Sample Category Title

USD/JPY Analysis: Steady In This Trading Session

'While the dailies still point lower, the 4 hour charts are recovering after having become oversold and further short term gains would not surprise. On the downside, minor support will be seen at 111.00 and 110.70 ahead of the session low of 110.23.' – Jim Langlands, FX Charts (based on FX Street)

Pair's outlook

Yesterday, the US Dollar managed to regain some losses after the massive plummet on Wednesday. However, it seems that traders are once again looking in the direction of the save-haven currency. The nearest support formed by the weekly S2 at 111.41 may hinder the rate from trading lower; however, it may not be strong enough to halt it, thus leading the pair to the 111.30 territory. In case the Greenback manages to push north, a penetration of the 100-day at 111.77 might indicate that the currency has finally recovered from the latest political turmoil. This scenario is confirmed by bullish short-term technical indicators.

Traders' sentiment

Market sentiment remains bearish, as 56% of open positions are short. Meanwhile, 51% of pending orders are to buy the US Dollar.

Gold Analysis: Finds Support Below 1,250

'The gold rally was overdone and there was a correction on Thursday.' – Brian Lan, GoldSilver Central (based on Reuters)

Pair's outlook

On Friday morning, the yellow metal's price was regaining some of the losses, which were suffered during Thursday's trading session. During that day the bullion retreated down to the levels below the 1,250 mark, where the 20, 55 and 200-day SMAs are located at. The combined support of these levels of significance managed to stop the fall of the commodiy price. Afterwards a rebound began, which has passed the resistance of the 50.00% Fibonacci retracement level at 1,249.16 level. Due to these factors combined it can be assumed that the bullion will attempt to reach the weekly R3 at 1,261.72 once more.

Traders' sentiment

Traders are neutral in regard to the metal. However, 70% of pending commands are to buy the bullion.

BRL Tumbles Amid Political Uncertainty

Brazilian assets fell sharply yesterday at the market opening in São Paulo as the political uncertainty rose by another notch. The Brazilian real fell more than 7% against the greenback with USD/BRL rising at around 3.3760 compared to Wednesday's close of 3.1349 after Brazilian newspaper reports about President Michel Temer.

On the equity side, the situation is not bright either as sell-off in Brazilian equities triggered a circuit-breaker that halted trading after futures on the Bovespa crashed 10% at the Thursday open. In one day, the Brazilian stock market erased almost entirely the gains accumulated since the New Year as the Bovespa closed at 61,597 yesterday.

Investors were caught by surprise as the political situation seemed to settling down as the business-friendly Brazilian President successfully managed to ease foreign investors' concerns. Traders' panicked reaction sent option's implied volatility on USD/BRL through the roof with the 1m measure spiking to 24% from 13.5% a day earlier. The 1m 25 delta risk reversal measure, which is the difference between the price of a call and a put, spiked to 5.74%. Despite the fact that Michel tried to reassure markets, financial indicators continued to move in the other direction with treasury yields and CDS exploding.

Investors reacted aggressively to the news therefore we may see a temporary stabilisation of Brazilian assets morning, especially since the global risk-off sentiment is easing with global equities recovering this morning. However, investors are more than accustomed with the Brazilian political landscape and they know that it may take months before an equilibrium may be reached again. Therefore we would remain cautious regarding the BRL's outlook, even though there will be some opportunities in the short-term.

Greece: Tsipras negotiates on new austerity policies

It has been a while since Greece was at the top of the market news. We consider this is as a key issue for the European Union so we are still monitoring the country. It is now back into recession (printing two consecutive growth negative quarters) despite the massive austerity policies over the last few years.

Pension cuts or the increase in taxes do not seem to be sufficient and the cost of servicing the debt is way too massive so we do not see any positive issue on that. Greece cannot devalue its currency and so it is then forced to devalue internally, for instance its public aid (pensions in particular).

Since February 2015, Greece has repaid €35.4 billion and by the end of 2018 Greece must repay €28 billion (including €2.7 billion of interest). To put that into perspective, the 2016 nominal GDP was €176 billion. The economy must then expand by at least more than 1.5% next year. And next year repayments are less than half of what Greece will need to pay in 2019.

We don't see how Greece will be able to reimburse this debt as it is clear that the country won't be able to print a growth above the cost of servicing its debt. In the short-term, everything looks decent on the single currency side but what will happen when Portugal or Spain have issues as deep as Greece. Uncertainties are far from over on the euro side.

Markets Priced In OPEC Output Cut Extension

There are two upcoming events that are expected to impact the price of Oil; firstly, the Iran presidential election will be held today (May 19th) and secondly, the OPEC meeting will be held on May 25 in Vienna. The result of the Iran presidential election and the associated geo-political risks will likely affect its oil production.

Overall, the execution of OPEC's output cut agreement has been sound. However, some OPEC member states exempted from the agreement, such as Iran, Libya, and Nigeria, have been increasing their production. Some non-OPEC oil producers, such as Russia and Kazakhstan, also attempt to enlarge their production.

In addition, the US shale oil industry has seen a marked recovery since February last year because of higher oil prices. The US Baker Hughes data (that records the number of new Oil Rigs) is showing additional Rigs added every week. Since May 2016 the US has added more than 400 new rigs.

In general, the oil supply remains high, which has and will offset OPEC's output cut effort to an extent. If OPEC announces that the output cut is to be extended we will likely see a moderate rally in oil prices, instead of a surge, as markets have priced in the extension to an extent.

Oil prices have rebounded approximately 7% since May 5th. On Thursday, WTI spot hit a 4-week high of $50.29 a barrel. Brent crude spot hit a 4-week high of $53.29 a barrel. USD/CAD has seen a 1% retracement since May 5th because of the oil price rebound. The level at 1.3500 will likely provide a stronger support.

Today we will see the release of a set of Canadian economic data for March and April, including; CPI, core CPI and retail sales. These data releases will likely affect CAD and CAD crosses.

On Thursday, the dollar index hit a post presidential election low of 97.26, then experienced a moderate rebound, touching 97.96 then retraced, as there is heavy pressure at the level at 98.00. USD/JPY hit a 3-and-a-half week low of 110.22 with the downtrend holding above a significant support line at 110.00.

Gold has seen a 1.19% correction after hitting a 2-and-a-half-week high of $1264.92 because of the dollar rebound.

It was reported that the Trump Camp had contacted Russian officials 18 times by phone and emails before the presidential election (from April to November 2016). Some election staff pointed out that it is not unusual for presidential candidates to contact foreign officials. However, liaison with a non-aligned country (Russia) with high frequency seems to be unusual.

The downtrend of USD has been temporarily held; the next move of USD will likely depend on upcoming economic data, FOMC minutes and the progress of the FBI investigation into Trump's Russia leak scandal.

Euro Edges Up On German Inflation Report

The euro has edged higher in the Friday session, erasing some of the gains seen on Thursday. Currently, EUR/USD is trading at 1.1140. In the eurozone, German PPI improved to 0.4%, beating the estimate of 0.2%. Later, the eurozone releases current account and consumer confidence. There are no US events on the schedule.

German inflation numbers were stronger in the first quarter, but inflation numbers continue to meet or exceed the forecasts in the second quarter. Producer Prices posted a gain of 0.4% in April, and the Wholesale Price Index gained 0.3% in April. The news was not as good from Final CPI, which dipped to 0.0%, marking a 3-month low. Still, this figure matched the estimate. In the eurozone, Final CPI for April matched the forecast with a strong gain of 1.9% in April, considerably higher than last month’s gain of 1.5%. Eurozone inflation is once again closing in on the ECB’s target of 2.0%, which could increase pressure on the ECB to consider tapering its ultra-loose monetary policy. However, the ECB seems content to hold course on interest rates and its quantitative easing program, and the central bank will be reluctant to make any moves with key elections coming up in France and Germany.

It’s been an excellent week for the euro, as the chaos in Washington continues to unnerve investors and has weighed on the US dollar. The Trump administration is in damage control mode, although there is no sign of the political firestorms letting up any time soon. Facing relentless pressure from Democrats and some Republicans, the Justice Department has appointed a former FBI director as a special prosecutor to investigate possible Russian involvement in the US presidential election as well as any connection between Trump and the Russians during the election campaign. President Trump fired back on Thursday, angrily denouncing this move as a 'witch hunt'. The media and the Democrats have had a field day with Trump’s woes, and many Republicans are expressing unease with an administration that appears rudderless and is staggering from crisis to crisis. Trump has been relentlessly dogged by accusations of being cozy with the Russians, and his meeting with the Russian foreign minister last week was a public relations disaster, as Trump came under heavy criticism for releasing classified information at the meeting. The latest string of controversies has had a chilling effect on global stock markets, and many investors have ditched their dollar-held assets in favor of the euro and other currencies.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

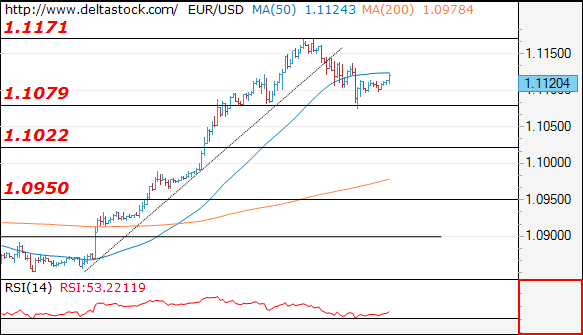

EUR/USD

Current level - 1.1120

Yesterday's peak at 1.1171 started a pullback and the intraday bias is slightly bearish, with a risk of a slide through 1.1080, towards 1.1020 support area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.1130 |

1.1130 |

1.1094 |

1.1022 |

|

1.1200 |

1.1300 |

1.1022 |

1.0838 |

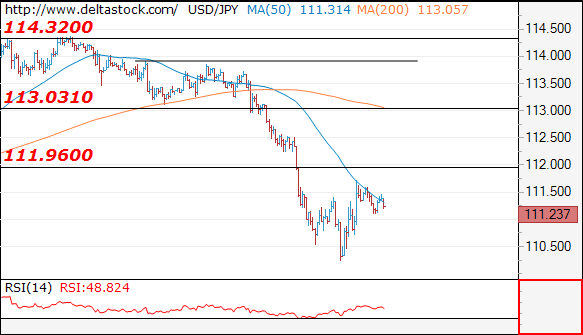

USD/JPY

Current level - 111.23

The reversal at 110.23 shows a positive bias, for a break through 111.90resistance, towards 113.00 hurdle.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

113.00 |

114.30 |

112.00 |

109.40 |

|

114.30 |

115.60 |

112.00 |

108.12 |

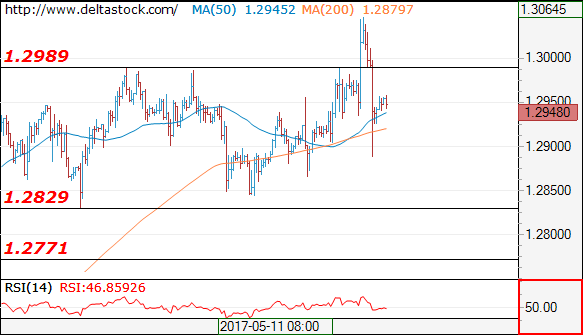

GBP/USD

Current level - 1.2948

The recent break through 1.2990 resistance was a short-lived one and the return below the mentioned area signals a risk of another attempt at 1.2830 crucial level. A break through the latter will confirm a reversal on the senior frames, challenging 1.2770 and 1.2610 areas. Key on the upside is 1.2990.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.2990 |

1.3120 |

1.2830 |

1.2770 |

|

1.3050 |

1.3500 |

1.2770 |

1.2610 |

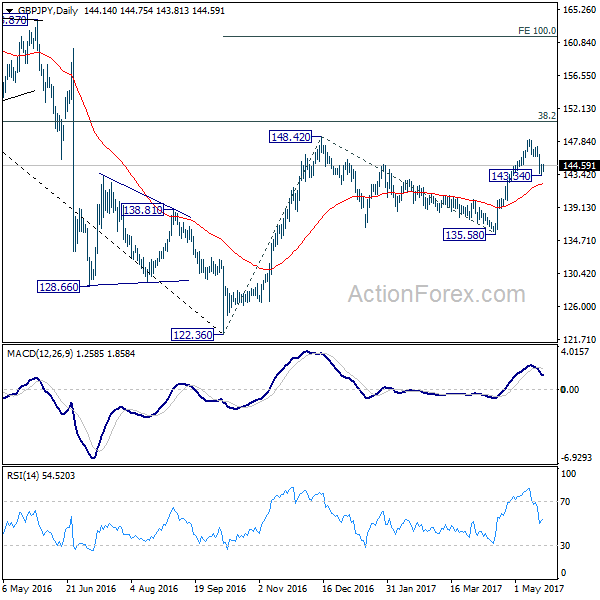

GBP/JPY Daily Outlook

Daily Pivots: (S1) 142.85; (P) 144.48; (R1) 145.34; More....

Intraday bias in GBP/JPY is turned neutral as it drew support from 38.2% retracement of 135.58 to 148.09 at 143.31 and recovers. Overall, we'd still expect the rise from 122.36 to resume after pull back from 148.09 completes. Above 145.78 minor resistance will turn bias to the upside for 148.09. Break there will target 150.42 long term fibonacci level. Nonetheless, break of 143.34 will extend the pull back to 61.8% retracement at 140.35.

In the bigger picture, based on current momentum, rise from 122.36 bottom should be developing into a medium term move. Break of 38.2% retracement of 195.86 to 122.36 at 150.42 should pave the way to 61.8% retracement at 167.78. This will now be the favored case as long as 135.58 support holds.

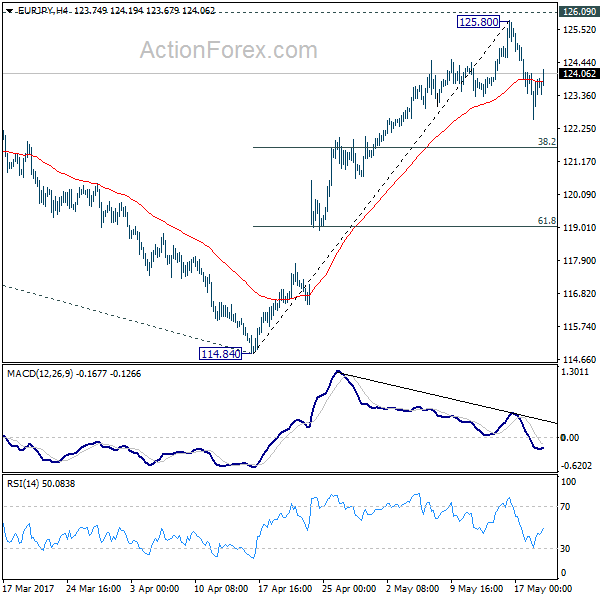

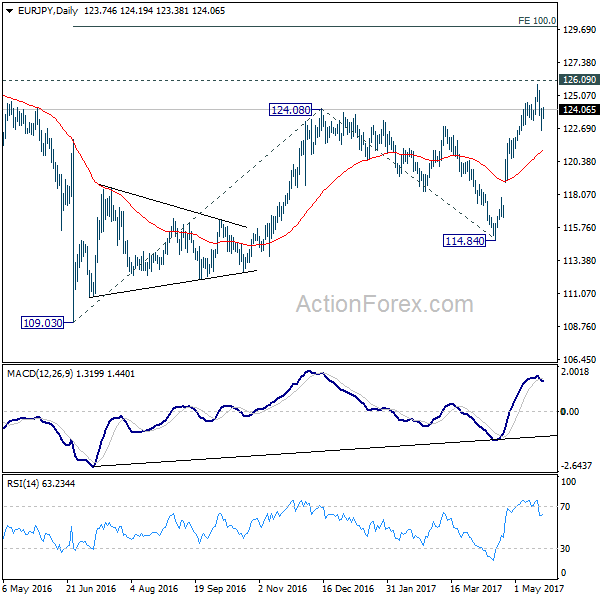

EUR/JPY Daily Outlook

Daily Pivots: (S1) 122.85; (P) 123.47; (R1) 124.40; More...

Intraday bias in EUR/JPY remains neutral for consolidation below 125.80 short term top. Deeper pull back could be seen. But downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

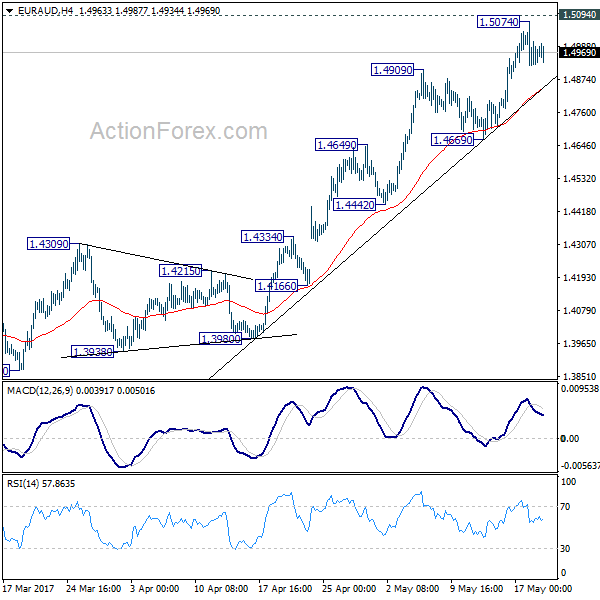

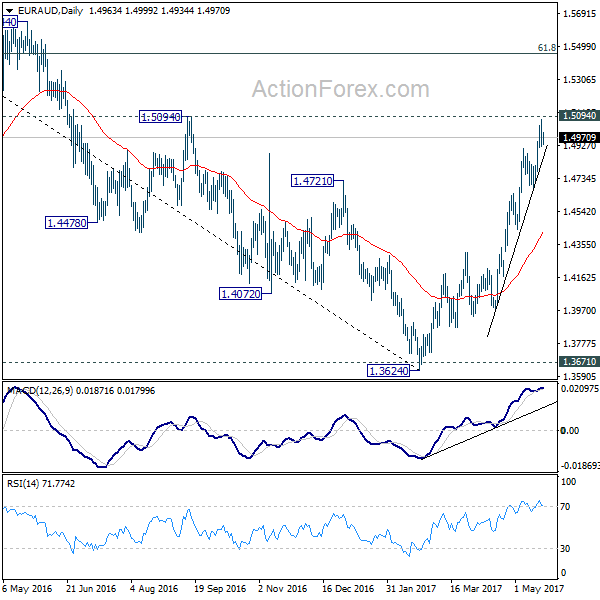

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4939; (P) 1.4991; (R1) 1.5065; More...

Intraday bias in EUR/AUD remains neutral for consolidation below 1.5074 temporary top. Deeper retreat could be seen but outlook will remain bullish as long as 1.4669 support holds. We're holding on to the view of trend reversal. Break of 1.5094 will extend the rise from 1.3624 to next medium term fibonacci level at 1.5455.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455 and above. In any case, outlook will now stay cautiously bullish as long as 1.4309 resistance turned support holds.

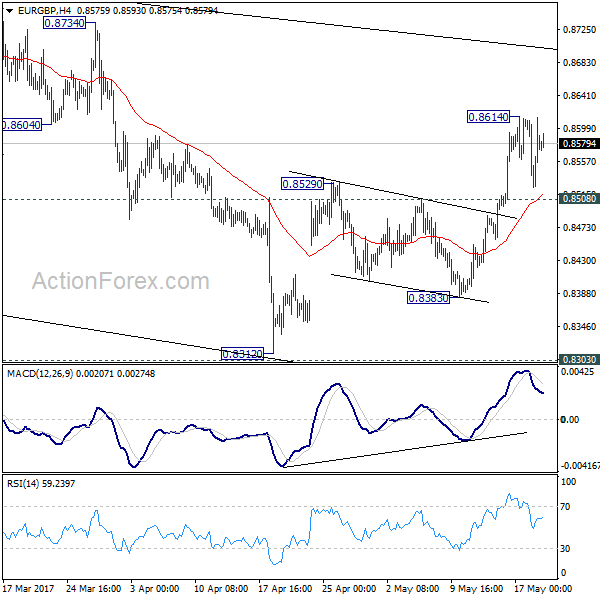

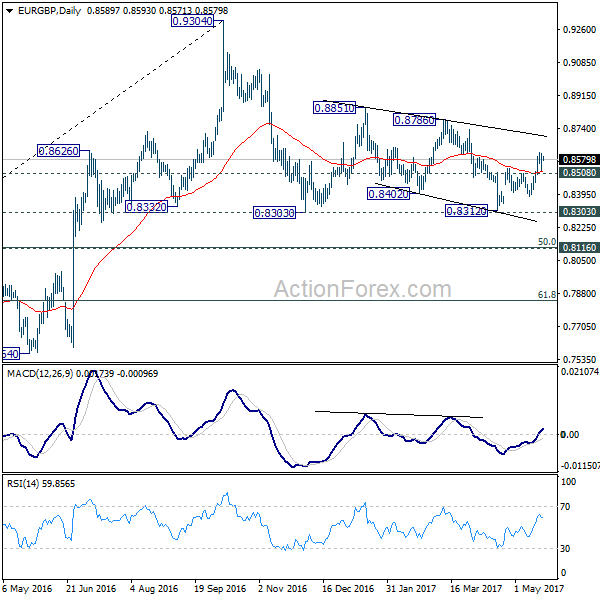

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8531; (P) 0.8571; (R1) 0.8619; More...

A temporary top is in place at 0.8614 and intraday bias is turned neutral first. Another rise is expected as long as 0.8508 resistance turned support holds. Above 0.8614 will target 0.8786 resistance next. Overall, price actions 0.9304 are viewed as a medium term corrective pattern that is extending. As EUR/GBP has just defended 0.8303 resistance. Break of 0.8786 could bring a retest on 0.9304 high. On the downside, below 0.8508 minor support will turn bias back to the downside for 0.8383 support instead.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.