Sample Category Title

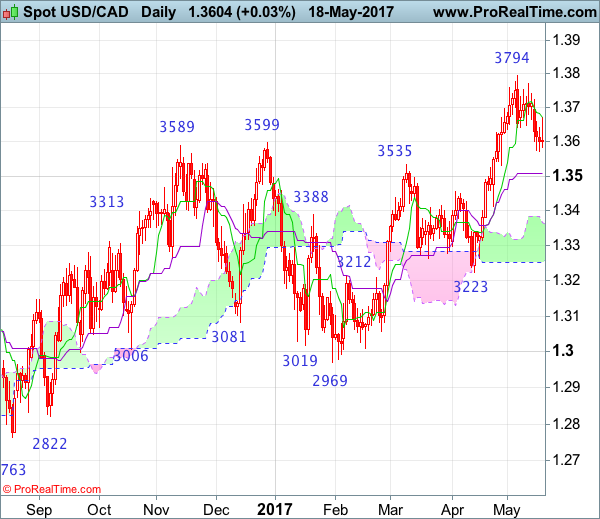

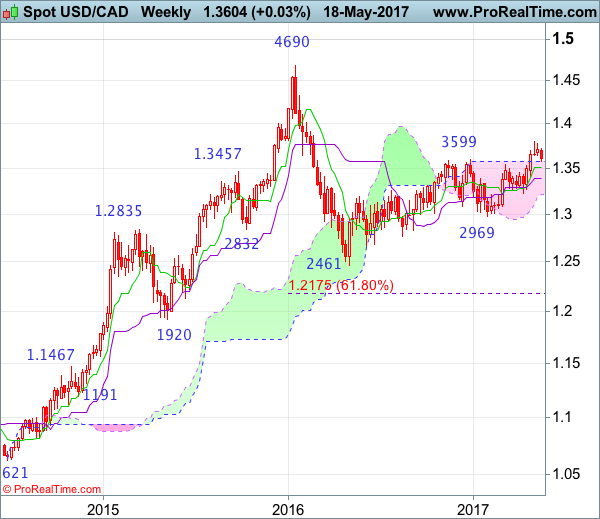

USD/CAD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting doji

• Time of formation: 02 May 2016

• Trend bias: Up

Daily

• Last Candlesticks pattern: Bearish engulfing

• Time of formation: 5 May 2017

• Trend bias: Up

USD/CAD – 1.3597

As the greenback has retreated again after faltering below recent high of 1.3794, suggesting further consolidation below this level would be seen, however, still reckon downside would be limited to 1.3540-50 and bring rebound later, above 1.3670 would bring test of 1.3720-25 but break of 1.3770 is needed to signal the pullback from 1.3794 has ended, bring retest of this level. Once this recent high is penetrated, this would confirm resumption of upmove from 1.2461 and extend gain to 1.3835-40 (61.8% Fibonacci retracement of 1.4690-1.2461) and possibly towards 1.3900-10 but overbought condition should prevent sharp move beyond 1.3950 and price should falter below psychological resistance at 1.4000.

On the downside, below 1.3530 support would abort and signal a temporary top has been formed at 1.3794, bring retracement of recent upmove to 1.3470-75, then 1.3440 but reckon previous support at 1.3411 would hold from here and bring rebound later. Looking ahead, only a daily close below this support at 1.3411 would signal recent upmove from 1.2461 has ended instead, bring further fall to the upper Kumo (now at 1.3359) and possibly 1.3300 but reckon the lower Kumo (now at 1.3258) would hold.

Recommendation: Hold long entered at 1.3650 for 1.3850 with stop below 1.3550.

On the weekly chart, although the greenback rose to as high as 1.3794 earlier this month, the subsequent retreat formed a doji pattern with a long upper shadow (shooting star alike) on the weekly chart, suggesting consolidation below this level would be seen and pullback to the upper Kumo (now at 1.3576) cannot be ruled out before prospect of another rise, above 1.3770 would bring retest of 1.3794 but break there is needed to extend recent erratic upmove from 1.2461 (2016 low) to 1.3835-40 (61.8% Fibonacci retracement of 1.4690-1.2461) and then 1.3900 but overbought condition should prevent sharp move beyond psychological resistance at 1.4000, risk from there has increased for a retreat to take place later.

On the downside, below 1.3530 support would defer and suggest a temporary top is possibly formed, bring test of the Tenkan-Sen (now at 1.3509), a weekly close below there would add credence to this view, bring retracement of recent upmove to 1.3450, then test of support at 1.3411 but reckon the Kijun-Sen (now at 1.3382) would limit downside and bring another rise later. In the event the pair drops below the Kijun-Sen, this would suggest top is formed instead, bring weakness to 1.3300, then 1.3260-65 but reckon support at 1.3223 would remain intact.

Currencies: Dollar Decline Slows, But No Sustained Rebound Yet

Sunrise Market Commentary

Rates: Cautiousness remains warranted, but 2.16% should hold

Risk sentiment will remain key for trading. Ahead of the weekend, cautiousness could be warranted (positive core bonds) with investors waiting on new developments in the Trump affaire. The US Note future tested the contract high (126-20) yesterday (2.16% support for US 10-yr yield), but a break higher didn't occur. Time to enter new short positions?

Currencies: Dollar decline slows, but no sustained rebound yet

The USD decline slowed yesterday as US tensions became less intense. The equity performance will probably guide USD trading short-term. Some ST consolidation might be on the cards. Cable failed to sustain north of 1.30 after strong UK retail sales, suggesting some underlying sterling softness

The Sunrise Headlines

- US stocks recovered from opening weakness to end around 0.3% higher with Nasdaq outperforming (+0.75%). Overnight, most Asian stock markets eke out small gains in subdued trading.

- President Trump said that the “witch hunt” should be quickly brought to a close, but the appointment of a special counsel and recent grand jury subpoenas suggest a federal probe is expanding to other suspicious activity and countries.

- The ECB should use its June meeting to start building the case for unwinding its monetary stimulus before making an announcement in the fall, according to Governing Council member Vasiliauskas.

- Cleveland Fed Mester said that financial-market volatility has not affected her economic outlook and the US central bank prefers to look through short-term swings in markets as it guides monetary policy

- Greece's Parliament approved a raft of fresh austerity measures and economic reforms that the country must implement in the next four years to unlock a much-needed cash payment to meet upcoming debt obligations.

- Mexico's central bank defied most market expectations and lifted its key lending rate by 0.25 point to 6.75%, after inflation surged past its target range last month. The increase is the sixth in a row and the eighth since February 2016

- Today's eco calendar only contains EMU consumer confidence. ECB Praet, ECB Constancio, Fed Bullard and Fed Williams are scheduled to speak

Currencies: Dollar Decline Slows, But No Sustained Rebound Yet

USD decline slows

On Thursday, European markets initially stayed in modest in risk-off modus, but the risk-off trade had no additional negative impact on the dollar. Interest rate differentials turned slightly in favour of USD. The US eco data were also better than expected. Later in the session, US equities even recouped a small part of Wednesday's losses, squeezing the dollar higher. EUR/USD closed the session at 1.1103 (from 1.1159). USD/JPY finished the session at 111.49 (from 110.83).

Overnight, Asian equities are trading slightly higher, reversing earlier losses. The immediate stress from the Trump crisis is easing. For now, the fall-out from the Brazil crisis on other Emerging markets looks contained. The cautious riskrebound is no big help for the dollar. USD/JPY is going nowhere and trades currently in 111.40 area. EUR/USD is holding a tight range in the low 111 area. Markets look for new impetus.

Today, there are no US data and only second tier ones in the EMU. Markets will keep an eye at the speeches from ECB' Praet and Constancio and Fed governors Williams and Bullard. We expect the ECB speakers to take a guarded approach as the internal debate on the communication at the June ECB meeting is still ongoing. The Fed speakers won't question the case for a June rate hike. Remarks on the tapering of the balance sheet remain interesting, but the impact on USD trading will be limited. The dynamics of equities will probably remain the key driver for FX trading.

In an daily perspective, some further consolidation might be on the cards, both for equities and for the dollar. Markets haven't made up their mind on the LT impact of the recent developments.

In a longer term perspective, we maintain the working hypothesis that recent turmoil makes it more difficult for US equities to extend the record rally. Maybe, we entered a sell-on-upticks market. At the same time, a June Fed rate hike is not in question and US yields are near important support levels. So, the dollar shouldn't lose that much interest rate support, even if sentiment on risk turns less buoyant. In this context, we assume that a sustained rebound of USD/JPY has become tough short term. A cautious sell-on-upticks approach is preferred. There is maybe more room for a ST rebound of the dollar against the euro. We remain sceptic on the safe haven characteristics of the euro if sentiment on risk would turn really risk-off.

Technical picture.

The USD/JPY rebound ran into resistance last week. Initially, it was no more than a correction, but Wednesday's sell-off/re-break below the 112.20 previous top aborted the uptrend and made the short-term picture negative. Return action lower in the 108.13/114.37 range is possible.

Last week, it looked that EUR/USD could revisit the 1.0821/1.0778 support (gap). However, Friday's US data and political unheaval finally propelled EUR/USD north the 1.1023 range top, improving the technical picture. The correction tops at 1.1300/1.1366 is the next resistance. We think that USD sentiment will have to be extremely negative to clear this hurdle short-term. Further ST EUR/USD gains might become tougher. Yesterday's top at 1.1172 is a first reference. A return below 1.1023 would indicate that the upside momentum has eased.

EUR/USD: euro breaks topside of the ST range but the rally is slowing

EUR/GBP

Cable fails to sustain gains north of 1.30

Yesterday, sterling showed two faces. Initially, sterling rebounded after very strong UK April retail sales. The report eased recent fears that a decline in real income due to higher inflation could weigh on domestic spending. EUR/GBP dropped from the 0.86 area to fill bids around 0.8525. Cable finally cleared the 1.30 barrier and came close to the 1.3050 area. However, sterling couldn't maintain the positive momentum. Especially cable was hit hard by a USD up-tick during the US trading session. We don't see high profile UK news to explain the manifest underperformance of sterling. The pair dropped to the 1.29 area and closed the session at 1.2938. EUR/GBP finished the session at 0.8580.

Today , the CBI trends orders are expected stable at 4. The impact of the report will only be of intraday significance for sterling trading. Sterling might be slightly more sensitive to a weak report rather than to a strong one. Of late, the positive sterling sentiment eased and euro strength prevailed in EUR/GBP trading.. The pair bottomed out with 0.84/0.8330 as a solid bottom. The breach of 0.8509/31 (previous ST tops) improved the technical picture. For now, we stick to the EUR/GBP uptrend even as the euro rebound might slow short-term. Longer term, Brexit remains potentially negative for sterling.

EUR/GBP: jumps north of ST range top

Market Update – Asian Session: Volatility Subsides As Trump Heads To Israel

US Session Highlights

(US) INITIAL JOBLESS CLAIMS: 232K V 240KE; CONTINUING CLAIMS: 1.90M V 1.95ME

(US) MAY PHILADELPHIA FED BUSINESS OUTLOOK: 38.8 V 18.5E; new orders remain strong

(US) Treasury Sec Mnuchin: affirms 3% or higher GDP growth is achievable if we reform taxes and regulation; reiterates plan to provide middle-class tax relief; we've had no talks about a national sales tax; on Glass-Steagall, Treasury does not support separation of banks from investment banks

(US) APR LEADING INDEX: 0.3% V 0.4%E

(US) March Factory Orders revised higher to +0.5% from +0.2%, Durables Orders revised higher to +1.7% from +0.9%

All major stock indices recovered some lost ground as investors regained confidence in the markets as an independent counselor was appointed by the Justice Department to investigate the claims of Russian contacts with the Trump campaign. Stocks were also helped by strong data and higher energy prices. The US dollar regained some lost ground against most Majors and the 10-year Treasury yield stabilized at 2.23%.

US markets on close: Dow +0.3%, S&P500 +0.4%, Nasdaq +0.7%

Best Sector in S&P500: Telecom

Worst Sector in S&P500: Energy

Biggest gainers: INCY +6.9%; KMX +6.2%; NVDA +5.4%

Biggest losers: CSCO -7.2%; MNK -3.5%; PRGO -3.5%

At the close: VIX 15.7 (-0.9pts); Treasuries: 2-yr 1.28% (+2bps), 10-yr 2.23% (+2bps), 30-yr 2.91% (+1bps)

US movers afterhours

ADSK: Reports Q1 -$0.16 v -$0.23e, R$486M v $473Me- Guides Q2 -$0.18 to -$0.14 v -$0.15e, R$488-500M v $489Me ; +10.1% afterhours

SPWH: Reports Q1 -$0.08 v -$0.07e, R$156.9M v $151Me- Guides Q2 $0.12-0.14 v $0.13e, R$189-194M v $189Me, SSS +8% to +10% ; +9.9% afterhours

MCK: Reports Q4 $3.42 v $3.04e, R$48.7B v $49.8Be- Guides initial FY18 adj EPS $11.75-12.45 v $11.51e ; +8.2% afterhours

SB: Reports Q1 -$0.07 v -$0.09e, R$33.3M v $28.5Me; +7.8% afterhours

ROST: Reports Q1 $0.82 v $0.79e, R$3.31B v $3.27Be; +4.2% afterhours

GPS: Reports Q1 $0.36 v $0.29e, R$3.44B v $3.41Be; affirms FY17 $1.95-2.05 v $1.98e (prior $1.95-2.05); +4.1% afterhours

CRM: Reports Q1 $0.28 v $0.26e, R$2.39B v $2.35Be; +1.4% afterhours

Key economic data

(NZ) NEW ZEALAND APR CREDIT CARD SPENDING M/M: 0.9% V 0.8% PRIOR; Y/Y: 6.4% V 7.1% PRIOR

(NZ) New Zealand Mar Net Migration: 5.8K v 6.1K prior; Annual net migration 71.9K v 68.1K y/y

(CL) CHILE CENTRAL BANK (BCCH) CUTS OVERNIGHT RATE TARGET BY 25BPS TO 2.50%; NOT EXPECTED

(MY) Malaysia Q1 GDP Q/Q: 1.8% v 1.2%e v 1.4% prior; Y/Y: 5.6% v 4.8%e

Asia Session Notable Observations, Speakers and Press

Asian indices are mixed, tracking a day of stabilization on Wall St where equities recovered, treasury yields found support, Gold returned below $1,250, and Fed Funds futures outlook for June hike was back above 70%. Investors noted a big beat in the Philly Fed index and a slide in weekly jobless claims as evidence the political turmoil may not overshadow economic recovery that follows a soft Q1. Pres Trump was also largely quiet aside from overnight tweets claiming extreme press bias against his administration as he prepared to travel to Israel on Friday for his first official out-of-state visit. Trump's 9-day trip will also take him to Saudi Arabia and Brussels to discuss the NATO treaty with European leaders. In FX, USD/JPY was the most volatile among the majors, slipping some 50pips from the early highs around 111.10, while AUD and NZD traded within 25pip ranges against USD. Momentum in Oil Price bounce also remained, with WTI rising above 49.80 for a 4-week high.

Economic data were limited to New Zealand, where card spending continued to rise and net migration hit new record highs. Earlier, both Chile and Mexico central banks surprised with a 25bp rate cut against anticipated hold, citing external challenges.

Among notable corporates, Takata was limit-up after reports of a settlement with top automakers. Toshiba also traded higher as Broadcom/KKR and Bain/Hynix partnerships battled out for the chip stake.

China

(CN) Two China fighter jets flew within 150 feet of a USAF jet while it was flying in international air space over Yellow Sea - US press

(CN) Fitch: China hard landing risks are receding; Geopolitical risks on the rise

(CN) China financial companies said to have issued CNY168T in wealth management products (WMPs) in 2016 - Chinese press

(CN) China may add to pension fund by using state capital - Chinese Press

Korea

(KR) China Pres Xi said to have told South Korea envoy he is willing to work to put bilateral relations on normal track - press

(KR) US Navy said to have moved a 2nd aircraft carrier near North Korea - US press

Asian Equity Indices/Futures (23:30ET)

Nikkei -0.2%, Hang Seng +0.3%, Shanghai Composite -0.1%, ASX200 -0.3%, Kospi +0.1%

Equity Futures: S&P500 -0.1%; Nasdaq -0.1%, Dax -0.1%, FTSE100 flat

FX ranges/Commodities/Fixed Income (23:30ET)

EUR 1.1095-1.1115; JPY 111.10-111.60; AUD 0.7405-0.7430; NZD 0.6880-0.6900

June Gold -0.3% at 1,250/oz; June Crude Oil +0.8% at $49.73/brl; July Copper +0.1% at $2.54/lb

SPDR Gold Trust ETF daily holdings fall 1.2 tonns to at 851.9 tonnes; 5th straight decline

iShares Silver Trust ETF daily holdings rise to 10,693 tonnes from 10,660 tonnes prior (4th straight increase)

(CN) China Finance Ministry sells 50-yr bonds at 4.08%, bid-to-cover 1.89x

(CN) PBOC SETS YUAN MID POINT AT 6.8786 V 6.8612 PRIOR; first weaker Yuan fix in 7 sessions; biggest margin of weakness since Feb 20th

(CN) PBOC to skip open market opeations v CNY80B prior injected; Sees banking liquidity at appropriate level

(AU) Australia MoF (AOFM) sells A$900M in 2.0% 2021 Bonds; avg yield: 1.980% v 2.044% prior; bid-to-cover: 3.48x v 4.96x prior

Asia equities notable movers

Australia

Fairfax Media (FXJ) -0.2%; TPG Capital and Hellman & Friedman have each asked for 4-5 weeks to perform due diligence on Fairfax; Bids unlikely to firm until FY17/18 - AFR

Ooh!Media (OML) -0.7%; Confirms termination of APN deal on regulatory concerns

Japan

Takata (7312) +20.0%; Trades limit-up 20% following $553M settlement with automakers

Toshiba (6502) +3.1%; Broadcom/KKR partnership said to be the leading bidder for chip unit, offering ¥2.2T

Renesas (6723) +2.7%; Strength attributed to announcement of plan by INCJ to sell shares in Renesas

Kobe Steel (5406) +1.5%; Began production of aluminum sheet for cars in China - Nikkei

SKY Perfect JSAT (9412) -4.2%; Reports FY16/17

Hong Kong

Evergrande (3333) +9.7%; S&P raises rating to B from B-; Outlook Stable

Global Tech (143) +3.8%; H1 result

Cogobuy Group (400) -5.1%; Q1 result

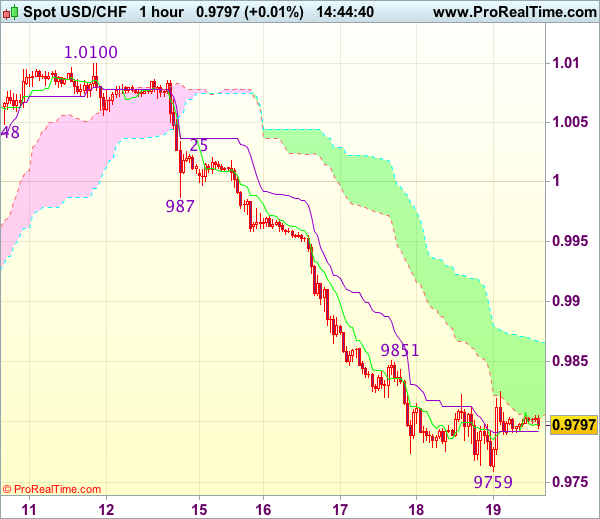

Trade Idea : USD/CHF – Sell at 0.9870

USD/CHF - 0.9792

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9798

Kijun-Sen level : 0.9866

Ichimoku cloud top : 0.9803

Ichimoku cloud bottom : 0.9792

Original strategy :

Sell at 0.9870, Target: 0.9770, Stop: 0.9905

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9870, Target: 0.9770, Stop: 0.9905

Position : -

Target : -

Stop : -

As dollar has recovered after yesterday’s marginal fall to 0.9764, suggesting minor consolidation above this level would be seen and recovery to 0.9850 cannot be ruled out, however, reckon 0.9860-70 would limit upside and bring another decline later, below said support at 0.9774 would extend early selloff from 1.0344 top towards 0.9735-40 (76.4% retracement of 0.9550-1.0344), however, near term oversold condition should prevent sharp fall below 0.9700, risk from there is seen for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 0.9860-70 should limit upside. Above 0.9900 would defer and risk rebound to 0.9925-30 but upside should be limited to 0.9950 and price should falter well below previous support at 0.9987, bring another decline.

Trade Idea : GBP/USD – Sell at 1.2990

GBP/USD - 1.2951

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2947

Kijun-Sen level : 1.2969

Ichimoku cloud top : 1.2947

Ichimoku cloud bottom : 1.2929

Original strategy :

Bought at 1.2945, stopped at 1.2910

Position : - Long at 1.2945

Target : -

Stop : - 1.2910

New strategy :

Sell at 1.2990, Target: 1.2890, Stop: 1.3025

Position : -

Target : -

Stop : -

Although cable resumed recent upmove to as high as 1.3048, the subsequent stronger-than-expected retreat to 1.2889 suggests top is possibly formed there and consolidation with mild downside bias is seen, break of said support would add credence to this view and extend weakness to support at 1.2866, however, reckon another previous support at 1.2844 would hold from here.

In view o this, we are looking to turn short on recovery as 1.2990-00 should limit upside, bring another decline later. Above 1.3020-25 would risk retest of said resistance at 1.3048 but break there is needed to revive bullishness and signal upmove has once again resumed for headway to 1.3075-80 and possibly 1.3100-10.

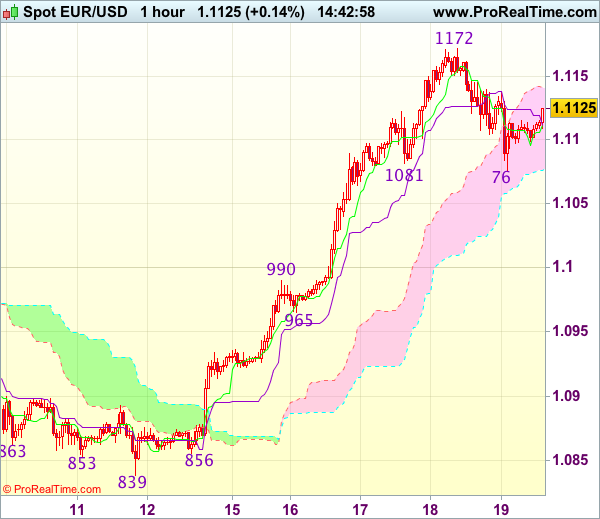

Trade Idea : EUR/USD – Buy at 1.1055

EUR/USD - 1.1123

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1113

Kijun-Sen level : 1.1111

Ichimoku cloud top : 1.1141

Ichimoku cloud bottom : 1.1076

Original strategy :

Buy at 1.1055, Target: 1.1155, Stop: 1.1020

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1055, Target: 1.1155, Stop: 1.1020

Position : -

Target : -

Stop : -

Although the single currency has rebounded after finding support at 1.1076 and consolidation with mild upside bias is seen for gain to 1.1140-45, break there is needed to signal the retreat from yesterday’s high of 1.1172 has ended, bring retest of this level, break there would extend recent upmove to 1.1200-10 (1.618 times projection of 1.0839-1.0990 measuring from 1.0965) but loss of momentum should limit upside and 1.1250 should hold. If said resistance continues to hold, then further consolidation would take place and another corrective fall to 1.0076 cannot be ruled out but downside should be limited to 1.1050-55 and bring another rise later.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as 1.1065-70 should limit downside. Below previous resistance at 1.1025 (now support) would defer and suggest top is possibly formed instead, risk test of another previous resistance at 1.0990 first.

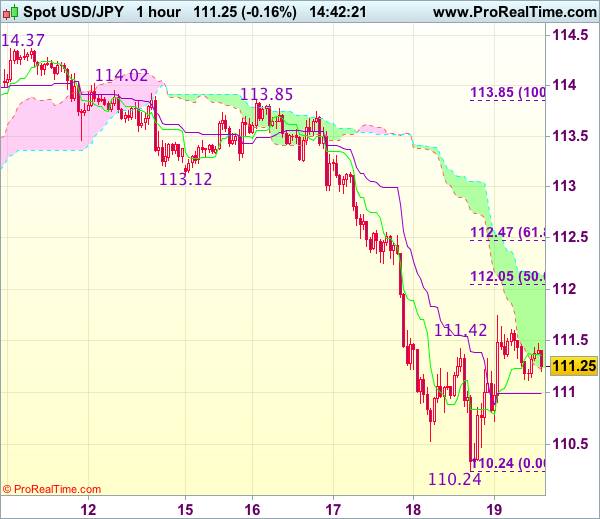

Trade Idea : USD/JPY – Sell at 112.05

USD/JPY - 111.20

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.36

Kijun-Sen level : 110.99

Ichimoku cloud top : 112.14

Ichimoku cloud bottom : 111.22

Original strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

Dollar’s rebound after falling to 110.24 suggests consolidation above this level would be seen and corrective bounce to 112.00-05 (50% Fibonacci retracement of 113.85-110.24) cannot be ruled out, however, reckon upside would be limited and bring another decline later, below 110.70-75 would suggest the rebound from 110.24 has ended, bring retest of this level first.

In view of this, would not chase this fall here and would be prudent to sell dollar on subsequent recovery as 112.05-10 should limit upside and bring another decline. Above 112.35-40 would defer and signal low is formed instead, risk a stronger rebound to 112.65-70.

US Equities Recovered Some Ground

Market movers today

Today is another quiet day in terms of data releases. In the afternoon, the euro area consumer confidence indicator for May is due out , which we expect to show a rise to -3.1 from -3.6 in April. Although political events seem to have limited effect on consumer confidence, the election of Emmanuel Macron could potentially give further tailwind to consumer confidence

A few central bank speeches are scheduled but we do not consider them market movers.

In Denmark, the consumer confidence indicator for May is due out this morning, which we expect to be largely unchanged from April at 7.4.

Selected market news

Asian stocks are mixed this morning after US equities recovered some ground yesterday as focus shifted from political risks in the US back to economic data. The Philly Fed Index showed a stronger-than-expected rise in factory activity in the mid-At lantic region, abating the risk-off mood somewhat after the biggest sell-off in US stock markets in eight months on Wednesday. However, investors remain cautious due to uncertainties surrounding US President Trump and his capacity to push through with promised tax cuts and infrastructure spending, bringing 10Y US Treasury yields down to 2.23%, their lowest level since April. Former FBI Director James Comey's testimony to the Senate next week will be watched closely by the market for any new clues on Trump's involvement in the federal investigation , after he denied any wrongdoing yesterday.

In the ECB minutes from the April meeting released yesterday, policymakers indicated a cautious approach to changes in policy communication to prevent undue market upheaval. This confirms our view that the ECB will take only very small and gradual steps in moving in a more hawkish direction and we still believe it is less likely the ECB will change its forward guidance at the June meeting (see more here ECB research: Hawkish wording but changed forward guidance less likely, 10 May). However, this should not exclude that the ECB will argue that the options for providing additional accommodation have become less likely.

Presenting the Conservat ives' manifesto yesterday ahead of the elect ion on 8 June, Theresa May pledged voters to press on with her approach to Brexit , cut immigrat ion and introduce corporate reform. Our main scenario remains that the Conservatives will consolidate their majority after the election, reducing the risk of a 'no deal Brexit '.

Reports alleging that the Brazilian President Michel Temer gave his blessing to an attempt to pay to silence a potential witness in the country's biggest-ever graft probe brought back investor concerns about a possible government collapse and added to market jitters across the Americas, causing Brazilian stocks and the real to fall sharply.

FTSE Eyes Higher Open As Sterling Tumbles

- Trump anxiety remains but investors not too concerned yet;

- FTSE seen higher as sterling loses ground over night following “mini crash”;

- Light data session ahead, with focus on Canadian numbers and oil rig release.

European equity markets are expected to open higher on Friday, buoyed by gains in the US overnight where indices staged a moderate recovery following some heavy selling the day before.

Investors are clearly still a little anxious about the political situation in the US, which showed to an extent on Wednesday, but as it stands I don’t think they’re too concerned. Wednesday’s sell-off may have shocked a few people but US indices remain in the same range they’ve traded in for the last few months and as long as that remains the case, it would suggest that investors are not too concerned.

The FTSE looks to be leading the gains in Europe ahead of the open on Friday, boosted no doubt by sterling’s performance since yesterday’s European close. The pound showed its vulnerability once again on Thursday – albeit on a much smaller scale than seen previously – as it fell around one cent against the US dollar in a very short space of time. Given the timing of the plunge, it would seem the liquidity of the market as opposed to any particular catalyst was largely responsible for the mini “flash crash”.

The pound has now settled around 1.2950 against the dollar and 0.8575 against the euro, having failed to hold onto its gains earlier in the day which came on the back of a much better than expected retail sales report. Particularly against the dollar, the pound was already looking a little unstable around 1.30 and yesterday’s mini crash has done little to convince me otherwise. We’ve seen a lot of consolidation in the pair overnight, I wonder whether we’ll see one more burst before the week is out.

The final trading session of the week is looking a little light on the events and data side of things. We have a few pieces of low tier data being released this morning which should have little impact, while the only notable releases this afternoon come from Canada, with retail sales and inflation data due out. We’ll also get the latest oil rig number from the US, as Brent and WTI continue to stage a recovery on the expectation that an extension to the output cut will be agreed. The first cut was less successful than participating countries expected, largely due to the sudden increase in US output, as shale producers looked to capitalise on higher prices. The number of oil rigs has more than doubled since last summer and it will be interesting to see whether the industry can continue to chip away at the efforts of the other producers to bring the market back into balance.

Aussie Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.27% against the USD and closed at 0.7413.

LME Copper prices declined 1.5% or $85.0/MT to $5490.0/MT. Aluminium prices declined 1.2% or $23.0/MT to $1905.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7421, with the AUD trading 0.11% higher against the USD from yesterday's close.

The pair is expected to find support at 0.7394, and a fall through could take it to the next support level of 0.7367. The pair is expected to find its first resistance at 0.7457, and a rise through could take it to the next resistance level of 0.7493.

Moving ahead, traders will look forward to Australia's Westpac leading index, the sole important release next week.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.