Sample Category Title

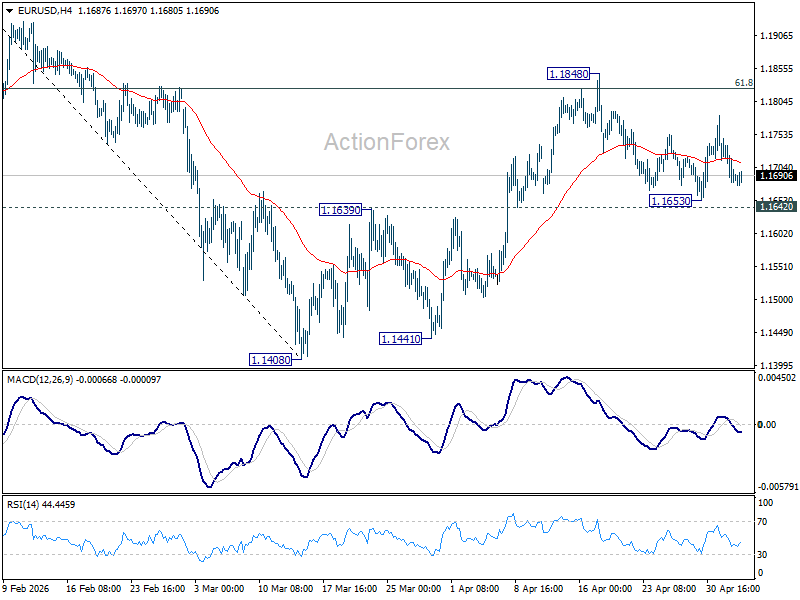

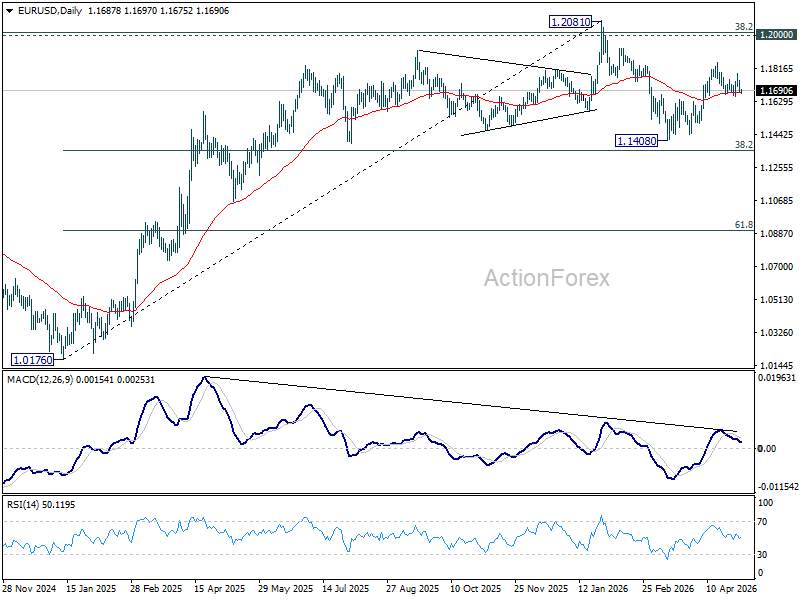

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1664; (P) 1.1707; (R1) 1.1732; More….

Range trading continues in EUR/USD and intraday bias stays neutral. Rise from 1.1408 is expected to continue as long as 1.1642 support holds. Firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

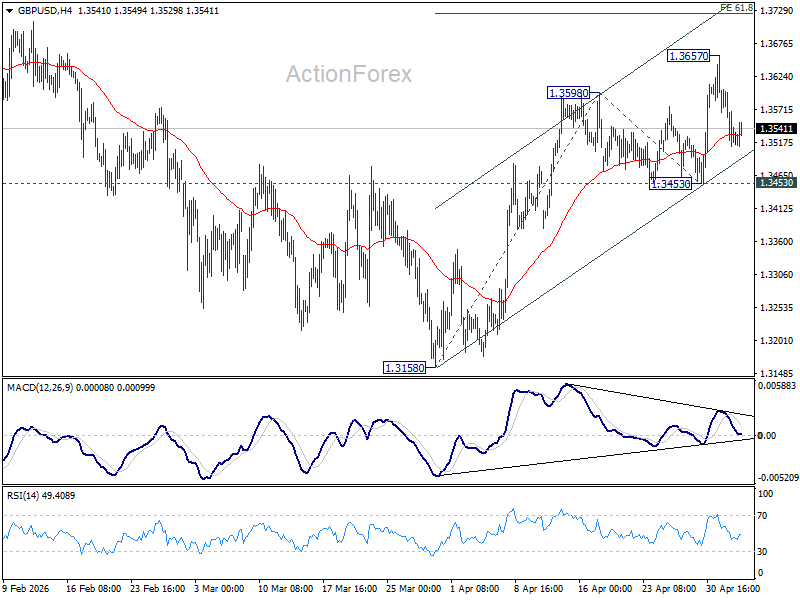

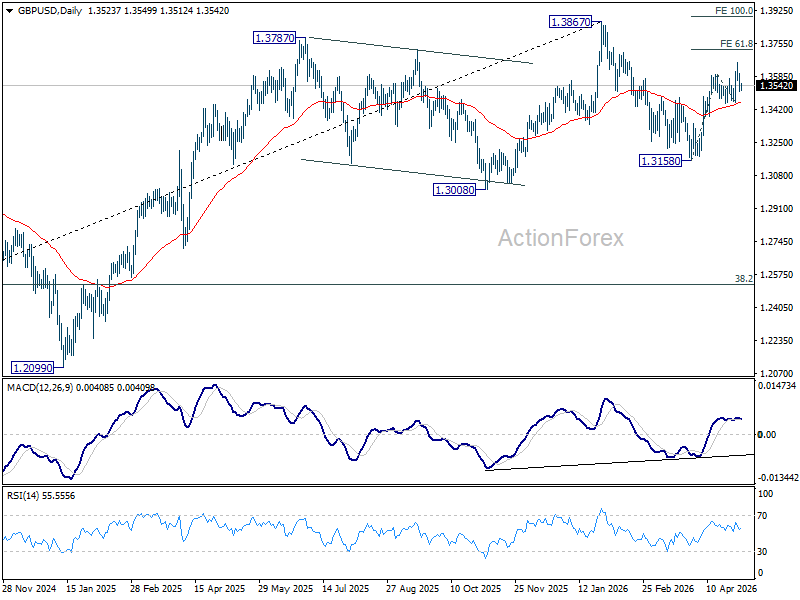

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3542; (P) 1.3601; (R1) 1.3634; More...

Intraday bias in GBP/USD stays neutral as consolidations continue. Further rise is still expected as long as 1.3453 holds. Above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

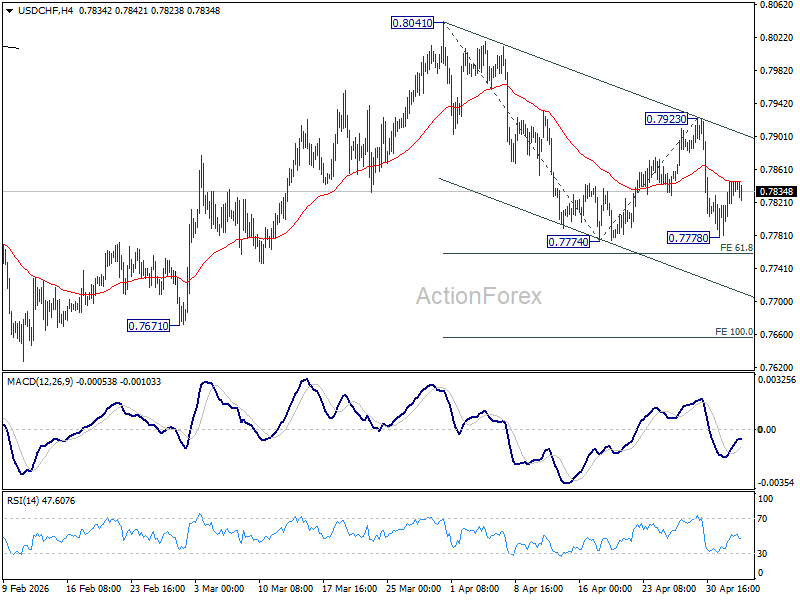

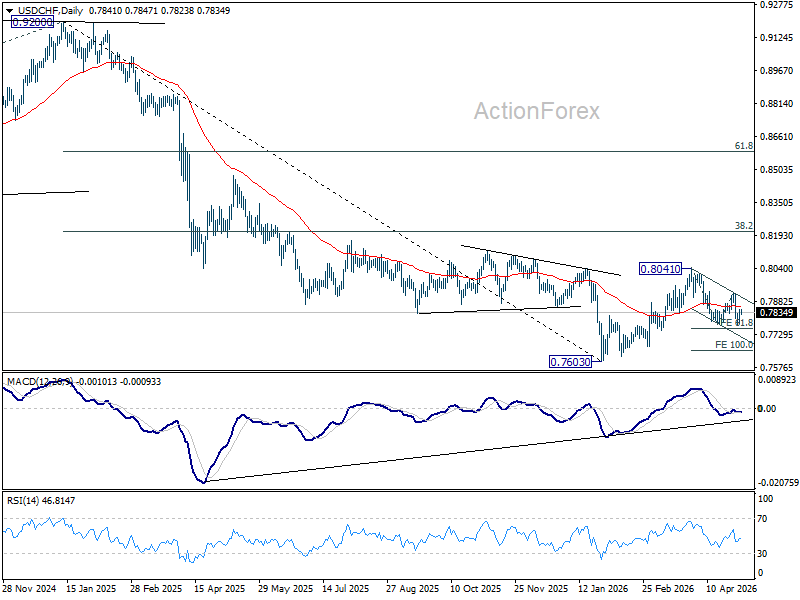

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7808; (P) 0.7829; (R1) 0.7861; More….

USD/CHF is staying in consolidations above 0.7778 and intraday bias remains neutral. Risk will remain on the downside as long as 0.7923 resistance holds. Firm break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will extend the fall from 0.8041 to 100% projection at 0.7656. However, firm break of 0.7923 will turn bias back to the upside for stronger rebound.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

Is USD/JPY Heading Back to 160? Not Yet—Unless Yields Break 4.5% and Oil Hits $120

Is USD/JPY heading back to 160? For now, the answer is no—but the risk is clearly building as global yield dynamics shift and geopolitical tensions intensify. The Yen is back under pressure today, driven primarily by widening rate differentials as US and European yields continue to climb.

The US 10-year Treasury yield has surged above 4.45% and is now approaching the key 4.5% mark, a level that has previously acted as a psychological ceiling. The move is being fueled by a combination of factors: renewed geopolitical tensions in the Middle East, rising inflation concerns linked to higher energy prices, and a shift in Federal Reserve expectations away from rate cuts.

Energy markets remain on high alert as the fragile ceasefire between the US and Iran shows signs of breaking down. Elevated oil prices are reinforcing inflation risks, which in turn are pushing bond yields higher. Markets are increasingly concerned that sustained energy-driven price pressures could delay disinflation and force the Fed to tighten policy again.

This repricing is already visible in interest rate markets. Fed funds futures are now assigning nearly a 30% probability of a rate hike by year-end, while expectations for rate cuts have largely been priced out. The shift marks a significant turnaround in policy expectations and is providing strong support for US yields.

The global yield move is not limited to the US. Germany’s 10-year Bund yield has risen above 3.05%, while the UK 10-year gilt yield has climbed to 5.04%. These moves reflect both the global nature of the inflation shock and the possibility that the ECB and BoE would also need to maintain or even tighten policy at the next meeting.

For the Yen, widening yield differentials are once again driving weakness. USD/JPY has rebounded following last week’s sharp decline, though the current move still appears to be driven more by short covering than fresh directional positioning.

That said, the outlook could change quickly if key thresholds are breached. A sustained move in US 10-year yields above 4.5% would likely trigger a stronger wave of algorithmic selling in the Yen, amplifying upward pressure on USD/JPY. At the same time, a further rise in oil prices toward the $120 level would reinforce inflation fears and strengthen the case for higher global yields.

Intervention risk remains a complicating factor. Japanese authorities are reported to have deployed more than USD 30 billion in last week's operations that helped push USD/JPY back toward the 155 area. Officials have also signaled a willingness to act again, even during the Golden Week holiday period.

However, intervention may prove less effective if underlying market forces intensify. Acting against a backdrop of rising yields and surging oil prices would present a much more difficult challenge. In such a scenario, attempts to stabilize the Yen could slow the move, but are unlikely to reverse the broader trend.

For now, USD/JPY remains contained within last week’s range, suggesting that markets are not yet fully committed to a renewed push higher. But with yields and oil prices approaching key trigger levels, the risk of a move back toward 160 is no longer hypothetical—it is conditional.

For the day so far, Yen is currently the worst performer, followed by Dollar, and then Euro. Kiw is the strongest, followed by Aussie and then Loonie. Sterling and Swiss Franc are positioning in the middle.

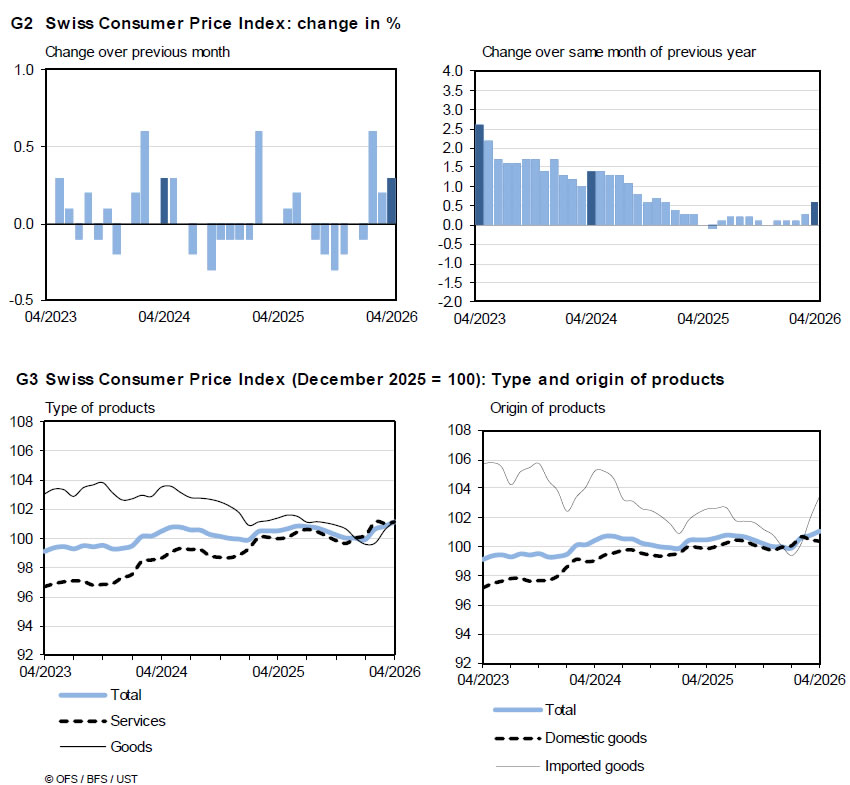

Swiss CPI Accelerates to 0.6% YoY as Energy Import Costs Rebound

A rise in Swiss CPI masks weak underlying inflation. Energy-driven import costs are lifting headline prices, but core inflation is flat and domestic pressures are subdued. The trend suggests limited internal inflation momentum. Read More.

RBA Hikes to 4.35%, Signals It’s Not Done Yet

RBA raise interest rate as expected, and signaled a clear shift to higher-for-longer policy. Inflation is now expected to peak higher and fall more slowly, while growth forecasts are being downgraded. With rates projected near 4.7% through 2028, the central bank is preparing for a prolonged fight against persistent price pressures. Read more.

Gold Slides on Hormuz Attacks, 4,400 Breakdown in Focus, 4,000 Next

Gold is under renewed pressure as Hormuz tensions escalate and oil prices surge. Iran’s attacks on ships and a UAE oil port have intensified supply fears, lifting the Dollar and shifting focus back to inflation risks. With 4,400 support now under threat, a breakdown could accelerate the slide toward the 4,000 level. Read More.

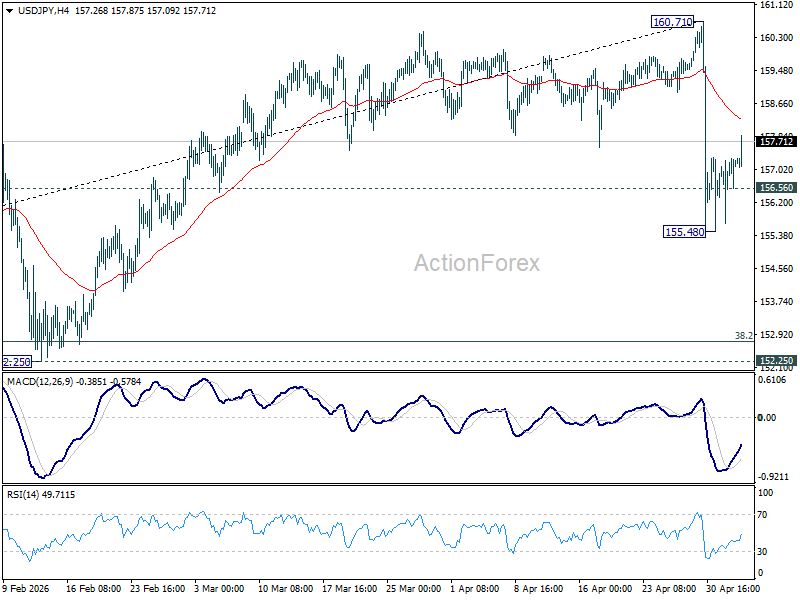

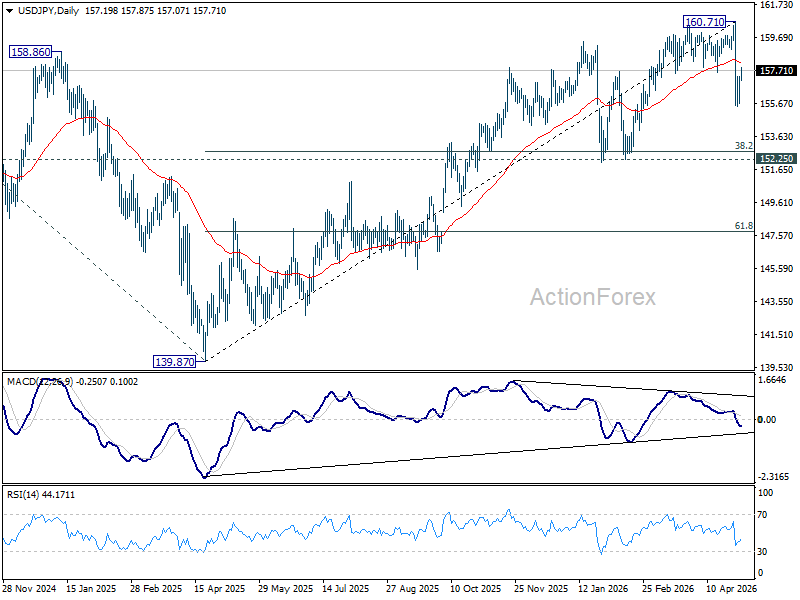

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.22; (P) 156.76; (R1) 157.79; More...

USD/JPY's recovery from 155.48 accelerates higher today, but it stays below 55 4H EMA (now at 158.27). Intraday bias remains neutral and further decline is still in favor. Below 156.55 minor support will bring retest of 155.48. Break there will extend the fall from 160.71 and target 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). However, sustained break of the 55 4H EMA will bring stronger rebound back to retest 160.71 high.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.03) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.22; (P) 156.76; (R1) 157.79; More...

USD/JPY's recovery from 155.48 accelerates higher today, but it stays below 55 4H EMA (now at 158.27). Intraday bias remains neutral and further decline is still in favor. Below 156.55 minor support will bring retest of 155.48. Break there will extend the fall from 160.71 and target 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). However, sustained break of the 55 4H EMA will bring stronger rebound back to retest 160.71 high.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.03) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

ETH/USD: Corporate Demand For the Coin Is Rising

According to Santiment, in early May large holders acquired more than 140,000 ETH within 96 hours. This demand is forming against a backdrop of growing corporate interest in Ethereum as a reserve asset: Bitmine Immersion Technologies holds over 5 million ETH. At the same time, an opposing trend is emerging: total assets under management in ETH-focused ETPs and ETFs amount to around $16 billion; however, at the beginning of 2026 the ETF segment experienced a period of subdued activity, with interest only starting to recover by April (source: CoinLaw).

Technical Picture

On the daily chart, an extended downward structure is evident: since early October 2025, the price has been declining within a descending channel, reaching a culmination in early February 2026 near the $1,750 level. Vertical volume during this period showed peak values, signalling the exhaustion of selling pressure. This was followed by a rebound: the price broke above the upper boundary of the channel and, during subsequent trading, formed a horizontal volume zone in the $1,920–$2,240 range, where the bulk of transactions over the period was concentrated. The point of control (POC) of this volume zone lies around $2,050–$2,100.

The price is currently trading above this zone, indicating a shift in favour of buyers. Support at $1,800 coincides with the February low from which the reversal began. Above current levels lies a resistance area near $2,500 — a zone the price approached in April but failed to consolidate above the round level. The RSI + MAs indicator shows readings of 57, 54 and 54: the oscillator is positioned above neutral, while the moving averages remain broadly neutral.

Key Takeaways

The technical profile reflects a transition from a prolonged downtrend to a consolidation phase above the volume zone. Further movement will depend on whether corporate demand for ETH can provide a sufficient basis to sustain a move towards the resistance area.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service (additional fees may apply). Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Bitcoin Has Begun Hunting Down Short Sellers

Market Overview

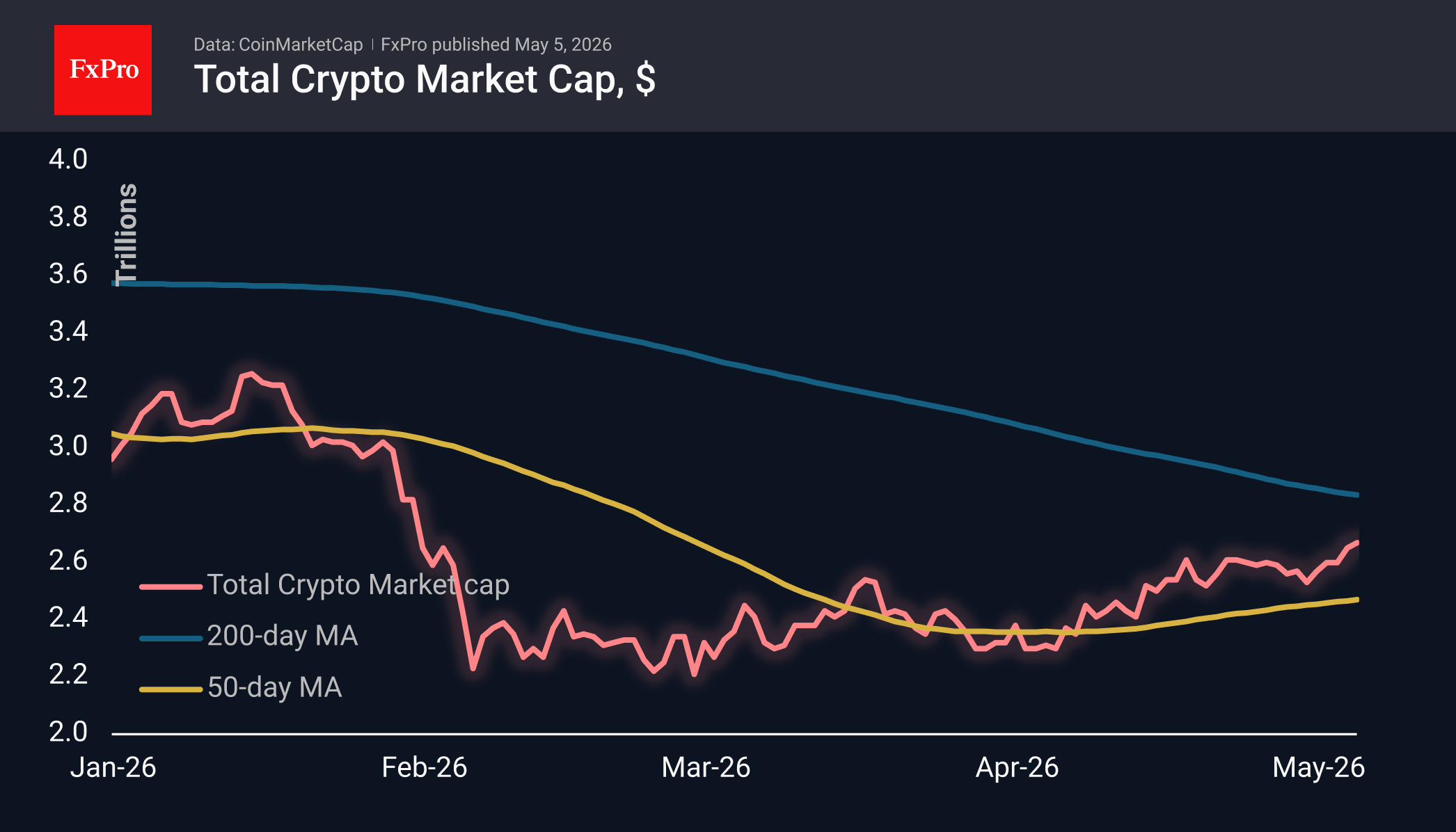

The crypto market capitalisation has continued to hit new highs since early February, reaching $2.67 trillion. This time, the movement was not uniform, consisting of individual surges led by Toncoin (+29%), followed by Algorand (+4.5%) and Basic Attention (+4%). The underperformers include Dash (-5.5%), Aptos (-2.1%) and VeChain (-1.6%).

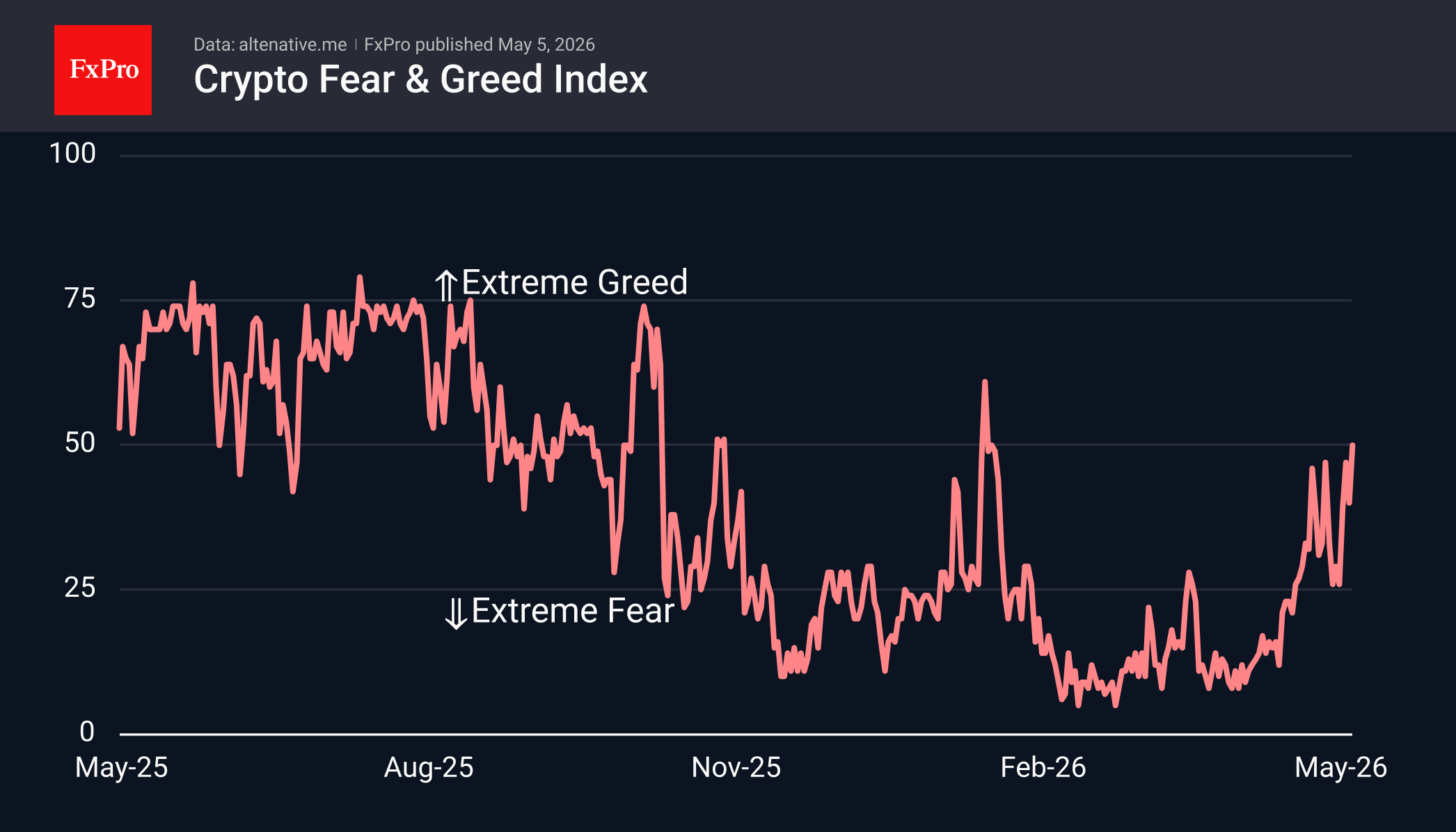

The sentiment index has reached 50, the midpoint of the indicator’s range, where it last stood on 17 January. The market is approaching a significant turning point. Since last October, there have been only brief surges in sentiment to higher levels, but these have provided excellent opportunities for bears to sell at higher prices.

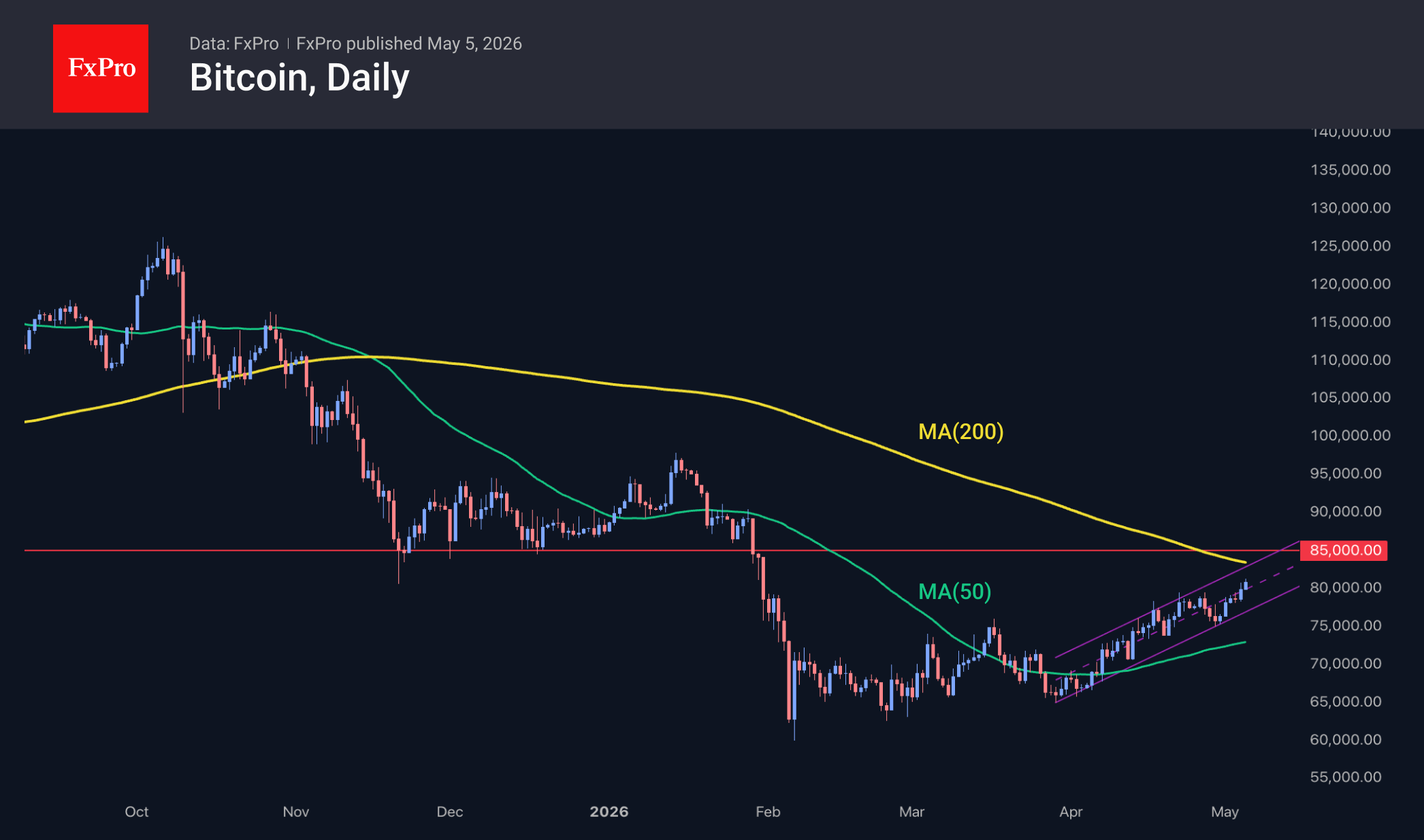

Although Bitcoin faced some pressure midday on Monday, it overcame it on Tuesday, reaching $81K and gaining 1.3% for the day, though, by and large, it covered this ground in just the last 4 hours. We attribute this rally to short squeezes, as the rise occurred during the period of the most aggressive movements ahead of the start of active trading in Asia, when liquidity is at its lowest. Meanwhile, on the stock markets, there was only a slight pullback following the downward momentum. In any case, on the daily charts, Bitcoin is recording its sixth bullish candle, and the entire April uptrend now fits within a new upward channel, with the upper boundary currently at the 200-day moving average.

News Background

The Capriole investment fund has noted a sharp rise in demand for Bitcoin from major players. Institutional investors are buying up more than 500% of the daily mining output of the leading cryptocurrency every day. Historically, such a supply shortage has led to a 24% rise in BTC over the following month.

Bitcoin appears poised for an upward surge. A break above $80K opens up the possibility of reaching $86K0–$88K in the coming period, notes MN Trading founder Michael van de Poppe.

Following the latest adjustment, Bitcoin’s mining difficulty has fallen by 2.3% to 132.47 T. According to Glassnode, the network’s average hash rate, smoothed by a 7-day moving average, stands at around 955 EH/s.

Senators Tom Tillis and Angela Olsbrooks have reached a compromise regarding stablecoin yields in the CLARITY Act. This bill regulating the US crypto market may be considered by the Senate Banking Committee in the week following 11 May.

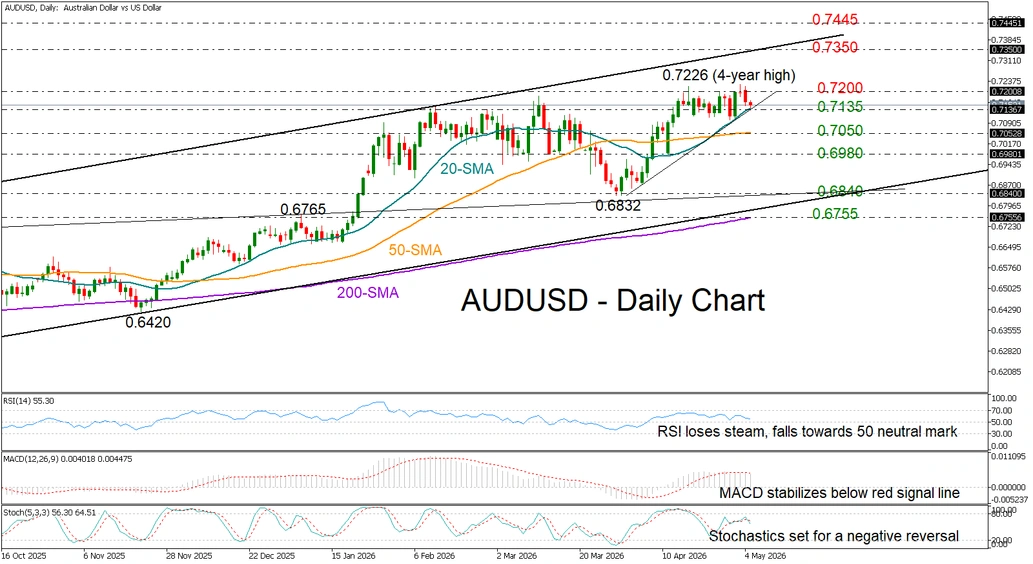

AUD/USD Slips to 20-SMA After RBA Rate Hike

- AUD/USD loses ground as RBA meets rate hike expectations.

- Short-term risk is tilted to the downside.

- A close below 20-SMA could extend decline.

AUD/USD retreated to 0.7134, extending Monday’s losses after the Reserve Bank of Australia (RBA) delivered its third consecutive rate increase, as expected, to quell inflation while signaling a data-dependent approach for future policy actions. A relatively firmer dollar, amid escalating tensions in the Middle East, added extra pressure on the pair.

Technically, the pullback emerged after the 0.7200 bar stood firm once again near four-year highs, bringing the 20-day simple moving average (SMA) at 0.7135 back into view. A break lower would put April’s upleg into question, shifting the spotlight toward the 50-day SMA at 0.7050. Should the sell-off extend beyond 0.6980, the next pivot point could come at the March low of 0.6840.

Given the negative trajectory in the RSI and the MACD, there is limited optimism for short-term acceleration. Nevertheless, if the bulls reclaim the 0.7200 level and revive the 2025 uptrend, the door could open toward the ascending trendline connecting the 2025 and 2026 highs, currently seen near 0.7350. The 0.7445 resistance taken from April 2025, could be the next destination.

In summary, AUD/USD appears to be losing bullish momentum in the short-term picture as it tests a key support area around 0.7135. Failure to hold this level could trigger another wave of selling.

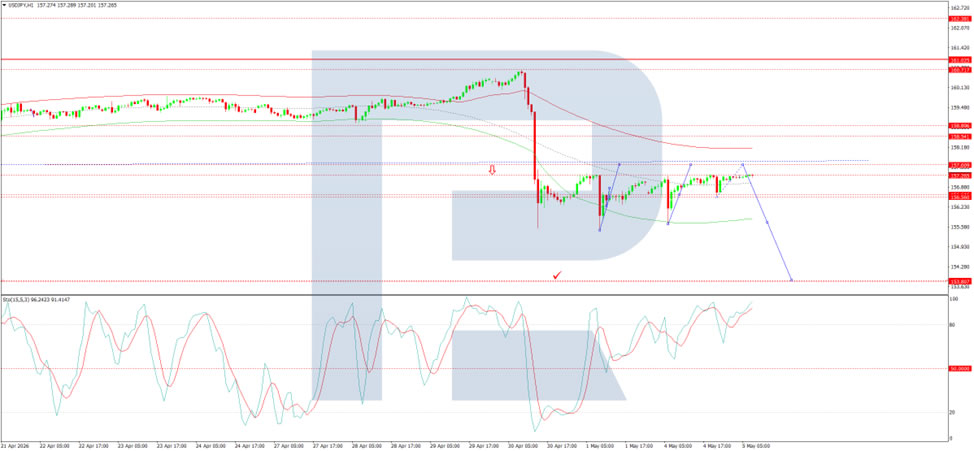

Yen Weakens as Demand for the US Dollar Returns

USD/JPY held near 157.22 on Tuesday following a volatile start to the week. Pressure on the Japanese yen has increased as demand for the US dollar has returned, with investors once again favouring the greenback as a defensive asset. The move comes amid renewed tensions in the Middle East, which threaten the fragile truce between the US and Iran.

The renewed escalation around the Strait of Hormuz has pushed energy prices higher and reignited inflation concerns. In turn, this has supported the US dollar by increasing expectations that the Federal Reserve may need to maintain a tighter monetary stance for longer.

At the same time, markets remain cautious following Japan’s suspected currency intervention last week, which triggered a sharp rebound in the yen. Market estimates suggest Tokyo may have spent as much as USD 35 billion, although the authorities have yet to confirm any direct action.

Investors continue to price in the risk of further intervention. Japan has historically preferred to act during periods of thinner liquidity and has often intervened in waves, helping to sustain elevated volatility across the foreign exchange market.

Technical Analysis

On the H4 chart, USD/JPY is trading within a consolidation range around 156.50 and is now moving towards 157.60. This level remains the immediate upside target. Once reached, a corrective move lower may begin, with scope for a decline towards 153.80 and potentially 153.00 thereafter. The MACD supports this scenario, with its signal line below zero but pointing firmly upwards, indicating that bullish momentum is still building in the short term before a broader correction may emerge.

On the H1 chart, the market is attempting a breakout above 157.26. A further push higher towards 157.60 is likely in the near term. After that, a pullback towards 155.77 may follow, with the potential for the decline to extend to 153.80. The Stochastic oscillator supports this view, with its signal line above 80, indicating overbought conditions and suggesting that short-term downside pressure may begin to build once the current upward move fades.

Conclusion

USD/JPY remains supported by renewed demand for the US dollar amid heightened geopolitical tensions and inflation concerns, strengthening the greenback’s defensive appeal. However, the risk of renewed intervention from Japan continues to cap upside potential, leaving the pair vulnerable to sharp reversals despite the near-term bullish bias.

Swiss CPI Accelerates to 0.6% YoY as Energy Import Costs Rebound

Swiss inflation picked up modestly in April, with headline CPI rising 0.3% month-on-month, driven largely by higher energy and travel-related costs. According to the Federal Statistical Office, increases in petrol, diesel and heating oil prices were key contributors, alongside higher airfares and international package holidays.

The underlying picture remains subdued. Core CPI was flat on the month, while domestic product prices slipped by -0.1% mom, pointing to limited internal price pressures. In contrast, imported product prices jumped 1.5% mom, highlighting that the recent pickup in inflation is being driven primarily by external cost factors rather than domestic demand.

On an annual basis, CPI rose from 0.3% yoy to 0.6% yoy, while core inflation edged lower from 0.4% yoy to 0.3% yoy. Domestic price growth remained unchanged at 0.5% yoy, but imported inflation rebounded sharply from -0.3% yoy to 0.9% yoy.

The data suggest that Switzerland’s inflation remains low overall, with the latest increase largely reflecting rising import costs linked to energy rather than broad-based price pressures.

| Indicator | Previous | Latest |

|---|---|---|

| CPI (YoY) | 0.3% | 0.6% |

| Core CPI (YoY) | 0.4% | 0.3% |

| Domestic Prices (YoY) | 0.5% | 0.5% |

| Imported Prices (YoY) | -0.3% | 0.9% |