Sample Category Title

EUR/JPY Daily Outlook

Daily Pivots: (S1) 187.22; (P) 187.47; (R1) 187.83; More...

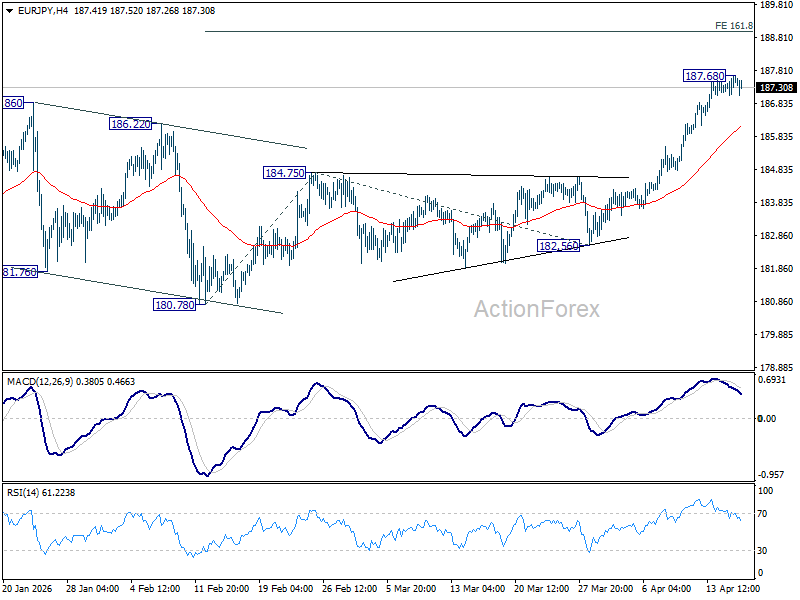

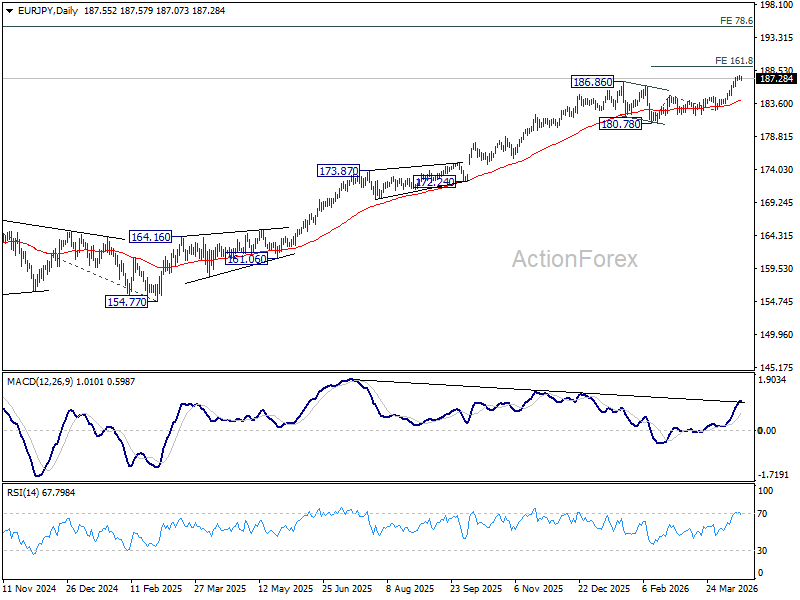

Intraday bias in EUR/JPY is turned neutral first with current retreat, and some consolidations could be seen below 187.68 temporary top. Downside of retreat should be contained well above 184.75 resistance turned support. Above 187.68 will resume larger up trend to 161.8% projection of 180.78 to 184.75 from 182.56 at 188.98 next.

In the bigger picture, up trend from 114.42 (2020 low) in in progress and should be ready to resume. Next target is 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. For now, medium term outlook will stay bullish as long as 175.41 resistance turned support holds, even in case of deeper pullback.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8691; (P) 0.8697; (R1) 0.8707; More…

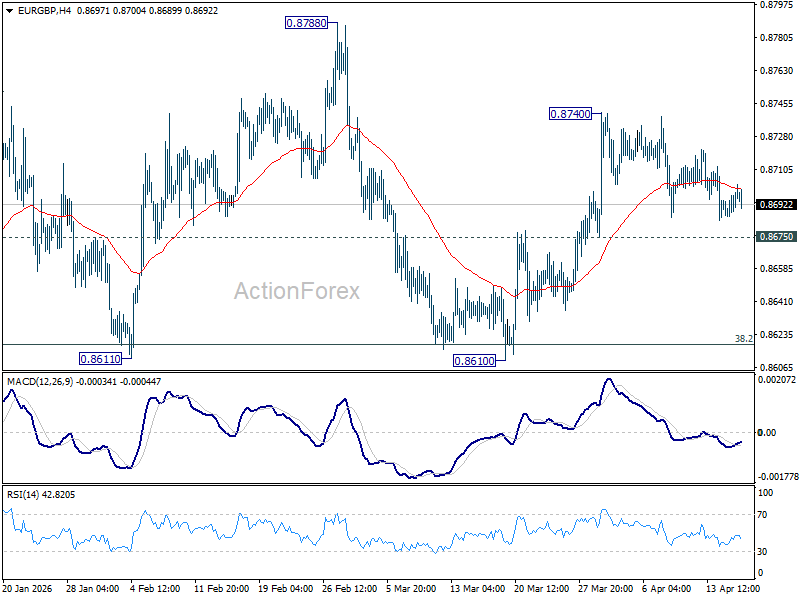

EUR/GBP is staying in consolidations from 0.8740 and intraday bias remains neutral. Further rise is mildly in favor as long as 0.8675 support holds. Break of 0.8740 will resume the rebound from 0.8610 to 0.8788 resistance. However, firm break of 0.8675 will turn bias back to the downside for retesting 0.8610 low instead.

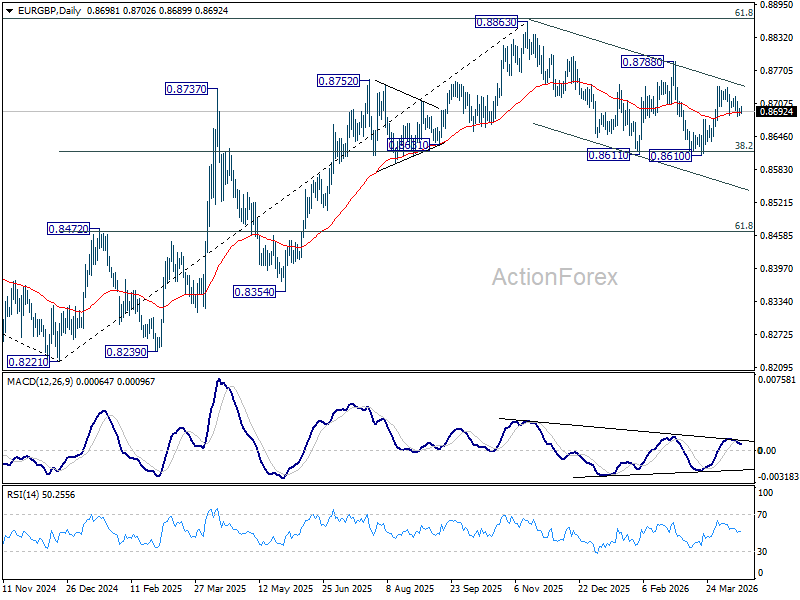

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be ready to resume through 0.8863 (2025 high). Nevertheless, sustained trading below 0.8618 should confirm bearish reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

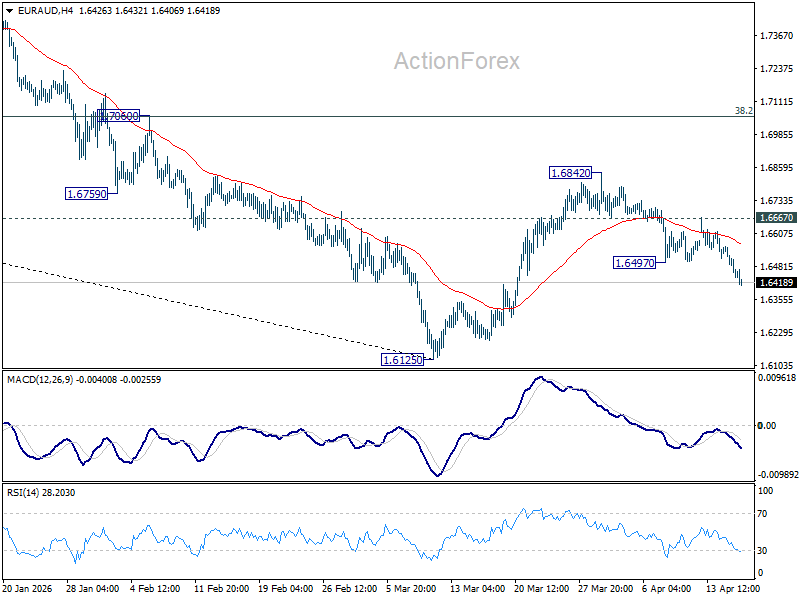

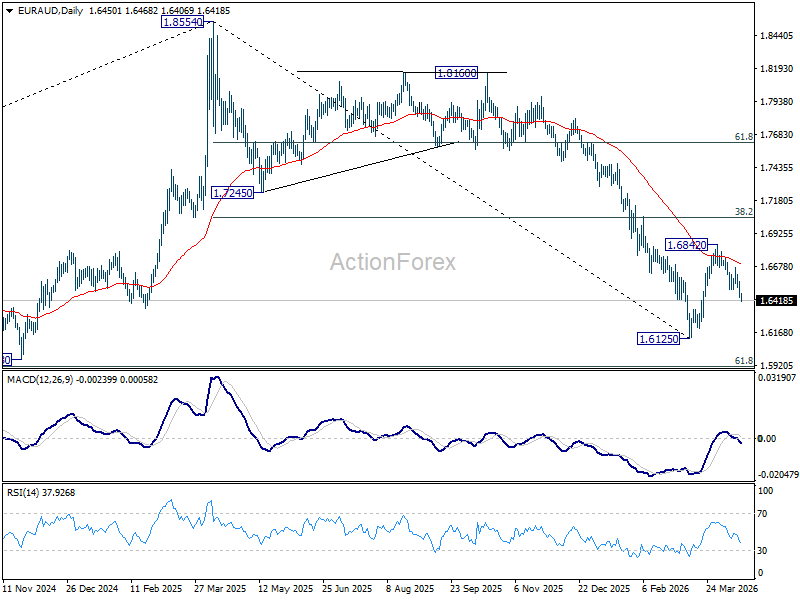

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6405; (P) 1.6493; (R1) 1.6544; More...

Intraday bias in EUR/AUD remains on the downside as this point. Fall from 1.6842 is in progress for retesting 1.6125 low. Firm break there will resume larger down trend. On the upside, above 1.6667 minor resistance will turn intraday bias neutral again first.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7163) holds, even in case of strong rebound.

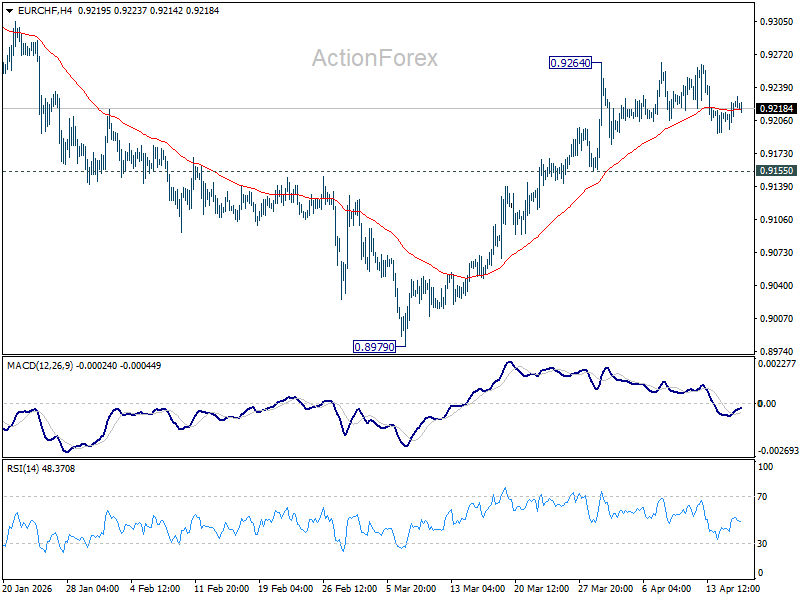

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9206; (P) 0.9218; (R1) 0.9239; More....

EUR/CHF is still bounded in consolidation below 0.9264 and intraday bias remains neutral. Further rise is expected with 0.9155 support intact. Firm break of 0.9264 will resume the rebound from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9281) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

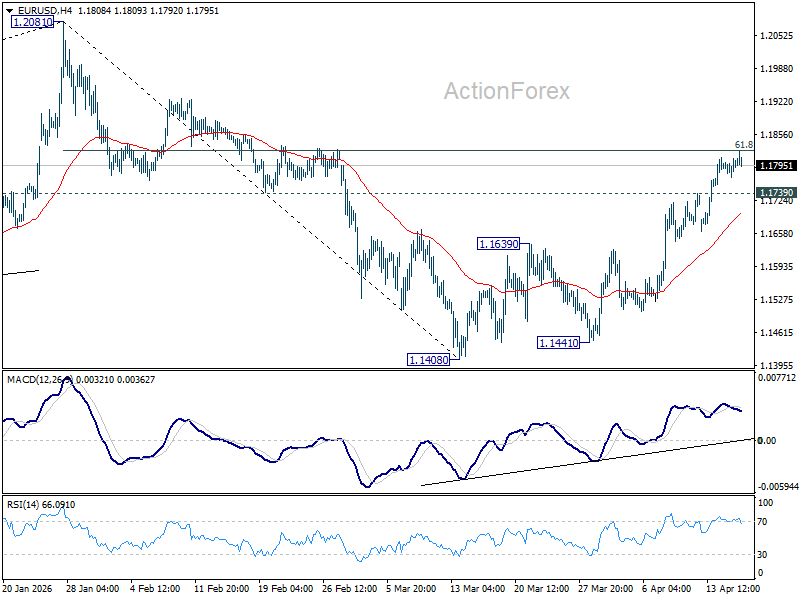

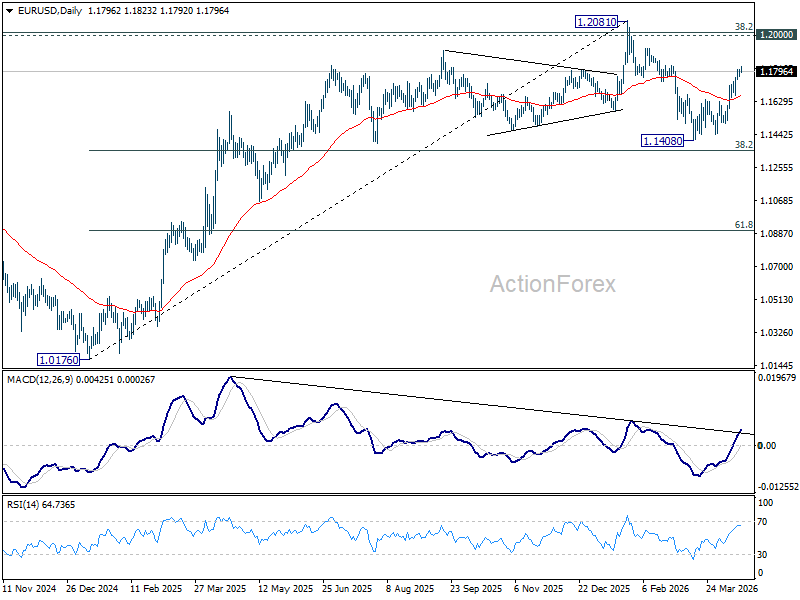

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1778; (P) 1.1793; (R1) 1.1815; More….

Intraday bias in EUR/USD remains on the upside for the moment. Decisive break of 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will extend the rally from 1.1408 to retest 1.2081 high. On the downside, below 1.1739 minor support will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

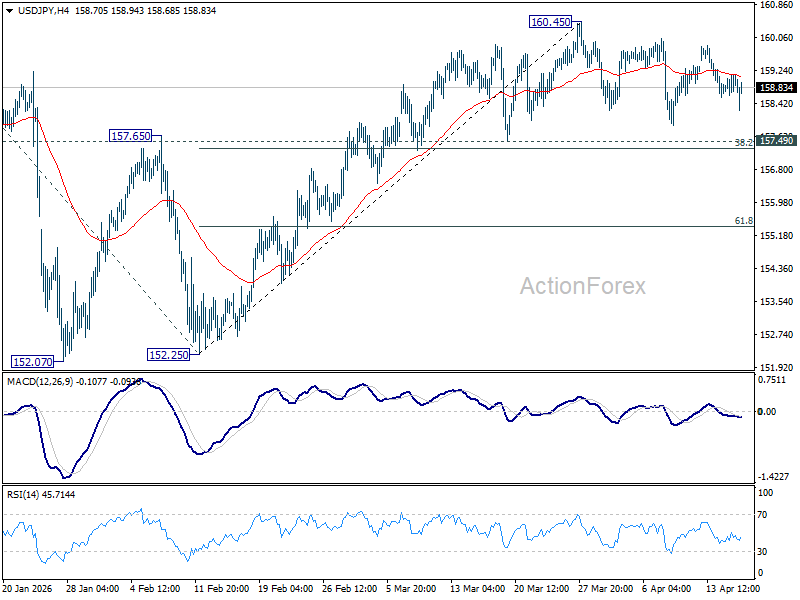

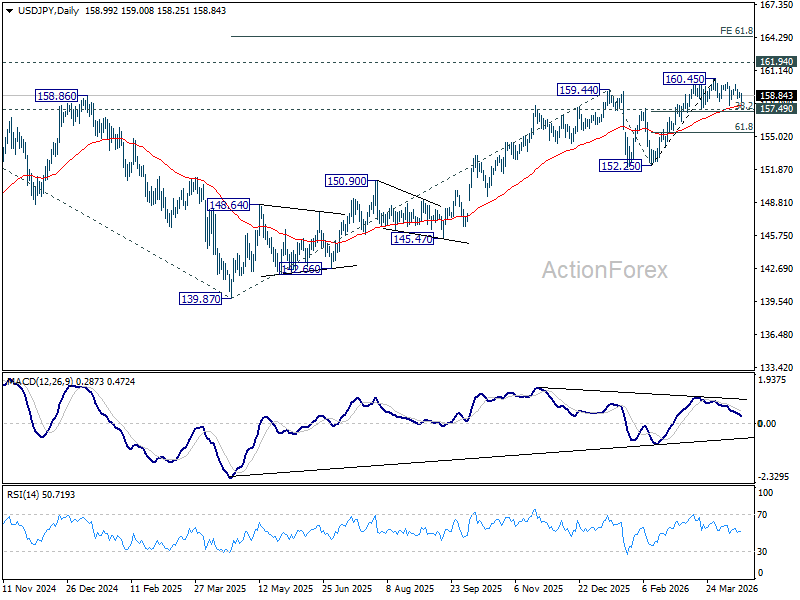

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.67; (P) 158.95; (R1) 159.26; More...

USD/JPY is still extending the consolidation pattern from 160.45 and intraday bias remains neutral. Outlook will stay bullish as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 155.24) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

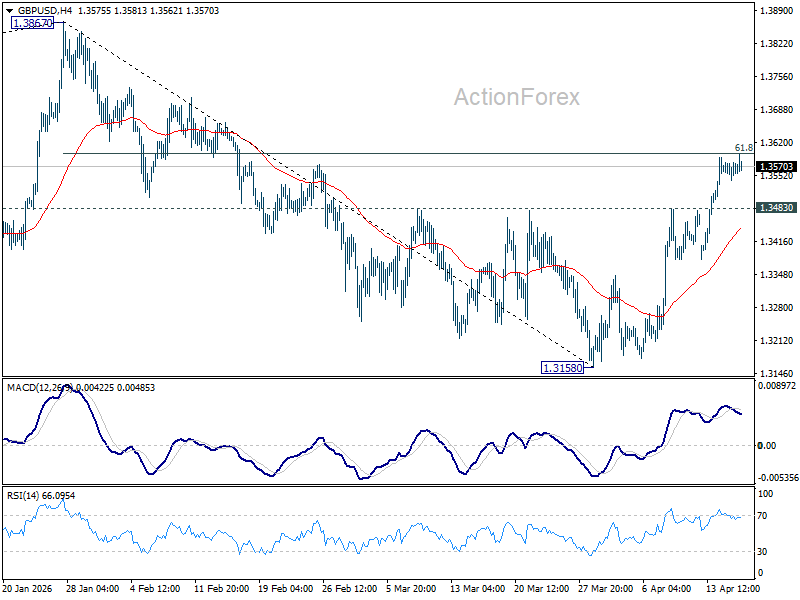

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3543; (P) 1.3562; (R1) 1.3581; More...

Further rally is still expected in GBP/USD with 1.3483 minor support intact. Firm break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will extend the rise from 1.3158 to retest 1.3867 high. On the downside, below 1.3483 minor support will turn intraday bias neutral first.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

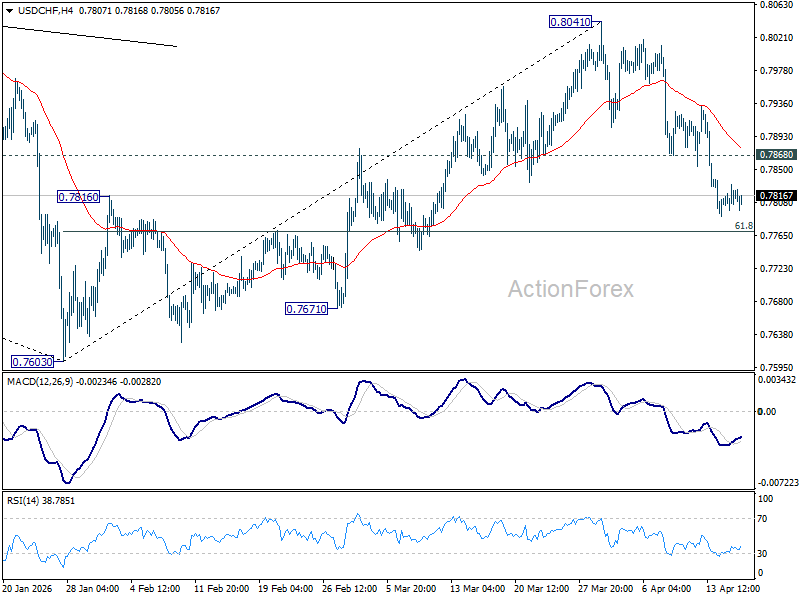

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7801; (P) 0.7816; (R1) 0.7835; More….

Further decline is still expected in USD/CHF with 0.7868 minor resistance intact. Fall from 0.8041 should target 61.8% retracement of 0.7603 to 0.8041 at 0.7770. Decisive break there will target a retest on 0.7603 low. On the upside, above 0.7868 minor resistance will turn intraday bias neutral first.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8071) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

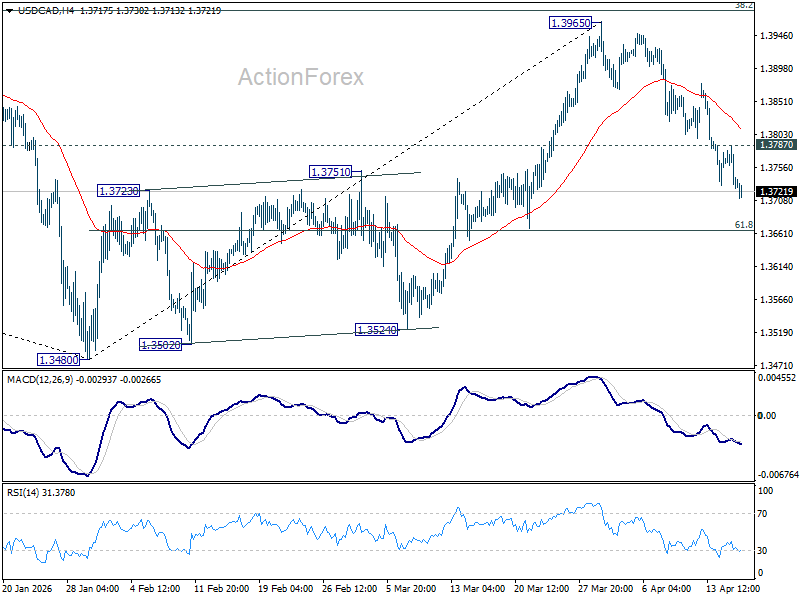

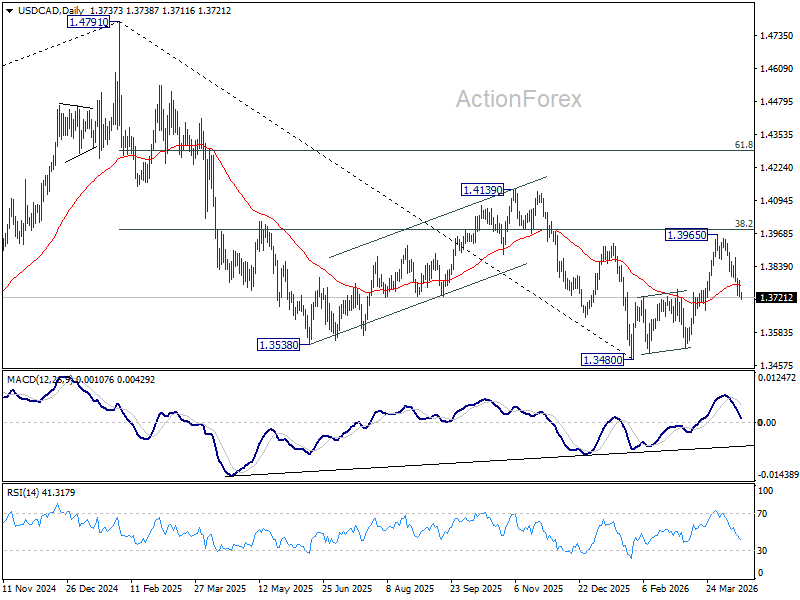

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3715; (P) 1.3752; (R1) 1.3777; More...

Intraday bias in USD/CAD remains on the downside as fall from 1.3965 is in progress for 61.8% retracement of 1.3480 to 1.3965 at 1.3665. Decisive break there will extend the decline from 1.3965 to retest 1.3480 low. On the upside, above 1.3787 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

Nikkei 225’s Bullish Reversal Extends Towards New All-Time Highs

Key takeaways

- Ceasefire optimism driving rebound: Improving prospects of a US–Iran ceasefire and reduced escalation risks have lifted sentiment, fuelling a strong recovery in the Nikkei 225 despite lingering stagflation concerns.

- Macro support from JGB yield curve steepening: Bullish steepening in Japan’s yield curve signals easing growth fears and has historically moved in tandem with equities, reinforcing the bullish outlook for the Nikkei.

- Uptrend gaining momentum near record highs: The index has rallied ~18% from late-March lows and is approaching all-time highs, with further upside likely if key support holds, while a break below support may trigger a short-term pullback.

The current US-Iran ceasefire optimism, which is now translating into a higher chance of a peace deal, has ignited the bulls in the Japanese stock market despite the ongoing blockage of the Strait of Hormuz that hinders global oil supply, which, in turn, may rouse stagflation risk.

The failure of the negotiation talks between the US and Iran over the last weekend did not lead to a further escalation of attacks by both sides, but rather some form of compromise to find a “middle ground” as the US and Iran are considering extending the earlier ceasefire deadline agreement, due on next Tuesday, 21 April, by another two weeks, and to allow make time to set up another round of negotiation talk before 21 April.

Nikkei 225 trimmed losses above the key 200-day moving average

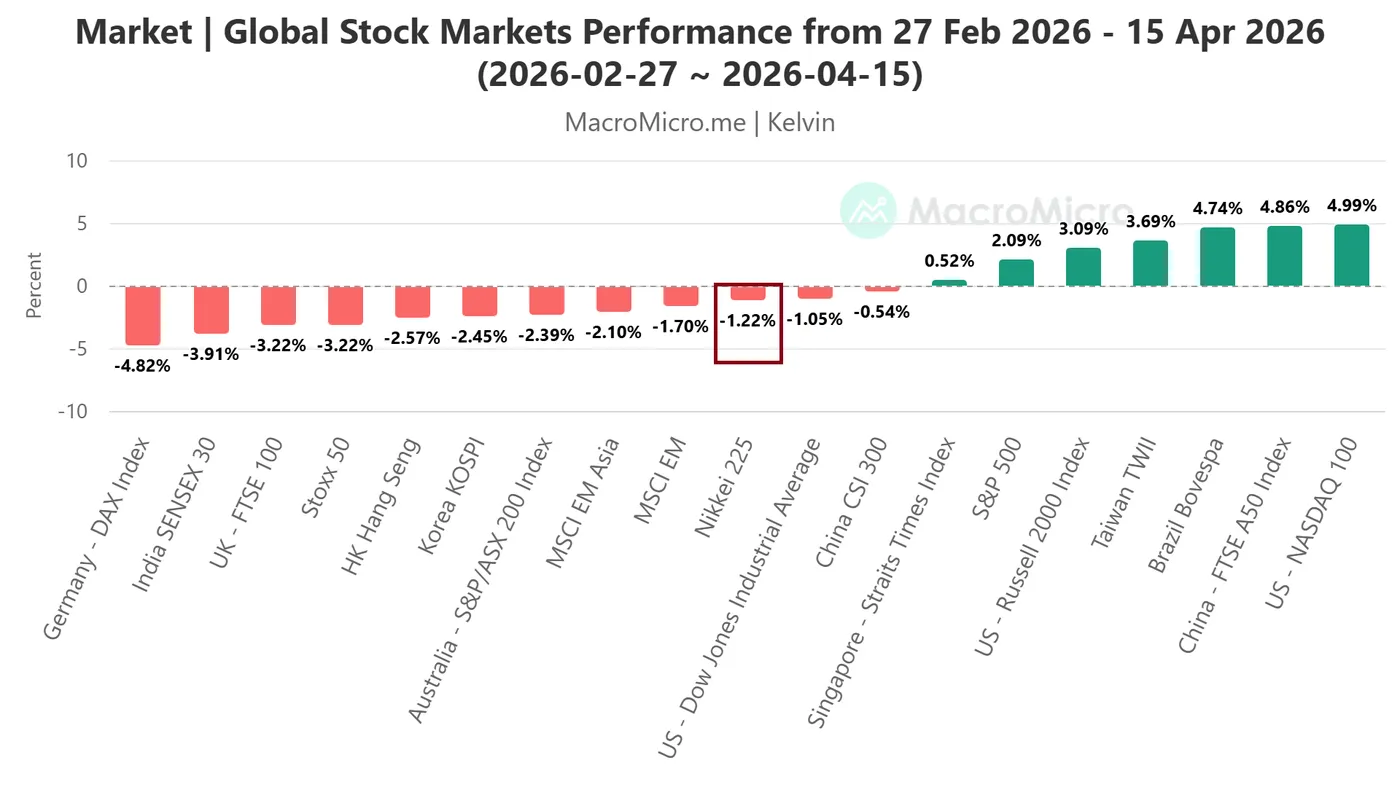

Fig. 1: Global major benchmark stock indices performances from 27 Feb 2026 to 15 Apr 2026 (Source: MacroMicro).

Since the start of the US-Iran war, the Nikkei 225 has declined by 13% from the 27 February 2026 high towards a low of 50,395 printed on 30 March 2026 while holding above its key 200-day moving average at around 48,250.

In the past five trading sessions, the losses have been trimmed, and the Nikkei 225 has now recorded a marginal loss of 1.2% measured from 27 February 2026 to 15 April 2026 (see Fig. 1).

Continuation of JGB yield curve bullish steepening has discounted stagflation fear

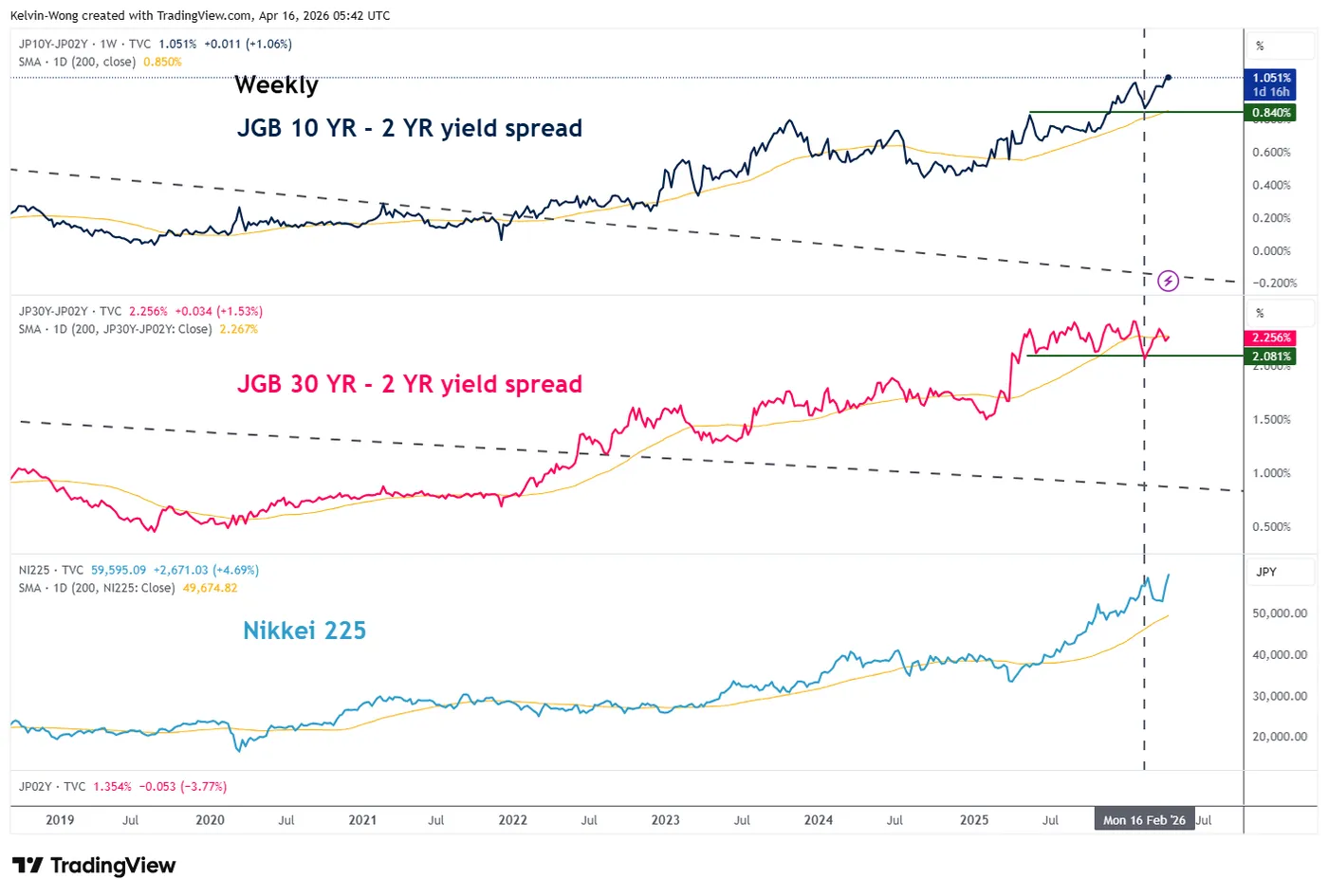

Fig. 2: JGB yield curves major trends with Nikkei 225 as of 16 Apr 2026 (Source: TradingView).

Since last Monday, 6 April 2026, the shorter-term (2-year) Japanese Government Bond (JGB) yield has declined at a faster pace (6 basis points) versus a drop of 4 bps seen the 10-year JGB yield.

Therefore, a bull steepening has occurred on the yield spread between the 10-year and 2-year JGBs that led to trade higher above its key 200-day moving average, acting as a support at 0.84%, to a 15-year high at 1.05% at this time of writing.

A further continuation of a bullish steepening seen in the JGB yield curve is likely to support a further bullish impulse up move sequence in the Nikkei 225, as both move in direct lockstep since June 2022 (see Fig. 2).

Let’s now focus on the technical factors to determine Nikkei 225’s potential short-term trajectory (1 to 3 days).

Nikkei 225 – Oscillating within a minor ascending channel

Fig. 3: Japan 225 CFD index minor trend as of 16 Apr 2026 (Source: TradingView).

The ongoing 18% rally seen from the 31 March 2026 low on the Japan 225 CFD index (a proxy of the Nikkei 225 futures) is now fast approaching an intermediate resistance of 59,890/60,075 (also the current all-time high printed on 26 February 2026).

Watch the 57,830/57,274 short-term pivotal support to maintain the bullish momentum for the next intermediate resistances to come in at 60,832 and 62,044 (Fibonacci extension clusters) in the first step (see Fig. 3).

On the other hand, a break and an hourly close below 57,274 invalidates the bullish bias for a minor corrective decline within an uptrend phase to expose the next intermediate support at 55,695 (also the 50-day moving average), and below it may see 55,130/54,600 next (also the 20-day moving average)

Key elements to support the near-term bullish bias on Nikkei 225

- Price actions are trading above the 20-day and 50-day moving averages.

- The hourly RSI momentum indicator hit an overbought reading without a bearish divergence condition.