Sample Category Title

GBP/JPY Weekly Outlook

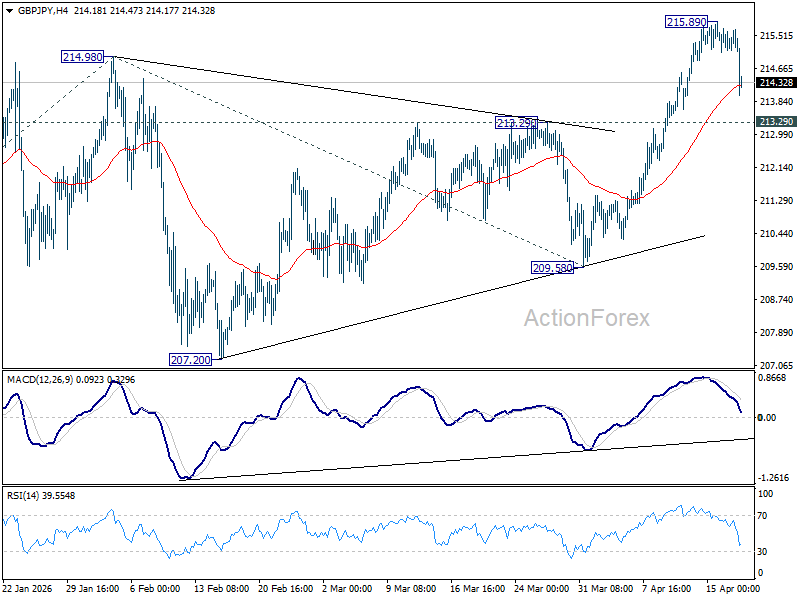

GBP/JPY's pullback from 215.89 accelerated lower last week, but downside is contained above 213.29 resistance turned support. Initial bias stays neutral this week first. Firm break of 215.89 will resume larger up trend to 61.8% projection of 199.04 to 214.98 from 209.58 at 219.43.

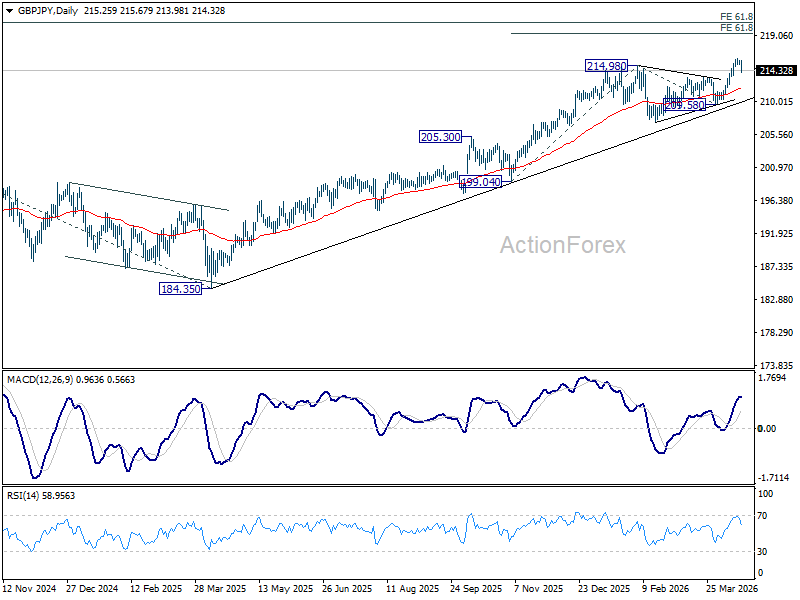

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 204.10) holds, even in case of another deep pullback.

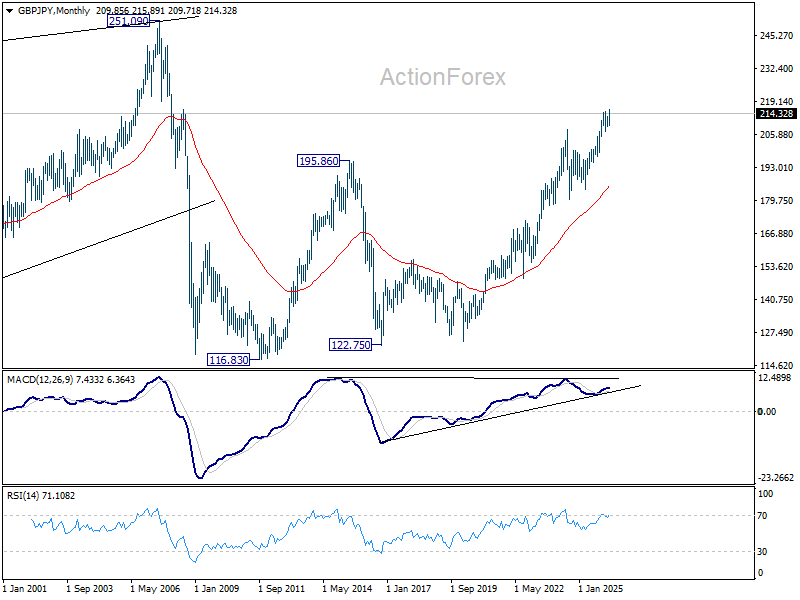

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 184.82) holds.

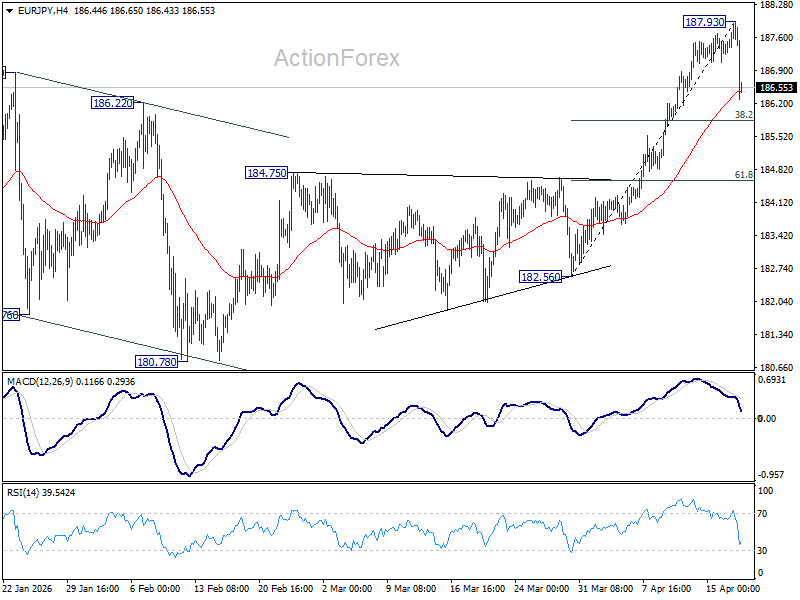

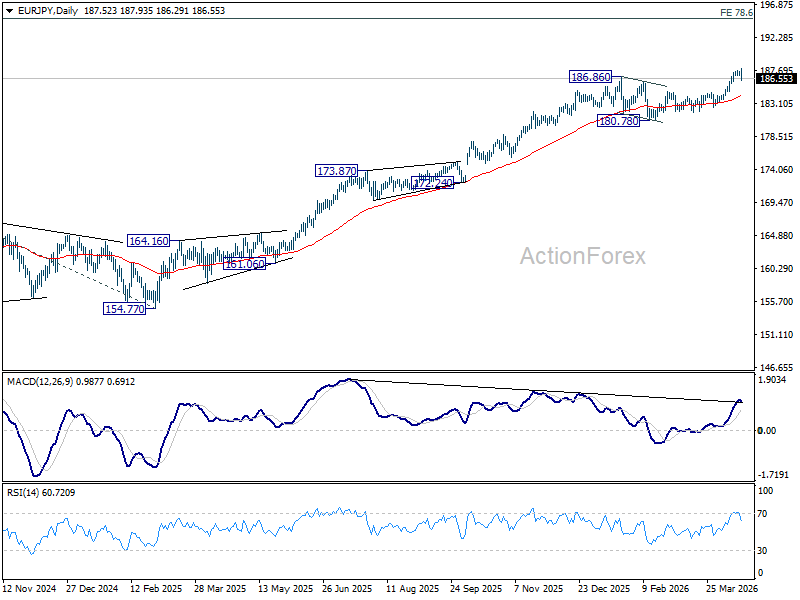

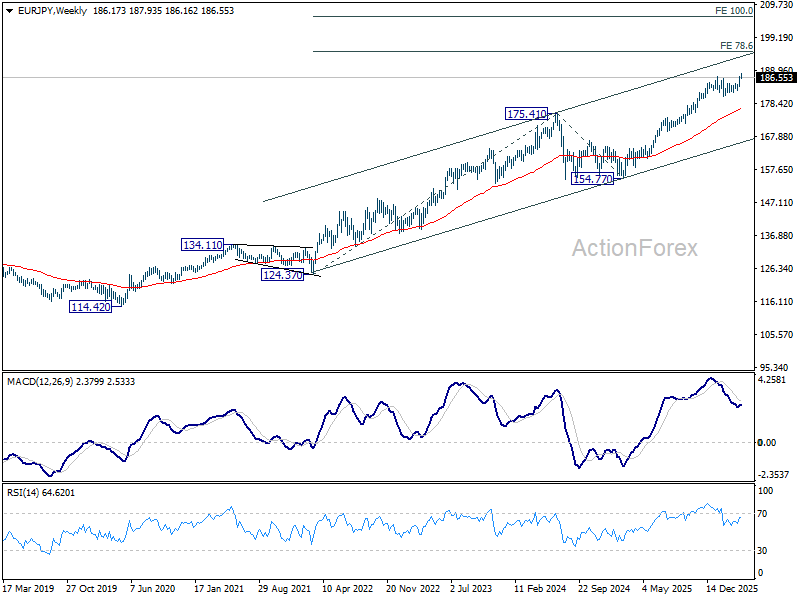

EUR/JPY Weekly Outlook

EUR/JPY's sharp reversal last week suggests that a short term top was already formed at 187.93. Initial bias is mildly on the downside this week for 38.2% retracement of 182.56 to 187.93 at 185.87. For now, risk will stay mildly on the downside as long as 187.93 resistance holds, in case of recovery.

In the bigger picture, up trend from 114.42 (2020 low) is in progress Next target is 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. For now, medium term outlook will stay bullish as long as 180.78 support holds, even in case of deeper pullback.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long 55 W EMA (now at 176.94) holds.

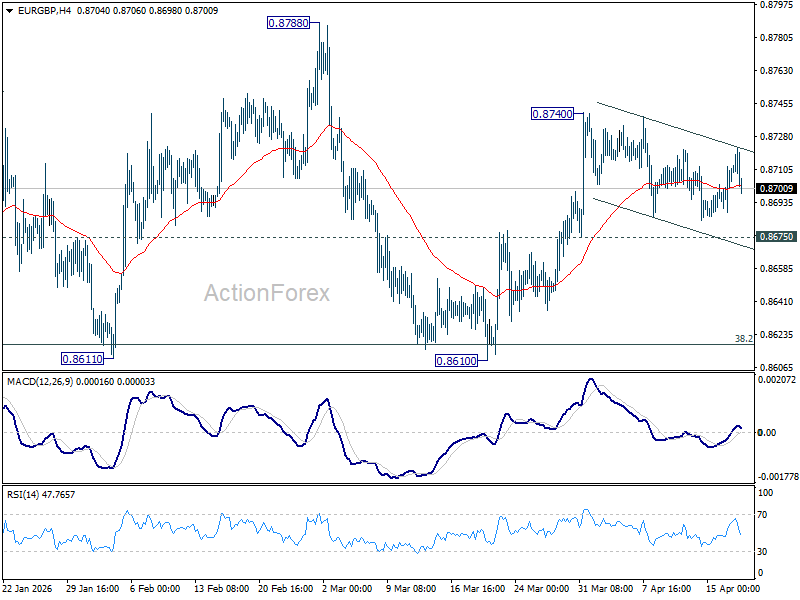

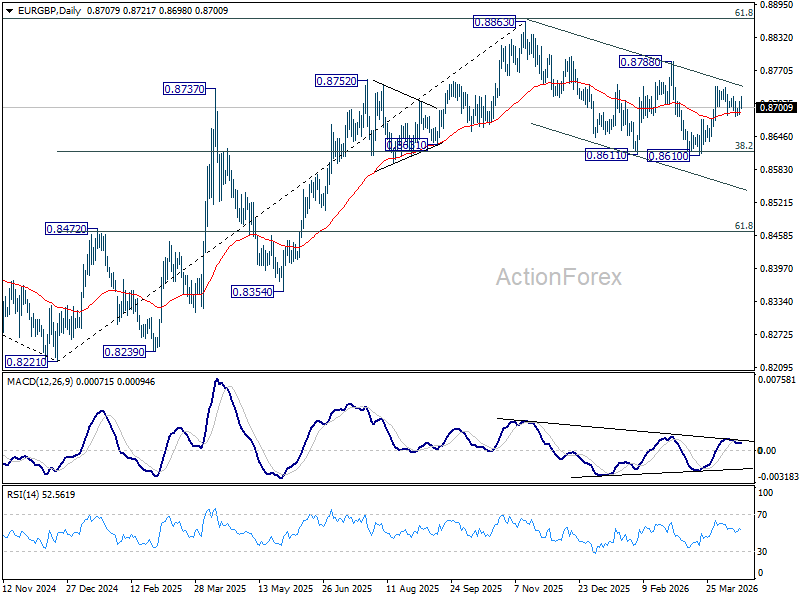

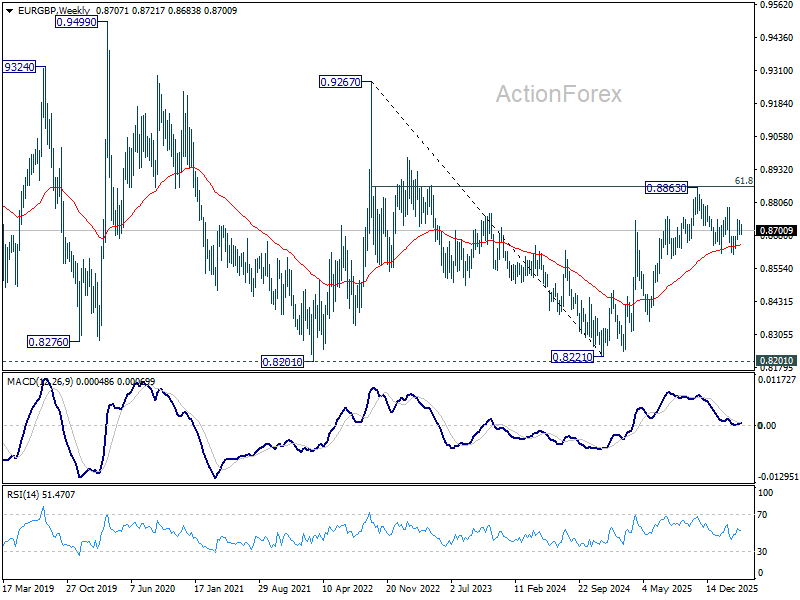

EUR/GBP Weekly Outlook

EUR/GBP gyrated in range below 0.8740 last week and outlook is unchanged. Initial bias remains neutral this week first. As long as 0.8675 support holds, further rise remains mildly in favor. On the upside, break of 0.8740 will resume the rally from 0.8610 to 0.8788 resistance. However, firm break of 0.8675 will turn bias back to the downside for retesting 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be ready to resume through 0.8863 (2025 high). Nevertheless, sustained trading below 0.8618 should confirm bearish reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

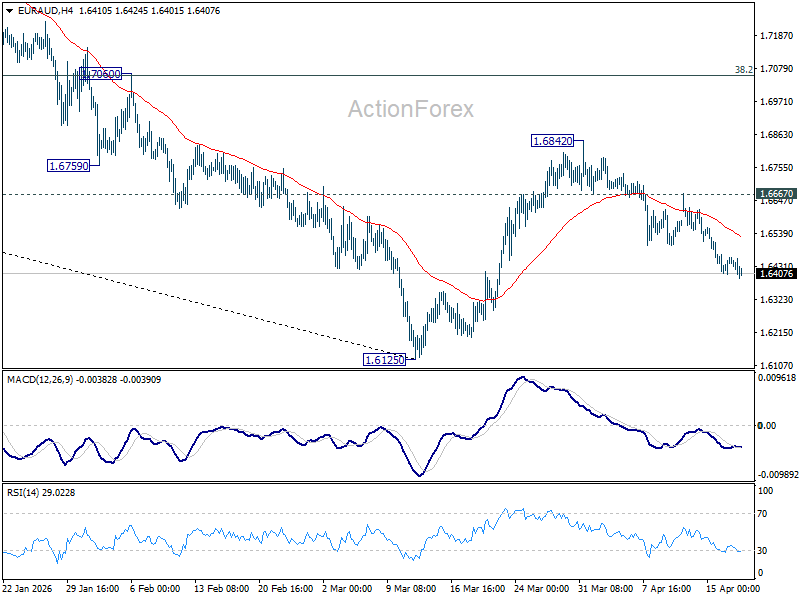

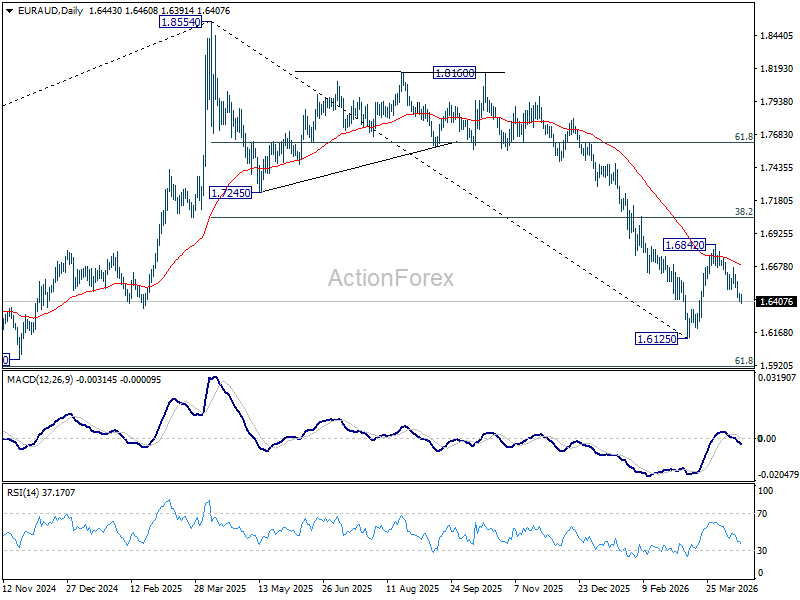

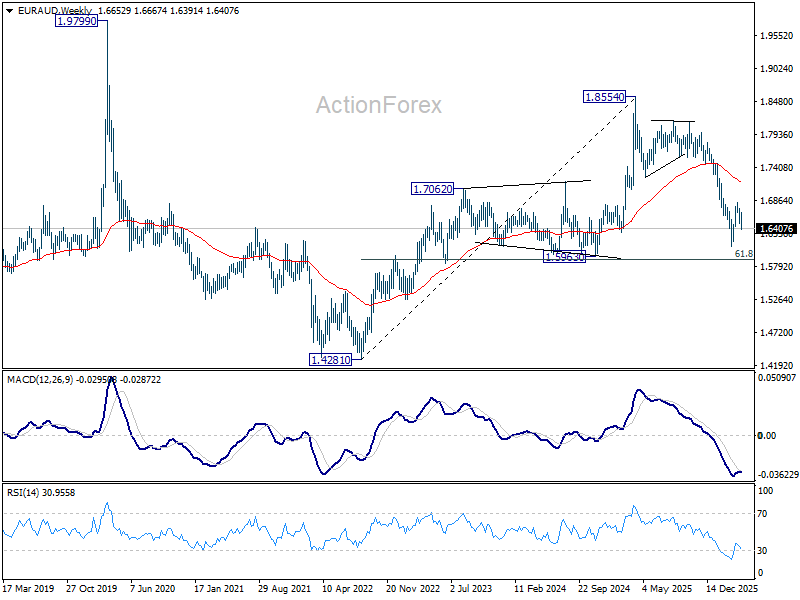

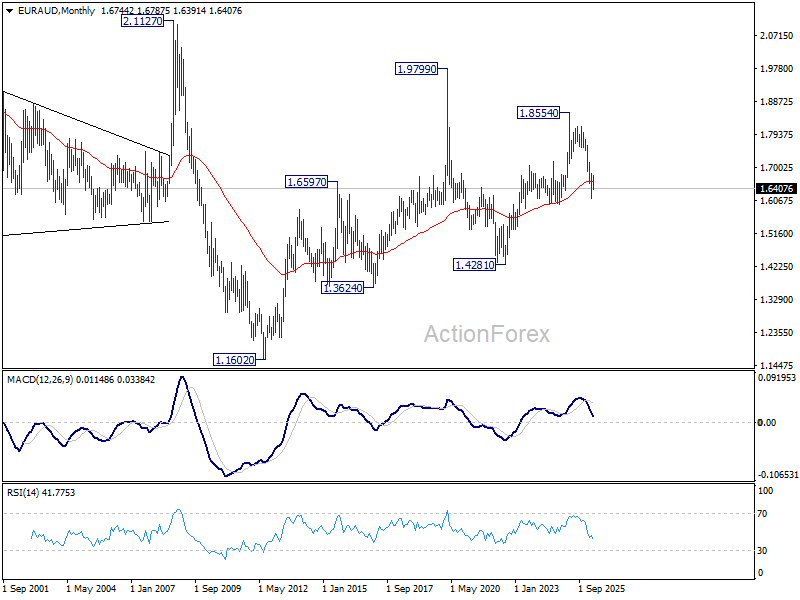

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.6842 resumed last week. Outlook is unchanged that rebound from 1.6125 should have completed after rejection by 55 D EMA. Initial bias remains on the downside this week for retesting 1.6125 low. Firm break there will resume whole down trend from 1.8554 to 1.5913 fibonacci level next. For now, risk will stay on the downside as long as 1.6667 resistance holds, in case of recovery.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7157) holds, even in case of strong rebound.

In the longer term picture, fall from 1.8554 is seen as the third leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Sustained trading below 55 M EMA (now at 1.6601) will confirm this bearish case, and pave the way back towards 1.4281.

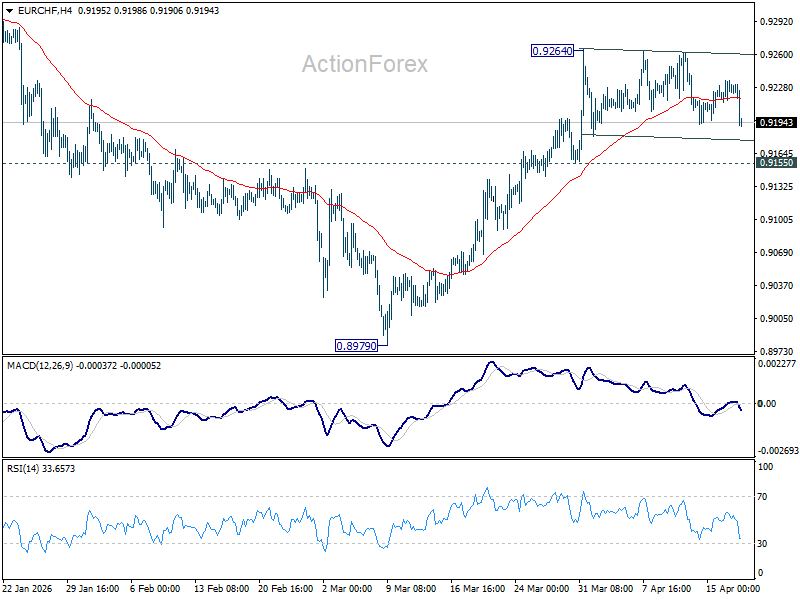

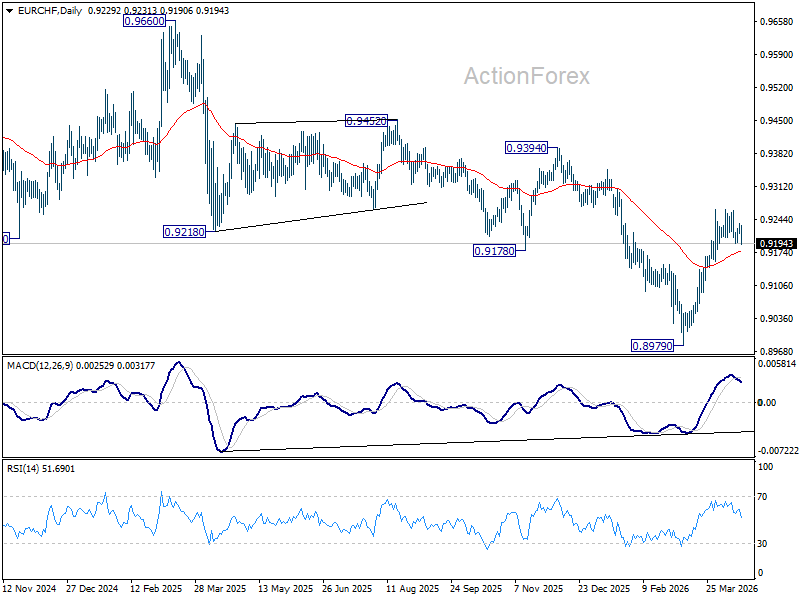

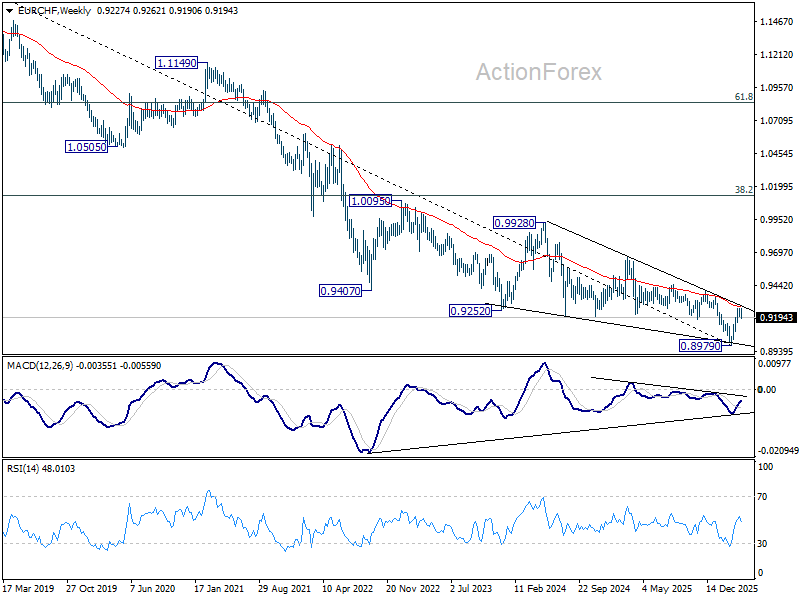

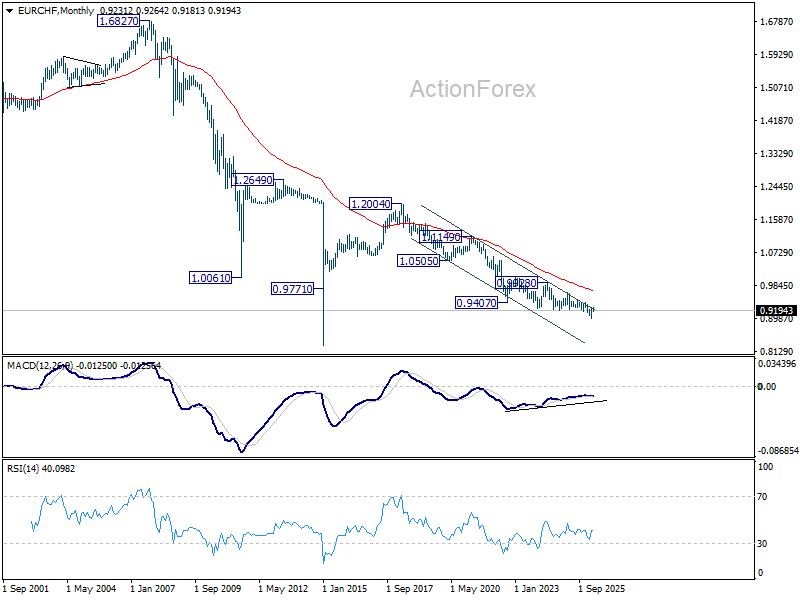

EUR/CHF Weekly Outlook

EUR/CHF's sideway consolidation continued last week and outlook is unchanged. Initial bias remains neutral this week. With 0.9155 support intact, further rally is still expected. Firm break of 0.9264 will resume the rise from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9280) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

In the long term picture, outlook will stay bearish as long as 0.9407 support turned resistance (2022 low) holds. However, firm break of 0.9407 will argue that the down trend from 1.2004 (2018 high) has completed with five waves down to 0.8979. Stronger rebound should then be seen to 38.2% retracement of 1.2004 to 0.8979 at 1.0135 in the medium term.

Summary 4/20 – 4/24

Monday, Apr 20, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 175M | -257M |

| 01:00 | CNY | 1-y Loan Prime Rate | 3.00% | 3.00% |

| 01:00 | CNY | 5-y Loan Prime Rate | 3.50% | 3.50% |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | -0.40% | 1.70% |

| 06:00 | EUR | Germany PPI M/M Mar | 1.40% | -0.50% |

| 06:00 | EUR | Germany PPI Y/Y Mar | -3.30% | |

| 12:30 | CAD | CPI M/M Mar | 1.10% | 0.50% |

| 12:30 | CAD | CPI Y/Y Mar | 2.50% | 1.80% |

| 12:30 | CAD | CPI Median Y/Y Mar | 2.40% | 2.30% |

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 2.30% | 2.30% |

| 12:30 | CAD | CPI Common Y/Y Mar | 2.60% | 2.40% |

| 14:30 | CAD | BoC Business Outlook Survey |

| 22:45 | NZD |

| Trade Balance (NZD) Mar | |

| Consensus | 175M |

| Previous | -257M |

| 01:00 | CNY |

| 1-y Loan Prime Rate | |

| Consensus | 3.00% |

| Previous | 3.00% |

| 01:00 | CNY |

| 5-y Loan Prime Rate | |

| Consensus | 3.50% |

| Previous | 3.50% |

| 04:30 | JPY |

| Tertiary Industry Index M/M Feb | |

| Consensus | -0.40% |

| Previous | 1.70% |

| 06:00 | EUR |

| Germany PPI M/M Mar | |

| Consensus | 1.40% |

| Previous | -0.50% |

| 06:00 | EUR |

| Germany PPI Y/Y Mar | |

| Consensus | |

| Previous | -3.30% |

| 12:30 | CAD |

| CPI M/M Mar | |

| Consensus | 1.10% |

| Previous | 0.50% |

| 12:30 | CAD |

| CPI Y/Y Mar | |

| Consensus | 2.50% |

| Previous | 1.80% |

| 12:30 | CAD |

| CPI Median Y/Y Mar | |

| Consensus | 2.40% |

| Previous | 2.30% |

| 12:30 | CAD |

| CPI Trimmed Y/Y Mar | |

| Consensus | 2.30% |

| Previous | 2.30% |

| 12:30 | CAD |

| CPI Common Y/Y Mar | |

| Consensus | 2.60% |

| Previous | 2.40% |

| 14:30 | CAD |

| BoC Business Outlook Survey | |

| Consensus | |

| Previous | |

Tuesday, Apr 21, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 22:00 | NZD | NZIER Business Confidence Q1 | 48 | |

| 22:45 | NZD | CPI Q/Q Q1 | 0.80% | 0.60% |

| 22:45 | NZD | CPI Y/Y Q1 | 2.90% | 3.10% |

| 06:00 | GBP | Claimant Count Change Mar | 21.4K | 24.7K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | 5.20% | 5.20% |

| 06:00 | GBP | Average Earnings Excl Bonus 3M/Y Feb | 3.50% | 3.80% |

| 06:00 | GBP | Average Earnings Incl Bonus 3M/Y Feb | 3.60% | 3.90% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | -6.7 | -0.5 |

| 09:00 | EUR | Germany ZEW Current Situation Apr | -69.5 | -62.9 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | -10.3 | -8.5 |

| 12:30 | USD | Retail Sales M/M Mar | 1.30% | 0.60% |

| 12:30 | USD | Retail Sales ex Autos M/M Mar | 1.30% | 0.50% |

| 14:00 | USD | Pending Home Sales M/M Mar | 0.00% | 1.80% |

| 14:00 | USD | Business Inventories Feb | 0.10% | -0.10% |

| 22:00 | NZD |

| NZIER Business Confidence Q1 | |

| Consensus | |

| Previous | 48 |

| 22:45 | NZD |

| CPI Q/Q Q1 | |

| Consensus | 0.80% |

| Previous | 0.60% |

| 22:45 | NZD |

| CPI Y/Y Q1 | |

| Consensus | 2.90% |

| Previous | 3.10% |

| 06:00 | GBP |

| Claimant Count Change Mar | |

| Consensus | 21.4K |

| Previous | 24.7K |

| 06:00 | GBP |

| ILO Unemployment Rate (3M) Feb | |

| Consensus | 5.20% |

| Previous | 5.20% |

| 06:00 | GBP |

| Average Earnings Excl Bonus 3M/Y Feb | |

| Consensus | 3.50% |

| Previous | 3.80% |

| 06:00 | GBP |

| Average Earnings Incl Bonus 3M/Y Feb | |

| Consensus | 3.60% |

| Previous | 3.90% |

| 09:00 | EUR |

| Germany ZEW Economic Sentiment Apr | |

| Consensus | -6.7 |

| Previous | -0.5 |

| 09:00 | EUR |

| Germany ZEW Current Situation Apr | |

| Consensus | -69.5 |

| Previous | -62.9 |

| 09:00 | EUR |

| Eurozone ZEW Economic Sentiment Apr | |

| Consensus | -10.3 |

| Previous | -8.5 |

| 12:30 | USD |

| Retail Sales M/M Mar | |

| Consensus | 1.30% |

| Previous | 0.60% |

| 12:30 | USD |

| Retail Sales ex Autos M/M Mar | |

| Consensus | 1.30% |

| Previous | 0.50% |

| 14:00 | USD |

| Pending Home Sales M/M Mar | |

| Consensus | 0.00% |

| Previous | 1.80% |

| 14:00 | USD |

| Business Inventories Feb | |

| Consensus | 0.10% |

| Previous | -0.10% |

Wednesday, Apr 22, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Mar | 0.20T | -0.37T |

| 01:00 | AUD | Westpac Leading Index M/M Mar | -0.10% | |

| 06:00 | GBP | CPI M/M Mar | 0.60% | 0.40% |

| 06:00 | GBP | CPI Y/Y Mar | 3.30% | 3.00% |

| 06:00 | GBP | Core CPI Y/Y Mar | 3.20% | 3.20% |

| 06:00 | GBP | RPI M/M Mar | 0.40% | |

| 06:00 | GBP | RPI Y/Y Mar | 3.90% | 3.60% |

| 06:00 | GBP | PPI Input M/M Mar | 2.90% | 0.80% |

| 06:00 | GBP | PPI Input Y/Y Mar | 0.70% | 0.50% |

| 06:00 | GBP | PPI Output M/M Mar | 1.00% | -0.50% |

| 06:00 | GBP | PPI Output Y/Y Mar | 1.70% | |

| 06:00 | GBP | PPI Core Output M/M Mar | -0.80% | |

| 06:00 | GBP | PPI Core Output Y/Y Mar | 2.00% | |

| 12:30 | CAD | New Housing Price Index M/M Mar | 0.20% | 0.30% |

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | -17 | -16 |

| 14:30 | USD | Crude Oil Inventories (Apr 17) | -1.9M | -0.9M |

| 23:50 | JPY |

| Trade Balance (JPY) Mar | |

| Consensus | 0.20T |

| Previous | -0.37T |

| 01:00 | AUD |

| Westpac Leading Index M/M Mar | |

| Consensus | |

| Previous | -0.10% |

| 06:00 | GBP |

| CPI M/M Mar | |

| Consensus | 0.60% |

| Previous | 0.40% |

| 06:00 | GBP |

| CPI Y/Y Mar | |

| Consensus | 3.30% |

| Previous | 3.00% |

| 06:00 | GBP |

| Core CPI Y/Y Mar | |

| Consensus | 3.20% |

| Previous | 3.20% |

| 06:00 | GBP |

| RPI M/M Mar | |

| Consensus | |

| Previous | 0.40% |

| 06:00 | GBP |

| RPI Y/Y Mar | |

| Consensus | 3.90% |

| Previous | 3.60% |

| 06:00 | GBP |

| PPI Input M/M Mar | |

| Consensus | 2.90% |

| Previous | 0.80% |

| 06:00 | GBP |

| PPI Input Y/Y Mar | |

| Consensus | 0.70% |

| Previous | 0.50% |

| 06:00 | GBP |

| PPI Output M/M Mar | |

| Consensus | 1.00% |

| Previous | -0.50% |

| 06:00 | GBP |

| PPI Output Y/Y Mar | |

| Consensus | |

| Previous | 1.70% |

| 06:00 | GBP |

| PPI Core Output M/M Mar | |

| Consensus | |

| Previous | -0.80% |

| 06:00 | GBP |

| PPI Core Output Y/Y Mar | |

| Consensus | |

| Previous | 2.00% |

| 12:30 | CAD |

| New Housing Price Index M/M Mar | |

| Consensus | 0.20% |

| Previous | 0.30% |

| 14:00 | EUR |

| Eurozone Consumer Confidence Apr P | |

| Consensus | -17 |

| Previous | -16 |

| 14:30 | USD |

| Crude Oil Inventories (Apr 17) | |

| Consensus | -1.9M |

| Previous | -0.9M |

Thursday, Apr 23, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Apr P | 49.8 | |

| 23:00 | AUD | Services PMI Apr P | 46.3 | |

| 00:30 | JPY | Manufacturing PMI Apr P | 51.2 | 51.6 |

| 00:30 | JPY | Services PMI Apr P | 53.4 | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Mar | 10.3B | 14.3B |

| 07:15 | EUR | France Manufacturing PMI Apr P | 49.5 | 50 |

| 07:15 | EUR | France Services PMI Apr P | 48.5 | 48.8 |

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 51.3 | 52.2 |

| 07:30 | EUR | Germany Services PMI Apr P | 50.4 | 50.9 |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 50.7 | 51.6 |

| 08:00 | EUR | Eurozone Services PMI Apr P | 49.8 | 50.2 |

| 08:30 | GBP | Manufacturing PMI Apr P | 50.2 | 51 |

| 08:30 | GBP | Services PMI Apr P | 50 | 50.5 |

| 12:30 | CAD | Industrial Product Price M/M Mar | 1.80% | 0.40% |

| 12:30 | CAD | Raw Material Price Index Mar | 9.50% | 0.60% |

| 12:30 | USD | Initial Jobless Claims (Apr 17) | 210K | 207K |

| 13:45 | USD | Manufacturing PMI Apr P | 52.5 | 52.3 |

| 13:45 | USD | Services PMI Apr P | 50.1 | 49.8 |

| 14:30 | USD | Natural Gas Storage (Apr 17) | 96B | 59B |

| 23:00 | AUD |

| Manufacturing PMI Apr P | |

| Consensus | |

| Previous | 49.8 |

| 23:00 | AUD |

| Services PMI Apr P | |

| Consensus | |

| Previous | 46.3 |

| 00:30 | JPY |

| Manufacturing PMI Apr P | |

| Consensus | 51.2 |

| Previous | 51.6 |

| 00:30 | JPY |

| Services PMI Apr P | |

| Consensus | |

| Previous | 53.4 |

| 06:00 | GBP |

| Public Sector Net Borrowing (GBP) Mar | |

| Consensus | 10.3B |

| Previous | 14.3B |

| 07:15 | EUR |

| France Manufacturing PMI Apr P | |

| Consensus | 49.5 |

| Previous | 50 |

| 07:15 | EUR |

| France Services PMI Apr P | |

| Consensus | 48.5 |

| Previous | 48.8 |

| 07:30 | EUR |

| Germany Manufacturing PMI Apr P | |

| Consensus | 51.3 |

| Previous | 52.2 |

| 07:30 | EUR |

| Germany Services PMI Apr P | |

| Consensus | 50.4 |

| Previous | 50.9 |

| 08:00 | EUR |

| Eurozone Manufacturing PMI Apr P | |

| Consensus | 50.7 |

| Previous | 51.6 |

| 08:00 | EUR |

| Eurozone Services PMI Apr P | |

| Consensus | 49.8 |

| Previous | 50.2 |

| 08:30 | GBP |

| Manufacturing PMI Apr P | |

| Consensus | 50.2 |

| Previous | 51 |

| 08:30 | GBP |

| Services PMI Apr P | |

| Consensus | 50 |

| Previous | 50.5 |

| 12:30 | CAD |

| Industrial Product Price M/M Mar | |

| Consensus | 1.80% |

| Previous | 0.40% |

| 12:30 | CAD |

| Raw Material Price Index Mar | |

| Consensus | 9.50% |

| Previous | 0.60% |

| 12:30 | USD |

| Initial Jobless Claims (Apr 17) | |

| Consensus | 210K |

| Previous | 207K |

| 13:45 | USD |

| Manufacturing PMI Apr P | |

| Consensus | 52.5 |

| Previous | 52.3 |

| 13:45 | USD |

| Services PMI Apr P | |

| Consensus | 50.1 |

| Previous | 49.8 |

| 14:30 | USD |

| Natural Gas Storage (Apr 17) | |

| Consensus | 96B |

| Previous | 59B |

Friday, Apr 24, 2026

| GMT | Ccy | Events | Cons | Prev |

|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Apr | -25 | -21 |

| 23:30 | JPY | National CPI Y/Y Mar | 1.30% | |

| 23:30 | JPY | National CPI Core Y/Y Mar | 1.70% | 1.60% |

| 23:30 | JPY | National CPI Core-Core Y/Y Mar | 2.50% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 2.90% | 2.70% |

| 06:00 | GBP | Retail Sales M/M Mar | 0.20% | -0.40% |

| 08:00 | EUR | Germany IFO Business Climate Apr | 85.6 | 86.4 |

| 08:00 | EUR | Germany IFO Current Assessment Apr | 85.5 | 86.7 |

| 08:00 | EUR | Germany IFO Expectations Apr | 83.9 | 86 |

| 12:30 | CAD | Retail Sales M/M Feb | 0.90% | 1.10% |

| 12:30 | CAD | Retail Sales ex Autos M/M Feb | 0.80% | 0.80% |

| 14:00 | USD | UoM Consumer Sentiment Apr F | 47.6 | 47.6 |

| 14:00 | USD | UoM 1-Yr Inflation Expectations Apr F | 4.80% | 4.80% |

| 23:01 | GBP |

| GfK Consumer Confidence Apr | |

| Consensus | -25 |

| Previous | -21 |

| 23:30 | JPY |

| National CPI Y/Y Mar | |

| Consensus | |

| Previous | 1.30% |

| 23:30 | JPY |

| National CPI Core Y/Y Mar | |

| Consensus | 1.70% |

| Previous | 1.60% |

| 23:30 | JPY |

| National CPI Core-Core Y/Y Mar | |

| Consensus | |

| Previous | 2.50% |

| 23:50 | JPY |

| Corporate Service Price Index Y/Y Mar | |

| Consensus | 2.90% |

| Previous | 2.70% |

| 06:00 | GBP |

| Retail Sales M/M Mar | |

| Consensus | 0.20% |

| Previous | -0.40% |

| 08:00 | EUR |

| Germany IFO Business Climate Apr | |

| Consensus | 85.6 |

| Previous | 86.4 |

| 08:00 | EUR |

| Germany IFO Current Assessment Apr | |

| Consensus | 85.5 |

| Previous | 86.7 |

| 08:00 | EUR |

| Germany IFO Expectations Apr | |

| Consensus | 83.9 |

| Previous | 86 |

| 12:30 | CAD |

| Retail Sales M/M Feb | |

| Consensus | 0.90% |

| Previous | 1.10% |

| 12:30 | CAD |

| Retail Sales ex Autos M/M Feb | |

| Consensus | 0.80% |

| Previous | 0.80% |

| 14:00 | USD |

| UoM Consumer Sentiment Apr F | |

| Consensus | 47.6 |

| Previous | 47.6 |

| 14:00 | USD |

| UoM 1-Yr Inflation Expectations Apr F | |

| Consensus | 4.80% |

| Previous | 4.80% |

A Real Peace Process or a Fantasy? – Markets Weekly Outlook

- Discover our Weekly Market Outlook, exploring themes and events that forged financial flows throughout the week.

- Markets conclude a very volatile week, with hopes for peace going back and forth and sentiment losing its head

- Get ready for next week's action by exploring upcoming events across global Markets.

Week in review – A proper peace process unfolding, will it lead to an actual deal?

This week has been nothing short of historic.

Both the Nasdaq and S&P 500 have charged to fresh all-time highs, completely leaving the geopolitical panic behind as traders aggressively price in a proper peace agreement – The move has bulldozed through any type of resistances and prior records, in a move that has left many traders scratching their head.

Only the Dow Jones is looking to catch up to its younger peers, but is already on pace to do so – That is, if the current pricing withstands the weekend.

Nasdaq Daily Chart – April 17, 2026 – Source: TradingView

While the past two weeks of US-Iran negotiations have generated their fair share of chaotic headlines, the diplomatic process unfolding in Pakistan appears genuinely serious, with both sides making significant, market-moving concessions.

The absolute catalyst for the week was this morning's market-rocking news regarding the reopening of the Strait of Hormuz.

Bolstered by President Trump's remarks that he expects a finalized deal in a day or two, the geopolitical risk premium imploded.

WTI 4H Chart – April 17, 2026 – Source: TradingView

Oil prices collapsed nearly 10% since yesterday, completely erasing their previous rally to trade comfortably right below the $90 handle.

Notably, clear signs of insider trading emerged in the Crude market just before the announcement—a continuation of the wild market craziness that has defined Trump’s second term, but certainly not a first.

Moving forward, physical traders will be closely monitoring the Strait to see if actual tanker flows resume.

The euphoria isn't limited to traditional equities paying out big peace dividends. Cryptocurrencies caught a massive bid, with Bitcoin exploding back to life and rallying to sit just below the $80,000 (~$78,000) mark as the weekend approaches, also boosting other crypto assets.

On the macroeconomic front, the reality of the recent commodity shock is setting in. Both US CPI and PPI inflation reports rose strongly, although optimists will console as they missed their most extreme upside expectations.

However, this energy-driven jump could merely be the beginning of a much more significant inflationary wave hitting the economy over the coming months.

This week will provide fresh insights on inflation in other countries including Japan, Canada and the UK.

Now, participants are bracing for a pivotal week.

The current ceasefire officially expires on April 22 – Without a formal extension or a signed peace deal, this historic progress could vanish in a flash, throwing markets back into extreme volatility.

An actual deal will be mandatory to sustain the rally.

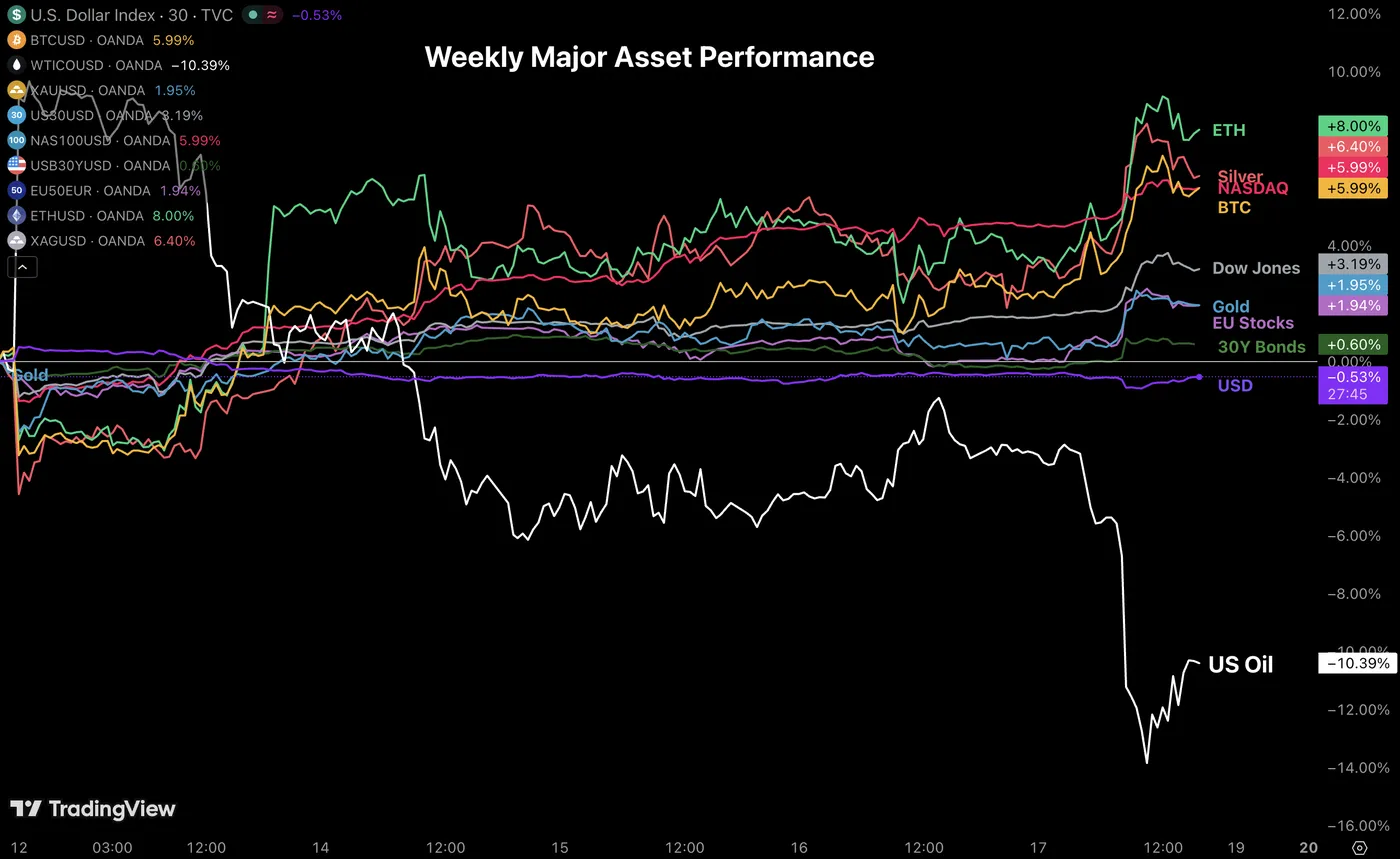

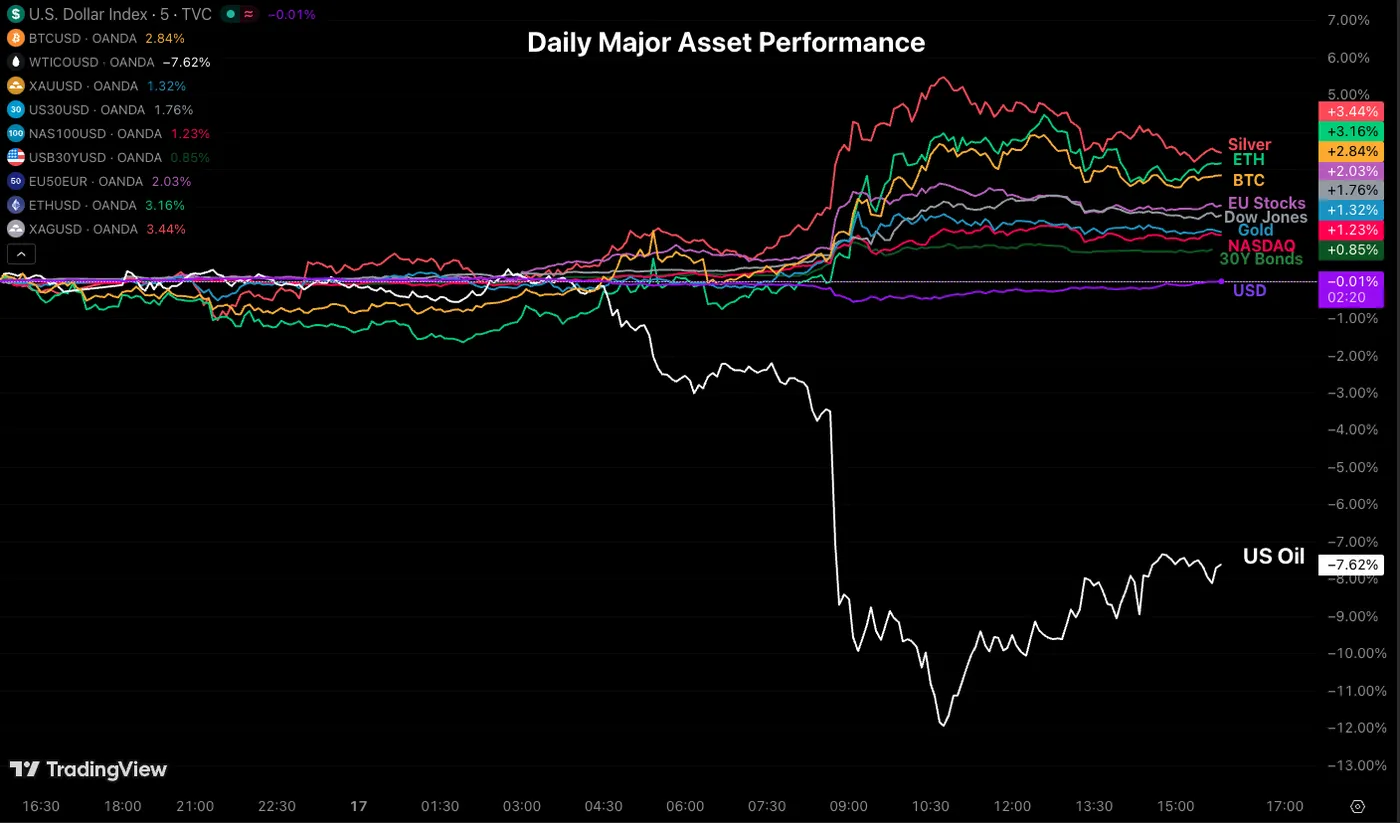

Weekly Performance across Asset Classes

Weekly Asset Performance – April 17, 2026 – Source: TradingView

As you can see, when Oil suffers, everybody dances. Even with the commodity gapping higher at the beginning of the week, Stock Markets have continued to explode higher and shortly after, everything followed.

WTI Crude is down 10% since the beginning of the week, and off 17% from its weekly opening gap.

The most risky assets have naturally outperformed the recovery, with Cryptos (ETH and Altcoins) on top, Silver dominating the Metals market and Nasdaq dominating global Stock benchmarks.

The Week Ahead – Major Inflation data coming up for Canada, the UK and Japan

Traders will have to get ready for a roller-coaster week, with macroeconomic data and major peace headlines on schedule.

Asia Pacific Markets – Japanese Inflation

Japan is under heavy pressure regarding their future monetary policy, and with the Inflation report for March incoming, where the first effects of Energy price hikes will be felt, the moment could be decisive.

The release is expected on Thursday evening (7:30 P.M.) – A large beat could confirm a rate hike at the end-May meeting if economic conditions don't worsen by then.

Bank of Japan representatives did refuse to comment on the issue during the IMF Meeting.

Europe and UK Markets – A Focus on the UK and Germany data

GBP traders will have a lot on their plate in the coming week, with a three-streak combo:

UK Employment, Inflation and Retail Sales, providing insights on the state of the economy and price rises as participants prepare for an economic shock.

Euro traders will have to pay close attention to the ZEW Economic Sentiment Survey and German PMIs that could also reshape forward looking pricing for the Old Continent.

North American Markets – Rare releases in the US, Geopolitics, and Canadian Inflation

The US takes a relative break from economic data, only releasing Retail sales on Tuesday and leaves space for continued price discovery.

Keep in mind that past week movements will be contingent on a sustainable peace deal with Iran, with the talks expected throughout the weekend.

CAD traders will also have to reprice chances of future hikes with Canadian Inflation opening the North American week on Monday.

A 2.5% consensus is announced, but energy price rises could definitely point to a beat on such low expectations.

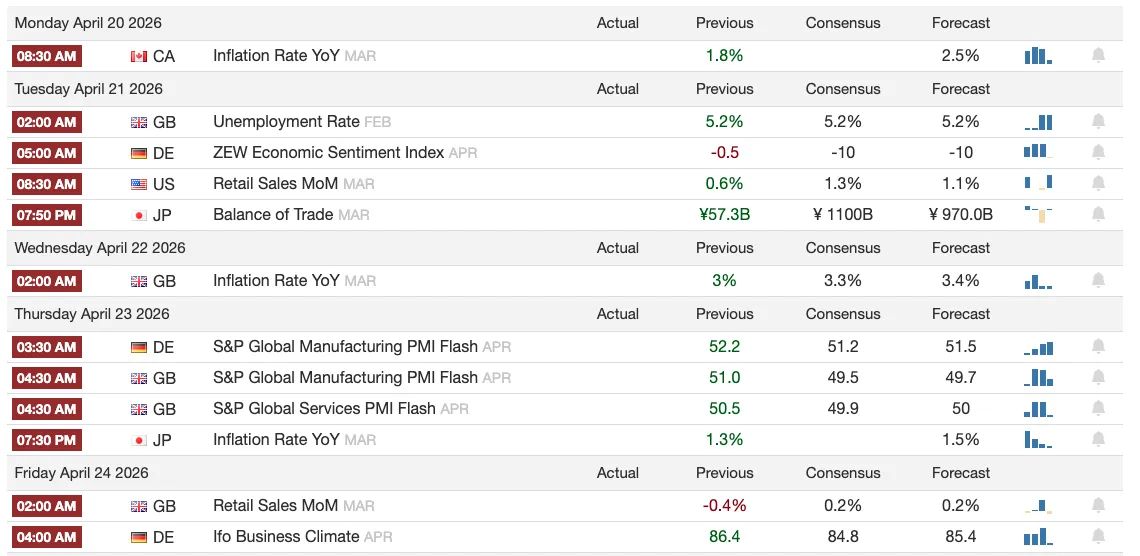

Next Week's High Tier Economic Events

Next week's Economic Calendar – Courtesy of TradingEconomics

Daily Market Wrap

Cross-Asset Daily Performance, April 17, 2026 – Source: TradingView

The Hormuz reopening news was icing on a very bullish cake to conclude this extremely positive week.

The heaviest Beta assets did what they did best and kept exploding higher across the Asset map – Cryptos and Silver, finish on top, both up around 3% on average.

US Benchmarks kept extending further to their newfound peaks, with the Dow Jones catching up and concluding the session on top.

On the other side, Crude Oil took a 10% beating after the news, but somewhat bounced as the session went by – Expect a lot of movement in the commodity in the coming week.

Safe Trades and an enjoyable weekend!

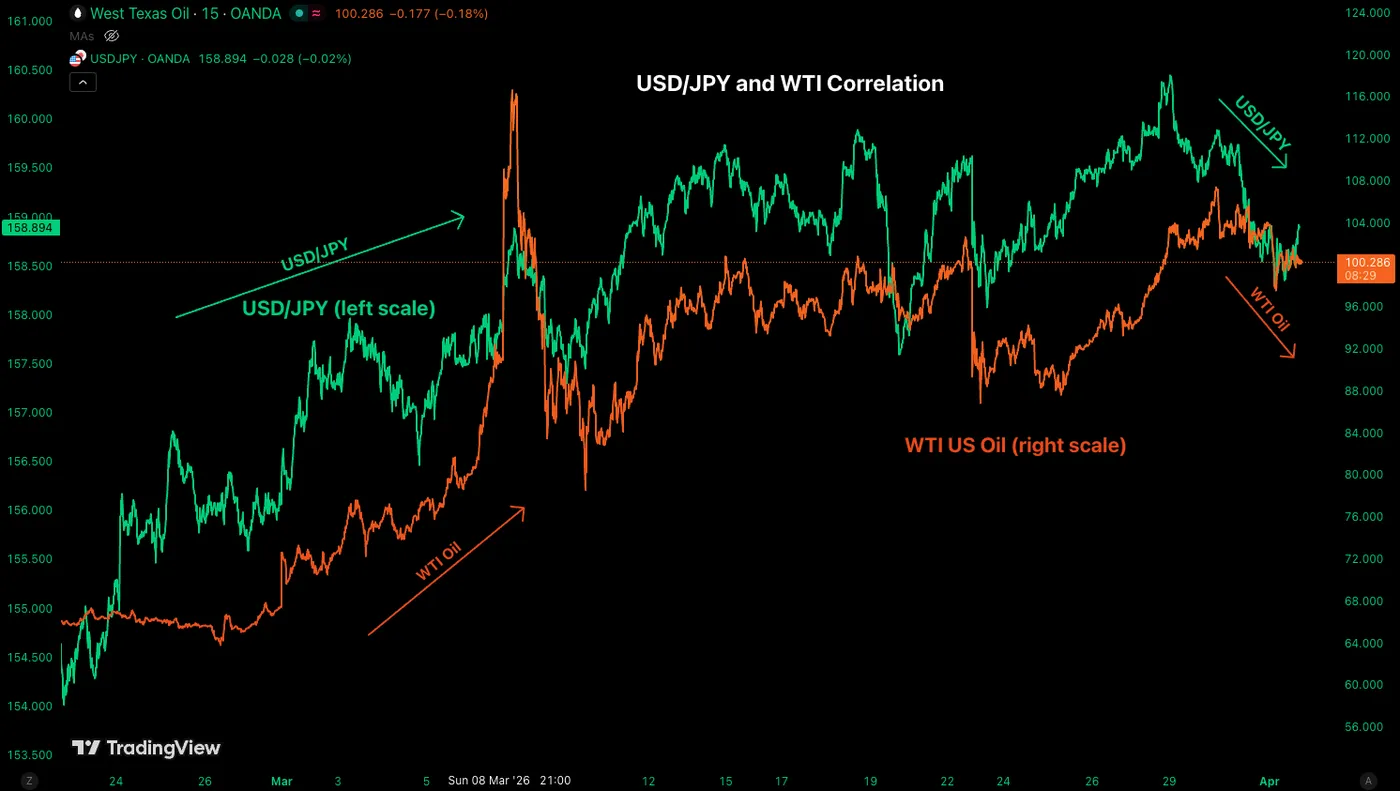

USD/JPY Forms a Major Head & Shoulders Pattern as Oil Crumbles – FX Analysis

USD/JPY was once again the main target for US Dollar bulls amid the ongoing major US-Iran War, which began on February 27 (with a positive twist in the past week and a half).

Energy commodity prices have more than doubled since the imposition of ceaseless supply restrictions from Iran's capture of the Strait of Hormuz. WTI and Brent Crude prices have at some point risen by more than 100% and are remaining about 35% higher than they were just at the beginning of February.

A significant portion of Asian crude oil imports depends on this region. As a result, prices for both physical crude and refined products have soared.

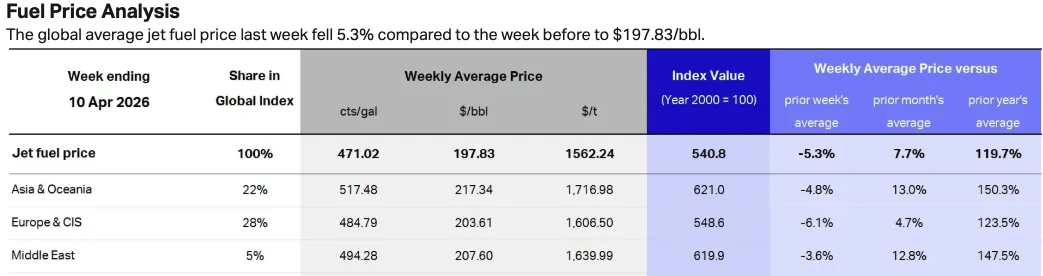

This was seen as a particular strain on the Eastern continent, and the clearest evidence is in the change in Jet Fuel prices.

Jet Fuel Prices Averages in Asia and Europe – Source: IATA. April 17, 2026

For such a populous region, particularly dependent on fossil fuels for electricity production and manufacturing, this has proven quite damaging.

Luckily for Japan, it has held the largest proven strategic oil reserves in the world, but this hasn't helped Forex hawks severely punish the JPY against the dominant US Dollar.

Victim of its own confused Monetary Policy, with largely expected rate hikes progressively fading out due to slower inflation reports and contradicting policymakers, the Land of the Rising Sun was the target of a large FX repricing.

Luckily for the Yen, the conflict is now priced to end soon.

The Strait of Hormuz was announced reopened this morning, with statements from both the US and Iran, and the Administration pushing for it to move forward with the negotiations.

USD/JPY and WTI Correlation. April 17, 2026 – Source: TradingView

USD/JPY has now entered a corrective phase, which could extend if the conflict were to end.

With a Head and Shoulders pattern forming, it will be important to see whether this move indeed has legs, pointing to longer-term bearish positioning in the pair.

Let's dive right into a multi-timeframe analysis for the Gopher – more commonly named, USD/JPY.

USD/JPY Multi-Timeframe Analysis

Daily Chart

USD/JPY Daily Chart. April 17, 2026 – Source: TradingView

USD/JPY is now entering a potentially significant corrective phase, pushing towards a break of the range established since March 10.

Testing and wicking at the 50-Day Moving Average (157.60), mean-reversion buying has faded the morning move, but the Daily RSI, now falling in bearish territory, is pointing to a move that could have just begun.

Let's take a closer look.

4H Chart and Technical Levels

USD/JPY 4H Chart. April 17, 2026 – Source: TradingView

The action shows a bit more details on the morning volatile action, with buyers re-entering at the precise 157.533 lows reached on March 19.

With the RSI quickly falling, the action is now close to oversold which could prompt interesting mean-reversion to offer pullback entry opportunities.

A break of the morning lows could extend to the 155.00 Mini-Support, target of the Head & Shoulders measured move.

Resistance levels

- 158.50 to 159.50 2026 Major Resistance (pullback interest)

- 4H 200-period MA 158.920

- April 2024 160.00 to 160.40 Major Resistance

- June Mini resistance 160.70 to 161.00

Support levels

- 157.533 lows reached on March 19 (bearish below)

- December highs Major Pivot 157.40 to 157.85

- 156.485 4H 200-period MA

- 156.00 Pivotal Support

- 155.00 Mini-Support

Safe Trades and wishing you a pleasant week-end ahead!

The Weekly Bottom Line: Temporary Reopening of Strait of Hormuz Boosts Financial Markets

Canadian Highlights

- Iran announced that the Strait of Hormuz will be open to commercial traffic during the Israel-Lebanon ceasefire. Details are still unfolding, but oil prices have plunged on the news.

- Ottawa moved earlier this week to blunt fuel‑price pressures by suspending the federal excise tax on gasoline, diesel, and aviation fuels through Labour Day.

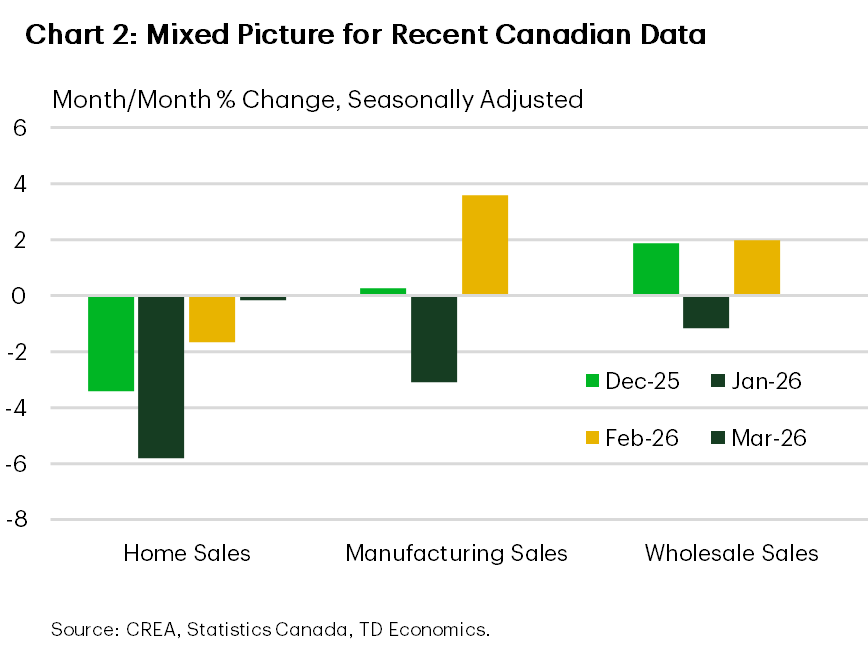

- Rebounds in manufacturing and wholesale sales in February offset continued softness in the housing market. Inflation data next week should confirm that underlying trends still argue for the Bank of Canada to keep interest rates steady at its April 29th decision.

U.S. Highlights

- Oil prices plummeted Friday morning as Iran declared the Strait of Hormuz fully open to commercial traffic during the 10-day cease fire between Israel and Lebanon.

- The producer price index rose to a three year high of 4% year-on-year in March, as energy prices rose sharply during the month.

- Federal Reserve officials generally voiced caution in public comments this week, as uncertainty related to the duration of the conflict complicates monetary policy deliberations.

Canada – Tax Breaks and Open Straits

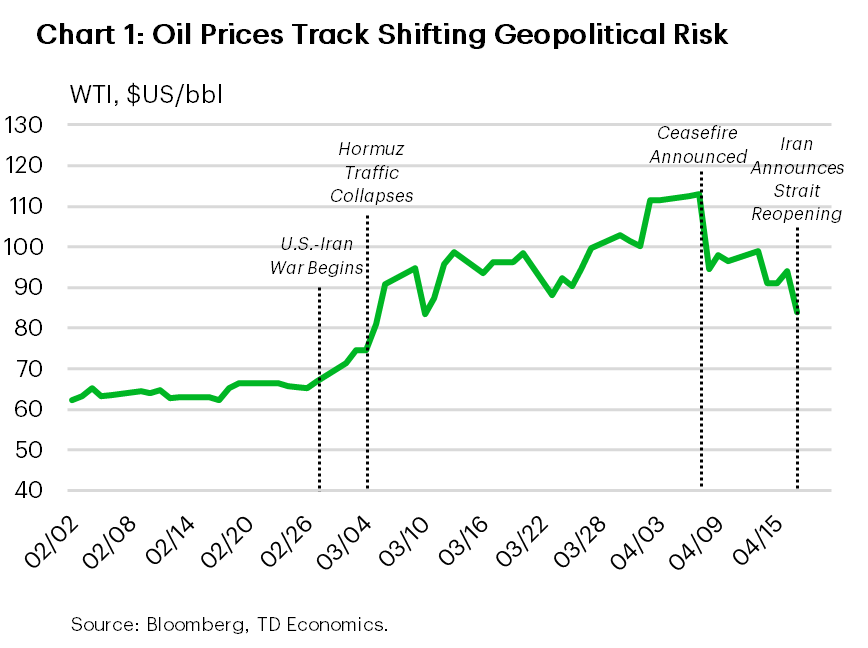

Hopes for a sustained easing in Middle East tensions firmed this morning after Iran announced it would fully reopen the Strait of Hormuz to commercial shipping for the duration of the Israel–Lebanon ceasefire. The move sent WTI prices cratering to below $84/bbl, down 13% on the week (Chart 1). That said, Tehran emphasized the reopening is temporary and conditional on the ceasefire holding, leaving markets sensitive to any renewed flare‑ups. Markets still need to digest the news, but for now, the TSX edged up roughly 1.5%, supported by strength in energy shares, while reduced U.S. Dollar safe-haven demand and supportive commodity prices lifted the CAD by 1.2% to 73.2 cents/USD.

In response to higher fuel costs, the Carney government announced a temporary suspension of federal fuel excise taxes earlier this week. These taxes amount to 10 cents/litre on gasoline and 4 cents/litre on both diesel and aviation fuels. The suspension will run from April 20th through Labour Day (September 7th), delivering about $2.4 billion in tax relief. The move is framed as short-term affordability support for households and fuel intensive sectors. The Liberal government also secured a majority in parliament this week after sweeping three federal byelections in Ontario and Quebec.

We won’t need to wait long to see how Ottawa’s finances are faring, with the Spring Economic Update set for April 28th. This update will show how war related shocks and new affordability measures affect the outlook. Importantly, this will be the first spring update under the new fiscal calendar adopted last fall, and markets will watch closely to see how temporary relief measures and higher defence and infrastructure ambitions are reconciled with medium-term deficit management.

Data releases continued to show subdued, but stabilizing, activity (Chart 2). National home resales were nearly flat in March, and prices slipped. Housing starts also weakened. The Canadian housing market remains stuck between uncertainty and affordability challenges, with early-spring activity lagging typical seasonal levels. However, manufacturing and wholesale sales improved in February, rebounding from January’s decline. This recovery was driven by better transportation equipment output, as auto assembly lines returned to normal after shutdowns for retooling. While these gains are positive, they follow earlier softness and leave activity levels only slightly higher than a year ago.

Next week’s focus turns to March inflation data, due Monday, which will help clarify how much of the recent energy shock is feeding through beyond gasoline. With inflation having been relatively well behaved heading into the conflict, the Bank of Canada (BoC) is likely to look through near term energy driven volatility, provided core measures remain contained. That sets up an important backdrop for the April 29th BoC decision, where we expect the policy rate to remain unchanged at 2.25%. That said, we expect them to monitor this shock carefully and act if circumstances change.

U.S. – Temporary Reopening of Strait of Hormuz Boosts Financial Markets

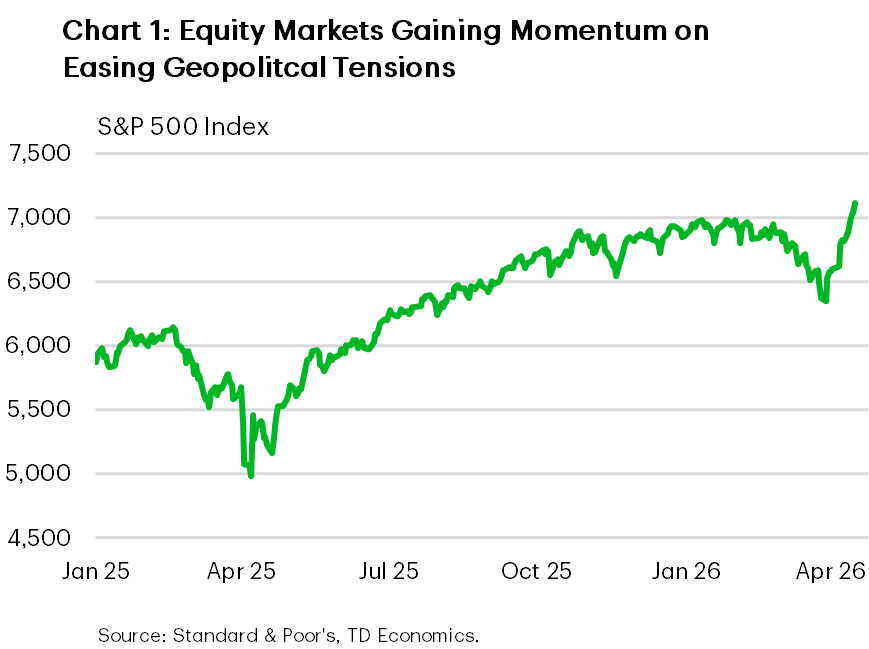

As the seventh week of the conflict in the Middle East comes to a close, the attention of financial markets remains squarely focused on the comments of officials in relation to a sustained resolution. Iran’s foreign minister announced Friday morning that the Strait of Hormuz would be open to commercial traffic during the recently negotiated 10-day ceasefire between Israel and Lebanon. This was met by a positive reaction in financial markets, but geopolitical risks are likely to remain elevated until a permanent resolution is achieved. The S&P 500 rose 4.4% this week to a new all-time high (Chart 1), while WTI oil fell 16% to $81/barrel as of the time of writing.

Economic data releases were sparse this week, but we did get an update on the housing market, which showed a 3.6% decline in existing home sales in March. The conflict in the Middle East and concerns regarding its impact on inflation has led to upward pressure on U.S. Treasury yields and subsequently mortgage rates. With mortgage rates continuing to fluctuate near a 6-month high of 6.4%, housing demand is likely to remain soft to start the spring buying season.

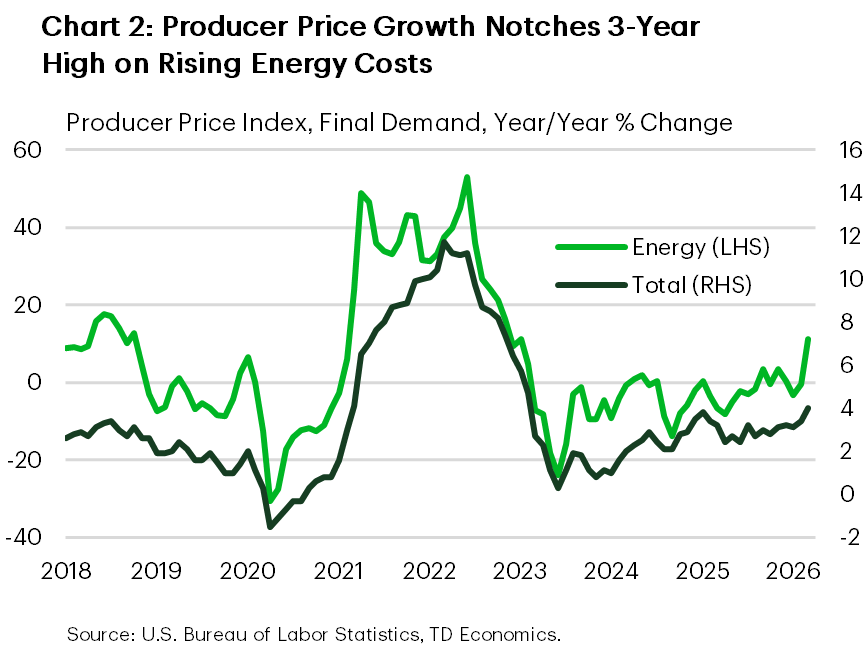

On the inflation front, the producer price index showed a sharp uptick in March, with energy prices driving the annual percentage change in the final demand index to 4% - the highest level since early 2023 (Chart 2). Similar to the March consumer price index report, spillover of higher energy prices into core inflation was largely absent, but this will be a key risk the Federal Reserve will be monitoring moving forward. If the current downward trend in oil prices is substantiated by a concrete resolution to the current supply disruptions in the Middle East, then this inflation shock is likely to prove transitory. However, risks remain skewed to the contrary the longer it takes for a permanent resolution to be achieved, with material impacts on households and businesses already occurring.

In the Federal Reserve Beige Book for April 2026, the conflict was cited as a major source of uncertainty that complicated decisions around hiring, pricing, and capital investments. In addition to higher energy costs, which were reported across all regions, businesses also reported facing input cost pressures from tariffs on metal products – which were expanded at the start of April – in addition to higher technology costs. Cumulatively, businesses noted these pressures were leading to margin compression, which could weigh on economic growth moving forward when combined with elevated uncertainty.

Comments from Federal Reserve officials this week were cautious overall. New York Fed President Williams stated on Thursday that stagflation risks were a concern, but also that the current stance of monetary policy was well-positioned to deal with the impacts of the conflict. Chicago Fed President Goolsbee also noted this week that the longer the conflict persists, the less likely rate cuts are for this year. In the wake of lower oil prices Friday morning, markets have increased bets to better than 50-50 that the Fed will cut rates a quarter point by the end of the year.

Economics Week Ahead

United States:

- Retail Sales (Tuesday), Kevin Warsh Confirmation Hearing (Tuesday)

G10 Economies:

- Canada CPI (Monday), U.K. Labor Market & CPI (Tuesday & Wednesday)

U.S. Week Ahead

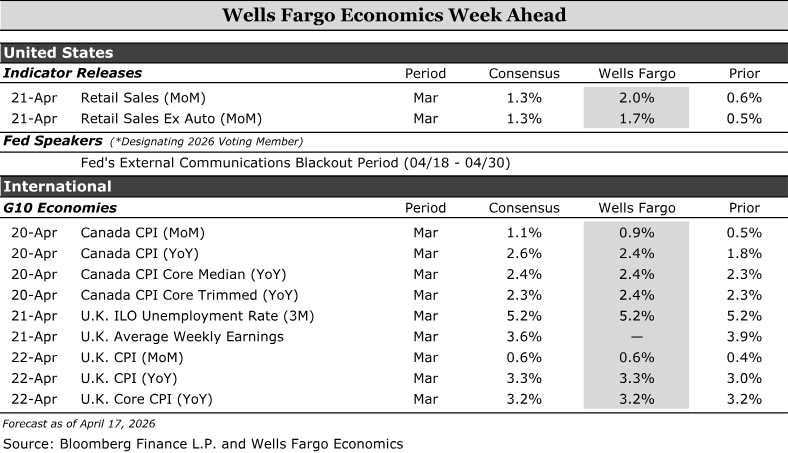

Retail Sales • Tuesday

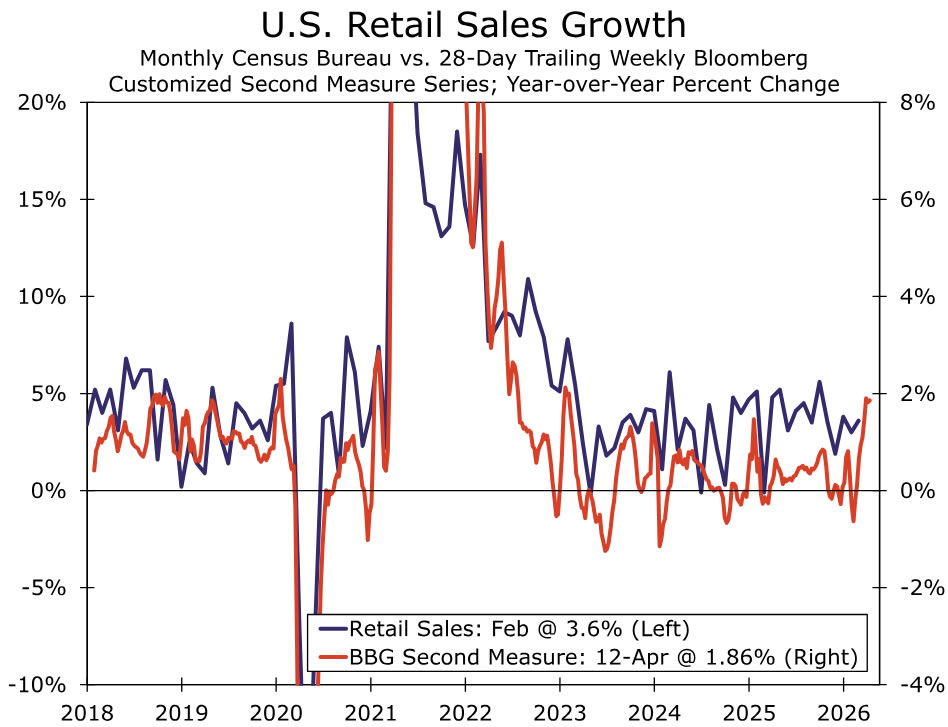

Consumers have largely been unfazed by the initial move higher in prices at the pump. High-frequency credit card data from Bloomberg suggests households have continued to spend into early April (chart), and we forecast broader retail sales popped 2.0% in March.

That gain, however, partially reflects higher prices rather than increased sales volume given retail sales are reported nominally. Overall sales were likely still broad in March, but we expect an outsized gain will stem from gasoline sales specifically reflecting higher prices. Consumer goods prices jumped 2% in March from a month earlier. In stripping out the price effects, sales were weaker last month than the headline data will suggest.

We expect continued but slower spending in the wake of the ongoing conflict in Iran as higher tax refunds and after-tax incomes are largely offsetting the initial hit from higher gas prices. The longer this goes on, and the broader inflationary pressure becomes, the more concerned we grow on consumer resilience.

Kevin Warsh Confirmation Hearing • Tuesday

The Senate Banking Committee is scheduled to hold a confirmation hearing for Kevin Warsh on April 21. Warsh's nomination to be the next Chair of the Federal Reserve has been in limbo since President Trump chose Kevin Warsh for the position on January 29. Completing his confirmation hearing is an important step toward eventually becoming Fed Chair, but a major hurdle still looms, with Senator Thom Tillis (R-NC) still promising to block Warsh's nomination until the criminal probe by the Department of Justice into the Fed is lifted. Powell's term as Chair ends in May, but if Warsh is not confirmed by then, Powell will continue to serve as Chair pro tempore until his replacement has been confirmed.

Warsh's confirmation hearing will be a helpful update on his views on the monetary policy outlook and the Federal Reserve more generally. Warsh's last public comments on monetary policy came way back in November in a Wall Street Journal opinion piece. We are particularly interested in Warsh's near-term views on the appropriateness of the current level of the fed funds rate, the longer run neutral rate and Fed policy implementation questions, such as its communication tools and balance sheet.

We suspect Warsh will play it safe and try to be as vague as possible in most of his answers, a strategy designed to avoid alienating Senate support as well as members of the FOMC. But, he will not be able to duck all the questions, and given his lack of recent public comments and the wide range of views across the Committee at present, any tips or clues on core views will be extremely helpful for understanding the outlook.

G10 Week Ahead

Canada CPI • Monday

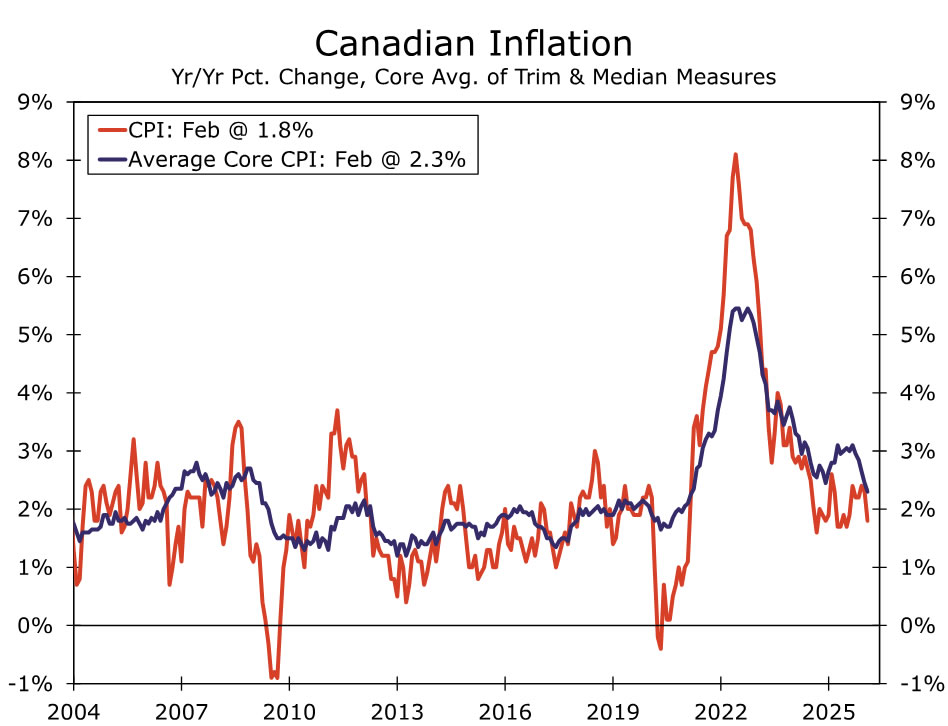

We expect March headline CPI to print 0.9% month-over-month implying 2.4% year-over-year, which would be a significant acceleration from 1.8% in February. The February print was deceptively soft on account of the GST/HST holiday, and the March reading will be the last to carry those effects. At the same time, the energy supply shock as a result of the US-Iran conflict will add substantially to the March reading with additional carryover for April. In fact, our early estimate for April inflation is for the year-over-year print to be close or above 3%. On the core measures, we expect a slower move higher with both the year-over-year median and trimmed CPI at 2.4%. We continue to believe the overall effect of higher energy prices is a small positive for growth and more of an inflationary concern for the Bank of Canada (BoC). As such, the BoC’s calculus has likely shifted from a hold-cut decision to hold-hike in upcoming meetings. A +3% inflation reading is a breach of the upper bound of the BoC’s target range and implies negative real rates in Canada at least through end-2026 if current policy is maintained. An April 29 hold looks certain to us with the BoC likely to lean heavily on optionality given uncertainty in the Middle East and the USMCA renegotiation. With a clean reading on the effect of higher energy prices more likely starting in the April reading, June is the earliest possible timing for a BoC hike. We think that the BoC may opt to delay a hike decision till July, especially with the looming USMCA renegotiation deadline for July 1 and a broader presentation of its outlook in the July Monetary Policy Report.

U.K. Labor Market & CPI • Tuesday & Wednesday

Next week will be busy for U.K. data releases, which market participants will closely scrutinize as they assess the economic impact of the conflict in the Middle East and its implications for Bank of England (BoE) policy.

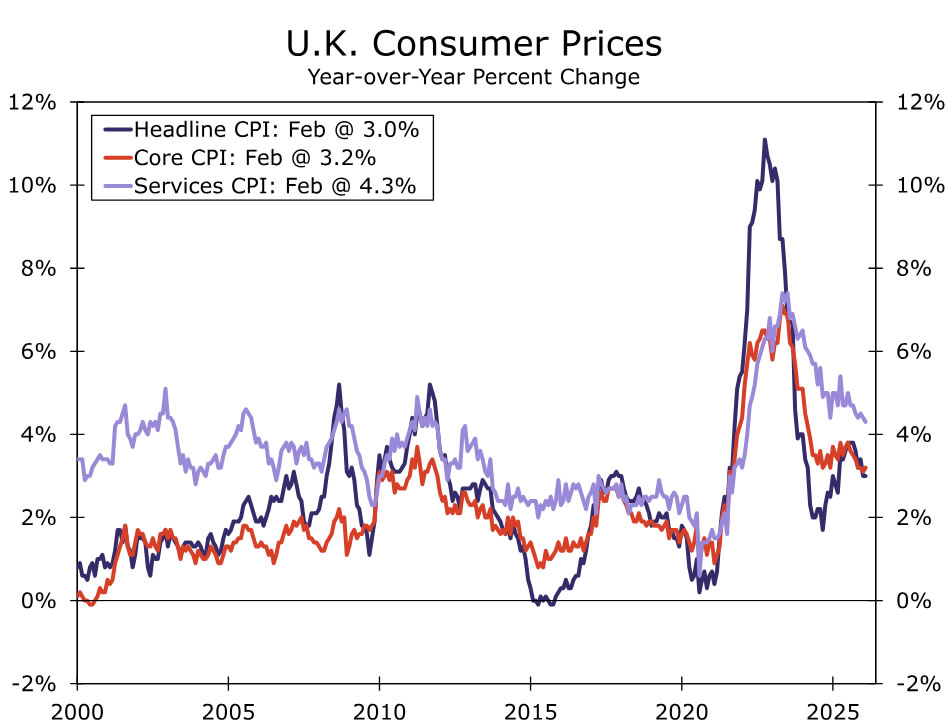

The key release will be the March CPI report. We expect headline inflation to rise to 3.3% year-over-year from 3.0%, driven by the energy supply shock, while core inflation is expected to hold at 3.2%, matching February and in line with consensus expectations. This would mark a significant reversal in the progress toward disinflation seen in the U.K. through February and is likely to persist for several months.

CPI will not be the only release next week. We expect further moderation in wage growth over the three months through February, an unchanged unemployment rate at 5.2% in March and a subdued March retail sales reading, likely reflecting higher fuel prices. Taken together, these data should reinforce the case, in our view, for continued BoE caution and data dependence. While a higher headline inflation print may be viewed as a tightening signal, as long as wage pressures remain contained amid weak growth and elevated unemployment, we expect the BoE to remain on hold at 3.75% this year. Risks are skewed to the upside, particularly if underlying dynamics shift and second-round effects become more prominent.