Sample Category Title

Dollar Firm Ahead of NFP, Can Jobs Data Fuel Further Gains?

Dollar continues to dominate the currency markets this week, holding its position as the strongest performer as focus shifts to the upcoming non-farm payroll report from the US. Market reactions to this data will be crucial in shaping financial movements leading up to FOMC rate decision in November. If the employment figures support a standard 25bps rate cut by Fed, risk markets may respond negatively, giving a significant boost to the greenback. Dollar is attempting to reverse its third-quarter losses against major rivals, and supportive NFP data could further enhance this momentum.

Overall in the currency markets, Yen remains the weakest currency this week, influenced by diminishing expectations of a December rate hike by BoJ. Kiwi follows as the second weakest, pressured by firm expectations of a 50 bps rate cut by RBNZ next week. Sterling is the third worst performer after BoE Governor Andrew Bailey raised the possibility of aggressive rate cuts ahead. However, there is prospect for the Pound to rebound significantly if BoE Chief Economist Huw Pill sings a different tune in his speech today.

On the other hand, Canadian Dollar stands as the second strongest currency after the greenback, supported by the rally in oil prices. Developments in the Middle East—specifically whether the US and Israel would strike Iranian oil facilities—are critical factors that could influence the next move in oil prices and, consequently, the Loonie. Aussie is the third strongest, although its upward momentum has slowed as the rally in Hong Kong stock markets pauses. Aussie would await guidance from the reopening of Chinese markets after the holiday next week. Meanwhile, Swiss Franc and the Euro are positioned in the middle of the pack.

Technically, EUR/USD is sitting on an important cluster support level at 1.1001 (38.2% retracement of 1.0665 to 1.1213 at 1.1004). Strong bounce from current level will retain near term bullishness for rallying through 1.1213 and 1.1274 high in the near term. However, decisive break of 1.1001/4 will argue that whole rise from 1.0665 has completed, and risk deeper fall to 61.8% retracement at 1.0874, and possibly below. The market's reaction today will likely set the tone for EUR/USD's next major move.

In Asia, at the time of writing, Nikkei is up 0.20%. Hong Kong HSI is up 1.79%. China is still on holiday. Singapore Strait Times is up 0.17%. Japan 10-year JGB yield is up 0.0509 at 0.878. Overnight, DOW fell -0.44%. S&P 500 fell -0.17%. NASDAQ fell -0.04%. 10-year yield rose 0.065 to 3.850.

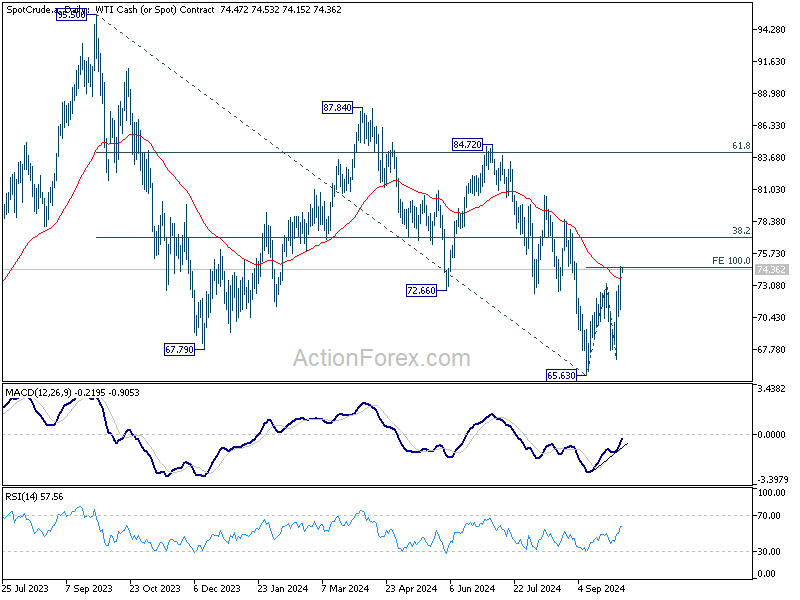

Oil prices rise as US strikes on Iran oil sites, but no runaway rally yet

Oil prices surged as escalating tensions in the Middle East have raised fears of supply disruptions. US President Joe Biden confirmed that he is considering airstrikes on Iran’s oil facilities in retaliation for Tehran’s missile attack on Israel. The growing conflict, already being described as the most severe in the region since the Gulf War, has fueled a sharp rise in oil prices throughout the week. However, the rally has yet to become "runaway", largely due to OPEC+ holding significant spare capacity, which could be deployed to stabilize the market if needed.

Technically, while WTI's breach of 55 D EMA is a near term bullish sign, the upside is so far capped by 10% projection of 65.63 to 73.23 from 66.97 at 74.57. Rebound from 65.63 is still seen as a corrective recovery for now. Break of 70.47 minor support will argue that the recovery has completed, and the larger down trend is ready to resume through 65.63 low.

However, decisive break of 74.57 could prompt upside acceleration through key fibonacci level at 38.2% retracement of 95.50 (2023 high) to 65.63 at 77.04. In this case, WTI could be reversing the whole fall from 95.50 and target 61.8% retracement at 84.08.

NFP to back 25bps Fed rate cut in Nov?

The September non-farm payroll report is in sharp focus today, as it plays a critical role in shaping expectations for Fed's upcoming monetary policy decisions. Currently, markets are pricing in 33% probability of a 50bps rate cut in November, with 67% chance of a 25bps cut. These odds have shifted notably from a week ago, when the probability of a 50bps cut stood at 50%, following comments from Fed Chair Jerome Powell, who indicated two more "normal-sized" cuts are likely by year-end.

It's important to recall that Fed's larger-than-usual 50bps rate cut in September was primarily a "catch-up) to their inaction in July. Many Fed officials believed that July would have been a more opportune time to initiate the easing cycle, had they had access to subsequent economic data. Therefore, barring any significant negative surprises in today's NFP report, Fed is likely to adhere to its current plan outlined in the dot plot, implementing two additional 25 bps cuts in November and December respectively.

NFP is expected to show an increase of approximately 140k in September, with the unemployment rate remaining steady at 4.2%. Average hourly earnings are projected to slow to a month-over-month growth of 0.3%.

Recent related data offers mixed signals: ISM Manufacturing Employment Index declined sharply from 46.0 to 43.9, and ISM Services Employment Index also fell from 50.2 to 48.0. ADP employment report showed private sector job gain of 143k. Four-week moving average of initial jobless claims decreased slightly from 230,000 to 224,000.

Overall, these indicators suggest that while job growth remains robust, the likelihood of a significant upside surprise in today's NFP release is low.

Risk sentiment and the market’s reaction to the NFP will be pivotal in shaping financial markets for the remainder of October, including currency movements.

Technically, NASDAQ is clearly losing momentum, as seen in 55 D MACD, after hitting 18327.33. Decisive break of 55 D EMA (now at 17587.55) will argue that rebound from 15708.53 has completed. In the bearish case, the corrective pattern from 18671.06 high could have already started the third leg, back towards 15708.53 and possibly below.

Looking ahead

Swiss unemployment rate, France industrial production, Italy retail sales, and UK PMI construction will be released in European session. Later in the day, US NFP will take center stage. Canada will release Ivey PMI.

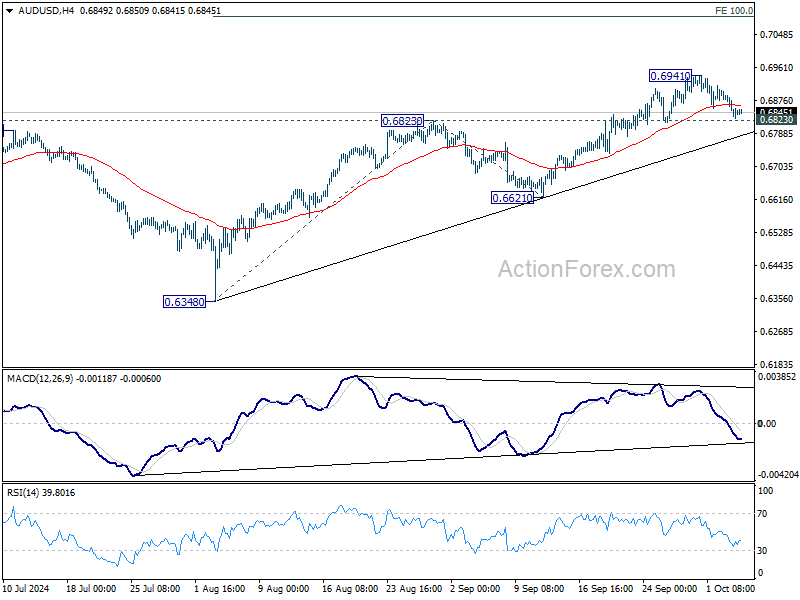

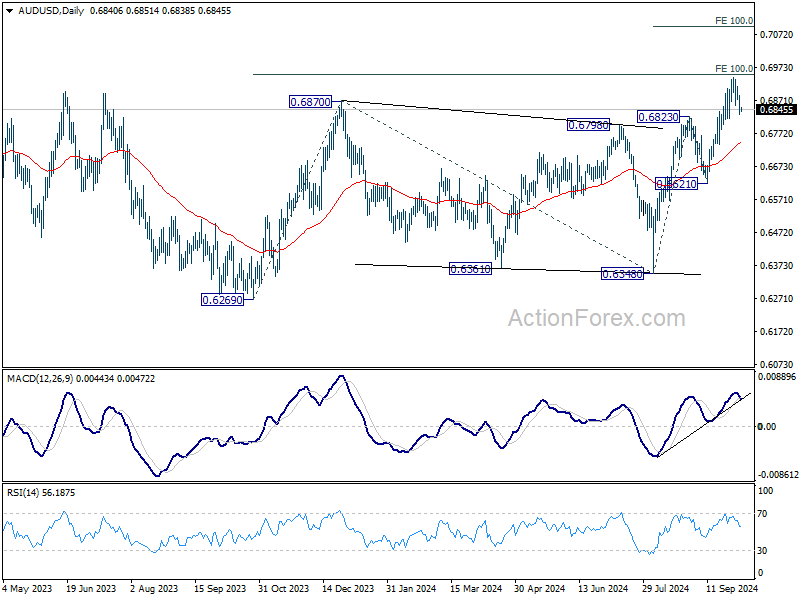

AUD/USD Daily Report

Daily Pivots: (S1) 0.6818; (P) 0.6853; (R1) 0.6877; More...

Intraday bias in AUD/USD remains neutral for the moment. Further rally is still in favor as long as 0.6823 resistance turned support holds. Above 0.6941 will resume the rise from 0.6348 to 100% projection of 0.6348 to 0.6823 from 0.6621 at 0.7096. However, firm break of 0.6823 will indicate rejection by 0.6941 medium term fibonacci level. Intraday bias will be turned back to the downside for 55 D EMA (now at 0.6742) and possibly below.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

NFP to back 25bps Fed rate cut in Nov?

The September non-farm payroll report is in sharp focus today, as it plays a critical role in shaping expectations for Fed's upcoming monetary policy decisions. Currently, markets are pricing in 33% probability of a 50bps rate cut in November, with 67% chance of a 25bps cut. These odds have shifted notably from a week ago, when the probability of a 50bps cut stood at 50%, following comments from Fed Chair Jerome Powell, who indicated two more "normal-sized" cuts are likely by year-end.

It's important to recall that Fed's larger-than-usual 50bps rate cut in September was primarily a "catch-up) to their inaction in July. Many Fed officials believed that July would have been a more opportune time to initiate the easing cycle, had they had access to subsequent economic data. Therefore, barring any significant negative surprises in today's NFP report, Fed is likely to adhere to its current plan outlined in the dot plot, implementing two additional 25 bps cuts in November and December respectively.

NFP is expected to show an increase of approximately 140k in September, with the unemployment rate remaining steady at 4.2%. Average hourly earnings are projected to slow to a month-over-month growth of 0.3%.

Recent related data offers mixed signals: ISM Manufacturing Employment Index declined sharply from 46.0 to 43.9, and ISM Services Employment Index also fell from 50.2 to 48.0. ADP employment report showed private sector job gain of 143k. Four-week moving average of initial jobless claims decreased slightly from 230,000 to 224,000.

Overall, these indicators suggest that while job growth remains robust, the likelihood of a significant upside surprise in today's NFP release is low.

Risk sentiment and the market’s reaction to the NFP will be pivotal in shaping financial markets for the remainder of October, including currency movements.

Technically, NASDAQ is clearly losing momentum, as seen in 55 D MACD, after hitting 18327.33. Decisive break of 55 D EMA (now at 17587.55) will argue that rebound from 15708.53 has completed. In the bearish case, the corrective pattern from 18671.06 high could have already started the third leg, back towards 15708.53 and possibly below.

Oil prices rise as US strikes on Iran oil sites, but no runaway rally yet

Oil prices surged as escalating tensions in the Middle East have raised fears of supply disruptions. US President Joe Biden confirmed that he is considering airstrikes on Iran’s oil facilities in retaliation for Tehran’s missile attack on Israel. The growing conflict, already being described as the most severe in the region since the Gulf War, has fueled a sharp rise in oil prices throughout the week. However, the rally has yet to become "runaway", largely due to OPEC+ holding significant spare capacity, which could be deployed to stabilize the market if needed.

Technically, while WTI's breach of 55 D EMA is a near term bullish sign, the upside is so far capped by 10% projection of 65.63 to 73.23 from 66.97 at 74.57. Rebound from 65.63 is still seen as a corrective recovery for now. Break of 70.47 minor support will argue that the recovery has completed, and the larger down trend is ready to resume through 65.63 low.

However, decisive break of 74.57 could prompt upside acceleration through key fibonacci level at 38.2% retracement of 95.50 (2023 high) to 65.63 at 77.04. In this case, WTI could be reversing the whole fall from 95.50 and target 61.8% retracement at 84.08.

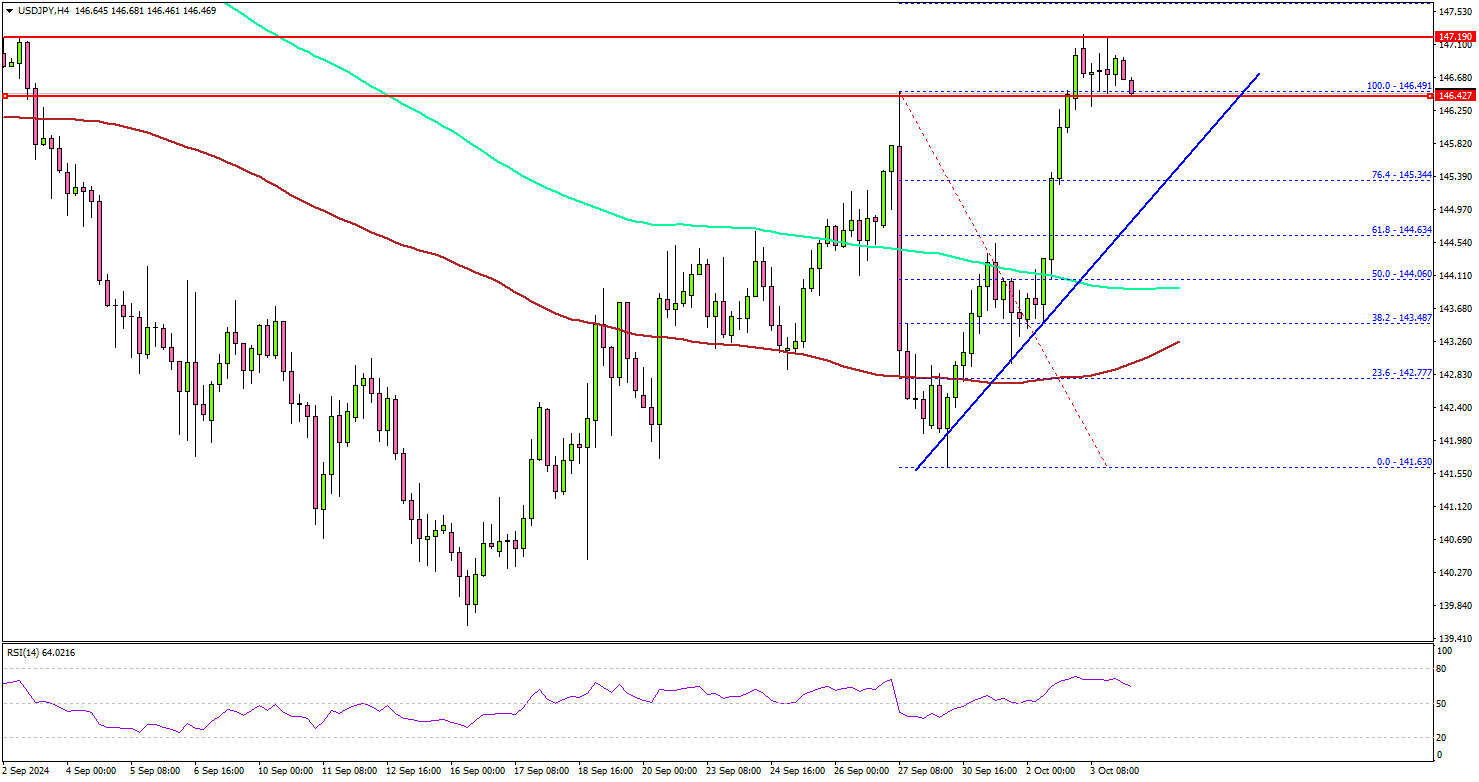

USD/JPY Restarts Its Rally, US Nonfarm Payrolls Report Next

Key Highlights

- USD/JPY started a fresh increase above the 145.00 resistance.

- A key bullish trend line is forming with support at 145.80 on the 4-hour chart.

- EUR/USD declined below the 1.1075 support level.

- GBP/USD trimmed gains and traded below the 1.3200 support level.

USD/JPY Technical Analysis

The US Dollar formed a base above 141.65 and started a fresh increase against the Japanese Yen. USD/JPY broke the 142.50 and 143.00 levels to turn positive.

Looking at the 4-hour chart, the pair gained bullish momentum above the 145.00 resistance zone, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The pair surpassed the 76.5% Fib retracement level of the downward move from the 146.49 swing high to the 141.63 low. It is now attempting more gains above the 147.20 level. On the upside, the bears might be active near the 147.50 level.

A close above the 147.50 level could set the tone for another increase. The next major resistance could be 148.00. A clear move above the 148.00 level might send USD/JPY toward 149.20. Any more gains might call for a test of the 150.00 zone.

On the downside, immediate support sits near the 145.80 level. There is also a key bullish trend line forming with support at 145.80 on the same chart, below which the pair might test 145.20.

The next key support sits near the 143.65 level and the 200 simple moving average (green, 4-hour). Any more losses could send the pair toward the 100 simple moving average (red, 4-hour) at 143.20.

Looking at EUR/USD, the pair failed to start a fresh increase and saw a downside break below the 1.1075 support zone.

Upcoming Economic Events:

- US nonfarm payrolls for Sep 2024 – Forecast 140K, versus 142K previous.

- US Unemployment Rate for Sep 2024 - Forecast 4.2%, versus 4.2% previous.

Cliff Notes: Policy’s Impact Being Felt

Key insights from the week that was.

In Australia, the week began with the Federal Government’s announcement of a better-than-expected final budget outcome for 2023/24, a second consecutive surplus of $15.8bn. Relative to May’s estimates, the outcome was driven mostly by fewer payments, associated with delays in outflows to states and other programs, although receipts were also lower than expected too, reflecting a softening labour market. The budget has been in a temporary ‘sweet spot’, banking the windfalls associated with bracket creep, high commodity prices and high inflation. However, these are temporary dynamics; with inflation pressures fading and commodity prices falling – driving a narrowing in goods trade surplus since 2022 – forward estimates have the budget set to tip back into deficit.

Over the past two years, bracket creep has acted as a major drag on households’ disposable income growth, seeing consumer spending slow in official data. It was therefore encouraging to see retail sales bounce higher in August, up 0.7% (3.1%yr). While this may be partly explained by warmer-than-usual weather, the onset of Stage 3 tax cuts seems like the more likely culprit behind the larger increase – a lagged effect that is consistent with tax cuts through recent history.

While Stage 3 tax cuts are set to give back around $23bn in bracket creep, it has had a relatively muted impact on spending thus far, a conclusion that has been echoed in Westpac’s latest card activity data up to mid-September. More broadly, against the backdrop of persistent cost-of-living pressures and rapid population growth over the past two years, real (inflation-adjusted) spending remains quite weak on a per capita basis, suggesting that it will likely take some time before a meaningful pick-up in consumption takes hold.

Diverging trends across the states also remained an important theme in the latest CoreLogic data; underlying the 6.7%yr lift nation-wide house prices in September is a wide range of outcomes, from –1.4%yr in Melbourne up to 24.1%yr in Perth. The tight supply-demand balance across medium-sized capital cities is having a clear impact on affordability; and, in a context where dwelling approvals are showing a few signs of sustainable upwards momentum (WA being the only exception), risks around residential construction activity remain front-of-mind, once existing projects are worked through.

Offshore, escalation of the conflict in the middle east and US data was in focus. Comments from FOMC Chair Jerome Powell provided a positive view for the US economic outlook highlighting that the FOMC “is not a committee that feels like it's in a hurry to cut rates quickly”. He also noted that a further deterioration in labour market conditions is not required to achieve the Fed’s inflation target. Economic data, released so far this week, was consistent with greater stability in the US labour market. Most notably, this week’s JOLTS report showed that the job openings recovered in August rising above 8mn after two months below that level. While the hiring rate ticked down from 3.4% to 3.3%, a bottom of the recent range, the separation rate decreased more sharply, to a multi-year low of 3.1%. Against this backdrop, all eyes are on the release of the US labour market report out later tonight, it is expected to show that the non-farm payrolls rose at a similar pace to that seen in August, by 150k.

The September manufacturing and services ISM PMIs were mixed once again highlighting diverging trends in the two sectors in the US. The manufacturing index disappointed, with the headline index coming in unchanged at 47.2, the second lowest level this year and well below historical average. Meanwhile, the services ISM index increased by 3.4pt to 54.9, the highest reading in nineteen months. The employment component was significantly weaker dipping back below 50 after two months in the expansionary territory. Prices paid were up for a third consecutive month to 59.4, the highest level since the start of the year.

Across the pond, European prices eased to 1.8%yr in September off the back of lower energy prices marking the first sub-2% reading of this cycle. Services inflation remained sticky at 4.1%. Commentary by ECB staff through the week suggests that with growth risks emerging, a faster cutting cycle could be expected. Inflation running below the ECB’s forecasts supports this.

Meanwhile, in the UK, the BoE Governor Andrew Bailey suggested that the BoE could be “a bit more aggressive” on lowering interest rates. His comments hinted at a possible shift from the forward guidance provided by the Monetary Policy Committee in September, when the monetary policy statement said that “a gradual approach to removing policy restraint remains appropriate”. In Japan, chances of another rate increase are looking slim as new PM Shigeru Ishiba noted he does not “think the environment is ready for an additional rate hike.” The comment followed a meeting with Governor Ueda who has increasingly lowered expectations for tightening. Ishiba also noted there will be further support for households in coming months which could help boost spending.

Markups and Downs

The RBA no longer says that wages growth is too high to be consistent with inflation returning to target. But how did it come to that conclusion in the first place?

Last week we noted that, in its September post-meeting communications, the RBA was no longer saying that wages growth was ‘above the level that can be sustained given trend productivity growth’, as it did in August. How did it make that judgement in the first place, and why does trend productivity growth come into the story?

The answer rests on the RBA’s beliefs about how the economy works, based on analytical frameworks first introduced in the 1990s. This framework starts from the premise that consumer prices can be represented as a markup over labour and other costs. For a given percentage markup, the growth rate of prices (inflation) will line up with the growth rate of costs.

If the split between labour and non-labour costs is also stable, then growth in labour costs will also line up with inflation. Labour costs per unit of output is equivalent to labour costs per hour divided by output per hour. Ignoring some second-order maths pedantry, this means that inflation should line up with growth in labour costs per hour (average earnings growth) minus growth in output per hour worked. Output per hour worked is the definition of productivity in the national accounts, and what economists mean when they say ‘productivity’. The link between productivity and achieving the inflation target comes from this relationship.

To make the example concrete, if you think productivity growth is about 1% per year, and wages growth has a 3 in front of the decimal point, then according to the RBA’s rule of thumb, you should be relaxed about wages growth being consistent with the inflation target: 3-and-a-bit minus 1 is 2-and-a-bit, and so would be in line with inflation in the 2–3% target range.

If you have been following along, though, you will notice that there were a lot of things held constant in this mapping between wages growth, productivity growth and inflation. Firstly, it requires that growth in labour costs and in non-labour costs are similar and persistent. Secondly, it assumes that the percentage markup over costs is constant. Neither is true in the short run or even the medium run.

Non-labour costs have been a key driver of the recent surge in costs. Transport and energy costs, building materials and insurance had all been rising faster than overall CPI inflation until recently; insurance inflation is still at double-digit rates, being downstream of some of the other costs. Labour costs have also been growing quickly, but since 2021 growth in the Wage Price Index (WPI) lagged inflation in final-stage producer prices.

In addition, a period of strong growth in unit labour costs will not persist if productivity growth increases but is not matched by a pick-up in wages growth. The RBA recognised this in its August media statement by expressing the relationship as being between wages growth and trend productivity growth. The trend is not quite the right measure to use in a markup model, but this framing points to where future productivity growth might converge. However, the Statement on Monetary Policy still focused on recent outcomes. One of the reasons cited for the RBA’s assessment that supply capacity was weaker than previously thought was ‘wages growth has been high relative to productivity outturns’.

Meanwhile, markups and profit margins do not stand still. Mechanically mapping the latest data on unit labour cost growth to the latest inflation outcome would be misleading as a forecast. Even the RBA’s markup model for forecasting inflation allows the markup to vary over the cycle.

It is understandable that the RBA would not want to get into the weeds on whether profit margins might rise or fall. It matters whether you are talking about markups over average cost (as implied by the RBA’s markup model) or over marginal cost (the focus of much of the academic literature). And the literature has not even reached a consensus on whether markups rise or fall when demand is strong. Any discussion of the issue would get messy. The controversy around whether ‘greedflation’ had been a factor in Australia’s inflation experience also makes a nuanced discussion difficult. That said, implicitly assuming that margins are constant and unit labour costs map mechanically to inflation is not ideal, either.

Finally, all this assumes that productivity growth in the whole economy is the relevant measure for this model of inflation determination. Yet there are significant sections of the economy where the price as measured in the CPI and the costs implied by wages and productivity are not tightly linked. Public sector and other non-market activity simply is not priced this way, at least not in the short to medium run.

This is the point our Westpac Economics colleague, Senior Economist Pat Bustamante, made in his recent note. Partly because the share of activity in the (low measured average productivity) non-market sector is rising, measured total productivity growth is weaker than usual. In the market sector, though – the part of the economy where markups matter for pricing – productivity growth is already above 1%.

Why has the monetary policy discourse in Australia become so hung up on productivity growth? On top of the RBA’s use of markup models, it is a peculiarity of the Australian economic discourse more generally to worry about productivity growth and assume that the government should do something about it. We have a Productivity Commission, after all – it must be a government responsibility, right? This mentality is reinforced by a narrowly country-specific view (outside the RBA, to be fair) that does not recognise that the slowdown in trend productivity growth since the GFC was common to most Western economies.

Another factor is an apparent view that wages growth will be too sticky. Our own forecasts see the WPI measure of wages growth slowing from 4.1% over the year to the June quarter to 3.5%yr September and 3.2% over calendar 2024, as the outsized September quarter 2023 increase drops out of the calculation. The RBA’s forecasts are noticeably higher – 3.6% over 2024 – and the average earnings measure more relevant to the unit labour cost calculation is higher still. And maybe they will be right, but this is still a significant slowing.

Even using their own forecasts, though, there was a choice between ‘wages are above the level that can be sustained’ and ‘the expected decline in wages growth would return it to levels consistent with’. The shift in language in the September media release better aligns with a forward-looking view. When the WPI and national accounts data for the September quarter are released ahead of the RBA Board’s December meeting, a further pivot in RBA rhetoric might be needed. If we are right that the Board will wait until the February 2025 meeting to cut rates, then perhaps the December meeting before it will be the point to acknowledge that Australia’s domestic cost story has not been that unusual after all.

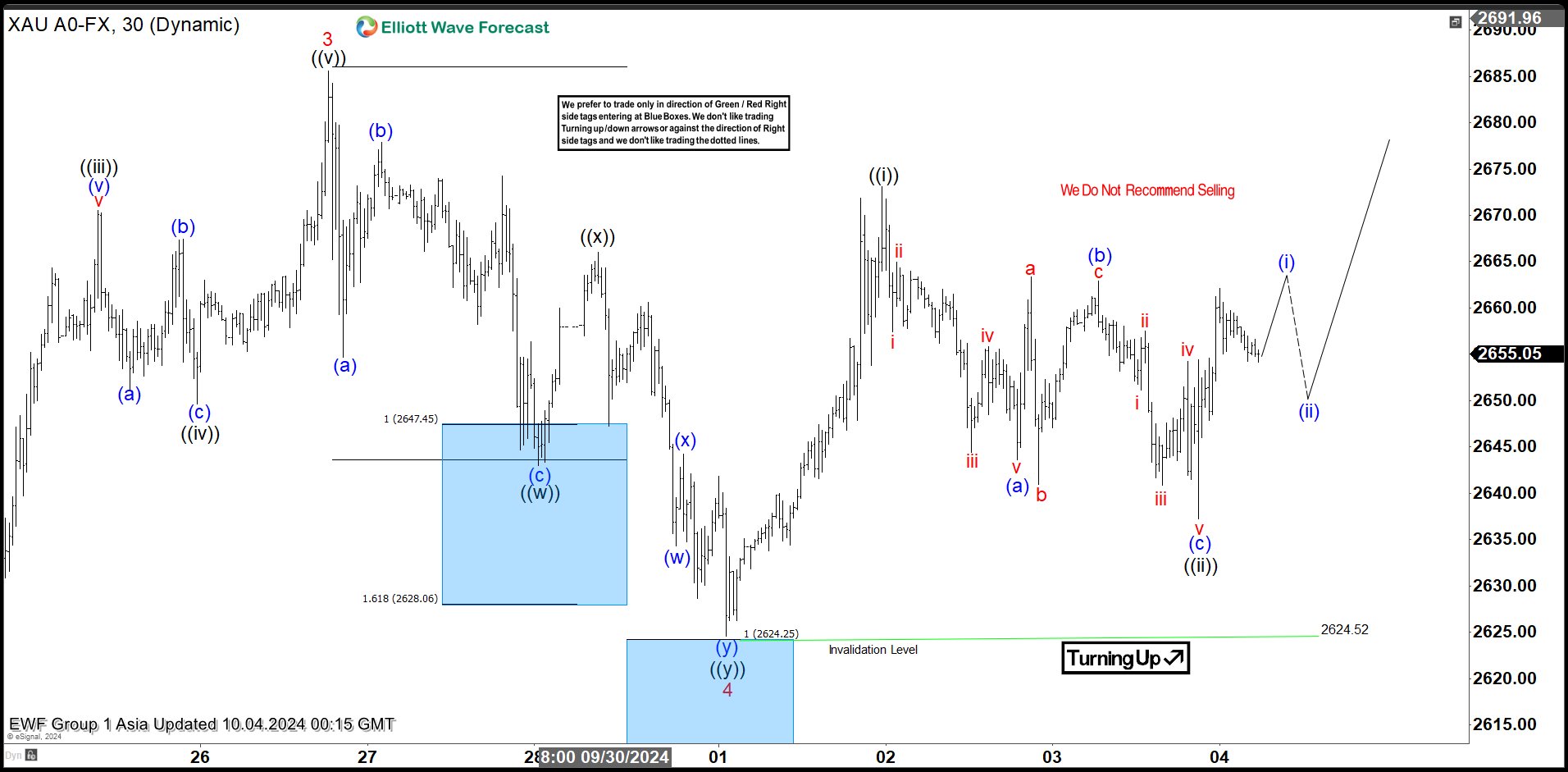

Intraday Elliott Wave View on Gold (XAUUSD) Looking to Resume Bullish Trend

Short Term Elliott Wave View in Gold (XAUUSD) suggests that rally to 2685.58 ended wave 3. The metal then did a pullback in wave 4 with internal subdivision as a double three Elliott Wave structure. Down from wave 3, wave (a) ended at 2654.68 and wave (b) rally ended at 2677.86. The metal extended lower in wave (c) towards 2643.02 which completed wave ((w)). Rally in wave ((x)) ended at 2665.99 and the metal has extended lower again.

Down from wave ((x)), wave (w) ended at 2634.3 and wave (x) rally ended at 2644.20. Wave (y) lower ended at 2624.52 which completed wave ((y)) of 4 in higher degree. The metal has turned higher in wave 5, but it still needs to break above wave 3 at 2685.58 to rule out a double correction. Up from wave 4, wave ((i)) ended at 2673.14. Down from there, wave (a) ended at 2643.65 and wave (b) ended at 2662.92. Wave (c) lower ended at 2637.26 which completed wave ((ii)) in higher degree. The metal has resumed higher in wave ((iii)). Near term, while above 2624.5, expect pullback to find buyers in 3, 7, 11 swing for further upside.

Gold (XAUUSD) 30 Minutes Elliott Wave Chart

XAUUSD Elliott Wave Video

https://www.youtube.com/watch?v=6AElpQj0TzE

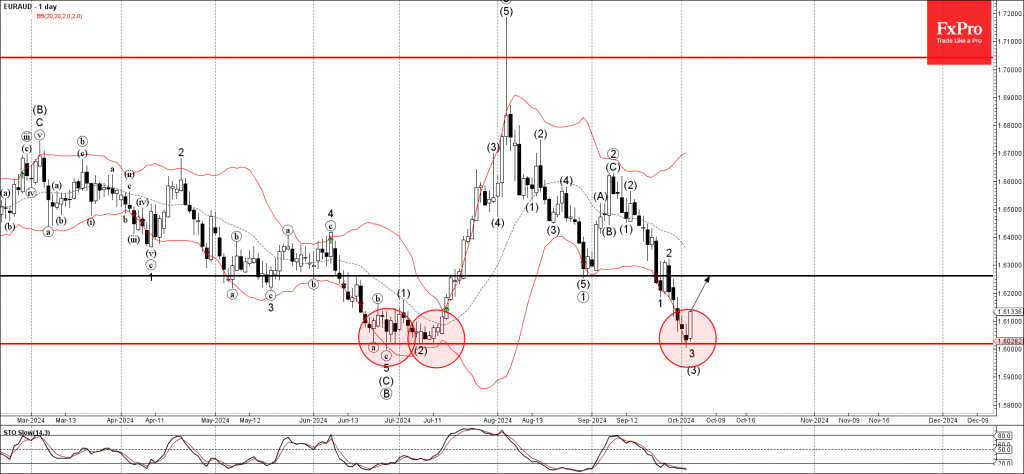

EURAUD Wave Analysis

- EURAUD reversed from strong support level 1.6020

- Likely to rise to resistance level 1.6260

EURAUD currency pair recently reversed up from the strong support level 1.6020 (which stopped the multi-month downtrend in June) intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 1.6020 will likely form the daily Japanese candlestick reversal pattern Morning Star.

Given the strength of the support level 1.6020, bullish euro sentiment and the oversold daily Stochastic, EURAUD currency pair can be expected to rise further to the next resistance level 1.6260 (former low from August).

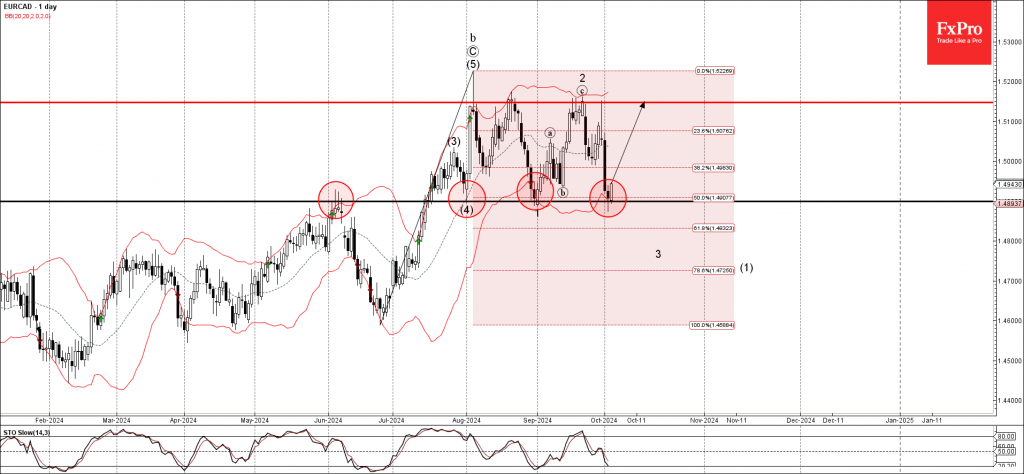

EURCAD Wave Analysis

- EURCAD reversed from key support level 1.4900

- Likely to rise to resistance level 1.5150

EURCAD currency pair recently reversed up from the key support level 1.4900 (former resistance from June, which stopped the previous waves (4) and 1) intersecting with the lower daily Bollinger Band and the 50% Fibonacci correction of the sharp upward impulse from June.

The upward reversal from the support level 1.4900 created the daily Japanese candlesticks reversal pattern Hammer.

Given the clear daily uptrend, EURCAD currency pair can be expected to rise further to the next resistance level 1.5150 (top of wave 2 from last month).

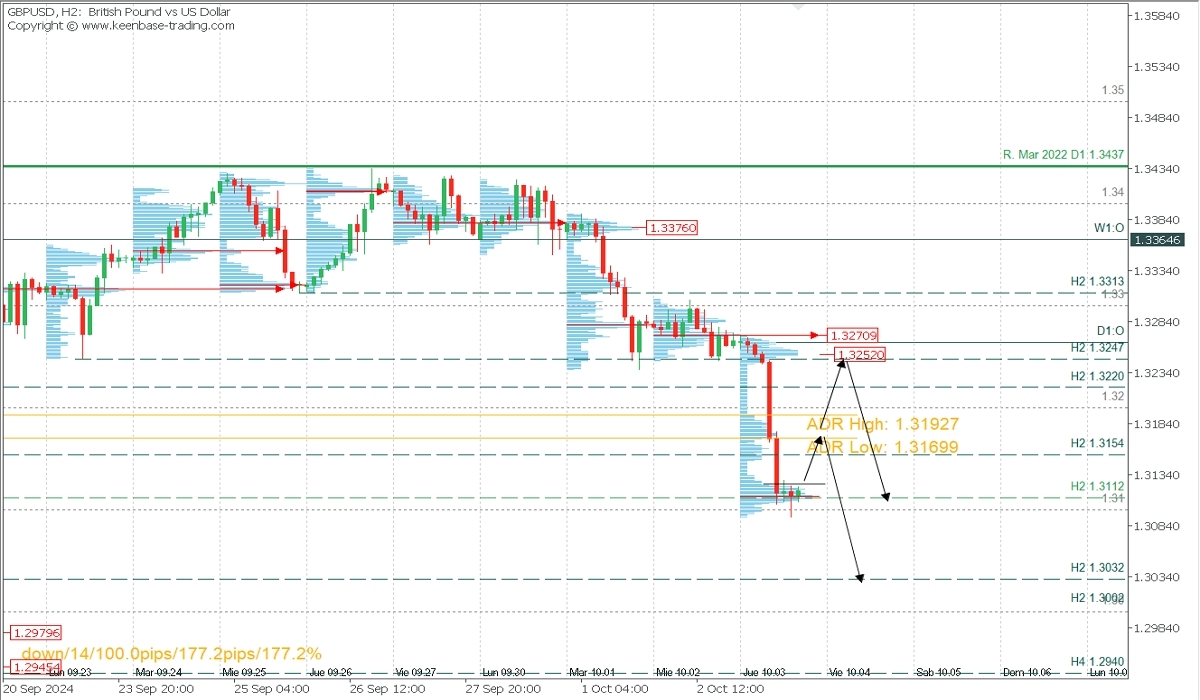

GBPUSD Seeking Supply Zones After Thursday’s Massive Sell-off

Fundamental Analysis

The pound has faced strong bearish pressure following statements from Bank of England Governor Andrew Bailey, who hinted that the institution might adopt a more proactive stance on rate cuts if inflation continues to decline. Additionally, the September services and composite PMI data came in at 52.4 and 52.6, respectively, below previous figures and market expectations. These results reflect a slowdown in UK economic activity, further weakening the pound, which fell to 1.3130, its lowest level in two weeks.

On the other hand, the strengthening of the US dollar has exacerbated GBPUSD’s decline, driven by solid US labour market data, increasing expectations of a less aggressive rate-cut scenario by the Federal Reserve. Despite market volatility due to tensions in the Middle East, the dollar has solidified its position as a safe haven, keeping pressure on the pair and opening the possibility of further declines if support at 1.3100 does not hold.

Technical Analysis

GBPUSD, H2

- Supply Zones (Sells): 145.08 and 145.89

- Demand Zones (Buys): 143.13, 142.00, and 140.60

After reaching a buy zone at 1.3112, breaking through the day’s bearish range, a corrective rebound towards 1.3154 and the high-volume node zone below the daily bullish range can be expected. There's potential to extend the buying on Friday during early sessions towards 1.3220 or the supply zone around 1.3252. Both areas have the potential to trigger bears to renew intraday sells toward 1.31 again and 1.3032 or 1.30 on further downside on Friday.

Technical Summary

- Buys above 1.3128 with TP at 1.3154, 1.32, 1.3220, or 1.3247 extension. All these levels have the potential to activate bulls, so it’s suggested to wait for the formation and confirmation of an exhaustion/reversal pattern on M5.

- Sells below 1.3190 if an exhaustion/reversal pattern (PAR) forms and confirms on M5; otherwise, wait to sell around 1.3247.

Always wait for the formation and confirmation of an Exhaustion/Reversal Pattern (PAR)on M5 like those shown [here](https://t.me/spanishfbs/2258) before entering any trade in the key zones indicated.

POC Discovered:

POC = Point of Control: The level or zone where the highest concentration of volume occurred. If a bearish move follows, it is considered a sell zone, forming a resistance zone. Conversely, if a bullish move follows, it is considered a buy zone, usually located at lows, forming support zones.