Sample Category Title

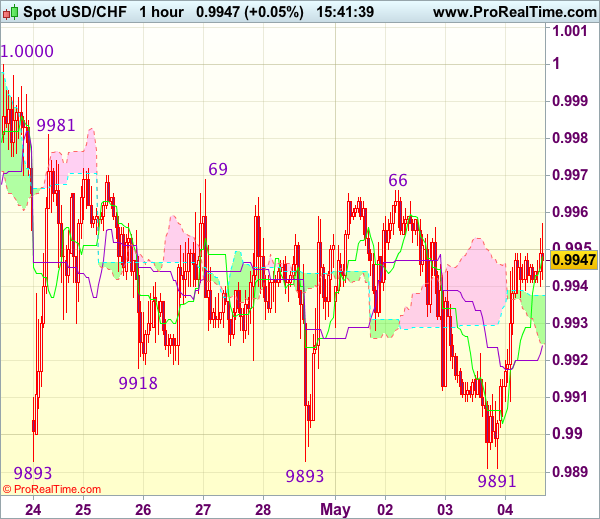

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9929

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9942

Kijun-Sen level : 0.9924

Ichimoku cloud top : 0.9938

Ichimoku cloud bottom : 0.9925

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s brief fall to 0.9891, lack of follow through selling on break of previous support at 0.9893 and the subsequent rebound has retained our view that further consolidation is in store and test of 0.9966-69 resistance cannot be ruled out, however, a break of 0.9981 is needed to signal low is formed, bring a stronger rebound to 1.0000-08 resistance, above there would confirm a temporary low has been formed at 0.9891, bring retracement of recent decline to 1.0020-30 (61.8% Fibonacci retracement of 1.0108-0.9891) but price should falter well below resistance at 1.0067.

On the downside, below 0.9905-10 would bring retest of 0.9891 but break there is needed to confirm recent decline from 1.0108 top has resumed and extend weakness to 0.9865-70 (2 times extension of 1.0108-1.0008 measuring from 1.0067), however, support at 0.9831 would hold from here, bring rebound later. As near term outlook is still mixed, would be prudent to stand aside for now.

Trade Idea : GBP/USD – Buy at 1.2790

GBP/USD - 1.2877

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2860

Kijun-Sen level : 1.2885

Ichimoku cloud top : 1.2911

Ichimoku cloud bottom : 1.2906

Original strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2790, Target: 1.2910, Stop: 1.2755

Position : -

Target : -

Stop : -

Although cable has rebounded after intra-day brief fall to 1.2831, reckon upside would be limited to 1.2910-15 and near term downside risk remains for the corrective fall from 1.2965 to bring retracement of recent upmove, below said support at 1.2831 would extend weakness to 1.2790-95 (38.2% Fibonacci retracement of 1.2515-1.2965) where renewed buying interest should emerge, bring another rise later. Above 1.2948 would bring retest of 1.2965, break there would confirm upmove has resumed for headway towards 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on further subsequent pullback as downside should be limited to 1.2790-95. A drop below previous support at 1.2757 would abort and signal top is formed instead, bring correction to 1.2740 (50% Fibonacci retracement of 1.2515-1.2965) first.

Technical Outlook: EURUSD – No Significant Changes After Fed, Focus Turns On US NFP And French Election

The Euro was weaker after Fed on Wednesday and ended trading in red but remains within 1.0850/1.0950 congestion that extends into eight straight day. Fed's statement did not bring anything significantly new, being in a rather familiar tone and pointing that interest rate increases will be gradual in 2017. Fed pointed to the labor sector which continues to strengthen, while inflation continues to run near 2% target. Markets understood Fed's tone as hawkish and subsequent dollar's rally came as a result of rising expectations of rate hike in June. However, the single currency was not seriously impacted by stronger dollar, remaining in directionless mode and awaiting further signals from two coming events, US Non-Farm Payrolls due on Friday and the final round of French presidential election on Friday. From the technical point of view, situation remains unchanged compared to few previous sessions. Rising 10 SMA (1.0877) is so far holding today's action, which moved within narrow range in Asia and guarding key 200SMA support (1.0831). Violation of the latter is needed to generate stronger negative signal, while extension below 1.0800 zone (Fibo 38.2% of 1.0568/1.0949 / base of 4-hr cloud) would confirm reversal. Otherwise, near-term focus will remain shifted higher while 10SMA holds with break above 1.0950 pivot to open way for 1.1000+ extension.

Res: 1.0900, 1.0935, 1.0950, 1.1000

Sup: 1.0873, 1.0850, 1.0831, 1.0800

Trade Idea : EUR/USD – Buy at 1.0900

EUR/USD - 1.0916

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0897

Kijun-Sen level : 1.0901

Ichimoku cloud top : 1.0920

Ichimoku cloud bottom : 1.0911

New strategy :

Buy at 1.0900, Target: 1.1000, Stop: 1.0870

Position : -

Target : -

Stop : -

Although the single currency fell briefly to 1.0875, lack of follow through selling and current rebound suggest consolidation with upside bias would be seen and test of indicated resistance at 1.0951 (last week’s high) would be seen, however, break there is needed to signal recent upmove from 1.0340 low has resumed for headway to 1.0975-80 and possibly towards 1.1000 but price should falter below 1.1025 (50% projection of 1.0602-1.0951 measuring from 1.0851).

In view of this, we are looking to buy euro on dips. Below intra-day support at 1.0875 would prolong consolidation below said resistance at 1.0951, bring correction towards support at 1.0851 but price should stay above 1.0821 support, bring another rise later.

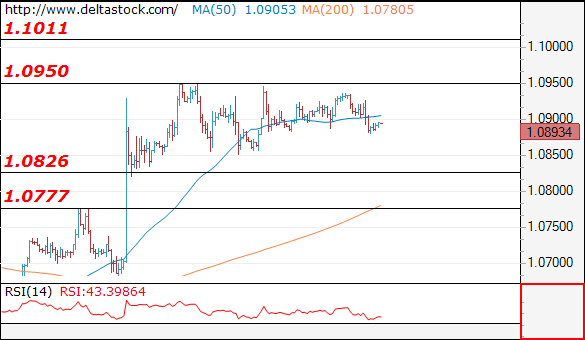

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 10893

The intraday bias is negative, for a slide towards 1.0826 support and a break through the latter will challenge 1.0770 area. Key resistance is still projected at 1.0950.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0950 | 1.0950 | 1.0826 | 1.0780 |

| 1.1010 | 1.1010 | 1.0780 | 1.0676 |

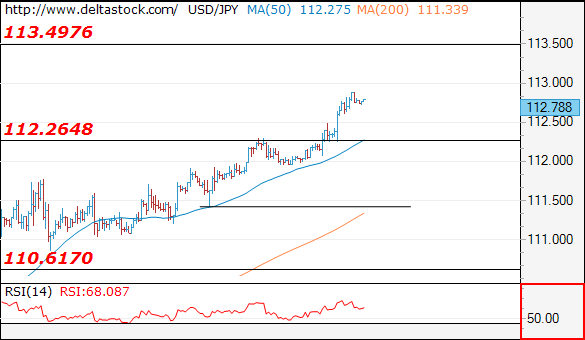

USD/JPY

Current level - 112.78

The pair has reached the dynamic resistance at 112.90, but there are no signs of a reversal yet, so the outlook remains positive, for a rise towards 113.50 zone. Key support lies at 112.26.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.90 | 113.50 | 112.26 | 109.40 |

| 113.50 | 115.60 | 110.40 | 108.12 |

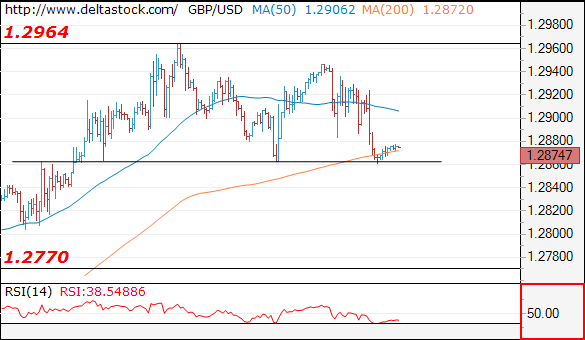

GBP/USD

Current level - 1.2874

The intraday bias here is bearish, for a break through 1.2860 hurdle, towards 1.2770 support zone. Crucial on the upside is 1.2965 peak.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2965 | 1.3120 | 1.2860 | 1.2610 |

| 1.3000 | 1.3500 | 1.2770 | 1.2510 |

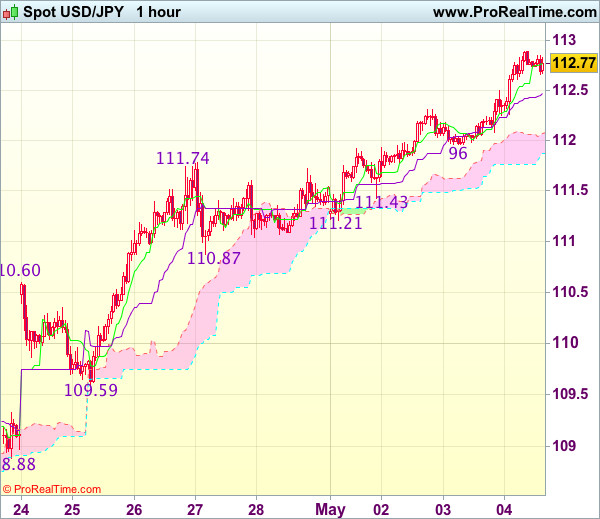

Trade Idea : USD/JPY – Buy at 112.00

USD/JPY - 112.75

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.78

Kijun-Sen level : 112.47

Ichimoku cloud top : 112.07

Ichimoku cloud bottom : 111.87

Original strategy :

Buy at 111.25, Target: 112.55, Stop: 110.90

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.00, Target: 113.00, Stop: 111.65

Position : -

Target : -

Stop : -

As the greenback has surged again after finding renewed buying interest at 111.96 yesterday, adding credence to our view that recent upmove is still in progress and bullishness remains for further subsequent gain to 113.10-15 (61.8% projection of 108.13-111.78 measuring from 110.87) but near term overbought condition should limit upside to previous resistance at 113.54 and reckon 113.75-80 (76.4% retracement of 115.51-108.13) would hold, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as said support at 111.96 should limit downside and bring another rise later. Below previous resistance at 111.78 would abort and suggest a temporary top is formed instead, bring correction to 111.43, then 111.21 support.

Dollar Bulls Return On Confident Fed

The U.S. dollar and Treasury yields across the curve bounced higher after the Fed signaled that a June rate hike is still on the way. Monetary policy-makers acknowledged that there is some softness in the economy, but seemed confident that recent economic slowdown is likely to be temporary. Otherwise there wereno surprises in the statement.

The positive tone struck by the Fed was slightly surprising, especially asconsumer consumption, inflation, and nonfarm payrolls all headed south in March. Having said that, I wouldn't fight the Fed and take an opposing view unless softening data continues,forcingthe Fed to change trajectory.

Traders' attention will shift to Friday's nonfarm payrolls and given the latest ADP private payrolls and ISM non-manufacturing figures, there's potential for an upside surprise. Private payrolls came slightly above expectations at 177,000 and the employment component of the services index printed 51.4 which also indicates a rebound in NFP after a sluggish 98,000 jobs added in March.

A reading above 190K jobs tomorrow may provide additional support to the U.S. dollar, but it requires a pickup in wages for the rally to sustain on the short term, as suchtraders should look at the overall health of the jobs market.

The most significant move in currency markets was not the JPY, which declined to a six-week low against the dollar, but the Aussie plummeting 1.5% yesterday. The commodity currency was pressured by falling iron ore and other base metal prices. Iron ore, coking coal, and copper fell 8%, 4.5% and 3% respectively. Meanwhile, gold resumed its downtrend falling by more than 1.1% since yesterday's Fed decision.

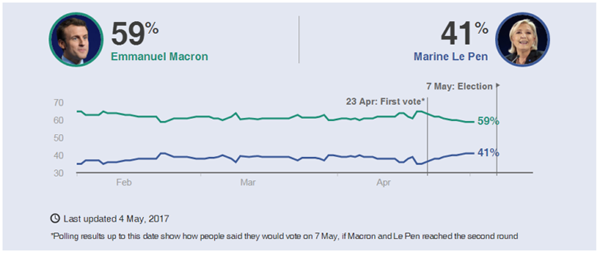

In Europe, the final debate between Marine Le Pen and Emmanuel Macron did little to shift market expectations. With more than a 20% margin for Macron in the final round of Presidential Election voting, this seems to be fairly priced in the Euro. Today's services PMI figures across Europe and the U.K. aren't likely to provide much direction to EURUSD and GBPUSD, with most traders preferring to wait for Friday's NFP report before taking action.

Europe Boosted As Macron Retains Large Poll Lead

The European session is likely to get off to a positive start on Thursday after French Presidential candidate Emmanuel Macron appeared to edge one step closer to the Elysee, following Wednesday evenings debate with rival Marine Le Pen.

Macron retains poll lead after TV debate performance

With Macron already holding a considerable lead in the polls, the TV debate was Le Pen's best opportunity to close the gap ahead of voting on Sunday. While Le Pen was widely seen as being better suited to the event, it is Macron that is believed to have fared better in the scathing encounter, helping to protect his substantial lead in the process and ease concerns about a late surge by the National Front leader.

The FOMC provided some unexpected impetus

While we have seen Le Pen risk abate in recent weeks as her lead in the polls slipped and Macron took the first round, the spread between French and German 10-year yields remains at the top end of the range it traded at prior to the election premium being priced in. If this is also being reflected elsewhere then there may be potential for a small relief rally next week, should Macron win as expected.

*The polling average line looks at the five most recent national polls and takes the median value, ie, the value between the two figures that are higher and two figures that are lower.

Gold hit by Macron risk rally and dollar gains as Fed hints at June hike

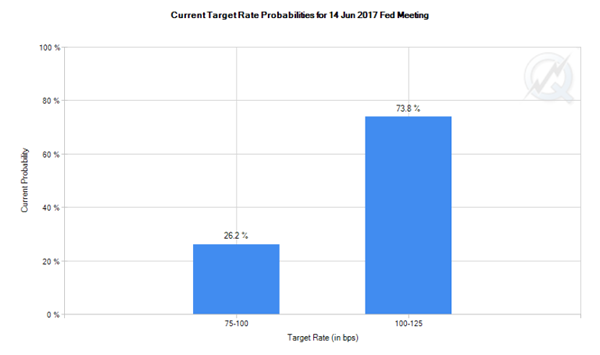

Gold has been dealt a double blow over the last 24 hours, with the post-debate boost to risk appetite and stronger dollar weighing on the yellow metal. The gains in the dollar came as the Fed indicated that it is willing to look through the first quarter weakness which it views as “transitory”, a sign that a second rate hike this year in June very much remains on the table. Markets are now pricing in a 74% chance of a hike next month, up from 68% prior to the statement.

Numerous data releases to come throughout the day on Thursday

With arguably the two biggest events this week now behind us, attention will turn to Friday's jobs report which will offer our first insight into how the US rebounded in the first month of the second quarter. Prior to that though, there is a lot of economic data to come today with services PMIs across Europe being released throughout the morning, followed later this afternoon by jobless claims, productivity, labour costs and factory orders data from the US.

USD/CAD Canadian Dollar Flat After Fed Holds Interest Rate

This morning's Chinese Caixin services PMI got us off to a rocky start but whereas the world's second largest economy is widely expected to slow following a bumper first quarter, data so far this week suggests confidence in Europe is on the rise.

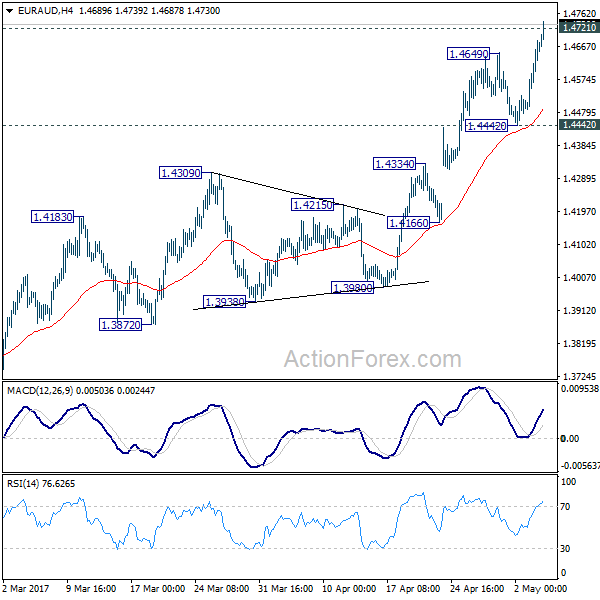

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4537; (P) 1.4612; (R1) 1.4736; More...

EUR/AUD's rally resumed after brief retreat and reaches as high as 1.4739 so far, breaching 1.4721 key resistance. Intraday bias remains on the upside for the moment. We'd holding on to the view of trend reversal after defending 1.3671 key support. Sustained break of 1.4721 will confirm our bullish view. In such case, the next target is 1.5455 medium term fibonacci level. On the downside, break of 1.4442 support is needed to indicate short term topping. Otherwise, outlook will remains bullish in case of retreat.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after defending 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

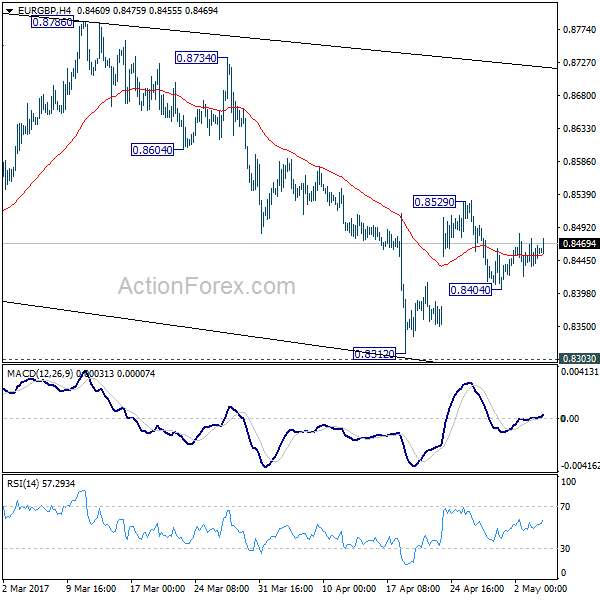

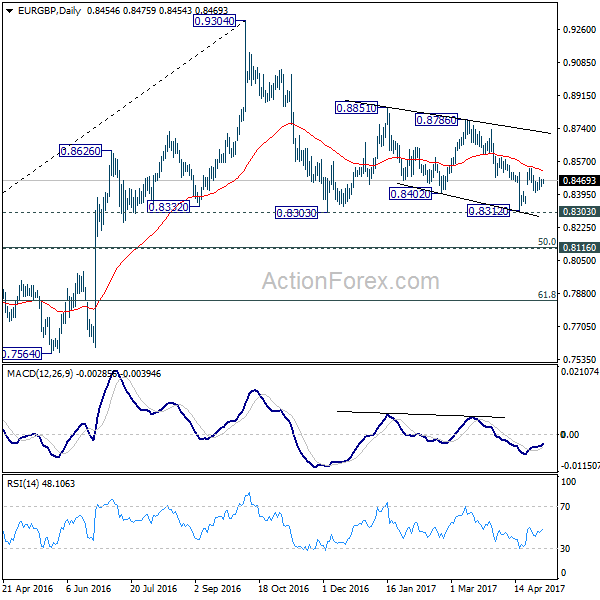

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8437; (P) 0.8456; (R1) 0.8478; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, below 0.8404 will turn focus back to 0.8303 low. Break there will extend the whole corrective pattern from 0.9304. On the upside, above 0.8529 will resume the rebound from 0.8312 towards 0.8786 resistance. Overall, price actions form 0.9304 are seen as a corrective pattern and is extending.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.