's more, a couple of days ago, Draghi clearly said that an extraordinary amount of monetary policy support is still needed, including through the use of the Bank's forward guidance. In any case, for now, market focus will be on the bloc's CPI figures for May, due out today (see below).

Today's highlights:

During the European day, Eurozone's preliminary CPI figures for May will capture market attention. The forecast is for both the headline and the core rates to have declined. The focus will probably be on the core rate, which is anticipated to have declined to +1.0% yoy from +1.2% yoy previously. Even though this could hurt EUR somewhat, we doubt that such a modest pullback will materially curb speculation regarding a more optimistic tone by the ECB with regards to economic growth. We also get the bloc's unemployment rate for April, which is expected to have declined even further.

EUR/JPY traded higher yesterday after it hit support near the 123.00 (S2) level, to break above the resistance (now turned into support) barrier of 124.00 (S1). During the early European morning Wednesday, it is trading marginally above that level and in case of a pullback in Eurozone's core CPI rate, we could see the pair moving back below 124.00 (S1), and perhaps aim for another test of 123.00 (S2).

From Canada, we get GDP data for March. The forecast is for GDP growth to have risen following a stagnant print in February. The forecast is supported by the strong retail sales print, as well as the fact that net exports turned positive during the month. Indeed, in its latest policy statement, the BoC also noted that growth was very strong in the first quarter. In case of a strong print, CAD could extend its recent gains.

In the US, the Chicago PMI for May and pending home sales for April are coming out.

We have three speakers on the agenda: ECB Executive Board member Benoit Coeure, ECB Executive Board member Sabine Lautenschlager and Dallas Fed President Robert Kaplan.

GBP/USD

Support: 1.2770 (S1), 1.2700 (S2), 1.2600 (S3)

Resistance: 1.2850 (R1), 1.2900 (R2), 1.2950 (R3)

EUR/JPY

Support: 124.00 (S1), 123.00 (S2), 122.00 (S3)

Resistance: 124.50 (R1), 125.30 (R2), 125.80 (R3