Sample Category Title

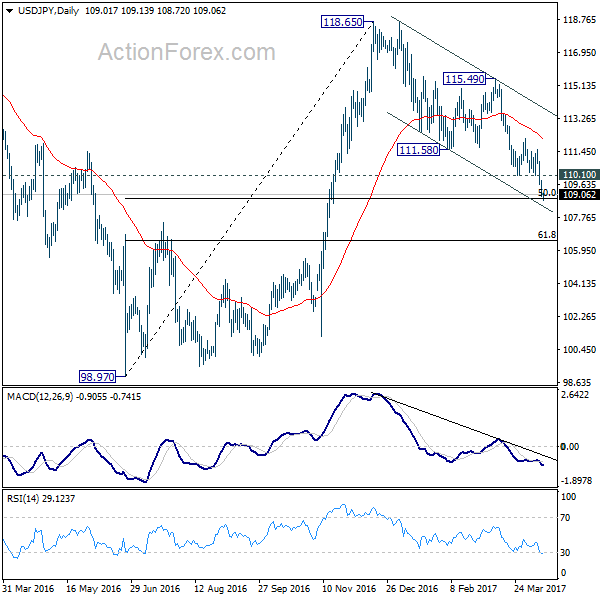

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.67; (P) 109.26; (R1) 109.58; More....

USD/JPY reaches as low as 108.72 so far as the fall from 118.65 extended. Deeper fall could still be seen as long as 110.10 support turned resistance holds. Sustained break of 50% retracement of 98.97 to 118.65 at 108.81 will target 61.8% retracement at 106.48 and possibly below. Nonetheless, break of 110.10 will indicate short term bottoming and turn bias back to the upside for 112.19 resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. Sustained trading below 55 week EMA (now at 111.15) will indicate that the second leg from 98.97 has completed at 118.65. And in that case, USD/JPY would start the third leg down through 98.97 low to 61.8% retracement of 75.56 to 125.85 at 94.77. On the upside, break of 115.49 resistance should resume the rise from 98.97 for a test on 125.85 high.

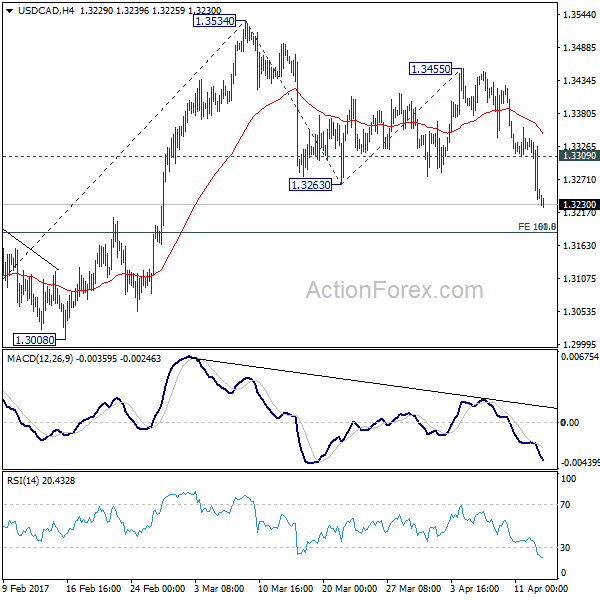

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3207; (P) 1.3272; (R1) 1.3311; More....

USD/CAD's fall extends to as low as 1.3225 so far and intraday bias remains on the downside. Firm break of 1.3263 support confirms resumption of whole fall from 1.3534. At this point, such decline is still viewed as a correction. hence we'd expect strong support from 1.3184 cluster level to contain downside (61.8% retracement of 1.2968 to 1.3534 at 1.3184, 100% projection of 1.3534 to 1.3263 from 1.3455 at 1.3814 too). Break of 1.3309 minor resistance will indicate short term bottoming and turn bias back to the downside for 1.3455. However, sustained break of 1.3184 will dampen our view and could bring deeper fall back to 1.2968 key support level.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

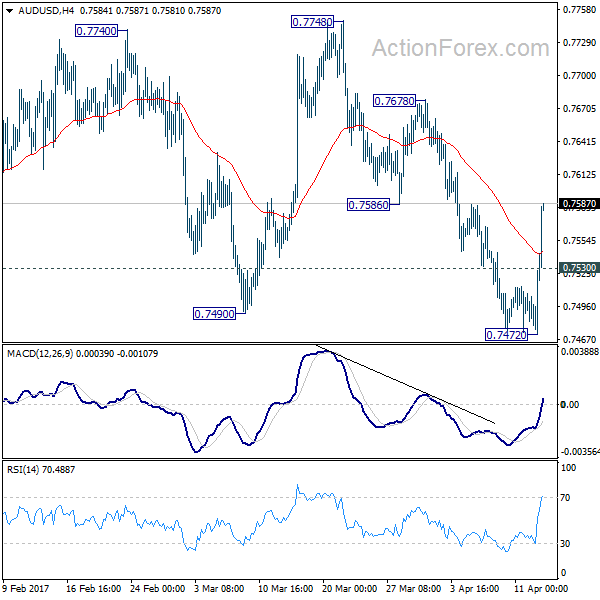

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7487; (P) 0.7507; (R1) 0.7542; More...

AUD/USD rebounded strongly with firm break of 0.7531 minor resistance. That indicates fall from 0.7748 is completed at 0.7472, after failing to sustain below 0.7490 key support. Intraday bias is turned back to the upside for 0.7678 resistance. More importantly, the development argues that rise from 0.7158 may be resuming. Break of 0.7678 could now pave the way through 0.7748 and put key fibonacci level at 0.7849 in focus. On the downside, below 0.7530 minor support will turn bias neutral again.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8142) and above.

Dollar Talked Down by Trump, Australian Surges on Jobs, Canadian Firm on BoC

US Dollar tumbled broadly and is now trading as the weakest major currency after US President Donald Trump talked down the exchange rate. The Dollar index reaches as low as 100.01 so far. It's still holding on to 100 handle mainly thanks to the relative weakness of Euro, who's trading as the second weakest one. But this 100 psychological level looks vulnerable. Commodity currencies are broadly higher. Canadian Dollar maintains post BoC gains. Aussie is lifted by strong employment data. Yen pares back some gains but remains the strongest one for the weak on falling treasury yields. US 10 year yield closed at 2.296 and is now close to last week's low at 2.271. In other markets, Gold is staying firm at 1287 at the time of writing. But it's starting to feel a bit heavy ahead of 1300 handle, as risk aversion eases. WTI crude oil also retreats mildly and is back at around 53.

Trump complained Dollar Strength. China not currency manipulator

In an interview with the Wall Street Journal, US President Donald Trump complained that US dollar "is getting too strong, and partially that's my fault because people have confidence in me. But that's hurting - that will hurt ultimately". He added that "it's very, very hard to compete when you have a strong dollar and other countries are devaluing their currency". Meanwhile, Trump also reversed his position and said that China is "not currency manipulators". And he hailed that Chinese President Xi Jinping "wants to help us with North Korea."

Trump undecided on Fed chair Yellen's second term

On interest rates, Trump affirmed his preference over a low-interest rate policy, noting that "as soon as [rates] go up, your stock market is going to go way down, most likely". During his election campaign, Trump had not reserved his criticism over Fed Chair Janet Yellen and indicated that he would replace her if he's got elected. However, he showed in the interview his "respect" for Yellen and suggested that he has not decided whether he would reappoint her for the second term.

Separately, Dallas Fed President Robert Kaplan said that the plan to shrink Fed's balance sheet won't prompt adjustment in the rate path. He echoed other Fed speakers and said that Fed will start balance sheet normalization "as soon as later this year". Meanwhile, three rate hikes in total in 2017 remains his "baseline" case. He also noted that "we are not at full employment but we are getting there". And Fed can "afford to be gradual and patient" on rate hikes.

Canadian Dollar boosted by upbeat BoC

BoC appeared more confident over the economic growth outlook, although it maintained the policy rate unchanged at 0.50% yesterday. The central bank upgraded the GDP growth forecast for this year amidst strong housing market activities in the first quarter, but revised lower the figure for 2018. The country's economy is expected to expand 2.6% this year, up from 2.1% in January's projection, before decelerating to 1.9% in 2018 (January: 2.1%) and 1.8% in 2019. BoC now expects the output gap to close in 1Q18. Meanwhile, BoC has revised down the "projection of potential growth, reflecting persistently weak investment".

BoC remained cautious, suggesting that "it is too early to conclude that the economy is on a sustainable growth path". The central bank revised the inflation forecast a tick higher to 1.9% and 2% in 2017 and 2018, respectively. Inflation would then further improve to 2.1% in 2019. On the monetary policy, Governor Stephen Poloz described the stance as "decidedly neutral" as the members weighed the improved economic developments against the uncertain trade policy. BoC's policy rate is expected to stay unchanged at 0.5% for the rest of the year.

More on BoC:

- BOC Upgraded Growth Outlook, Remains Cautious Over Trade Relations With US

- Bank of Canada Assumes a "Decidedly Neutral" Policy Stance

- Bank of Canada Interest Rate Announcement: Still Waiting for Sunny Stephen

Aussie boosted by strong job data

Australia Dollar is boosted by strong employment data today. Employment grew 60.9k in March, triple of expectation of 20.0k. Prior month's figure was revised up from -6.4k to 2.8k. Full time jobs rose by 74.5k, highest jump in nearly 30 years since December 1987. Part-time jobs dropped -13.6k. Participation rate also rose from 64.6% to 64.8%. Unemployment rate was unchanged at 5.9% as more people are back in the market. Also from Australia, consumer inflation expectation rose 4.1% in April.

Adding to the support to Aussie, RBA said in its semiannual Financial Stability Review that " vulnerabilities related to household debt and the housing market more generally have increased." And, "some riskier types of borrowing, such as interest-only lending, remain prevalent." RBA also expressed the concern that "investors are likely to contribute to the amplification of the cycles in borrowing and housing prices, generating additional risks to the future health of the economy." Today's job number certainly removed much burden on RBA for lowering interest rate again, with the background of worries on housing market bubble. Q1 CPI and GDP will be the next key pieces of data to watch.

Elsewhere...

Japan M2 rose 4.3% yoy in March. China trade surplus came in larger than expected at USD 23.9b, CNY 164b in March. German CPI final, Swiss PPI will be released in European session. Canada new housing price index, manufacturing shipments will be released in US session. US PPI, jobless claims and U of Michigan sentiment will also be featured.

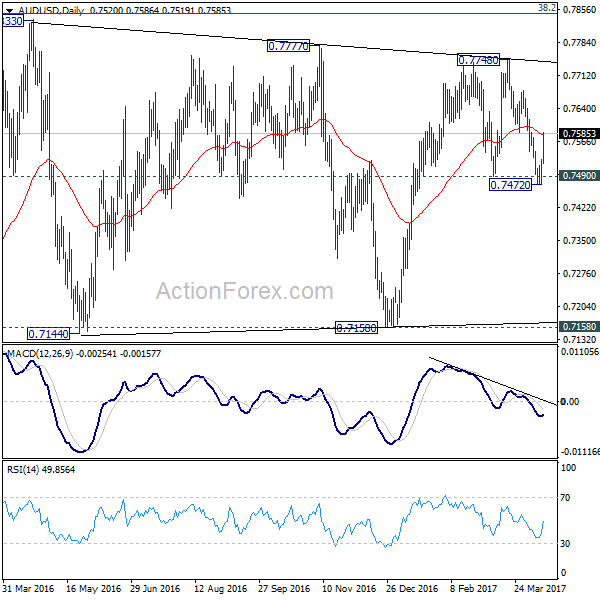

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7487; (P) 0.7507; (R1) 0.7542; More...

AUD/USD rebounded strongly with firm break of 0.7531 minor resistance. That indicates fall from 0.7748 is completed at 0.7472, after failing to sustain below 0.7490 key support. Intraday bias is turned back to the upside for 0.7678 resistance. More importantly, the development argues that rise from 0.7158 may be resuming. Break of 0.7678 could now pave the way through 0.7748 and put key fibonacci level at 0.7849 in focus. On the downside, below 0.7530 minor support will turn bias neutral again.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8142) and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Mar | 4.30% | 4.20% | 4.20% | |

| 1:00 | AUD | Consumer Inflation Expectation Apr | 4.10% | 4.00% | ||

| 1:30 | AUD | RBA Financial Stability Review | ||||

| 1:30 | AUD | Employment Change Mar | 60.9k | 20.0k | -6.4k | 2.8k |

| 1:30 | AUD | Unemployment Rate Mar | 5.90% | 5.90% | 5.90% | |

| 3:15 | CNY | Trade Balance (USD) Mar | 23.9B | 12.5B | -9.1B | |

| 3:15 | CNY | Trade Balance (CNY) Mar | 164B | 76B | -60B | |

| 6:00 | EUR | German CPI M/M Mar F | 0.20% | 0.20% | ||

| 6:00 | EUR | German CPI Y/Y Mar F | 1.60% | 1.60% | ||

| 7:15 | CHF | Producer & Import Prices M/M Mar | 0.10% | -0.20% | ||

| 7:15 | CHF | Producer & Import Prices Y/Y Mar | 0.90% | 1.30% | ||

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.20% | 0.10% | ||

| 12:30 | CAD | Manufacturing Shipments M/M Feb | -0.70% | 0.60% | ||

| 12:30 | USD | PPI M/M Mar | 0.00% | 0.30% | ||

| 12:30 | USD | PPI Y/Y Mar | 2.40% | 2.20% | ||

| 12:30 | USD | PPI Core M/M Mar | 0.20% | 0.30% | ||

| 12:30 | USD | PPI Core Y/Y Mar | 1.80% | 1.50% | ||

| 12:30 | USD | Initial Jobless Claims (APR 08) | 245k | 234k | ||

| 14:00 | USD | U. of Michigan Confidence Apr P | 96.6 | 96.9 | ||

| 14:30 | USD | Natural Gas Storage | 2B |

Mixed Forecast Ahead For The Loonie

Key Points:

- Near-term bias remains bearish but a reversal should be on the way.

- Gartley pattern and falling wedge are the two key structures in play.

- Currently waiting for the 61.8% Fibonacci level to break.

In the wake of the Bank of Canada's Overnight Rate decision, it may be worth taking a closer look at the Loonie's technical forecast to get a feel for what could be on the way over the coming weeks. As we do this, it will likely become apparent that we could see some fairly sharp reversals as the pair continues to navigate its long-term consolidation phase whose end is not yet in sight.

First and foremost, let's look at what is on the cards for the near-term given that we have seen some heavy selling pressure over the past week. Of course, a large portion of this downside price action stems for the broader market's swing away from the USD following a rather torrid week of geopolitical and Trump-based headline risk. Nevertheless, this plunge lower also has broad support from the technical bias which is actuallyindicating that further losses could now be warranted.

In particular, the latest slip has now forced the EMA configuration into one of the more bearish positions. Notably, price action is below the 100 day moving average and the two shorter averages have now experienced a bearish crossover. Additionally, the MACD remains bearish alongside the Parabolic SAR readings. Most importantly, there is a loose Gartley pattern becoming apparent which could see the pair sink even lower as we move forward.

All this being said and done, there is still one final hurdle that the bears will need to overcome before we can be relatively certain that we do in fact have further losses on the way. Specifically, the 61.8% Fibonacci level remains intact which could hamper any efforts to mount that final push back to the downside constraint of the long-term falling wedge. Fortunately, with the exception of the stochastics being in oversold territory, there is little in the way of technical evidence to suggest that this level should hold which means losses are like to restart shortly.

Once the tumble has resumed, we expect the pair to sink to around the 1.3128 level before running into another impasse. Namely, the presence of the downside of the wedge should prove to be a robust support which would take a fundamental upset to be broken. However, the ending on the Gartley pattern will also be worth keeping in mind as this would typically suggest that an uptrend should be on the way in fairly short order. This upswing could extend as high as the 1.3386 mark but it will likely run into resistance around the 1.3234 handle as that Fibonacci level and the 100 day EMA provide a decent cap on upside action.

Australia Posts Strongest Jobs Gain In More Than A Year In March

For the 24 hours to 23:00 GMT, the AUD rose 0.35% against the USD and closed at 0.7528.

LME Copper prices declined 1.1% or $61.0/MT to $5685.0/MT. Aluminium prices declined 0.03% or $0.5/MT to $1907.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7568, with the AUD trading 0.53% higher against the USD from yesterday’s close, after early morning data indicated that number of people employed in Australia increased more-than-expected by 60.9K in March, rising by the most since October 2015, thus offering signs of recovery in Australia’s labour market. Investors had envisaged for an advance of 20.0K, following a revised gain of 2.8K in the prior month.

Additionally, the nation’s seasonally adjusted unemployment rate remained steady at 5.9% in March, in line with market expectations. Moreover, the nation’s consumer inflation expectations rose to 4.1% in April, after recording a reading of 4.0% in the prior month.

Elsewhere, China, Australia’s largest trading partner, registered a more-than-expected trade surplus to a level of CNY164.34 billion in March, compared to market consensus for the nation to record a surplus of CNY75.80 billion and following a deficit of CNY60.36 billion in the previous month. Further, the nation’s exports jumped by 22.3% YoY in March, surpassing market expectations for an advance of 8.0%. In the prior month, exports had registered a gain of 4.2%. Also, imports advanced more-than-estimated by 26.3% in March, following a gain of 44.7% in the preceding month.

The pair is expected to find support at 0.7500, and a fall through could take it to the next support level of 0.7433. The pair is expected to find its first resistance at 0.7604, and a rise through could take it to the next resistance level of 0.7641.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro Trading Higher, Ahead Of Germany’s Final Inflation Figures For March

For the 24 hours to 23:00 GMT, the EUR rose 0.58% against the USD and closed at 1.0665.

In economic news, Germany's wholesale price index remained flat on a monthly basis in March, following a revised rise of 0.5% in the prior month.

The greenback tumbled against a basket of currencies, after the US President, Donald Trump, stated that the local currency was getting ‘too strong'.

On the macro front, the US budget deficit widened more-than-anticipated to a level of $176.2 billion in March, compared to market expectations for the nation to post a deficit of $169.0 billion and following a deficit of $108.0 billion in the preceding month. On the contrary, the nation's mortgage applications rebounded 1.5% in the week ended 07 April, compared to a fall of 1.6% in the previous month.

In other economic news, the nation's import price index recorded a drop of 0.2% YoY in March, meeting market expectations and following a revised gain of 0.4% in the prior month. Further, the nation's export price index surprisingly climbed 0.2% on a monthly basis in March. The index had climbed by 0.3% in the previous month, while markets anticipated for a flat reading.

In the Asian session, at GMT0300, the pair is trading at 1.0673, with the EUR trading 0.08% higher against the USD from yesterday's close.

The pair is expected to find support at 1.0614, and a fall through could take it to the next support level of 1.0556. The pair is expected to find its first resistance at 1.0704, and a rise through could take it to the next resistance level of 1.0736.

Going ahead, investors will focus on Germany's final consumer price index for March, slated to release in a few hours. Additionally, in the US, the flash Reuters/Michigan consumer confidence index for April, coupled with weekly jobless claims data, will be on investor's radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK’s ILO Unemployment Rate Steady At An 11-Year Low Level In The Three Months Through February

For the 24 hours to 23:00 GMT, the GBP rose 0.41% against the USD and closed at 1.2538, after UK's ILO unemployment rate remained steady at an eleven-year low level of 4.7% in the three months to February, in line with market expectations.

However, the nation's average earnings excluding bonus rose 2.2% YoY in the three months through February, rising at its weakest pace in seven months, indicating that consumer spending is unlikely to contribute to economic growth in the first quarter of 2017. The average earnings excluding bonus had recorded a revised gain of 2.4% in the November-January 2017 period, while markets expected for a rise of 2.1%.

In the Asian session, at GMT0300, the pair is trading at 1.2567, with the GBP trading 0.23% higher against the USD from yesterday's close.

Data released overnight indicated that the nation's RICS house price balance remained steady at a level of 22.0 in March, in line with market expectations.

The pair is expected to find support at 1.2505, and a fall through could take it to the next support level of 1.2442. The pair is expected to find its first resistance at 1.2602, and a rise through could take it to the next resistance level of 1.2636.

Moving ahead, the Bank of England's (BoE) credit conditions survey report, set to release in a few hours, will be eyed by market participants.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.57% against the JPY and closed at 109.05.

In the Asian session, at GMT0300, the pair is trading at 108.83, with the USD trading 0.2% lower against the JPY from yesterday’s close.

The pair is expected to find support at 108.40, and a fall through could take it to the next support level of 107.97. The pair is expected to find its first resistance at 109.56, and a rise through could take it to the next resistance level of 110.29.

Moving ahead, market participants will closely monitor Japan’s industrial production data for February, due to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.52% against the CHF and closed at 1.0022.

In the Asian session, at GMT0300, the pair is trading at 1.0010, with the USD trading 0.12% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9982, and a fall through could take it to the next support level of 0.9953. The pair is expected to find its first resistance at 1.0064, and a rise through could take it to the next resistance level of 1.0117.

Ahead in the day, traders would focus on Switzerland’s producer and import prices for March.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.