Sample Category Title

Euro Steady as Germany’s CPI lower Than Expected

The euro is steady at the start of the trading week. EUR/USD is trading at 1.1170 in the North American session at the time of writing, up 0.06% on the day.

Germany’s CPI eases to 1.6%

Inflation in Germany slowed to 1.6% y/y in September, down from 1.9% in August and shy of the market estimate of 1.6%. This was the lowest level since February 2021 and was driven by a sharp drop in energy costs. Monthly, inflation was flat, up from -0.1% in August and below the market estimate of 0.1%. Core inflation dropped to 2.7%, down from 2.8% in August and its lowest level since January 2022.

The decline in inflation in the eurozone’s largest economy is typical of what is happening across the bloc. Eurozone inflation will be released on Tuesday with a market estimate of 1.9%, compared to 2.2% in August, which was a three-year low. An inflation reading below the 2% target would be highly symbolic and increase the pressure on the ECB to continue to trim rates in order to kick-start the weak economy.

The ECB remains cautious about rate cuts as services inflation and wage growth remain high. Policy makers are likely to stay on the sidelines in October in order to monitor key data and wait until December before making any rate moves.

US Core PCE Index drops to 0.1%

The Fed appears to have inflation under control and the US Core PCE Price Index, the Fed’s preferred inflation indicator, was within expectations on Friday. The index rose 0.1% m/m in August, a three-month low. This was down from 0.2% in July and below the market estimate of 0.2%. Yearly, Core PCE ticked up to 2.7%, after three consecutive months at 2.6% and in line with expectations.

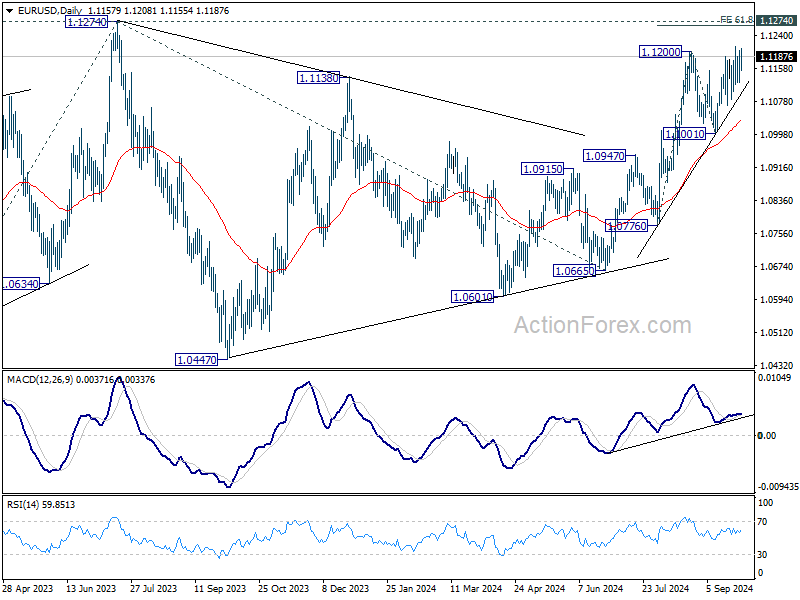

EUR/USD Technical

- EUR/USD is testing resistance at 1.1164. Above, there is resistance at 1.1202

- 1.1124 and 1.1086 are providing support

Sunset Market Commentary

Markets

With national German (and Italian) inflation data, an appearance of ECB present Christine Lagarde before the EU Parliament and Fed Chair Powell speaking before the National Association of Business Economics conference (Nashville), investors today already receive quite some interesting input to challenge their positioning regarding the outcome of the next ECB (Oct 17, unchanged or frontloading to 25 bps cut) and Fed meetings (Nov 7, 25 bps or 50 bps). German headline HICP eased further to -0.1% M/M and 1.8% Y/Y (from -0.2% M/M and 2.0% last month), but contrary to Spanish and French data on Friday didn’t bring a big downside surprise. German national data (headline 0.0% and 1.6%) released by the statistical office showed ongoing disinflation in goods (-0.3% Y/Y) with energy prices declining 7.6%% Y/Y. However, the slowdown in core inflation (2.7% from 2.8%) and services inflation (3.8% from 3.9%) proceeds only at a very gradual pace. With markets this morning discounting a 75% chance of an October ECB rate cut, some investors turned a bit more cautious. 2-y German yields intraday added 5 bps ahead the speeches of ECB’s Lagarde and Fed’s Powell. The US 2-y even added about 6 bps. At the hearing before the European Parliament, Lagarde acknowledged that Europe’s recovery is facing headwinds and saw disinflation accelerating. It might rise again due to base effects in Q4. Still, the ECB will take into account the increased confidence of taming inflation in October. With core inflation still sticky, this is no outright commitment to cut. Even so, it is no formal dismissal either. The issue might lead to an interesting (public) debate between hawks and doves that might already openly start in the coming days. EMU yields reversed most of the intraday uptick (German 2-y yield +1.0 bp, 30-y -1.0 bp). Understandably, the intraday setback in the US is much more modest. The US 2-y yield adds 5.0 bps. The 30-y +0.5 bps. Will Powell be as ‘clement’ as his European counterpart this evening? On other markets, the ongoing, stimulus-driven China equity rally doesn’t provide further spill-overs to European and/or US equity markets anymore. The Eurostoxx 50 cedes 1.0 %. US indices area easing modestly after the Dow (-0.5%) closed at a record level last Friday. Lagarde keeping the door open to at least to assess the merits of an October cut and as such a widening of the US-EMU interest rate differentials again has remarkably little impact on the euro (or the dollar). After again filling offers north 1.12 (and near the YTD top) EUR/USD currently eases only modestly to 1.1175. DXY still struggles to avoid further losses (little changed at 100.4).

News & Views

The Swiss KOF Economic barometer continued to rise in September, albeit only very slightly. It increased from 105 in August (upwardly revised from 101.6) to 105.5, the second best level since October 2021, suggesting that the Swiss economy is slowly working its way out of the trough. Details showed that almost all indicator bundles for the economic sectors point to a more favourable outlook than before with producing industries (manufacturing & construction) standing out. General business situation, export opportunities and intermediate input purchases are increasingly pointing to improvement. On the demand side, indicators for consumer demand were unchanged (slightly above average) while indicator for future foreign demand are weakening. The Swiss franc loses some ground today, but that’s not related to the data. Rising core bond yields even outweigh risk-off market sentiment, putting CHF in the defensive. EUR/CHF rises from 0.9390 to 0.9440.

September Polish inflation figures printed exactly in line with consensus, sticking with the 0.1% M/M pace from August to rise from 4.3% Y/Y to 4.9% Y/Y and further away from the National Bank of Poland’s 2.5% inflation target (with a +-1 ppt tolerance band). It’s the sixth consecutive Y/Y-increase lifting inflation to its highest level YTD. Details showed fuel prices dropping by 3.4% M/M while prices for food and non-alcoholic drinks and for electricity, gas and others both rise by 0.2% M/M. Core inflation will only be published on October 16, but the current breakdown suggests a new acceleration likely bringing core CPI back above 4% (from 3.7% in September) in Y/Y terms. Inflation developments defend the current NBP approach of sticking to the 5.75% policy rate for now and holding back from a protracted cutting cycle like local peers (eg CNB and MNB). The NBP meets on Wednesday, but the November meeting (including updated growth and inflation forecasts) will be more interesting. EUR/PLN holds near multi-year strongest levels for PLN at 4.28.

Graphs

EUR/PLN: rising inflation suggest zloty won’t lose interest rate support anytime soon.

EUR/CHF: improving growth outlook might make it less evident for SNB to reduce policy rate. CHF is holding strong.

EMU 2-y swap: Lagarde acknowledging faster disinflation and poor growth keeps EMU short-term yields under pressure.

Iron ore: propelled higher on China stimulus.

ECB’s Lagarde signals growing confidence in disinflation but economic recovery faces obstacles

During a hearing before the Committee on Economic and Monetary Affairs of the European Parliament today, ECB President Christine Lagarde indicated that inflation might "temporarily increase" in Q4, largely due to the previous sharp declines in energy prices dropping out of the annual inflation rate calculations.

However, she added that "the latest developments strengthen our confidence that inflation will return to target in a timely manner". ECB will factor these dynamics into its next monetary policy meeting scheduled for October.

On the topic of economic growth, Lagarde acknowledged that the "suppressed level of some survey indicators" points to the challenges the recovery is facing. Nonetheless, she anticipates that the recovery will strengthen over time, as rising real incomes are expected to boost household consumption.

Lagarde reiterated ECB's data-dependent approach and emphasized that ECB is "not pre-committing to a particular rate path".

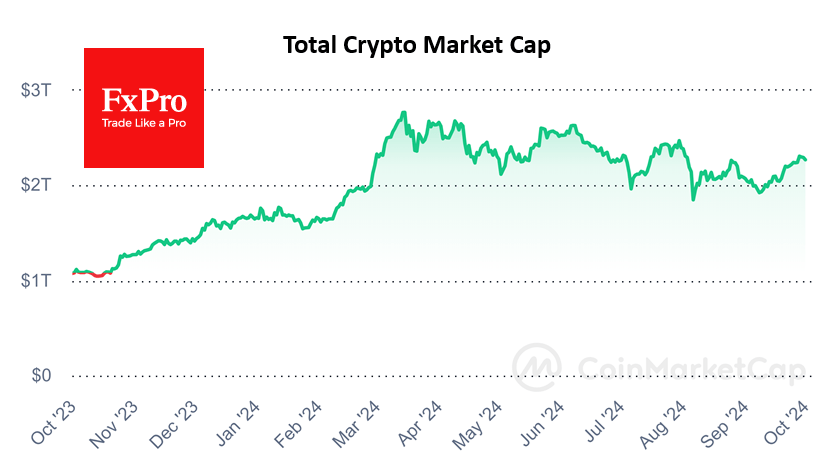

Crypto Market Takes Defence

Market Picture

The cryptocurrency market starts the week on the defensive, losing 1.2% of its capitalisation in 24 hours to $2.27 trillion, although it is still up 3% from a week ago. This drawdown looks like short-term profit-taking from the recent wave of gains amid the risks of the upcoming jobs report and Powell’s comments.

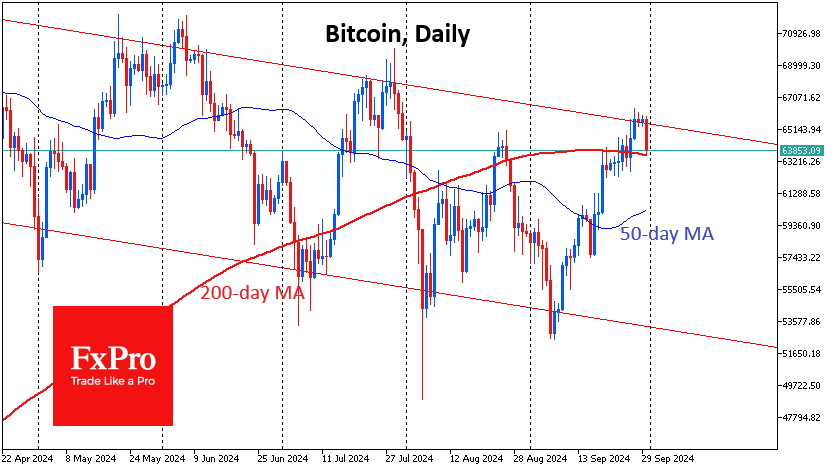

The first cryptocurrency is down 2.6% on Monday, retreating to $64.0K. On the technical side, bitcoin has come under pressure near the upper border of a multi-month downtrend. However, we see this as having more of an emotional component, as we believe that the break above the previous highs and the 200-day moving average served as an important signal of bullish dominance.

Bitcoin is on the verge of its best September since 2012. BTC has gained more than 11% since the beginning of the month, in stark contrast to the typical decline this month. The altcoin index is up more than 20% after easing financial conditions amid a global wave of interest rate cuts by the Fed, ECB and PBC.

Bitcoin closed higher for the third week, hitting its highest level since late July on Friday at around $66,500. The positive momentum in US spot bitcoin ETFs continued through all five trading sessions of the week.

News Background

According to SoSoValue, inflows into US spot bitcoin ETFs totalled $1.11 billion last week, the largest in 10 weeks, including inflows of $494.3 million. Cumulative inflows since the launch of BTC ETFs in January rose to $18.80 billion (+6.3% for the week). The Ethereum ETF turned positive after six weeks of outflows, with net inflows of $84.5 million.

Prices for 90% of altcoins traded on Binance have crossed above the 50 DMA, notes GoaSymmetric. Altcoins are ‘waking up’. ‘This is nothing compared to what we will see in the next six months,’ said Michael van de Poppe, founder of MN Trading.

Grayscale has updated its list of 20 cryptocurrencies that could outperform the market in Q4. As a result of the next rebalancing, SUI, TAO, OP, HNT, CELO, and UMA will be added to the ‘model portfolio’. RENDER, MNT, RUNE, PENDLE, ILV and RAY were removed.

CCData calculates that the companies behind the top five stable coins by market capitalisation will lose about $625m in annual revenue after the Fed’s 50bp rate cut in September. US Treasuries account for 80.2% of stablecoin issuers’ reserves. Cumulatively, they hold around $125bn of the country’s national debt.

Australian Dollar Reaches 19-Month High Boosted by Chinese Economic Stimulus and Weaker US Dollar

The AUD/USD pair climbed to 0.6922 on Monday, marking its highest point since February 2023. This surge was primarily triggered by China’s announcement of economic stimulus measures, which is significant given China’s status as Australia’s largest trading partner. Such support for the Chinese economy will likely increase demand for commodities and bolster major currencies tied to trade with China.

Additionally, the Australian dollar has benefited from the recent weakness in the US dollar, spurred by disappointing economic data from the US. This has heightened market expectations that the Federal Reserve will persist with rapid interest rate cuts.

At its September meeting, the Reserve Bank of Australia (RBA) opted to maintain its interest rate at 4.35% per annum, suggesting that the current monetary policy might remain unchanged for some time. The RBA’s cautious approach reflects its strategy of closely monitoring inflation and employment trends without immediate concern about aligning its pace with other global central banks.

This week is set to be significant for the Australian dollar. Australia is scheduled to release data on retail sales, construction, and various trade indicators, which could influence the currency’s trajectory.

Technical analysis of AUD/USD

The AUD/USD market is extending the fifth wave of growth, with a consolidation range forming around the 0.6925 level. There is potential for an upward break targeting 0.6983. After reaching this level, a corrective movement to retest 0.6925 may occur. If the bullish momentum continues, the next wave could reach 0.7033. The MACD indicator supports this bullish scenario, with its signal line well above zero and upwards.

On the hourly chart, the AUD/USD has achieved a growth wave up to 0.6926 and is now consolidating just below this level. If the pair exits this range downward, a correction to 0.6877 could be expected. Conversely, a breakout above could extend the uptrend towards 0.6982, potentially reaching 0.7033. The Stochastic oscillator, currently above 80 and trending downward, suggests a short-term pullback might occur before further advances.

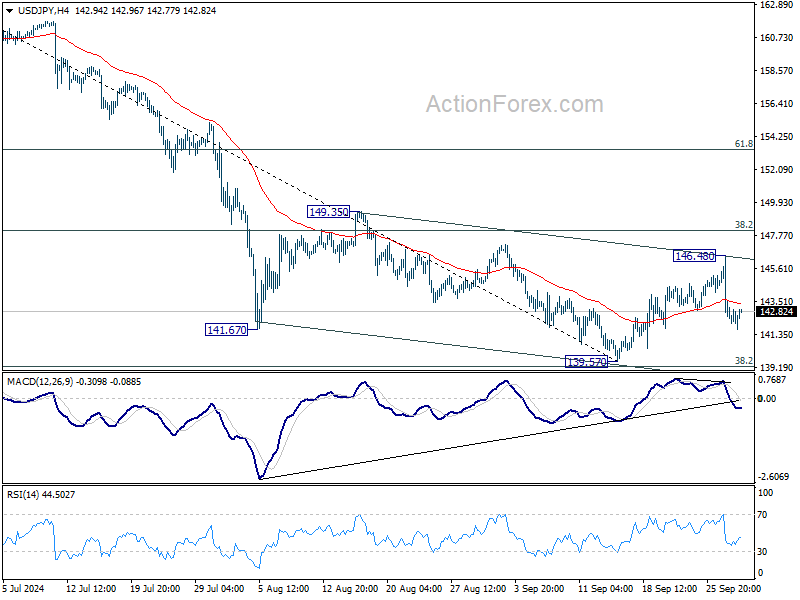

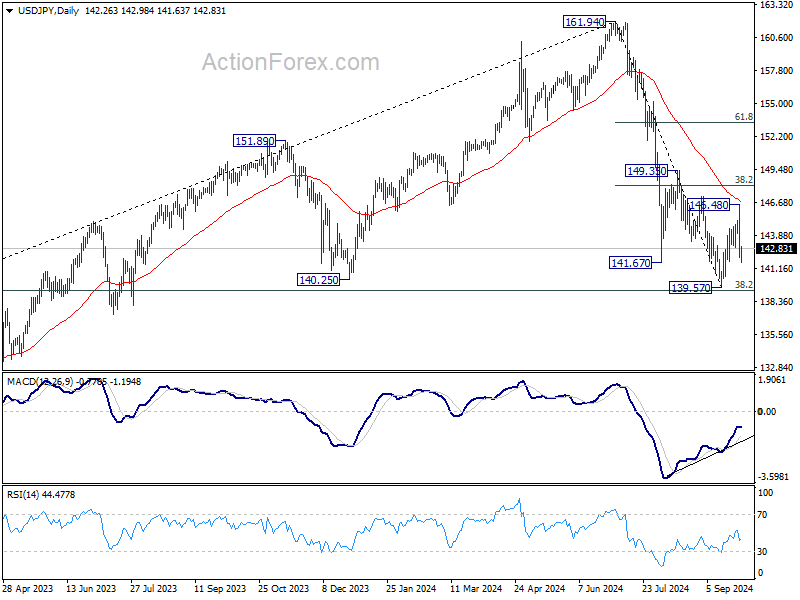

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.66; (P) 143.58; (R1) 145.08; More...

Intraday bias in USD/JPY remains on the downside for the moment. Fall from 146.48 is in progress for retesting 139.578. Strong support could be seen again from 139.26 fibonacci level to bring rebound. However, firm break of 139.26 will carry larger bearish implications.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

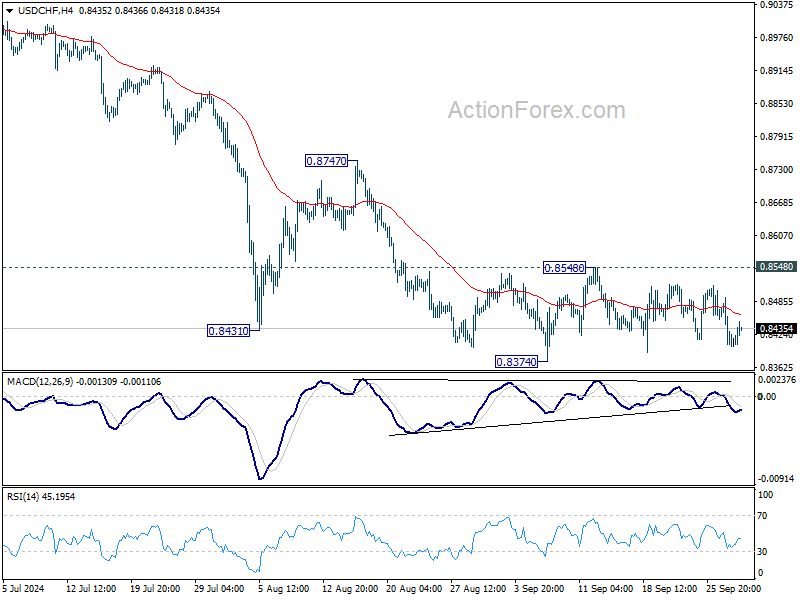

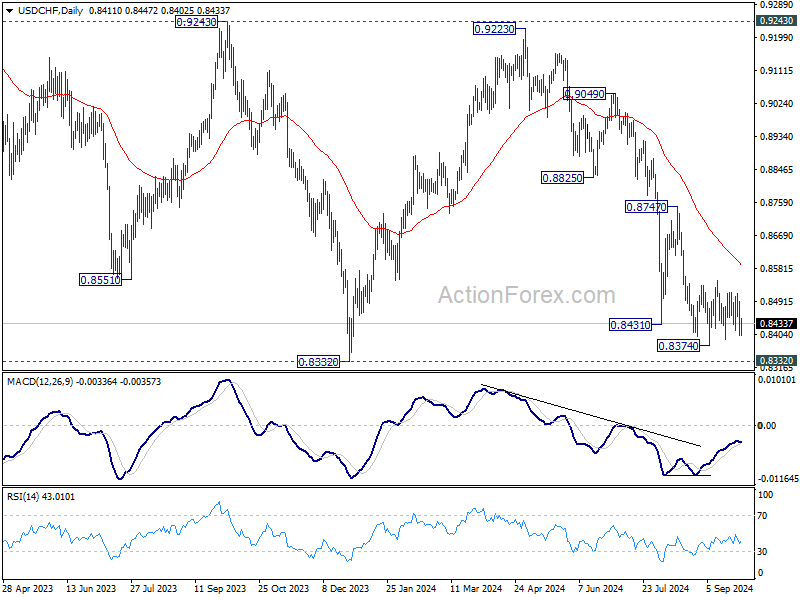

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8374; (P) 0.8433; (R1) 0.8465; More…

USD/CHF is still bounded in sideway trading and intraday bias remains neutral. Further decline is in favor with 0.8548 resistance intact. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. Nevertheless, firm break of 0.8548 will turn bias back to the upside for stronger rebound to 0.8747 resistance instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

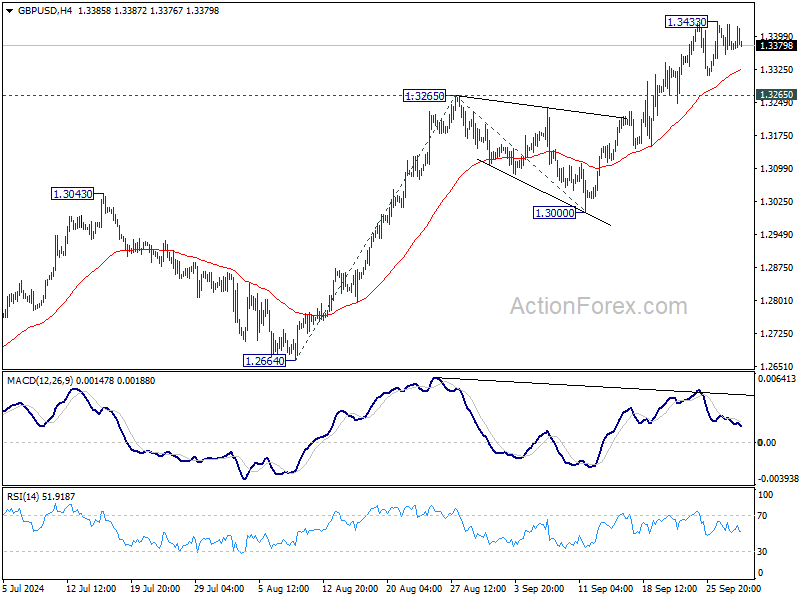

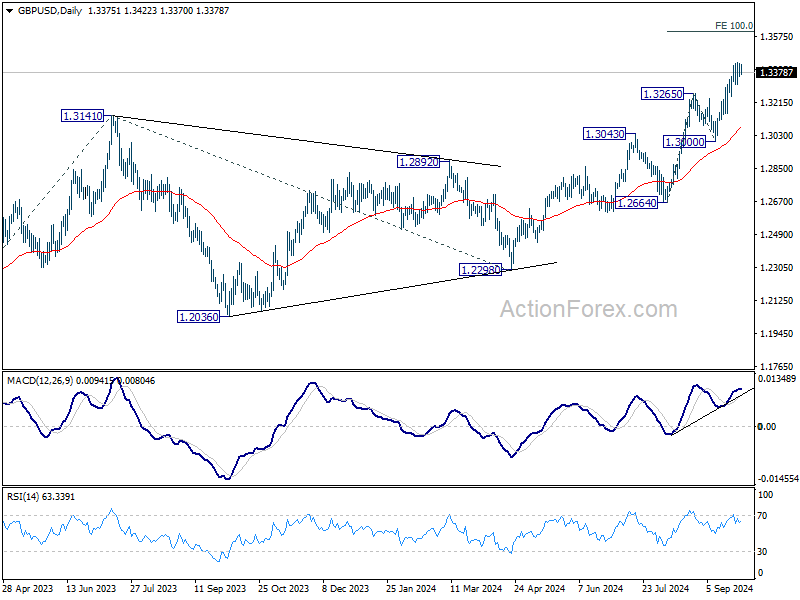

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3346; (P) 1.3387; (R1) 1.3414; More...

GBP/USD is extending consolidation below 1.3433 temporary top and intraday bias remains neutral. Further rally is expected as long as 1.3265 resistance turned support holds. Above 1.3433 will resume larger rise to 100% projection of 1.2664 to 1.3265 from 1.3000 at 1.3601 next. Nevertheless, considering bearish divergence condition in 4H MACD, firm break of 1.3265 will indicate short term topping and turn bias back to the downside for 1.3000 support instead.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. For now, outlook will stay bullish as long as 1.3000 support holds, even in case of deep pullback.

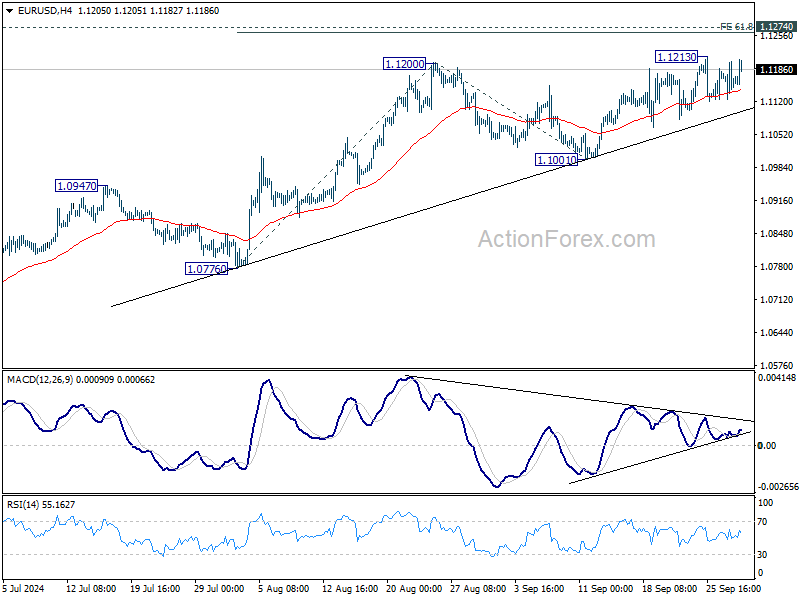

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1124; (P) 1.1164; (R1) 1.1202; More....

EUR/USD recovers mildly today but stays in range below 1.1213. Intraday bias remains neutral and more consolidations could still be seen. But further rally is expected as long as 1.1001 support holds. Above 1.1213 will resume the rise from 1.0665 to 1.1274 high. Firm break there will resume larger up trend. Next near term target will be 100% projection of 1.0776 to 1.1200 from 1.1001 at 1.1425.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.