Sample Category Title

NZ Labor Data Gives RBNZ Room to Stay on Hold

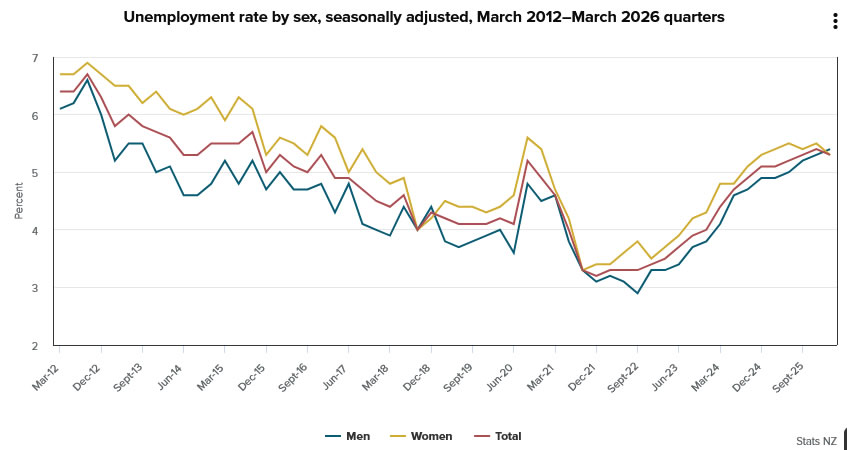

New Zealand’s labor market showed tentative signs of stabilization in the first quarter, with the unemployment rate unexpectedly falling from 5.4% to 5.3%, below expectations for no change. Employment rose 0.2% qoq, slightly under the expected 0.3% gain, marking modest improvement.

However, the decline in unemployment was not entirely driven by stronger hiring. The labor force participation rate edged down from 70.5% to 70.4%, while the employment rate held steady at 66.7%. This suggests that part of the fall in unemployment reflected weaker labor force participation rather than a significant acceleration in job creation.

For the Reserve Bank of New Zealand, the key takeaway was steady growth in wages. Private sector wage growth, measured by the Labor Cost Index, rose 0.4% qoq, leaving annual growth steady at 2.0%. Public sector wages increased 1.7% yoy, while overall salary and wage rates rose 2.0% yoy. With annual CPI inflation running at 3.1%, wage growth remains well below consumer price inflation, suggesting limited evidence of a wage-price spiral.

The data are likely to reinforce the RBNZ’s cautious wait-and-see stance. While energy-related inflation risks remain elevated, stable wage growth gives policymakers more confidence that broader inflation pressures are not yet becoming entrenched through the labor market. As a result, the figures support the view that the RBNZ can remain on hold at 2.25% through the winter rather than rushing toward additional tightening.

| Indicator | Previous | Latest |

|---|---|---|

| Employment Growth (QoQ) | 0.5% | 0.2% |

| Unemployment Rate | 5.4% | 5.3% |

| Underutilisation Rate | 12.9% | 12.9% |

| Employment Rate | 66.7% | 66.7% |

| Participation Rate | 70.5% | 70.4% |

| Private Sector LCI (YoY) | 2.0% | 2.0% |

Breakout Time for Cryptos? Bitcoin at $80K; BTC and Ethereum (ETH) Technical Outlook

- Bitcoin bullies through $80,000 with Tech flows unstoppable and helping the Crypto space to continue higher

- The gradual rise in Cryptocurrencies could be helping to stabilize the rally, now developing into a more sustainable breakout

- Exploring a Technical Analysis and trading levels for Bitcoin and Ethereum

Bitcoin has officially broken through the significant $80,000 mark, driven by strong tech-focused investment that is lifting the entire cryptocurrency market in a moment when least expected.

Markets are insanely good at playing tricks on expectations and sentiment.

Despite their high-risk and beta profile, the technology sector and digital assets are attracting significant attention because traditional investments are under pressure from higher energy prices.

With Oil prices rising and affecting the broader economy and corporate profits, the more traditional stocks and sectors are exposed to squeezing margins and performance, hence, investors are now looking at spots unaffected by the geopolitical change.

This can be seen in the fantastic rise in the Crypto Market Cap ever since the start of the war, a very surprising dynamic.

Total Crypto Market Cap – Daily Chart. May 5, 2026 – Source: TradingView

The entire Crypto Market is up 22% since the beginning of the War. Quite surprising especially when looking at the price action before the war.

Another factor is the high level of short positions in the market since last October.

As these positions are closed, the steady rise in cryptocurrencies is forcing highly leveraged sellers and pushing the ongoing dynamic even further.

Large-scale buying is also happening in the background.

As mentioned in our late-February analysis when the geopolitical conflict began, most of the long-term distribution in digital assets had already taken place.

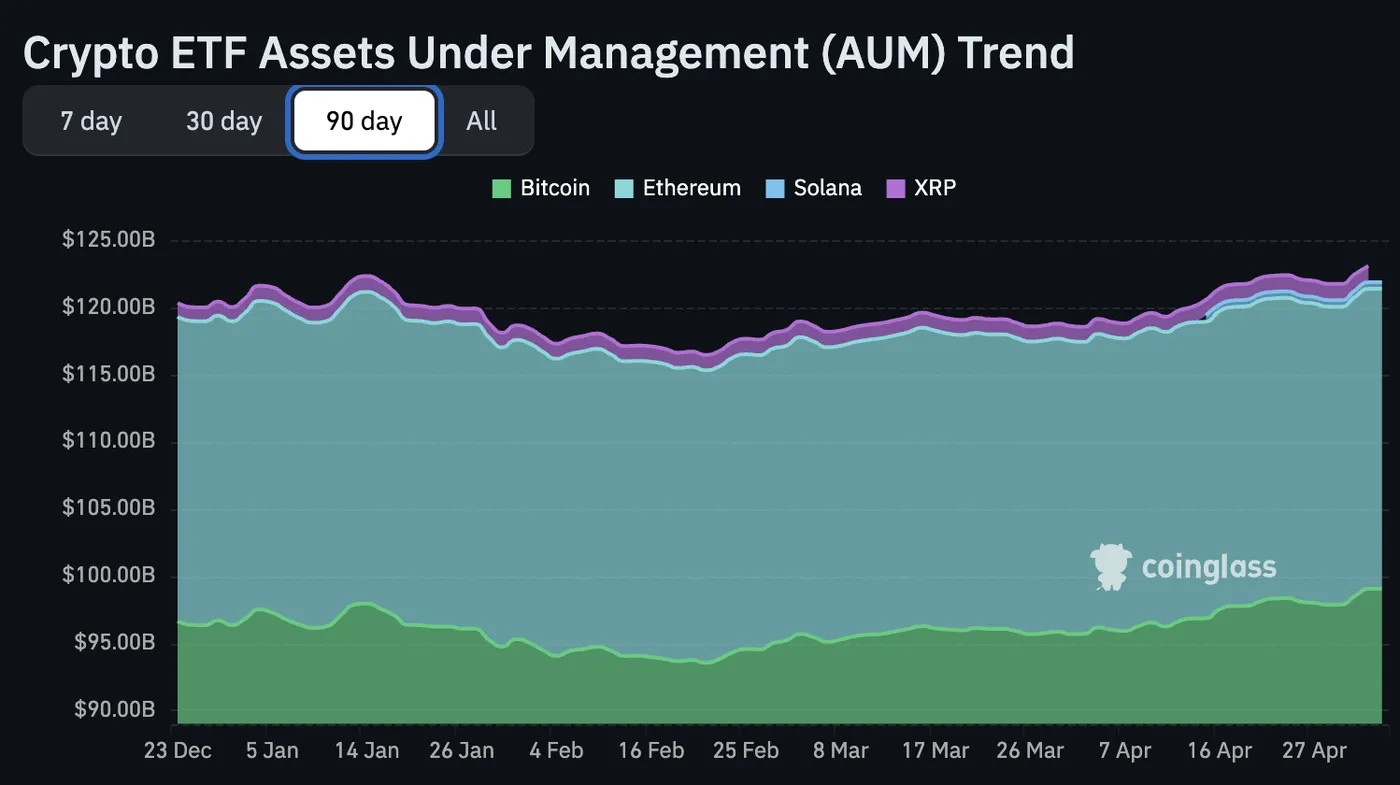

Bitcoin and Crypto ETF Inflows and Outflows since 2026 – Source: Coinglass

Could a major rally be on the way? For this breakout to continue, the market will need more geopolitical stability and ongoing strong investor interest.

Every significant rally starts with a foundation, and the current rebound is building a solid base for future growth. If prices stay above the important $70,000 level, the outlook for this crypto rally remains positive.

Let's dive right into a technical analysis and key trading levels for both Bitcoin and Ethereum to spot if a clear breakout in indeed into play from here.

Bitcoin (BTC) 4H Chart and Technical Levels

Bitcoin (BTC) 4H Chart, May 5, 2026 – Source: TradingView

Bitcoin is now pushing within the $80,000 to $83,000 Resistance, a key region of interest for bulls to break in order to confirm the breakout.

The bull channel is still holding strong for now with its top around $85,000.

- Above this, the longer-term breakout is confirmed

- Rejecting $83,000 level could on the other hand provide a good opportunity for sellers to retake control of the mid-term action

We are entering a pivotal moment for Cryptocurrency Markets, hence, make sure to track the price action in upcoming weeks.

Levels of interest for BTC trading:

Support Levels:

- $75,000 Key long-term Pivot (acting as resistance)

- $70,000 Short-term momentum Pivot (50 and 200-4H MA)

- $60,000 to $63,000 Main 2024 support (recent double bottom)

- $59,935 February Lows

- $52,000 to $58,000 Next support and 200-Week MA ($55,000 Mid-point)

- $40,000 Mid-2024 breakout support

Resistance Levels:

- $80,000 to $83,000 mini-resistance (entering, bullish above)

- $85,000 bull channel top

- $90,000 to $95,000 minor Resistance

- $98,000 to $100,000 Pivotal Resistance

- Current ATH Resistance $124,000 to $126,000

Ethereum (ETH) 4H Chart and Technical Levels

Ethereum (ETH) 4H Chart, May 5, 2026– Source: TradingView

Ethereum has been somewhat struggling a bit more than Bitcoin to push above its prior month's highs.

Nonetheless, with Bitcoin dragging market sentiment higher, it wouldn't be surprising to see the second crypto catch up within the next few days (barring any major negative news).

The top of its bull channel is at $2,530; breaking above this should push a particularly bullish momentum, hence this will have to be watched.

- On the other hand, below $2,200 the price action would get bearish again

- Make sure to check out reactions to the Non-Farm Payrolls, which will surely have their impact on general risk-sentiment.

Levels of interest for ETH trading:

Support Levels:

- 4H 50 MA $2,300

- Channel lows $2,200

- $1,700 to $1,800 Pre-Bounce 2025 Key Support (testing)

- $1,744 February 6 lows

- $1,380 to $1,500 2025 Support

- 2025 Lows $1,384

Resistance Levels:

- Mini-Resistance $2,400

- $2,500 to $2,800 June 2025 Pivotal Resistance

- $3,000 to $3,200 Major momentum Pivot (Test of the $3,000)

- $4,950 Current new All-time highs

The narrative is easing, but keep track of WTI Crude and the latest headlines to stay ahead of the game.

Safe Trades!

GBP/USD Potential Trade Setups: Two Opportunities on the Bullish Retest and Breakout Play

- GBP/USD has reclaimed the key psychological level of 1.35000, which now serves as a foundational support zone.

- The analysis presents a cautiously optimistic outlook, with medium-term momentum shifting toward the bulls based on the H4 chart MAs.

- Two potential trade setups are detailed: a Bullish Retest near 1.35380-1.35400 and a Breakout Play above the 1.35844 resistance level.

The British Pound has showcased significant resilience over the past few sessions against the Greenback. After finding solid ground near the psychological 1.3500 handle, cable has embarked on a steady recovery, supported by a confluence of technical indicators across various timeframes.

H4 Chart: The Macro View – Breaking Structural Resistance

On the H4 timeframe, the narrative is one of a trend reversal in the making. For much of the previous month, Cable was locked in a descending channel, characterized by lower highs and lower lows. However, the recent price action shows a definitive break above the descending trendline.

More importantly, the pair has reclaimed the psychological 1.35000 handle, which has transitioned from a stubborn resistance level to a foundational support zone. The 100-period Simple Moving Average (MA) (Blue) is currently trending above the 200-period MA (Black), signaling that the medium-term momentum has shifted in favor of the bulls.

The RSI (Relative Strength Index) on the H4 is hovering around the 53 mark, suggesting there is ample "runway" left before the pair reaches overbought territory, leaving the door open for a test of the 1.35844 resistance level.

GBP/USD Four-Hour Chart, May 5, 2026

Source: TradingView

H1 Chart: Intra-day Consolidation and Moving Average Support

Zooming into the H1 chart, we can see the granularity of the recent rally. The pair has spent the last 24 hours consolidating just above the 1.35300 area.

Looking at price action and GBP/USD is consistently finding support at the 100-MA. Each time the price dips toward the 1.35400 level, buyers have stepped in, creating a series of higher lows.

The immediate hurdle for intra-day bulls is the 1.35844 horizontal resistance. A clean hourly candle close above this level would likely trigger a momentum move toward the next major objective at 1.36965.

GBP/USD One-Hour Chart, May 5, 2026

Source: TradingView

M15 Chart: Scalping Opportunities and Entry Triggers

The M15 chart reveals the immediate tactical environment. We are seeing a classic "buy the dip" configuration. The price recently spiked toward the 200-MA (1.35573) and is currently seeing a minor pullback.

The RSI Divergence indicator at the bottom of the chart shows a "Pivot" high followed by a "Bear" tag, which explains the current cooling off. This is not necessarily a reversal, but rather a healthy breather within an uptrend.

Potential Trade Opportunities (M15):

The Bullish Retest: Traders may look for a long entry if the price retraces to the 1.35365 area (confluence of the M15 100-SMA and previous structural support).

- Potential Entry: 1.35380 - 1.35400

- Stop Loss: Below the 1.35200 swing low.

- Target 1: 1.35844 (Recent High/H4 Resistance)

- Target 2: 1.36200

The Breakout Play: A high-conviction move would be a break and retest of the 1.35844 ceiling. If the price clears this level with strong volume, it confirms the H4 bullish bias.

- Potential Entry: Buy stop at 1.35860 or wait for a retest of 1.35844 as support.

- Stop Loss: 1.35500

- Target: 1.36900

GBP/USD M15 Chart, May 5, 2026

Source: TradingView

The technical outlook for GBP/USD remains cautiously optimistic. As long as price action maintains its position above the 1.35000 psychological floor, the path of least resistance is to the upside.

However, traders should keep a close eye on the RSI on the lower timeframes; if the M15 RSI fails to make a higher high alongside price, a deeper correction toward 1.35100 could be on the cards before the next leg up.

RBA May 2026 Meeting: Cash Rate up 25bp to 4.35%, to Head Off Rising Inflation Expectations

RBA hikes as expected in 8–1 vote, citing Middle East boost to existing inflation pressures. Further hikes this year remain likely but June timing is more finely balanced now.

As expected, the RBA Monetary Policy Board (MPB) raised the cash rate 25bps to 4.35% following its May 2026 meeting. The vote was again split, this time 8–1, after the 5–4 vote in March. In explaining the decision, the MPB cited the higher inflation stemming from the Middle East conflict, including second-round effects, with risks tilted to the upside. These added to the inflationary pressures already arising from what it sees as capacity pressures. It also noted indications that “higher fuel prices are likely to have second-round effects on prices for goods and services more broadly”, as we have been highlighting.

While the MPB regards monetary policy as mildly restrictive, both the Statement on Monetary Policy (SMP) and the Governor pointed to credit growth and other indicators as suggesting that financial conditions are not as tight for the same level of the cash rate as was true a few years ago.

We still expect the RBA to tighten rates again this year. However, we think a June move now looks more finely balanced. The Governor’s language in the press conference was a bit more dovish than our read of the media release and the SMP or the implications of the RBA staff forecasts. Governor Bullock characterised the three rate hikes so far as dealing with the high inflation issue that already existed before the conflict in the Middle East started, and that this “gives space” for the MPB to see how the conflict played out. On a plain reading, this might suggest that the MPB is more inclined to pause in June.

The RBA’s inflation forecasts show trimmed mean inflation peaking in Q2 at 3.8% and moderating a little from there but only getting back to the 2.5% target midpoint by June 2028. Contrary to the Governor’s remarks, this implies that the MPB is comfortable with the idea of following something like the market path from here, which at the time the forecasts were finalised implied one-and-a-half more hikes. This forecast is also based on a futures market path for oil tracking back to USD80/bbl by year-end, which might be too optimistic.

Our own assessment, however, is that there is a bit more near-term inflation to come, both from a higher oil price than future markets imply and greater, more drawn-out second-stage pass-through to other prices, especially in areas such as home-building costs. We therefore think the near-term inflation risks are tilted to the upside relative to the RBA forecasts. Our own inflation forecasts see trimmed mean inflation peaking at 4% and staying there for the remainder of 2026.

The question is what might happen between now and the June meeting that would dislodge their view about the outlook. While there are several key events, including the Federal budget and National Wage Case decision, these are unlikely to turn the dial on the RBA forecasts. Meanwhile, the inflation expectations story is going to be hard to monitor in the near term.

We were surprised that the Governor appeared to give the green light to firms passing these fuel and fertiliser cost increases into their own prices, saying that it is reasonable for them to do so. This stood in contrast to the discussion in the media conference about avoiding pass-through to wages. At several points, the Governor emphasised that the energy price shock “makes us all poorer” and there was nothing that could be done about that. In our view, it would have been more helpful to the RBA’s own inflation fight if the Governor had encouraged firms that had the capacity to absorb those cost increases to do so.

Consistent with the track for both inflation and interest rates, the revised forecasts are for lower growth in GDP and consumption, with business investment softening later this year as well. The labour market softens with a lag, though we note that both the solid near-term forecasts for hours worked and the forecast decline in participation further out are fragile.

The SMP included some forecast scenarios centred on higher outcomes for oil prices. These were qualitatively similar to the scenarios we have been publishing and revising since 3 March, though the decline in inflation in their scenarios is relatively front-loaded.

There are a number of tensions in the RBA’s forecast revisions. Although measures of labour market slack, especially underemployment, have been revised up, so was the Wage Price Index, marginally. The RBA assesses that a little spare capacity will open up in the labour market, but not until 2028. A lot hangs on a relatively downbeat government forecast for population growth and an assumption that the participation rate cyclically declines, against the upward trend that has persisted for decades.

Similarly, the near-term forecast for productivity growth is quite downbeat. With actual productivity growth at 0.9%yr for 2025, the forecast of 0%yr to June quarter 2026 implies quite a turnaround, particularly for hours worked. While measured productivity growth is cyclical, this may induce the RBA to remain pessimistic about the underlying trend.

Eco Data 5/6/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Employment Change Q1 | 0.20% | 0.30% | 0.50% | |

| 22:45 | NZD | Unemployment Rate Q1 | 5.30% | 5.40% | 5.40% | |

| 22:45 | NZD | Labour Cost Index Q/Q Q1 | 0.50% | 0.40% | 0.40% | |

| 01:45 | CNY | RatingDog Services PMI Apr | 52.6 | 52 | 52.1 | |

| 07:50 | EUR | France Services PMI Apr F | 46.5 | 46.5 | 46.5 | |

| 07:55 | EUR | Germany Services PMI Apr F | 46.9 | 46.9 | 46.9 | |

| 08:00 | EUR | Eurozone Services PMI Apr F | 47.6 | 47.4 | 47.4 | |

| 08:30 | GBP | Services PMI Apr F | 52.7 | 52 | 52 | |

| 09:00 | EUR | Eurozone PPI M/M Mar | 3.40% | 3.30% | -0.70% | -0.60% |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | 2.10% | 1.80% | -3% | |

| 12:15 | USD | ADP Employment Change Apr | 109K | 79K | 62K | 61K |

| 14:00 | CAD | Ivey PMI Apr | 57.7 | 49.9 | 49.7 | |

| 14:30 | USD | Crude Oil Inventories (May 1) | -2.3M | -3.4M | -6.2M |

| 22:45 | NZD |

| Employment Change Q1 | |

| Actual | 0.20% |

| Consensus | 0.30% |

| Previous | 0.50% |

| 22:45 | NZD |

| Unemployment Rate Q1 | |

| Actual | 5.30% |

| Consensus | 5.40% |

| Previous | 5.40% |

| 22:45 | NZD |

| Labour Cost Index Q/Q Q1 | |

| Actual | 0.50% |

| Consensus | 0.40% |

| Previous | 0.40% |

| 01:45 | CNY |

| RatingDog Services PMI Apr | |

| Actual | 52.6 |

| Consensus | 52 |

| Previous | 52.1 |

| 07:50 | EUR |

| France Services PMI Apr F | |

| Actual | 46.5 |

| Consensus | 46.5 |

| Previous | 46.5 |

| 07:55 | EUR |

| Germany Services PMI Apr F | |

| Actual | 46.9 |

| Consensus | 46.9 |

| Previous | 46.9 |

| 08:00 | EUR |

| Eurozone Services PMI Apr F | |

| Actual | 47.6 |

| Consensus | 47.4 |

| Previous | 47.4 |

| 08:30 | GBP |

| Services PMI Apr F | |

| Actual | 52.7 |

| Consensus | 52 |

| Previous | 52 |

| 09:00 | EUR |

| Eurozone PPI M/M Mar | |

| Actual | 3.40% |

| Consensus | 3.30% |

| Previous | -0.70% |

| Revised | -0.60% |

| 09:00 | EUR |

| Eurozone PPI Y/Y Mar | |

| Actual | 2.10% |

| Consensus | 1.80% |

| Previous | -3% |

| 12:15 | USD |

| ADP Employment Change Apr | |

| Actual | 109K |

| Consensus | 79K |

| Previous | 62K |

| Revised | 61K |

| 14:00 | CAD |

| Ivey PMI Apr | |

| Actual | 57.7 |

| Consensus | 49.9 |

| Previous | 49.7 |

| 14:30 | USD |

| Crude Oil Inventories (May 1) | |

| Actual | -2.3M |

| Consensus | -3.4M |

| Previous | -6.2M |

Sunset Market Commentary

Markets

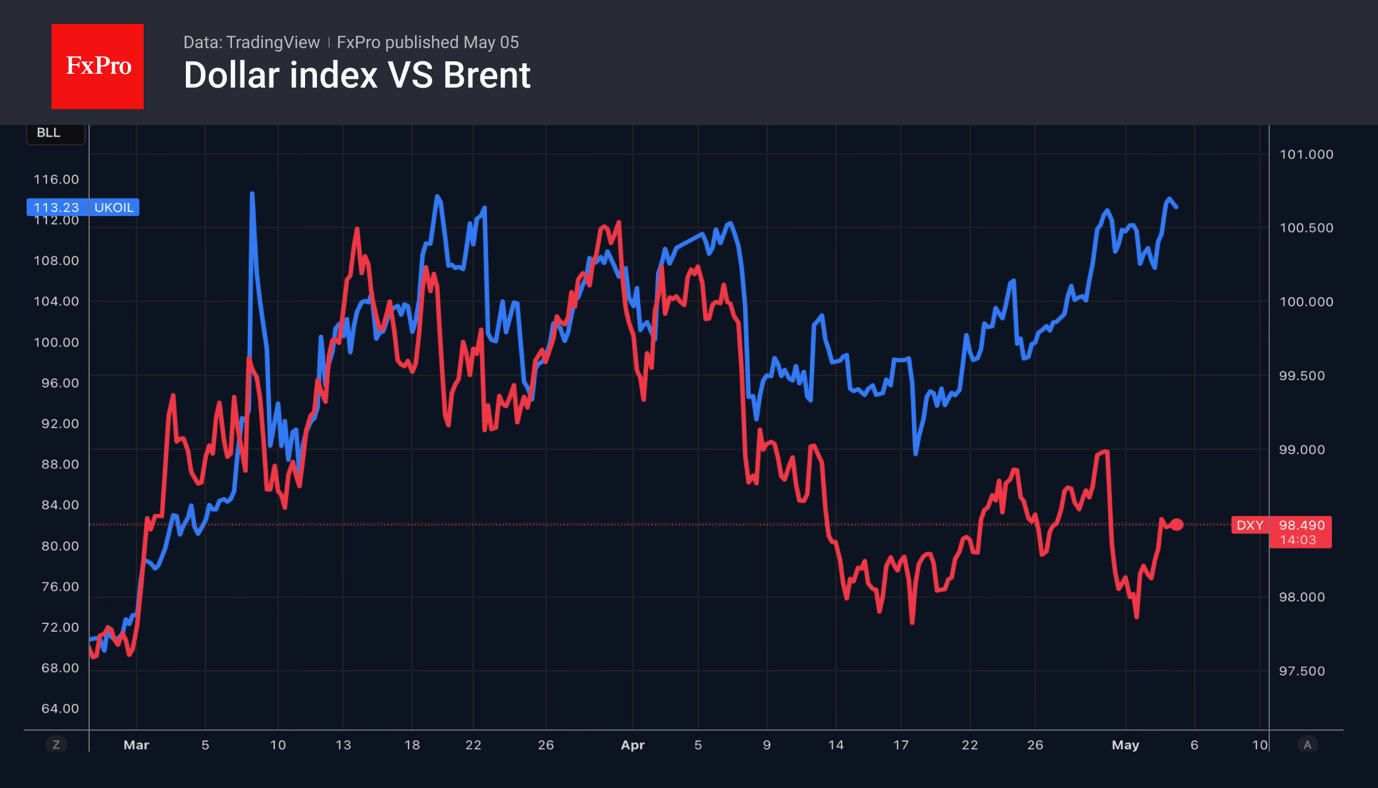

The by-nature fragile ceasefire between the US and Iran was weakened severely by yesterday’s skirmishes in the Persian Gulf but survives so far. US Defense Secretary Hegseth detailed Operation Freedom in a press conference today, calling it a defensive and temporary mission to open up the vital Hormuz Strait and added that while the US is locked and loaded, it isn’t “looking for a fight”. Monday’s developments had pushed Brent oil towards the $115 barrier. Prices ease a bit today to around $112. In a broader perspective, the current actual level of oil prices is perhaps not the worrying part. On a closing basis, they haven’t so far surpassed the pre-ceasefire peak just short of $120. But what is changing is that markets are becoming increasingly concerned on the longer-term fall out of the conflict. There are non-linear consequences tied to the duration of the (oil, fertilizer, helium, LNG …) supply disruption in terms of the time it takes to normalize and inflation. The Brent forward curve is shifting higher by the week with financial markets for example now pricing in an at least $100 price through September this year.

Markets move on the rhythm spelled by oil so we’re seeing core bond yields correct a little lower from yesterday’s surge on the slight drop in Brent today. Bund yields change -4 bps to +0.6 bps in a bull steepening move. Net daily changes in the US vary between -0.8 (30-yr) and -1.4 bps (2-yr). It is telling how ultralong maturities barely respond, highlighting the presence of risk premia. The US 30-yr yield rests at 5%, the German variant is on the verge of reaching new 15-year highs. UK markets were closed yesterday for May Day and are now catching up. Gilt yields rally 10-12 bps. The UK 30-yr yield hit its highest level since 1998. European equity markets recoup some of the 2% losses at the start of the week with gains mounting to 1.4% (EuroStoxx50). US equities open between 0.2 and 1% higher. FX markets are treading water. EUR/USD is flat on the day around 1.17. Same goes for the trade-weighted dollar index around 98.5. The yen is among the few showing some volatility. Drawing conclusions comes with caution since Japanese markets are closed through Wednesday. Last week’s interventions (reportedly) are being further undone for a third day straight. USD/JPY hit a two-month low of 156.6 but has recovered the last couple of trading sessions to 157.8 currently.

The March JOLTS report and April US services ISM were perhaps the only important event from a market point of view today. The headline number printed in line with expectations at 53.6. The new orders component retreated more than expected from March’s 60.6 to 53.5 while the unemployment gauge improved to a still contractionary 48. Prices paid stabilized at a 4-year high of 70.7, defying odds for an uptick to 73.5. March JOLTS job openings at 6.8 million were in line with the readings of the last year so far. Both the USD and yields shrugged at the outcome.

News & Views

The Swiss Statistical office today reported headline inflation in the country in April accelerated to 0.3% M/M and 0.6% Y/Y (from 0.2% M/M and 0.3% Y/Y in March). The monthly rise was due to factors including rising prices for petrol, diesel and heating oil. Prices for air transport also increased, as did international package holidays. Core inflation was unchanged M/M and even eased to 0.3% Y/Y from 0.4%. Especially inflation of domestic products (-0.1% M/M, 0.5% Y/Y) remains very modest which is also visible in subdued services inflation (0.1% M/M and 1.1% Y/Y). Imported good prices accelerated further to 1.5% M/M and 0.9% Y/Y (from 1.8% M/M and -0.3% Y/Y). Goods price deflation is gradually coming to an end (0.6% M/M and -0.2% Y/Y from -0.7%Y/Y). With inflation holding in the lower part of the 0-2% band, the SNB can feel comfortable to hold the policy rate at 0%. A risk-off spike in the franc caused EUR/CHF to test the 0.90 area early March. Strong SNB intervention warnings (and perhaps to be confirmed actual CHF) caused the franc to settle in the 0.915/0.925 trading range over the previous month.

The minority government of Romania led by Ilie Bolojan was toppled after a confidence vote supported by the nationalist far right AUR (Alliance for the Unity of Romanians) and the Social Democrats (PSD). The latter left the collation last month over disagreement with some austerity measures that PM Bolojan introduced to address a 7.65% budget deficit (2025). Reforms were a condition for the country to get access to additional EU funds. The country now faces a (potentially long) period of political uncertainty as it might not be evident for the President to bring together parties that are able/prepared to form a majority in a fractured parliament. The Romanian leu at 5.217 trades near its all-time low against the euro. A 10-y domestic government bond shows a yield near 7.25%.

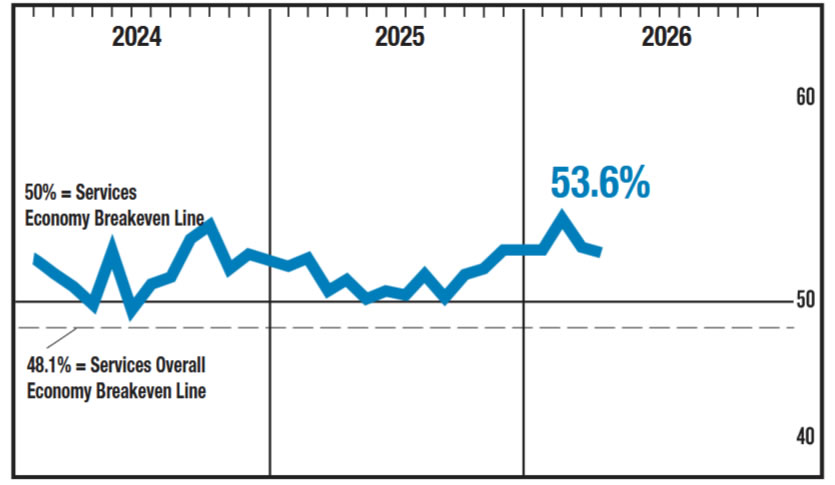

US ISM Services Eases to 53.6, Prices Index Holds Near Multi-Year High

US ISM Services PMI edged down from 54.0 to 53.6 in April, slightly missing expectations of 53.8 but still remaining above the 12-month average of 52.5, indicating continued expansion in the sector. Fourteen industries reported growth, one more than in March, while the number of industries in contraction held steady at three, pointing to a broadly resilient services economy.

Details of the report were mixed but generally supportive. Business activity rose from 53.9 to 55.9, signaling stronger output, while the employment index improved from 45.2 to 48.0, though it remains in contraction territory. The data suggest that while hiring is stabilizing, momentum in services output remains intact.

Inflation pressures remain a key concern. The prices index held at 70.7, its highest level since October 2022, and has stayed above 60 for 17 consecutive months. ISM noted that rising costs for materials such as aluminum, copper, lumber, and petroleum products continue to filter through supply chains, with further upward pressure expected in coming months.

Historically, a PMI reading at this level is consistent with around 1.7% annualized GDP growth.

| Indicator | Previous | Latest | Notes |

|---|---|---|---|

| PMI Services | 54.0 | 53.6 | Slight dip, still expanding |

| Business Activity | 53.9 | 55.9 | Stronger output |

| Employment | 45.2 | 48.0 | Improving but still <50 |

| Prices Index | 70.7 | 70.7 | Highest since Oct 2022 |

FX Confusion as the US Dollar Forms a Double Bottom – Can the Ceasefire Stand? DXY Outlook

- The US Dollar recovered a good part of its losses in the early week, forming a key double-bottom – More upside to come?

- With Oil bouncing back above $105, its correlation with the FX Market picks up again

- US Dollar Index (DXY) in-depth Technical Analysis

The US Dollar regained much of its early-week losses and formed a double-bottom pattern on the charts, making traders question if more gains are ahead. As WTI Crude jumped back above $105, the link between energy prices and the wider FX market is growing stronger again.

After all, if the past session’s speech by Fed’s Williams (the most influential voter at the Federal Reserve) showed elevated concerns about energy prices, there are many reasons to put emphasis on their price rises as traders.

Still, the NY Fed’s president eased the influence of hiking dissents, so for now, this is won’t add to the nascent flame in the Dollar.

WTI Crude and Dollar Index (DXY) Correlation since Late February – Source: TradingView

Many in the market hoped to move past this long conflict.

But after yesterday’s serious geopolitical events, dollar bulls quickly returned to price in the risk of renewed war.

The semi-official Fars Agency reported that Iran launched missiles at US Navy ships in Iranian waters and carried out drone strikes on the UAE.

The US military and Israel are reportedly working together on possible limited responses. With the ceasefire just failing to lead to real diplomatic progress, hopes for peace could soon fall apart.

As a result, the wider FX markets are now at pivotal turning points, with the US Dollar leading the way, so we will look at the currency to spot how it could influence the action.

The Greenback is close to breaking its recent downtrend that followed the ceasefire.

If Crude oil rallies further, especially if it moves above $110, the petrodollar trade could quickly accelerate. Traders should keep a close eye on the war situation to see if any major breakouts are supported by real changes.

FX Performance (09:06 ET) – Source: TradingView. May 5, 2026

We’ll explore a few scenarios for upcoming action in an in-depth technical analysis of DXY.

Dollar Index (DXY) Multi-Timeframe Analysis

Daily Chart

Dollar Index (DXY) Daily Chart. May 5, 2026 – Source: TradingView

The US Dollar is stalling right at the middle of its 96.00 to 100.00 July 2025 range, forming a double bottom after repeatedly failed diplomatic attempts.

The Daily moving averages are now flattening, showing the general confusion across the FX and overall Markets – With the 200-Day MA getting tested in the morning, right at the 98.50 level, traders will want to see if it holds or breaks to power the next moves in currencies.

Let's take a closer look.

4H Chart and Technical Levels

Dollar Index (DXY) 4H Chart. May 5, 2026 – Source: TradingView

The immediate action is tricky:

Sellers are attempting an entry at the downward channel top and 4H 50-period MA, but their momentum is shy.

Two scenarios should help to discern upcoming action.

- Above 98.60, the rally in the dollar confirms, with the next key level entering at 99.00 (and possibility for 99.50)

- Below 98.20, the bear channel holds and this could point to a test of 97.60 in coming days (this would require a lower WTI Crude).

Depending on the bull/bear scenarios, look for trades in FX pairs which provide interesting risk-reward scenarios, including EUR/USD, GBP/USD and GBP/USD – Don't forget to do your own due diligence!

Levels to place on your DXY charts:

Resistance Levels

- 98.50 4H 50-period MA & 200-day MA

- 99.00 4H 200-period MA

- 99.30 to 99.50 Resistance

- 100.00 to 100.50 Main resistance and Range highs

- War Highs 100.544 (Double Top)

Support Levels

- 98.00 Major Support

- Support 97.40 to 97.70 (double bottom level)

- 2025 Lows Major support 96.50 to 97.00 (bear channel lows)

- Range lows at Early 2022 Consolidation just below 96.00

Safe Trades and keep track of the latest headlines!

Canada’s Trade Books Flip to a Surplus in March

Canada's trade balance moved into a $1.8 billion surplus in March, from a $5.1 billion deficit the prior month.

Exports in March surged by 8.5% month-on-month (m/m) following February's sturdy gain. Rapidly rising energy prices pushed crude oil exports up 18.9% m/m, while exports of unwrought gold, silver, and platinum rose by a sizeable 37.7% m/m. Meanwhile, exports of motor vehicles and parts (+4.5% m/m) rose again in March as they continued their recovery from January's depressed level. In total, 7 of 11 product categories registered a gain.

Goods imports decreased by 1.6% m/m in March, paring some of the prior month's robust 9.4% monthly gain, with 8 of 11 subsectors booking a loss. Consumer goods imports (-3.9% m/m) and imports of aircraft and other transportation equipment (-12.8% m/m) contributed most to the monthly decline.

In volume terms, exports edged lower by 0.3% m/m while imports fell by a larger 2.0% m/m.

Canada's merchandise trade surplus with the United States widened from $2.9 billion in February to $7.1 billion in March. Exports to non-U.S. destinations rose by a healthy 9.1% m/m, setting a new all-time high.

Key Implications

March's trade data showed some firming in headline activity, though all of the positive print in exports came from price impacts of higher oil prices. With data up until March in the books, net trade still appears poised to subtract from Q1 2026 real GDP growth, reflecting a broadly stronger quarter for imports. Looking ahead, higher oil prices should meaningfully lift nominal export values into Q2, helping to further improve the trade balance.

The upcoming USMCA renegotiation remains a key near-term risk for Canada. With the July 1st review approaching, renewed engagement between Canadian and U.S. officials is a positive first step, but concrete outcomes remain limited. Our base case continues to assume the agreement stays intact, though elevated uncertainty is likely to restrain business confidence and investment decisions.

Politics is Weighing on the Pound

- Labour risks losing the local elections, which could pressure GBPUSD.

- Japan may be able to afford further currency intervention.

The US dollar capitalised on the pullback in stock indices from record highs and the surge in Brent futures. Buyers of the USD index stepped up their pressure, driven by rising demand for safe-haven assets and a worsening economic outlook in the eurozone amid higher energy prices.

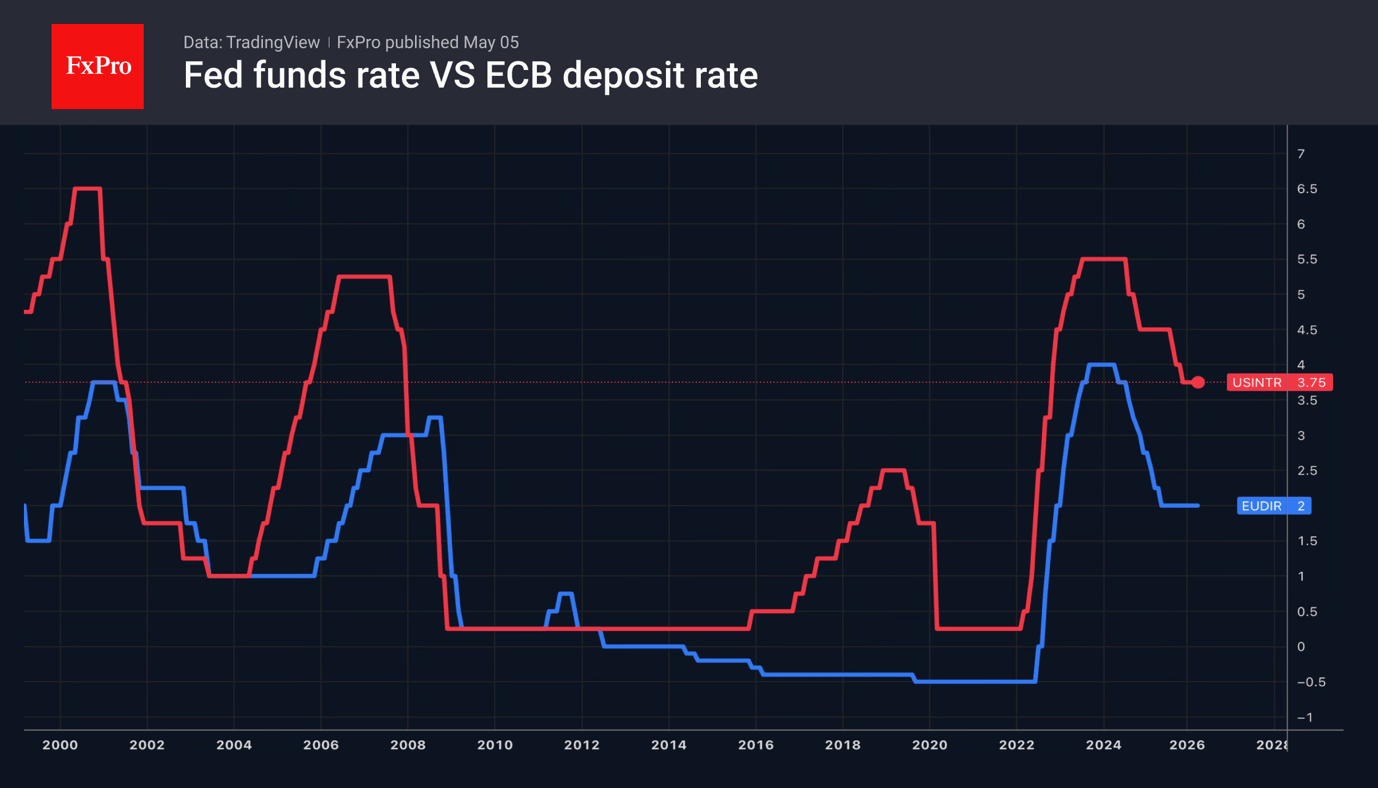

The escalation of the conflict in the Middle East has reignited investor interest in the US dollar as a safe-haven asset. At the same time, oil prices have risen, as have the risks of a surge in US inflation. To combat this, the Fed may raise interest rates this year, with the likelihood of such a move rising from 11% to 32%.

The Bundesbank is prepared to follow the ECB’s path of monetary tightening. According to Bundesbank President Joachim Nagel, the objective is clear: to bring inflation back to 2% in the medium term. If this does not happen, interest rates will have to be raised. Nevertheless, investors view such rhetoric as a ‘hawkish’ bluff. EU Economic Affairs Commissioner Valdis Dombrovskis argues that Europe is facing a stagflationary shock, as high energy prices are pushing the region towards higher inflation and slower GDP growth.

The yen’s appreciation over three consecutive days following currency intervention has prompted the Ministry of Finance to comment on the rules. The IMF regards this entire period as a single episode. Unless there are up to three such episodes within six months, the exchange rate regime will not be changed from a managed float to a free float. This means that Japan may resume selling USDJPY until 5 May.

The escalation in the Middle East and the approaching local elections in Britain are putting pressure on GBPUSD. Labour risks losing the vote due to Keir Starmer’s weakened approval ratings. Rising political uncertainty is driving volatility in the pound and a decline in its exchange rate.