Sample Category Title

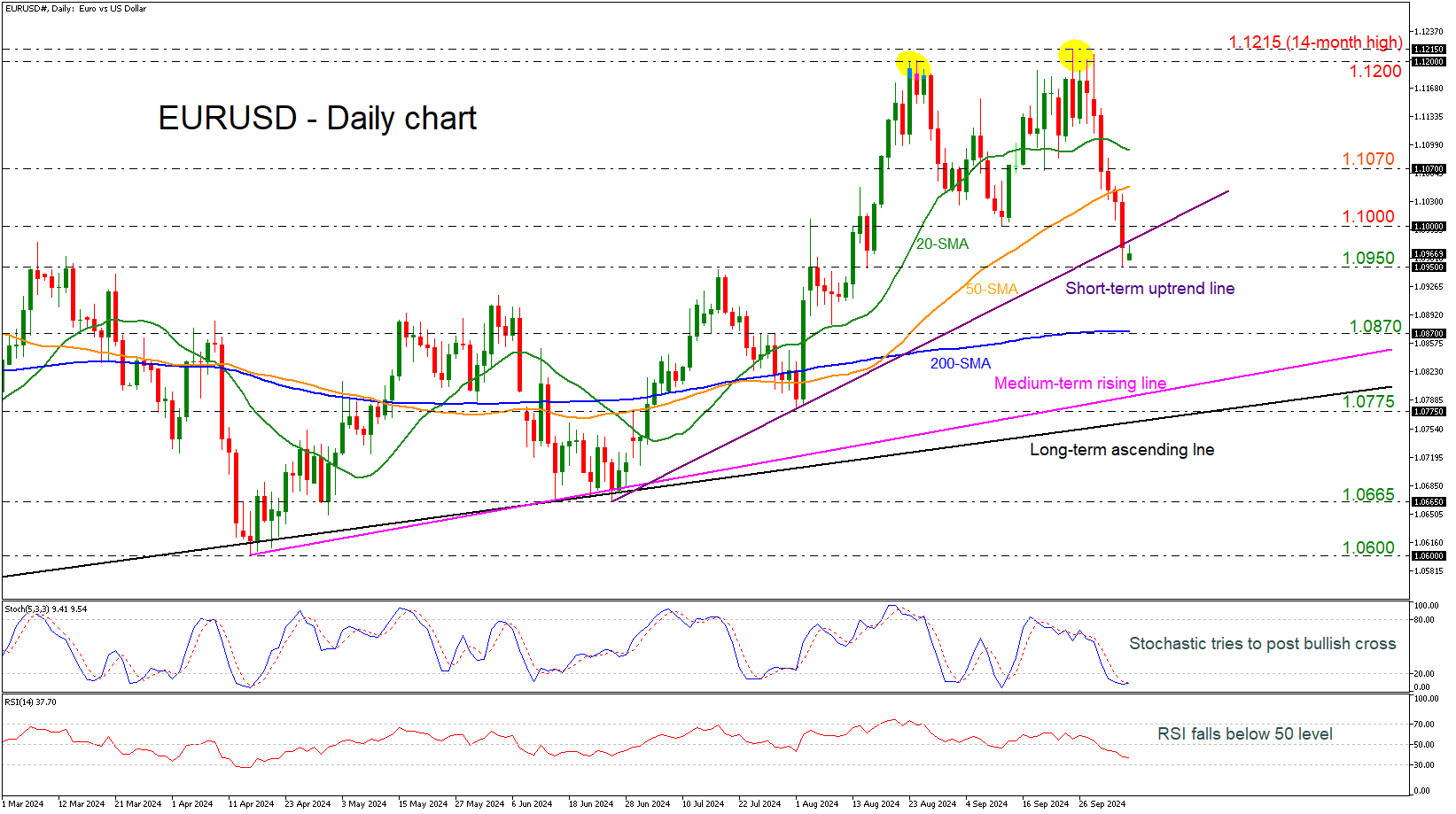

EURUSD Pauses Southward Run Near 1.0950

- EURUSD posts 6 red sessions

- Price plunges below 1.1000

- Stochastics indicates upside recovery

- But RSI keeps falling

EURUSD plummeted more than 2% after the pullback from the double top around 1.1200, recording six straight red days. The price also tumbled beneath the short-term uptrend line and the 1.1000 round number, confirming the bearish correction in the near term.

The RSI indicator is falling beneath the neutral threshold of 50; however, the stochastic is suggesting the end of the negative retracement as it is posting a bullish cross within its %K and %D lines in the oversold territory.

If the selling interest continues, then the market may re-challenge the strong flat 200-day simple moving average (SMA) at 1.0870 before resting near the medium-term ascending line at 1.0800.

In the positive scenario, a climb back above the 1.1000 round number could add some optimism for bullish actions until the 50-day SMA at 1.1050, ahead of the 1.1070 resistance level. A slightly higher jump above the 20-day SMA at 1.1090 could pave the way for another test of the 1.1200-1.1215 restrictive region.

To sum up, EURUSD has been in a dilemma about whether the bearish correction would be deeper or whether the end of the correction is near. In the broader outlook, the price is still in a bullish area.

Payrolls Proved to be a Game-changer

Markets

The US September payrolls report beat market expectations for all key metrics. It also made markets question the need for ‘aggressive’ Fed-support to prevent a potential unwarranted softening of the labour market. US job growth in September reaccelerated from 159k to 254k and the figure for the previous two months was upwardly revised by 72k. The data of the consumer survey this time fully confirmed the payrolls’ data. The unemployment rate declined from 4.2% to 4.1% as job growth outpaced the a further rise in the labour force. Wage growth also printed at an higher than expected 0.4% M/M and 4.0% Y/Y. The market repositioning was impressive. US yields jumped between 21.6 bps (2-y) and 7.2 bps 30-y, with the move mainly driven by a rise in real yields (US 10-y +9.5 bps at 1.74%). The recent steepening trend also faced a hard roadblock. Money markets now discount a scenario of 25 bps steps at each of the four upcoming Fed meetings, at best. The trough of the cycle now is again seen near 3.25% rather than near 3.0%. EMU yields rose in sympathy even as the ECB is likely to step up the pace of easing with an ‘intermediate ‘ step later this month. German yields added between 12.2 bps (2-y) and 2.9 bps (30-y). ECB’s Villeroy in an interview this weekend said that a rate cut this month is quite probable as the ECB must watch the risk of inflation … undershooting the target! The rise in US (real) yields, this time didn’t hurt US equities as markets for now embrace the hypothesis of a no-landing scenario for the US economy, with solid growth supporting corporate earnings. US indices added between 0.81% (Dow) and 1.22% (Nasdaq). Of late, the dollar showed tentative signs of bottoming, but gains often were unconvincing. However, the payrolls in this respect also proved to be a gamechanger, improving the technical picture for the greenback. DXY now easily trades above 101.91 ST top (102.55). EUR/USD dropped below the 1.1002 neckline (close 1.0974). USD/JPY jumped from the 147 area to close at 148.7.

Asian markets this morning stay in risk-on modus. US yields tentatively drift further north. The dollar holds Friday’s gains. Today’s eco calendar is thin. Later this week, the US September CPI inflation will be published on Thursday. Markets will also keep an eye on how Fed governors assess the strong payrolls report. The US Treasury will sell 3-y, 10-y and 30-y notes at a regular auction series. From a market point of view, the burden of prove again shifted. Short-term, data will have to be unexpectedly weak, for markets to reconsider bets on faster easing. If not, the risk is for yields and the dollar to drift higher. For the US 2-y yield (currently 3.95%) 4.12% is a first ST target. EUR/USD is developing a double top pattern. The break of the 1.1002 neckline suggests a return to targets near 1.08.

News & Views

The US Committee for a Responsible Federal Budget calculated that US president-candidate Trump’s promises of tax cuts, tariff increases, military expansion and mass deportations would widen budget deficits by an estimated $7.5tn over the next decade. That’s on top of the $22tn deficits the US would run if Congress wouldn’t change current policies. Democratic-nominee and current vice-president Harris’ plans would increase deficits by $3.5tn over the same time horizon. The US debt ratio (currently 99% of GDP) is set to rise to 125% by 2035 if there are no changes to current laws, to 133% under Harris’ proposals and to 142% if Trump manages to implement his full policy agenda. The CRFB warns that the large and growing national debt threatens to slow economic growth, boost interest rates and payments, weaken national security, constrain policy choices and increase the risk of an eventual financial crisis.

The KMPGB and REC, UK report on jobs pointed at a further reduction in permanent placements during September, extending the current run of contraction to two years. Temp billings were also lowered for a third successive month. Uncertainty in the outlook, including around government policy ahead of late October’s Budget, meant companies were cautious in their hiring activity. REC chief executive Carberry said that recruiters report that projects in client businesses are ready to go, but that confidence is not yet high enough to push the button. Latest data showed the weakest rise in salaries for over three-and-a-half years. A greater number of candidates and reduced demand helped to limit pay growth.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) still is a source of concern, but very weak PMI’s and soft comments of Lagarde (and other MPC members) suggest the ECB is likely to step up the pace of easing with an October cut. Spill-overs from strong US data prevented a test of the 2.0% barrier. 2.00-2.35% might serve as a ST consolidation range.

US 10-y yield

The Fed kicked off its easing cycle with a 50 bps move. The Fed shifting focus from inflation to a potential slowdown in growth/employment made markets consider more 50 bps steps. Strong US September payrolls suggest the economy doesn’t need aggressive Fed support for now, but the debate might resurface as the economic cycle develops. For the US 10-y, 3.60% serves as strong support. The steepening trend is taking a breather.

EUR/USD

EUR/USD moved above the 1.09 resistance area and twice tested the 1.12 big figure as the dollar lost interest rate support at stealth pace. Bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) partially offset some of the general USD weakness. After solid early October US data, the dollar regained traction, with EUR/USD breaking the 1.1002 neckline. Targets of this pattern are near 1.08.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness was indicated to be further unwound gradually. The economic picture between the UK and Europe also was increasingly diverging to the benefit of sterling, pulling EUR/GBP below 0.84 support. Dovish comments by BoE Bailey ended by default GBP-strength.

US Dollar Rallies as Fed Doves Lost Field

Surprise! The US economy added more than 250’000 new nonfarm jobs last month, the unemployment rate fell to 4.1% and wages grew faster than expected both on monthly and on a yearly basis. On a yearly basis, the US workers earned 4% more on average compared to a year ago. On top, the strikes at the US ports were paused until mid January and the goods are being moved until further notice.

The US treasuries got heavily sold off on Friday, the US 2-year yield jumped 25bp as it became clearer that the Federal Reserve’s (Fed) decision to cut rates by 50bp last month was probably a mistake. The US 10-year yield rose about 12bp. The probability of another 50bp from the Fed in the November meeting crashed to 0 and activity on Fed funds futures now gives close to 100% chance for a 25bp cut, and a meagre 2% chance for a no rate cut.

Consequently, the US dollar index jumped more than 2.5% last week, and is now drilling above the 102.50 level, the major 38.2% Fibonacci retracement on June to September decline. A decisive move above this level should send the index into the medium-term bullish consolidation zone and pave the way for a further recovery.

The EURUSD slipped below the 1.10 psychological support last Friday and below 1.0980, the major 38.2% Fibonacci retracement which distinguishes the summer positive trend and a medium-term bearish reversal. And beyond the technical signal that autumn is coming for the EURUSD, the fundamentals also make sense for a softer euro. The European economies are not doing strongly, the latest PMI numbers showed further weakness in activity, inflation eased below the European Central Bank’s (ECB) 2% policy target. As such, a further EURUSD weakness would make sense. The next bearish targets stand at 1.0930, the 100-DMA and the 1.0875 – the 200-DMA.

Across the Channel, the pound sterling got heavily hit last week, as the Bank of England (BoE) Governor Andrew Bailey said that the bank could get a bit ‘more aggressive’ in cutting the rates. Cable fell to 1.3070 but found support near its 50-DMA, 1.3080, and hasn’t yet got a chance to test the major 38.2% support, that stands just a few pips below the 1.30 psychological mark.

Elsewhere, the NZDUSD starts the week under a decent selling pressure as the Reserve Bank of New Zealand (RBNZ) is expected to cut its rates by 50bp when it meets this week and the USDJPY consolidates past the 148 level this morning, having stepped into the medium-term bullish consolidation zone on the back of newly elected PM rejection of the idea of another rate hike in Japan this year, and a broad-based rally in the US dollar. The pair will likely consolidate between the 148-150 range until further notice.

Even the Swiss franc lost some field against the greenback last week. The USDCHF rose above its 50-DMA as the Swiss National Bank’s (SNB) new governor Martin Schlegel said that the bank will be prepared to intervene in the FX markets to manage the franc’s value if necessary.

In summary, the US dollar is better bid at the start of this week, but the US inflation report due Thursday could temper some of this bullish momentum. The US headline inflation is expected to have further eased from 2.5% to 2.3% in September. But core inflation is still above the 3% mark. Figures in line with expectations, or ideally softer-than-expected, will keep the Fed doves in charge of the market – even though another 50bp cut looks farfetched at this point. The major risk is to see a stronger-than-expected figure that would bolster the idea that the Fed may have made a mistake by cutting rates by 50bp and boost the chances of a no cut in November.

The earnings season will kick off this Friday with big bank earnings. The Q3 earnings estimates have fallen from a 7.9% growth estimated in July to 4.7%, but the latter didn’t prevent the S&P500 from recovering summer losses. The index trades 2% above the July peak, and lower expectations are easier to beat.

Probability of 50bp Fed Rate Cut Declines After Strong Jobs Report

In focus today

Today, 7 October marks one year since Hamas' terrorist attack that started the ongoing conflict in Middle East. On the eve of the day of memorial, Israel expanded its attacks both in Lebanon and Gaza and the threat of a full-blown regional war hangs in the air.

In the euro area, we receive the Sentix investor confidence indicator, which will give the first indication of sentiment in October. Also, the August retail sales will shed light on consumer spending, which is key for the growth outlook.

In Germany, the August factory orders will give a hint of where we can expect the industrial production figure tomorrow to land.

Early Tuesday, we get total cash earnings in Japan for August. Real earnings growth turned positive over the summer, a prerequisite for fuelling private spending. The Bank of Japan needs the trend to continue in order to normalise policies further.

Later Tuesday, we get the NFIB's small business optimism index. Early Wednesday, the Reserve Bank of New Zealand announce its cash rate decision. Wednesday evening minutes from the Fed September meeting is released. On Thursday we get September CPI from the US, the main release of the week, and on Friday, US October consumer sentiment survey from University of Michigan is due for release.

Economic and market news

What happened over the weekend

In the Middle East, on the eve of Monday 7 October that marks one year since Hamas' terrorist attack, Israel expanded their operations both in Gaza and Lebanon. A Hezbollah rocket launch got past Israel's defence system in Haifa. Meanwhile, Iran has cancelled some overnight flights, apparently in the fear of Israel's response to Tuesday's missile barrage. An Israeli attack on a military target would be comparable to what happened in April, and in the best case, would open the door for Iran to restraining from retaliatory measures. An Israeli attack on Iran's oil facilities would mark an escalation. Iran's oil exports represent approximately 2% of global supply, and while oil market would likely react, any impact should be relatively short-lived as long as other OPEC members would be willing to increase production. Most of the spare capacity is in Saudi Arabia and the country has already showed readiness to step up production.

ECB's villeroy, spoke about monetary policy in an interview and stated that he thinks that ECB will lower rates again at the October meeting. He stated that the main risk has changed from overshooting inflation to undershooting due to weak growth if monetary policy is kept restrictive for too long. On Friday, ECB's Centeno, who is a well-known dove, pointed out that the European labour market is starting to cool, and that he thinks that inflation is under control, which sounds like he is ready for more rate cuts. Next ECB meeting is on 17 October, where we expect ECB to deliver another 25bp rate cut.

What happened on Friday

In the US, the jobs report was much stronger than expected. Change in non-farm payrolls came in 254k (Danske forecast: 160k, consensus: 150k, prior 142k). Average hourly earnings increased by 0.4% m/m seasonally adjusted (Danske forecast: 0.2%, consensus: 0.3%, prior: 0.4%). The unemployment rate dropped to 4.1% (Danske forecast: 4.2%, consensus: 4.2%, prior: 4.2%. 2y UST yields surged more than 20bp while 10y UST yields traded more than 10bp higher. EUR/USD fell below 1.10 mark and ended Friday at 1.098. Markets pulled back from speculating in another 50bp cut from the Fed and are now very closely aligned with our call for both 2024 and 2025 in terms of Fed pricing.

In the UK, BoE chief economist Pill (who was one of the dissenters in August, voting for unchanged in a 5-4 vote) delivered hawkish remarks saying that he felt that August was too early to start cutting rates and stressed that BoE should continue a gradual approach with further rate cuts. He also stated that it will be important to guard against the risk of cutting rates either too far or too fast.

Oil prices ended the week at the highest level since late August with the price of Brent Crude oil just above 78 USD/barrel. It was the highest weekly gain in nearly a year starting the week at around 74.4 USD/barrel. The main driver behind the higher prices has been the increased geopolitical tensions in the Middle East with Israel making it clear they will strike Iran after the country launched a missile attack on Israel last Tuesday. Prices rose further at the end of the week after US president Biden confirmed that the US had talks with Israel about backing an attack on Iranian energy infrastructure.

Equities: Global equities were sharply higher on Friday, with all regions posting gains and the US leading the advances due to their weight and the influence of the NFP. However, the uplift was not broad-based across sectors, as the bond markets reacted more than equities, sending the short end of the curve massively higher. Consequently, most defensive sectors underperformed while banks emerged as the big winners, benefiting from reduced recession fears and higher yields. Notably, small caps also outperformed despite the rise in yields and the underperformance of REITs. The key takeaway here is that investors are currently more concerned about a weakening job market than a reacceleration in inflation. Both factors could lead to a worsening outlook, particularly for Commercial Real Estate (CRE), but Friday's developments provided more support to the soft-landing scenario and hence to small caps. In the US on Friday, the indices reported gains with Dow +0.8%, S&P 500 +0.9%, Nasdaq +1.2%, and Russell 2000 +1.5%. Asian markets are broadly higher this morning, led by Japan as the yen continues to weaken. US futures are flat this morning, while European futures are higher.

FI: Global yields repriced significantly following the strong US labour market report on Friday. The 254k NFP number, plus upward revisions of the previous two months sent yields higher from the front as markets reassessed the probability of a 50bp rate cut in November in the US. Markets priced SOFR rates 10bp higher to 25bp rate cuts priced.

FX: EUR/USD declined below 1.10 following Friday's very strong NFP print of 254k, making it the biggest weekly rally for the USD in about two years. With global yields moving higher and comments to the hawkish side from the BoE, EUR/GBP reversed its recent move higher firmly back below 0.84. On the contrary, the SEK did not approve of last week's market sentiment and EUR/SEK shifted back up to its previous range of 11.30-11.40, currently edging close to the upper end.

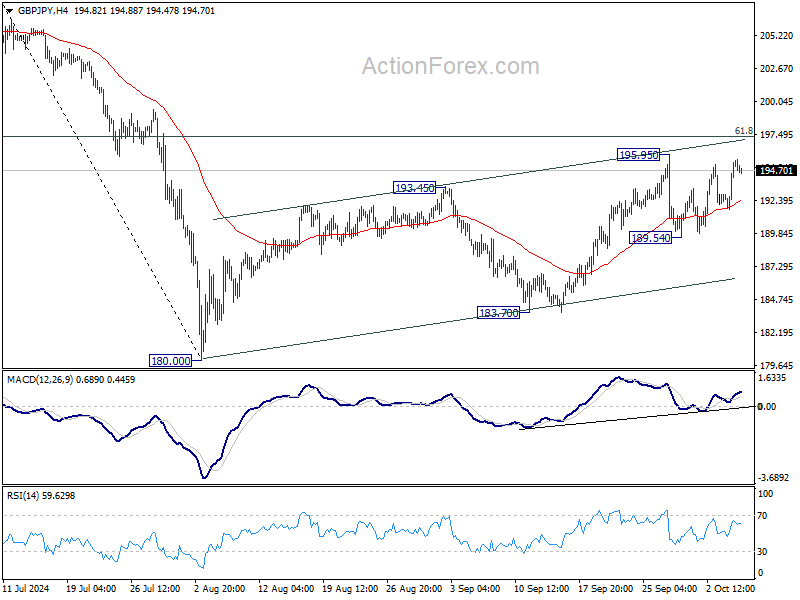

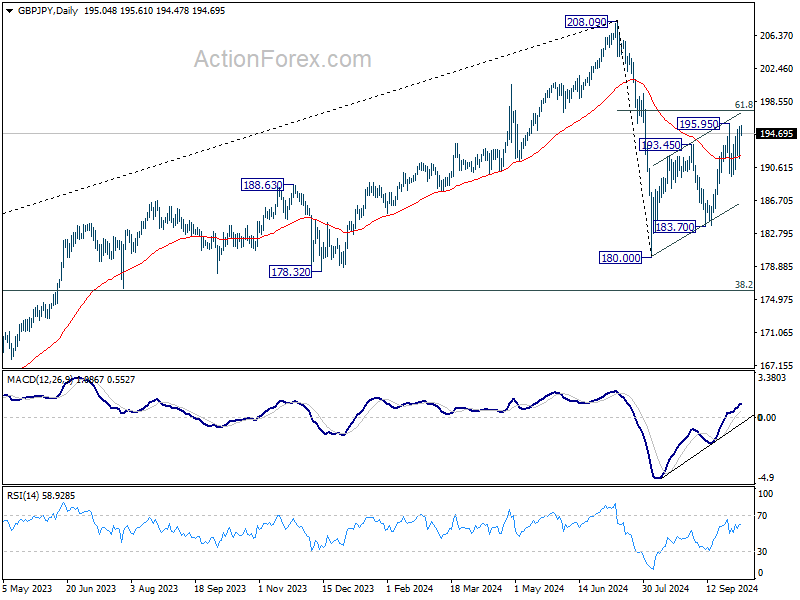

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.82; (P) 194.17; (R1) 196.61; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the upside break of 195.95 will resume whole rise from 180.00 to 61.8% retracement of 208.09 to 180.00 at 197.35 next. On the downside, break of 189.54 will turn bias back to the downside for 183.70 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

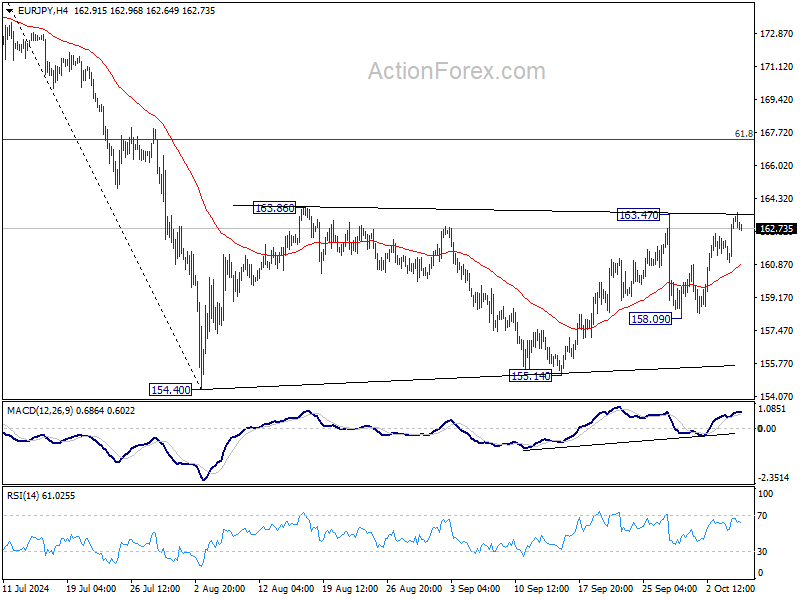

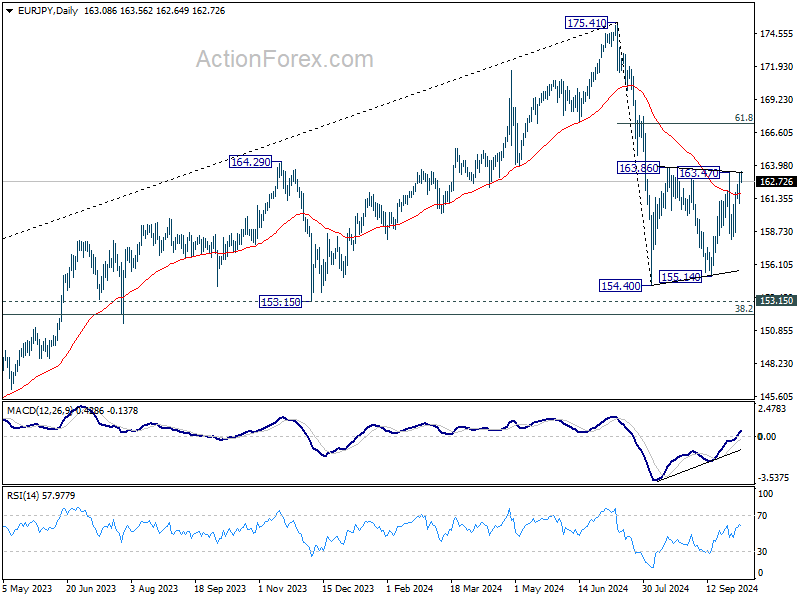

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.72; (P) 162.55; (R1) 164.07; More....

Intraday bias in EUR/JPY stays neutral at this point. On the upside, break of 163.47 resistance will resume the rebound from 154.40 to 61.8% retracement of 175.41 to 154.40 at 167.38. On the downside, break of 158.09 will bring deeper fall back to 154.40/155.14 support zone instead

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

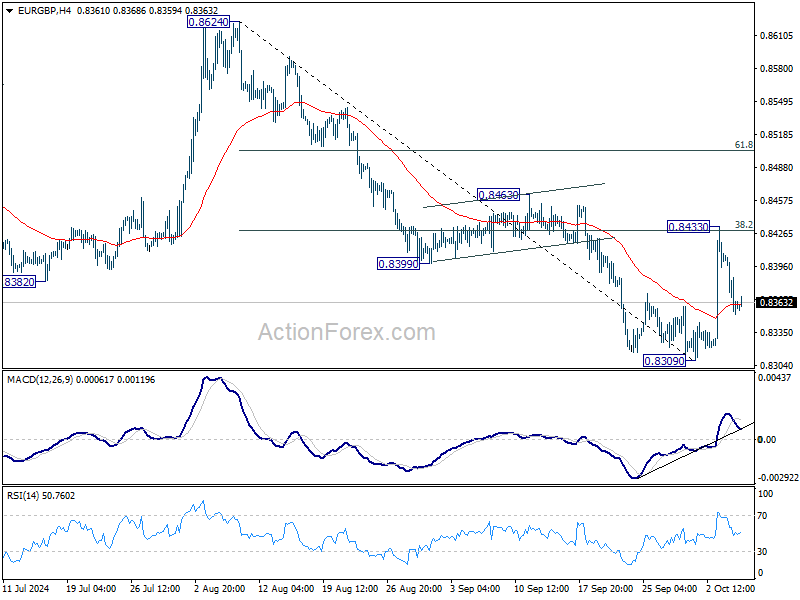

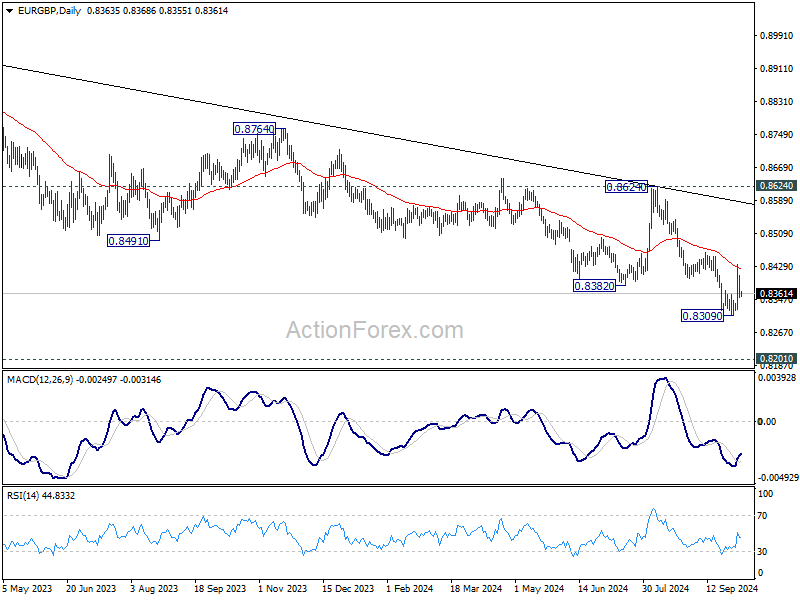

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8341; (P) 0.8374; (R1) 0.8396; More...

Intraday bias in EUR/GBP remains neutral for the moment, and outlook stays bearish. On the downside, break of 0.8309 will resume larger down trend to 0.8201 key support next. However, decisive break of 38.2% retracement of 0.8624 to 0.8309 at 0.8429 will pave the way to 61.8% retracement at 0.8504 and possibly above.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.

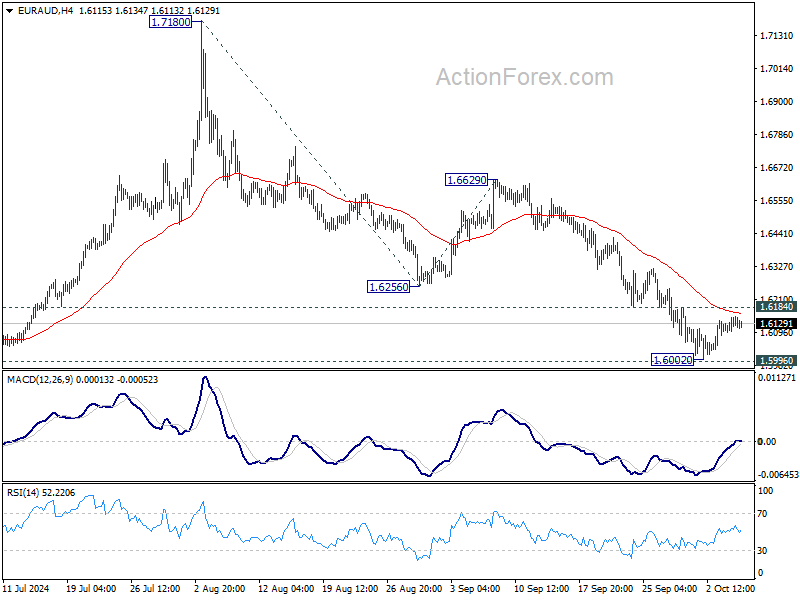

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6118; (P) 1.6137; (R1) 1.6174; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the upside, firm break of 1.6184 resistance should confirm short term bottoming after defending 1.5996 key support. Intraday bias will be back on the upside for 1.6256/6629 resistance zone. However, sustained break of 1.5996 will carry larger bearish implications, and target 100% projection of 1.7180 to 1.6256 from 1.6629 at 1.5705.

In the bigger picture, as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

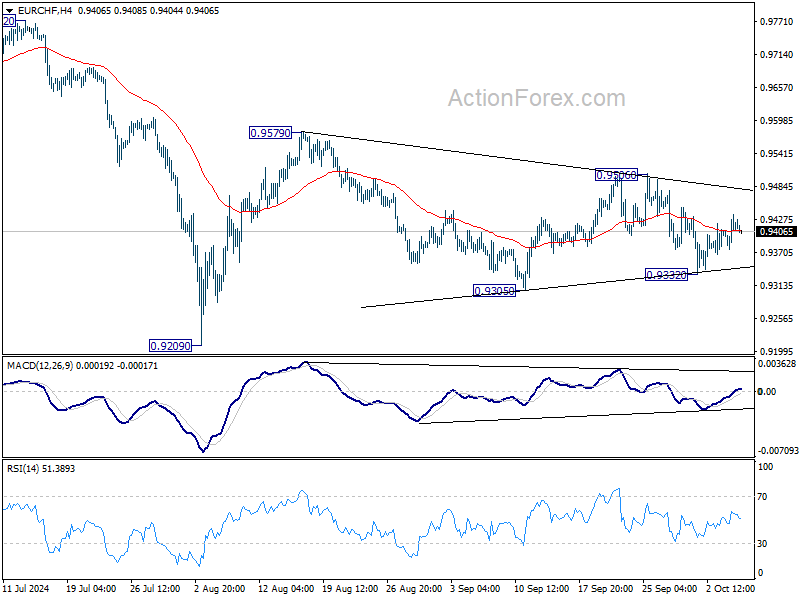

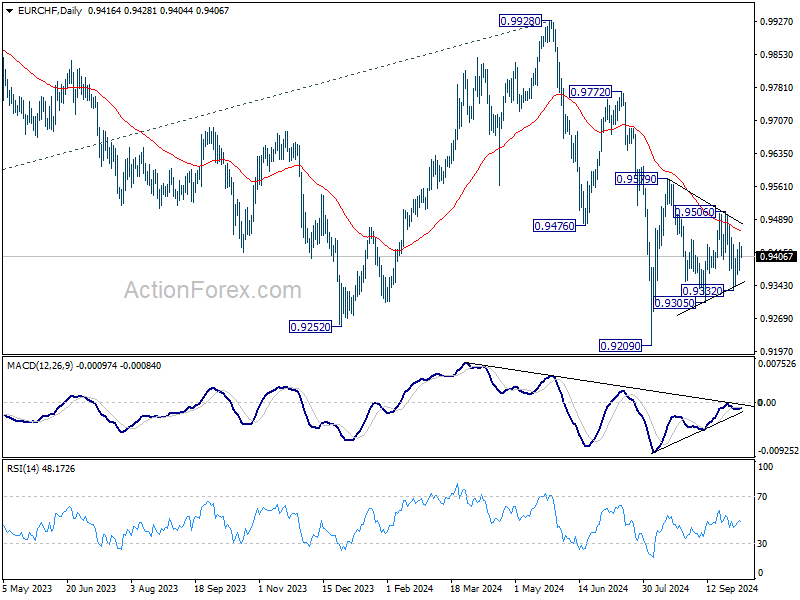

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9384; (P) 0.9411; (R1) 0.9445; More....

Intraday bias in EUR/CHF remains neutral as range trading continues. For now, the favored case is that rise from 0.9209 low is not finished yet. Break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above. However, break of 0.9332 will dampen this view and bring deeper decline through 0.9305 support instead.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

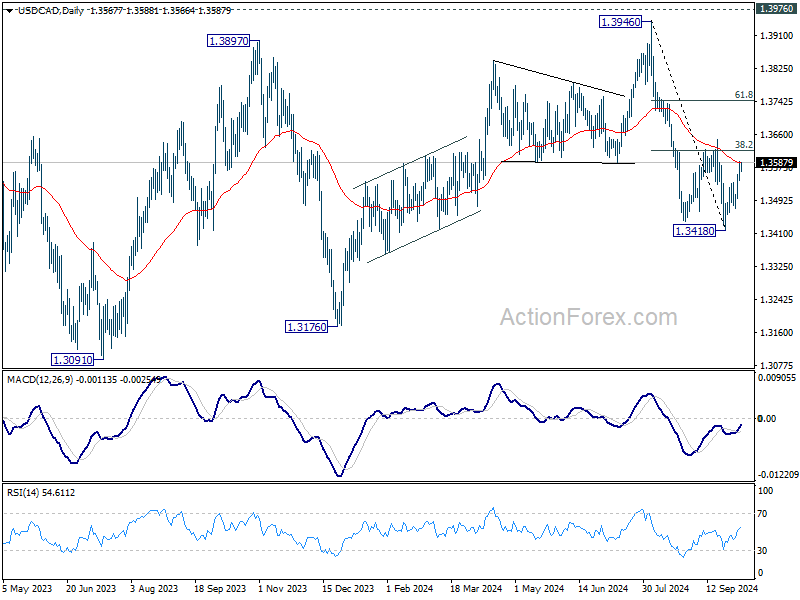

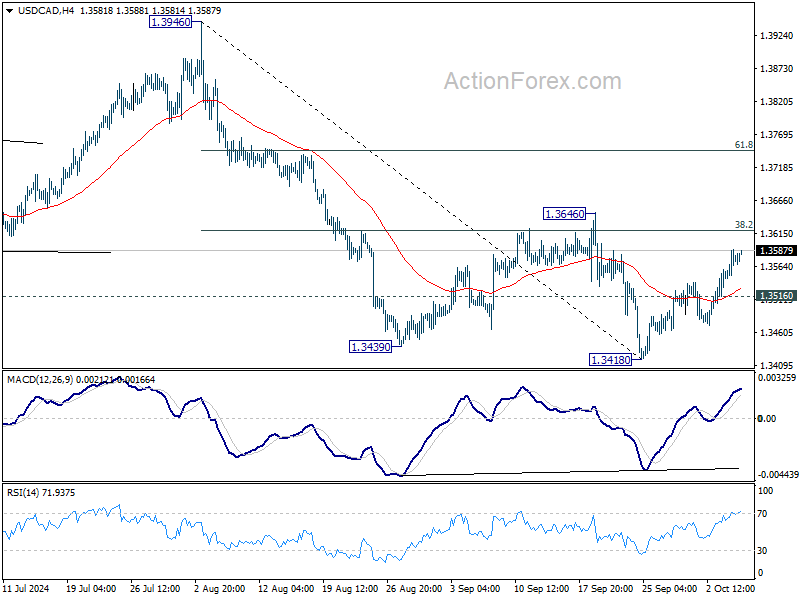

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3538; (P) 1.3565; (R1) 1.3602; More...

Intraday bias in USD/CAD remains mildly on the upside for the moment. Rebound from 1.3148 is in progress for 38.2% retracement of 1.3946 to 1.3418 at 1.3505. Decisive break there will target 61.8% retracement at 1.3559 next. On the downside, however, break of 1.3516 minor support will turn bias to the downside, to resume the fall from 1.3946 through 1.3418.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.