Sample Category Title

Japanese Yen Rises 1.3% vs Dollar on Political News/Economic Data

USDJPY rose to three-week high (146.49) and subsequently fell over three full figures on Friday, on speculations about new prime minister’s support to BOJ’s further policy tightening, which was seen as a violation of central bank’s independence, initially weakening yen and then sparking strong rally after news proved false.

Yen strengthened more after US data showed moderate increase in consumer spending in August, while inflation continued to slow, adding to expectations for another Fed outsized rate cut (bets are currently 50-50).

Technical structure is weakening on daily chart as falling 14-d momentum is cracking the centreline and about to break into negative territory, MA’s returned to full bearish setup, and a double bull-trap above 144.82 (Fibo 23.6% of 161.80/139.57).

Friday’s large bearish daily candle with long upper wick, to weigh on near-term action, along with falling and thickening daily cloud, which stays above the price.

Daily close below 143.00 zone (broken 50% of 139.57/146.49 /10DMA) to boost bearish signal and keep fresh bears firmly in play for extension through 142.21 (Fibo 61.8%) and 141.68 (Aug 5 spike low).

Res: 143.16; 143.84; 144.02; 144.85

Sup: 142.21; 142.00; 141.68; 141.20

Sunset Market Commentary

Markets

Today started somewhat as expected. French and Spanish September CPI data printed below consensus. French prices fell by 1.2% M/M to 1.5% Y/Y (from 2.2%), the first sub-2% reading since July 2021. Significantly lower fuel prices, but also lower services costs (turnaround after Olympics) drove the move. Spanish inflation was 0.1% M/M lower with only the second below 2% Y/Y-reading since March 2021 (1.7% from 2.4%). Core CPI slowed as well (2.4% from 2.7%) whereas markets expected a stabilization. Fuel prices were again the main culprit. EMU money markets nevertheless added to October ECB rate cut bets in the wake of the release. Their reasoning is simple: the only two key data points in the brief intermeeting period both surprised on the downside (PMI’s and now CPI’s). While markets currently attach an 80% probability to a follow-up rate cut, we still err on the side of the status quo. Recall ECB President Lagarde’s Q&A after the September meeting: “We are looking at a whole battery of indicators. And I’m saying that in particular because September will certainly deliver a low reading of inflation. Very likely. We expect, because of the base effect, particularly on energy, our inflation numbers to be up in the fourth quarter, so the last three months of 2024. But September is going to deliver a low reading.” In our interpretation, Lagarde basically hedged the September CPI figures with the central bank wanting more input on services and especially wages going into their final meeting this year. The ECB president can on Monday settle the debate when she appears in front of EU parliament. German yields lose 4 to 5 bps across the curve today. The euro initially dipped from levels near EUR/USD 1.1170 to 1.1130. The move was erased by the time of the release of US eco figures with bullish risk sentiment helping out. Key European stock markets add another 1% today. Disappointing US personal income/spending data (both +0.2% M/M in September) and a marginally lower core PCE deflator (0.1% M/M vs 0.2%) equally convinced (US) money markets to add to 50 bps Fed rate cut bets in November, our preferred scenario. Going into next week’s key eco data (ISM’s, payrolls) and Powell speech, the odds are perfectly in balance between 25 bps and 50 bps. US yields lose around 3 bps after the release, propelling EUR/USD back to first resistance at 1.1202/14. We stick to our sell USD on upticks approach. The trade-weighted dollar already set a minor new sell-off low at 100.16 with the 2023 low at 99.58 being the next target. USD/JPY’s drop from an intraday high of 146.20 to currently 142.70 helps explaining. JPY rebounded after results of the LDP leadership contest which was lost by a dovish BoJ advocate (Takaichi) in favour of Ishiba.

News & Views

Belgian inflation fell by 0.5% M/M in September to 3.06% Y/Y (from 0.0% M/M and 2.86% Y/Y) in August. Core inflation (ex-energy products and unprocessed food) was little changed at 2.80% from 2.78%. Energy inflation was an important factor at 6.72% Y/Y, compared to 6.96% last month and 14.01% in July. Electricity prices rose 14.8% Y/Y from 11.3%. For natural gas, it went from 103.0% last month to 138.1% this month. The increase is the result of the extinction of the impact of the basic package for electricity and natural gas. The disappearance of the package will have an increasing effect on inflation until February 2025. Services inflation is stable at 4.04%. Inflation for rents also remains stable at 4.74%. Inflation for food products (including alcoholic beverages) stands at 1.08% compared to 0.04% last month. Main monthly price increases concerned electricity (4.4%), natural gas (4.5%), travels abroad and city trips (2.6%), clothing (0.6%) and tobacco (3.9%. Plane tickets (-17.7%), motor fuels (-3.8%), hotel rooms (-10.0%), domestic heating oil (-2.9%), domestic trips (-9.9%), non-alcoholic beverages (-2.0%), alcoholic beverages (-1.8%), cleaning and maintenance products (-5.7%), confectionery (-2.0%) and meat (-0.8%) decreased. The estimate according to the European harmonised index (HICP flash estimate) amounts to 4.5% in September 2024.

The Brazilian unemployment rate unexpectedly declined from 6.8% to 6.6% in August. The consensus only expected a decline to 6.7%. The level is the lowest since current methodology which goes back to 2012. The strong labour market data come as Brazil’s central bank last week raised its policy rate by 25 bps to 10.75%, as its concerned about the inflationary impact of ongoing stronger than expected growth and a tight labour market. The BCB this week also already raised this year’s growth forecast (3.2% from 2.3%) and the inflation forecast over the period 2024-2026 to 4.3%-3.7%-3.3% from 4%-3.4%-3.2%. The real trades little changed near USD/BRL 5.44.

Graphs

USD/JPY: yen rebounds after outcome LDP leadership contest. Dovish BoJ advocate lost run-off.

EU 2y swap rate: markets add to October ECB rate cut bets, pulling the front end of the curve to lowest levels since 2022

German Dax: German stocks are today’s outperforms as industrial stocks make comeback

Gold extends rally as investors pile up on easing bets

U.S. Personal Income and Spending Grow Less Than Expected in August

Personal income grew 0.2% month-on-month (m/m) in August, down from July's 0.3% gain and below market expectations (0.4%).

Accounting for inflation and taxes, real personal disposable income grew a modest 0.1% for a third consecutive month.

Personal consumption expenditures grew 0.2% m/m in August. This was lower than the 0.5% recorded in July, and below market expectations (0.3%). Spending in real terms rose 0.1% m/m – much lower than the 0.4% gain recorded in July. Real spending was largely a result of increases in services outlays (0.2%), as goods spending was flat.

On inflation, the Fed's preferred inflation metric, the core PCE price deflator, rose 0.1% m/m, weaker than a 0.2% in the prior month. Thanks to base effects core PCE inflation rose from 2.6% to 2.7%. While the annual reading was in line with market expectations (2.7%), the monthly number came in marginally lower than expected (0.2%).

The personal savings rate declined to 4.8% in August from 4.9% in July (previously 2.9%).

Key Implications

Yesterday's release of the comprehensive annual GDP update revealed that the savings rate and income growth for the first half of the year were both stronger than previously reported. Thus it appears consumers had more gas in the tank to facilitate spending. Nonetheless, today's data suggests that they may be taking their foot off the pedal. Consumer spending is expected to remain subdued as the labor market continues to cool, though a greater savings buffer than previously thought could help to temper the slowdown.

On the inflation front, the Fed's preferred core measure continues to head in the right direction, even though base effects are boosting the yearly pace. Given that inflation continues to remain contained, the Fed will be paying even keener attention to labor market developments, with September payrolls data released next Friday as they calibrate further policy action.

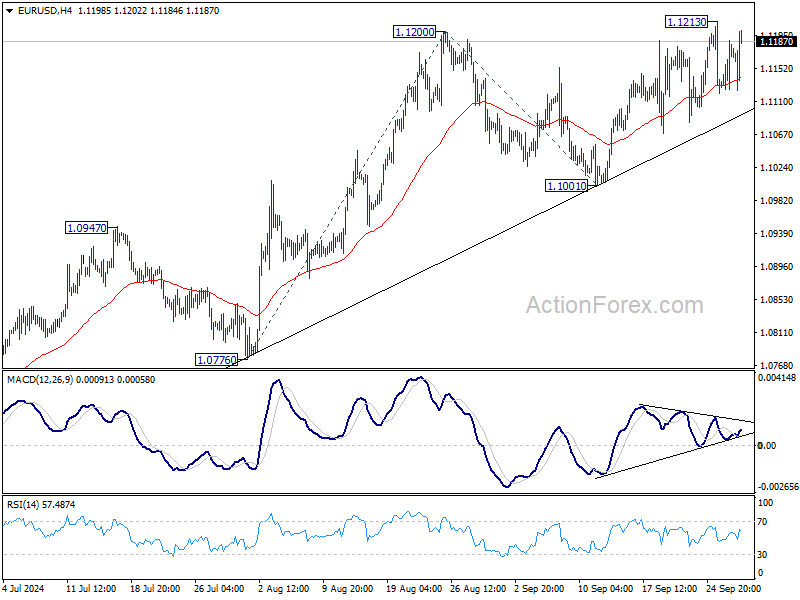

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1138; (P) 1.1164; (R1) 1.1201; More....

Intraday bias in EUR/USD remains neutral for the moment. Further rally is expected as long as 1.1001 support holds. Above 1.1213 will bring retest of 1.1274 high. Firm break there will resume larger up trend. Next near term target will be 100% projection of 1.0776 to 1.1200 from 1.1001 at 1.1425.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.

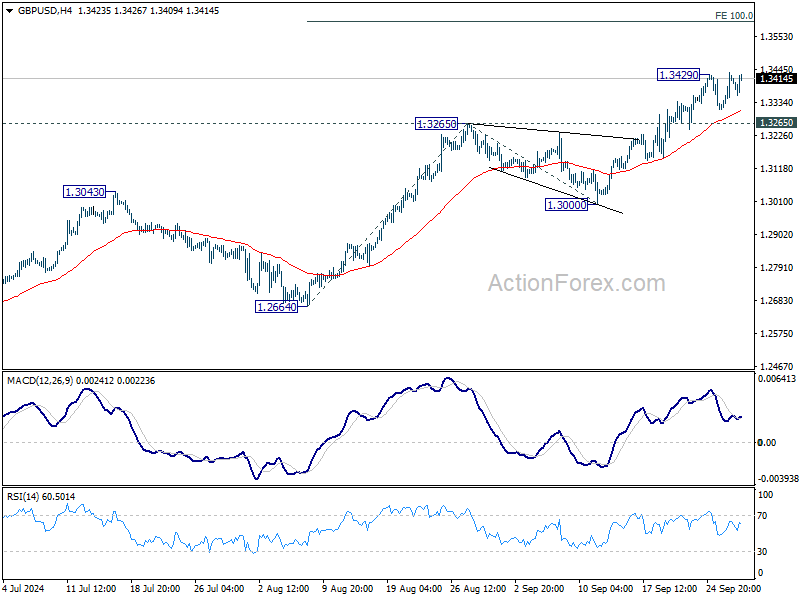

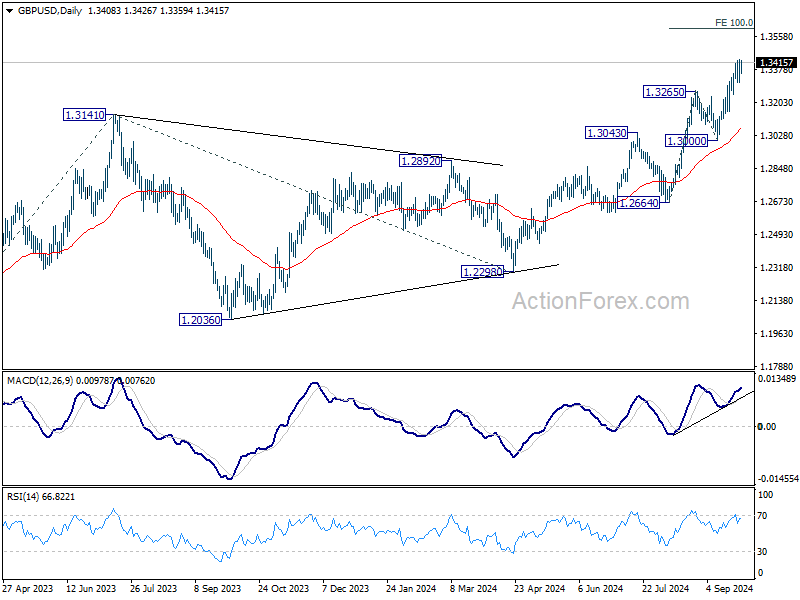

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3335; (P) 1.3384; (R1) 1.3465; More...

Intraday bias in GBP/USD remains neutral first, but further rally is expected as long as 1.3265 resistance turned support holds. Above 1.3429 will extend larger rally to 100% projection of 1.2664 to 1.3265 from 1.3000 at 1.3601 next. Nevertheless, break of 1.3265 will turn bias to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. For now, outlook will stay bullish as long as 1.3000 support holds, even in case of deep pullback.

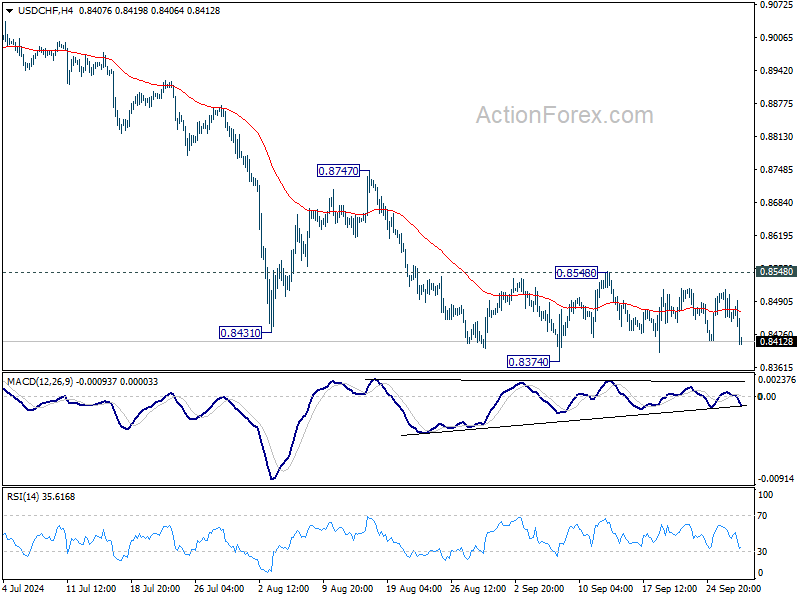

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8438; (P) 0.8477; (R1) 0.8501; More…

No change in USD/CHF's outlook as range trading continues. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, break of 0.8548 resistance will turn bias back to the upside for 0.8747 resistance.

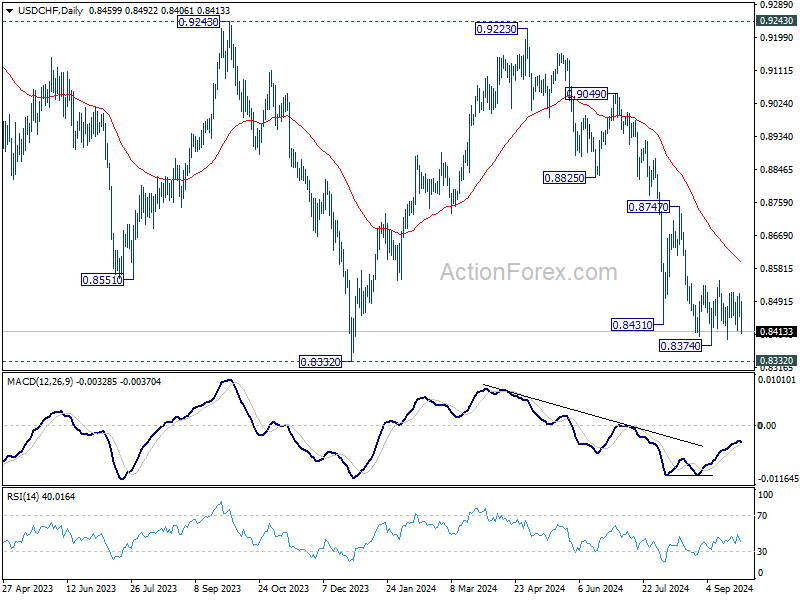

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Canada’s Economy Advanced in July, Growth Stalled in August

The Canadian economy grew by 0.2% month-on-month (m/m) in July after June's flat reading. This print landed ahead of Statistics Canada's advanced guidance and consensus expectations. Early guidance from Statistics Canada points to no growth in August.

May's reading was broad-based, with output expanding in 13 of 20 industries. Growth in services-producing industries (0.2% m/m) advanced at a slightly faster pace than in goods-producing industries (0.1% m/m).

On a weighted basis, the retail trade sector contributed most to the overall gain in July's GDP, and was up for a second consecutive month (+1.0% m/m). Elsewhere on the services side, gains in the finance and insurance industry (+0.5% m/m) and the public administration sector (+0.4% m/m) were offset partially by a drag in the transportation sector (-0.4% m/m) that were impacted by wildfires.

On the goods side, utilities (+1.3% m/m) did most of the heavy lifting on the back of increased demand for electricity. Meanwhile, the manufacturing sector reversed some of last month's slide and the construction sector slumped for a third straight month, down 0.4% m/m.

Behind the advanced reading of stalled growth in August is an increase in oil & gas and public sector activity offset by pullbacks in the manufacturing and transportation & warehousing sectors.

Key Implications

GDP data for July came in stronger than expectations, but the momentum should be short-lived. With the current guidance for flat industry-GDP growth next month, third quarter GDP is tracking just north of 1.0% quarter-on-quarter (q/q) annualized, significantly below the Bank of Canada's (BoC) 2.8% forecast, but broadly in line with our recent forecast update.

The BoC next rate decision is in late October and more cuts are certainly on the table. The BoC has shifted their tone as of late, putting more emphasis on their fears around a weakening economy. For what it's worth, we don't think today's data tips the scales any more-or-less in favour of a potential 50 basis point (bps) interest rate cut, which would follow the recent move from the Federal Reserve. Instead, more emphasis will be placed on upcoming labour market data as well as inflation data, where the Bank will be looking for signs that price growth can remain durably at 2%.

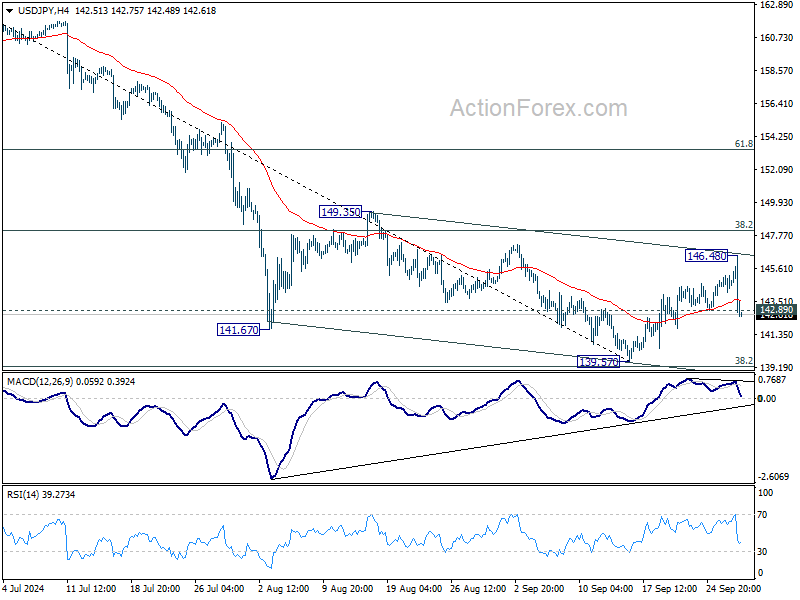

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.21; (P) 144.71; (R1) 145.31; More...

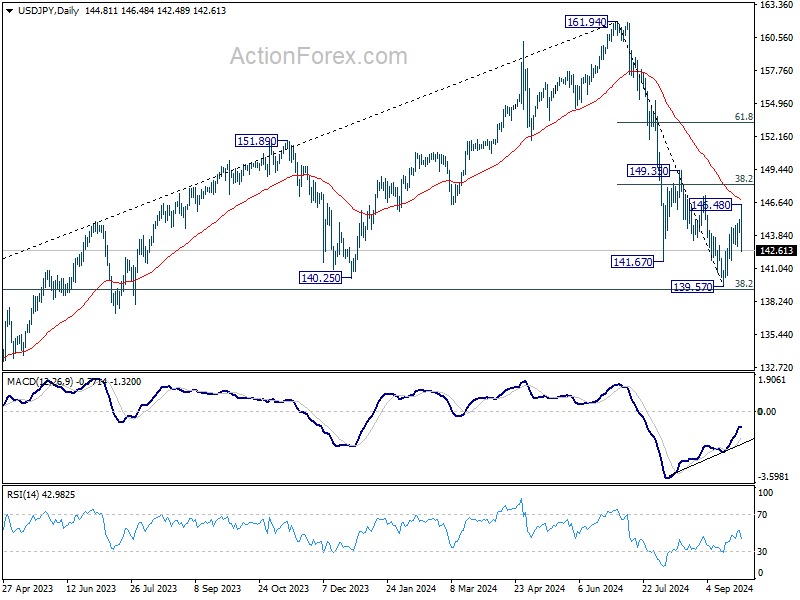

USD/JPY's break of 142.89 minor support suggests that recovery fro 139.57 has completed at 146.48 already. Intraday bias is back on the downside for 139.57 low. Strong support is still expected from 139.26 to contain downside to bring another rebound. But decisive break there will carry larger bearish implications. On the upside, above 146.48 will resume the rebound to 38.2% retracement of 161.94 to 139.57 at 148.11.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US Inflation Data Fuels More Risk-On Rally, Yen Surges After Ishiba’s LDP Leadership Win

Risk-on sentiment returned to global markets again in early US trading, driven by lower-than-expected inflation data. While annual PCE core inflation edged up to 2.7%, the monthly increase was a modest 0.1%. This tamer monthly inflation growth suggests that underlying price pressures would, at least, not obstruct Fed's to another aggressive rate cut at its next meeting. However, upcoming non-farm payrolls and CPI data will still play a decisive role in Fed’s final decision.

In Japan, Yen staged a sharp turnaround after Shigeru Ishiba unexpectedly secured leadership of the ruling Liberal Democratic Party, setting him on the path to become the next Prime Minister. Known for his hawkish monetary stance, Ishiba's ascent has intensified speculation that BoJ may implement another rate hike in December. However, the political landscape remains uncertain. There is a possibility that Ishiba may call for a snap general election to secure a stronger mandate from voters, and that could delay any BoJ action until 2025.

For the week, Kiwi and Aussie remain the top performers, with the Swiss Franc catching up as the third strongest due to today's rebound. Dollar has become the weakest currency as Yen recovers. Euro and Sterling are also underperforming, while Yen and Loonie are positioned in the middle of the currency spectrum.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 1.20%. CAC is up 0.59% UK 10-year yield is down -0.0528 at 3.964. Germany 10-year yield is down -0.054 at 2.130. Earlier in Asia, Nikkei rose 2.32%. Hong Kong HSI rose 3.55%. China Shanghai SSE rose 2.88%. Singapore Strait Times fell -0.25%. Japan 10-year JGB yield fell -0.0239 to 0.807.

US PCE inflation falls to 2.2% in Aug, core PCE ticks up to 2.7%

US personal income rose USD 50.5B or 0.2% mom in August, below expectation of 0.4% mom. Personal spending rose USD 47.2B or 0.2% mom, below expectation of 0.3% mom.

PCE price index rose 0.1% mom, matched expectations while core PCE (excluding food and energy)price index rose 0.1% mom,m below expectation of 0.2% mom. Good prices fell -0.2% mom while services prices rose 0.2% mom. Food prices rose 0.1% mom and energy prices fell -0.8% mom.

From the same month a year ago, PCE price growth slowed from 2.5% yoy to 2.2% yoy, below expectation of 2.3% yoy. Core PCE price growth accelerated fro 2.6% yoy to 2.7% yoy, matched expectations. Prices for goods decreased -0.9% yoy and prices for services increased 3.7% yoy. Food prices increased 1.1% yoy and energy prices -decreased 5.0% yoy.

Canada's GDP grows 0.2% mom in Jul essentially unchanged in Aug

Canada's GDP grew 0.2% mom in July, above expectation of 0.1% mom. Services-producing industries grew 0.2% mom while goods- producing industries rose 0.1% mom. Overall, 13 of 20 sectors expanded in July.

Advance information indicates that real GDP was essentially unchanged in August. Increases in oil and gas extraction and the public sector were offset by decreases in manufacturing and transportation and warehousing.

Eurozone economic sentiment dips slightly to 96.2

Eurozone Economic Sentiment Indicator fell slightly from 96.5 to 96.2 in September. Employment Expectations Indicator ticked up from 99.4 to 99.5. Economic Uncertainty Indicator rose from 17.5 to 17.8. Industry confidence fell from -9.9 to -10.9. Services confidence rose from 6.4 to 6.7. Consumer confidence rose from -13.4 to -129. Retail trade confidence fell from -7.9 to -8.5. Construction confidence rose from -6.3 to -5.8.

EU Economic Sentiment Indicator was unchanged at 96.7. For the largest EU economies, the ESI worsened markedly in France (-1.4) and Germany (-1.2), while it improved significantly in Poland (+2.0), Spain (+1.9), Italy (+1.2) and, more moderately, in the Netherlands (+0.5).

Japan's Tokyo core inflation slows to 2%, supporting BoJ's cautious approach

Japan's Tokyo CPI core (excluding fresh food) slowed from 2.4% yoy to 2.0% yoy in September, aligning with expectations and marking its lowest level since May. Headline CPI dropped to 2.2% yoy from 2.6% yoy , while CPI core-core (excluding food and energy) remained stable at 1.6% yoy.

The primary driver of the deceleration in inflation was reduction in electricity and gas prices, influenced by government energy subsidies reintroduced by outgoing Prime Minister Fumio Kishida. These subsidies helped alleviate the impact of a particularly hot summer, shaving 0.5 percentage points off overall inflation.

This data, especially the stable core-core inflation, supports BoJ's cautious stance regarding more tightening. BoJ Governor Kazuo Ueda recently noted that inflationary risks have diminished, particularly with Yen's recent gains. BoJ is likely to remain on hold during its upcoming policy meeting on October 31.

PBoC cuts RRR and repo rate

In a follow-up to Governor Pan Gongsheng's earlier remarks this week, the People's Bank of China announced today a 50bps cut in the reserve requirement ratio and a 20bps reduction in the seven-day reverse repurchase rate.

This move is intended to release approximately CNY 1T in long-term liquidity, enabling banks to lend more and increase purchases of government bonds aimed at funding infrastructure projects. With the cut, the weighted average RRR will drop to around 6.6%. The central bank also lowered the seven-day reverse repo rate from 1.7% to 1.5%.

Further fiscal measures are anticipated before China's National Day holiday on October 1, as the Politburo has signaled a heightened focus on addressing economic pressures.

Reports indicate that the government will raise CNY 1T via special bonds, which will fund consumer goods subsidies, upgrades to business equipment, and provide a monthly allowance of CNY 800 yuan per child for households with multiple children. Additionally, another CNY 1T in special sovereign debt could be issued to help local governments manage their mounting debt burdens.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.21; (P) 144.71; (R1) 145.31; More...

USD/JPY's break of 142.89 minor support suggests that recovery fro 139.57 has completed at 146.48 already. Intraday bias is back on the downside for 139.57 low. Strong support is still expected from 139.26 to contain downside to bring another rebound. But decisive break there will carry larger bearish implications. On the upside, above 146.48 will resume the rebound to 38.2% retracement of 161.94 to 139.57 at 148.11.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Sep | 2.20% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Sep | 2.00% | 2.00% | 2.40% | |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Sep | 1.60% | 1.60% | ||

| 06:45 | EUR | France Consumer Spending M/M Aug | 0.20% | -0.10% | 0.30% | 0.20% |

| 07:55 | EUR | Germany Unemployment Rate Sep | 6.00% | 6.00% | 6.00% | |

| 07:55 | EUR | Germany Unemployment Change Sep | 17K | 9K | 2K | |

| 09:00 | EUR | Eurozone Economic Sentiment Sep | 96.2 | 96.5 | 96.6 | 96.5 |

| 09:00 | EUR | Eurozone Industrial Confidence Sep | -10.9 | -9.8 | -9.7 | -9.9 |

| 09:00 | EUR | Eurozone Services Sentiment Sep | 6.7 | 5.6 | 6.3 | 6.4 |

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | -12.9 | -12.9 | -12.9 | |

| 12:30 | CAD | GDP M/M Jul | 0.20% | 0.10% | 0.00% | |

| 12:30 | USD | Personal Income M/M Aug | 0.20% | 0.40% | 0.30% | |

| 12:30 | USD | Personal Spending Aug | 0.20% | 0.30% | 0.50% | |

| 12:30 | USD | PCE Price Index M/M Aug | 0.10% | 0.10% | 0.20% | |

| 12:30 | USD | PCE Price Index Y/Y Aug | 2.20% | 2.30% | 2.50% | |

| 12:30 | USD | Core PCE Price Index M/M Aug | 0.10% | 0.20% | 0.20% | |

| 12:30 | USD | Core PCE Price Index Y/Y Aug | 2.70% | 2.70% | 2.60% | |

| 12:30 | USD | Goods Trade Balance (USD) Aug P | -94.3B | -100.6B | -102.7B | |

| 12:30 | USD | Wholesale Inventories Aug P | 0.20% | 0.20% | 0.20% | |

| 14:00 | USD | Michigan Consumer Sentiment Sep F | 69 | 69 |

Canada’s GDP grows 0.2% mom in Jul essentially unchanged in Aug

Canada's GDP grew 0.2% mom in July, above expectation of 0.1% mom. Services-producing industries grew 0.2% mom while goods- producing industries rose 0.1% mom. Overall, 13 of 20 sectors expanded in July.

Advance information indicates that real GDP was essentially unchanged in August. Increases in oil and gas extraction and the public sector were offset by decreases in manufacturing and transportation and warehousing.