Sample Category Title

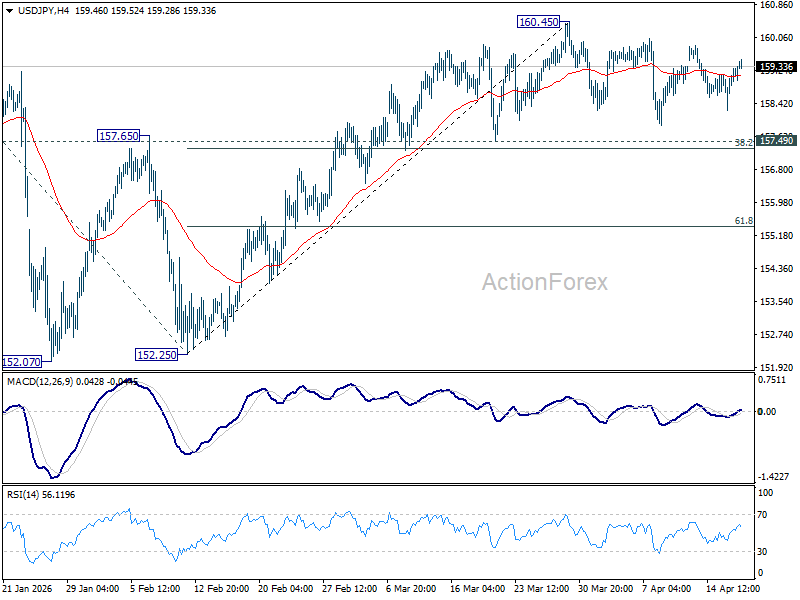

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.48; (P) 158.90; (R1) 159.56; More...

USD/JPY is still bounded in sideway trading and intraday bias remains neutral at this point. Outlook will stay bullish as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

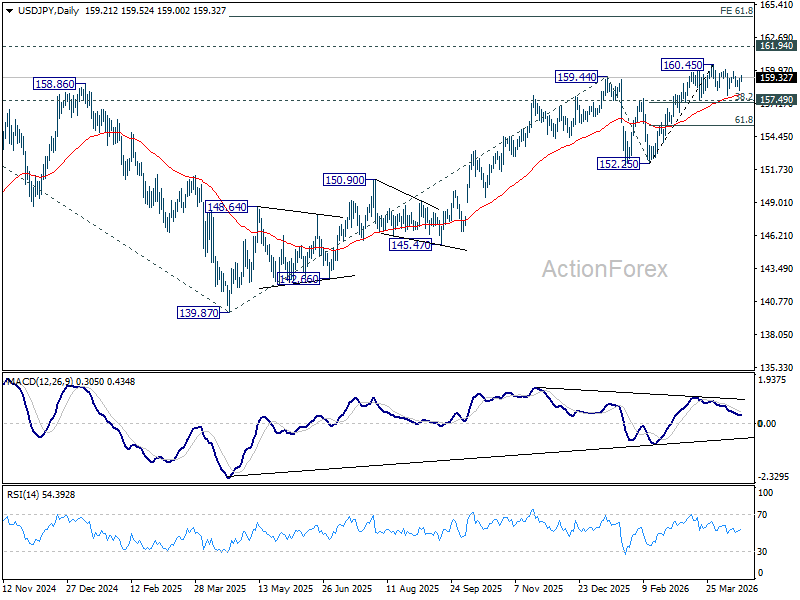

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 155.24) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

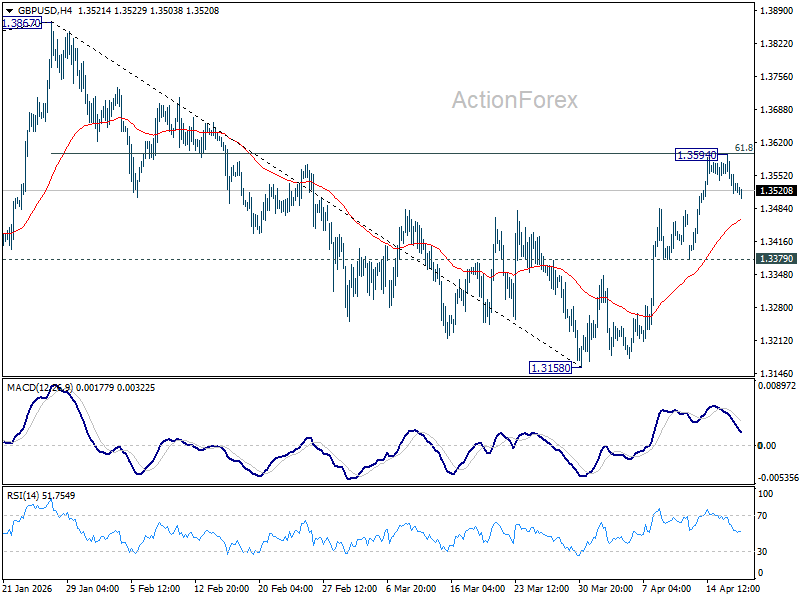

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3498; (P) 1.3547; (R1) 1.3576; More...

Intraday bias in GBP/USD remains neutral for consolidations below 1.3594 temporary top. Further rally is expected as long as 1.3379 support holds. On the upside, firm break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will extend the rise from 1.3158 to retest 1.3867 high.

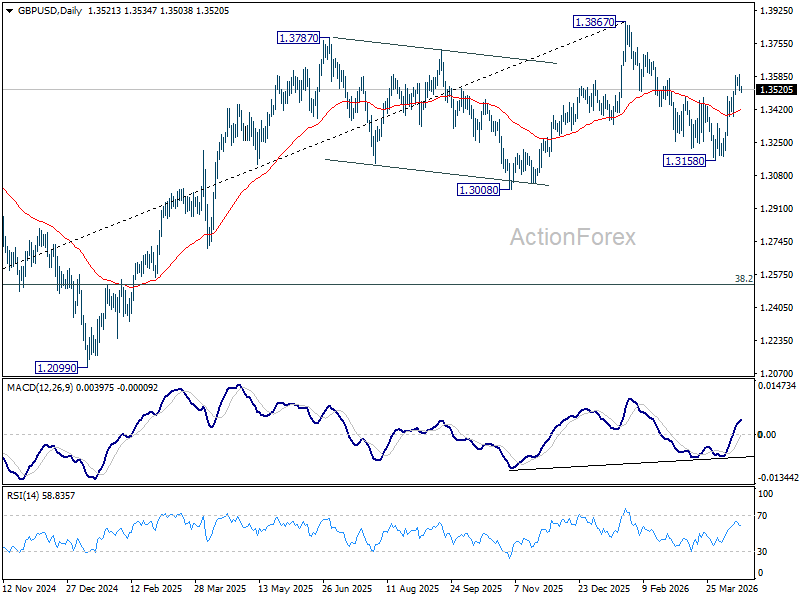

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

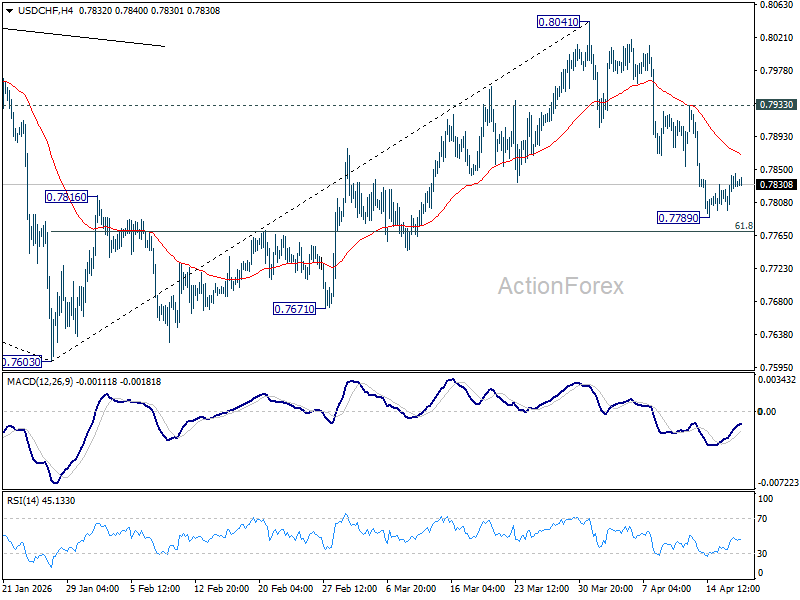

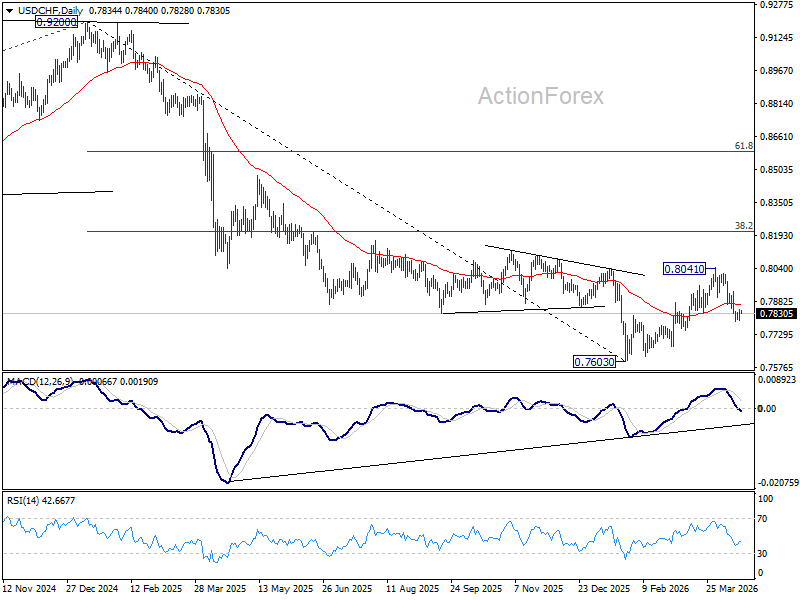

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7808; (P) 0.7827; (R1) 0.7857; More….

Intraday bias in USD/CHF remains neutral and more consolidations would be seen above 0.7789 temporary low. Further decline is expected as long as 0.7933 resistance holds. Below 0.7789 will resume the fall from 0.8041 to 61.8% retracement of 0.7603 to 0.8041 at 0.7770. Decisive break there will target a retest on 0.7603 low.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8071) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

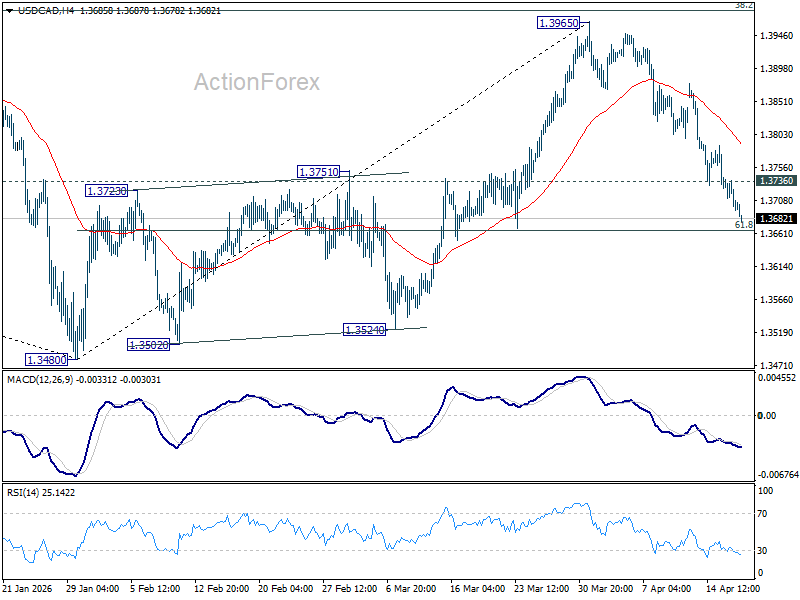

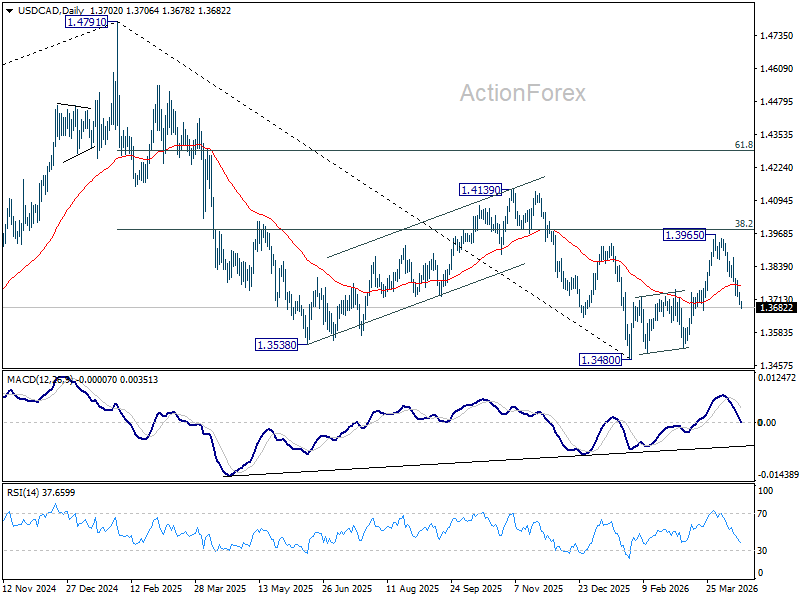

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3685; (P) 1.3715; (R1) 1.3733; More...

USD/CAD's fall from 1.3965 continues today and intraday bias stays on the downside for 61.8% retracement of 1.3480 to 1.3965 at 1.3665. Decisive break there will extend the decline from 1.3965 to retest 1.3480 low. On the upside, above 1.3736 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

Positioning Becomes Overly Bullish with Risks of Disappointment

Markets

Brent crude prices started creeping back up yesterday as the clock ticks down to next week’s Tuesday end to the current cease-fire between the US and Iran. Both parties dig their heels in the sand with back-channel diplomacy hoping for another twee week truce extension. In the meantime, the US keeps stepping up its economic warfare in Hormuz (naval blockade and not extending waivers on purchases of Iranian & Russian oil) aiming to make Iran almost unconditionally surrender to US demands. Bloomberg reported that people close to EU and Arab leaders feared that reaching a deal might take about six months. Immediately opening the Strait of Hormuz is key to restore energy flows and stop the developing global food crisis. The International Energy Agency also warned that Europe has maybe six weeks of jet fuel left. If supplies remain blocked, flight cancellations will be coming. IEA chief Birol added that we must start preparing for significantly higher energy prices if Hormuz is not reopened. More emergency oil reserve releases are under consideration. He also thinks that it will take approximately two years to reach pre-war production levels again. Brent crude moved from $94.5/b to almost $100 yesterday. They retreated to close near $98. US President Trump announced a 10-day cease-fire deal between Israel en Lebanon, but the value is low given that Hezbollah wasn’t involved. He keeps trying to talk up the market, saying that the war in Iran should be ending pretty soon. On Wednesday he suggested that the next two days were going to be amazing. Yesterday he changed that to “let’s see what happens over the next week or so” but still “going to see some incredible results”. At the moment it remains unclear whether US and Iranian delegations will meet again over the weekend. Given the empty eco calendar, the headline roulette will keep spinning and determine market action. From a risk point of view, we believe that positioning became overly bullish with risks of disappointment if the current stalemate drags on. Especially if Brent crude tips back above the $100 risk on/risk off switch. Approaching that barrier yesterday resulted in some fatigue on stock markets (ending between small losses and small gains) and FX market (1.18 barrier holding).

News & Views

The incoming Tisza administration in Hungary has articulated an economic program centered on the restoration of the rule of law and the modernization of the domestic business environment, in-house KBC analysis finds. A central pillar of this strategy is the immediate unblocking of approximately €18bn in frozen EU funds, roughly 10% of annual GDP. Tisza intends to achieve this by joining the European Public Prosecutor's Office and conducting a rigorous audit of previous public procurement practices to reclaim siphoned state funds. Fiscal policy represents a shift toward progressivity and the support of SMEs. Proposed measures include lowering the personal income tax rate on minimum wage earners from 15% to 9%, while simultaneously introducing a 1% asset tax on individuals with net wealth exceeding HUF 1 bln. This redistributive approach is designed to increase household disposable income and domestic demand, which has been stagnant or contracting in recent years. Beyond these measures, Tisza's manifesto outlined ambitions to adopt the euro by 2030, reduce the budget deficit to below 3% of GDP and transition away from Russian energy dependence by 2035. However, to achieve this, some degree of fiscal consolidation would be necessary, which could act as a drag on domestic demand in the short term. The proposed tax cuts might be difficult to implement given the challenging state of public finances, with the fiscal deficit at approximately 4.8–5% of GDP. The country's heavy reliance on energy imports — four-fifths of its oil and two-thirds of its gas — adds further complexity, as dismantling Orbán-era price controls and energy subsidies risks weakening growth, while maintaining them would strain the budget.

The Financial Times, citing people familiar with the matter, reported that Germany will slash its 2026 growth forecast to 0.5% from 1%. The meagre expansion would mean a fourth consecutive year of near-stagnation in the euro area’s largest economy, dashing hopes of a public spending lead recovery. The government’s stimulus package is indeed the main impulse to this year’s limited growth, a government source told FT, with exports, domestic consumption and private investments all stagnating. The growth downgrade is the result of the Iran war, which lead to an energy price spike weighing on the country’s vast chemical and pharma industry. It comes on top of structural issues including a shrinking workforce, limited productivity growth and excessive regulation.

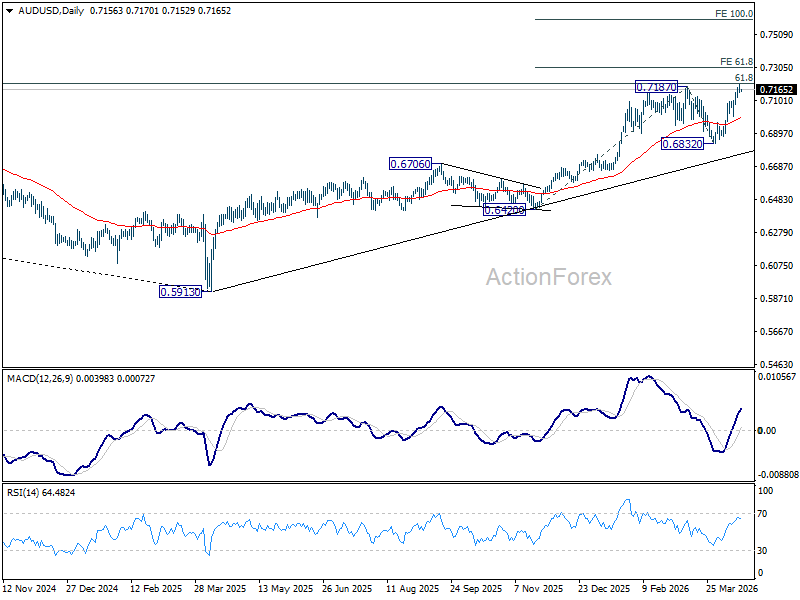

AUD/USD Daily Report

Daily Pivots: (S1) 0.7144; (P) 0.7171; (R1) 0.7190; More...

Intraday bias in AUD/USD is turned neutral with current retreat and some consolidations would be seen below 0.7197 temporary top first. Further rally is expected as long as 0.7000 support holds. Above 0.7917 will resume larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. Decisive break there could prompt upside acceleration to 100% projection at 0.7599.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

Markets Shift from Chasing to Waiting Ahead of Key US-Iran Talks Weekend

The market narrative is shifting from chasing the risk rally to waiting for confirmation. After a sustained push higher driven by optimism around US-Iran negotiations, investors are becoming more cautious ahead of a critical weekend. The rally remains intact, but the willingness to extend positions without new information is fading.

US equities pushed to fresh record highs overnight, with the S&P 500 and NASDAQ extending gains overnight. But the lack of follow-through elsewhere suggests that conviction is fading temporarily. This hesitation is most visible in Asia. Japan’s Nikkei has pulled back from its own record highs, trimming gains as traders lock in profits ahead of the weekend. Oil markets are sending a similar signal. Prices are holding in a tight range just below the $100 mark.

That caution is justified given evolving expectations for the US-Iran negotiations. Reports indicate that both the US and Iran are scaling back ambitions from a comprehensive agreement toward a more achievable interim framework. The focus is shifting toward a temporary memorandum that would prevent renewed conflict rather than deliver a full resolution. Back-channel diplomacy appears to be playing a key role. Lower-level discussions have reportedly made progress in narrowing differences, raising the possibility of an agreement in principle. However, significant technical details are likely to be deferred.

US President Donald Trump has maintained an upbeat tone, saying the US is “very close to making a deal with Iran” and even hinting he could travel to Islamabad for a signing. Such rhetoric is supporting underlying optimism, but markets are turning cautious about taking it at face value without concrete outcomes.

At the same time, geopolitical efforts are expanding beyond the core US-Iran channel. The UK and France are set to chair a meeting of around 40 countries to coordinate efforts to keep the Strait of Hormuz open once hostilities ease. The proposed mission could involve intelligence sharing, mine-clearing operations, and military escorts to secure shipping lanes. Even if tensions ease, the need for a transitional security framework suggests that normalization will not be immediate.

In the currency markets, Yen has overtaken Dollar's place as the worst performer of the week so far, while Sterling is the third. Aussie continues to lead at the top, followed by Loonie, and then Kiwi. Euro and Swiss Franc are positioning in the middle.

In Asia, Nikkei fell -1.13%. Hong Kong HSI is down -1.15%. China Shanghai SSE is down -0.06%. Singapore Strait Times is down -0.27%. Japan 10-year JGB yield rose 0.015 to 2.421. Overnight, DOW rose 0.24%. S&P 500 rose 0.26%. NASDAQ rose 0.36%. 10-year yield rose 0.027 to 4.309.

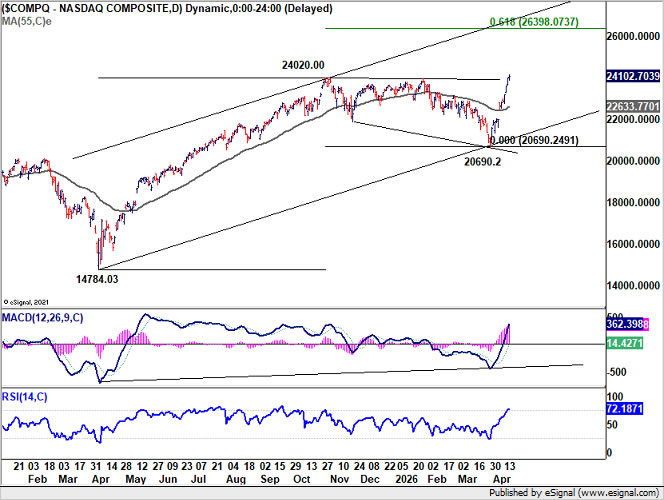

NASDAQ Hits Record High as AI Trade Revives, Eyes 26k+ if Oil Normalizes to $80

NASDAQ has surged to record highs as the AI trade revives The next move toward 26k depends on whether oil prices fall back toward $80 and ease inflation pressure. Read more.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7144; (P) 0.7171; (R1) 0.7190; More...

Intraday bias in AUD/USD is turned neutral with current retreat and some consolidations would be seen below 0.7197 temporary top first. Further rally is expected as long as 0.7000 support holds. Above 0.7917 will resume larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. Decisive break there could prompt upside acceleration to 100% projection at 0.7599.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

ECB Expected to Hold Rates in April

In focus today and over the weekend

The potential for talks between the US and Iran over the weekend to reach an agreement will be in focus, as a ceasefire between Israel and Lebanon was reached yesterday. We expect the two sides will agree on an extension to the temporary ceasefire, while a more permanent peace deal will take more time.

Early Monday morning, China will announce the 1-year and 5-year Loan Prime Rates (LPR). While we expect monetary easing in the coming months, we look for the LPRs to be unchanged this time. The LPRs normally change only following changes in the 7-day reverse repo rate, which has not been adjusted since May last year.

Economic and market news

What happened yesterday

In the euro area, the final HICP inflation data was slightly higher than the flash release with headline at 2.6% y/y compared to 2.5% y/y in the flash, mainly due to rounding. Core inflation confirmed the flash release of 2.3% y/y. The rise in inflation was due to higher energy-related expenses. Hence, the data does not change the picture compared to the flash release and in isolation supports a hold in April, although the future inflation prints will be much more important for the ECB than the March one.

Furthermore, an ECB sources story revealed that the Governing Council is leaning towards keeping interest rates unchanged in April as it is too early to give a verdict on the consequences of the Iran war. Schnabel also stated that the ECB can afford to take time to analyse the shock and that they do not want to impose unnecessary costs on the economy. This has decreased the likelihood of an April hike with markets pricing in 5bp worth of hikes. We have adjusted our ECB call and now expect hikes in June and July.

In the Middle East, US President Trump stated last night that Israel and Lebanon had agreed on a 10-day ceasefire taking effect at 23:00 CET yesterday. Israel's Prime Minister Netanyahu confirmed the ceasefire. However, he also said the truce would not include troop withdrawal from Lebanon. Hezbollah, not being part of the talks, responded that the presence of Israeli forces on Lebanese territory gave Lebanon and its people the "right to resist". This morning, Hezbollah claims that Israel broke the ceasefire overnight, by opening fire against cities in the south. The fragile ceasefire between Israel and Lebanon removes one key obstacle for the US-Iran talks. However, a number of issues remain, not least Iran's nuclear program and the control of the strait of Hormuz. We expect the ceasefire to be extended over the weekend, but as European and Gulf officials warned yesterday, we think a more permanent deal will take months.

In the UK, February GDP growth was much stronger than expected as GDP increased 0.5% m/m in February 2026 (cons: 0.1% m/m) following a disappointing standstill in January. Services are still largely driving the progress, but car production is also back on track. Strong growth in February is well in line with the solid PMIs we saw in January/February, however, March PMIs have indicated stagnation. From what we know this far, prices have not rubbed off on wage growth. We will know more next week when we get a new labour market report. This will be key for the Bank of England outlook, where we expect them to hold interest rates for the foreseeable future.

In the US, industrial production decreased by -0.5% m/m (Feb: +0.2% m/m, cons: +0.1% m/m), which is the largest decline since September 2024, however, it was up +0.7% y/y. Manufacturing production, which makes up approximately 78% of industrial production, declined -0.1% m/m in March (Feb: +0.4% m/m, cons: +0.1% m/m), a negative after showing signs of recovery at the beginning of the year after tariffs hit manufacturing hard in 2025.

In Sweden, the Riksbank's Per Jansson said the food VAT cut is exerting downward pressure on inflation, while higher energy costs are pushing inflation up. He therefore noted that this supply shock can largely be looked through, though vigilance remains warranted. He added that the situation remains different from 2022 as inflation pressure is now lower, demand is weaker and SEK is stronger.

Equities: Equities were higher, driven by tech-heavy US and Asia. S&P 500 rose a meagre 0.2% which was enough for a new all-time high. What was interesting, however, was the rotation underneath. While tech, communication and real estate were all >1% higher, value sectors such as industrials and banks were 0.5% lower. Software continued its recent outperformance, up over 2% and a full 13% week to date. Value indices performed decently yesterday, as the energy sector rose meaningfully. However, the story last week has been growth, not about cyclicals vs defensives per se.

FI and FX: Treasury yields moved higher throughout the US session leaving the UST10y at 4.32% this morning as the oil price climbed a little higher too where Brent crude trades at USD 98 per barrel. Fed's Miran, the dovish outlier within FOMC, trims his forecast from four to three cuts this year. The market is pricing in c. 10bp of cuts. Within FX majors, EUR/USD has flatlined overnight just below 1.18 while USD/JPY hovers around 159. EUR/NOK continues to grind lower toward 11.00, having started the week just shy of 11.20. Meanwhile, EUR/SEK is comfortable around 10.80 for the time being. As a result, NOK/SEK is back above 0.98. EUR/DKK is stuck close to the 7.4732 level.

Later this morning we will published our monthly FX Forecast Update this time titled "USD erases war-fuelled gains as downtrend resumes", 17 April. Over the past month, EUR/USD has retraced its war-linked move lower, now trading around the 1.18 mark. In short, we have revised our 1M and 3M EUR/USD forecasts to 1.18 and thus look for the cross to stay around current level in the short-term. In the longer term, we expect a higher EUR/USD, driven by three key factors: a drop in carry as ECB hikes and Fed cuts are expected this year, normalisation in oil prices, and relatively higher US inflation. For EUR/SEK, we leave our forecast profile unchanged, forecasting EUR/SEK at 11.00 in 6-12M. For EUR/NOK, we remain skeptical with respect to the longevity of the rally and thus leave our forecast profile unchanged this month keeping an upward slope in 6M and 12M. For the rest of our forecasts please see the full piece.

NASDAQ Hits Record High as AI Trade Revives, Eyes 26k+ if Oil Normalizes to $80

NASDAQ is rallying on more than just optimism—it’s being powered by fundamentals. The index surged to a fresh record high this week as markets increasingly price in a resolution to Middle East tensions that would bring oil price back to pre-war levels, while at the same time embracing a renewed wave of confidence in the AI trade. This is not just a risk rally—it’s a structural shift back into tech leadership.

At the heart of the move is a decisive turn in AI sentiment. Strong earnings from TSMC and ASML delivered what markets had been waiting for: proof that the AI cycle remains intact. While both stocks saw “sell-the-news” reactions, the broader message was clear—AI demand is real and durable. More importantly, leadership has broadened beyond the traditional “picks and shovels” into the “miners,” with Nvidia, Microsoft, Meta, and Alphabet driving gains as AI monetization begins to show up in earnings.

This expansion in leadership is a key bullish signal. The fact that NASDAQ is hitting new highs even as TSMC and ASML consolidate suggests the rally is no longer narrow. The AI trade has evolved from infrastructure buildout to revenue generation, and markets are now pricing that transition aggressively. What was doubted earlier this year is now being confirmed—and repriced.

Macro dynamics are reinforcing this shift. Optimism around a potential US-Iran deal is driving expectations that oil prices will normalize back below $80 at a later stage. That assumption is critical, as it underpins the view that the current energy-driven inflation spike will prove temporary rather than structural.

In a counterintuitive twist, the geopolitical shock has actually strengthened the dovish Fed narrative. Higher energy prices and supply disruptions have weighed on consumer activity and labor momentum. If oil does normalize, the Fed would have clearer scope to resume its rate-cut cycle later this year.

Taken together, markets are pricing both the end of the oil shock and the return of AI dominance. This dual tailwind—macro relief and micro confirmation—is what sets the current rally apart from earlier moves that relied more heavily on sentiment alone.

Technically, while some volatility could be seen, near term outlook will stay bullish in NASDAQ as long as 55 D EMA (now at 22,633) holds. Next medium term target is 61.8% projection of 14,784 to 24,020 from 20,690 at 26,398.

Reading the Markets EUR: From Spring Hikes to Summer Hikes; Receive 2Y1Y ESTR Swap

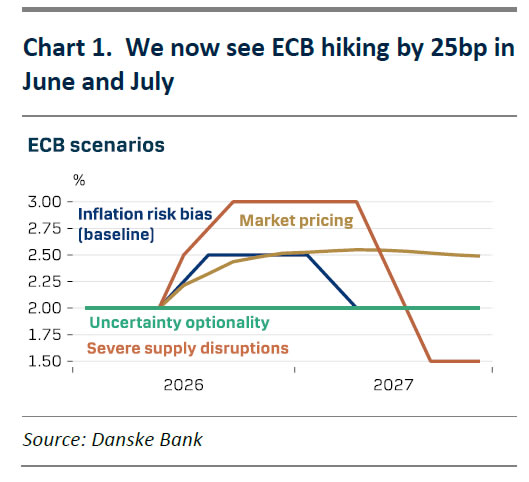

We tweak our ECB call and now expect the ECB to remain on hold at the April meeting before increasing policy rates by 25bp in each of June and July, bringing the deposit rate to 2.50% in July. Our previous call included two 25bp rate hikes in April and June. There are two main reasons for the change: 1) the ECB’s communication has shifted to a less hawkish stance; and 2) the two-week ceasefire has caused commodity prices to decline significantly over the past week.

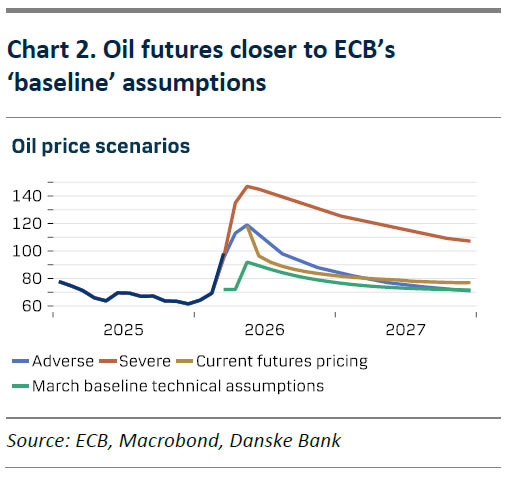

Regarding the ECB’s communication, a sources story released overnight revealed that the GC is leaning towards keeping policy rates unchanged in April as it is too early to give a verdict on the consequences of the war in Iran. The highly influential GC member Schnabel at the same time stated that ECB can afford to take time to analyse the shock and that they do not want to impose unnecessary costs on the economy. The minutes from the March ECB meeting were on the dovish side and resembled Lagarde’s calm ‘wait and see’ stance at the press conference in March. Hence, we expect the ECB is likely to use the uncertainty optionality of the situation to hold rates unchanged at the April meeting. Regarding commodity prices, the two-week ceasefire in Iran and reports of continued talks between the US and Iran have caused a drop in the spot brent oil price to around 97 USD/bbl from 110 USD/bbl last week. The futures curves remain in steep backwardation and are now closer to the ECB’s baseline staff projections’ technical assumptions (see Chart 2), while the April and May contracts were above.

We expect two 25bp hikes, in June and July, bringing the deposit rate to 2.50%

We continue to expect the ECB to hike policy rates by a total of 50bp this year due to the still relatively hawkish sentiment in the GC, but we now see the first hike in June and not April. Lagarde has stated that the ECB runs a communication risk of not hiking to higher prices, so they remain “agile”. Furthermore, we anticipate rate increases to ensure inflation expectations remain anchored. Several GC members have emphasised that inflation expectations may be more responsive to energy price rises, given that the 2022 episode remains fresh in memory. Whilst we believe the 2022 episode cannot be compared with the current situation, the GC appears to have a lower threshold for rate increases. Additionally, European governments have already begun stimulating demand, with 20 out of 27 EU member states having introduced tax cuts or price subsidies on oil products. Although the total fiscal allocation to these measures remains modest relative to the size of the eurozone economy, they demonstrate a clear bias towards non-targeted measures, which makes ECB rate hikes more probable. Given that monetary policy affects the economy with significant lags, we expect the ECB to deliver rate increases relatively quickly, in June and July, rather than later in the year.

We view the risks to our new call as tilted to the downside. We believe that the longer the ECB delays rate hikes, the more the probability of future hikes declines, as negative growth effects become more apparent and the ECB treats the shock as a "one-off". The likelihood of the ECB looking through the energy shock entirely has therefore increased. The past month has demonstrated how quickly sentiment can shift within the GC, from being calm at the March meeting (as minutes reveal), extremely hawkish in the days after the March meeting (e.g. Nagel saying on 20 March the ECB would need an April hike if the price outlook soured), and now less hawkish again (as the sources story overnight showed). This relative shift could occur again before June, leading to no rate increases at that time, in contrast to our baseline of two hikes.

However, much of the outlook also depends on the war in the Middle East. There remains a clear risk that the ceasefire turns out to be only temporary and that energy prices will rise again as the two sides disagree on key matters, see Geopolitical Radar: Pause, Not Peace, 10 April. Furthermore, the risk of supply shortages on key refined oil products such as jet fuel is also increasing, as shipments through the Strait of Hormuz remain low. The IEA has stated that Europe has 'maybe' six weeks of jet fuel remaining, which could raise airfares and thus core services inflation. With the ECB staff projections' 'adverse' and 'baseline' scenarios including approximately 35bp worth of hikes, we believe they provide the ECB with comfort in raising policy rates in June and July. Given that economic activity in the eurozone is negatively affected by the supply shock and expected rate hikes, we still anticipate the ECB lowering policy rates by 25bp in each of March and April 2027, bringing the DFR back to 2.00%.

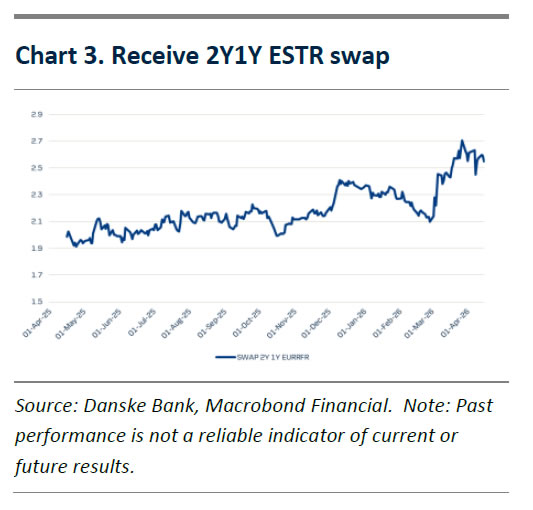

Rates Strategy: New trade – receive 2Y1Y ESTR swap

In last week’s Reading the Markets EUR (RtM EUR, 9 April), we highlighted that if the two-week ceasefire was the first step towards a lasting resolution and we saw a further drop in oil price, we would position for a move lower in short-term interest rates and would fade the April meeting pricing. Since then, it has become increasingly evident that both the US and Iranians are looking for an off-ramp in the Middle East, and that the ECB is taking a more cautious stance. As highlighted above, we have therefore pushed our call for hikes to June and July (previously April and June).

Given recent developments, we see value in receiving the 2Y1Y ESTR swap. On one hand, given the ECB’s more cautious stance, we see a possibility that the wait-and-see approach would gain traction within the GC as time passes and would increasingly favour that the ECB could see through the pick-up in headline inflation and remain on hold. Conversely, a war in the Middle East constituting a negative supply shock with elevated energy prices puts downward pressure on growth prospects. We think the narrative of worsening growth prospects due to high energy prices, which would only be further exacerbated by the outlook for monetary tightening, will gain traction in the coming months, and favour receiving the front-end of the curve. The 2Y1Y point offers a 6M roll-down of around 5bp.

Risks to the trade are more pronounced fiscal easing triggering a more forceful response from the ECB, and developments in the Middle East.

New trade: We recommend receiving the 2Y1Y ESTR swap @ 2.55% with a soft target of 2.35% and a stop-loss at 2.75%.