Sample Category Title

EURUSD: Bullish, Rallies Further

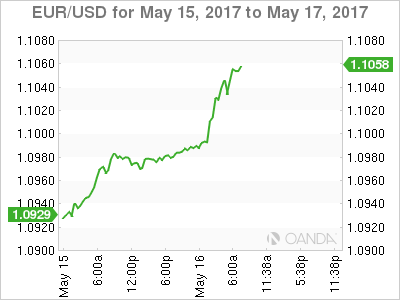

EURUSD: With the pair retaining its short term uptrend by rallying further on Tuesday, more strength is envisaged in the days ahead. Resistance comes in at 1.1100 level with a cut through here opening the door for more upside towards the 1.1150 level. Further up, resistance lies at the 1.1200 level where a break will expose the 1.1250 level. Its daily RSI is bullish and pointing higher suggesting more strength. Conversely, support lies at the 1.1000 level where a violation will aim at the 1.0950 level. A break of here will aim at the 1.0900 level. All in all, EURUSD faces further bull pressure.

Euro Zone Q1 GDP Data Backs ECB View of Recovery Broadening; UK CPI Remains above BOE Target

Notes/Observations

- European Q1 GDP data falls in-line with ECB view that recovery is being more broad-based

- UK Apr CPI beats expectations (Y/Y: 2.7% v 2.6%) and remains above BOE target for the 3rd straight month

Overnight:

Asia:

- Reserve Bank of Australia (RBA) May 2nd Meeting Minutes:Maintaining the current accommodative stance of monetary policy would be consistent with achieving sustainable growth and the inflation target over time. Q1 inflation data had generally increased confidence that underlying inflation would pick up to around 2% by early 2018.

- Bank of Japan (BOJ) Gov Kuroda reiterates its view that was not exiting at this stage but quite sure exiting from its easy monetary policy could be managed quite well; BoJ had tools to manage exit from stimulus. Reiterated view that Japan inflation rate was still quite low and that current YCC policy was appropriate. Reiterated view that would take more stimulus steps if needed

- China Banking Regulator (CBRC) to tighten disclosure rules on lenders' wealth management products to track risky lending practices in shadow banking sector and launch approx. 4 dozen new rules

Europe:

- France President Macron 1st full day in office noted that he planned to carry out reforms in the next few months. France-German relationship needed to be more pragmatic and wanted to set up roadmap with Germany to reform the Euro zone. Treaty changes would not longer be taboo as France was ready for EU treaty change if necessary

- Germany's Merkel met the French President. Noted that France and Germany want to develop roadmap to deepen EU integration and make the region more resilient to crises. Was possible to change EU treaties but first needed to decide on what reforms were needed

- UK Labour party said to plans to introduce taxes on companies that pay staff more than £330K/ year if it wins general election

Americas:

- President Trump reportedly revealed highly classified intelligence information to Russian Foreign Min Lavrov last week that intelligence agency partners had not given permission to share

- White House official Powell denied President Trump gave classified information to Russian diplomats, as reported in Washington Post. National Security Advisor McMaster added that at no

- time were any intelligence sources or methods discussed and no military operation were disclosed that were not already known publically

- Mar Total Net Tic Flows -$0.7B v $13.2B prior; Long-term TIC Flows $59.8B v $53.1B prior; both Japan and China increased their Treasury holdings

Energy:

- EIA forecasted June total shale regions oil production at 5.40M bpd, +122K bbd m/m (vs +109K bpd rise in May)

Economic Data

- (NO) Norway Q2 Consumer Confidence: 11.1 v 7.3 prior

- (EU) Apr EU27 New Car Registrations: -6.6% v +11.2% prior (1st negative reading in 41 months)

- (NO) Norway Q1 GDP Q/Q: 0.2% v 0.2%e; GDP Mainland Q/Q: 0.6% v 0.5%e

- (RO) Romania Q1 Advance GDP Q/Q: 1.7% v 1.0%e; Y/Y: 5.7% v 4.4%e

- (FR) France Apr Final CPI M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

- (FR) France Apr Final CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e, CPI (Ex-Tobacco) Index: 101.23e

- (CZ) Czech Q1 Advance GDP Q/Q: 1.3% v 0.7%e; Y/Y: 2.9% v 2.3%e

- (HU) Hungary Q1 Preliminary GDP Q/Q: 1.3% v 1.2%e; Y/Y: 4.1% v 3.2%e

- (NL) Netherlands Q1 Preliminary GDP Q/Q: 0.4% v 0.5%e; Y/Y: 3.4% v 2.8%e

- (IT) Italy Q1 Preliminary GDP Q/Q: 0.2% v 0.2%e; Y/Y: 0.8% v 0.8%e

- (PL) Poland Q1 Preliminary GDP Q/Q: 1.0% v 0.8%e; Y/Y: 4.0% v 3.9%e

- (UK) Apr CPI M/M: 0.5% v 0.4%e; Y/Y: 2.7% v 2.6%e; CPI Core Y/Y: 2.4% v 2.3%e

- (UK) Apr RPI M/M: 0.5% v 0.4%e; Y/Y: 3.5% v 3.4%e; RPI Ex Mortgage Interest Payments (RPIX) Y/Y: 3.8% v 3.7%e

- (UK) Apr PPI Input M/M: 0.1% v 0.0%e; Y/Y: 16.6% v 17.0%e

- (UK) Apr PPI Output M/M: 0.4% v 0.2%e; Y/Y: 3.6% v 3.4%e

- (UK) Apr PPI Output Core M/M: 0.5% v 0.2%e; Y/Y: 2.8% v 2.5%e

- (DE) Germany May ZEW Current Situation Survey: 83.9 v 82.0e; Expectation Survey: 20.6 v 22.0e

- (EU) Euro Zone May ZEW Expectations Survey: 35.1 v 26.3 prior

- (EU) Euro Zone Mar Trade Balance (Seasonally Adj): €23.1B v €18.7Be; Trade Balance NSA (unadj): €30.9B v €25.8Be

- (EU) Euro Zone Q1 Preliminary GDP (2nd reading) Q/Q: 0.5% v 0.5%e; Y/Y: 1.7% v 1.7%e

Fixed Income Issuance:

- (FR) France Debt Agency (AFT) opened its book to sell new May 2048 Oat; Guidance seen mid-teens bps to French Treasuries

- (SI) Slovenia Debt Agency opened its book to sell EUR-denominated 2027 and 2040 bonds

- (ID) Indonesia sold total IDR6.02T in 2-year,4-year,7-year and 15-year Project-based Sukuk (PBS)

- (ES) Spain Debt Agency (Tesoro) sold total €1.605B vs. €1.0-2.0B indicated range in 3-month and 9-month Bills (Apr 18th 2017)

- (UK) DMO opened its books to sell 1.75% July 2057 Gilt; guidance seen +2.5-2.75bps to UK Treasuries

- (ZA) South Africa sold total ZAR2.35B vs. ZAR2.35B indicated in 2026, 2036 and 2048 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.1% at 3268, FTSE +0.4% at 7486, DAX -0.1% at 12799, CAC-40 -0.4% at 5394, IBEX-35 +0.1% at 10972, FTSE MIB +0.1% at 21714, SMI -0.2% at 9094, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes

European Indices trade mixed this morning, with out performance in the FTSE100 led by Vodafone up ~4% following their Full year results, EasyJet on the other hand one of the leading decliners after missing estimates. Earlier the DAX hit a new record high before pulling back, after record highs for US indices yesterday. Telecoms are outperforming with Car makers and Healthcare stocks declining.

Looking ahead to the US morning notable earnings on the calendar include Home Depot, Staples, Dick's Sporting Goods and TJX.

Equities

- Consumer discretionary: [EasyJet [EZJ.UK] -6.6% (Earnings), DCC [DCC.IL] -3.1% (Earnings), SpeedyHire [SDY.UK] +3% (Earnings)]

- Consumer Staples: [ITE Grp [ITE.UK] -4.3% (Earnings)]

- Financials: [Crest Nicholson [CRST.UK] -1.9% (Earnings)]

- Technology: [Sonova [SOON.CH} +0.8% (Earnings)]

- Telecom: [Vodafone [VOD.UK] +4.0% (Earnings)]

- Healthcare: [AB Science [AB.FR] -29% (Announces that ANSM requested the temporary suspension of clinical studies conducted in France following deviations from Good Clinical Practice (GCP) standards), BTG [BTG.UK] -9.0% (Earnings)]

Speakers

- Italy PM Gentiloni commented from Beijing that China President Xi had expressed confidence in the future of EU -

- German ZEW Economists noted that the latest figure suggested on GDP confirm German economy is in good shape with prospects gradually improving; exports continue to strengthen. Euro Zone prospects were also better

- Sweden Central Bank (Riksbank) publishes Opinion on Inflation Target Variable; Proposes CPIF from CPI. changes are expected to be able to be implemented at the monetary policy meeting in September 2017. Proposal will would not entail any change to policy being conducted

- European Court of Justice (ECJ): Free trade agreement with Singapore needed the approval of national parliaments before it can become legal (**Insight: case widely seen as setting a precedent for the UK and pave the way for the trade negotiations as he country prepares to leave the bloc)

- IEA Monthly Report noted that if saw a sharp stockpile draw if production cuts were extended. Trimmed 2017 global oil demand growth from 1.32M bpd to 1.30M bpd. Raised 2017 Non-Opec oil supply growth forecast from 485K bpd to 600K bpd. Opec production was higher from 31.68M to 31.78M, +65K bpd; compliance of 96% v 99% m/m

- Russia Energy Min Novak: Looking to extend timeframe for production cuts; keep continues in place

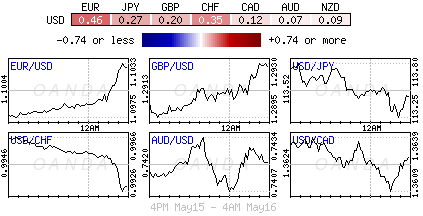

Currencies

- USD still hampered by a spat if weaker-than-expected economic data that any upward expectations that Fed 2017

- EUR/USD hit fresh 7-month highs in the session at 1.1050. Dealers cited continued optimism following the election of Macron. German Chancellor Merkel noted that she was open to changing the EU's treaties to strengthen the bloc, voicing a desire to work closely with France. Both leaders agreed to "develop and renew" their bilateral relationship and that their cabinet ministers would meet shortly after the French parliamentary election in June

- GBP/USD was firmer as UK inflation data remain hot. Apr CPI YoY reading topped estimates and remained above the BOE target for the 3rd straight month. GBP/USD tested above 1.2950 area afterwards but still unable to fiund the momentum to tackle the 1.30 handle. The pair failed at several attempts last week to bust above the key resistance. GBP saw its gains erode just ahead of the NY morning with GBP/USD back below the 1.29 level.

Fixed Income

- Bund futures trade at 160.36 down 18 ticks, continuing to come off Friday's high of 160.99. Initial resistance comes from the 161.01 level, while medium –term resistance lies near the April 27th high of 162.01 level followed by 163.68.

A break of 160.01 support level could see lows target 159.01 followed by 157.50. - Gilt futures trade at 127.55 lower by 6 ticks, but off the lows of 127.45 after UK inflation came in hotter than expected. Last week's rally saw a pause from the continuation of the pullback from the 129.14 April 18th high. Price still finds key support at the 126.41 support level. An acceleration lower could test the 125.80 region. Resistance remains the 128.51 level then 129.14 followed by 132.80.

- Tuesday's liquidity report showed Monday's excess liquidity rose to €1.6536T a rise of €9.6B from €1.6440T prior. Use of the marginal lending facility climbed to €227M from €248M prior.

- Corporate issuance saw over $13.5B come to market via 11 issues headlines by Intl Flavors & Fragrances $2.0B in a 2-part senior unsecured notes & bond offering and Wells Fargo $3.0B in a 2-part senior notes and non-call 10-year offering

Looking Ahead

- (IT) Italy PM Gentiloni meets Russia President Putin

- (CO) Colombia Apr Consumer Confidence Index: No est v -21.1 prior

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

- 05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

- 06:00 (IE) Ireland Mar Trade Balance: No est v €4.7Be

- 06:00 (IL) Israel Q1 Advance GDP Annualized: 3.7%e v 6.3% prior

- 06:00 (TR) Turkey to sell 2019 and 2022 bonds

- 06:30 (SE) Sweden Central Bank (Riksbank) Gov Ingves speech

- 07:00 (BR) Brazil May FGV Inflation IGP-10 M/M: -1.0%e v -0.8% prior

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (IS) Iceland Apr Unemployment Rate: No est v 2.4% prior

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr Housing Starts: 1.26Me v 1.22M prior; Building Permits: 1.27Me v 1.267M prior (revised from 1.260M)

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves:

- 09:00 (NZ) Fonterra Global Dairy Trade Auction

- 09:00 (RU) Russia announces weekly OFZ bond auction

- 09:15 (US) Apr Industrial Production M/M: 0.4%e v 0.5% prior; Capacity Utilization: 76.3%e v 76.1% prior, Manufacturing Production: +0.4%e v -0.4% prior

- 10:00 (US) Q1 MBA Mortgage Foreclosures: No est v 1.53% prior; Mortgage Delinquencies: No est v 4.8% prior

- 10:30 (CA) Canada to sell 3-month, 6-month and 12-month Bills

- 11:00 (BR) Brazil to sell 2022, 2026 2035 and 2055 I/L Bonds - 08/15/2022

- 11:30 (US) Treasury to sell 4-Week Bills

- 11:30 (AT) ECB's Nowotny (Austria) speaks in Vienna

- 16:30 (US) Weekly API Oil Inventories

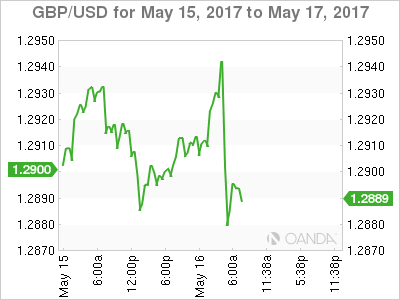

Sterling Dips Despite Inflation Hitting Near Four Year High

- GBP spikes after inflation data before quickly spiralling lower;

- Good reason to look beyond today's inflation numbers;

- EURUSD hits six month high and further gains could lie ahead.

Equity markets in Europe are trading a little mixed on Tuesday, offering little direction for US futures ahead of the open on Wall Street, while commodities are broadly in the green as oil looks to extend its winning run to five straight session. There's been some interesting moves in currency markets this morning, with sterling being particularly volatile on the back of some interesting inflation data.

This morning's UK CPI data caused quite a stir for the pound, with the spike in headline and core inflation in April initially sending the currency higher before almost immediately spiralling lower. As always, there's a number of things to consider here, which would explain such a strong reaction. The above expectation spike in inflation is typically bullish for the currency, especially when the rate is already above the central bank's target. Add to this the sheer size of the jump and the BoEs acknowledgement last week that "some MPC members would need relatively little upside news on growth or inflation to consider voting for tighter policy" and the initial spike will perhaps seem justified.

That said, there are other things to consider here, not least the fact that Easter this year fell in April rather than March, therefore the year on year comparison is naturally skewed to the upside. The 18.6% increase in air fares which largely contributed to the rise in transport prices is a clear indication of this. The other thing to consider here is that the BoE will likely have been aware of the spike in April when it released its new forecasts and made its decision last week, so from a monetary policy perspective, little has probably changed. Finally, with the pound already struggling around 1.30 against the dollar, the sell-off that followed to levels well below where it was prior to the release is an indication of an exhausted rally that's possibly crying out for a correction. Given the size of the moves we've seen over the last month, this could easily be what we're seeing, having failed repeatedly at the recent highs.

The euro on the other hand has had a much more positive start to the day, breaking and holding above 1.10 against the dollar to trade at its highest level in six months. The ZEW economic sentiment figures were broadly supportive for the euro – despite the pause that initially followed it – with economic sentiment in Germany rising, albeit less than expected, while the eurozone as a whole rose to a near two year high. This morning's break could be significant for the pair, with 1.1125-1.1150 being the next big test for the pair.

Reserve Bank of Australia (RBA) Minutes Hold No Surprises

- Reserve Bank of Australia (RBA) minutes hold no surprises

- German ZEW report is key for Euro today

- UK Inflation and Retail data awaited for GBP

Overnight, the Reserve Bank of Australia published the minutes from their last board meeting and there were few surprises. It was in line with their statement. The housing and labour markets are in focus, economic activity is expected to pick up and inflation is slowly rising. No news there, then, and the Aussie Dollar was largely unruffled.

This morning brings UK Inflation data and we are expecting a small uptick. This would be in line with the Bank of England's (BoE) thinking, as shown in the minutes from their last meeting. However, their central target is 2.0% and we are expecting something between 2.5 and 2.7%. No need to panic, in other words, but it may turn up the volume on calls for the BoE to bring forward their next interest rate hike.

From the Eurozone, we will get confirmation of the final Q1 economic growth rate. A quarterly rise of 0.5% is almost inked into the books, so any variation on that would be influential. For now, the Euro is strengthening. We have seen it gain ground against the Pound and USD amongst others. If this morning's German ZEW Index is as positive as many predict, further EUR strength is a given.

This afternoon brings US construction data in the form of the building permits count. That is considered a bellwether for the US construction sector confidence and the forecasts are positive. We also get US industrial production. That is likely to show a small decline on last month's very positive 0.5% growth. So, on balance, if all this data is as expected, the effect on the USD likely to be muted.

And many 'news' reporters are covering a story about a new trend amongst clubbers. Young women are apparently going out for the night wearing nothing but strategically placed duct tape. My mother always warned me about women like that and I probably don't go to the same sorts of clubs as them. I doubt they are into plane spotting and fly fishing but I was left wondering about the pain of getting ready for bed at the end of the night. Removing an Elastoplast is bad enough but a whole covering of duct tape…..ouch.

Winner

Interviewer: "Congratulations on winning the £120 million Euromillions lottery."

Farmer: "Thank you."

Interviewer: "Do you have any special plans for spending all of that money?"

Farmer: "Not really. I'm just gonna keep farming until the money runs out."

Technical Outlook: Spot Gold May Extend Recovery Towards $1245 On Clear Break Above $1233 Pivot

Spot Gold is holding positive tone and probing again above cracked $1233 barrier (Fibo 23.6% of $1295/$1214 downleg), following Monday’s recovery stall at $1237 and subsequent pullback.

The price may extend recovery on sustained break above $1233 pivot towards key near-term barriers at $1245 (daily cloud top / Fibo 38.2% retracement, reinforced by 55SMA), $1247 (200SMA) and $1248 (20SMA).

Bounce from $1214 low is seen as correction and should be ideally capped under these barriers, before broader bears retake control.

Alternative scenario sees break above $1245/48 pivots as strong bullish signal for fresh recovery that may extend towards $1250/54 targets.

Res: 1237, 1245, 1247, 1248

Sup: 1230, 1226, 1216, 1214

Elliott Wave View: NZD/JPY Sequence Forecasts The Rally

In this technical blog we’re going to take a quick look at the past Elliott Wave charts of NZD JPY published in members area of www.elliottwave-forecast.com. We’re going to take a look at the structures, count the swings and explain the trading setup.

The chart below is NZD JPY 4 hour update from 05.04.2017. As our members know, we were pointing out that NZDJPY is having incomplete bullish swings sequnces from the 75.62 low. Structure has been calling for more strength in 7th swing toward 78.40-78.94 ( taking profit area). Once the pair reaches proposed area in 7 swings, we expect to see 3 wave pull back to correct the cycle from the lows.

NZD JPY 1 Hour Chart 05.04.2017

The pair is bullish against the 76.112 low. Wave (x) pull back is expected to make another short term low ideally to reach 77.22-76.90 ( buying area). As we got incomplete bullish sequences in 4 hour chart, we advised our members to avoid selling the pair and keep buying dips in 3,7,11 swings. Invalidation level for the trade comes at 76.90 and we’re targeting 78.40-78.94 area.

NZD JPY 1 Hour Chart 05.09.2017

Eventually the pair has reached proposed target, giving us nice profits. As of right now, the pair has scope to extend little bit higher still toward 79.03-79.32 area before find sellers for for a 3 wave pull back at least.

Trumps Political Gaff Has EUR Soaring

The 'mighty' dollar has taken it on the chin in the overnight session, weakening for a fifth consecutive day, allowing the EUR to soar to its highest point in six-months on a hearsay report that U.S President Donald Trump revealed classified information to a Russian diplomat last week.

The time and effort that it taking for his administration to put out fires has investors questioning the President's ability to deliver on his economic agenda.

Elsewhere, the surge in oil prices is boosting commodity currencies (CAD, MXN and NOK) even as concern grows over the strength of the global economy. Stocks are mixed.

In the U.S, today's industrial production print (08:30 am EST) will provide useful insight into how the factory sector is performing.

1. Global stocks mixed results

Stocks opened the week upbeat on higher commodity and oil prices, with the S&P touching a new all-time high, before closing lower.

However, investors are growing increasingly wary as valuations look stretched and with the latest rally taking place in thinner volumes and led by just a few sectors.

In Japan, the Nikkei share average edged up +0.25%, drawing support from a sagging yen (¥113.61), while the broader Topix rallied +0.3%, paring an earlier gain of +0.7%.

In Hong Kong, China shares retreated -0.3% after surging +1.6% yesterday amid optimism over Beijing's infrastructure spending program.

In China, the Shanghai Composite Index increased +0.7%, erasing an earlier loss, while the Shenzhen Composite surged +2.1%, the most in nine-months, while India's Sensex rallied +0.5% to a new record.

In Europe, indices are trading mixed. The DAX hit a record high before pulling back, supported by Telecoms, while healthcare and automakers decline. On the FTSE 100, air transport and commodity prices are providing the early support.

U.S equities are set to open in the red (-0.1%).

Indices: Stoxx50 -0.1% at 3268, FTSE +0.4% at 7486, DAX -0.1% at 12799, CAC-40 -0.4% at 5394, IBEX-35 +0.1% at 10972, FTSE MIB +0.1% at 21714, SMI -0.2% at 9094, S&P 500 Futures -0.1%.

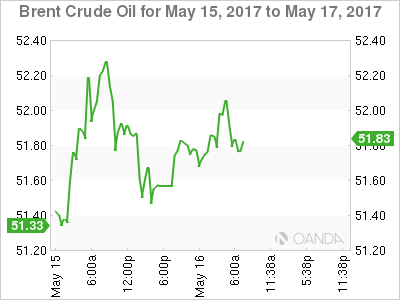

2. Oil rises on expectations output cuts, gold shines

Oil prices have extended yesterday's gains this morning after top producers – the Saudi's, Russia and Kuwait – supported prolonging supply cuts until the end of March 2018 in a bid to drain a global glut.

Brent crude oil is up +30c at +$52.12 a barrel, while U.S light crude (WTI) is +25c higher at +$49.10 a barrel.

Note: Both benchmarks have rallied more than +$5 a barrel since hitting five-month lows last week.

Global inventories remain high, and the output from other producers, especially the U.S is rising, which is keeping prices below the psychological +$60 some OPEC members would like to see.

OPEC and non-OPEC countries meet to decide policy on May 25 in Vienna.

Data last Friday showed that U.S energy firms added oil rig's for a 17th consecutive week, extending a 12-month drilling recovery.

Note: Today, the IEA comes out with estimates of April OPEC production.

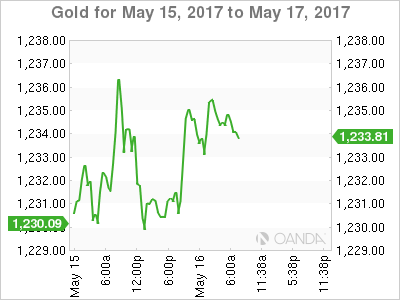

Gold prices (+0.4% at +$1,234.81 per ounce) are rallying for a fourth consecutive day as the dollar slides on signs of slower economic activity in the U.S which is denting dealers expectations of an aggressive string of interest rate hikes by Fed.

The Fed remains on track to hike rates next month; however, the odds have fallen to +70% from +83% on waning U.S inflation outlook.

3. Yields on the move, but beware

If and how the Trump administration delivers on its promise to boost the country's growth rate may influence the pace by which the Fed drains easy money from the financial system.

If growth advances due to productivity gains, policy makers could keep interest rates “lower for longer,” but, if growth rises because it boosts demand without 'higher employment or higher productivity,' U.S policy makers could feel pressure to raise interest rates to prevent stronger inflation.

Nevertheless, last Friday's disappointing U.S data (Retail Sales and CPI) has fixed income dealers trimming the odds for a Fed hike next month. Fed fund futures currently see a +70% chance of a hike, down from +83% pre data release.

The yield on 10-year Treasury notes have backed +1 bps to +2.34%, after dropping -6 bps Friday when the weaker-than-expected CPI report buoyed bond prices.

Elsewhere, yields on Aussie 10's lost -5 bps to +2.59%. Benchmark yields in France and Germany rose +1 bps.

4. 'Big' Dollar sees red

The mighty greenback is under pressure from a number of sources – geo-political, economic and rate differential odds.

Ahead of the U.S open, Europe's single unit hit a fresh seven-month high (€1.1050) on continued optimism following the election of new French President Macron.

Germany's Chancellor Merkel is open to changing the E.U's treaties to strengthen the region, voicing a desire to “develop and renew” their bilateral relationship. The EUR continues to face strong resistance around the €1.1060-70 area, however, through here the techies sees it open to €1.1125-50 area.

The pound was firmer, trading atop of £1.2932, as U.K inflation (see below) data topped estimates and remained above the BoE's target for the third straight month.

But, unable to find the momentum to tackle the psychological £1.30 handle, has since reversed to test back below the £1.29 level. Fixed income dealers are pricing in a BoE unlikely to raise interest rates in 2017 or 2018. With the Fed on track to hike rates next month and the worries of tough Brexit negotiations with the E.U, sterling bears have their sights on a sub £1.28 in the short-term.

5. U.K Inflation, Euro GDP and trade data

In the U.K, April data this morning indicates that consumer prices rose at the fastest pace in over three-years (y/y +2.7% vs. March +2.3%).

This may suggest that the U.K is facing a living-standards squeeze as the country heads into a general election (June 8) and begins its exit from the EU.

Compared with March, prices rose +0.5%, slightly above market expectations.

In the eurozone, exporters enjoyed a record March, with sales of goods to buyers outside the currency area at an 18-year high. Despite imports also up on the year, the trade surplus widened to €30.9B.

Other data also showed that preliminary Eurozone GDP rose by +0.5% q/q, and +1.7% y/y for Q1.

UK Inflation Accelerates In April, Sterling Sinks

Sterling tumbled lower on Tuesday following reports of UK consumer prices jumping to 2.7% in April, the highest level since September 2013. It is becoming quite clear that the Brexit-fuelled currency weakness has elevated inflation to uneasy levels with consumers likely to feel the pinch if wage growth fails to keep up. Despite the rising prices, expectations of an interest rate increase in the short term remain subdued with uncertainty over Brexit and BoE doves playing a key part. The Bank of England may receive further headaches in the future with the combination of rising inflation and slowing economic growth weighing heavily on sentiment.

Sterling/Dollar is under pressure on the daily charts as bulls are struggling to keep above 1.2900. An intraday breakdown below 1.2850 should encourage a further depreciation lower towards 1.27750.

Dollar bulls missing in action

The Greenback entered the trading week under renewed selling pressure as the amalgamation of political tensions in the US and soft economic data impeded investor attraction towards the currency. Sentiment towards the Greenback took another hit on Monday after sellers exploited the surprisingly soft US manufacturing report to enforce further downside pressures. With the Dollar descending to its lowest level at 98.50 since Donald Trump’s presidential victory in November, the Trump rally could be on its last leg. While heightened expectations remain over the Federal Reserve raising US interest rates in June, the ongoing uncertainty revolving around Trump may ensure Dollar bulls remain missing in action. From a technical standpoint, the Greenback is bearish on the daily charts with weakness below 98.50 opening a path towards 98.00.

EURUSD breaks above 1.1000

A recent relief of political risk in Europe has rekindled appetite for the Euro with prices lurching to a fresh six-month high at 1.1040 as of writing. With Emmanuel Macron’s victory in the French Presidential election dealing a symbolic blow to populism and quelling fears of “Frexit”, investors have redirected their attention back towards the macro-economics in Europe. The overall data from Europe in recent months has displayed a touch of resilience and it will be interesting to see how the improving macro-fundamentals and Macron’s victory impact the ECB meeting in June. Euro bulls seem to be back in town with a vulnerable Dollar fuelling the upside rally.

From a technical standpoint, the breakout above 1.1000 has turned the EURUSD bullish on the daily charts. A daily close above 1.1000 should encourage a further appreciation towards 1.1120

Commodity spotlight – Gold

A vulnerable Dollar supported Gold on Tuesday with the metal finding comfort around $1235 as of writing. Although US interest rate hike expectations are likely to dictate where Gold trades to in the medium to longer term, uncertainty, and geological tensions should support the metal in the short term. Persistent Dollar weakness should encourage short term bulls to send prices above $1235. A breakout above $1235 may provide permission for buyers to send prices higher towards $1245.

GOLD Medium-Term Bullish, SILVER Monitoring Fibonacci Retracement At 16.92, CRUDE OIL Strong Upside Pressures.

GOLD Medium-term bullish.

Gold seems on its way back up. Hourly support is now located at 1195 (10/03/2017 low). Expected to show further upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Monitoring Fibonacci retracement at 16.92.

Silver is bouncing back. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high).

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Strong upside pressures.

Crude oil continues to bounce on shortsqueeze move. Support is given at a distance 43.76 (05/05/2017 low). Demand is very strong and crude oil is set to be monitor again the $50 mark.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

DAX Flat As German Economic Sentiment Misses Estimate

The DAX index is showing limited movement in the Tuesday session. Currently, the DAX is trading at 12,794.00. On the economic front, Eurozone Flash GDP climbed 0.5%, matching the forecast. German ZEW Economic Sentiment disappointed, as the reading of 20.6 fell short of the forecast of 22.3 points, There was better news from Eurozone ZEW Economic Sentiment, which jumped to 35.1, easily beating the forecast of 29.1 points. On Wednesday, the eurozone releases Final CPI, which is expected to rise to 1.9%.

The DAX remains close to record highs, buoyed by a solid reading from growth data for the eurozone. Market predictions for Eurozone growth were on target, as Flash GDP came in at 0.6% in the first quarter of 2017. This figure was slightly higher than Preliminary GDP back in April, which showed a gain of 0.5%. The eurozone continues to show improved numbers in 2017, boosted in no small part by the German economy, which also expanded 0.6% in the first quarter. However, the well-respected ZEW Economic Sentiment surveys, which gauge optimism among investors and analysts, were a mixed bag for May. The German indicator improved to 20.6, short of expectations. What was more surprising was the unexpected jump from the Eurozone indicator, which improved to 35.1, its strongest level in almost two years. With the eurozone showing stronger growth, has inflation kept up? We’ll get an indication on Wednesday, with the release of Eurozone Final CPI, which is expected to rise to 1.9%. Stronger inflation levels will increase pressure on the ECB to consider tapering its ultra-loose monetary policy. Germany, for one, is finding that ultra-low interest rates is hampering growth, and wants Brussels to adopt a tighter monetary policy.

A rise in oil prices has boosted stock markets, and on Monday, brent crude climbed close to 2 percent. This surge boosted the DAX, which briefly touched a high of 12,833.00, a new record. The first quarter of 2017 has seen improved numbers in the euro area, largely due to strong numbers from Germany, the largest economy in the eurozone. Germany’s economy expanded 0.6% in the first quarter, compared to a 0.4% gain in Q4 of 2016. What was particularly encouraging was that the expansion was broadly based, with strong consumer and state spending, and an upsurge in the construction and manufacturing and export sectors.

Trumps Political Gaff Has EUR Soaring

President Trump and his aides continues to be preoccupied with damage control, as the White House and Congress remain focused on Comeygate, as the fallout from Trump’s dismissal of FBI director James Comey continues. There was more bad news for President Trump on Tuesday, with a report in the Washington Post that Trump had shared confidential intelligence reports with Russia’s foreign minister at a meeting last week. The White House has denied the report, but the timing is particularly bad for Trump, who is already under investigation for possible Russian involvement in the presidential campaign. The markets are concerned that Trump will be so busy trying to put out political firestorms, that his agenda of increased fiscal spending and tax reform will stall. These jitters could hurt investor confidence and send global stock markets lower.