Sample Category Title

US Economy Expands 1.2% In March Quarter, Orders For US-Manufactured Durable Goods Fall In March

'Economic indicators so far aren't entirely convincing on a second-quarter bounce in activity and show a U.S. economy struggling to surprise on the upside.' — Scott Anderson, Bank of the West

The US economy expanded at a stronger-than-initially-expected pace in the March quarter; however, an economic slowdown remained on the table in the second quarter. The Commerce Department reported on Friday that Q1 GDP growth came in at a seasonally adjusted annualised pace of 1.2%, compared to an originally reported pace of 0.7%. Meanwhile, analysts expected the economy to expand 0.9% in the reported quarter. However, that was the worst performance over the past 12 months. Back in the Q4 of 2016, the economy grew 2.1%. Analysts suggested that the Q1 slowdown was mainly driven by the US President Donald Trump's inability to boost economic growth as promised. Even though the Q1 figure was revised up sharply, weak retail sales, business investment, falls in investment inventories and an increase of the goods trade deficit destroyed hopes for a rebound in the Q2. A separate report released by the Commerce Department showed that new orders for US-manufactured durable goods dropped 0.7% last month, whereas orders for core durable goods fell 0.4%.

EUR/USD Analysis: Trades Below 1.12 Mark

'Draghi's four-year inflationary campaign has so far failed to put price growth on a self-sustaining path toward the ECB's goal of just under 2 percent.' – Alessandro Speciale, Bloomberg

Pair's Outlook

On Monday morning the common European currency began the week against the US Dollar below the resistance near the 1.1190 level. Near that level, at 1.1187, is located the monthly R2, and exactly at the 1.1190 mark resides the 61.80% Fibonacci retracement level. The currency exchange rate is expected to decline down to the first weekly support level, which is located at the 1.1141 mark. As it is a lone support level, it is highly possible that it will be passed and the pair will set its course for the weekly S2 at 1.1097.

Traders' Sentiment

SWFX traders remain bearish, as 60% of open positions are short. However, only 51% of trader set up orders are to sell the Euro.

GBP/USD Analysis: Correction Anticipated

'Any declines are now classified as corrective and should be well supported ahead of 1.2500 in favour of a higher low and bullish resumption.' – LMAX Exchange (based on PoundSterlingLive)

Pair's Outlook

The Sterling suffered from the election polls, which showed that Theresa May is barely ahead, thus, resulting in a breach of the strong support cluster around 1.2850. Although a technical correction after such a decline is likely, downside risks remain present as well. The 1.28 psychologic level is what keeps keeping the GBP/USD pair afloat at the moment, with the next strong demand area located only around 1.27, formed by the weekly S1, the 55-day SMA and the 23.60% Fibo. Meanwhile, technical indicators are in favour of the positive outcome, in which case the nearest significant resistance will be the weekly pivot point at 1.2977, but such a strong recovery is unlikely.

Traders' Sentiment

Bulls are now slightly outnumbering the bears, as 51% of all open positions are now long and the remaining 49% are short.

USD/JPY Analysis: Remains On The Back Foot

'The markets are used to news of North Korea's missile tests by now, and the dollar/yen is unlikely to move much unless there is some further escalation of the situation.' – Sony Financial Holdings (based on Reuters)

Pair's Outlook

Even though Friday's fundamentals turned out to be better than expected, the Core Durable Goods Orders still weighed on the Buck, ultimately resulting in the USD/JPY pair weakening that day. As a result, the pair prolonged its consolidation, once again putting the 111.00 level to the test. Technical indicators today suggest the Greenback could attempt to pierce the 111.00 mark to the downside again, which would leave the tough support cluster around 110.30 to limit the losses in the future. Trade is likely to be relatively flat this week ahead of Friday's NFP data.

Traders' Sentiment

There are 57% of traders holding short positions today, compared to 58% on Friday. Meanwhile, all pending orders in the 100-pip range are equally divided between the buy and the sell ones.

Gold Analysis: Reaches Near 1,270 level

'We remain friendly on gold and suspect that we will likely push higher over the course of the coming week.' – Edward Meir, INTL FCStone (based on Reuters)

Pair's Outlook

The yellow metal started the week below the 1,270 mark with a decline. The reason for the decline was the fact that the commodity price already reached and has bounced off the resistance put up by the monthly PP, which is located at the 1,269.77 level. In general, a continuation of the surge in the future is still expected. However, before that the bullion is most likely going to retreat until it finds support in the weekly PP at the 1,261.80 level. Afterwards, the already mentioned monthly level of significance will pose a resistance. Although, due to the month ending soon that resistance will become obsolete soon.

Traders' Sentiment

SWFX traders remain almost neutral, as 51% of open positions are long. Meanwhile, 67% of pending commands are set to buy the metal.

Daily Technical Analysis: GBP/JPY Now Moment Sellers Could Be Waiting At Confluence Zone

The GBP/JPY has broken through a flat bottom descending triangle that has been forming on H1 time frame. The triangle is classified as a running one due to lack of vortex at the top (the pinnacle). At this point the price is retracing towards the POC zone (W H3, D H3, order block, ATR pivot, 38.2) 143.20-40. If there are now moment sellers within the zone, the price could reject towards 142.00 and 141.65. Have in mind that UK banks will be closed today in observance of the Spring Bank Holiday, so the price might not get to it's full projected target if rejection from POC happens.

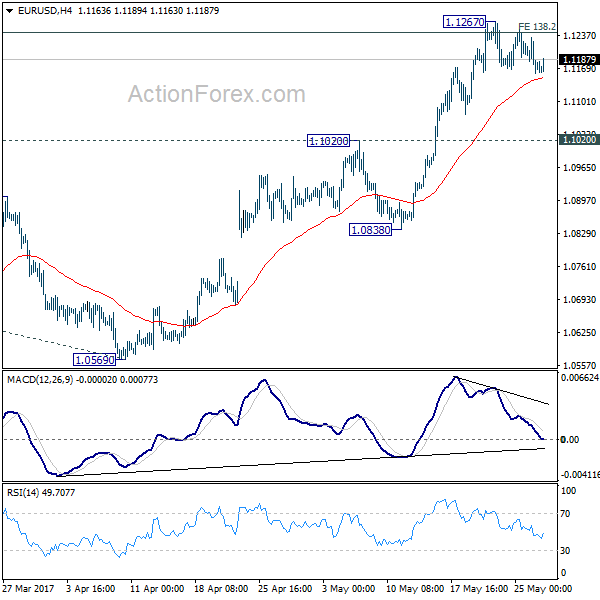

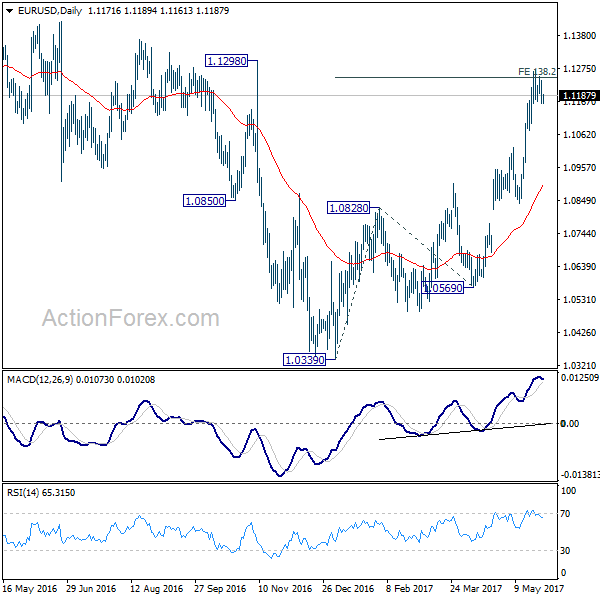

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1148; (P) 1.1191 (R1) 1.1222; More....

Intraday bias in EUR/USD remains neutral for the moment. At this point, remain cautious on strong resistance from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) to limit upside and bring reversal. But another rise will be in favor as long as 1.1020 resistance turned support holds. Decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. On the downside, though, break of 1.1020 resistance turned support will indicate rejection from 1.1245/98 and turn bias to the downside for 1.0838 support first.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

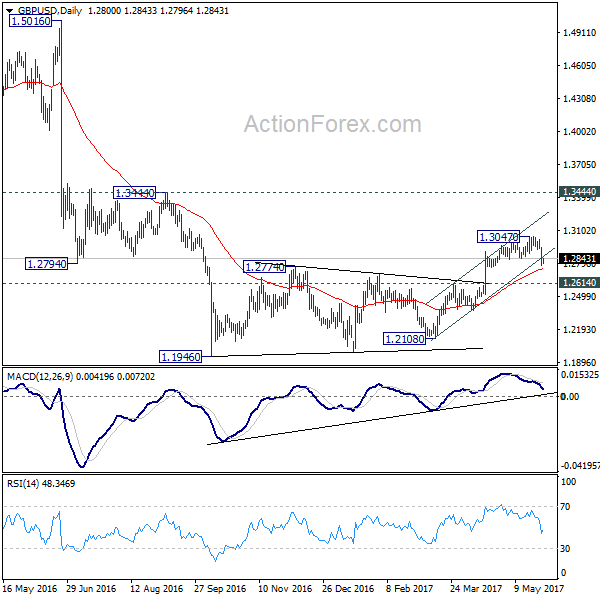

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2737; (P) 1.2841; (R1) 1.2908; More...

Intraday bias in GBP/USD remains on the downside despite mild recovery today. As noted before, a short term top is in place at 1.0347 on bearish divergence condition in 4 hour MACD. Also, rise from1.2108 could have completed too. Deeper fall would be seen for 1.2614 resistance turned support first. Break there should also indicate completion of whole consolidation pattern from 1.1946 and target a retest on this low. Meanwhile, above 1.2926 minor resistance will turn focus back to 1.3047 high instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

Technical Outlook: GBPUSD – Friday’s Long Red Candle Weighs And Risks Fresh Downside After Correction

Cable is consolidating above 1.2800 handle on Monday, following Friday's strong fall. Strong bearish acceleration was triggered after thick weekly cloud repeatedly capped bull-leg from 1.2365. Dip found footstep at 1.2775 and managed to close above 1.2786 pivot (Fibo 38.2% of 1.2356/1.3047 upleg), sidelining immediate downside risk.

However, Friday's long bearish candle continues to weigh, with daily studies losing traction and seeing risk of further easing.

Current action could be seen as positioning for fresh easing with extended upticks seen on oversold slow stochastic on daily chart, expected to stay capped under converged 20/10 SMA's (1.2926/35 respectively). Bearish continuation requires close below Fibo 1.2786 support to open way for extension towards 55SMA (1.2694) and daily cloud top at 1.2656.

Conversely, sustained break above 20/10SMA's would signal an end of corrective phase from 1.3047 (18 May peak).

Res: 1.2866, 1.2895, 1.2911, 1.2935

Sup: 1.2786, 1.2775, 1.2694, 1.2656

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9707; (P) 0.9722; (R1) 0.9745; More.....

Intraday bias in USD/CHF remains neutral at this point. Consolidation from 0.9691 could extend and stronger recovery cannot be ruled out. But upside should be limited by 0.9858 support turned resistance and bring fall resumption. Whole decline from 1.0342 is still in progress and below 0.9691 will target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.