Sample Category Title

China Set to Benefit from Global Energy Unrest

Chinese exports will receive a material boost from high oil prices. The consumer remains a risk to GDP growth, however.

China’s economy has begun 2026 in good health despite the conflict in the Middle East, registering annual GDP growth of 5.0% in Q1. In time, recent developments are likely to prove a net positive for China, spurring greater demand for green technology across developed and developing markets.

Not only were the March readings for the official NBS manufacturing and services PMI’s favourable, registering increases to 50.4 and 50.1, but the partial data through February and March showed the beginning of a long-awaited stabilisation in consumer demand and turn for housing investment, retail sales growth beating estimates in February at 2.8%ytd (although growth slowed again in March to 2.4%ytd) and the decline in property investment almost halving from –17.2%ytd in December to –11.2%ytd in March. The latter result is particularly welcome given construction activity has declined almost 40% since end-2021.

In the short term, an end to the sharp decline in property investment will add meaningfully to economic growth given the sector still makes up circa 15% of the aggregate economy. In the medium to long-term though, not only will investment activity need to expand sustainably, but wealth must follow. As yet, there is no evidence of price growth, with new and existing home prices falling a further 0.2% in March.

We remain circumspect on the rate at which retail sales growth will accelerate from here near term, anticipating it is unlikely to return to trend, let alone outperform, until pro-active fiscal policy comes into effect. Authorities signalled an intention to act at the March NPC, but detail has been scarce since.

It is potentially the case that the Government wants clean air for reforms, which the Middle East conflict and the upcoming May meeting between President Xi and President Trump precludes for now. Though authorities may also feel the domestic economy has been given additional time to find its own path without intervention. The response of consumers and businesses across developed and developing markets to the current surge in energy prices will almost surely be an acceleration in demand for renewable energy products and electric vehicles, which China is globally dominant in and has ample spare capacity to produce and ship.

Even without a further material improvement in domestic demand, the short-term downside risks for Chinese GDP growth are receding thanks to this catalyst. Note too, the positive impulse is likely to prove lasting as geopolitical uncertainty over energy supply produces a national imperative to reduce reliance on the Middle East, particularly amongst south-east Asia, Latin America and Africa, where Chinese firms are experiencing particularly rapid demand growth.

Indeed, the learnings from this crisis, and what is expected to be a favourable result from the May meeting between President Xi and President Trump, could also skew long-term risks for Chinese growth and sentiment to the upside. This is not to say that 5.0% growth is probable for 2026–2028, but rather that growth is increasingly likely to stabilise around 4.5% instead of 4.0%.

Attaining annual growth of 5.0% over successive years would require material gains for trade, industrial investment, property construction and household consumption. The latter would necessitate a dramatic turn in actual and expected wealth and sentiment, however. While not impossible, given the poor starting point on both fronts, this is best considered a low probability and long-coming upside risk.

Sooner than later though, the favourable shift in global opportunities and risks for China is likely to support stronger demand in Chinese financial instruments. Yields and credit spreads will remain compressed, enticing additional real economy investment, and equities should see sustained inflows of new capital.

Paired with continued strength in the trade balance and the returns from offshore investments currently being made by Chinese firms, demand for the renminbi will grow in depth and breadth. Given the diversity of Chinese interests across the globe, currency gains are expected on a trade-weighted basis but will be most acute bilaterally versus the US dollar – the only currency Chinese entities look to be reducing their exposure to. Importantly, trade-weighted currency gains are likely to be proportional to China’s competitiveness opportunities, and so should not materially narrow the current account.

This analysis was initially released in the April edition of Westpac Market Outlook.

Falling WTI Boosts Risk Appetite as Equities Rise and USD Falls

WTI price moves continued to lead most markets last week. Better sentiment around the Iran ceasefire pushed WTI lower from the start of the week, while the U.S. dollar weakened and global stock markets moved higher. Market focus stayed mainly on Iran developments, so economic data had less influence on overall price action.

The main economic highlights were lower-than-expected U.S. PPI and weaker U.S. industrial production data. Long-term U.S. interest rates also moved lower as Middle East tensions eased. At the same time, strong U.S. bank earnings supported the view that the U.S. economy is still holding up reasonably well.

Sentiment improved again toward the end of the week. On Friday, comments from the Iranian Foreign Minister that the Strait of Hormuz would remain “completely open” helped reduce market fears further. This pushed the U.S. dollar lower and helped equity markets finish the week with a strong rise.

Markets This Week

U.S. Stocks

U.S. equities posted another strong week, with Friday’s rally helping the market recover all of the losses seen at the start of the Iran conflict. However, weekend news about the closure of the Strait of Hormuz could lead to some pullback at the start of this week. As the two-week ceasefire moves closer to its end, markets may also become more cautious. Sentiment can still change quickly on any headline from U.S. or Iranian leaders, but for now, a sideways to slightly lower move looks more likely this week. Resistance levels are at 49,600, 50,000, 50,500 and 51,000. Support is seen at 48,500, 48,000, 47,000, 46,000, and 45,000.

Japanese Stocks

The Nikkei 225 moved back near the record highs seen earlier this year as tensions in Iran eased and the yen stayed weak. Comments from the Bank of Japan suggesting it may not raise interest rates at the April meeting also helped support stocks. The Nikkei has stayed strong in 2026, but after this latest rise, waiting for a pullback may still be the better strategy. Resistance is seen at 60,000, 60,500, 61,000, 61,500 and 62,000, while support is at 57,000, 56,000, 55,000, 54,000, and 52,000.

USD/JPY

USD/JPY moved lower last week as falling WTI prices and lower long-term U.S. interest rates put pressure on the pair, while resistance at 160 stayed strong. At the same time, the Bank of Japan remained cautious about raising interest rates, which helped buyers return when the pair dropped quickly on Friday. Overall, USD/JPY still looks stuck in a range with a slight downward bias, so range trading remains the better short-term approach. Resistance is at 160.00, 160.50, 162, and 165, while support is seen at 158.00, 157.50, 156.50 and 155.00.

Gold

After testing lower at the start of the week, gold rose steadily as lower long-term U.S. interest rates helped support the market. Trading conditions stayed fairly quiet as many traders focused more on other markets. Gold did meet resistance near the highs from early April, but the uptrend is still in place, so buying on dips remains the preferred strategy as the market moves toward a possible return to $5,000. Resistance is at $4,900, $5,000, and $5,100, while support is at $4,700, $4,600, $4,500, and $4,400.

Crude Oil

WTI moved lower through most of last week as the market reacted to ongoing negotiations to end the war in Iran. Friday’s news that the Strait of Hormuz had reopened added more pressure and encouraged stronger selling. However, weekend reports of another closure are likely to bring buyers back at the start of the week, as the Middle East situation remains very unstable. Headlines will continue to move WTI sharply, but with hopes that the war may eventually move toward an end, selling into strong rallies may be the better strategy this week. Resistance is at $90, $95, $100, $110, and $120, while support is at $80, $75, $70, and $67.5.

Bitcoin

Improved risk sentiment as tensions in Iran eased helped give buyers more confidence, pushing Bitcoin above resistance at $75,000. The market has now broken out of the $65,000 to $75,000 range, and the 10-day moving average is turning higher. For now, buying on dips looks like the better strategy. Resistance is at $80,000, $85,000, and $90,000 while support is at $75,000, $65,000, $60,000, and $55,000.

This Week’s Focus

- Monday: None

- Tuesday: Japan Adjusted Trade Balance, U.K Unemployment Rate, E.U ZEW Economic Sentiment, U.S. Retail Sales and Pending Home Sales

- Wednesday: Japan Trade Balance, U.K. CPI and PPI

- Thursday: Japan S&P Global Services PMI, Australia Unemployment Rate, E.U. HCOB Eurozone Manufacturing PMI, U.K. S&P Global Manufacturing PMI, U.S. S&P Global Manufacturing PMI

- Friday: Japan National Core CPI, U.K. Retail Sales, U.S. Michigan Consumer Sentiment

Weekend news about the renewed closure of the Strait of Hormuz is likely to create a busy start to the week and reduce hopes that the conflict in Iran will end quickly. Markets are expected to stay focused on WTI price moves and react quickly to new headlines. U.S. retail sales and consumer confidence may also affect sentiment, as traders watch whether higher oil prices are starting to hurt the consumer outlook and broader economic expectations.

Eco Data 4/20/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 698M | 175M | -257M | -365M |

| 01:00 | CNY | 1-y Loan Prime Rate | 3.00% | 3.00% | 3.00% | |

| 01:00 | CNY | 5-y Loan Prime Rate | 3.50% | 3.50% | 3.50% | |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | -0.40% | -0.40% | 1.70% | 2.00% |

| 06:00 | EUR | Germany PPI M/M Mar | 2.50% | 1.40% | -0.50% | |

| 06:00 | EUR | Germany PPI Y/Y Mar | -0.20% | -3.30% | ||

| 12:30 | CAD | CPI M/M Mar | 0.90% | 1.10% | 0.50% | |

| 12:30 | CAD | CPI Y/Y Mar | 2.40% | 2.50% | 1.80% | |

| 12:30 | CAD | CPI Median Y/Y Mar | 2.30% | 2.40% | 2.30% | |

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 2.20% | 2.30% | 2.30% | |

| 12:30 | CAD | CPI Common Y/Y Mar | 2.60% | 2.60% | 2.40% | |

| 14:30 | CAD | BoC Business Outlook Survey |

| 22:45 | NZD |

| Trade Balance (NZD) Mar | |

| Actual | 698M |

| Consensus | 175M |

| Previous | -257M |

| Revised | -365M |

| 01:00 | CNY |

| 1-y Loan Prime Rate | |

| Actual | 3.00% |

| Consensus | 3.00% |

| Previous | 3.00% |

| 01:00 | CNY |

| 5-y Loan Prime Rate | |

| Actual | 3.50% |

| Consensus | 3.50% |

| Previous | 3.50% |

| 04:30 | JPY |

| Tertiary Industry Index M/M Feb | |

| Actual | -0.40% |

| Consensus | -0.40% |

| Previous | 1.70% |

| Revised | 2.00% |

| 06:00 | EUR |

| Germany PPI M/M Mar | |

| Actual | 2.50% |

| Consensus | 1.40% |

| Previous | -0.50% |

| 06:00 | EUR |

| Germany PPI Y/Y Mar | |

| Actual | -0.20% |

| Consensus | |

| Previous | -3.30% |

| 12:30 | CAD |

| CPI M/M Mar | |

| Actual | 0.90% |

| Consensus | 1.10% |

| Previous | 0.50% |

| 12:30 | CAD |

| CPI Y/Y Mar | |

| Actual | 2.40% |

| Consensus | 2.50% |

| Previous | 1.80% |

| 12:30 | CAD |

| CPI Median Y/Y Mar | |

| Actual | 2.30% |

| Consensus | 2.40% |

| Previous | 2.30% |

| 12:30 | CAD |

| CPI Trimmed Y/Y Mar | |

| Actual | 2.20% |

| Consensus | 2.30% |

| Previous | 2.30% |

| 12:30 | CAD |

| CPI Common Y/Y Mar | |

| Actual | 2.60% |

| Consensus | 2.60% |

| Previous | 2.40% |

| 14:30 | CAD |

| BoC Business Outlook Survey | |

| Actual | |

| Consensus | |

| Previous | |

Diplomacy or Return to Conflict? Hormuz Closes Again, Oil Signals Path Into Ceasefire Cliff

The market narrative has flipped again—and the stakes are rising. The abrupt shift in the Strait of Hormuz—from briefly “open” to once again under strict military control within 24 hours—has underscored just how fragile the current ceasefire is. What initially looked like the beginning of de-escalation has quickly reverted to uncertainty, forcing investors to reassess whether the “peace trade” was premature, just as a critical deadline approaches.

After Iranian officials initially declared the Strait fully open for commercial shipping, the situation reversed sharply. Military control has been reimposed, and reports of direct confrontation—including incidents involving commercial vessels—have effectively ended any near-term assumption of safe passage.

At the core of the standoff is a breakdown in trust between Washington and Tehran. The U.S. has maintained its naval blockade on Iranian ports, insisting it will remain in place until a broader agreement is reached. Iran, in turn, has framed the blockade as a violation of ceasefire conditions and responded by tightening control over the Strait, linking any reopening to the restoration of “complete freedom of navigation.”

This dynamic has created a precondition deadlock that complicates the prospects for upcoming talks. While reports suggest another round of negotiations could take place on Monday, there is still no formal confirmation. Even if talks proceed, they are likely to unfold under significant tension, with both sides entering from hardened positions.

The broader risk is that time is running out. If no progress is made before the ceasefire expires on April 22, the probability of renewed hostilities rises sharply. That could include a return to direct military confrontation or escalation at strategic chokepoints like Hormuz.

For markets, this makes the coming days critical—not just for geopolitics, but for the direction of oil, inflation expectations, and global risk sentiment.

In this environment, oil remains the ultimate signal. Its ability—or failure—to break decisively lower will determine whether markets continue to lean toward diplomacy or begin to price in a return to conflict. With the ceasefire cliff approaching, that signal will become increasingly important. At the same time, key technical levels across major assets will help guide traders in assessing whether underlying market sentiment is truly shifting, or simply reacting to headline volatility.

Oil: Still the Ultimate Signal for Global Sentiment

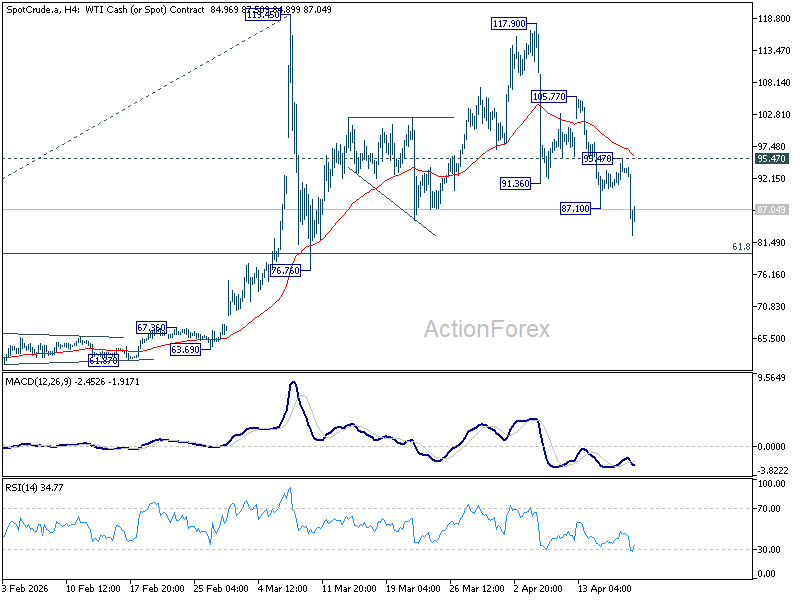

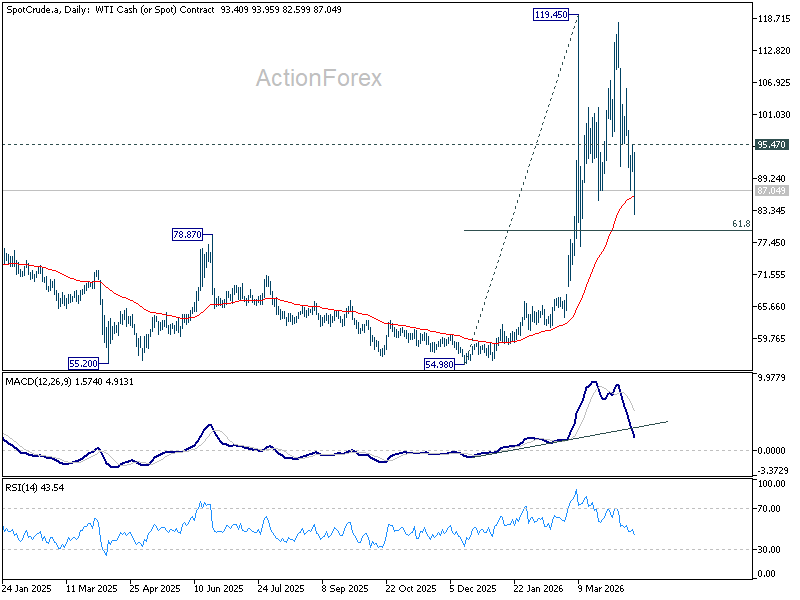

Oil remains the most important driver of global market sentiment. WTI’s decline from 117.90 resumed last week, extending sharply lower to as low as 82.59. While further downside is favored in the near term, a decisive break of the 61.8% retracement of 54.98 to 119.45 at 79.60 would likely require a more durable de-escalation in the Middle East—potentially including a confirmed and sustained normalization of the Strait of Hormuz. Absent that, the psychological 80 level should act as a near-term floor.

Meanwhile, as long as 95.47 resistance holds, the bias remains to the downside. In other words, while volatility may persist, there is no clear signal of a renewed US-Iran escalation as long as this cap remains intact.

Equities: New Records as Uptrend Reumes

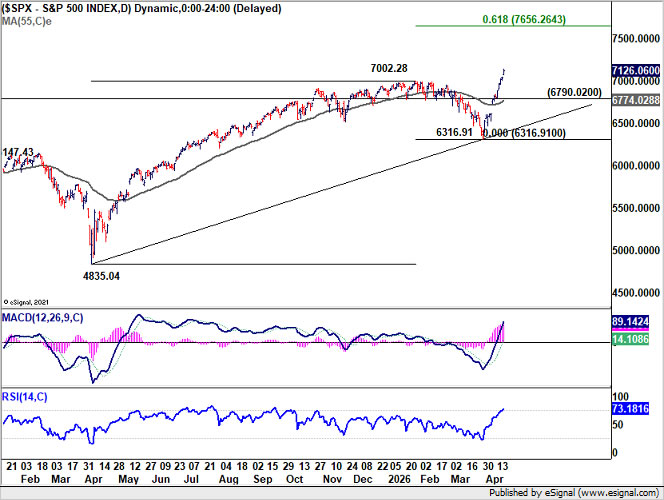

S&P 500 resumed its uptrend last week, breaking above 7,002.28 resistance and closing at a fresh record high of 7,126.06. While near-term volatility or a pullback cannot be ruled out given geopolitical uncertainty, the outlook remains bullish as long as 6,790.02 support holds. The current advance continues to target 61.8% projection of 4,835.04 to 7,002.28 from 6,316.91 at 7,656.26.

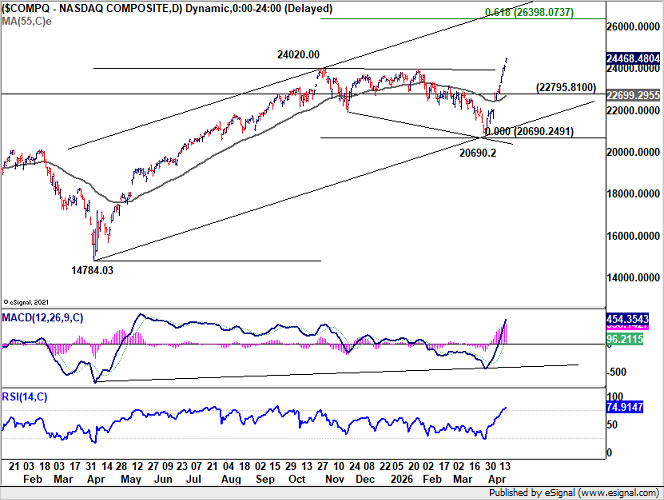

NASDAQ shows a similar structure, ending the week at a new record of 24,468.48. Near-term outlook remains bullish as long as 22,795.81 support holds, even in the event of a retreat. The broader uptrend targets 61.8% projection of 14,784.03 to 24,020.00 from 20,690.2 at 26,398.07 next.

Yields: At Key Support, Rebound or Breakdown Ahead

US 10-year yield’s pullback from the 4.484 short-term top remains corrective so far, suggesting that the rise from 3.956 is not yet complete. Yields are now testing a key support cluster, including 55 D EMA (now at 4.240), 50% retracement of 3.956 to 4.484 at 4.220, and 55 W EMA (now at 4.219).

A strong rebound from this zone, followed by a break above 4.351 resistance, would signal that the rise from 3.956 is ready to resume through 4.484 high. On the downside, firm break below 4.220 would open the way for a deeper pullback toward 61.8% retracement at 4.157 and below.

Dollar Index: Bearish Bias Intact Below Key EMA

Dollar Index’s break below 98.49 support last week suggests that the rebound from 95.55 has already completed. More importantly, rejection below 38.2% retracement of 110.17 to 95.55 at 101.13, combined with failure at the 55 W EMA (now at 99.57), keeps the medium-term outlook bearish.

Further downside is favored as long as 55 D EMA (now at 98.86) caps any recovery, with focus on a retest of the 95.55 low. While a break below that level is not yet the base case, it will depend on the momentum of the next leg lower.

Conversely, sustained move above 55 D EMA would suggest that the rebound from 95.55 is not yet complete, opening the way for another test of 100.64 and potentially the 101.13 Fibonacci level.

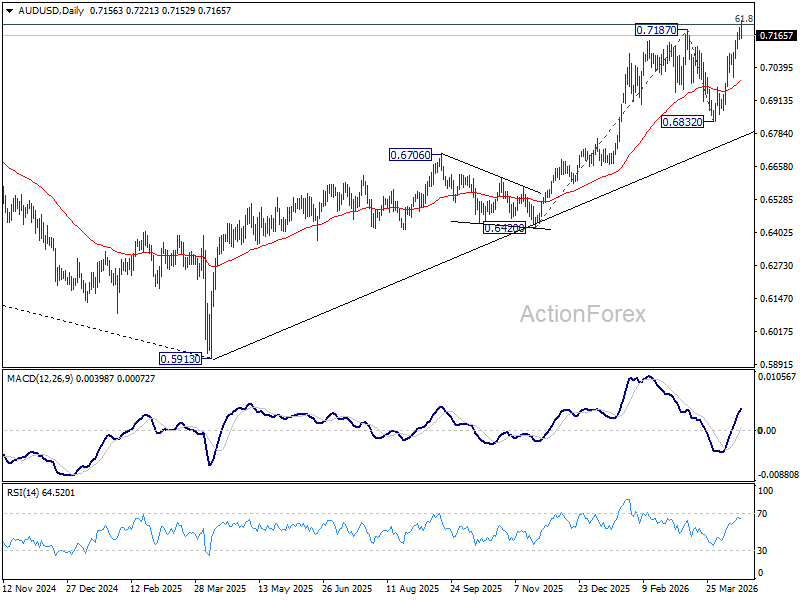

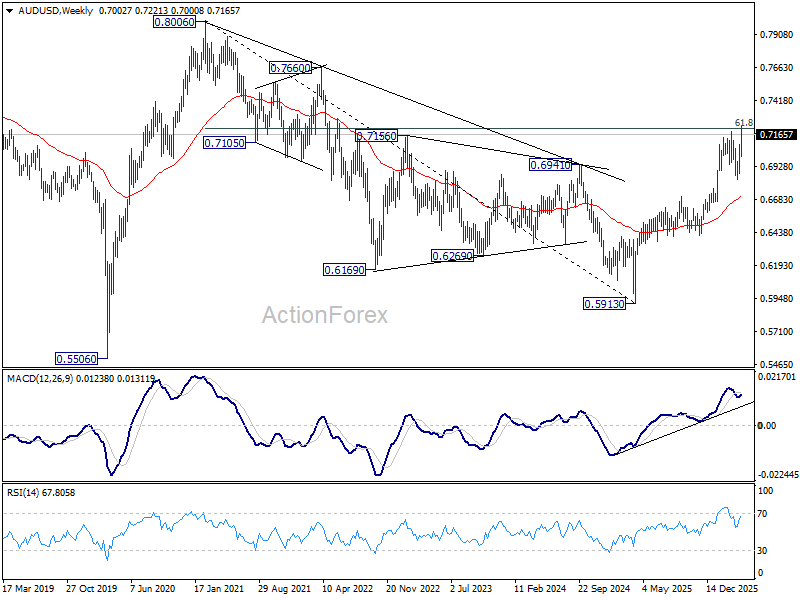

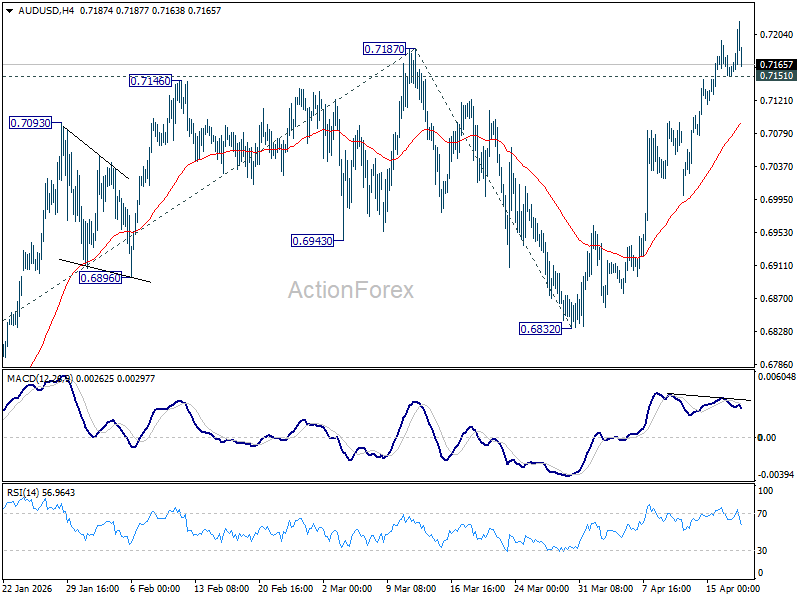

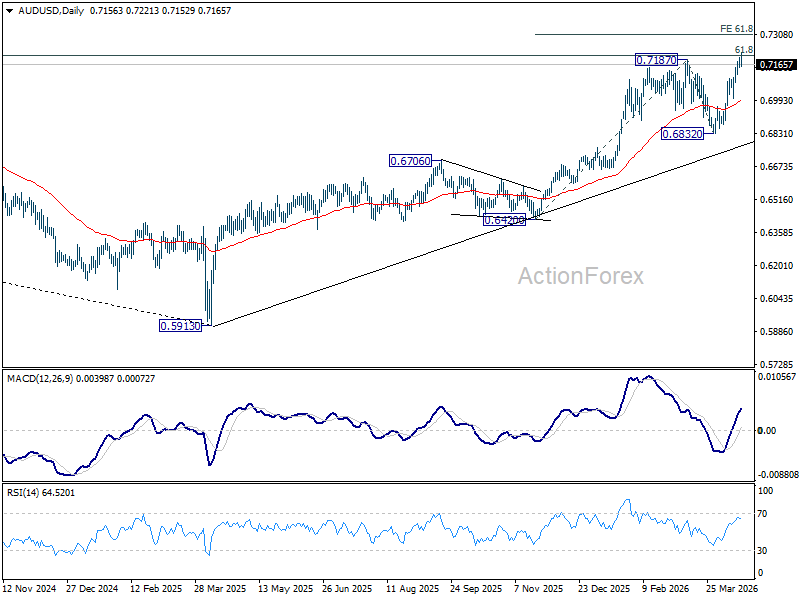

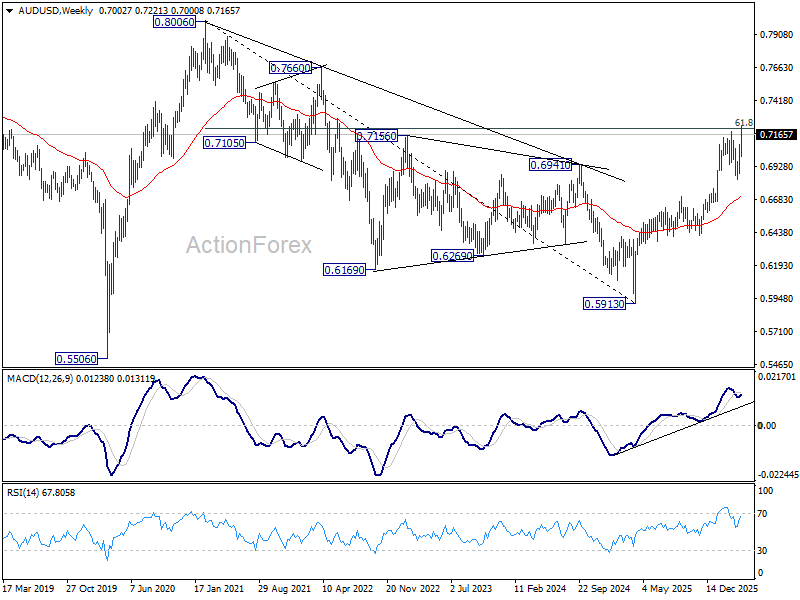

AUD/USD: Breakout Structure to Build Above 0.72

AUD/USD was the top performer last week, gaining 1.46%. While some near-term consolidation is possible after rejection at 0.72 handle on the first attempt, the broader outlook remains bullish as long as 55 D EMA (now at 0.6985) holds.

More importantly, decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's reversing the down trend from 0.8006 (2021 high), rather than correcting it. That should pave the way to retest 0.8006 at least.

EUR/USD Weekly Outlook

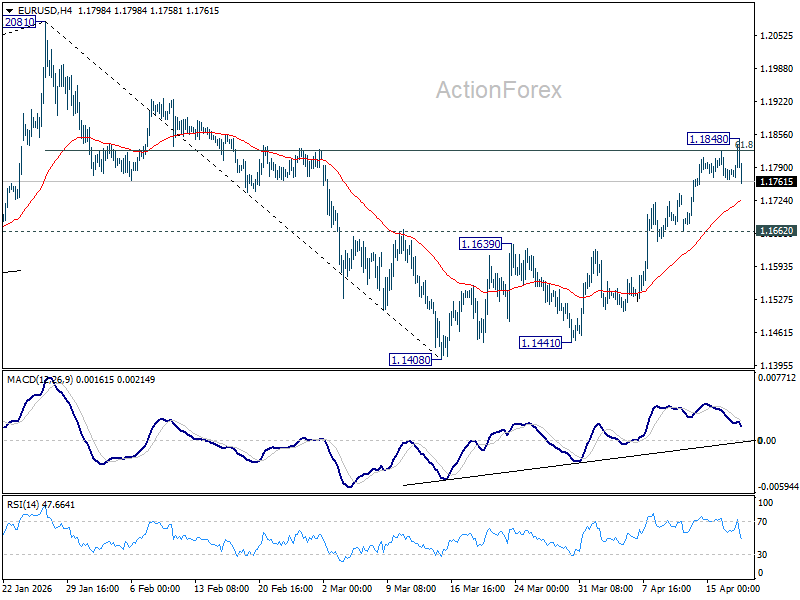

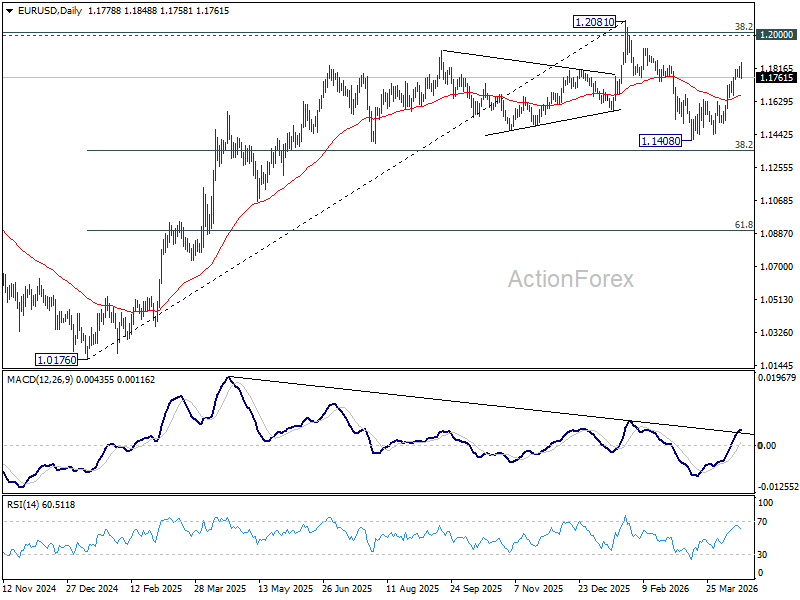

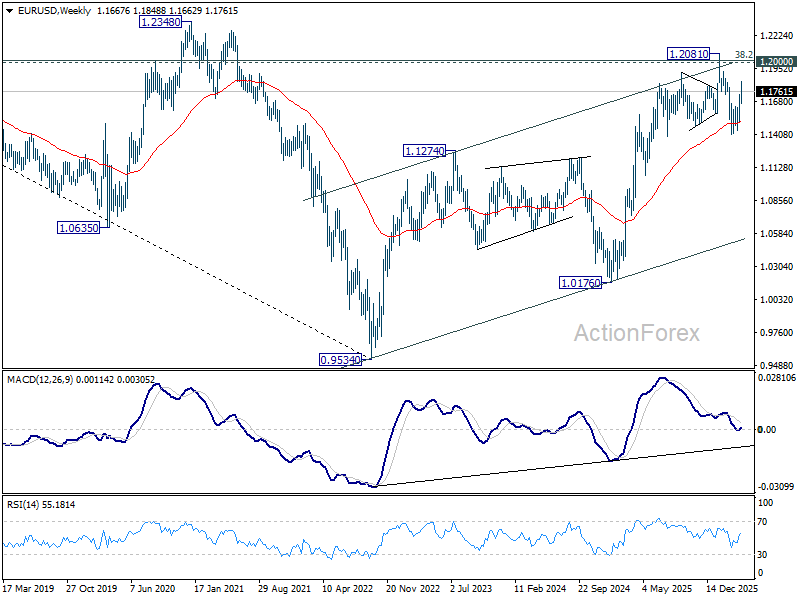

EUR/USD's rise from 1.1408 extended higher to 1.1848 last week, but failed to take out 61.8% retracement of 1.2081 to 1.1408 at 1.1824 decisively. Initial bias is turned neutral this week first. On the upside, sustained trading above 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will bring deeper decline back towards 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

EUR/USD Weekly Outlook

EUR/USD's rise from 1.1408 extended higher to 1.1848 last week, but failed to take out 61.8% retracement of 1.2081 to 1.1408 at 1.1824 decisively. Initial bias is turned neutral this week first. On the upside, sustained trading above 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will bring deeper decline back towards 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

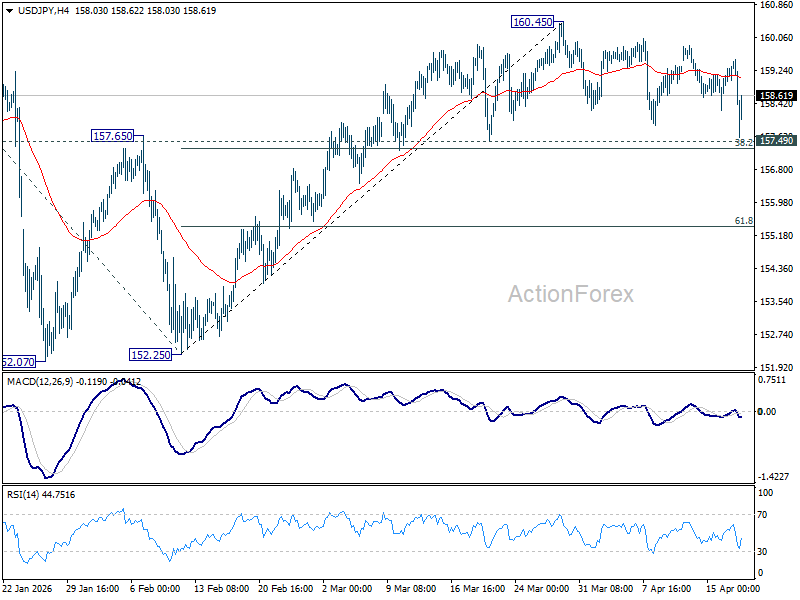

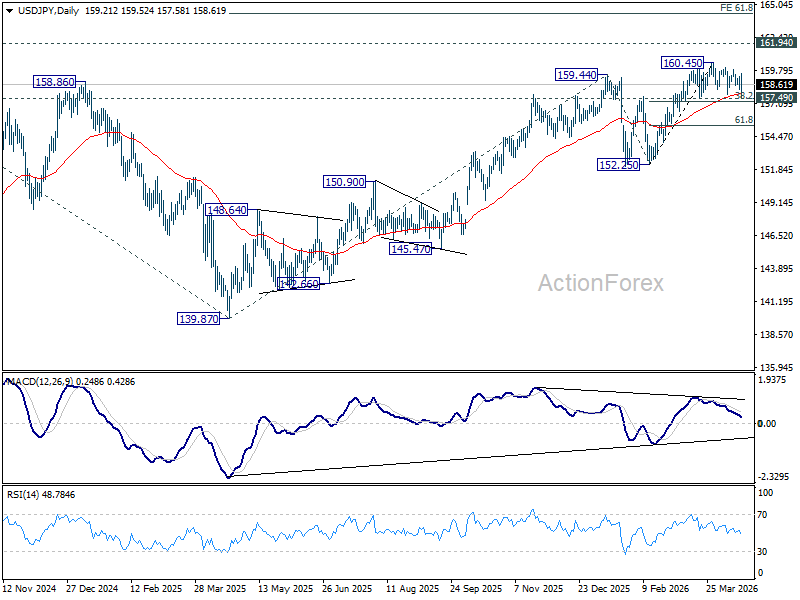

USD/JPY Weekly Outlook

USD/JPY experienced some high volatility last week but after all, it's still bounded in range trading below 160.45. Initial bias stays neutral this week first. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.61) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

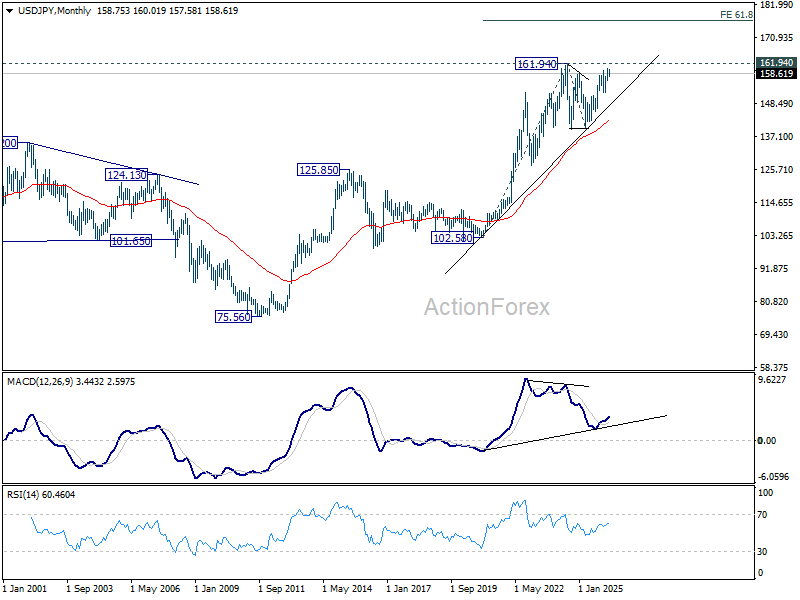

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resume. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.

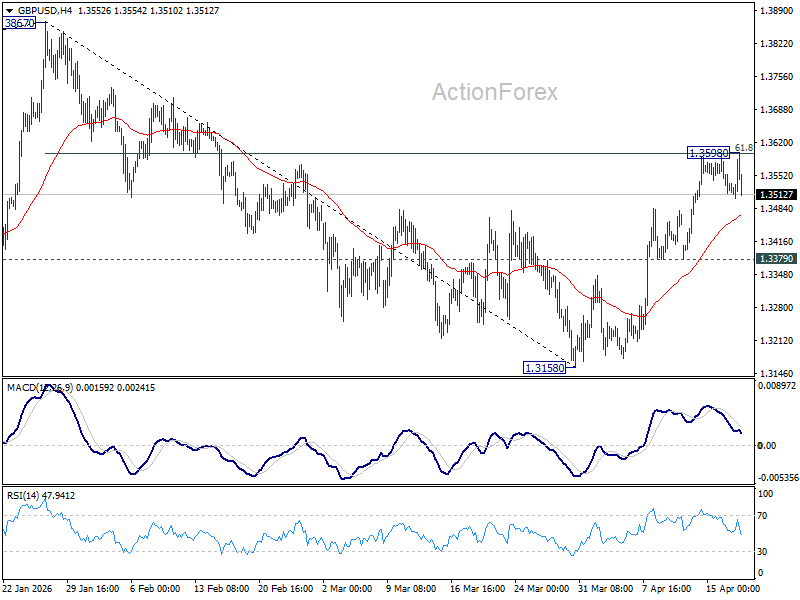

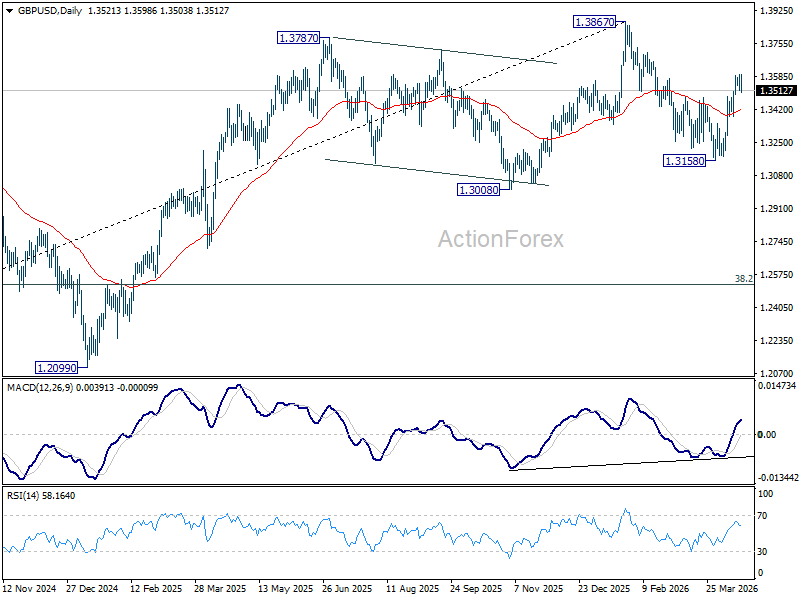

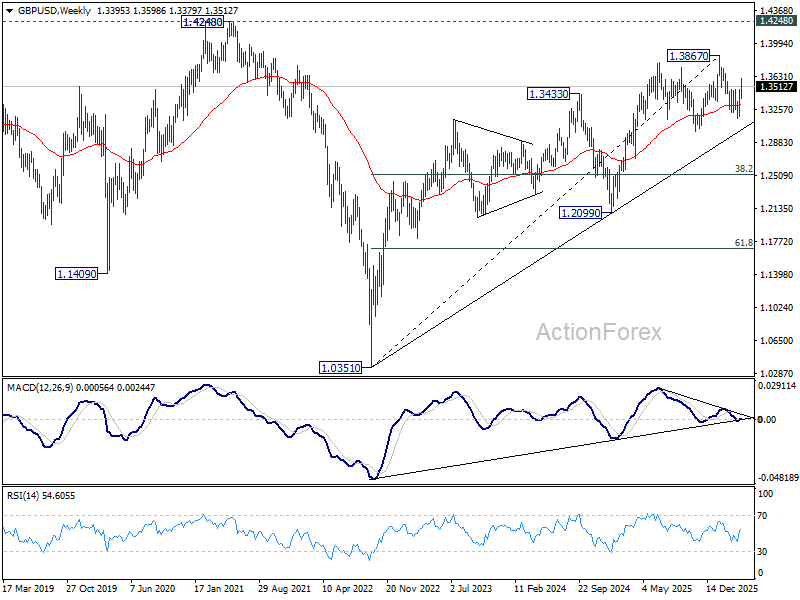

GBP/USD Weekly Outlook

GBP/USD's rebound from 1.3158 extended higher last week but failed to break through 61.8% retracement of 1.3867 to 1.3158 at 1.3596 decisively. Initial bias remains neutral this week first. On the upside, sustained break of 1.359 will pave the way to retest 1.3867 high. However, firm break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.0351 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

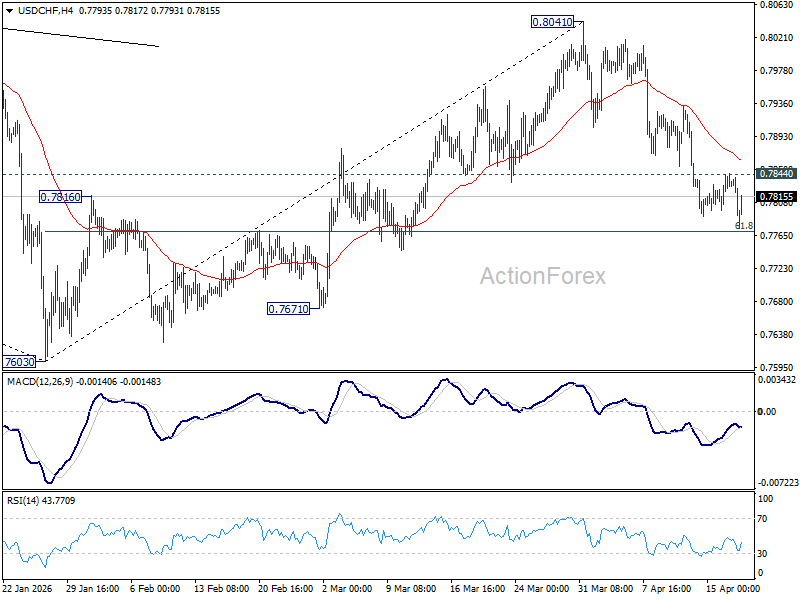

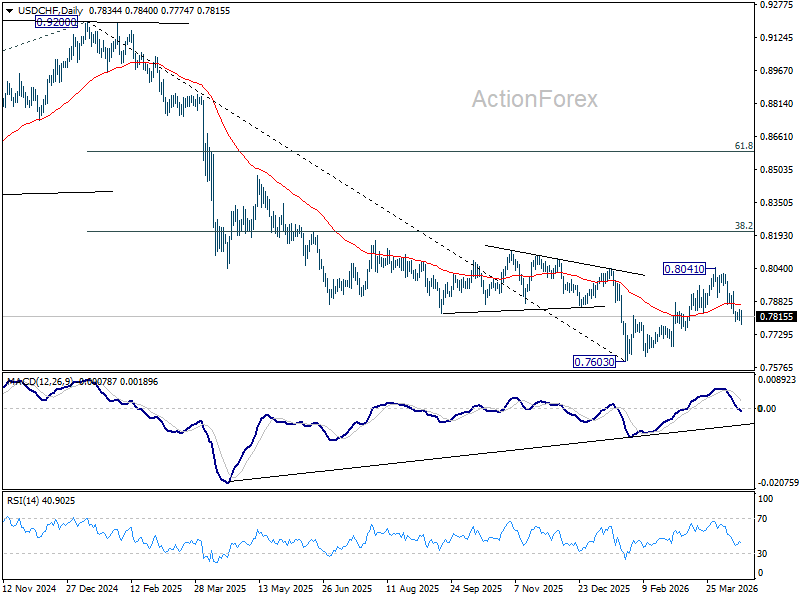

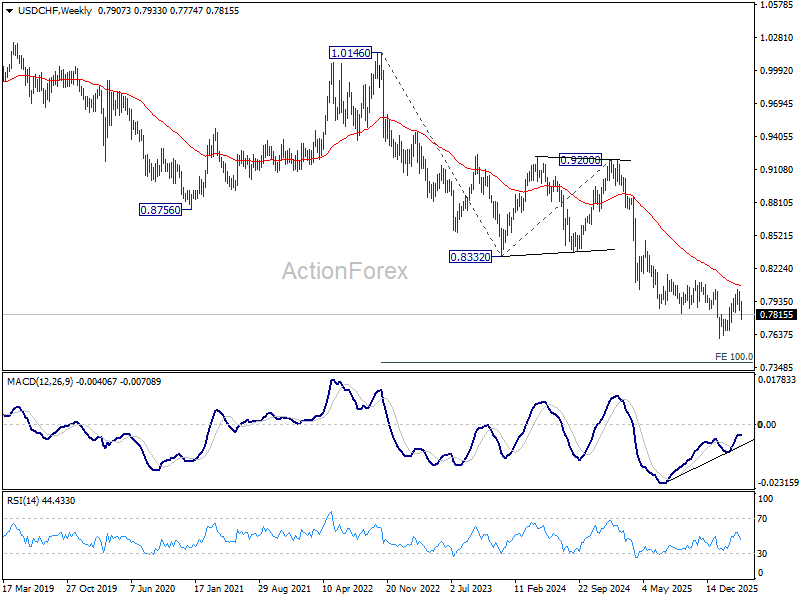

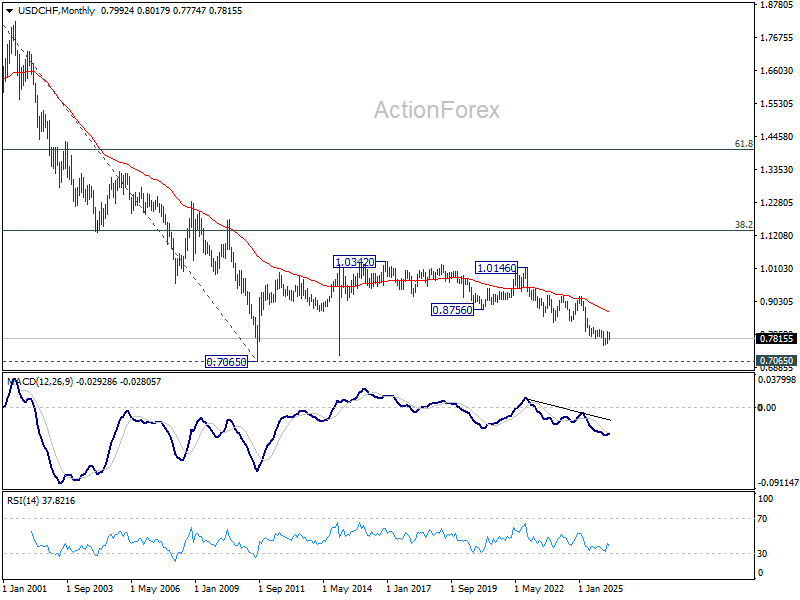

USD/CHF Weekly Outlook

USD/CHF's extended fall last week argues that rebound from 0.7603 has completed as a corrective move to 0.8041. Initial bias stays on the downside this week. Sustained break of 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will pave the way to retest 0.7603 low. On the upside, above 0.7844 minor resistance will turn intraday bias neutral first.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8068) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

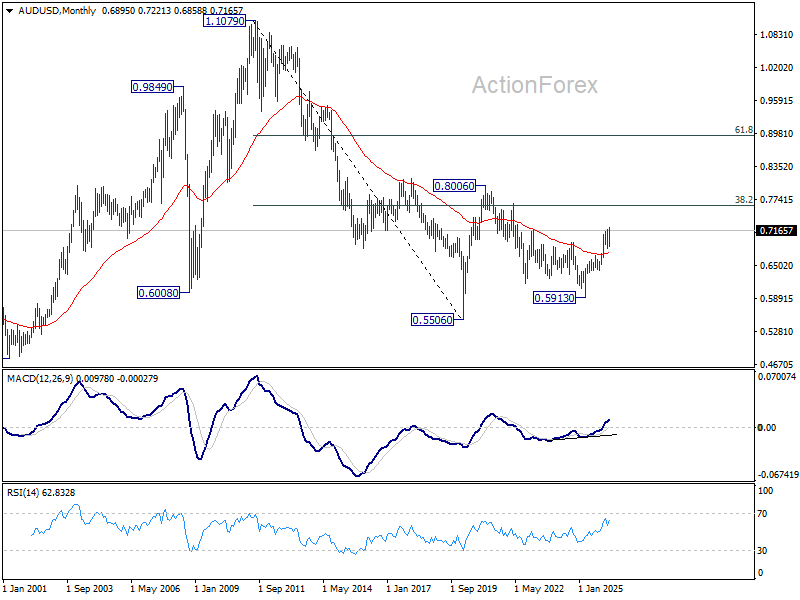

AUD/USD Weekly Report

AUD/USD's up trend resumed by breaking through 0.7187 last week. Initial bias stays on the upside this week for 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. On the downside, below 0.7151 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above. This will remain the favored case as long as 55 W EMA (now at 0.6714) holds.

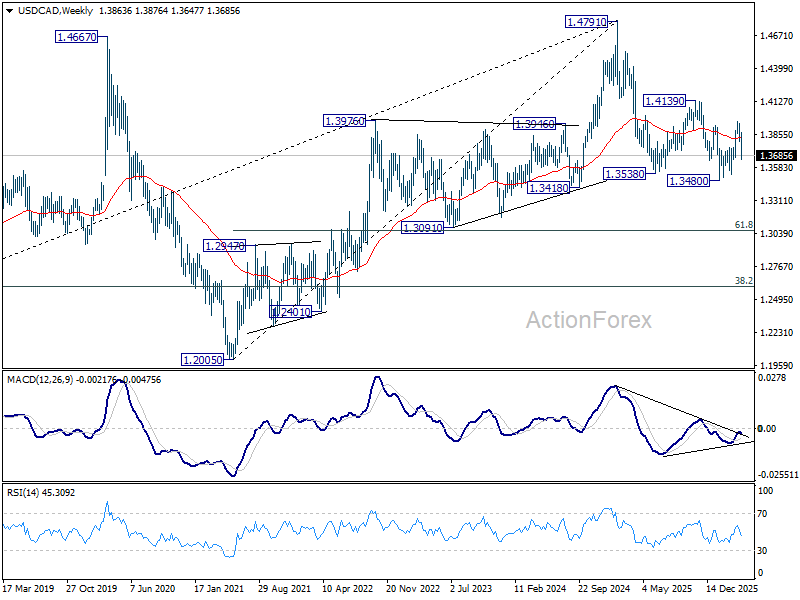

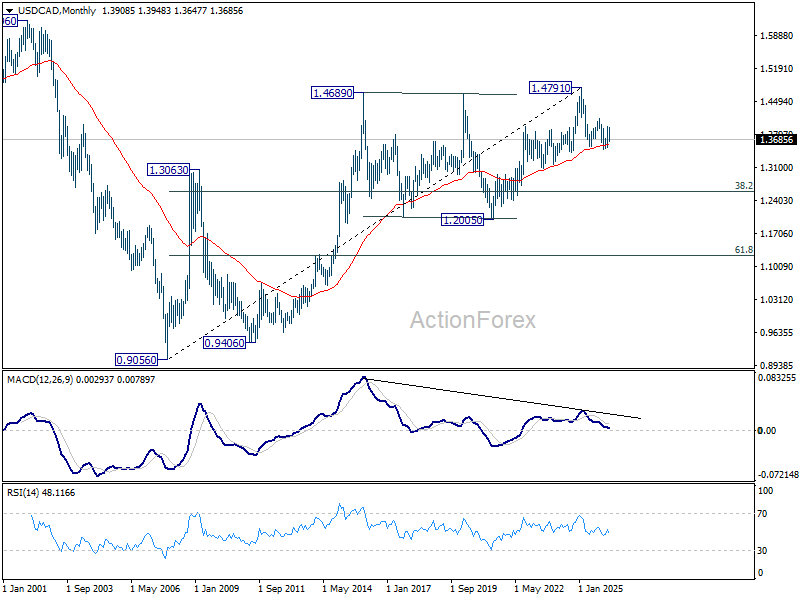

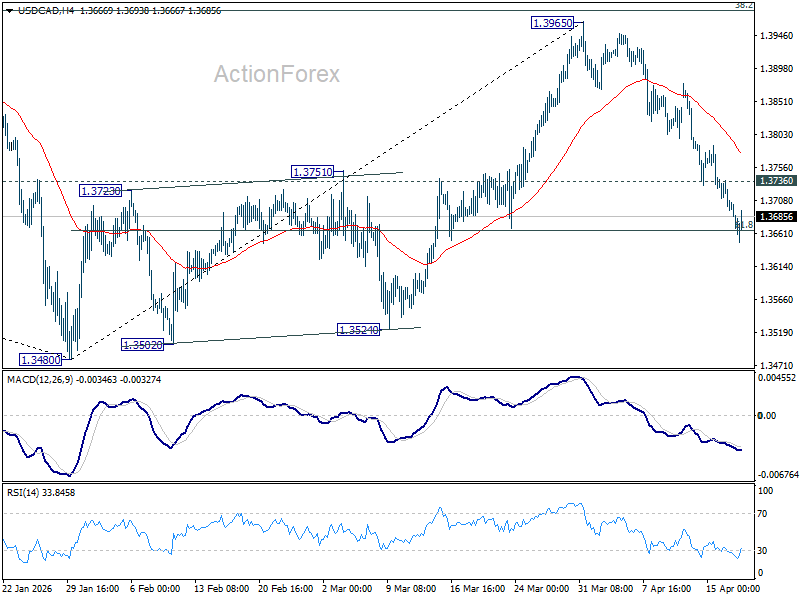

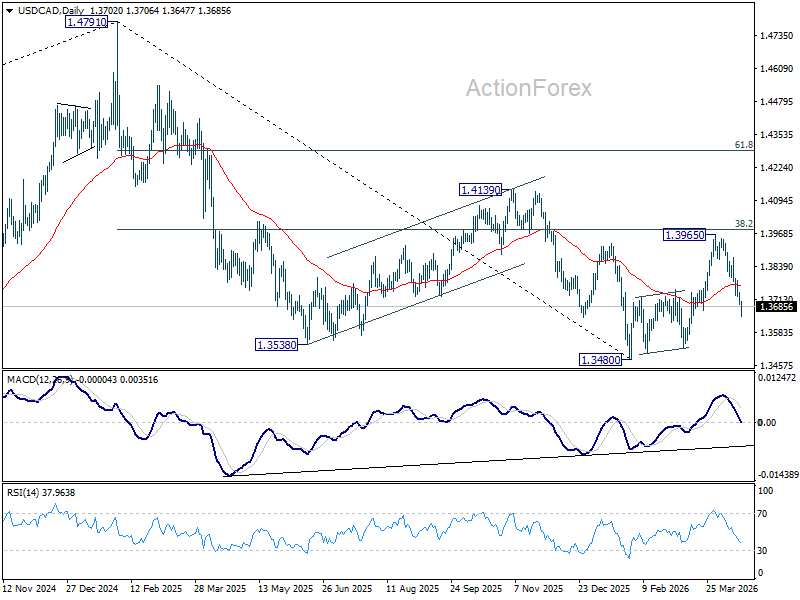

USD/CAD Weekly Outlook

USD/CAD's extended decline last suggests that rise from 1.3480 has completed with three waves up to 1.3965. Initial bias stays on the downside this week. Sustained break of 61.8% retracement of 1.3480 to 1.3965 at 1.3665 will pave the way to retest 1.3480 low. On the upside, above 1.3736 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

In the long term picture, rising 55 M EMA (now at 1.3590) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.