Sample Category Title

Japan’s PMI manufacturing PMI finalized at 49.7, output and new orders in contraction

Japan's Manufacturing PMI for September was finalized at 49.7, marginally lower than August's reading of 49.8, signaling continued contraction in the sector.

According to Usamah Bhatti from S&P Global Market Intelligence, the data reflected "muted trends" in Japan's manufacturing industry. Both output and new orders remained in negative territory, while the rate of job creation "slowed to a crawl."

While businesses expressed optimism about output growth over the next 12 months, the level of optimism softened, marking the weakest positive outlook since the end of 2022. Some manufacturers highlighted concerns over the "timing of a demand recovery," reflecting cautiousness in the face of global and domestic uncertainties.

Japan’s Q3 Tankan shows stability in manufacturing, slight gains in non-manufacturing

Japan's Q3 Tankan Large Manufacturing Index remained steady at 13, unchanged from Q2 and in line with market expectations, indicating stability in the country's manufacturing sector. Manufacturers’ outlook for the next three months improved slightly to 14, signaling cautious optimism about future business conditions.

Large Non-Manufacturers Index showed a modest rise to 34, up from 33 in June, surpassing expectations of 32. However, the outlook for non-manufacturers over the next three months dipped to 28, reflecting some uncertainty in the service and retail sectors.

Capital spending plans by big companies were revised down, with firms now expecting a 10.6% increase for the fiscal year ending in March 2025. This is below the median forecast of an 11.9% rise and down from an 11.1% forecast three months ago, suggesting some cooling in business investment intentions.

The Tankan survey results will be closely monitored by BoJ as it prepares for its monetary policy meeting on October 30-31, where it will set new growth and inflation forecasts.

BoJ opinions highlight divergence over timing of future rate hikes

The Summary of Opinions from BoJ's meeting on September 19 and 20 acknowledged that while outlook for Japan's economic activity and inflation will guide future changes in monetary accommodation, policymakers remain vigilant about developments in overseas economies, particularly the US, and their potential impact on Japan's financial markets and price stability.

With Yen's depreciation retracing and import price pressures easing, one view noted that BoJ has "enough time to assess the situation". Another opinion stressed that Japan's economy is not at risk of "falling behind the curve" if interest rates are not raised swiftly. BoJ should not raise interest rate when "financial and capital markets are unstable".

Another member suggested that while price stability has not yet been achieved and uncertainties persist, a shift to "full-fledged monetary tightening" would be undesirable at this stage.

However, a contrasting opinion within the BoJ indicated that if economic conditions remain stable and the outlook is confirmed, it would be preferable for the bank to raise rates "without taking too much time."

This divergence highlights the ongoing debate within BoJ about the timing of future rate hikes.

Fed’s Powell: No rush for rapid rate cuts

Fed Chair Jerome Powell made it clear during a speech at the NABE conference that FOMC is "not a committee that feels like it is in a hurry to cut rates quickly."

Powell noted that if the economy evolves as expected, Fed could enact "two more cuts" by the end of the year, reducing the policy rate by an additional half a percentage point. He reaffirmed that the US economy is on track for a continued slowdown in inflation, which should allow the Fed to reach a neutral interest rate level "over time."

"Disinflation has been broad-based," Powell said, citing recent data that shows progress towards Fed's 2% inflation target.

However, Powell stressed that Fed is "not on any preset course" and will assess risks on both sides of the economy. "We will continue to make our decisions meeting by meeting," he added.

Fed’s Goolsbee expects extended series of rate cuts as economy normalizes

Chicago Fed President Austan Goolsbee highlighted Fed's outlook for an extended period of monetary easing in an interview with FOX Business overnight.

He noted, "this is a process over a year or more that we're trying to get the rates down to normal."

He also pointed out that the Fed's latest forecasts suggest "a lot of cuts" ahead, with policymakers aligned on this approach.

Fed has already begun easing, cutting its policy rate by 50bps at last meeting, bringing it to the 4.75%-5.00%.

Goolsbee refrained from committing to a specific rate cut size at the upcoming November meeting, stressing that the overall process of returning rates to more "normal" levels is the focus.

Additionally, Goolsbee noted cautionary signals in the labor market, though he remarked that the current unemployment rate of 4.2% appears to be at a sustainable level.

Fed’s Bostic sees gradual easing, possible dramatic cuts if job growth falter

In an interview with Reuters overnight, Atlanta Fed President Raphael Bostic outlined his expectations for a gradual, "orderly" easing of monetary policy over the next 15 months. His baseline scenario sees policy rate falling to a range of 3.00% to 3.25% by the end of 2025, a level he considers neutral for the economy.

However, Bostic cautioned that a "much weaker" labor market could accelerate the pace of rate cuts. He emphasized that significant job market deterioration would "add urgency" to Fed's easing process, prompting another "dramatic move" such as the 50bps rate cut enacted in September.

Bostic also noted his close attention to job growth, stating that as long as the economy continues to produce net jobs and monthly job creation stays above 100,000, the labor market will likely remain on stable footing. This threshold, in Bostic’s view, is the minimum needed to absorb new entrants into the labor force.

Gold (XAU/USD) Prices Slide as Q3 Draws to a Close

- Gold prices fell due to a stronger dollar and end-of-quarter flows, despite being on track for the best quarter since Q1 2016.

- The market is awaiting US jobs data on Friday, which could impact rate cut expectations and the US dollar.

- Gold remains extremely overbought at present, will the NFP report inspire a deeper correction?

Gold prices slid this morning as a slightly stronger dollar and end of quarter flows weigh on the precious metal. Despite the drop off, Gold remains on course for its best quarter since Q1 of 2016, which recorded gains of 16% +.

Gold continues to find support as safe haven appeal and incoming rate cuts keep bulls interested. However, the drop to start the week could be down to a number of overlapping factors such as profit taking, repositioning and the recent rally in Chinese equities and emerging markets.

The stimulus announced by the PBoC is the gift that keeps on giving where China is concerned. The rally in Chinese equities could be impacting Gold as well, given the higher yield on offer. Gold remains in extremely overbought territory and thus further upside may also prove a challenge.

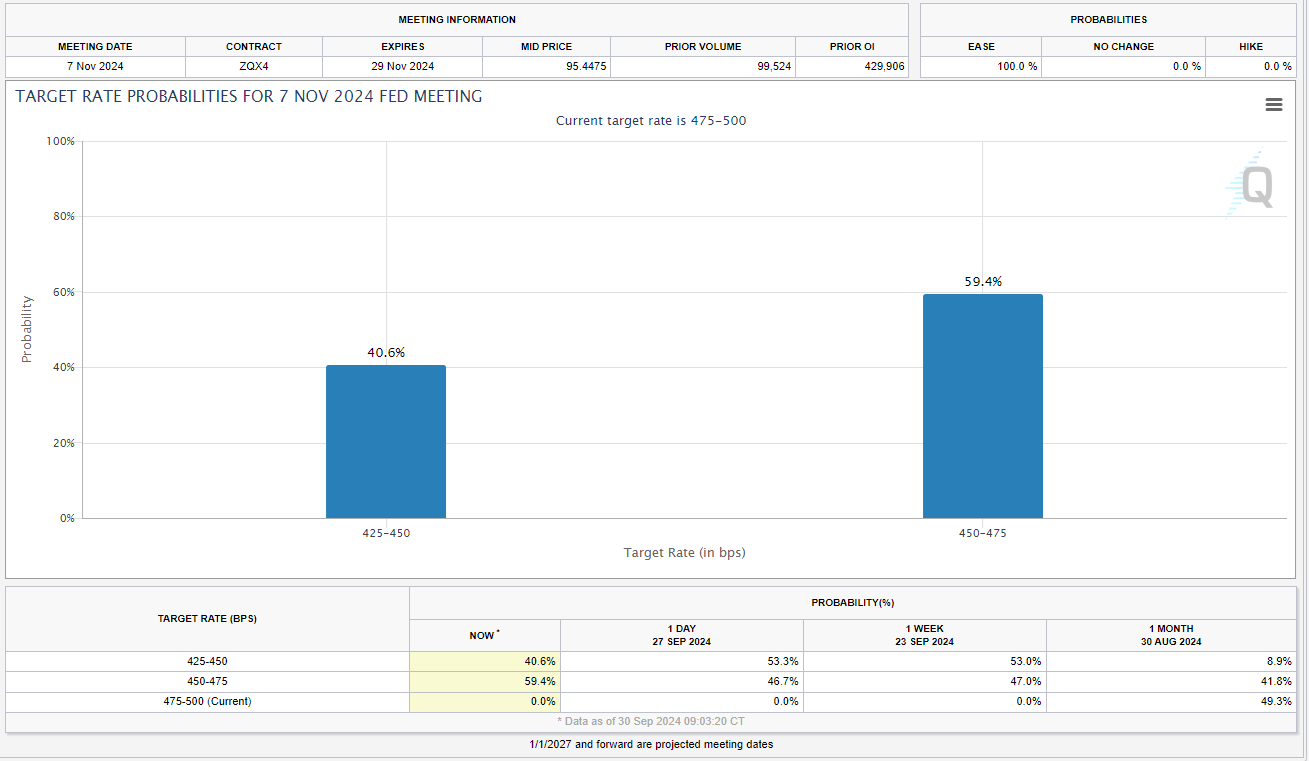

As things stand, markets could continue to range ahead of the jobs data on Friday. Any increase in rate cut expectations could lead to USD weakness. Current expectations have a 50 basis point cut in November at around 40%, down from 53% a day ago and could be partially responsible for the drop in the price of the precious metal.

Source: CME FedWatch Tool (click to enlarge)

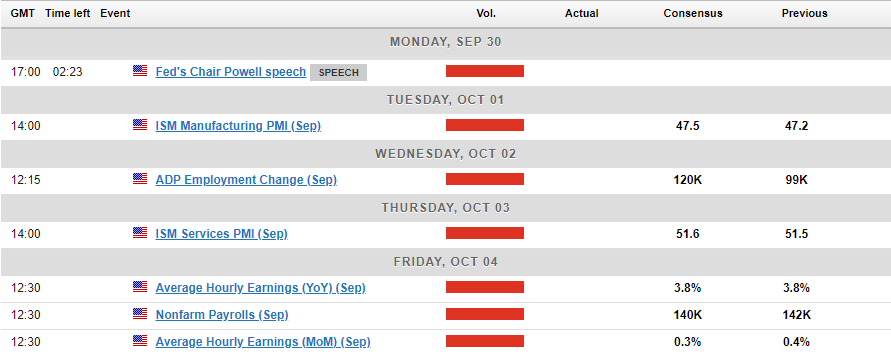

Economic Data Ahead

Gold prices face many challenges at the moment, both positive and negative. Safe haven appeal for now appears to be waning yet a weaker US Dollar as we are seeing today does have the potential to keep gold prices on the front foot.

There is a host of US data this week including services data, however the biggest volatility and potential for a change will come on Friday when the US jobs report is released. Signs of improving jobs numbers and a drop in the unemployment rate could push the precious metal lower.

Later in the day we do have a speech from Fed Chair Jerome Powell which could stoke volatility if the Fed President touches on rate cut expectations moving forward.

Technical Analysis Gold (XAU/USD)

From a technical analysis standpoint, Gold is tough to read at the minute particularly where areas of resistance is concerned. As we continue to print fresh all time highs it makes it difficult due to the lack of historical price data to analyze.

To put things into perspective, the RSI on the daily, weekly and monthly timeframe are all in overbought territory. However, as we know an instrument can languish weeks and sometimes months in overbought territory on the larger timeframes so this seems to be irrelevant at present.

The psychological 2650 mark is the most immediate area of resistance i would keep an eye on A break beyond that could open up a retest of last weeks and the all-time high print around 2685.50 before the 2700 comes into focus.

Looking at support and the 2625 area has been key over the last couple of days and could still serve as a base for gold prices. This may be a level worth monitoring moving forward.

GOLD (XAU/USD) Four-Hour (H4) Chart, September 30, 2024

Source: TradingView (click to enlarge)

Support

- 2625

- 2600

- 2585

Resistance

- 2650

- 2675

- 3000

How is Gold Prepping for NFP?

Gold prices are holding steady near $2,650 in Asian trading on Monday, despite positive market sentiment from China's new stimulus measures. Traders are hesitant to make any big moves before the speech from US Federal Reserve (Fed) Chairman Jerome Powell later today. Powell didn’t touch on the economy or monetary policy in his last speech, so investors are looking forward to hearing any clues on the possible interest rate cut in November.

Currently, the market sees a 52% chance of the Fed cutting rates by 50 basis points in November, according to the CME Group’s FedWatch Tool, slightly up from last week’s 50% odds. The recent US inflation data, especially the core Personal Consumption Expenditures (PCE) price index, hasn’t changed expectations. While the annual core PCE rate moved closer to the Fed's 2% target, Gold still pulled back from last week’s high of $2,686 as traders took profits ahead of key US employment data. Despite ongoing geopolitical tensions in the Middle East and fresh Chinese stimulus, Gold prices continue to face downward pressure Today.

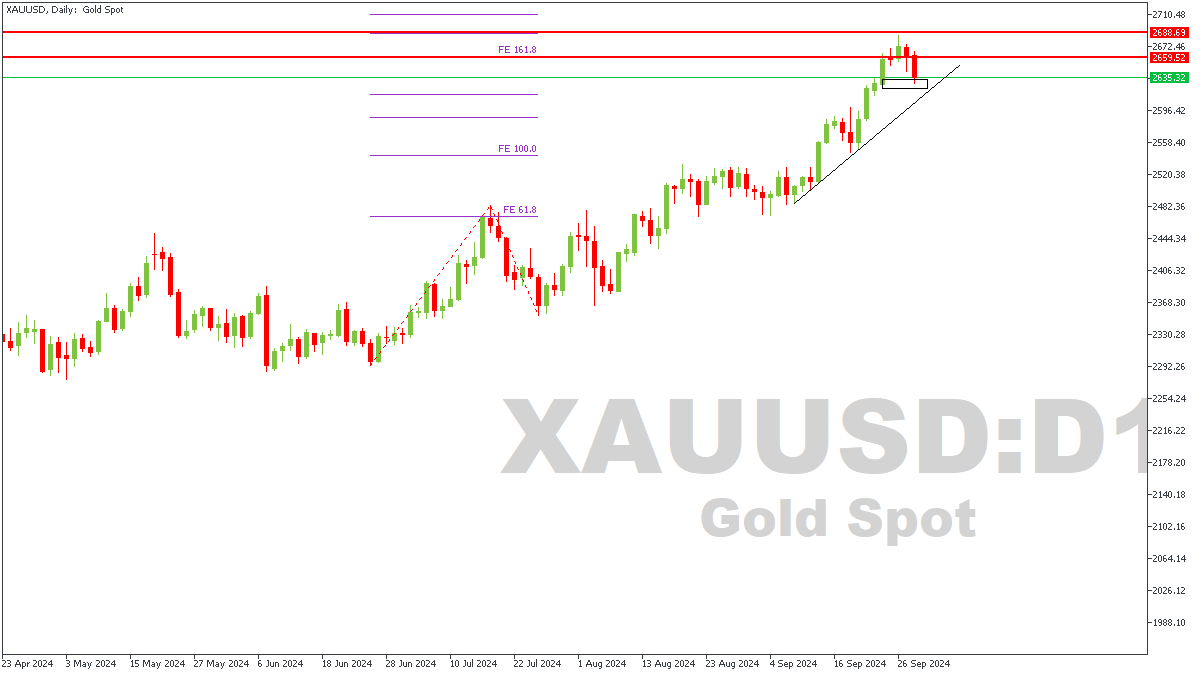

XAUUSD – D1 Timeframe

The two horizontal red lines you’re seeing on this daily timeframe chart of XAUUSD represent the pivots based on the Fibonacci expansion tool. Now, the fact that Gold is at an All-Time-High (ATH) necessitated the use of the Fibonacci expansion tool to figure out future pivots. We have also seen an initial rejection from this area, leading me to vote in favor of the ‘Bears.’

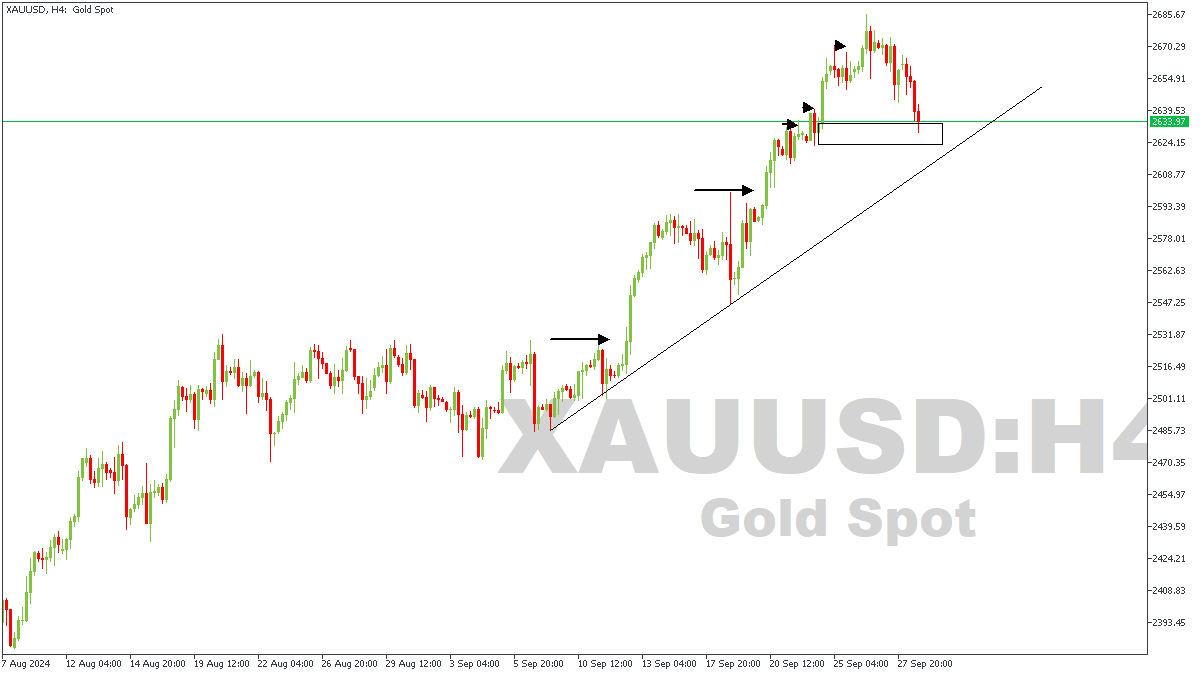

XAUUSD – H4 Timeframe

The 4-hour timeframe sheds more light into the criteria required for the confirmation of the bearish sentiment. The decider in this case being the break below the trendline support and the highlighted demand zone. Patience is advised, since a retest of the broken demand zone will provide a much safer point of entry than the aggressive approach.

Analyst’s Expectations:

- Direction: Bearish

- Target: $2,541.13

- Invalidation: $2,675.85

GBPUSD & EURUSD Outlook

The US Dollar (USD) is struggling to gain strength as it begins the last trading day of the third quarter. Investors are closely watching for inflation data from Germany and speeches from key Federal Reserve officials, including Chairman Jerome Powell, later in the day. On Friday, the USD Index fell to its lowest point in over a year, hitting 100.15, before slightly recovering. Early Monday, the USD Index is still under pressure, staying below 100.50. Meanwhile, US stock index futures are trading slightly lower.

In China, economic data showed a decline in both the manufacturing and services sectors, putting more pressure on the country’s already struggling economy. However, the Australian dollar (AUD) has benefited from positive business confidence data, pushing AUDUSD to its highest level since February 2023. In the UK, revised GDP data showed slower growth than initially reported, but GBPUSD remains steady just below 1.3400.

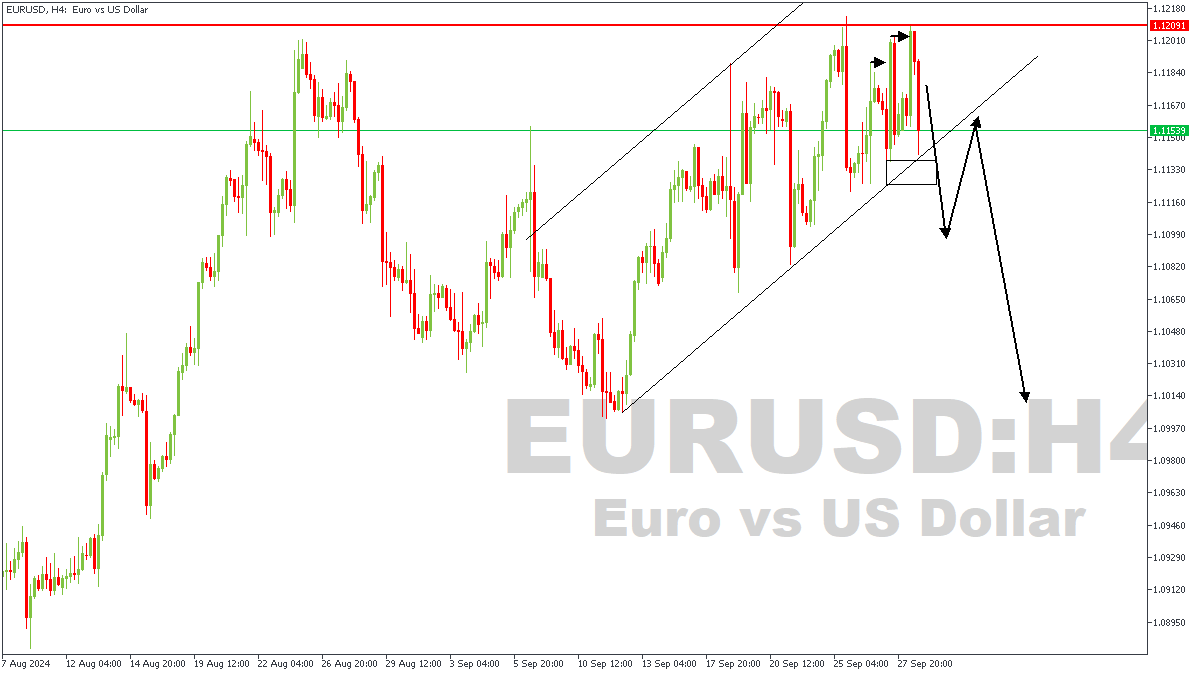

EURUSD– H4 Timeframe

The price on the 4-hour timeframe of EURUSD has recently come under heavy rejection from the daily timeframe pivot, leading to a suspicion that a bearish shift in market structure could be underway. The outcome is however going to depend on the ability of the momentum to break below the confluence region of the trendline support and the demand zone. What I mean is that if price can successfully break below the trendline and the demand zone, we would have confirmation of the bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.10460

- Invalidation: 1.12033

GBPUSD – H4 Timeframe

Price action on the 4-hour timeframe of GBPUSD closely mirrors what we have on the same timeframe chart of EURUSD. In the case of GBPUSD though, the rejection is coming from a pivot some within an area of imbalance on the weekly timeframe. The expected outcome is however the same. I’m looking forward to a break in the market structure, as well as the trendline as the requisite confluence for the bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.32176

- Invalidation: 1.34414