Sample Category Title

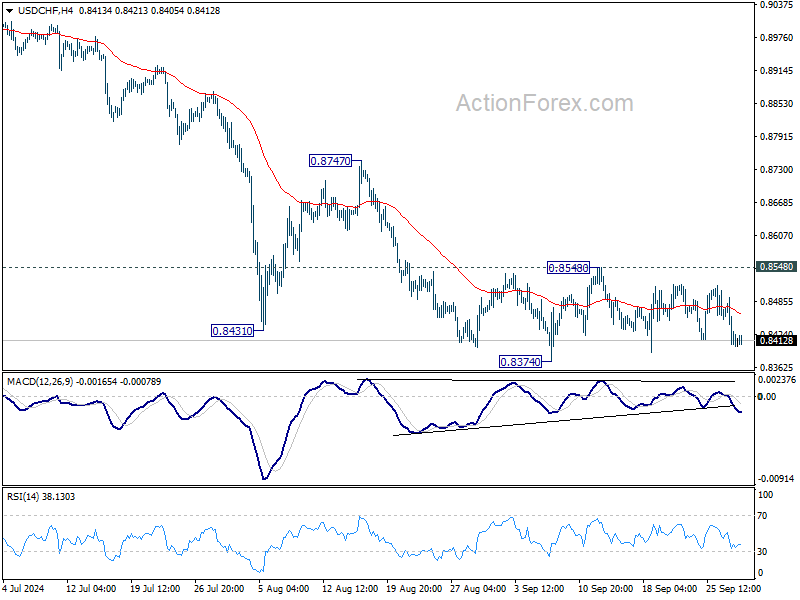

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8374; (P) 0.8433; (R1) 0.8465; More…

Intraday bias in USD/CHF remains neutral as range trading continues above 0.8374. Further decline is in favor with 0.8548 resistance intact. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. Nevertheless, firm break of 0.8548 will turn bias back to the upside for stronger rebound to 0.8747 resistance instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

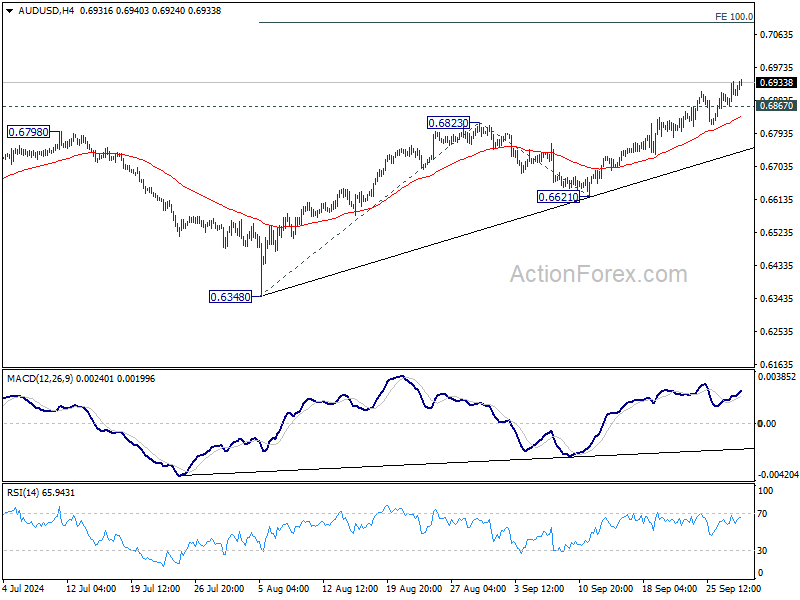

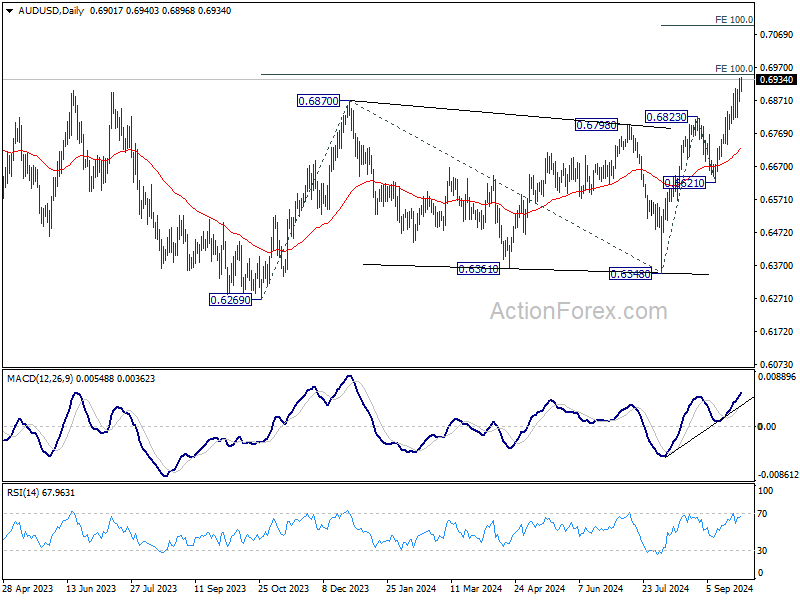

AUD/USD Daily Report

Daily Pivots: (S1) 0.6868; (P) 0.6902; (R1) 0.6937; More...

Intraday bias in AUD/USD remains on the upside for the moment. Current rally from 0.6340 should target 100% projection of 0.6348 to 0.6823 from 0.6621 at 0.7096. On the downside, below 0.6867 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

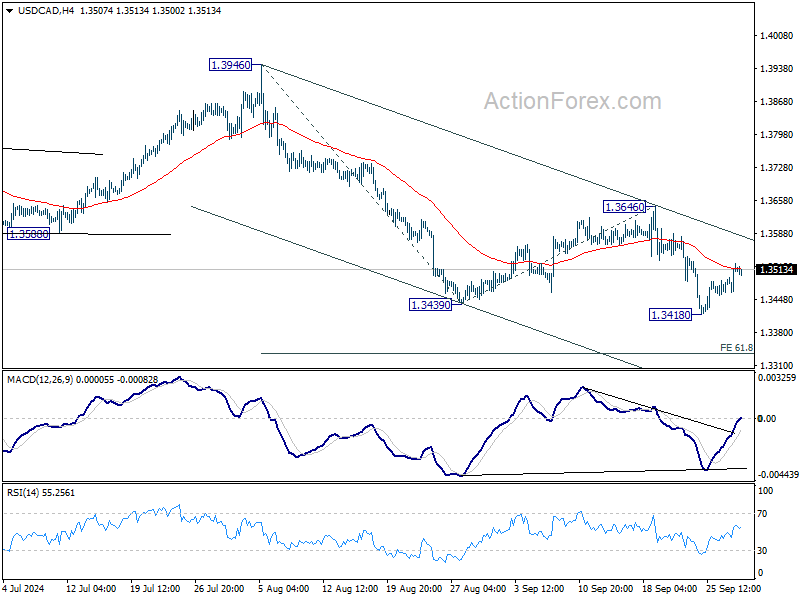

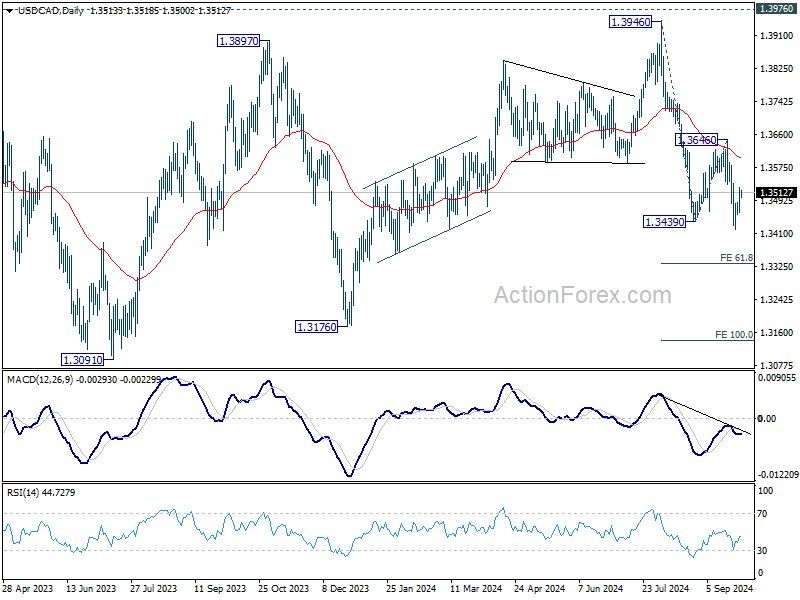

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3477; (P) 1.3502; (R1) 1.3540; More...

Intraday bias in USD/CAD remains neutral for the moment. While recovery from 1.3418 might extend higher, outlook will stay bearish as long as 1.3646 resistance holds. On the downside, break of 1.3418 will resume the fall from 1.3946 to 61.8% projection of 1.3946 to 1.3439 from 1.3646 at 1.3333.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

Swiss KOF rises to 105.5, economy slowly working out of trough

Swiss KOF Economic Barometer edged higher in September, rising from 105.0 to 105.5, surpassing market expectations of 102.0. This modest increase reflects a slow but steady recovery in the Swiss economy, with KOF noting that "the Swiss economy is slowly working its way out of the trough."

According to KOF, nearly all sectors show signs of a more favorable outlook. Manufacturing industry, in particular, has seen the most significant improvement, while financial and insurance services, construction, and other service sectors also show positive momentum.

Hospitality industry continues to maintain above-average prospects, with little change compared to prior months. On the demand side, consumer demand indicators remain stable and point to further growth. However, KOF highlighted that indicators for future foreign demand have weakened, suggesting potential challenges for Swiss exports going forward.

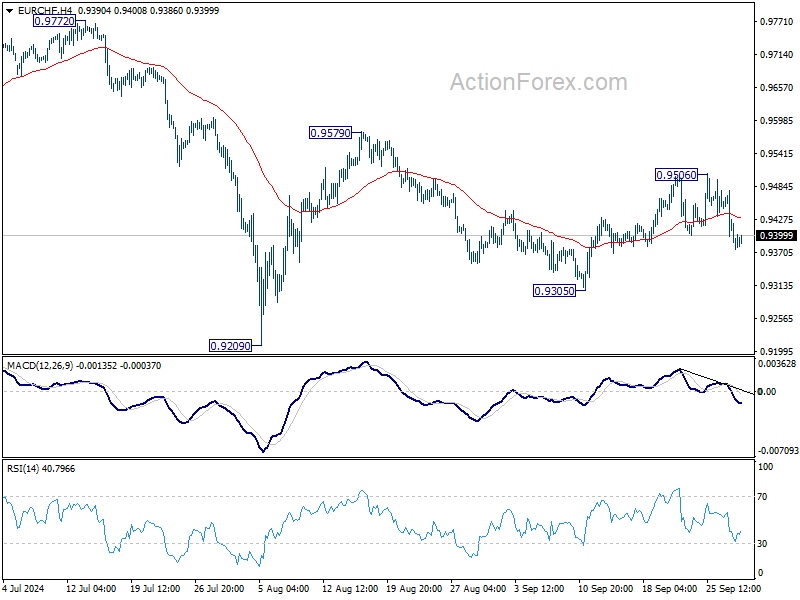

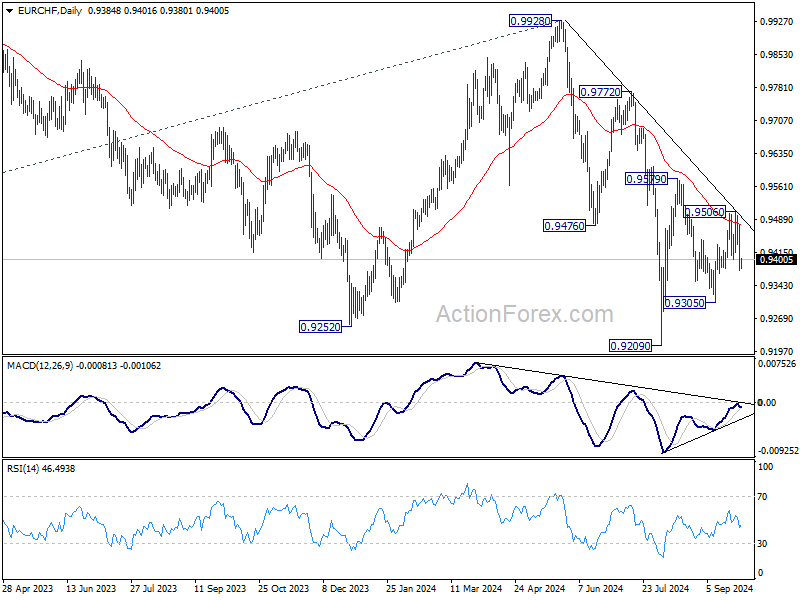

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9348; (P) 0.9413; (R1) 0.9449; More....

Intraday bias in EUR/CHF stays neutral for the moment. On the upside, above 0.9506 will resume the rebound from 0.9305 to 0.9579 resistance. However, break of 0.9305 will resume the fall for 0.9579 to retest 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

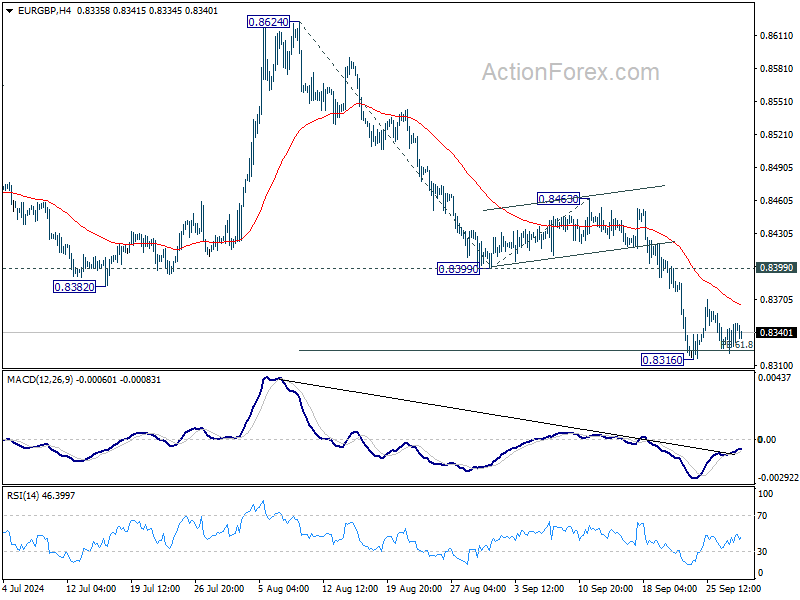

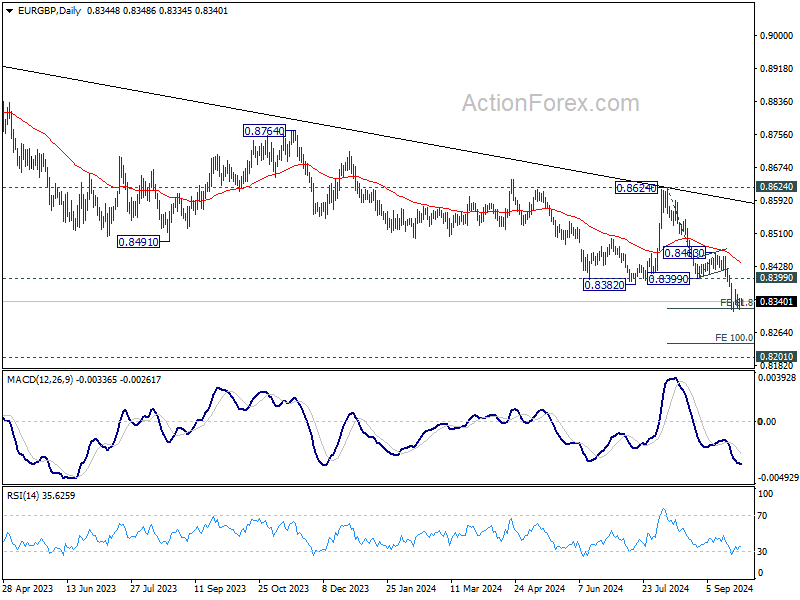

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8330; (P) 0.8340; (R1) 0.8358; More...

Intraday bias in EUR/GBP remains neutral for the moment, and more consolidations could be seen above 0.8316. Outlook will stay bearish as long as 0.8399 support turned resistance holds. On the downside, below 0.8316 will resume the fall from 0.8624 to 100% projection of 0.8624 to 0.8399 from 0.8463 at 0.8237 next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.

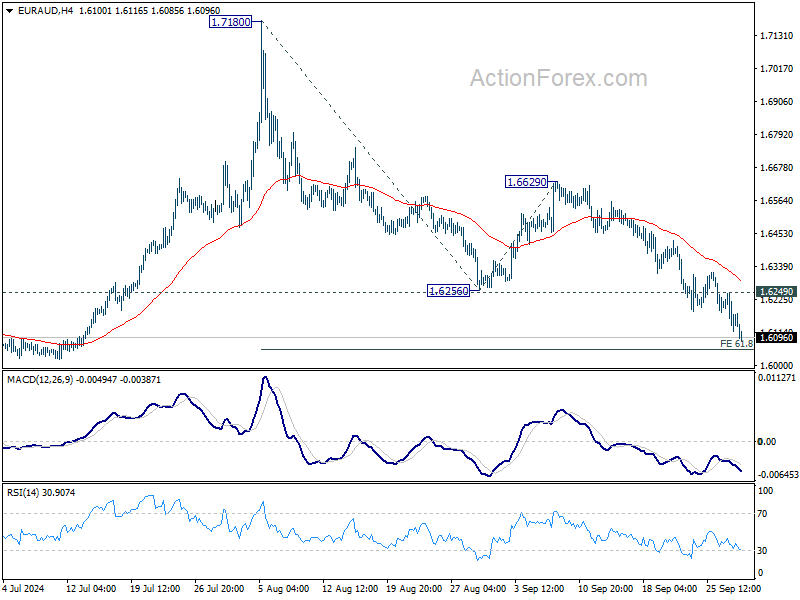

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6112; (P) 1.6181; (R1) 1.6245; More...

Intraday bias in EUR/AUD remains on the downside. Fall from 1.7180 is in progress for 61.8% projection of 1.7180 to 1.6256 from 1.6629 at 1.6058, and possibly below. But strong support should be seen from 1.5996 to contain downside and bring rebound. On the upside, above 1.6249 minor resistance will turn intraday bias neutral first.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still in favor to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed.

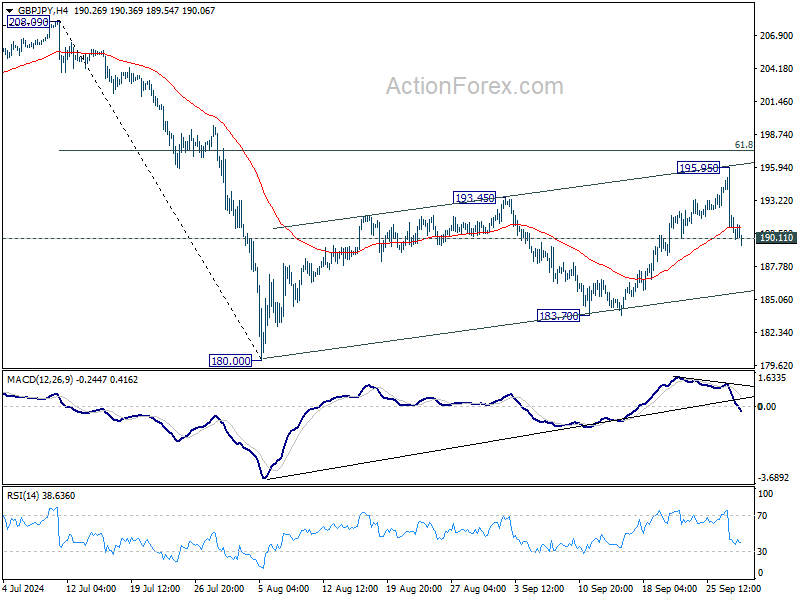

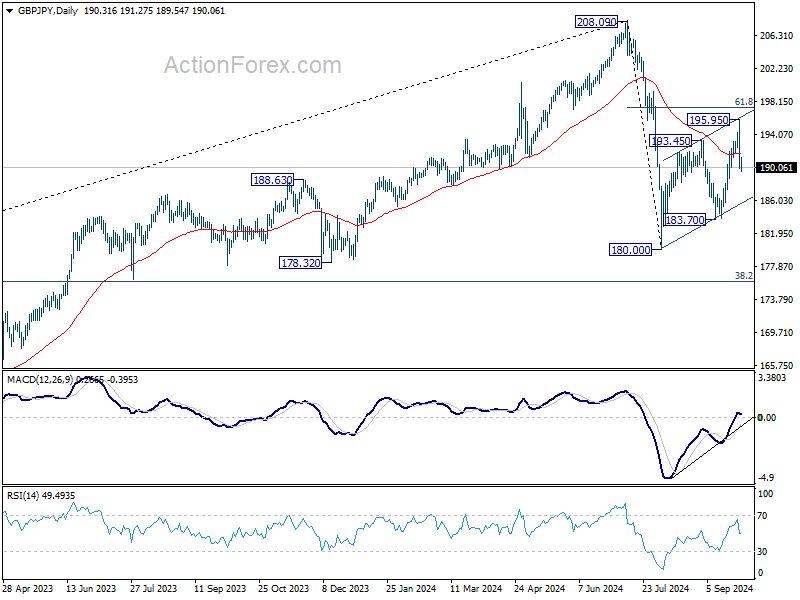

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.10; (P) 192.03; (R1) 194.06; More...

GBP/JPY's break of 190.11 support suggests that corrective pattern from 180.00 has completed with three waves up to 195.95 already. Intraday bias is now on the downside. Deeper decline would be seen back to 183.70 support next. For now, risk will stay on the downside as long as 195.95 resistance holds, in case of recovery.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

A Big Day and Big Week Ahead

Markets

We have a big day and big week ahead in terms of eco data and central bank speeches. EMU headline inflation (tomorrow) is on track to drop below the ECB’s 2% inflation target for the first time since June 2021 following downward surprises in French and Spanish readings end last week. German figures are released today. The September drop is mainly energy-inspired though as ECB President Lagarde suggested already at the Q&A session of the previous ECB meeting: “We are looking at a whole battery of indicators. And I’m saying that in particular because September will certainly deliver a low reading of inflation. Very likely. We expect, because of the base effect, particularly on energy, our inflation numbers to be up in the fourth quarter, so the last three months of 2024. But September is going to deliver a low reading.” While EMU money markets have been eager to nearly fully discount a 25 bps October ECB rate cut on the back of these softer national CPI readings and weak September PMI’s, we still tend to err on the side of the status quo. Unless the ECB president herself convinces us otherwise at an hearing in front of the European parliament later today.

The US eco calendar kicks off with the September Chicago PMI and with a speech by Fed Chair Powell at the National Association for Business Economics after European close. We are looking for clues in the comments (and the rest of this week’s figures) to strengthen our 50 bps Fed rate cut call for November. US money markets are currently evenly split between a 25 bps and a 50 bps scenario. That means room for market moves with a potential bull steepening of the US yield curve, a narrowing of the short-term spread differential between the US and Europe and a continuation of the sell-on-upticks in the greenback. Other eco data to spark volatility later this week are JOLTS job openings and manufacturing ISM (tomorrow), ADP employment change (Wednesday), weekly jobless claims and services ISM (Thursday) and payrolls (Friday). Unionized dockworkers are likely to start with strikes in many East Coast and Gulf Coast ports as their labor contracts expire today which is a wildcard for this week. They remain at odds with employers over the level of pay increases, with unions pushing for a 77% increase for workers over six years. West Coast port workers last year secured a 32% increase.

Chinese stock markets surge another whopping 8-10% this morning after three major cities eased rules on housing purchases. That makes a 25% gain for the CSI 300 since authorities started rolling out stimulus measures last week.

News & Views

Austria’s Freedom Party emerged as the biggest party after yesterday’s national elections. The far-right party is estimated to have secured 56 seats out of the 183 up for grabs. All other traditional parties, however, have vowed not to work with the group and instead look to each other for creating an at least 92-seat majority. The People’s Party and the Social Democrats have been the default option, making up more than half of Austria’s governments since WWII. This time around, though, they won 93 seats, making it a very fragile coalition. They could include a third party, most likely the liberal NEOS (18 seats) but finding common ground won’t be easy. Austria already has a tradition for negotiations to take months and talks may stretch well into next year. The outgoing coalition (People’s Party and the Greens) continues to govern in the meantime.

Flanders has formed a government over the weekend, almost four months since the June 9 elections. Matthias Diependaele from the Flemish nationalists N-VA will lead a coalition government that also include Vooruit’s Socialists and the Christian-Democrats. All parties have greenlighted the coalition agreement in the meantime. Some of the most high-profile policy changes include lower taxes for first-home buyers and for small-to-medium sized inheritances, job placement reforms & an easing of the home energy efficiency renovation rules. In addition, the new Flemish government will introduce a traffic tax for EV’s while removing the subsidies for buying one. A previously made pledge to ban the sale of combustion engines by 2029 is scrapped. A whopping €1bn is rolled out for daycare and another €300mln for elder care. The Flemish government also announced an industrial strategy (R&D and innovation). The agreement on the Flemish level potentially strengthens the three-party bloc in the still-ongoing negotiations on a federal level.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) make follow-up moves less evident. We expect the central bank to stick with the quarterly reduction pace. Disappointing US and unconvincing-to-outright-weak EMU activity data dragged the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed kicked off its easing cycle with a 50 bps move. It is headed towards a neutral stance now that inflation and employment risks are in balance. Conservative SEP unemployment forecasts risk being caught up by reality and with it the dot plot (50 bps more cuts in 2024). We hold our call for two more 50 bps cuts this year. Pressure on the front of the curve and weakening eco data keeps the long end in the defensive for now as well.

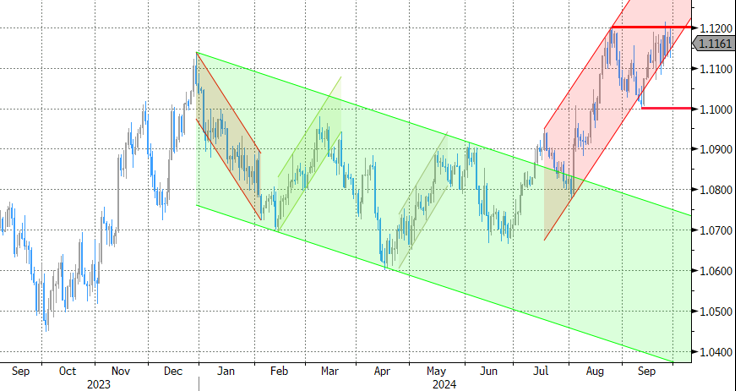

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) only briefly offset some of the general USD weakness. EUR/USD’s dollar-driven ascent is nearing resistance around 1.12 again.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. But the economic picture is increasingly diverging to the benefit of sterling. EUR/GBP succumbed to horrible European September PMI’s. Support at 0.84 broke and brings the 2022 low (0.8203) on the radar.

More Stimulus Before Holiday

The week kicked off with another bull run in Chinese stocks on further stimulus news. This time, three major cities announced to ease homebuying rules to prop up their housing market. The Chinese Communications Constructions surged another 7% following a stellar week, the CSI 300 added another 6% and is up by 25% since the mid-September dip, and the HIS index gained another 3%. The Chinese will be going on national holiday in an excellent mood, and investors – though skeptical that the measures will help lifting the EM giant in the long run – could give some time to the measures to show in the economic data. But data-wise, we are not there just yet. The previous measures announced by the Chinese authorities have barely borne fruit. The Caixin manufacturing index for example unexpectedly shrank into the contraction zone in September, and the services PMI is on the edge, near the 50 level that differentiates expansion from contraction. The Chinese EV sales fell by 48% - and the EU hasn’t yet increased import tariffs on China-made EVs. But anyway, China and its investors are breathing a sigh of relief… the CSI 300 had its best week since 2008, after all. Iron ore is up by 25% since mid-September. And the good news from China and the rising iron ore prices give a decent support to the AUDUSD, preparing to test the 0.70 cents level as Australian stocks extend rally to fresh ATH.

Over in Europe, growth and China-sensitive European stocks are also having their share of the Chinese pie. The Stoxx 600 index closed the week at an ATH. LVMH gained 20% in just a week.

In separate news, inflation data from France and Spain came in lower than expected. Both data slipped below the European Central Bank’s (ECB) 2% policy target in September. German inflation numbers are due today and the Eurozone’s aggregate inflation update is due tomorrow. Softening inflation, combined with Europe’s gloomy economic outlook, has room to boost the ECB rate cut bets, and keep the EURUSD offered near the 1.12 level – even against a broadly softening US dollar.

Across the Channel, Cable consolidates a touch below the 1.34 level and the FTSE 100 is better bid. The Chinese stimulus news is good for the British mining stocks. Increased negative pressure on oil prices weighed on the index last week, after the news that Saudi Arabia was looking to change strategy and focus on increasing its market share rather than trying to prop up oil prices by restricting output. The good news is, even oil seems to be boosted by the Chinese stimulus news since last Friday. Support is building near the $67pb level in WTI.

In Japan, mood is totally different since last Friday. Last week’s elections in Japan resulted in a surprise win of Shigeru Ishiba, who is known for his preference for higher interest rates. The USDJPY tumbled from above 146 to around 142 last Friday and is consolidating gains near this level, the Nikkei index tumbled more than 5% on Friday, sank below its 200-DMA, tested the 50-DMA to the downside and is back to around the 200-DMA this Monday morning. The 3% slump in industrial production in August certainly helped taming the yen bulls, but the rest of the data was good enough to keep the downside pressure in the USDJPY intact; the 140 level is totally within the reach of the yen bulls, especially given the sustained selling pressure on the US dollar, worldwide.

In the US, the data released on Friday printed a set of soft inflation data. The core PCE index, the Federal Reserve’s (Fed) favourite gauge of inflation, came in line with expectations on a yearly basis, and slightly lower than expected, and softer than last month on a monthly basis. The latter reinforced the expectation that the Fed’s next move could be a second 50bp cut. That probability currently stands at 55%, the US 2-year yield remains under pressure, and the major stock indices consolidate near their ATH levels. Friday’s PCE data didn’t spark a fresh wave of buying in the S&P500, but the index renewed record a few times during the course of last week, and the Dow Jones pushed to a fresh high on Friday.

This week, the attention shifts to the US jobs data – expected to print another NFP figure near 140Ks, the unemployment rate is seen stable near the 4.2% while the average earnings may have eased significantly from 3.8% to 3.3% on a yearly basis. A soft set of jobs data should keep the Fed doves in charge of the market.

Elsewhere, the US ports along the East and Gulf coasts are about to go into a strike this Tuesday, as the unions demand higher pay. The market doesn’t seem much worried for now, as most goods are believed to be already in for the upcoming holiday shopping season, but a strike is never good news for supply chains and prices. An extended period of disruption in ports could boost the prices of goods that flow into the country from these ports and generate an upward pressure on inflation.