Sample Category Title

GBP/USD Weekly Outlook

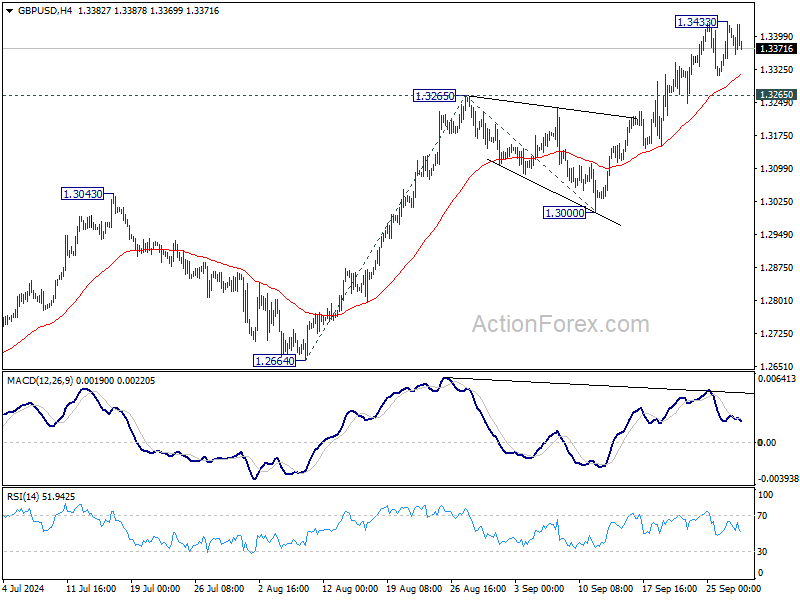

GBP/USD rose further to 1.3433 last week but turned sideway since then. Initial bias remains neutral this week for some more consolidations. But further rally is expected as long as 1.3265 resistance turned support holds. Above 1.3433 will resume larger rise to 100% projection of 1.2664 to 1.3265 from 1.3000 at 1.3601 next. Nevertheless, considering bearish divergence condition in 4H MACD, firm break of 1.3265 will indicate short term topping and turn bias back to the downside for 1.3000 support instead.

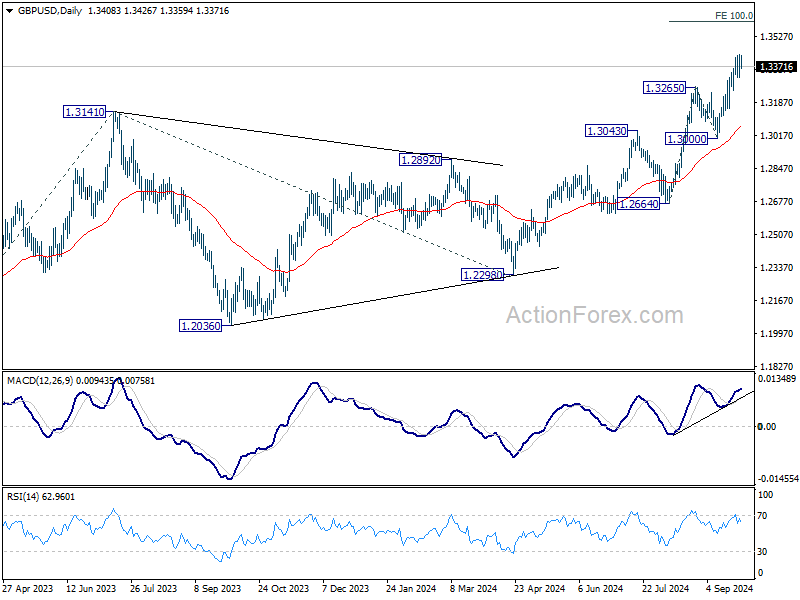

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. For now, outlook will stay bullish as long as 1.3000 support holds, even in case of deep pullback.

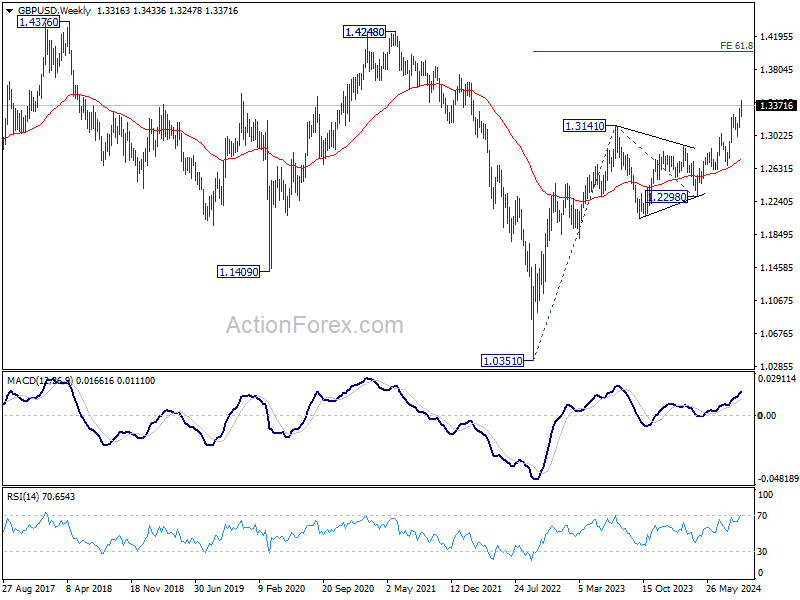

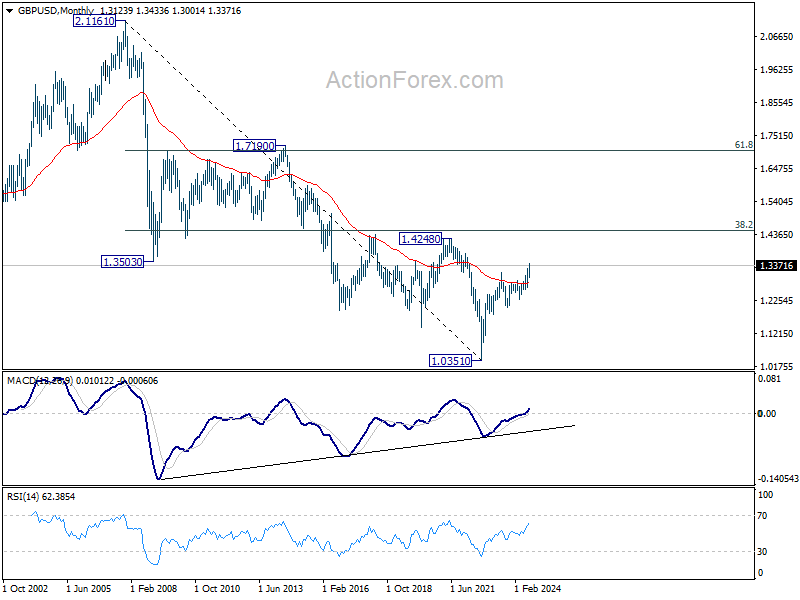

In the long term picture, as long as 1.2298 support holds, rise from 1.0351 long term bottom is expected to continue. The strong break of 55 M EMA (now at 1.2811) is a sign of bullish trend reversal. Yet, break of 1.4248 structural resistance is needed confirm. Otherwise, price actions from 1.0351 could just be part of a consolidation pattern.

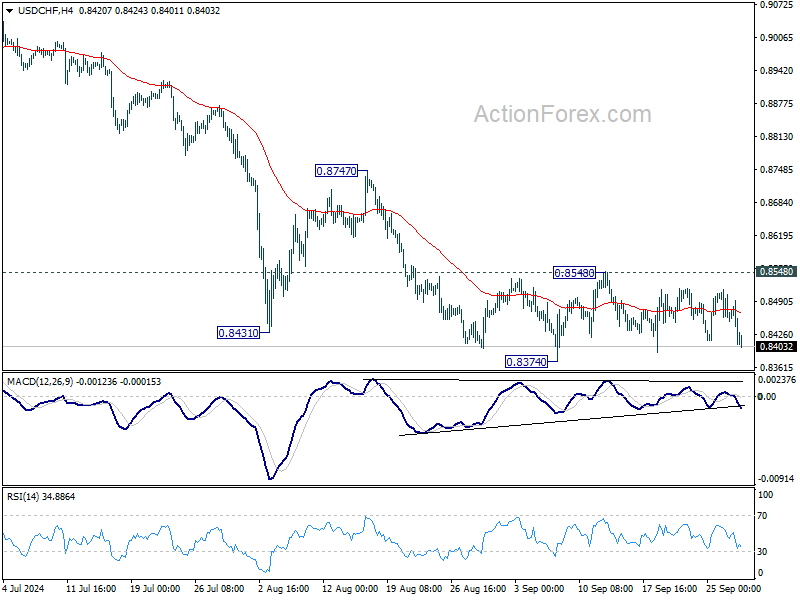

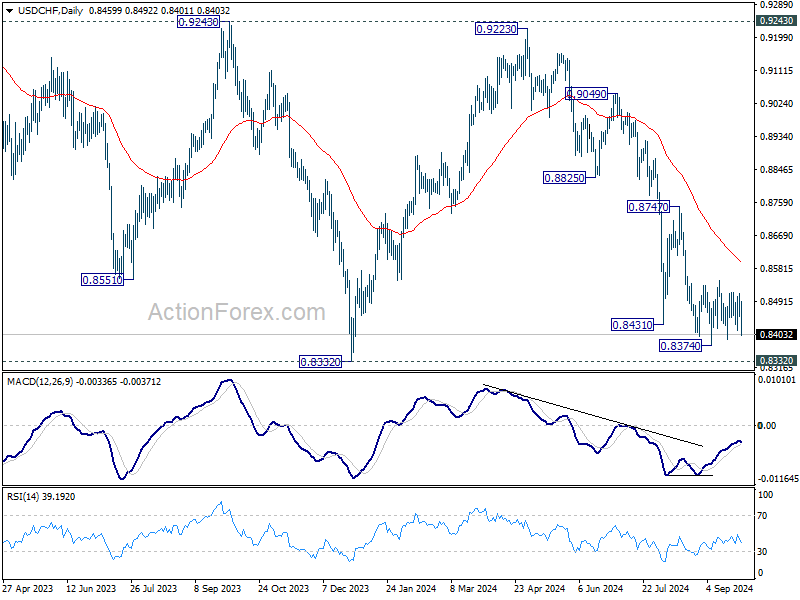

USD/CHF Weekly Outlook

Range trading continued in USD/CHF last week and outlook is unchanged. Further decline is in favor with 0.8548 resistance intact. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. Nevertheless, firm break of 0.8548 will turn bias back to the upside for stronger rebound to 0.8747 resistance instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

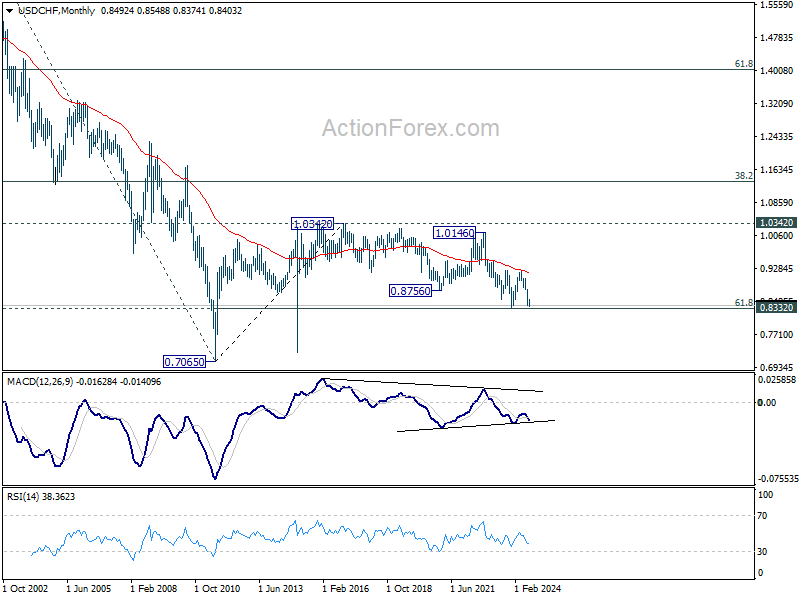

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Rejection by 55 M EMA suggest that this fall is in progress. Break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.

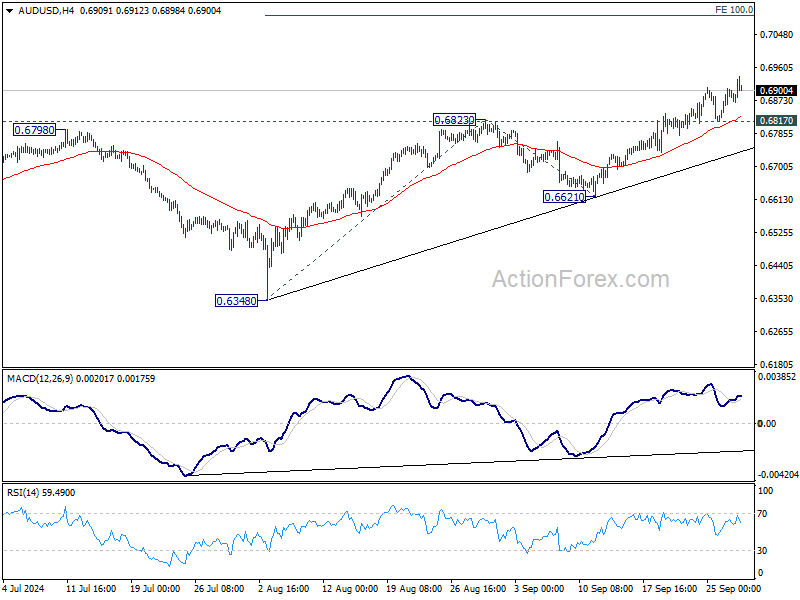

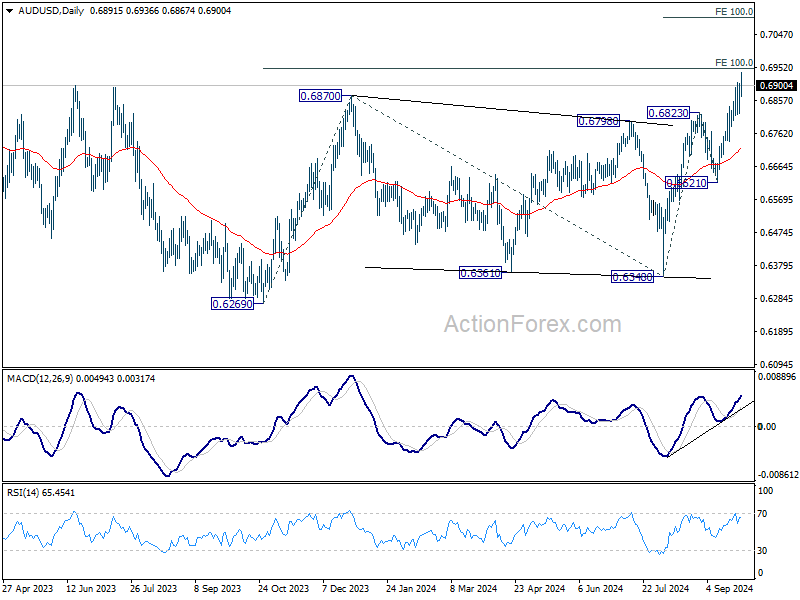

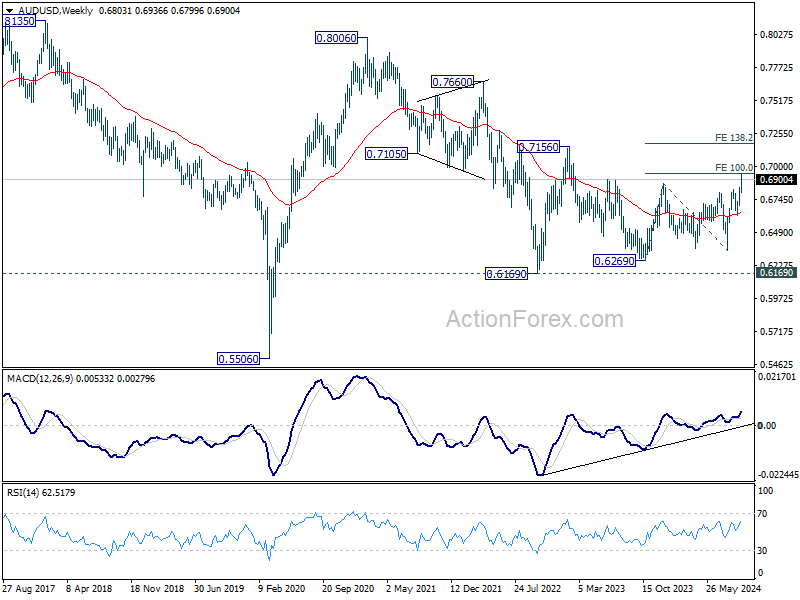

AUD/USD Weekly Report

AUD/USD's rally contained last week and hit as high as 0.6936. Initial bias is on the upside this week. Firm break of 0.6941 will pave the way to 100% projection of 0.6348 to 0.6823 from 0.6621 at 0.7096. On the downside, below 0.6817 support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen as the second leg of the pattern. Firm of 0.7156 resistance will argue that the third leg has already started towards 0.8006.

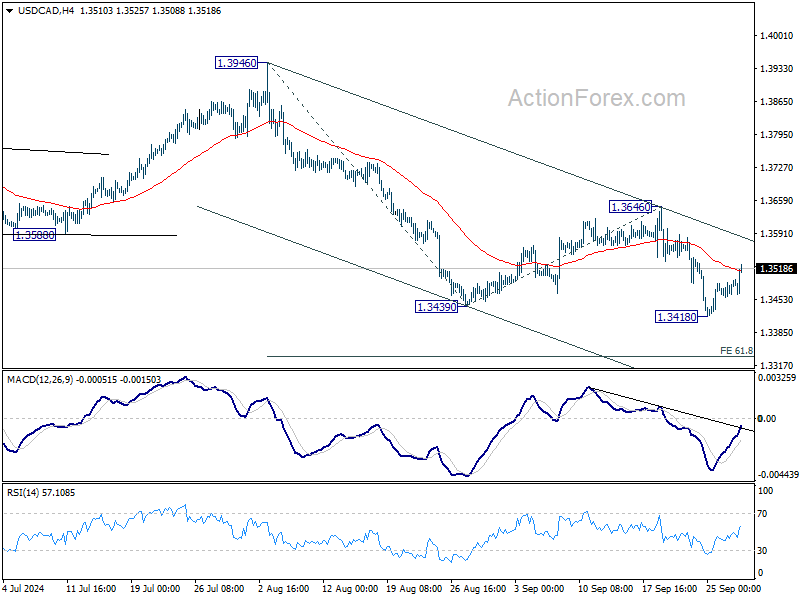

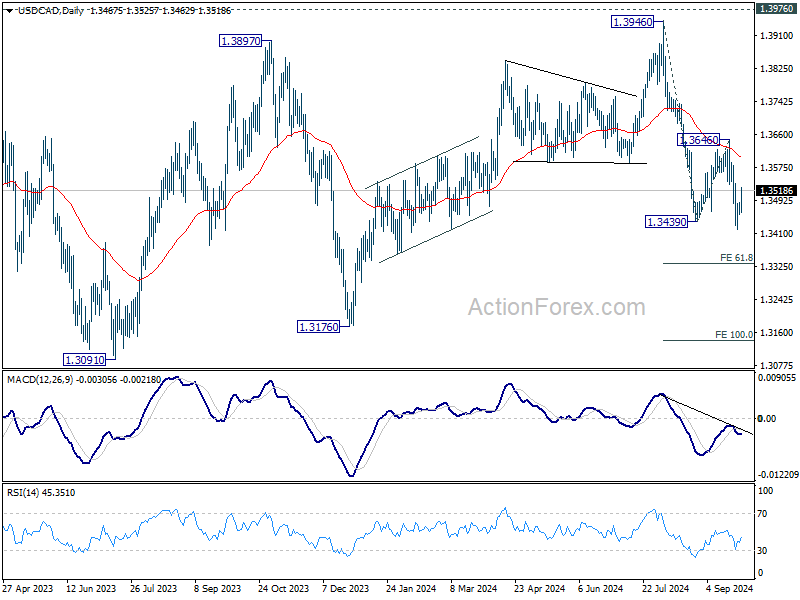

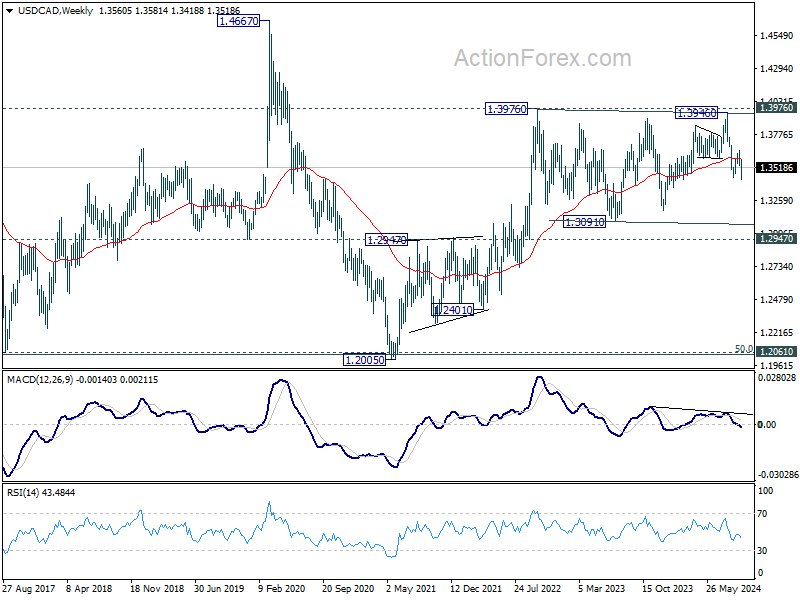

USD/CAD Weekly Outlook

USD/CAD's fall from 1.3946 resumed by breaching 1.3418, but recovered since then. Initial bias remains neutral this week first. Outlook will stay bearish as long as 1.3646 resistance holds. On the downside, break of 1.3418 will target 61.8% projection of 1.3946 to 1.3439 from 1.3646 at 1.3333.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

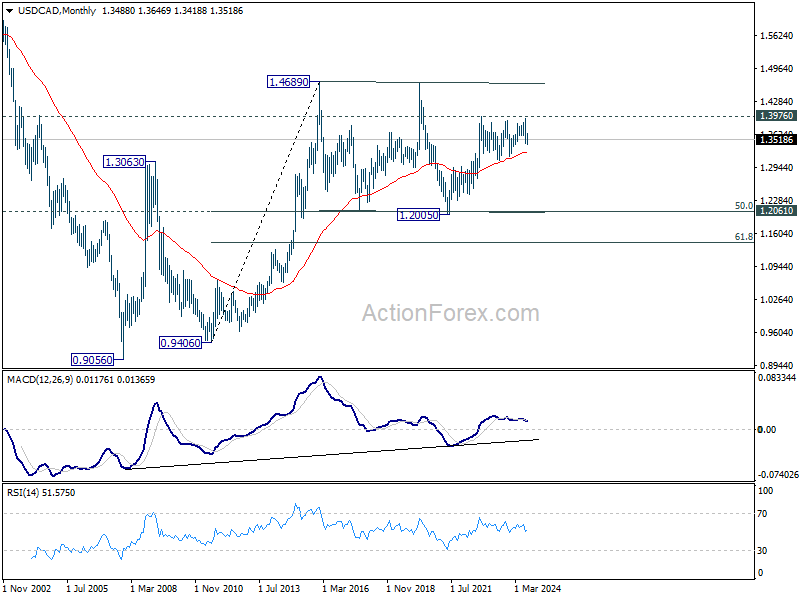

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

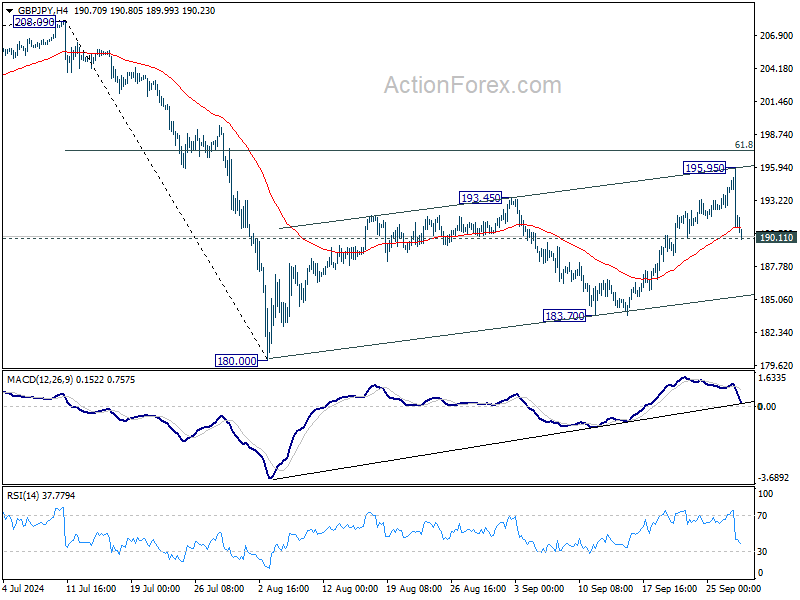

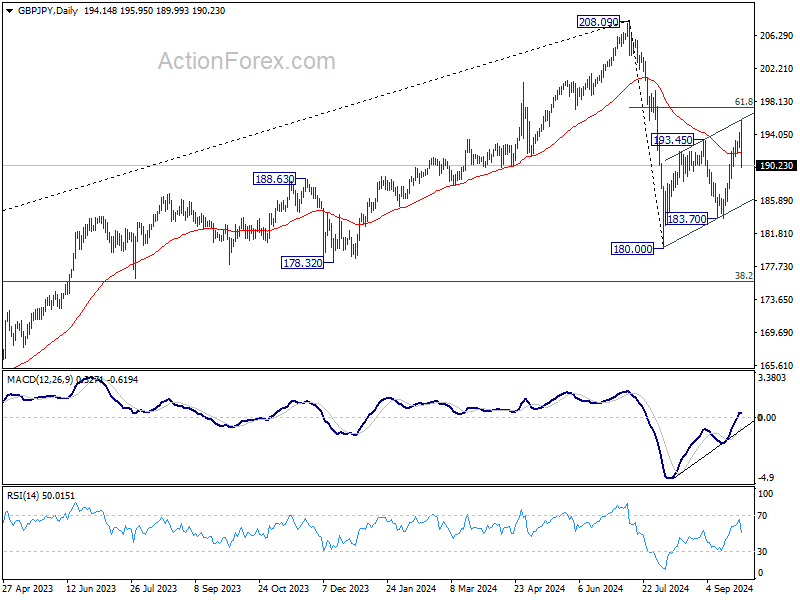

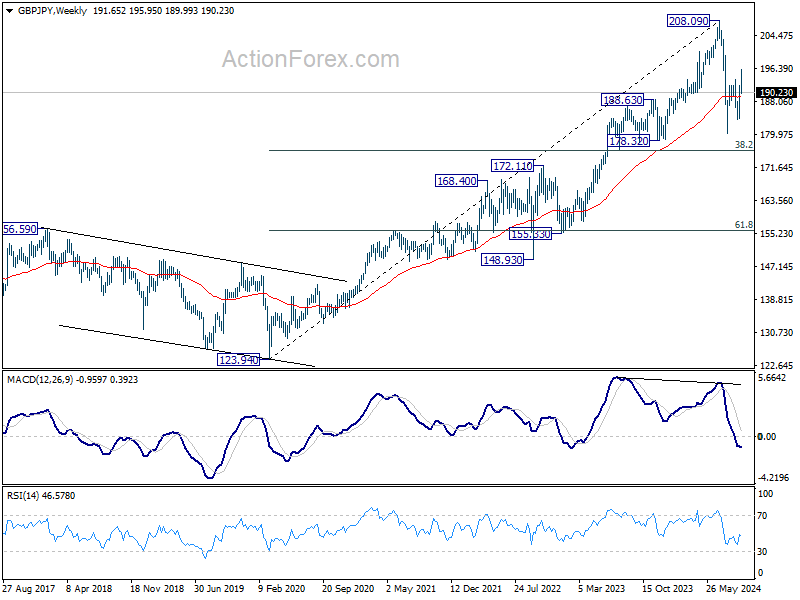

GBP/JPY Weekly Outlook

GBP/JPY retreated sharply after edging higher to 195.95 last week and initial bias is neutral this week first. On the upside, above 195.95 temporary top will extend the corrective rebound from 180.00 to 61.8% retracement of 208.09 to 180.00 at 197.35 next. However, firm break of 190.11 will argue that this correction might have completed, and turn bias back to the downside for 183.70 support next.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

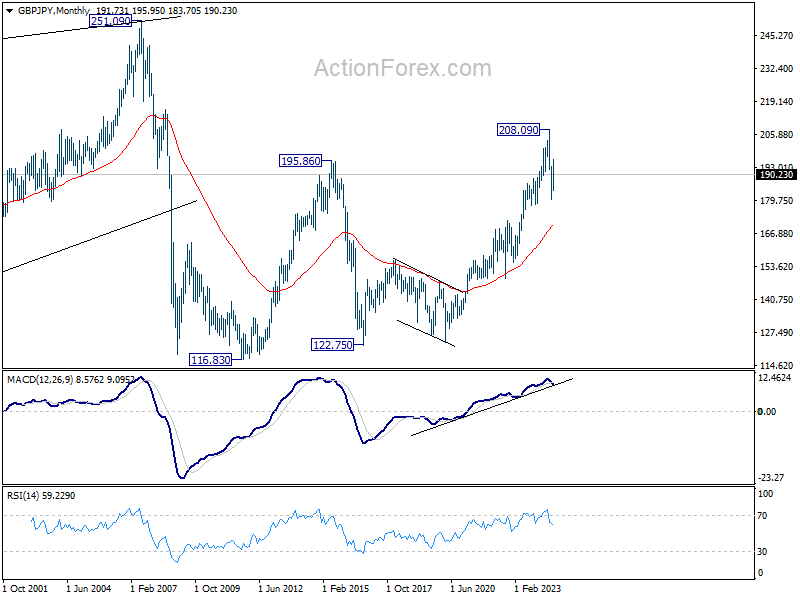

In the longer term picture, considering bearish divergence condition in W MACD, 208.09 is at least a medium term top. It's still early to conclude that the up trend from 122.75 (2016 low) has completed. But it's at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 170.18).

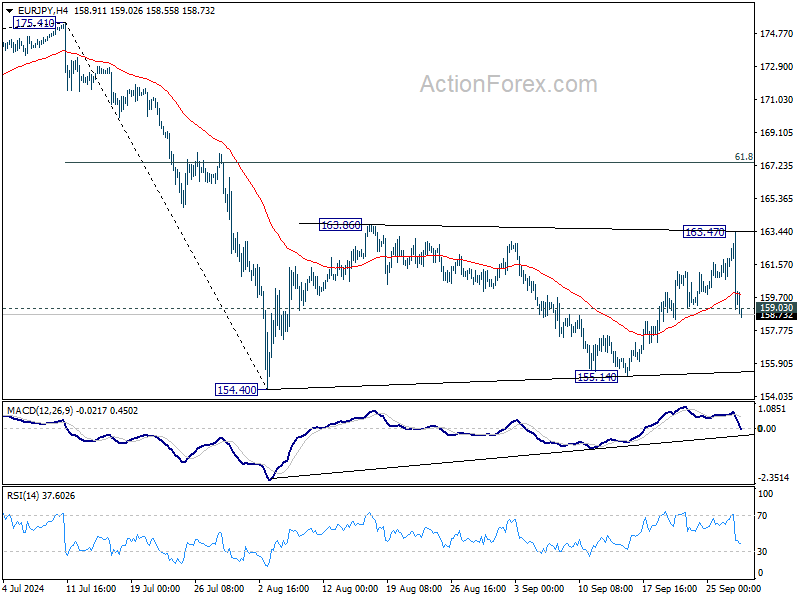

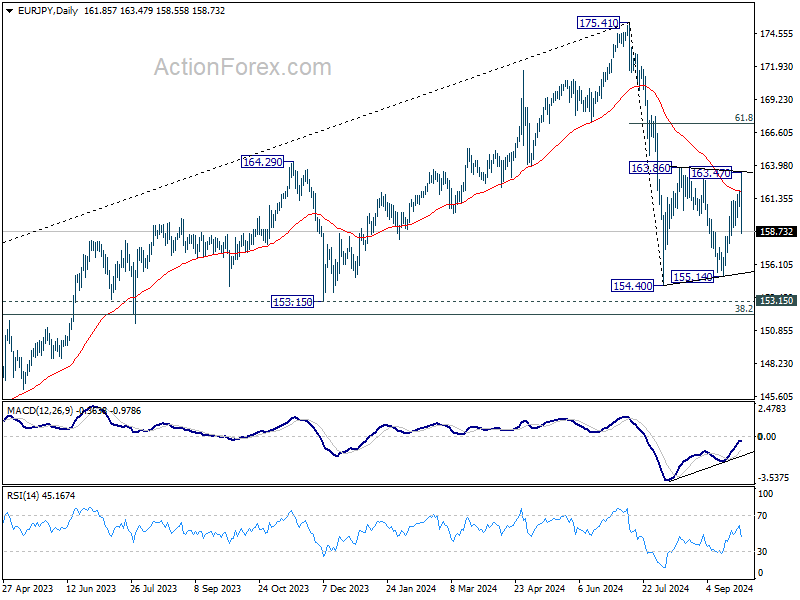

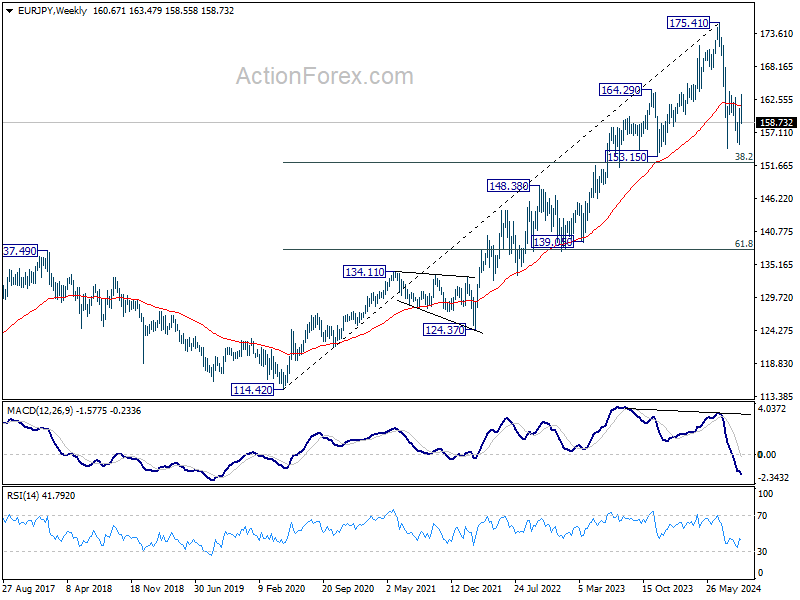

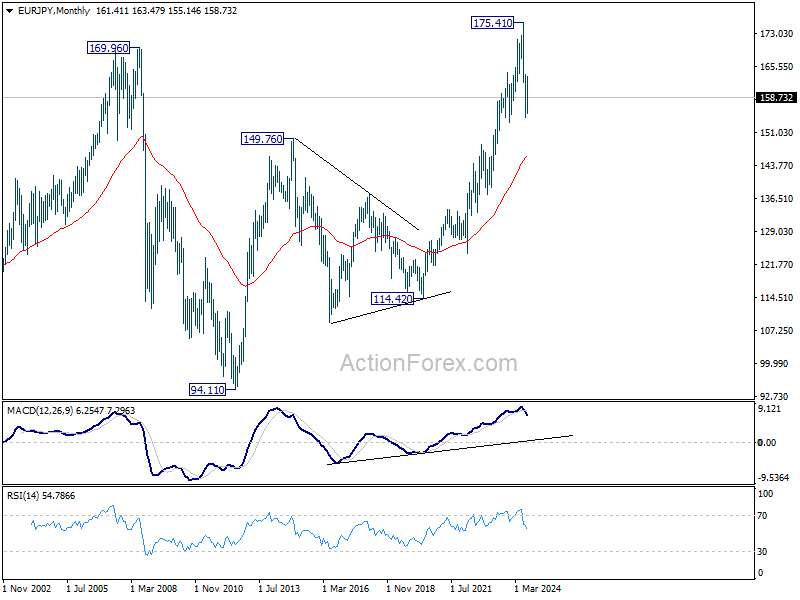

EUR/JPY Weekly Outlook

EUR/JPY reversed after rebounding further to 163.47 last week. The development argues that corrective pattern from 154.40 might have completed with three waves to 163.47 already. Initial bias is back on the downside this week for retesting 154.40/155.14 support zone. For now, risk will stay mildly on the downside as long as 163.47 resistance holds, in case of recovery.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

In the long term picture, considering bearish divergence condition in W MACD, 175.41 is at least a medium term top. It's still early to conclude that up trend from 94.11 (2012 low) has completed. But a medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 145.99).

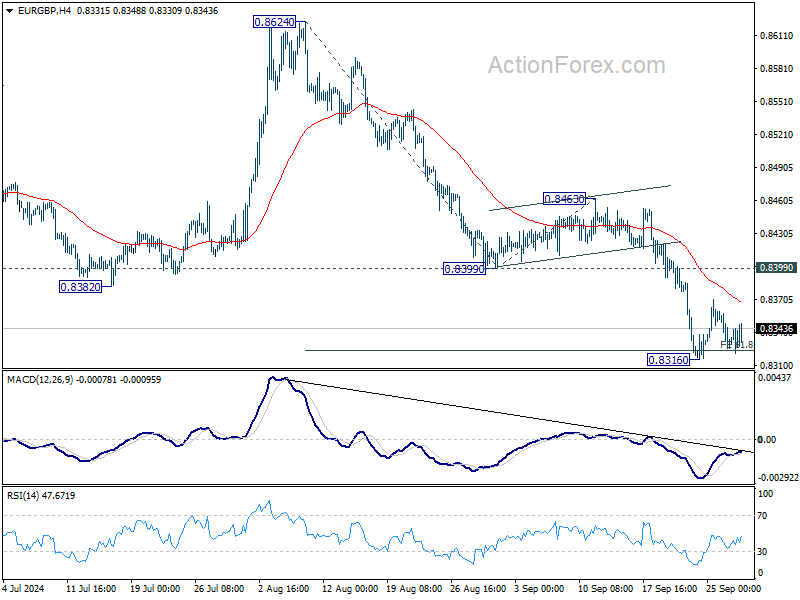

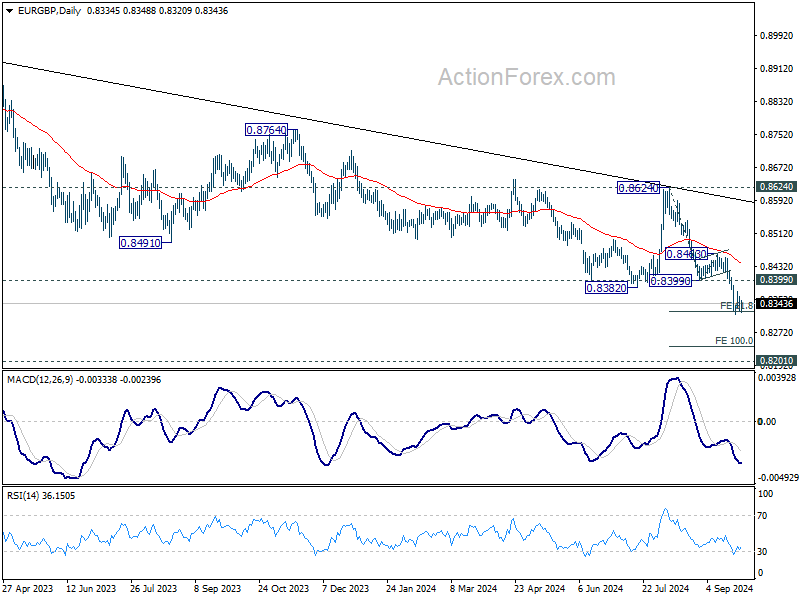

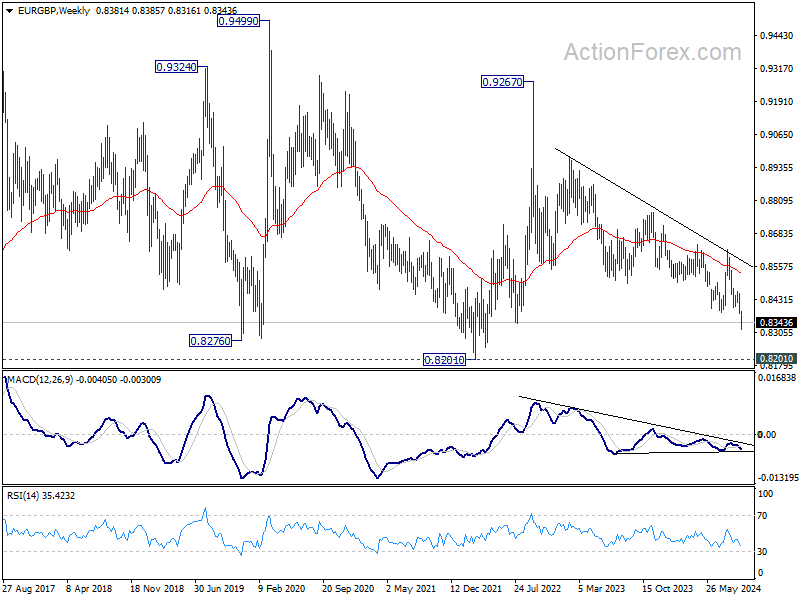

EUR/GBP Weekly Outlook

EUR/GBP's fall from 0.8624extended lower last week but recovered after hitting 61.8% projection of 0.8624 to 0.8399 from 0.8463 at 0.8324. Initial bias stays neutral this week for consolidations, and outlook will stay bearish as long as 0.8399 support turned resistance holds. On the downside, below 0.8316 will resume the fall from 0.8624 to 100% projection at 0.8237 next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.

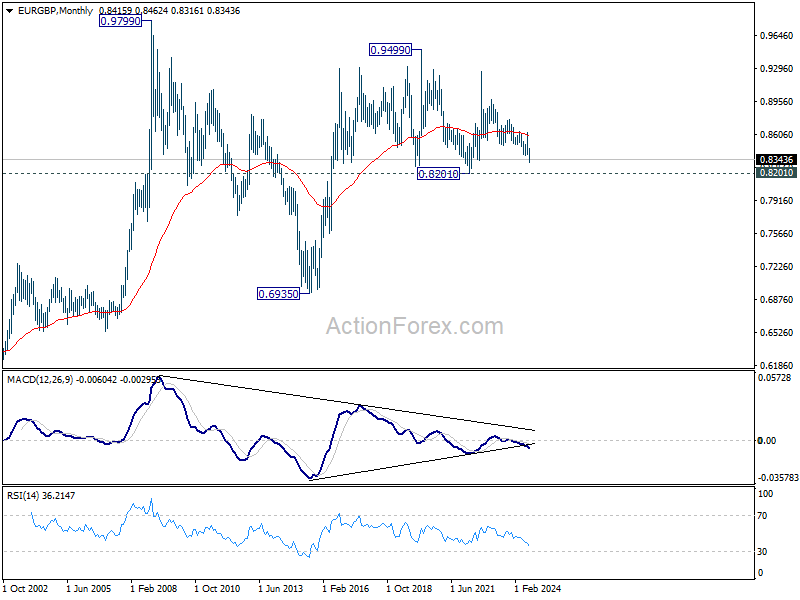

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

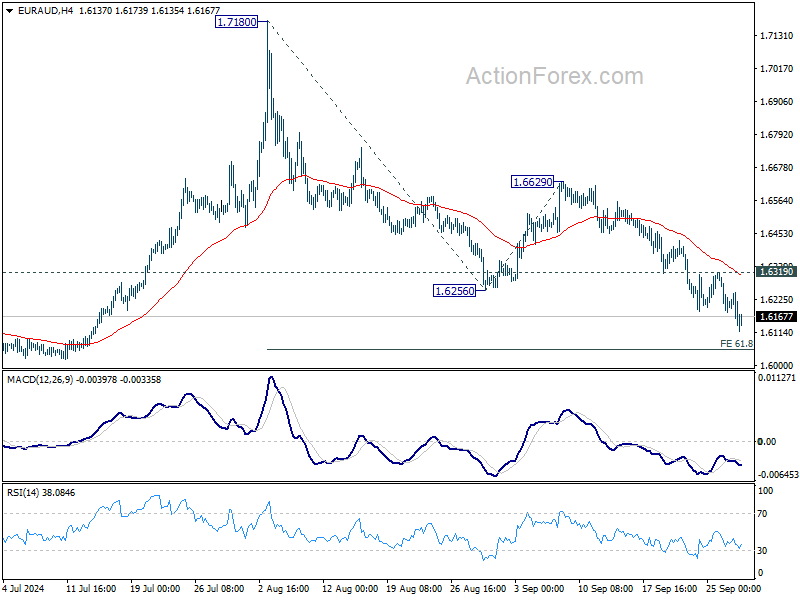

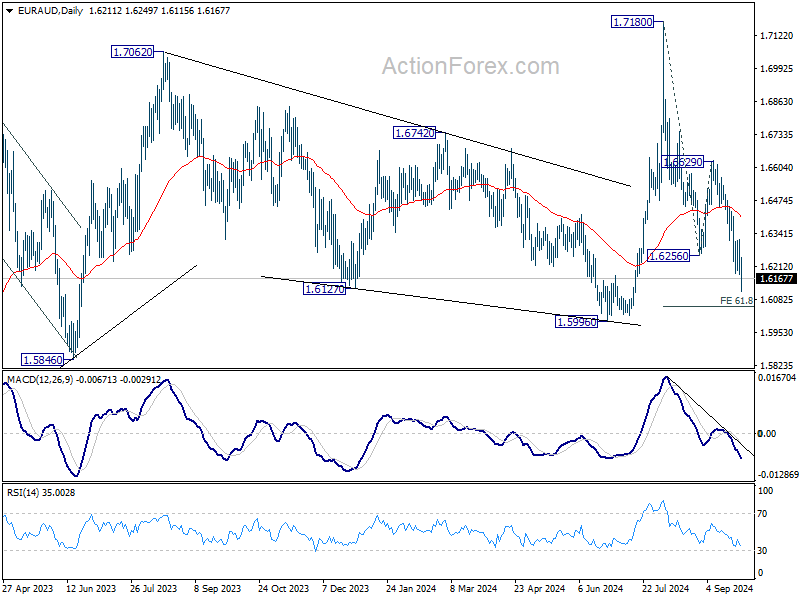

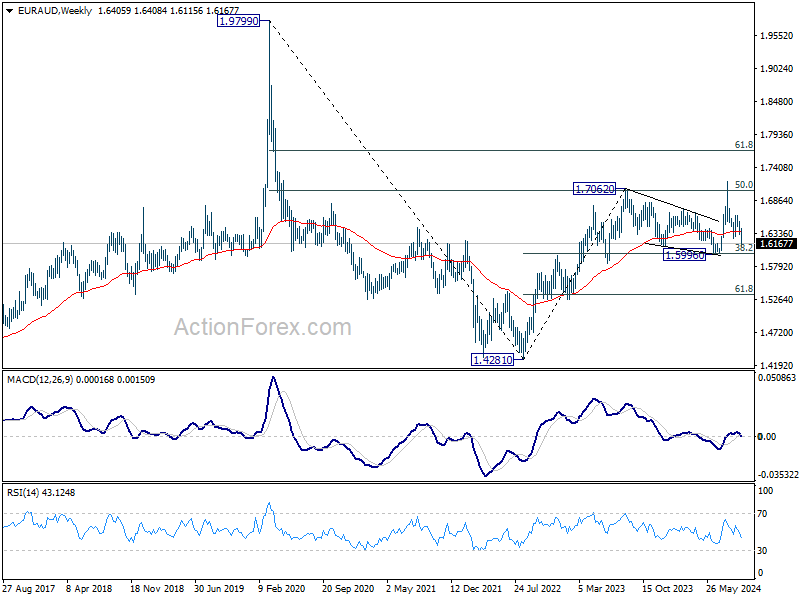

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.7180 resumed by breaking through 1.6256 last week. Initial bias stays on the downside this week for 61.8% projection of 1.7180 to 1.6256 from 1.6629 at 1.6058. Strong support should be seen from 1.5996 to contain downside and bring rebound. On the upside, above 1.6319 resistance will turn intraday bias neutral first.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still in favor to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed.

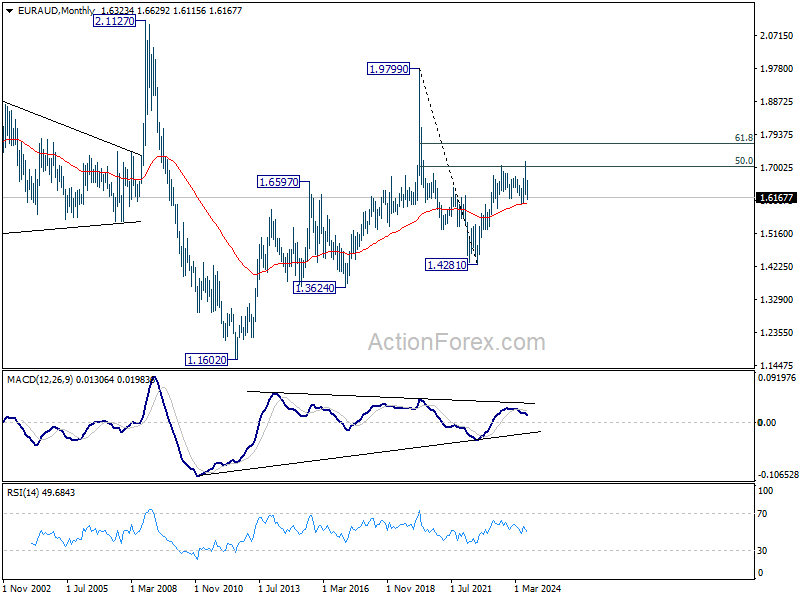

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5999) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

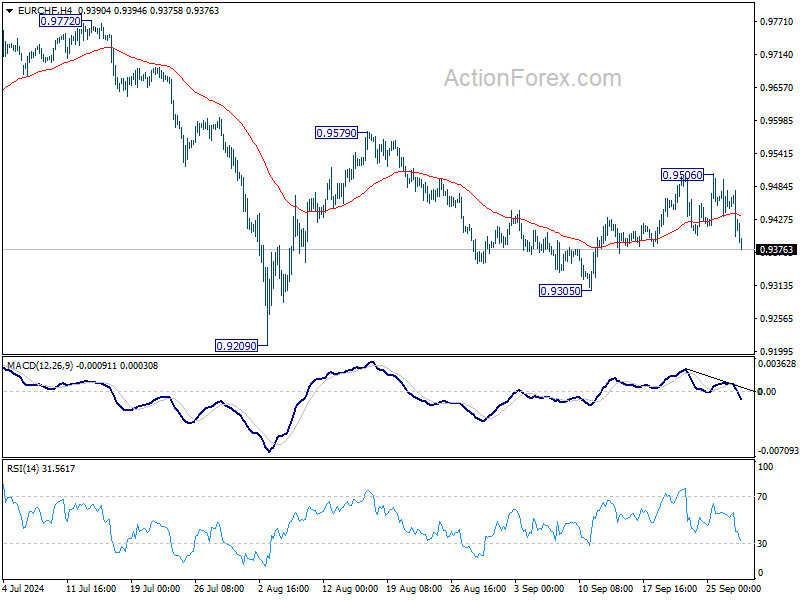

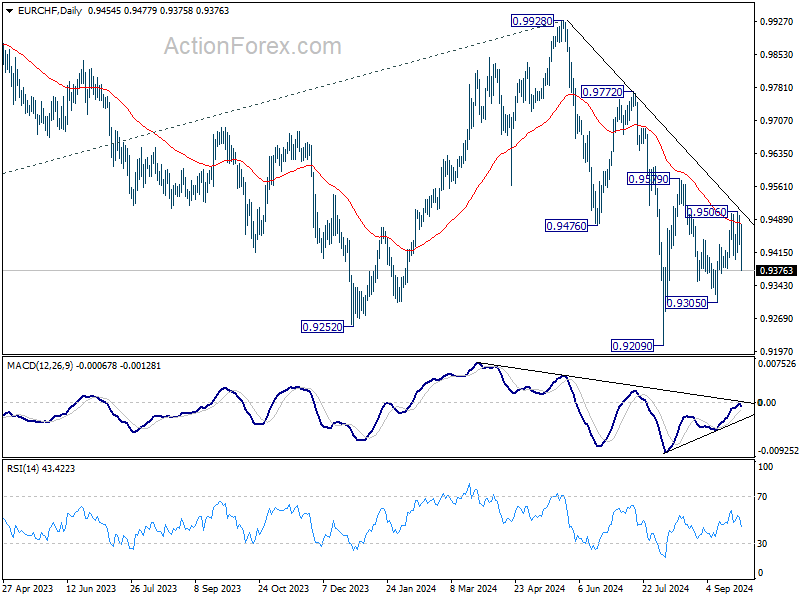

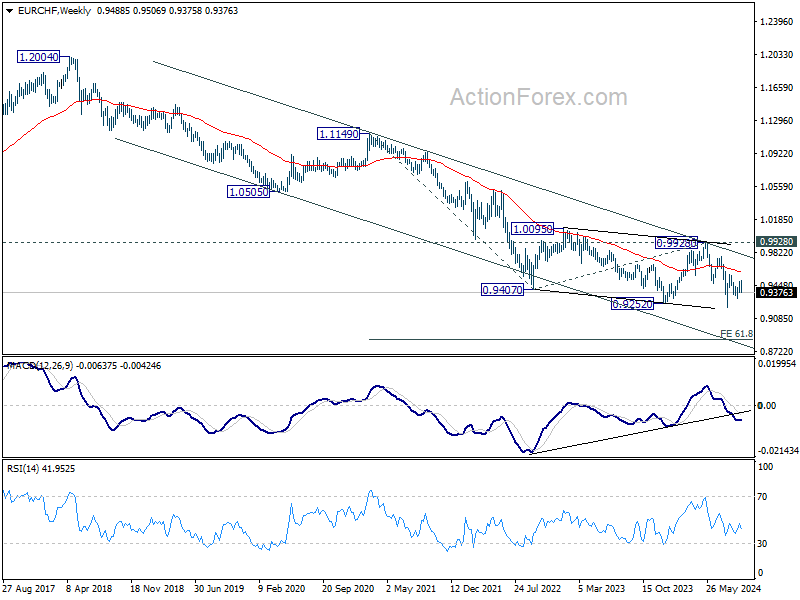

EUR/CHF Weekly Outlook

EUR/CHF reversed after edging higher to 0.9506 but stays above 0.9305 support. Initial bias remains neutral this week first. On the upside, above 0.9506 will resume the rebound from 0.9305 to 0.9579 resistance. However, break of 0.9305 will resume the fall for 0.9579 to retest 0.9209 low.

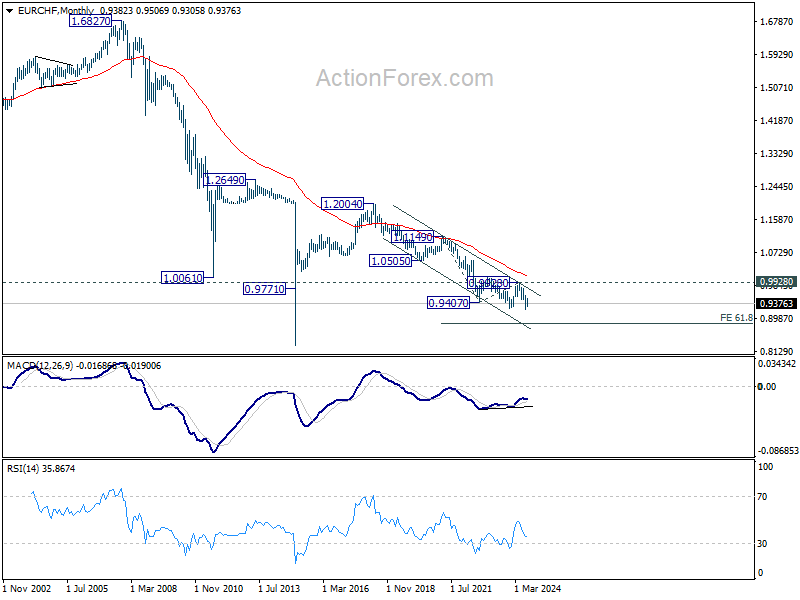

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 9/30 – 10/4

Monday, Sep 30, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Aug P | -0.50% | 3.10% |

| 23:50 | JPY | Retail Trade Y/Y Aug | 2.60% | 2.60% |

| 01:00 | NZD | ANZ Business Confidence Sep | 50.6 | |

| 01:30 | AUD | Private Sector Credit M/M Aug | 0.50% | 0.50% |

| 01:30 | CNY | NBS Manufacturing PMI Sep | 49.5 | 49.1 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Sep | 50.4 | 50.3 |

| 01:45 | CNY | Caixin Manufacturing PMI Sep | 50.5 | 50.4 |

| 01:45 | CNY | Caixin Services PMI Sep | 51.5 | 51.6 |

| 05:00 | JPY | Housing Starts Y/Y Aug | -3.00% | -0.20% |

| 05:00 | JPY | Consumer Confidence Index Sep | 36.7 | |

| 06:00 | EUR | Germany Import Price Index M/M Aug | -0.30% | -0.40% |

| 06:00 | GBP | GDP Q/Q Q2 F | 0.60% | 0.60% |

| 07:00 | CHF | KOF Economic Barometer Sep | 102 | 101.6 |

| 08:30 | GBP | M4 Money Supply M/M Aug | 0.20% | 0.30% |

| 08:30 | GBP | Mortgage Approvals Aug | 64K | 62K |

| 12:00 | EUR | Germany CPI M/M Sep P | 0.10% | -0.10% |

| 12:00 | EUR | Germany CPI Y/Y Sep P | 1.90% | |

| 13:45 | USD | Chicago PMI Sep | 46.5 | 46.1 |

| 21:45 | NZD | Building Permits M/M Aug | 26.20% | |

| 22:00 | NZD | NZIER Business Confidence Q3 | -44 | |

| 23:30 | JPY | Unemployment Rate Aug | 2.60% | 2.70% |

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 12 | 13 |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 14 | |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q3 | 32 | 33 |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q3 | 27 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 11.10% | |

| 23:50 | JPY | BoJ Summary of Opinions |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Aug P | |

| Forecast: -0.50% | Previous: 3.10% | ||

| 23:50 | JPY | Retail Trade Y/Y Aug | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 01:00 | NZD | ANZ Business Confidence Sep | |

| Forecast: | Previous: 50.6 | ||

| 01:30 | AUD | Private Sector Credit M/M Aug | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 01:30 | CNY | NBS Manufacturing PMI Sep | |

| Forecast: 49.5 | Previous: 49.1 | ||

| 01:30 | CNY | NBS Non-Manufacturing PMI Sep | |

| Forecast: 50.4 | Previous: 50.3 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Sep | |

| Forecast: 50.5 | Previous: 50.4 | ||

| 01:45 | CNY | Caixin Services PMI Sep | |

| Forecast: 51.5 | Previous: 51.6 | ||

| 05:00 | JPY | Housing Starts Y/Y Aug | |

| Forecast: -3.00% | Previous: -0.20% | ||

| 05:00 | JPY | Consumer Confidence Index Sep | |

| Forecast: | Previous: 36.7 | ||

| 06:00 | EUR | Germany Import Price Index M/M Aug | |

| Forecast: -0.30% | Previous: -0.40% | ||

| 06:00 | GBP | GDP Q/Q Q2 F | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 07:00 | CHF | KOF Economic Barometer Sep | |

| Forecast: 102 | Previous: 101.6 | ||

| 08:30 | GBP | M4 Money Supply M/M Aug | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 08:30 | GBP | Mortgage Approvals Aug | |

| Forecast: 64K | Previous: 62K | ||

| 12:00 | EUR | Germany CPI M/M Sep P | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 12:00 | EUR | Germany CPI Y/Y Sep P | |

| Forecast: | Previous: 1.90% | ||

| 13:45 | USD | Chicago PMI Sep | |

| Forecast: 46.5 | Previous: 46.1 | ||

| 21:45 | NZD | Building Permits M/M Aug | |

| Forecast: | Previous: 26.20% | ||

| 22:00 | NZD | NZIER Business Confidence Q3 | |

| Forecast: | Previous: -44 | ||

| 23:30 | JPY | Unemployment Rate Aug | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | |

| Forecast: 12 | Previous: 13 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | |

| Forecast: | Previous: 14 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q3 | |

| Forecast: 32 | Previous: 33 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q3 | |

| Forecast: | Previous: 27 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | |

| Forecast: | Previous: 11.10% | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

Tuesday, Oct 1, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Sep F | 49.6 | 49.6 |

| 00:30 | AUD | Retail Sales M/M Aug | 0.40% | 0.00% |

| 00:30 | AUD | Building Permits M/M Aug | -4.30% | 10.40% |

| 06:30 | CHF | Real Retail Sales Y/Y Aug | 2.60% | 2.70% |

| 07:30 | CHF | Manufacturing PMI Sep | 48.2 | 49 |

| 07:45 | EUR | Italy Manufacturing PMI Sep | 49.4 | 49.4 |

| 07:50 | EUR | France Manufacturing PMI Sep F | 44 | 44 |

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 40.3 | 40.3 |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 44.8 | 44.8 |

| 08:30 | GBP | Manufacturing PMI Sep F | 51.5 | 51.5 |

| 09:00 | EUR | Eurozone CPI Y/Y P | 1.90% | 2.20% |

| 09:00 | EUR | Eurozone CPI Core Y/Y P | 2.70% | 2.80% |

| 13:30 | CAD | Manufacturing PMI Sep | 49.5 | |

| 13:45 | USD | Manufacturing PMI Sep F | 47 | 47 |

| 14:00 | USD | ISM Manufacturing PMI Sep | 47.8 | 47.2 |

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 55 | 54 |

| 14:00 | USD | Construction Spending M/M Aug | 0.20% | -0.30% |

| 23:50 | JPY | Monetary Base Y/Y Sep | 0.80% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Sep F | |

| Forecast: 49.6 | Previous: 49.6 | ||

| 00:30 | AUD | Retail Sales M/M Aug | |

| Forecast: 0.40% | Previous: 0.00% | ||

| 00:30 | AUD | Building Permits M/M Aug | |

| Forecast: -4.30% | Previous: 10.40% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Aug | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 07:30 | CHF | Manufacturing PMI Sep | |

| Forecast: 48.2 | Previous: 49 | ||

| 07:45 | EUR | Italy Manufacturing PMI Sep | |

| Forecast: 49.4 | Previous: 49.4 | ||

| 07:50 | EUR | France Manufacturing PMI Sep F | |

| Forecast: 44 | Previous: 44 | ||

| 07:55 | EUR | Germany Manufacturing PMI Sep F | |

| Forecast: 40.3 | Previous: 40.3 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | |

| Forecast: 44.8 | Previous: 44.8 | ||

| 08:30 | GBP | Manufacturing PMI Sep F | |

| Forecast: 51.5 | Previous: 51.5 | ||

| 09:00 | EUR | Eurozone CPI Y/Y P | |

| Forecast: 1.90% | Previous: 2.20% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y P | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 13:30 | CAD | Manufacturing PMI Sep | |

| Forecast: | Previous: 49.5 | ||

| 13:45 | USD | Manufacturing PMI Sep F | |

| Forecast: 47 | Previous: 47 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | |

| Forecast: 47.8 | Previous: 47.2 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | |

| Forecast: 55 | Previous: 54 | ||

| 14:00 | USD | Construction Spending M/M Aug | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 23:50 | JPY | Monetary Base Y/Y Sep | |

| Forecast: 0.80% | Previous: 0.60% | ||

Wednesday, Oct 2 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 09:00 | EUR | Eurozone Unemployment Rate Aug | 6.40% | 6.40% |

| 12:15 | USD | ADP Employment Change Sep | 120K | 99K |

| 14:30 | USD | Crude Oil Inventories | -4.5M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 09:00 | EUR | Eurozone Unemployment Rate Aug | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 12:15 | USD | ADP Employment Change Sep | |

| Forecast: 120K | Previous: 99K | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -4.5M | ||

Thursday, Oct 3, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | 5.50B | 6.01B |

| 06:30 | CHF | CPI M/M Sep | -0.10% | 0.00% |

| 06:30 | CHF | CPI Y/Y Sep | 1.10% | 1.10% |

| 07:45 | EUR | Italy Services PMI Sep | 51.4 | |

| 07:50 | EUR | France Services PMI Sep F | 48.3 | 48.3 |

| 07:55 | EUR | Germany Services PMI Sep F | 50.6 | 50.6 |

| 08:00 | EUR | Eurozone Services PMI SepF | 50.5 | 50.5 |

| 09:00 | EUR | Eurozone PPI M/M Aug | 0.80% | |

| 09:00 | EUR | Eurozone PPI Y/Y Aug | -2.10% | |

| 08:30 | GBP | Services PMI Sep F | 52.8 | 52.8 |

| 12:30 | USD | Initial Jobless Claims (Sep 27) | 220K | 218K |

| 13:45 | USD | Services PMI Sep F | 55.4 | 55.4 |

| 14:00 | USD | ISM Services PMI Sep | 51.5 | 51.5 |

| 14:00 | USD | Factory Orders M/M Aug | 5% | |

| 14:30 | USD | Natural Gas Storage | 47B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | |

| Forecast: 5.50B | Previous: 6.01B | ||

| 06:30 | CHF | CPI M/M Sep | |

| Forecast: -0.10% | Previous: 0.00% | ||

| 06:30 | CHF | CPI Y/Y Sep | |

| Forecast: 1.10% | Previous: 1.10% | ||

| 07:45 | EUR | Italy Services PMI Sep | |

| Forecast: | Previous: 51.4 | ||

| 07:50 | EUR | France Services PMI Sep F | |

| Forecast: 48.3 | Previous: 48.3 | ||

| 07:55 | EUR | Germany Services PMI Sep F | |

| Forecast: 50.6 | Previous: 50.6 | ||

| 08:00 | EUR | Eurozone Services PMI SepF | |

| Forecast: 50.5 | Previous: 50.5 | ||

| 09:00 | EUR | Eurozone PPI M/M Aug | |

| Forecast: | Previous: 0.80% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Aug | |

| Forecast: | Previous: -2.10% | ||

| 08:30 | GBP | Services PMI Sep F | |

| Forecast: 52.8 | Previous: 52.8 | ||

| 12:30 | USD | Initial Jobless Claims (Sep 27) | |

| Forecast: 220K | Previous: 218K | ||

| 13:45 | USD | Services PMI Sep F | |

| Forecast: 55.4 | Previous: 55.4 | ||

| 14:00 | USD | ISM Services PMI Sep | |

| Forecast: 51.5 | Previous: 51.5 | ||

| 14:00 | USD | Factory Orders M/M Aug | |

| Forecast: | Previous: 5% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 47B | ||

Friday, Oct 4, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:45 | CHF | Unemployment Rate M/M Sep | 2.60% | 2.50% |

| 06:45 | EUR | France Industrial Output M/M Aug | 0.40% | -0.50% |

| 08:00 | EUR | Italy Retail Sales M/M Aug | 0.20% | 0.50% |

| 08:30 | GBP | Construction PMI Sep | 53.1 | 53.6 |

| 12:30 | USD | Nonfarm Payrolls Sep | 135K | 142K |

| 12:30 | USD | Unemployment Rate Sep | 4.20% | 4.20% |

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.30% | 0.40% |

| 14:00 | CAD | Ivey PMI Sep | 50.3 | 48.2 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:45 | CHF | Unemployment Rate M/M Sep | |

| Forecast: 2.60% | Previous: 2.50% | ||

| 06:45 | EUR | France Industrial Output M/M Aug | |

| Forecast: 0.40% | Previous: -0.50% | ||

| 08:00 | EUR | Italy Retail Sales M/M Aug | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 08:30 | GBP | Construction PMI Sep | |

| Forecast: 53.1 | Previous: 53.6 | ||

| 12:30 | USD | Nonfarm Payrolls Sep | |

| Forecast: 135K | Previous: 142K | ||

| 12:30 | USD | Unemployment Rate Sep | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 12:30 | USD | Average Hourly Earnings M/M Sep | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 14:00 | CAD | Ivey PMI Sep | |

| Forecast: 50.3 | Previous: 48.2 | ||