Sample Category Title

GBP/USD Analysis: Puts Consolidation Trend At Risk

'Due to the level of expectation in the market for a big CPI number, the bigger risk is a disappointing number that could weigh on the Pound. Key support levels to watch include 1.2900 for GBP/USD and 0.8500 for EUR/GBP.' – City Index (based on PoundSterlingLive)

Pair's Outlook

Monday ended with the Sterling once again being unable to post solid gains against the US Dollar, thus, prolonging its consolidation trend for another day. Nevertheless, the Cable has the opportunity to reach the trend's resistance line at 1.30 today and possibly even break it. Although technical indicators are in favour of the positive outcome, it still remains somewhat unlikely, as the Pound is eventually expected to test the wedge's lower boundary near 1.28. Assuming the pair consolidates until next week, a good confirmation of both trend support's would be achieved around 1.2850—where they coincide.

Traders' Sentiment

Market sentiment reached a perfect equilibrium today, while pending orders are close to that as well, with 51% of them set to sell the British currency.

Gold Analysis: Finds New Support

'The U.S. dollar was also hurt by weak data on New York state area manufacturing.' – Rodrigo Campos, Reuters

Pair's Outlook

Although on Tuesday morning the yellow metal's price was lower than the scored heights during Monday's trading session, the bullion continued to score gains. Moreover, on the hourly chart a new development was giving a positive signal for the commodity price. The 100-day SMA had begun to provide support rather than resistance to the commodity. It is most likely that the bullion will reach for the next resistance level, as the weekly R1 is located at the 1,239.37 level. However, the developments of the price search afterwards is unclear for now.

Traders' Sentiment

Traders are bullish in regard to the bullion, as 52% of open positions are long. In addition, 61% of trader set up orders are to buy.

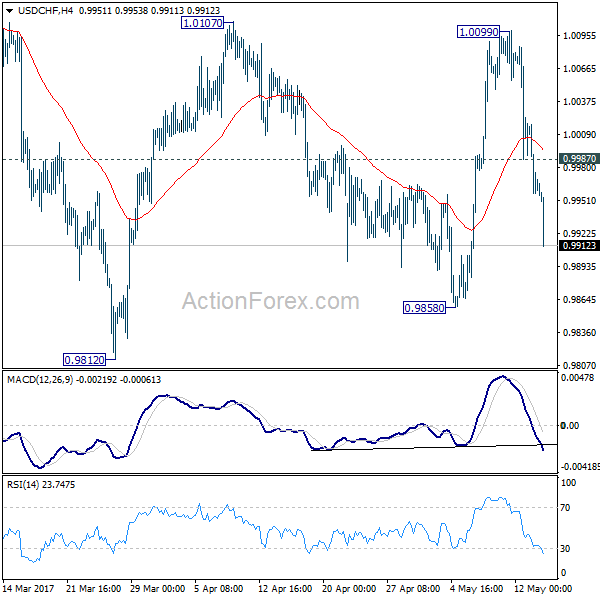

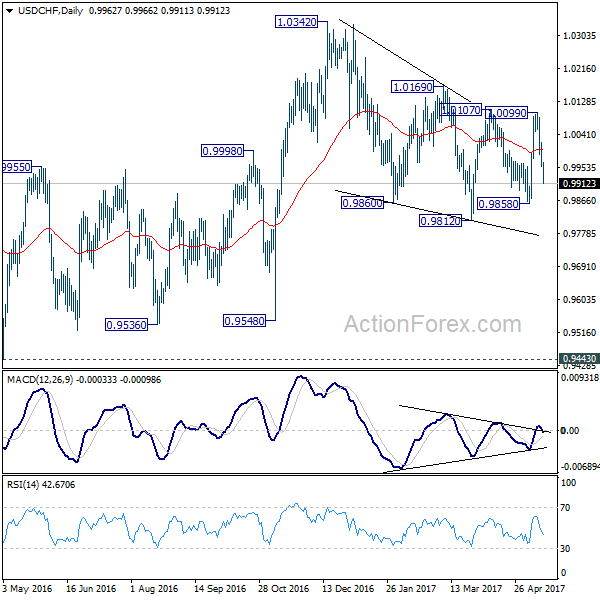

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9942; (P) 0.9980; (R1) 1.0003; More.....

Intraday bias in USD/CHF remains on the downside as fall from 1.0099 accelerates to as low as 0.9914 so far. Break of 0.9858 support will extend the corrective fall from 1.0342 through 0.9812 low. On the upside, above 0.9987 minor resistance will turn intraday bias neutral first.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, instead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

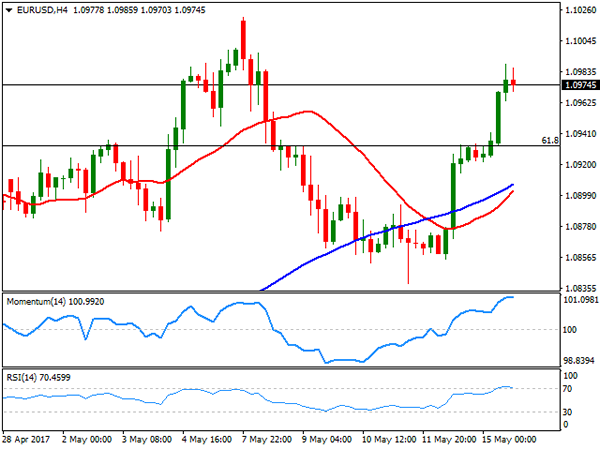

EUR/USD

The EUR/USD pair traded as high as 1.0989 this Monday, as the greenback remained on the back foot after worse-than-expected data released last Friday, further undermined early US session by a downside surprise in the NY Empire State manufacturing index, which showed that business activity in the region fell sharply according to the survey, down to -0.1 from previous 7.0. Dollar's decline paused after the release of the US NAHB house market index, as builders' confidence strengthened, with the index up to 70 in May from previous 68, but overall, the American currency remained weak, as the market is having second thoughts about a June Fed's hike. A sharp recovery in oil prices, after Russia and Saudi Arabia said they favor extending the oil output cut until March 2018, also weighed on the greenback. The European macroeconomic calendar will be quite busy this Tuesday, with the German ZEW survey, and the EU Trade Balance and Q1 preliminary GDP, this last expected at 0.5%, matching the last quarter of 2016.

The pair eased down to the 1.0970 region, where it spent most of the US afternoon, consolidating gains. From a technical point of view, the pair retains its bullish stance, with scope to extend its advance beyond the yearly high set earlier this month at 1.1020. Technical indicators in the 4 hours, have eased within overbought readings, but are far from changing course, whist the 20 and 100 SMA advanced below the current level, both now in the 1.0900 region. Stops have likely increased above 1.1020, last week's peak, with and advance beyond it probably resulting in an upward acceleration towards 1.1060.

Support levels: 1.930 1.0890 1.0850

Resistance levels: 1.0990 1.1020 1.1060

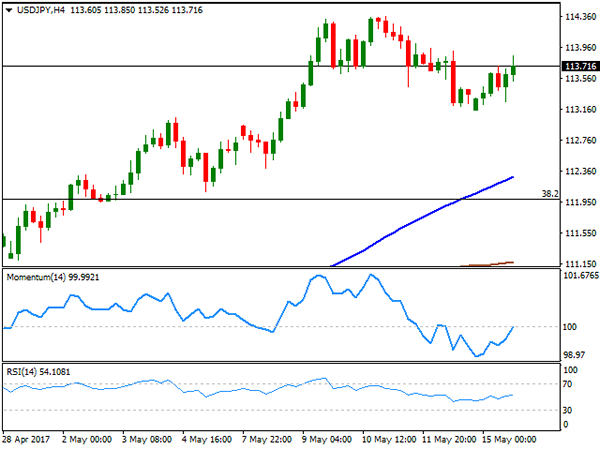

USD/JPY

The USD/JPY pair closed the day with modest gains around 113.70, recovering some ground late in the US afternoon on a modest up-tick in US Treasury yields. After starting the day with a weak tone, the greenback pared losses and managed to regain some ground against most of its major rivals, ending in positive territory, however, only against the Japanese yen. Limiting the safe-haven currency's gains were advances in most major indexes around the world. Japan will release its April Tertiary Industry Index during the upcoming Asian session, expected at 0.1% from previous 0.2%. In the meantime, and from a technical point of view, the downward pressure has eased on the pair, as the price bounced once again from the 113.20 region. Furthermore, the 4 hours chart shows that the price holds well above a bullish 100 SMA, now around 112.30, whilst technical indicators turned north, and are currently crossing their mid-lines into positive territory. Still, the pair needs to recover above 114.00 to be able to extend its gains beyond the monthly high and up to 114.50, a major Fibonacci resistance.

Support levels: 113.20 112.75 112.40

Resistance levels: 114.00 114.50 114.85

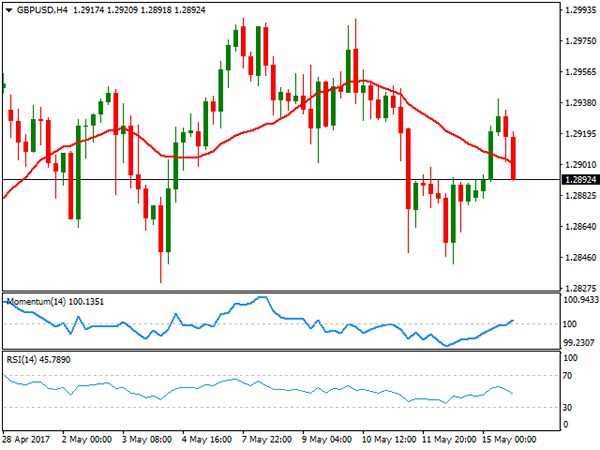

GBP/USD

The GBP/USD pair advanced up to 1.2940 at the beginning of the day, but trimmed all of its gains and settled at 1.2880 region, pretty much unchanged from Friday's close. There were no macroeconomic releases in the UK, with the pair led by dollar's self weakness/strength. PM Theresa May spoke to voters through a live Facebook Q&A, but added nothing new to the Brexit case, focusing more on campaigning towards the upcoming June election. On Tuesday, the UK will release multiple inflation figures for April, which if higher-than-expected, could result in a stronger Pound, as market players will rush to price in a soon-to-come rate hike in the kingdom. Short term, the pair is now at risk of extending its slide, given that in the 4 hours chart, the price was unable to sustain gains above a bearish 20 SMA, now back below it, whilst the Momentum indicator holds flat around its 100 level and the RSI indicator turned south, now around 44. The pair needs to advance beyond 1.2960 to turn bullish, while below 1.2830 the risk turns towards these last weeks' range in the 1.2760/70 region.

Support levels: 1.2830 1.2800 1.2765

Resistance levels: 1.2920 1.2960 1.2995

GOLD

Gold prices advanced this Monday beyond last week's highs, with spot peaking at $1,237.26 a troy ounce, but trimmed most of its daily gains to end the day barely higher at 1,231.00. Broad dollar's weakness was behind the early decline, but slipped on low physical demand and a bounce in the American currency. The daily chart shows that the price settled around a bearish 200 DMA after failing around the 100 DMA, whilst the 20 DMA maintains a strong bearish slope well above this last. In the same chart, technical indicators have lost upward strength and turned flat within bearish territory, suggesting the latest recovery was unsustainable and that the risk remains towards the downside. In the 4 hours chart, the 20 SMA heads higher below the current level, providing support at 1,226.60, while technical indicators turned lower within positive territory, not enough to confirm additional declines, but also limiting chances of a steeper recovery.

Support levels: 1.226.60 1,214.25 1,203.80

Resistance levels: 1,237.25 1,245.20 1,251.30

WTI CRUDE OIL

West Texas Intermediate crude oil futures closed the day at $48.79, its highest settlement for this May, boosted by comments from Saudi Arabia and Russia oil ministers, saying that they could extend their output cut deal until March 2018. The positive mood among oil traders, however, may quickly turn sour, if US data continue indicating rising production in the world's largest economy. From a technical point of view, the daily chart shows that the price advanced well above a still bearish 20 DMA, while technical indicators head north, albeit holding within their mid-lines. In the shorter term, and according to the 4 hours chart, the upward looks a bit more constructive, given that the Momentum indicator has bounced from its mid-line, while the RSI indicator also turned modestly higher after correcting overbought conditions, although both stand below previous highs. In the same chart, the 20 SMA is crossing above the 100 SMA, both around 48.00, providing now a strong support in the case of a downward move.

Support levels: 48.00 47.30 46.60

Resistance levels: 49.60 50.10 50.70

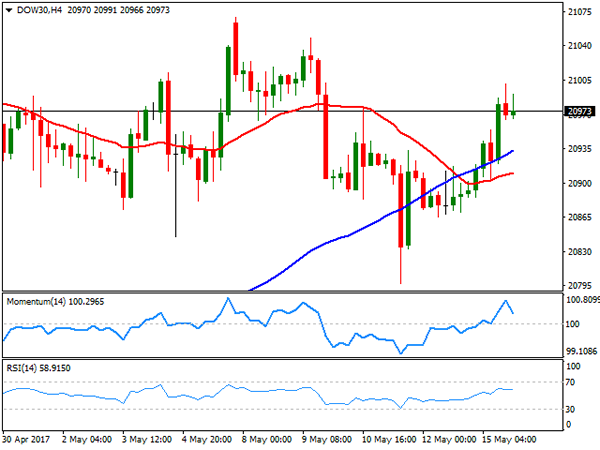

DJIA

US indexes closed in the green, with the Dow Jones Industrial Average adding 85 points to end at 20,981.94, fueled by an advance in retail and energy-related equities. The Nasdaq Composite added 28 points, to 6,149.67, while the S&P added 0.48% and closed at 2,402.32, both hitting fresh intraday records. Equities shrugged off a negative manufacturing report released at the beginning of the day, taking the lead from an almost 3% advance in oil prices, on renewed hopes worldwide producers will keep on battling against the market's glut, and strong gains in cybersecurity companies. Within the Dow, Johnson & Johnson was the best performer by adding 2.72%, followed by Cisco Systems that advanced 2.33%. Verizon Communications led losers by shedding 1.03%, followed by Nike that closed 0.79% lower. The DJIA maintains a neutral stance in its daily chart, still hovering around a modestly bullish 20 SMA, and with technical indicators turning higher around their mid-lines. Shorter term, and according to the 4 hours chart, the index is also biased higher, holding well above its moving averages, although technical indicators lost their upward momentum within positive territory, indicating that an advance beyond 21,000 the daily high, is required to confirm further gains.

Support levels: 20,865 20,822 20,797

Resistance levels: 20,900 20,941 20,977

FTSE100

The FTSE 100 advanced 19 points to settle at a new record high of 7,454.37, bolstered by commodity-related equities and persistent weakness in the British Pound. Anglo American led gainers, adding 3.22%, followed by Glencore which added 3.16%. BHP Billiton closed 2.28% as oil prices rallied. TUI was the worst performer, shedding 4.79%, followed by Next that lost 1.86%. The benchmark advanced further in after-hours trading, supported by a strong advance in Wall Street and currently at 7,464. From a technical point of view, the daily chart shows that the RSI indicator heads north around 67, while the Momentum indicator diverges from the index, having retreated from overbought territory. In the same chart, the 20 and 100 SMAs converge heading north around 7,270. Shorter term, the 4 hours chart shows that the index keeps posting higher highs and higher lows, holding far above a sharply bullish 20 SMA, whilst the RSI indicator heads north around 82 as the Momentum losses upward strength between positive territory, somehow warning of a possible bearish corrective move for the upcoming sessions.

Support levels: 7,447 7,398 7,365

Resistance levels: 7,465 7,500 7,545

DAX

European major indexes closed with gains this Monday, with the German DAX peaking to a new record high of 12,839 intraday and settling at 12,807.04, up 36 points or 0.29% on the back of gains in the financial and utilities sectors, and a recovery in commodities prices. RWE AG was the best performer within the German benchmark, adding 3.84%, followed by Commerzbank that gained 3.04%. Fresenius Medical Care led decliners, shedding 1.10%, followed by Merck that closed 1.07% lower. Heading into the Asian opening a few points above the mentioned close, the daily chart shows that the index advanced further above strongly bullish moving averages, as the RSI heads marginally higher around 71, but the Momentum indicator turned sharply lower within positive territory, diverging lower and favoring a downward corrective move for the upcoming session. In the 4 hours chart, intraday declines met buying interest around a bullish 20 SMA, this last now at 12,755, while technical indicators lack directional strength, but hold within positive territory.

Support levels: 12,801 12,755 12,718

Resistance levels: 12,839 12,870 12,920

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.32; (P) 113.58; (R1) 114.06; More...

Intraday bias in USD/JPY remains neutral as consolidation from 114.36 extends. Deeper fall cannot be ruled out but in that case, downside should be contained by 112.08 cluster support (38.2% retracement of 108.12 to 114.36 at 111.97) and bring rally resumption. We're holding on to the view that corrective fall from 118.65 is completed with three wave down to 108.12. Above 114.36 will target 115.49 resistance first. Break there should resume whole rise from 98.97 to 125.85 high.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

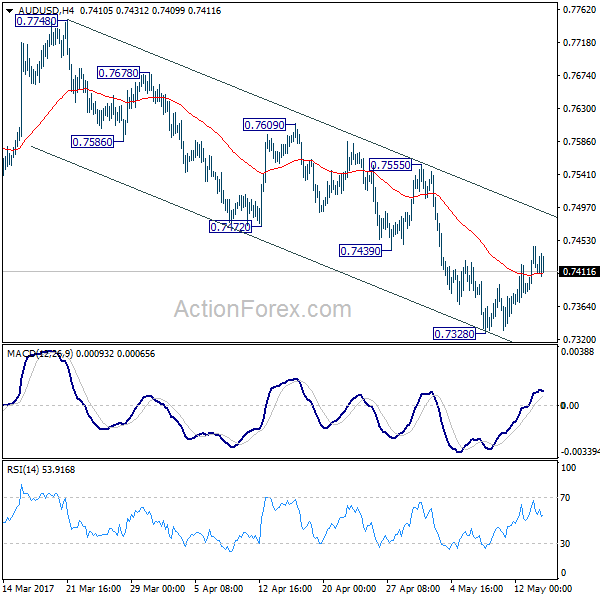

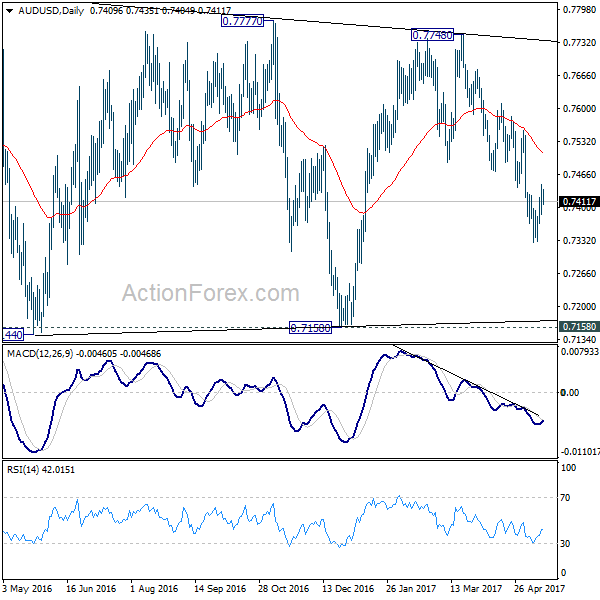

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7382; (P) 0.7414; (R1) 0.7445; More...

AUD/USD's corrective recovery from 0.7328 is still in progress and intraday bias stays neutral. As noted before, we'd expect upside to be limited below 0.7555 resistance to bring fall resumption. Below 0.7382 will target 0.7144/7158 support zone. However, there is no clear sign of larger down trend resumption yet. Hence we'll be cautious on strong support from 0.7144/58 to contain downside and bring rebound. On the upside, firm break of 0.7555 will argue that fall from 0.7748 is completed and turn bias back to the upside.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

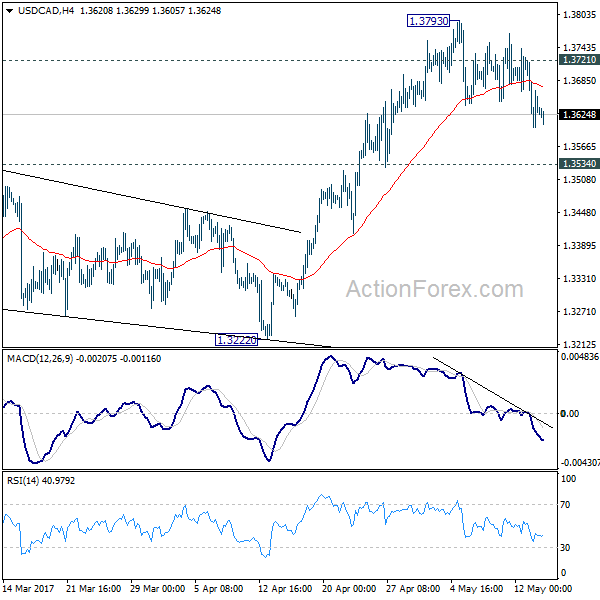

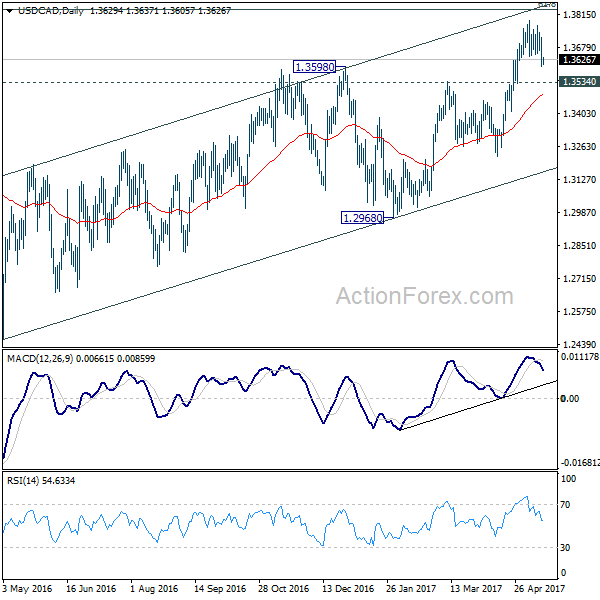

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3582; (P) 1.3652; (R1) 1.3702; More....

Intraday bias in USD/CAD remains cautiously on the downside for 1.3534 resistance turned support Break there should confirm completion of the rise from 1.2968 and target 1.3222 support next. On the upside, above 1.3721 will turn bias back to the upside and target 1.3793 and above. However, as noted before, choppy rise from 1.2460 is seen as a corrective move. In case of an extension, upside should be limited by 1.3838 fibonacci level to bring reversal.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and would end at around 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

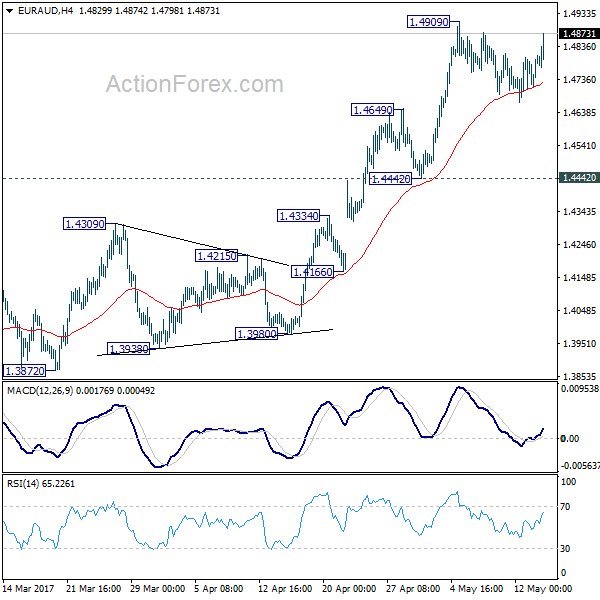

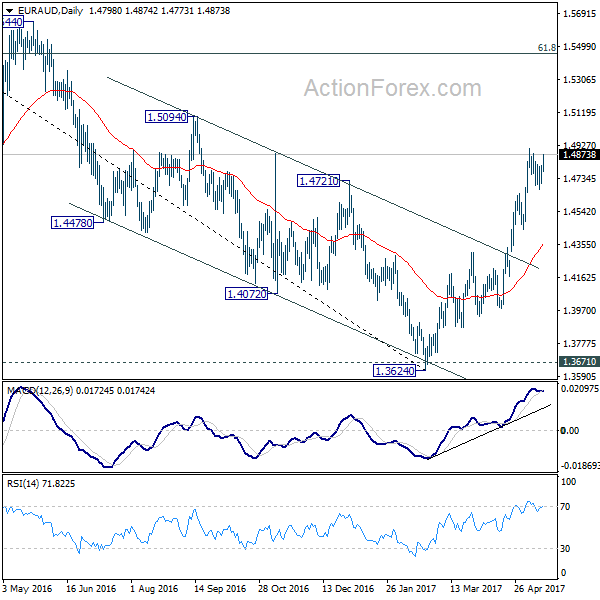

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4741; (P) 1.4775; (R1) 1.4836; More...

EUR/AUD rebounds strongly after drawing support from 5 hour 55 EMA. But as it's staying below 1.4909 temporary top, intraday bias remains neutral first. Overall outlook is unchanged as whole correction from 1.6587 has completed at 1.3624 already after defending 1.3671 key support level. Rise from 1.3624 is expected to continue. Hence, in case of another fall, downside should be contained by 1.4442/4649 support zone to bring rise resumption. Above 1.4909 will extend recent rally from 1.3624 to next medium term fibonacci level at 1.5455.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455 and above. In any case, outlook will now stay cautiously bullish as long as 1.4309 resistance turned support holds.

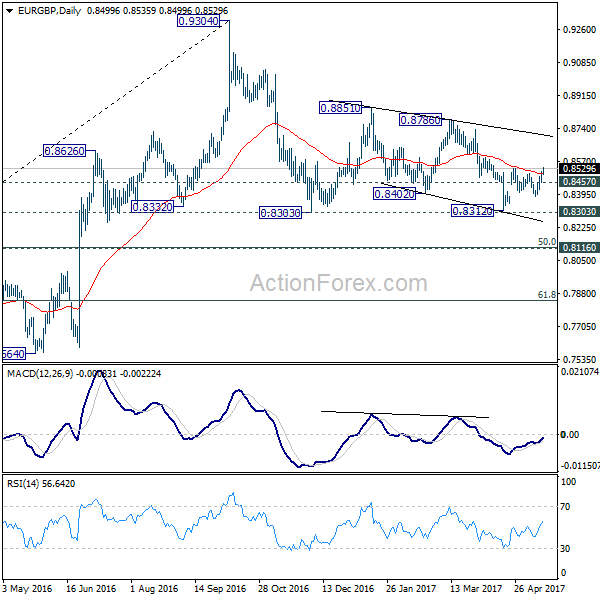

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8473; (P) 0.8494; (R1) 0.8530; More...

EUR/GBP's break of 0.8529 resistance confirms resumption of rebound from 0.8312. Intraday bias is back on the upside. Current rise would now target 0.8786 resistance next. On the downside, below 0.8457 minor support will dampen the bullish case and turn focus back to 0.8383 support instead. Overall, price actions 0.9304 are viewed as a medium term corrective pattern that is extending. As EUR/GBP has just defended 0.8303 resistance. Break of 0.8786 could bring a retest on 0.9304 high.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

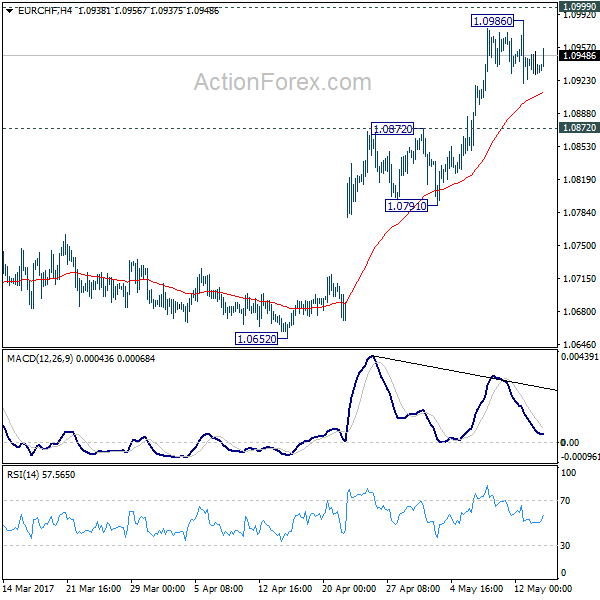

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0924; (P) 1.0938; (R1) 1.0951; More...

EUR/CHF is staying in consolidation below 1.0986 short term top and intraday bias remains neutral. More consolidative trading would be seen with risk of another dip. But downside should be contained by 1.0791/0872 support zone to bring rise resumption. Outlook is unchanged that corrective pattern from 1.1198 has completed already after defending 1.0653 fibonacci level. Firm break of 1.0999 resistance will pave the way for a retest on 1.1198 high.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.