Sample Category Title

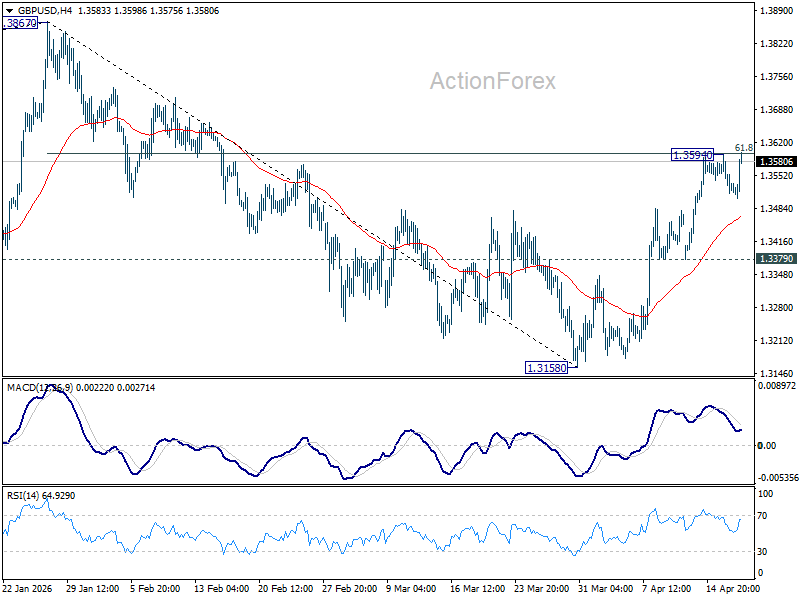

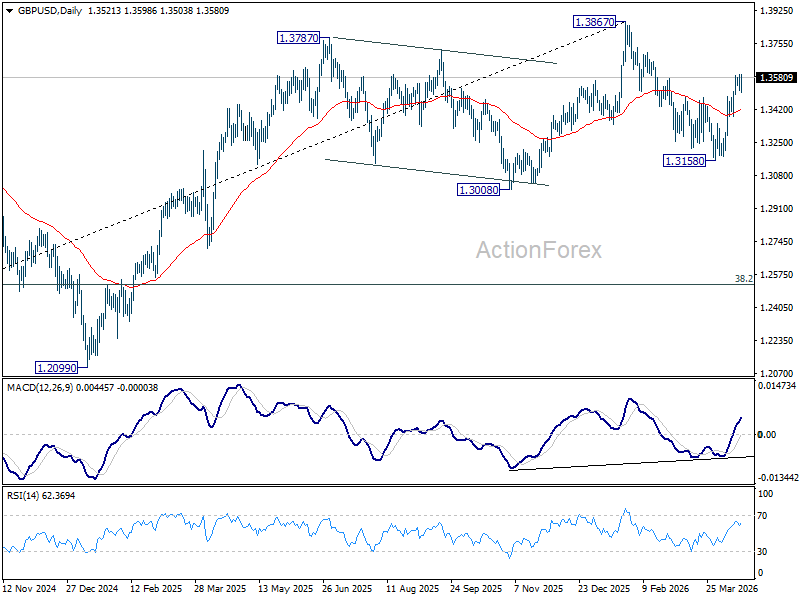

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3498; (P) 1.3547; (R1) 1.3576; More...

Intraday bias in GBP/USD stays neutral first and more consolidations could still be seen below 1.3594. Further rally is expected as long as 1.3379 support holds. On the upside, firm break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will extend the rise from 1.3158 to retest 1.3867 high.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

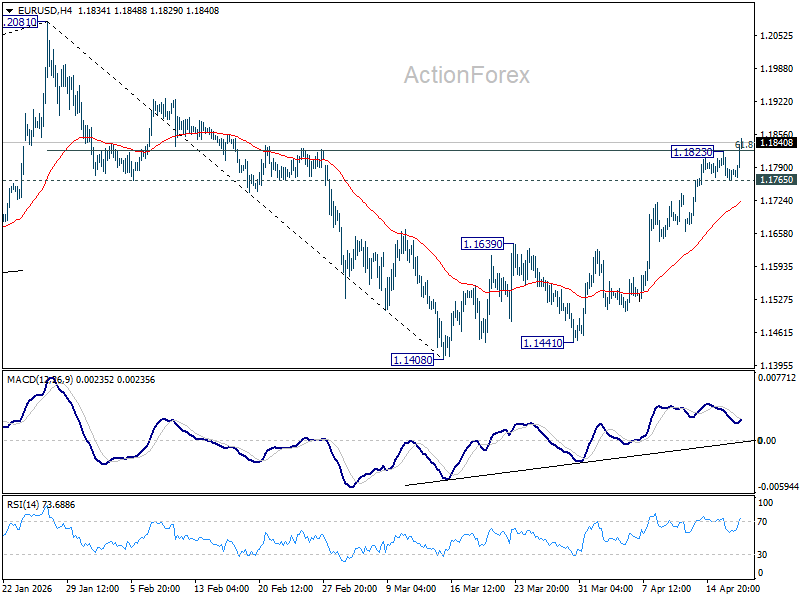

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1758; (P) 1.1792; (R1) 1.1817; More….

EUR/USD's rally resumed after brief consolidations and intraday bias is back on the upside. Sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will extend the rally from 1.1408 to retest 1.2081 high. On the downside, below 1.1765 minor support will turn intraday bias neutral again first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Markets Aggressively Price US-Iran Deal as Hormuz Reopens, Oil and Dollar Fall

Dollar tumbles again in early US session as oil prices dive on fresh geopolitical progress. A sharp selloff has pushed WTI back toward the mid-$80s and Brent into the low-$90s. The move reflects increasingly aggressive positioning ahead of the second round of US-Iran talks, with markets no longer waiting for confirmation but actively pricing a breakthrough.

The trigger was a key development out of Tehran. Iranian Foreign Minister Abbas Araghchi announced that the Strait of Hormuz is “completely open” for commercial shipping "in line with ceasfire in Lebanon. The move removes one of the most critical risk points in global energy supply and is being interpreted as a clear step toward de-escalation.

With key logistical risks easing, traders are leaning more confidently into a de-escalation scenario. The sequence is becoming clearer: open shipping lanes, sustained ceasefire, then formalized negotiations. In that context, the collapse in oil prices is not just a reaction—it is a forward-looking repricing of a normalization outcome.

At the same time, expectations for the talks have become more realistic—and more achievable. Rather than aiming for a full peace deal, both sides are now expected to settle for an interim memorandum or framework agreement. That shift lowers the threshold for success, increasing the likelihood that negotiations deliver a market-friendly outcome.

Meanwhile, Yen is also under broad-based pressure, but for very different reasons. Markets are expressing clear dissatisfaction with the lack of guidance from BoJ Governor Kazuo Ueda. Despite having a high-profile platform following IMF meetings, Ueda refrained from signaling any imminent policy shift this month, instead reiterating a data-dependent stance.

His comments—that inflation could rise with oil but fall if growth slows, and that decisions will be made “meeting by meeting”—were seen as overly open-ended. Markets had expected at least some forward guidance, especially given the BoJ’s past pattern of subtly preparing markets ahead of policy changes. The absence of such signaling is now being interpreted as inertia.

Still, it would be premature to fully rule out policy action. The BoJ has a history of surprising markets, and the current silence does not preclude a rate hike at upcoming meetings. But for now, the lack of direction is weighing on Yen, pushing it alongside Dollar at the bottom of the weekly performance table.

In contrast, pro-cyclical currencies remain firmly in control. Aussie continues to lead gains, supported by both global risk sentiment and domestic strength, followed by Loonie and Kiwi. Euro and Swiss Franc are holding mid-pack, reflecting a more neutral positioning.

In Europe, at the time of writing, FTSE is down -0.05%. DAX is up 0.72%. CAC is up 0.57%. UK 10-year yield is down -0.184 at 4.653. Germany 10-year yield is down -0.068 at 2.965. Earlier in Asia, Nikkei fell -1.75%. Hong Kong HSI fell -0.89%. China Shanghai SSE fell -0.10%. Singapore Strait Times fell -0.20%. Japan 10-year JGB yield rose 0.015 to 2.420.

BoE's Breeden Says Risks Often Underestimated Before Crises

BoE’s Sarah Breeden warns that while the financial system is more resilient, risks from leverage and complexity are re-emerging and could trigger instability. Read more.

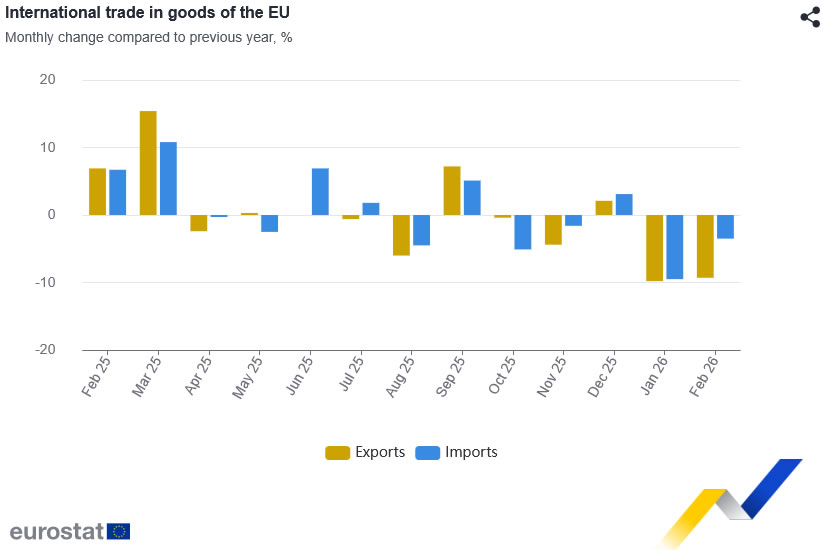

EU Exports to US Drop 26.4% YoY in February, Down 16.1% to China

EU exports dropped sharply in February, with shipments to the US and China falling significantly, signaling weakening global demand. Read more.

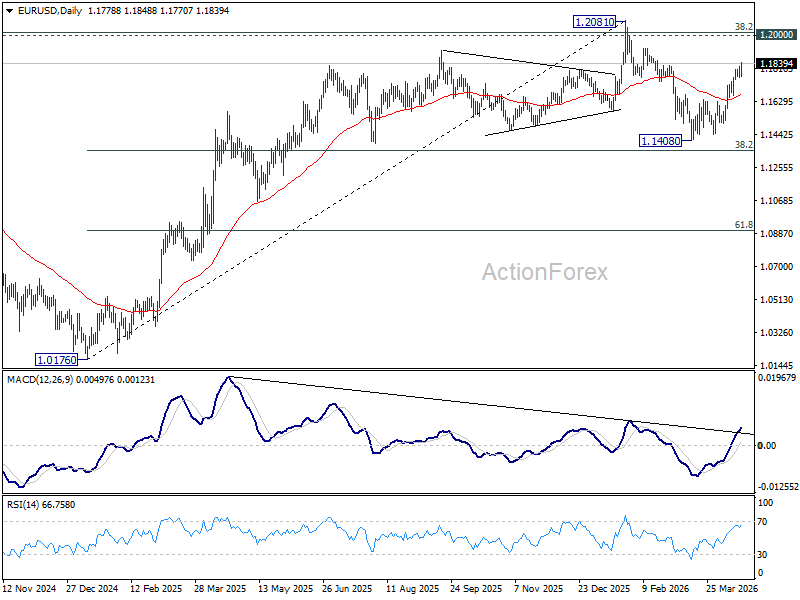

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1758; (P) 1.1792; (R1) 1.1817; More….

EUR/USD's rally resumed after brief consolidations and intraday bias is back on the upside. Sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will extend the rally from 1.1408 to retest 1.2081 high. On the downside, below 1.1765 minor support will turn intraday bias neutral again first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

BoE’s Breeden Says Risks Often Underestimated Before Crises

Sarah Breeden warned that while the global financial system has shown resilience in the face of recent shocks, underlying vulnerabilities remain. She noted that “large, correlated shocks can arrive with little warning,” emphasizing that current stability reflects structural improvements since the global financial crisis, particularly within the banking sector.

However, Breeden cautioned that risks have not disappeared but rather shifted across the financial system. She pointed to “familiar echoes of leverage, complexity, concentration and opacity” emerging in areas such as private markets, government bonds, and stretched asset valuations. If these vulnerabilities were to crystallize simultaneously, she warned, “we may be in for a rocky ride.”

Despite these concerns, Breeden stressed that the system is better equipped to manage stress than in the past. With a more resilient banking sector and enhanced system-wide surveillance, policymakers now have more targeted tools to respond. Still, she underscored a key lesson from history: the most dangerous moments are not when risks are obvious, but "when they are too easily dismissed"—highlighting the importance of vigilance even in periods of apparent stability.

WTI Oil: Growing Optimism Continues to Pressure Oil Prices

WTI Oil price fell on Friday following repeated failures to register close above $90 barrier and pressure the base of near-term congestion, defined by the base of daily Ichimoku cloud, as the price action moves within the cloud (spanned between $87.61 and $91.37) for the third consecutive session.

Growing optimism of a peace solution for Middle East war remains driven mainly by “Trump Indicator” after the US President said that the talks between two sides were very productive and that war is nearing its end, although persistent contradictory of his daily statements points to high volatility and suggests that the situation is still very fragile, requiring caution.

From the technical point of view, near-term structure continues to weaken, as the price action continues to move lower within the bear channel, with strengthening negative momentum and converged daily Tenkan/Kijun-sen about to form bear-cross.

Firm break of daily cloud base and nearby 50% retracement of $54.87/$119.44 ($87.16) is needed to generate fresh bearish signal and expose targets at $84.70/50; $81.78 and $80, in extension), as the WTI is on track for the second consecutive massive weekly loss (two large bearish weekly candles produce significant pressure).

On the other hand, prolonged sideways mode should be expected in case on repeated failure at cloud base, while first positive signal could be expected on lift above daily cloud.

Res: 90.00; 91.80; 92.46; 94.27.

Sup: 87.16; 84.80; 84.50; 80.00.

Chart Alert: The Laggard Dow Jones (DJIA) is in the Process of a Bullish Catch-up Above 47,895 Key Support

Key takeaways

DJIA lagging but poised for catch-up: While other major US indices have posted gains post ceasefire, the Dow has underperformed but is now showing signs of a bullish catch-up above key support at 47,895.

Macro tailwind improving for financials: Stabilisation and potential re-steepening of the US yield curve could boost bank profitability, supporting the Dow given its heavy financial sector weighting.

Bullish technical structure forming: The DJIA is in a minor uptrend within an ascending channel; a break above 48,850 may extend gains toward 49,715/49,835, while failure risks a pullback toward 47,460.

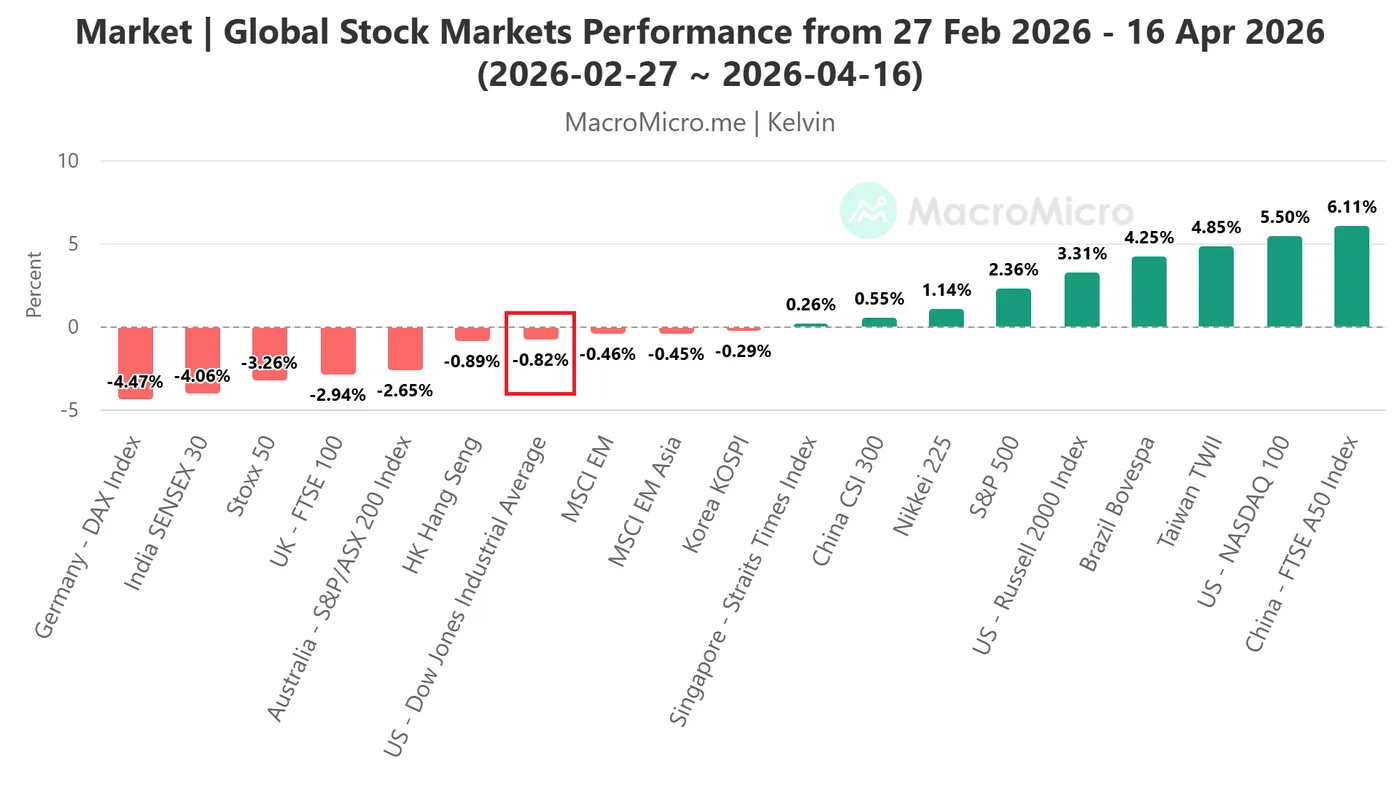

Since the start of the ongoing recovery seen in the risk assets, such as global equities, last Wednesday, 8 February 2026, on the backdrop of the US-Iran ceasefire agreement, which put a pause to the seven-week war, the Dow Jones Industrial Average (DJIA) has lagged behind the other three major US stock indices with a current loss of 0.8% from pre-war baseline on 27 February 2026 to Thursday, 16 April 2026.

In contrast, gains were recorded in the S&P 500 (+2.4%), small caps Russell 2000 (+3.3%), and the top performer, the higher beta technology heavyweight, Nasdaq 100 (+5.5%) (see Fig. 1).

Fig. 1: Global benchmark stock indices performances from 27 Feb 2026 to 16 Apr 2026 (Source: MacroMicro).

The US Treasury yield curve bear flattening has reached a plateau

Fig. 2: US Treasury yield curve (10-YR minus 2-YR) major trend as of 17 Apr 2026 (Source: TradingView).

The Financials sector is the top sector in the DJIA, with a weightage of around 27%, and Goldman Sachs is the top price-weighted component stock in the DJIA with a weight of 11.4% as of Thursday, 17 April 2026.

The underperformance of the Dow Jones Industrial Average has been underpinned by bear flattening of the US Treasury yield curve (10-year minus 2-year), where the yield spread dropped by 11 basis points (bps) to hit an eight-month low of 0.48% on the week of 16 March 2026; such a shift typically signals tighter financial conditions, which can weigh on economic growth and pressure bank profitability.

In the past five trading sessions, stagflation risk arising from a prolonged period of global oil supply crunch has eased, in turn, reducing the odds of a hawkish monetary policy guidance from the US Federal Reserve.

Hence, the 4 weeks of bear flattening movement seen in the US Treasury yield curve have started to plateau as the yield spread has increased by 5 bps to 0.53% at the time of writing (see Fig. 2).

A bull re-steepening in the US Treasury yield curve is likely to improve the earnings prospects of banks, in turn, triggering a positive feedback loop into the Dow Jones Industrial Average.

Let's now decipher the short-term trajectory (1 to 3 days) of the US Wall Street 30 CFD index and its supporting elements from a technical analysis perspective.

Dow Jones (DJIA) – Minor bullish trend from 30 March 2026 low remains intact

Fig. 3: US Wall Street 30 CFD index minor trend as of 17 Apr 2026 (Source: TradingView).

Watch the 47,895 key short-term pivotal support on the US Wall Street 30 CFD index (a proxy of the Dow Jones Industrial Average E-mini futures).

A clearance above the 48,850 near-term resistance increases the odds of the continuation of the bullish impulsive up move sequence for the next intermediate resistances to come in at 49,180/49,250 and 49,715/49,835 (see Fig. 3).

On the other hand, failure to hold at 48,850 with an hourly close below it negates the bullish tone for a minor corrective decline towards the next immediate supports at 47,460 and 46,970/46,710 (the area around the intersection of the 20-day and 200-day moving averages impending bullish crossover).

Key elements to support the near-term bullish bias on Dow Jones (DJIA)

- Price actions started to oscillate within a minor ascending channel from the 30 March 2026 low and traded above all three moving averages (20-day, 50-day, and 200-day).

- The hourly RSI momentum index has managed to stage a rebound after a retest on its ascending support on Thursday, 16 April 2026, at the 43 level.

- Elliot Wave Theory suggests the recent rally from the 2 April 2026 low of 45,882 is likely considered as a minor bullish impulsive wave three structure with its potential terminal zone at 49,715/49,835 (1.00 Fibonacci extension from the 2 April 2026 low and the upper boundary of the minor ascending channel).

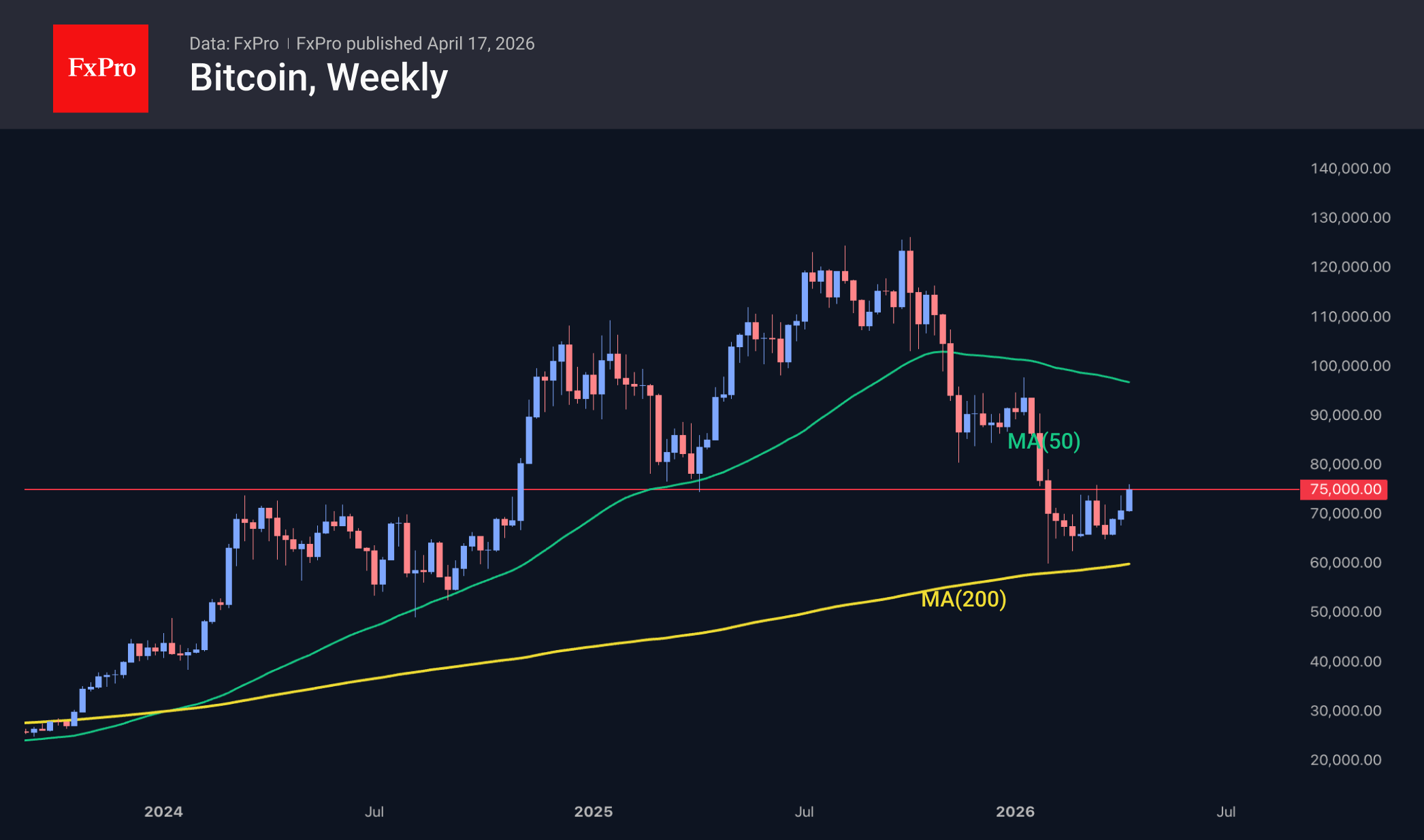

Bitcoin is Gathering Momentum Around $75K

Market Overview

The cryptocurrency market capitalisation stands at $2.55T, up 0.56% over the past 24 hours. The cryptocurrency sentiment index has fallen from 23 to 21, while US stock indices are rallying. The top performers among the most liquid coins are APT (+7.2%), AAVE (+6.4%) and IOTA (+5.2%); the underperformers are NEAR (−1%), ZEC (−2.5%) and DASH (−3.2%).

Bitcoin remains near $75K, showing little change over the last two days. However, this is not a lull but a build-up of momentum, as the leading cryptocurrency is at a key resistance level where the 61.8% retracement of the decline and the March highs converge. In the first half of 2025, this area acted as support, halting the correction, while in 2024 the rally ended at this level. Given this background, the direction chosen could determine the fate of the entire crypto market over the coming months. And here, both sides need thorough preparation.

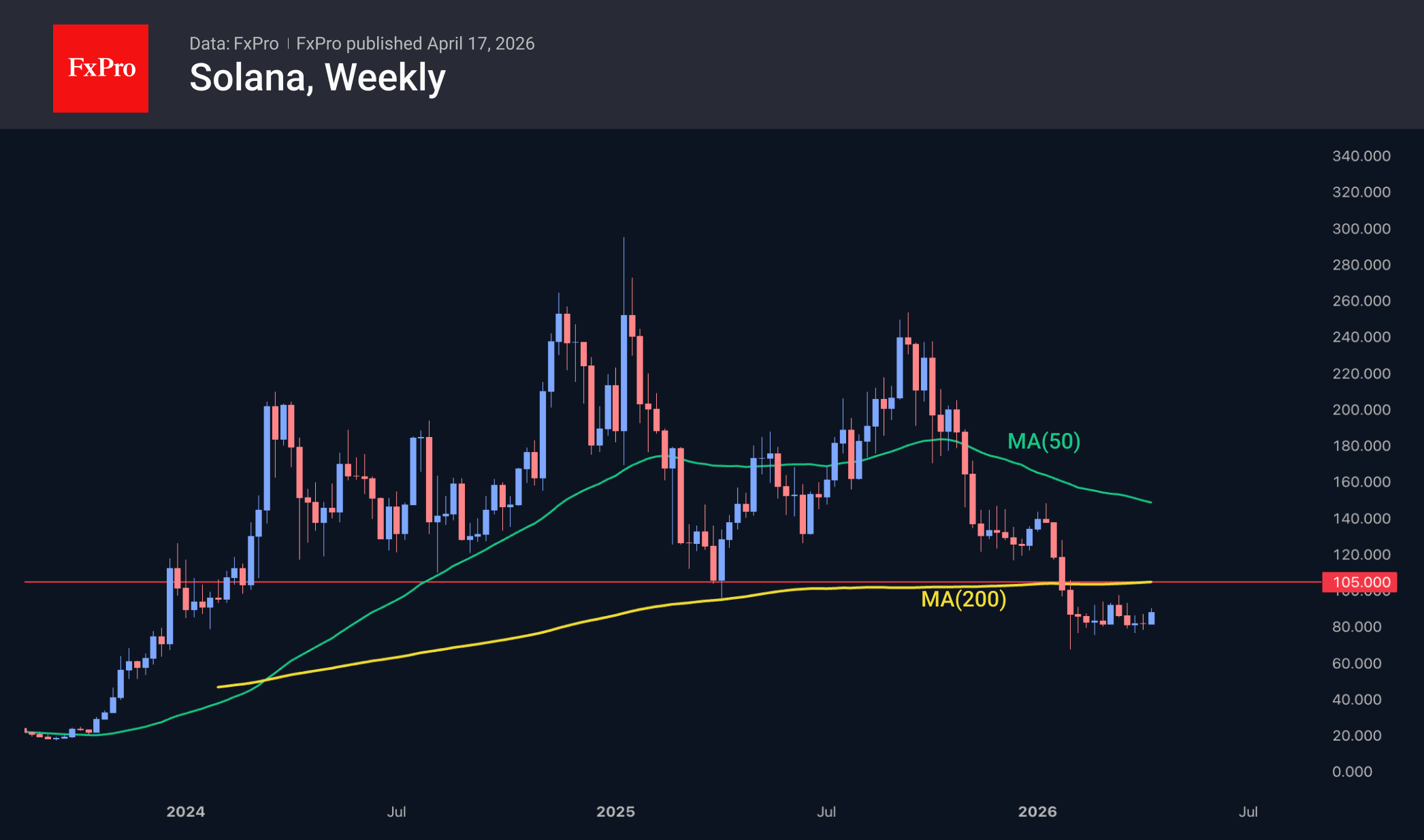

Solana has significantly outperformed the market over the last day, attempting to bounce off an important long-term support line, but failing to do so for over two months now. We will only be able to declare a victory for the bulls once it has consolidated above the $105 level, at which point we can talk about a return above the 200-week moving average, a break above previous local highs and a breach of the round figure.

News Background

The crypto market has entered a ‘no-trade zone’ and is awaiting a signal from the US Federal Reserve, said BitMEX co-founder Arthur Hayes. According to him, the current range-bound movement is due to the lack of clear macroeconomic signals.

Pension funds, insurance companies and large investors no longer view Bitcoin as a speculative instrument. They regard it as a standard component of an investment portfolio — regardless of capital inflows or outflows from crypto ETFs, Sygnum Bank notes.

Over the next few years, Ethereum could exceed $62,000, suggested BitMine CEO Tom Lee. According to him, the recent downturn in the crypto market can be viewed as a ‘mini-crypto winter’, which is nearing its end.

One of the Bitcoin developer groups has presented a new proposal to improve the first cryptocurrency’s network (BIP-361). The proposal involves freezing 1.7 million BTC held in obsolete P2PK addresses that are potentially vulnerable to quantum attacks.

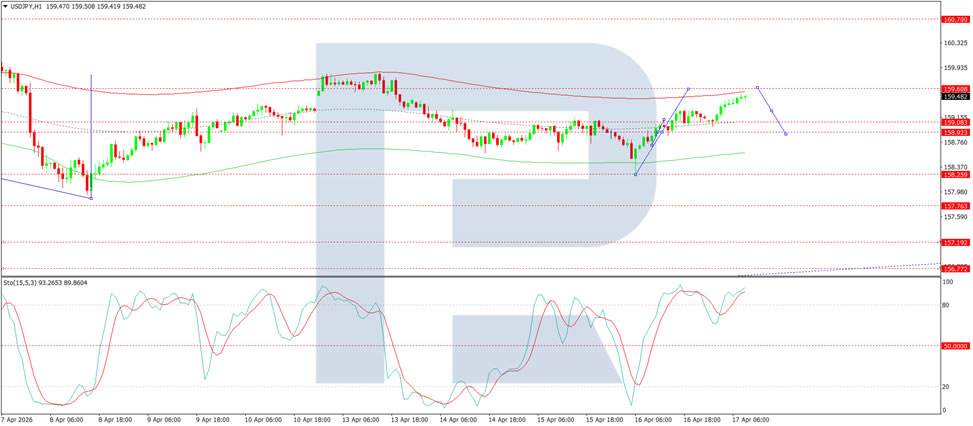

USD/JPY in Positive Territory: Yen Erases All Weekly Gains

USD/JPY rose to 159.40 on Friday, with the Japanese yen surrendering all the gains accumulated since the beginning of this week. Pressure intensified following comments from Bank of Japan Governor Kazuo Ueda, who failed to provide clear guidance on rates ahead of the next meeting.

Ueda noted that the regulator must balance rising inflation against the risks of an economic slowdown. Ahead of previous rate decisions, he had provided more explicit signals, and the market had expected a similar tone.

At the same time, investors acknowledge that the BoJ may raise its inflation forecasts amid rising energy prices.

Earlier in the week, the yen had strengthened following statements from Finance Minister Satsuki Katayama regarding coordination with the US Treasury on foreign exchange policy and a readiness to intervene in the market if necessary.

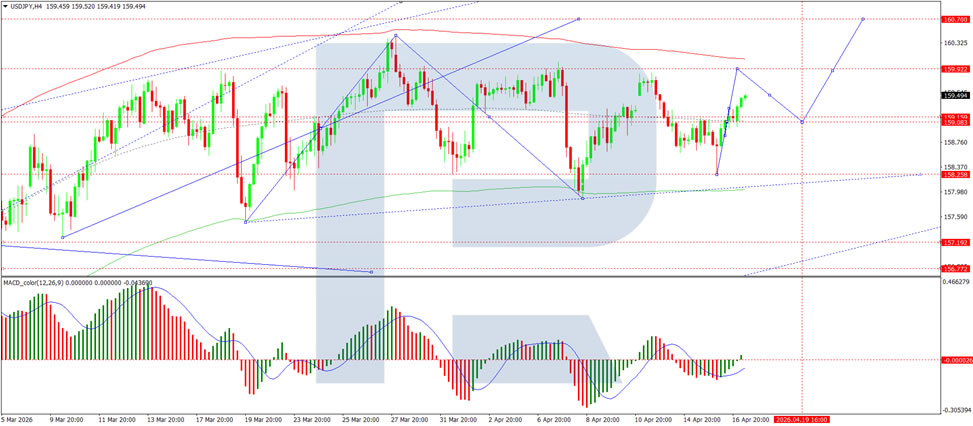

Technical Analysis

On the H4 USD/JPY chart, the market is forming a consolidation range around the 159.00 level, currently extending up to 159.25. A move higher towards 159.90 (testing from below) is likely, followed by a possible decline back to the 159.00 level. Technically, this scenario is confirmed by the MACD indicator, whose signal line is below the zero level and pointing firmly upwards.

On the H1 chart, the market is forming the structure of the next upward wave towards the 159.60 level. A wave extension to 159.90 is possible. Subsequently, a decline to at least 159.00 is likely. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line above the 80 level and pointing firmly upwards.

Conclusion

USD/JPY has returned to positive territory, with the yen erasing all its weekly gains after BOJ Governor Ueda's ambiguous rate guidance. Markets had anticipated clearer signals ahead of the upcoming meeting, but instead received a balanced assessment of competing inflation and growth risks. While the BoJ may yet raise its inflation forecasts due to higher energy prices, the lack of explicit hawkish communication has weighed on the currency. Earlier intervention warnings from the Finance Minister provided only temporary support. Technically, further upside towards 159.90 appears likely before any potential pullback, with the pair's direction hinging on whether Ueda delivers clearer signals at the April meeting.

EU Exports to US Drop 26.4% YoY in February, Down 16.1% to China

Eurozone trade surplus narrowed sharply in February, with the goods balance falling to EUR 11.5B from EUR23.1B a year earlier, as exports declined significantly. Total exports dropped by -6.7% yoy to EUR 232.4B. Imports fell more modestly by -2.2% yoy to EUR 220.9B, pointing to weakening external demand rather than a broad-based slowdown in trade activity.

The deterioration was even more pronounced at the EU level, where the surplus shrank to EUR 9.1B from EUR 22.9B a year earlier. Extra-EU exports declined by -9.3% yoy, outpacing the -3.5% yoy fall in imports.

Breaking down by partners, EU exports to the United States fell sharply by -26.4% yoy, contributing significantly to the overall decline in trade surplus. Exports to China dropped by -16.1% yoy even as imports from China rose by 3.4%, widening the deficit. In contrast, trade with the United Kingdom remained relatively stable.

USD/CAD Extends Pullback to Three‑Week Lows Below 1.3700

- USD/CAD extends almost two-week losing streak, drops below 50‑day SMA.

- Elevated oil prices underpin the loonie, weighing on the pair.

- RSI and stochastics slip into negative territory.

USD/CAD is extending its corrective decline from the year‑to‑date high of 1.3965 reached in late March, sliding for a fifth consecutive session and marking nine down days in the past ten. The move has dragged spot prices to more than three‑week lows near 1.3680, last seen on March 23. Elevated oil prices continue to support the commodity‑linked Canadian dollar, keeping pressure on the pair, although a modest USD recovery could help limit further downside amid ongoing US‑Iran talks.

The pair maintains a bearish near‑term bias after slipping below the 50‑day simple moving average (SMA) closely aligned with the 50% Fibonacci retracement of the January-March upswing at 1.3724. Momentum indicators point to weakening but stabilising downside pressure, with the RSI falling below its neutral threshold, the stochastics dipping into oversold territory, and the MACD remaining marginally positive. This suggests downside momentum is easing rather than reversing decisively.

On the downside, initial support is seen at the 61.8% Fibonacci retracement near 1.3667. Below that, a break beneath the short‑term rising trendline could expose 1.3570 – the range floor of a recent consolidation – and further below the March 9 swing low at 1.3525, where sellers may become more cautious.

On the upside, initial resistance lies at the 50‑day SMA near 1.3724, followed by the 38.2% Fibonacci retracement at 1.3781. A sustained break above this zone could open the way toward a confluence area near 1.3825, where the 20‑ and 200‑day SMAs align, ahead of the 23.6% Fibonacci level at 1.3850.

Overall, USDCAD is extending a sharp pullback from three‑month highs to three‑week lows, having slipped below all three key plotted SMAs. However, if the rising trendline manages to halt the decline, potential for a near‑term rebound may emerge.