Sample Category Title

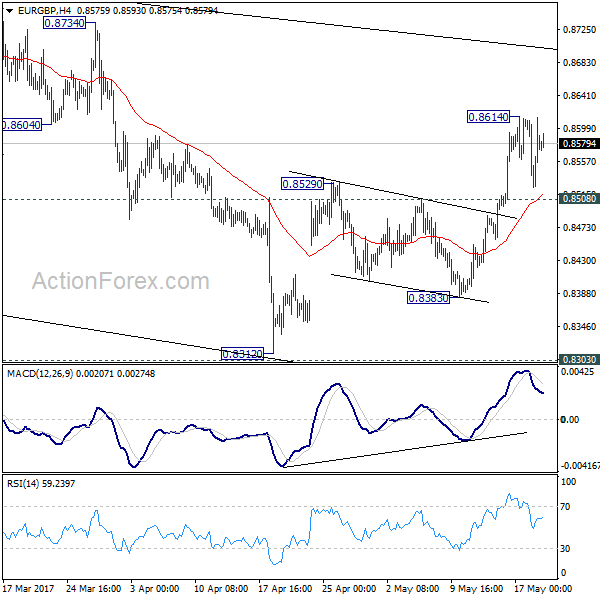

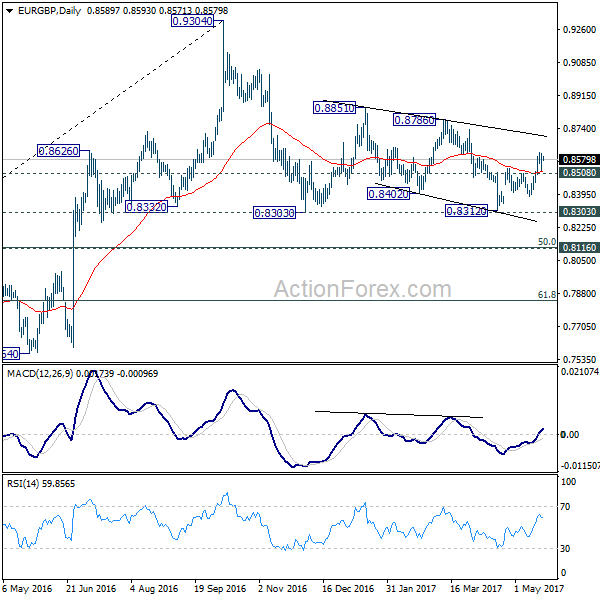

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8531; (P) 0.8571; (R1) 0.8619; More...

A temporary top is in place at 0.8614 and intraday bias is turned neutral first. Another rise is expected as long as 0.8508 resistance turned support holds. Above 0.8614 will target 0.8786 resistance next. Overall, price actions 0.9304 are viewed as a medium term corrective pattern that is extending. As EUR/GBP has just defended 0.8303 resistance. Break of 0.8786 could bring a retest on 0.9304 high. On the downside, below 0.8508 minor support will turn bias back to the downside for 0.8383 support instead.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

Trade Idea: EUR/JPY – Stand aside

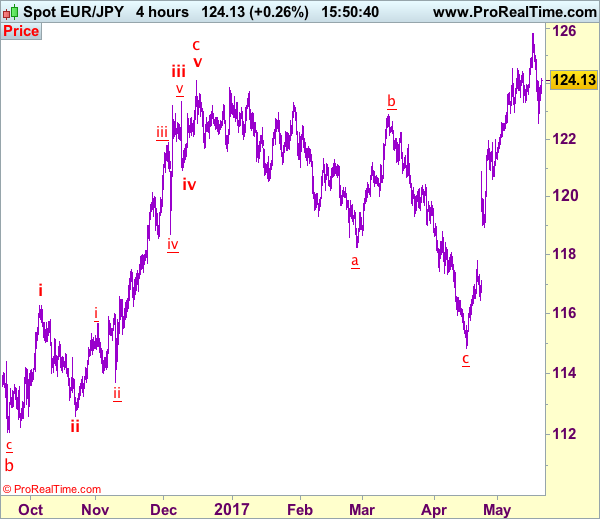

EUR/JPY - 124.16

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the sharp retreat from 125.82 to 122.56 (yesterday’s low) suggests a temporary top has possibly been formed there, as euro found support there and has rebounded, suggesting consolidation with initial upside bias would be seen and recovery to 124.40-50 cannot be ruled out, however, still reckon upside would be limited to 125.00 and price should falter below 125.40-50, bring another corrective fall later.

On the downside, below 123.35-40 would bring weakness to 122.90-00 but said support at 122.56 should hold on first testing. Only break there would add credence to our view that top has been formed, bring retracement of recent upmove to 122.00-10 and then 121.50-60 but downside should be limited to 121.20-30, bring rebound later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Buy at 0.7370

AUD/USD – 0.7437

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Buy at 0.7370, Target: 0.7520, Stop: 0.7320

Position: -

Target: -

Stop: -

New strategy :

Buy at 0.7370, Target: 0.7520, Stop: 0.7320

Position: -

Target: -

Stop:-

Although aussie has retreated after rising to 0.7467, if our view that low has been formed at 0.7329 is correct, downside should be limited to 0.7400 and renewed buying interest should emerge around 0.7370 and bring another rise later, above said resistance at 0.7467 would extend the rebound from 0.7329 to 0.7500-10 but break there is needed to add credence to this view, bring subsequent rise towards resistance at 0.7556 which is likely to hold from here due to near term overbought condition.

In view of this, we are looking to buy aussie on dips as 0.7360-70 should limit downside. A break of said support at 0.7329 would abort and signal recent decline is still in progress for weakness to 0.7295-00 (76.4% retracement of 0.7158-0.7750), however, loss of downward momentum should prevent sharp fall below 0.7300 and reckon 0.7245-50 would remain intact, bring another rebound later.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

Technical Outlook: Cable – Technicals Suggest Renewed Attempts Above 1.3000

Cable returned to back to the range after strong rally on Thursday probed above psychological 1.3000 barrier peaked at 1.3046 (the highest since Oct 2016). The pair was unable to sustain break above 1.3000 on first attempt and fell back after rally was capped by descending weekly cloud which offers significant resistance. However, overall bias remains with bulls and fresh attempts above 1.3000 could be expected while pivotal supports at 1.2924/07 (10SMA / 20 SMA respectively) stay intact and continue to underpin the action. Penetration into weekly cloud would support bulls for fresh extension higher and expose next objective at 1.3143 (Fibo 38.2% of 1.5015/1.1986 descend). Conversely, increased pressure could be expected on loss of 10/20SMA's that would expose lower triggers at 1.2843/30.

Res: 1.3000, 1.3046, 1.3100, 1.3143

Sup: 1.2944, 1.2924, 1.2907, 1.2889

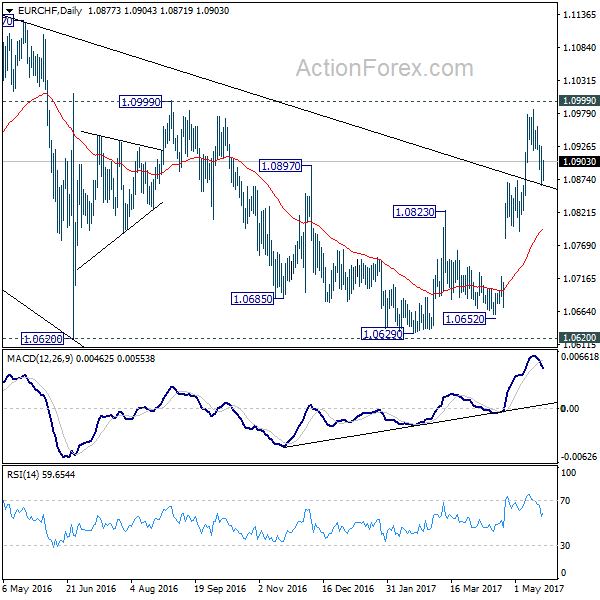

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0853; (P) 1.0890; (R1) 1.0915; More...

Despite breaching 1.0872 resistance turned support, EUR/CHF quickly recovered. Intraday bias in the cross remains neutral first. Price actions from 1.0986 is a corrective move and downside should be contained by 1.0791/0872 support zone to bring rise resumption. We're holding on to the bullish view that corrective pattern from 1.1198 has completed already after defending 1.0653 fibonacci level. Firm break of 1.0999 resistance will pave the way for a retest on 1.1198 high.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

Technical Outlook: EURUSD – Bullish Outlook Above Weekly Cloud Top

The Euro returned back above 1.1100 handle in early Friday after strong rally of past few days paused on Thursday for consolidation under fresh six-month high at 1.1171. Dips were contained just above critical support at 1.1065, provided by weekly cloud top, with weekly close above here to signal further advance in coming days and focus next objective at 1.1313 (Fibo 76.4% of 1.1614/1.0339 descend. The pair is on track for strong bullish weekly close that supports bullish stance. Technical studies are bullish but caution on overbought slow stochastic which may generate bearish signal on reversal. Break below weekly cloud top would risk easing towards next strong supports at 1.1044 (Fibo 38.2% of 1.0838/1.1171), 1.1020 (former top of 08 May) and psychological 1.1000 support.

Res: 1.1140, 1.1171, 1.1203, 1.1250

Sup: 1.1095, 1.1065, 1.1044, 1.1020

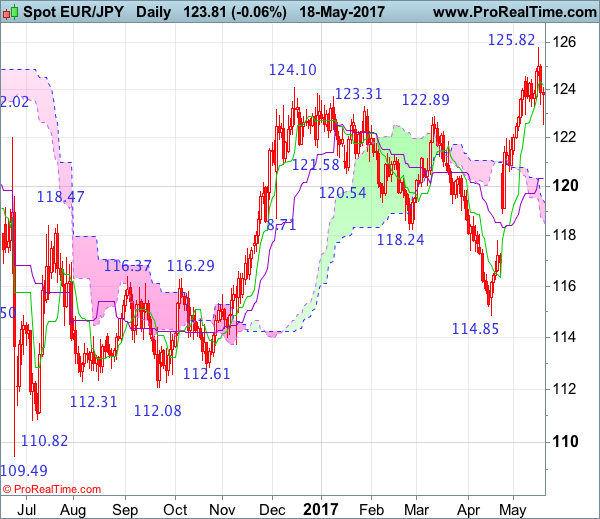

EUR/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Hammer

• Time of formation: 19 Sep 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Doji

• Time of formation: 28 Mar 2017

• Trend bias: Near term up

EUR/JPY – 124.16

Although the single currency extended recent upmove to as high as 125.82 earlier this week, lack of follow through buying and the subsequent retreat suggest consolidation below this level would be seen with initial downside bias for correction to 123.00, then 122.55-60, however, reckon 121.60-65 (38.2% Fibonacci retracement of 114.85-125.82) would limit downside and bring another rise later, above 125.05-10 would bring retest of 125.82 but break there is needed to signal recent upmove has once again resumed and extend subsequent gain to 126.50-60.

On the downside, whilst initial pullback to 122.90-00 and then 122.55-60 cannot be ruled out, reckon downside would be limited to 121.60-65 (38.2% Fibonacci retracement of 114.85-125.82) and bring another upmove later to aforesaid upside targets. Below indicated previous support at 120.60 would abort and signal a temporary top has been formed, bring retracement of recent entire rise to 120.30-35 (50% Fibonacci retracement) and then 120.00 but reckon downside would be limited to 119.40-50 and price should stay above indicated support at 118.92, bring rebound later.

Recommendation: Buy at 121.60 for 124.60 with stop below 120.60.

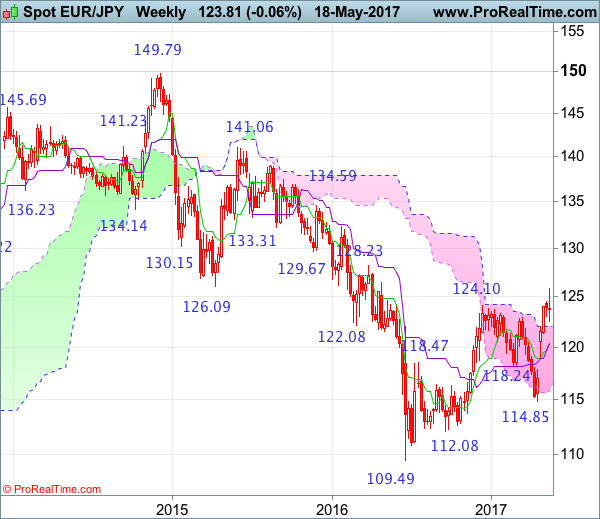

On the weekly chart, as the single currency has retreated after rising to 125.82, suggesting minor consolidation below this level would be seen and pullback to 123.00, then 122.00 cannot be ruled out, however, reckon 121.60-65 (38.2% Fibonacci retracement of 114.85-125.82) would limit downside and bring another rise later, above 125.00 would bring retest of said resistance at 125.82 but break there is needed to confirm the erratic rise from 109.49 has resumed for retracement of medium term downtrend to 125.25-30 (50% Fibonacci retracement of 141.06-109.49) but reckon upside would be limited to 126.00 and 126.45-50 would hold from here.

On the downside, although initial pullback to 122.90-00 and possibly test of the upper Kumo (now at 122.04) cannot be ruled out, reckon downside would be limited to 121.50-60 and bring another rise. Only below support at 120.60 would defer and risk weakness to the Kijun-Sen (now at 120.34) and then 120.00 which is likely to hold on first testing. Looking ahead, euro needs to penetrate indicated support at118.92 to shift risk to the downside for further fall to 118.00, however, downside should be limited to previous resistance at 117.82 and bring rebound later. A weekly close below 117.82 would suggest first leg of rebound from 114.85 has ended, bring weakness to 117.00 but price should stay above 116.20-25, bring another rebound later.

US Dollar Rebounds As Investor Nerves Cool

The US dollar managed to stem the strong declines after developments from Washington saw a special counsel being set up to oversee the investigations into the alleged Trump administration links with Russia.

The US Dollar Index which was seen trading at support managed to rebound with confidence. Technical resistance is seen at 99.23 which should help the greenback to recover some of the gains.

On the economic front, the weekly jobless claims fell to 233k, better than the forecasts of 240k while the Philly Fed manufacturing index rose to 38.8 in May, beating estimates of 18.5 and rising from April's 22.

In the UK, retail sales figures surprised, rising 2.3% on the month.

Looking ahead, Statistics Canada will be releasing the monthly inflation and retail sales figures today. Headline inflation rate is expected to rise 0.5% on a month over month basis in April, while core retail sales are expected to rise 0.2%, reversing the 0.1% decline posted in February.

EURUSD intraday analysis

EURUSD (1.1111): EURUSD formed a strong bearish outside bar yesterday after price touched a new 6-month high at 1.1171. Price action is likely to move into consolidation, but further downside cannot be ruled out. For the moment, support at 1.1100 is seen to offer some support pushing prices higher.

A break down below 1.1075 which marks the lows from Wednesday is required for price action to continue lower. Initial support is seen at 1.1000. To the upside, in the event of a rebound in prices, further gains can be seen coming only on the move above the previous highs at 1.1170.

GBPUSD intraday analysis

GBPUSD (1.2954): The British pound has retreated just after breaking past 1.3000 level and similar to the EURUSD, the GBPUSD has also closed with an outside bar.

This suggests a potential continuation if price breaks out above 1.3000 while to the downside, a close below Wednesday's lows 1.2905 will trigger a move towards the support level at 1.2800. The longer-term target at 1.2600 remains in place however which could be realized in the event that price can continue to break down lower.

XAUUSD intraday analysis

XAUUSD (1248.24): The bullish retracement in gold prices sent the precious metal briefly above $1250 handle without price testing the $1221 support. The price action in gold hints at a possible downside move in prices.

Currently, gold prices are seen retesting the 1250 handle where resistance could be seen forming. A bearish decline from here will validate the resistance and put gold prices on track to test the lower support level at 1221.47, from where we expect to see a renewed bullish momentum potentially push gold prices back above the $1250 handle.

British Retail Sales Post Surprise Jump Of 2.3% In April

'Today's data doesn't change the underlying story, where the squeeze in household incomes is starting to weigh on consumer activity.' - James Smith, ING Bank NV

UK retail sales rebounded markedly last month despite the post-Brexit sharp fall in the value of the Pound. The Office for National Statistics reported on Thursday that retail sales surged 2.3% in April, following the preceding month's upwardly revised fall of 1.4% and topping expectations for a 1.2% increase. The unexpected climb suggested that consumer spending also rebounded in April and would support economic growth in the second quarter. Last month's gain was mainly driven by the good weather that boosted demand for hardware and household goods. In volume terms, sales advanced 4.0% on an annual basis in April, compared to the prior month's increase of 2.0%. Meanwhile, market analysts expected sales volumes to rise 2.1% in the reported month. After the release, the Sterling rose above $1.30 for the first time since September 2016 and hit $1.3028 for a short time. Excluding automobiles, sales rose 2% on a monthly basis in April. Despite April's stronger than expected performance, retail sales are set to drop again in the upcoming months due to surging inflation.

Initial Jobless Claims Drop For Third Consecutive Week, Philly Fed Jumps To 38.8 Points

'The details were ... consistent with the recent pickup in manufacturing output in the industrial production report being sustained.' - Jim O'Sullivan, High Frequency Economics

The number of Americans filing for unemployment benefits dropped unexpectedly last month, official figures revealed on Thursday. The US Department of Labour reported that initial jobless claims fell to 232K in the week ending May 12, following the preceding week's 236K and posting the third consecutive decline. In the meantime, analysts held expectations for an increase to 240K. Claims remained below the 300K level for 115 straight weeks, the longest stretch since 1973. The number of continuous claims fell 22K to 1.90M during the week ended May 5, the lowest since November 1988. Back in April, US private companies created 211K jobs, roughly meeting analysts' expectations. Other data released on Thursday showed that manufacturing activity in Philadelphia jumped to 38.8 points in May, up from the preceding month's 22.0, whereas analysts anticipated a slight decrease to 19.9. More than half of market participants expect the Federal Reserve to raise rates next month. However, uncertainties tied to the US President Donald Trump and Russia may lower significantly the chances of a June rate hike.