Sample Category Title

Cliff Notes: Conflict in the Middle East to Cast a Long Shadow

Key insights from the week that was.

The first detailed look at the mindset of Australian consumers and businesses amidst the Middle East conflict proved sobering. Our Westpac-MI Consumer Sentiment Index posted its largest fall since COVID-19, down 12.5% to a deeply pessimistic reading of 80.1. The impact from the surge in fuel prices was acute, leading to a more pronounced deterioration in the sub-indexes tracking current conditions – namely ‘family finances vs a year ago’ (–16.7%) and ‘time to buy a major household item’ (–15.0%). There were also significant hits to the year-ahead outlook for family finances (–13.9%) and the economy (–12.4%), suggesting households are bracing for enduring pressure.

The tone of the March NAB business survey was no better, business confidence collapsing 29pts from a neutral reading in February. This came alongside a notable lift in purchase cost pressures, up 1.7ppts to a quarterly pace of 3.0%. That final producer prices lifted +0.4ppts emphasises the rapid pass-through of surging fuel costs, but also that businesses are currently absorbing most of the increase in costs via margins, impacting profitability. Note though, the readings for current trading conditions and employment were positive, enabling business conditions to hold around its long-run average. This suggests the underlying health of the economy can be maintained if risks subside quickly.

This week we also received the March Labour Force Survey. It showed the Australian labour market was in good health prior to the Middle East conflict and the RBA’s most recent rate hike. Employment growth continued to strengthen from its trough in March, from 1.0%yr to 1.5%yr on a three-month average basis, reflecting the economy’s momentum through the second half of 2025 and into 2026. The unemployment rate has also held at 4.3% over the past two months, a similar level to the second half of last year. It now looks increasingly like the 4.1% prints at the turn of the year were due to temporary weakness in participation, not a sustained re-tightening.

However, given the hit to business confidence and the expectation of further policy tightening, the Middle East conflict looks set to cast a long shadow over the labour market. We expect a combination of lower average hours worked and slower employment growth, seeing the unemployment rate lift to 5.0% in early 2027. Tracking industries most exposed to the fuel shock will provide an initial take on the scale of the impact. Manufacturing, construction, transport/logistics and travel/tourism are the sectors to watch.

Offshore, an abrupt end to the first round of in-person talks between the US and Iran and the US’ Navy’s subsequent blockade of Iranian ports and associated vessels was the main point of conversation for markets this week. The market’s take has been sanguine, the price of Brent oil retreating below US$100 and global equities rallying back to historic highs during the week. Comments made by both sides imply negotiations are ongoing and another round of in-person talks will occur before the two-week ceasefire ends in coming days. There is also the option to extend the ceasefire, if necessary.

Effectively cut off from global shipping, Iran’s need for a deal is clear. But arguably this is also the case for the US economy, University of Michigan consumer sentiment falling to a record low this week, 43% below the average of the survey since 1978. Price pressures are currently limited to first-order effects, headline CPI inflation printing at 0.9% against a core reading of just 0.2% in March; but, should the conflict persist, it is highly likely second-round effects will permeate through the US economy, materially increasing the likelihood of inflation holding well above target and term interest rates trending higher. FOMC members who spoke this week all showed confidence in the underlying health of the US economy but also concern over the potential for an lasting imbalance between growth and inflation.

In contrast, China’s economy showed strength this week, annual GDP growth accelerated from 4.5%yr in Q4 2025 to 5.0%yr in Q1, matching the full-year outcome for 2025. From the monthly partial data, China’s Q1 momentum was principally due to the strength of exporters and associated investment, both of which are likely to receive a lasting boost from increased demand for green technology given the Middle East’s impact on energy prices and supply. There is reason for guarded optimism over the outlook for property investment as well, the year-to-date decline having moderated from -17%ytd at December to -11%ytd in February and March. Still equivalent to circa 15% of GDP, an end to the sharp construction declines of recent years would provide a material boost to aggregate growth through 2026.

External demand and investment’s support for GDP masks the still-troubled state of consumer demand, however. Having surprised to the upside in February at 2.8%ytd, in March retail sales growth slowed once again to 2.4%ytd. While not a disastrous outcome by any means, it is less than half the average pace of the past five years post pandemic, a historically weak period for household demand growth. Policy makers have been clear in their intent to provide additional support to households but are yet to action plans. And, while equities have risen through the year, house prices continue to decline, weighing on wealth and sentiment. Without broadening the growth pulse, aggregate momentum will remain susceptible to slipping towards, or through, 4.0% in coming years, even with a significant benefit from global demand for green technology.

A full update of our expectations and assessment of risks for the global economy and markets will be made available today in the April edition of Market Outlook on Westpac IQ.

Draw a Line on Just Drawing a Line

Scenario analysis is essential in uncertain times, but it must be well-grounded, not just drawing an arbitrary line on a graph.

- You know times are uncertain when institutions start publishing scenarios alongside their normal forecasts. Two principles underlie good scenarios. First, the narrative underlying the scenario must hang together – no assuming people do things that are either individually irrational or infeasible. Second, the scenario must allow people to respond to the initial shock – avoid just drawing a price line on a graph and assuming people cannot adjust their behaviour.

- There is a tension, though, between the need to be realistic and a desire to highlight vulnerabilities or contemplate worst-case scenarios. There is a legitimate role for worst-case thinking, but it must be handled with care. Recall that even though our forecasts last year were less alarmist than many in the wake of Liberation Day, actual outcomes were even better than we had expected.

- The real value of scenarios is teasing out downstream effects and delayed responses. Sometimes the responses to temporary shocks can have lasting effects. From EV purchases to defence budgets, these could be especially important coming out of the current conflict. All the more reason to avoid just drawing a line and assuming that is the outcome.

In times as uncertain as these, you want to be able to articulate more than one possible future state of the world. That is where scenario analysis comes in. Indeed, when institutions start publishing scenarios, you can take it as a sign that things are unusually uncertain. The RBA used scenarios extensively during the pandemic. And while the IMF did not give scenarios any prominence in its previous full World Economic Outlook report in October, it did this week. Similarly, we have published several scenario iterations over the past six weeks and will provide an update later today in our Market Outlook report.

Using scenarios rather than simple uncertainty ranges or a description of risks is especially useful when the possible future states of the world are qualitatively different from the base case, and when the level of conviction about that base case is low. There is nothing wrong with a scenario that is only a little different from the base case, but it is not that interesting or informative.

Two key principles underlie good scenario analysis. First, the premise of the scenario needs to be well-grounded. The narrative motivating the initial impetus must hang together. It must be logically consistent and represent both the interests and the constraints of the actors within the system. In other words, scenarios should not assume that people do things that are either bonkers or infeasible. Individually rational behaviour that is harmful in aggregate, such as panic-buying toilet paper or conducting fire-sales of loss-making assets, should of course be allowed for, but make sure the action is indeed individually rational.

Second, the methods used in developing the scenario need to go beyond first-round thinking. You need to allow for other people to react. A good scenario cannot be just a one-off shock where nothing else changes. Sometimes it takes time for people to adjust to the new situation, so the reaction occurs with a lag. Teasing these reactions out is the value-add of the scenario.

There is a tension, though, between the need to be realistic and a desire to highlight vulnerabilities or contemplate worst-case scenarios. Sometimes a lack of realism is used to guard against a potential failure of imagination. There is a legitimate role for this approach when stress testing, for example. However, unrealistic assumptions in forecast-flavoured scenarios leave your forecasts open to misinterpretation. We have seen an example of this issue this week, where the IMF’s worst-case ‘severe’ scenario, which implies a global recession, has sparked unhelpful talk of recession here in Australia.

Part of the issue is that the IMF’s less-bad ‘adverse’ scenario (which assumes oil prices average USD100/bbl this year before moderating to USD75 next year) and worst-case ‘severe’ scenario (which assumes oil prices stay around USD125/bbl from the outbreak of the conflict all the way through to end-2027) are both ‘top-down’ scenarios that appear to start from an assumed path for oil prices. Unlike our own scenario work, they do not explicitly model loss of supply from the Middle East and work out what prices need to do to clear the global market. By effectively just drawing a line on a graph for oil prices, the scenarios assume away any scope for other producers to respond. This is not an issue in the near term, but the longer the assumption is maintained, the less realistic it is. High prices will spur non-OPEC producers such as the US and Canada to boost production. It takes time to get that expansion running, but eventually prices will start to ease.

Because it assumes high prices right through 2027, the ‘severe’ scenario is most challenged by this issue. This is not to say that the IMF should not have published that scenario, but it is important to understand the context and what it was trying to achieve in doing so.

When developing scenarios, you also need to avoid the trap of thinking only of downside risks. Part of the problem is that downside risks usually come from identifiable events. It is easy to construct a plausible narrative for a scenario starting from “this particular bad thing happened”. But as one of my old bosses used to remind us, sometimes you should also consider the risk everything just turns out a little bit better than expected.

As our April Market Outlook goes to publication later today, it is helpful to recall last April’s edition. The ‘Liberation Day’ tariffs had been announced a fortnight previously, and many voices in the market were predicting global or US recessions. At the time we took a more moderate view, based on the principles noted above. Firstly, continuing with very high tariff rates would have been an act of economic self-harm. While it was hard to bet on the Trump administration acting rationally in a context of ‘flood the zone’ headlines and intemperate social media posts, self-interest is still the best assumption. If there is nothing preventing someone from stopping punching themselves in the face, they will stop punching.

Secondly – and this was a key judgement in our forecast last year – other countries had agency and could respond. In particular, China had scope to stimulate, and this would also cushion growth in Australia. In that context, we note that the latest Chinese GDP growth has again surprised on the upside relative to market expectations.

It turns out that even we were too bearish a year ago: the global economy did much better than expected, and global trade kept expanding with barely a hiccup. Other factors, including a tech boom, turned out to be more important than expected. Trade patterns were also re-routed around the highest tariffs, and of course the US government de-escalated, as is proving to be its pattern.

These principles also hold for other kinds of scenarios. Whenever you read a prediction of doom concerning, say, adoption of a new technology, ask yourself what is preventing people from responding to ameliorate the bad thing. What prevents macroeconomic policymakers from easing, for example, or the tax system from redistributing unequal gains? While occasionally decision-makers decide that a bad thing is good actually, holding that position is itself fragile.

Where scenarios can really add value is when they highlight a lasting effect from a temporary shock. Whether it is the person who buys an EV in response to current high petrol prices and reduces their petrol consumption permanently, or the government that reassesses its defence spending, behavioural responses can change longer-term demand trends, and so the prices that prevail further out. Normalisation after a shock does not always take you back to where you were. That is another reason why it is so important to avoid just drawing a line on a graph and calling it a scenario, ignoring system-wide effects.

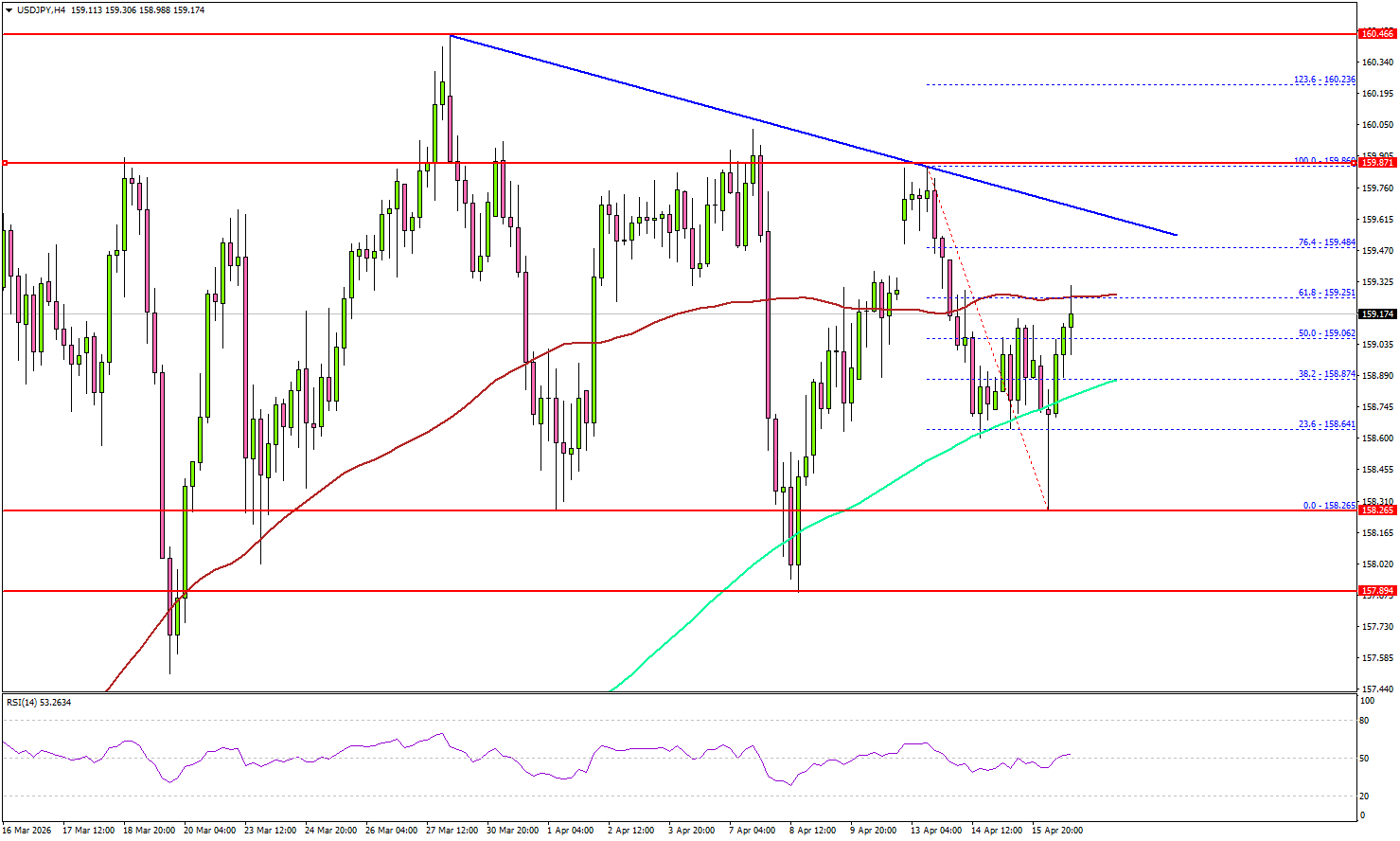

USD/JPY Upside Risks Fade Near 159.60, Bulls Face Key Test

Key Highlights

- USD/JPY is attempting a fresh increase from the 158.25 zone.

- A major bearish trend line is forming with resistance at 159.60 on the 4-hour chart.

- EUR/USD climbed toward 1.1820 before correcting some gains.

- WTI Crude Oil prices are under pressure below $96.40 and $98.50.

USD/JPY Technical Analysis

The US Dollar found support near 158.25 and started a fresh increase against the Japanese Yen. USD/JPY surpassed 158.80 and 159.20.

Looking at the 4-hour chart, the pair settled above the 158.80 level and the 200 simple moving average (green, 4-hour). There was a clear move above the 50% Fib retracement level of the downward move from the 159.86 swing high to the 158.26 low.

The pair even tested 159.25 and the 100 simple moving average (red, 4-hour). On the upside, the pair faces resistance at 159.50. The first major resistance sits at 159.60. There is also a major bearish trend line forming with resistance at 159.60.

The main resistance could be 159.85. A close above 159.85 could open doors for gains above 160.00. In the stated case, the bulls could aim for a move to 161.20.

Immediate support is seen near 158.85 and the 200 simple moving average (green, 4-hour). The first key support sits at 158.50. The next key area of interest might be near 158.25.

A close below 158.25 might push the pair toward 157.90. Any more losses could initiate a fresh move to 156.50 in the coming days.

Looking at Oil, the price started a consolidation phase, and upside might face resistance near $96.40 and $98.50.

Upcoming Key Economic Events:

- Fed's Daly speech.

- Fed's Waller speech.

NZD/USD Technical Outlook: Bulls Stare Down Major Resistance, Bullish Bias Hinges on the 0.5821 Pivot

- The NZD/USD is currently facing its sternest technical test at the 0.5918–0.5920 resistance zone

- The Daily chart suggests a potential long-term trend shift, but the H4 RSI shows bearish divergence, signaling short-term exhaustion.

- A clean break above 0.5920 would accelerate the move toward 0.5950.

- Inability to hold the level, followed by a break below 0.5873, risks a corrective slide back to the major support pivot at 0.5821.

The New Zealand Dollar may be about to face its sternest test yet. The pair has to grapple with a cluster of technical resistance levels around the 0.5918-0.5920 zone, the question for the upcoming session is whether the bulls have enough fuel left in the tank for a structural breakout or if we are due for a "mean reversion" back toward 0.5820.

Daily Chart: The Descending Trendline Challenge

The macro view on the daily chart reveals a pair attempting to break free from a long-term bearish regime. After a sharp sell-off in early 2026, NZD/USD has formed a classic "V-shaped" recovery, slicing through the first major obstacle at 0.5821.

Currently, spot prices are knocking on the door of the 0.5918 resistance level. A daily close above this confluence would signal a significant trend shift, potentially opening the door for a move toward the 0.6100 handle.

However, the Daily RSI at 56.4 shows that while momentum is positive, the pair is far from overbought, suggesting that there is still "white space" for bulls to exploit if the breakout is confirmed.

NZD/USD Daily Chart, April 16, 2026

Source: TradingView

H4 Chart: RSI Divergence Flags Exhaustion

Zooming into the H4 timeframe, the bullish structure remains intact, characterized by a series of higher highs and higher lows. The pair may find support at the 0.5870 - 0.5850 zone, which previously acted as a cap.

However, a note of caution for the bulls: the H4 RSI has printed multiple "BEAR" pivot warnings at the recent peaks near 0.5920. This bearish divergence suggests that the "easy money" on the long side may have been made, and the pair might need a period of consolidation or a slight pullback to gather strength before its next impulsive leg.

NZD/USD Four-Hour Chart, April 16, 2026

Source: TradingView

H1 Chart: Session Scenarios & Key Levels

The hourly chart provides a clear roadmap for the upcoming session, showing the pair currently trading around 0.5892 after a slight rejection from the 0.5918 ceiling.

The Bullish Scenario

For the rally to resume, the Kiwi needs to hold above the intraday support at 0.5873. If buying pressure returns, a clean break above 0.5920 would likely trigger stops from short-sellers, potentially leading to an accelerated move toward 0.5950 and 0.5980. Traders coul look for a "bull flag" consolidation pattern on the M30 or M15 as a precursor to this move.

The Bearish Scenario

The inability to hold above the 0.5920 level is the first warning sign. If we see a break below 0.5873, it would likely confirm a "double top" on the lower timeframes. This could trigger a corrective slide back toward the major support pivot at 0.5821, where the long-term descending trendline might be retested from the "top side."

Key Levels to Watch:

- Resistance: 0.5918 (Major), 0.5950, 0.6000

- Support: 0.5873, 0.5821 (Pivot), 0.5780

NZD/USD One-Hour Chart, April 16, 2026

Source: TradingView

NZD/USD is at a critical technical junction. While the daily structure is turning constructive, the short-term indicators are screaming for a breather. As long as the 0.5821 level holds on a closing basis, the bullish bias remains the dominant theme.

WTI and Brent Oil Bounce with US-Iran News Still Awaited – What’s Next? Intraday Analysis

- WTI and Brent Crude Oil Technical Analysis with key levels as US-Iran news are still awaited.

- Despite extreme positivism in Stock Markets, Energy commodities remain doubtful.

- Volatility continues to shrink, but the latest progress has largely stalled.

The pricing of a peace deal between the US and Iran is continuous but also quite coarse.

While Equity Markets have gone on an absolute frantic rally, boosted by short-covering, options delta hedging, TACOs, and an ever-hungrier investor, Commodities are subject to very different dynamics.

Particularly when it comes to Energy products, Supply and Demand play their own very influential role.

While Futures pricing helps to dictate expectations, Traders have to remember that, before anything else, real products are needed for production, consumption, and much more around the world – Hence, physical demand has an immense influence on prices.

A major narrative that has emerged throughout the War is the large difference between physical and futures pricing, which has raised questions about a disconnect between Market pricing and the real-life issues faced by large buyers.

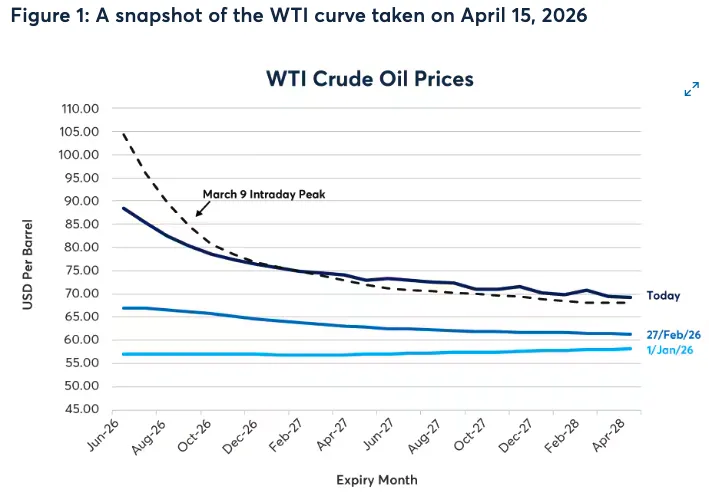

WTI Futures Backwardation from April 15, 2026 – Source: CMEGroup

The Futures Market has been in a large backwardation (where front contracts trade well above later contracts) – A natural formation amid supply fears, but no less damaging for hedgers. I invite you all to discover such dynamics throughout this fantastic CME piece.

Add to this gigantic regional discrepancies in Barrel prices, particularly in Asia, and you get a Market pulled higher by relentless demand while supply remains in a large drought.

This has created another wave of rallying throughout the session, with selloffs remaining supported by fresher bids – As long as Hormuz remains closed, a grind higher on pullbacks in Oil remains the path of least resistance.

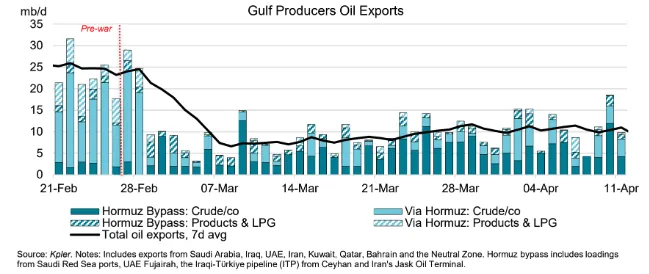

Meanwhile, US-Iran talks that were supposed to start again today, are finally set to only start throughout the weekend. This did come with its fair share of good news, with Israel and Lebanon agreeing to a ceasefire, a final step before the discussions.

Gulf Oil Delivery Issues since End-February. Source: IEA

With these factors in mind, let's dive right into an intraday outlook for both WTI and Brent Oil, highlighting their technical levels and outlining scenarios for their breakouts or breakdowns.

Crude Oil Market Check and Technical Levels

WTI 4H Chart

WTI Oil 4H Chart – April 16, 2026. Source: TradingView

WTI Crude has once again fallen below Brent after an irregular Market pricing throughout the past week, tumbling to $87.20 with Israel-Lebanon Peace talks boosting sentiment.

Nevertheless, as expressed in the introduction, the path of least resistance is to the upside, hence, bulls have pushed the commodity right back towards the 4H 200-period moving average (~$94.30).

Having rejected it, sellers will want to see extension back towards $90.

Failing to do so could see a large $90 to $100 range as traders await for clear instructions on where to look next.

Resistance and Support levels remain the best guides to navigate these volatile environments.

WTI Technical Levels:

Resistance Levels

- Daily highs $113.50 to $114.50 (small channel top)

- 2022 and Monday highs $117 to $120 (larger channel top)

- Ukraine War Spike $120 to $124

Support Levels

- War Support $93.00 - $95 (testing)

- $87 to $90 mini-Support (recent bounce)

- $82.80 to $84 micro-Support

- 2025 Highs Key Support $78 to $80

- $69 to $70 Final War Support

Brent 4H Chart

Brent Oil 4H Chart – April 16, 2026. Source: TradingView

Brent is still in a more contained price action compared to WTI, with the range now extending to $95 to $107.

Now testing its key 50 and 200-4H MAs, the action remains quite undecided.

Breakout traders will want to see a daily close below $95 (for sellers) and a clean break above $107 for buyers.

If the situation remains uncertain, the range should maintain.

Brent Technical Levels:

Resistance Levels

- $100 - $102 End-March Pivot

- Mini Resistance $105 - $107

- Range Resistance $111 to $114

- War Highs $117 to $120

Support Levels

- End-March Support $95 to $97

- $92.39 Recent dip

- $88 - $92 March 10 Bounce and 200-MA

- $80 - $82 Key War Support

- Pre-War Gap $75

Keep track of the headlines as the talks come closer by the second.

Safe Trades!

US Dollar Stalls as the World Awaits Ceasefire News – DXY Outlook

- The US Dollar stalls its correction as Traders hold their breath, awaiting for Ceasefire news

- After a 2.50% correction in the Dollar Index, FX remains quite stuck

- US Dollar Index (DXY) in-depth Technical Analysis

The US Dollar is under some complex dynamics, still moving along with Crude Oil prices, and both are just stuck in the mud.

The talks, supposed to begin today in Islamabad, haven't made it to the news yet, so it seems that there are some delays – The US is still eager to reach a deal, but Pete Hegseth, Head of the Department of War just issued a address to reaffirm that the most powerful army is "to restart combat if Iran doesn't agree to a deal".

Amid the borderline-insane price action in the Stock Markets, with two of the three Major Indexes reaching all-time highs (Nasdaq just set a new record in overnight trading), Participants are taking a break to await clearer developments.

After all, at current levels, whether for the USD, Stocks, or WTI, risks to the upside and downside are both extreme.

WTI Crude and Dollar Index (DXY) Correlation since April 5 – Source:TradingView

For now, Crude has stopped its move to the downside and is even moving higher, keeping the broader Market awaiting – You can see how significant the WTI-Dollar correlation has remained throughout the entire Ceasefire.

Hence, tracking Oil is almost more important than the headlines themselves for Forex trading.

Stock markets, on the other hand, did own heavily, lifting, having relatively decoupled from Black Gold, but will be looking at the commodity for the next phase.

In terms of pure geopolitics, the Israel-Lebanon talks under US supervision seems to be progressing smoothly, with a potential ceasefire in the coming hours/days.

Hezbollah will have to be put on the side, and they are reportedly exerting heavy pressure to not enter into deals with Israel. The terrorist organization has prevented deals ever since 1993, the year when Jordan and Israel reached a Peace deal that has held since.

There have been reports that there are no more deadlocks in the US-Iran mediated negotiations – But these headlines haven't been as decisive to provide further clarity on the situation. Hence, from here, all that traders will wait to see is a proper resolution.

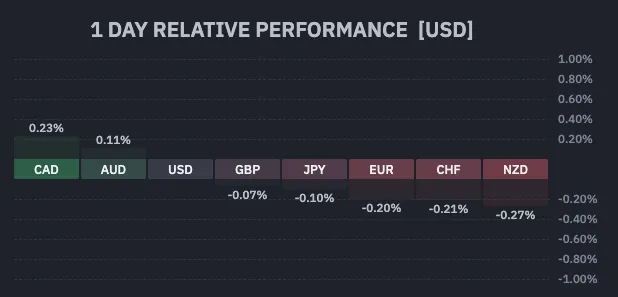

FX Performance (10:15 A.M. ET) – Source: TradingView. April 16, 2026

With WTI now catching a bid, the US Dollar is extending higher on the session, with moves still quite timid for now.

We’ll explore a few scenarios for a potential large reversal in an in-depth technical analysis of DXY.

Dollar Index (DXY) Multi-Timeframe Analysis

Daily Chart

Dollar Index (DXY) Daily Chart. April 16, 2026 – Source: TradingView

In the bigger picture, the large 95.50 to 100.00 range is holding extremely well, with a double top last at the most recent test that led to the ongoing correction in the US Dollar.

As always, it is more than advised to keep an eye on the bigger timeframes to see if any particular trend dictates the price action, as they offer some setups and allow to reduce if not discard the noise.

After the 2.50% correction, the move is stalling and this comes right around the middle of the range, an important level for the bull/bear intermediate outlook.

4H Chart and Technical Levels

Dollar Index (DXY) 4H Chart. April 18, 2026 – Source: TradingView

The Dollar Index is forming an immediate bullish divergence, boosting prospects for an immediate pullback higher.

The 98.50-98.70 War Pivot and Psychological level would offer strong opportunities in to rejoin the trend in other FX pairs.

Extending to 98.80 (4H 50-period MA) offers the best entries, however, any close above could entice a pursued rally in the USD.

Keep a close eye on other FX pairs to position yourself – GBP/USD, USD/CAD and USD/JPY offer favorable setups on pullbacks.

Levels to place on your DXY charts:

Resistance Levels

- 98.50 to 98.70 War Pivot

- 98.80 4H 50-period MA

- 99.40 to 99.50 Resistance

- 100.00 to 100.50 Main resistance and Range highs

- War Highs 100.544 (Double Top)

Support Levels

- 98.00 Major Support (rejecting)

- Support 97.40 to 97.60

- 2025 Lows Major support 96.50 to 97.00

- Range lows at Early 2022 Consolidation just below 96.00

Safe Trades and keep track of the latest headlines!

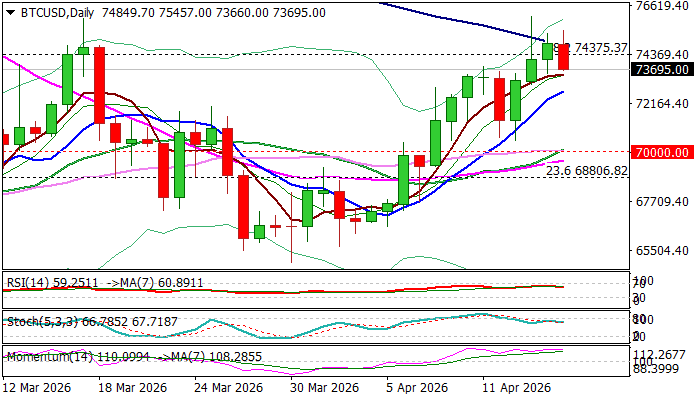

BTCUSD – Bulls Pause After Cracking Important Barriers

Bitcoin price edged lower after the acceleration in past three days broke above Fibo level at 74375 (38.2% of 97946/59805) and cracked strong barriers at 74575/74775 (daily cloud top / 100DMA).

Fresh optimism about solution for the Middle East conflict revived risk appetite and underpinned bitcoin, with predominantly bullish daily studies (strong positive momentum / multiple DMA bull-crosses) contributing to bullish near-term outlook.

On the other hand, the price hits again the top of multi-week range (76K zone) where bulls may face increased headwinds (after strong rejection here in mid-March), with further warning from daily Stochastic bearish divergence.

Potential dips should find firm ground above rising 10DMA (72796) and daily cloud base (70651) to mark healthy correction and keep broader bulls in play for attempts to clearly break of range top that would unmask targets at 78875 (50% retracement) and 80000 (psychological).

Res: 75457; 76111; 78875; 80000

Sup: 73581; 72796; 70486; 70000

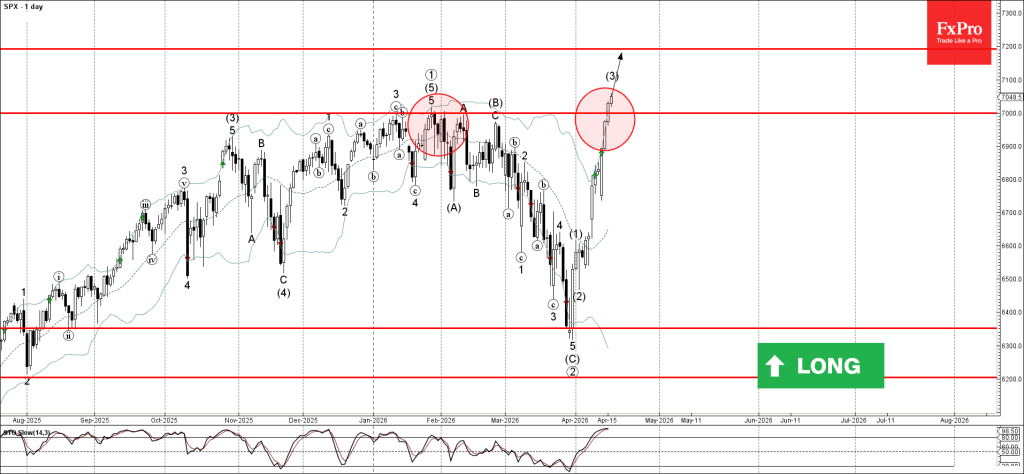

S&P 500 Wave Analysis

S&P 500: ⬆️ Buy

- S&P 500 broke round resistance level 7000.00

- Likely to rise to resistance level 7200.00

S&P 500 index recently broke and closed above the major round resistance level 7000.00, which has been repeatedly reversing the index from January.

The breakout of the resistance level 7000.00 accelerated the active medium-term impulse wave (3) from the start of April.

Given the strong daily uptrend, S&P 500 can be expected to rise toward the next resistance level 7200.00, target price for the completion of the active impulse wave (3).

Eco Data 4/17/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 24.9B | 29.8B | 37.9B | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Feb | 7.0B | 11.1B | 12.1B | |

| 12:15 | CAD | Housing Starts Mar | 236K | 253K | 251K |

| 08:00 | EUR |

| Eurozone Current Account (EUR) Feb | |

| Actual | 24.9B |

| Consensus | 29.8B |

| Previous | 37.9B |

| 09:00 | EUR |

| Eurozone Trade Balance (EUR) Feb | |

| Actual | 7.0B |

| Consensus | 11.1B |

| Previous | 12.1B |

| 12:15 | CAD |

| Housing Starts Mar | |

| Actual | 236K |

| Consensus | 253K |

| Previous | 251K |

Fed’s Williams: Energy Shock Inflation and Growth Risks “Have Begun to Play Out Already”

New York Fed President John Williams warned that rising energy prices are already feeding into inflation, as the Iran War pushed up costs across the economy. He noted that “developments in the Middle East are driving significant increases in energy prices,” with effects now visible not only in fuel but also in airfares, groceries, and other consumer goods.

Williams emphasized that the shock carries two-sided risks. While energy prices could ease if supply disruptions are resolved, he cautioned that the conflict could evolve into a broader supply shock that “simultaneously raises inflation… and dampens economic activity.” This dynamic, he said, “has begun to play out already,” highlighting early signs of stagflationary pressure.

Despite these risks, Williams struck a measured tone on policy. He said monetary policy is “well positioned to balance the risks” to both inflation and employment, without signaling any immediate shift in direction. While acknowledging that the outlook is “highly uncertain,” he maintained expectations for solid growth of 2%–2.5% this year, with inflation around 2.75%–3% before gradually returning to target by 2027, supported by stable longer-term inflation expectations.