Sample Category Title

Canada Inflation Jumps to 2.4% yoy in March, Gasoline Prices Up Record 21.2% mom

Canada’s inflation picked up in March as CPI rose from 1.8% yoy to 2.4% yoy, driven largely by a sharp rebound in energy prices, but missed expectation of 2.5% yoy. On a monthly basis, CPI increased 0.9% mom, also below expectation of 1.1% mom. Higher fuel costs linked to the Middle East conflict pushed headline inflation higher, offsetting softer underlying trends.

Energy was the dominant driver. Prices surged 13.1% mom on the month and swung from a -9.3% yoy decline in February to a 3.9% yoy increase. Gasoline led the move, rising 21.2% mom—the largest monthly increase on record—and 5.9% yoy, reflecting supply disruptions tied to geopolitical tensions. Fuel oil and other fuels also climbed sharply, up 26.1% yoy.

Despite the headline strength, underlying inflation pressures showed signs of easing. Excluding gasoline, CPI rose at a slower annual pace of 2.2% yoy compared with 2.4% yoy previously, suggesting that domestic price momentum remains contained for now. Even so, CPI common—a key core measure—accelerated from 2.4% yoy to 2.6% yoy, indicating that some underlying pressures are still building.

The data reinforces a familiar pattern: energy shocks are pushing headline inflation higher, while core trends remain more mixed. For the Bank of Canada, the key question will be whether these price increases begin to spill over into broader components. If second-round effects emerge, the current balance could shift quickly, complicating the policy outlook in the months ahead.

Crypto Market Has Taken a Step Back, While Remaining in an Uptrend

Market Overview

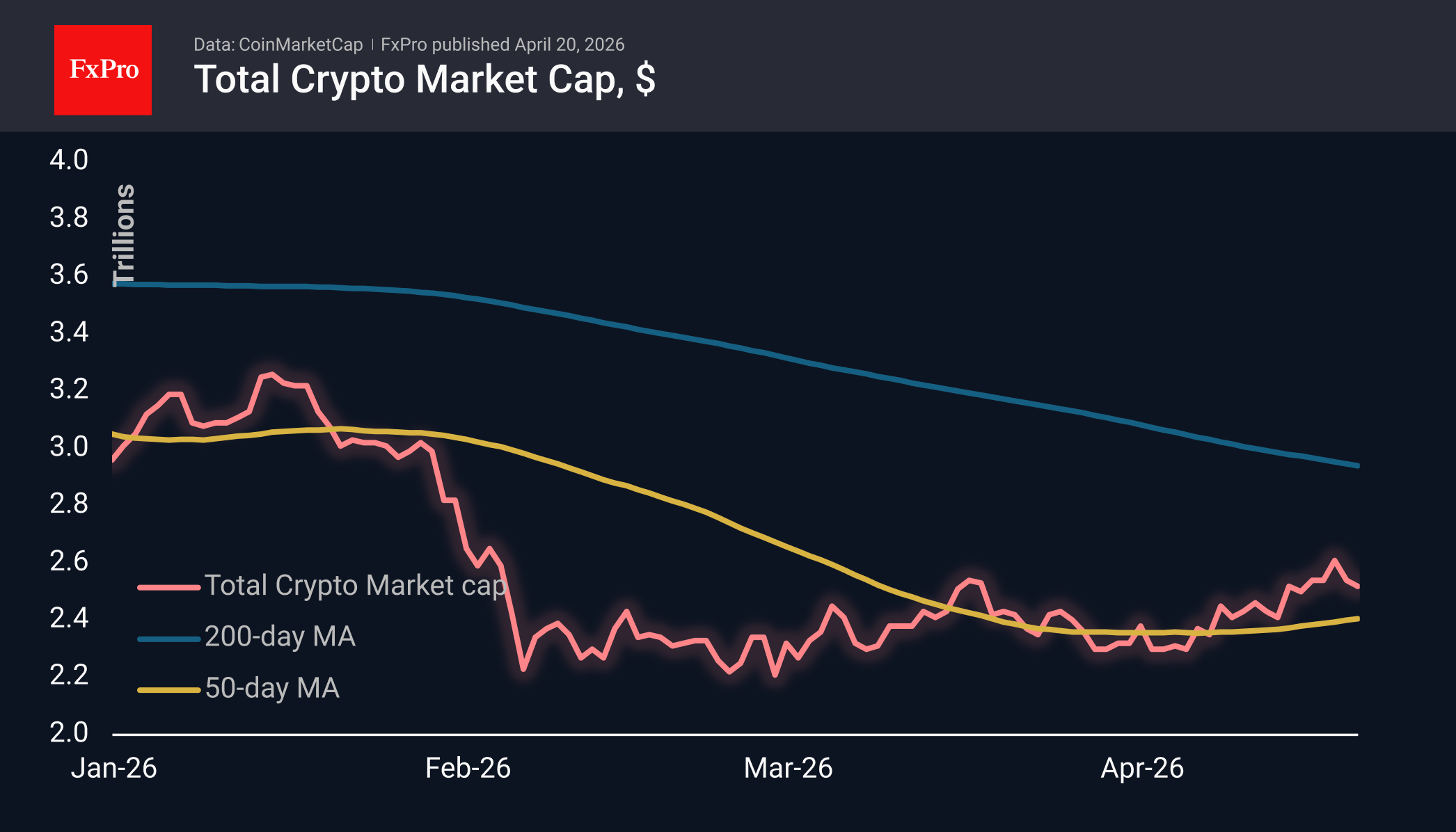

The cryptocurrency market capitalisation stands at $2.53T, down 0.81% over the past 24 hours but up 5% over the past week. The day’s top performers were SUSHI (+2.5%), IOTA (+2%) and NEAR (+2%). Among the underperformers were ZEC (−4.1%), ALGO (−2.5%) and ETH (−0.4%). The Fear and Greed Index rose to 29 points — its highest level since 28 January.

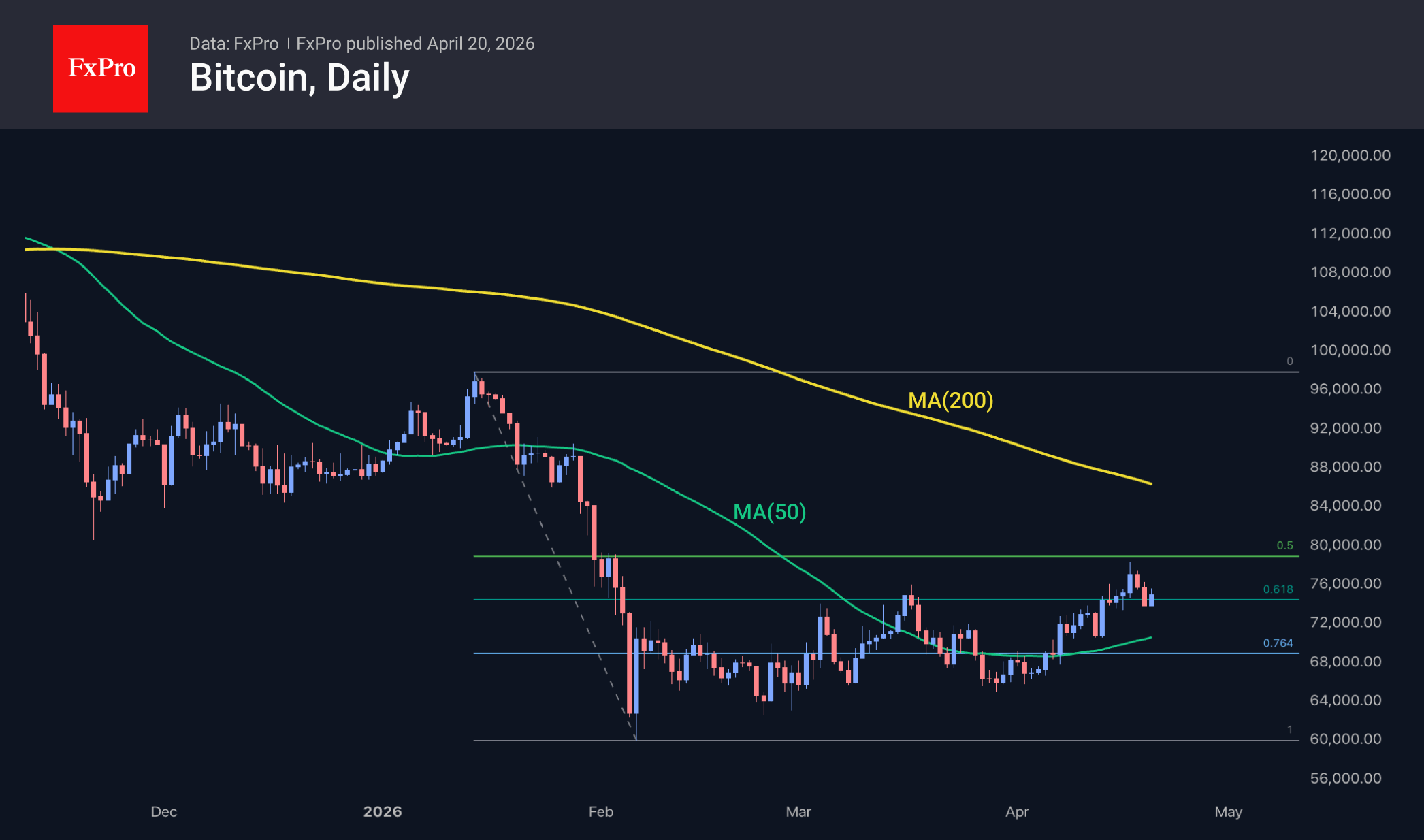

Bitcoin is trading just below $75K on Monday morning, having retreated from last week’s highs above $78K. For now, we view the current movement as a pullback within an uptrend, rather than a reversal back to a downtrend. The pressure on the leading cryptocurrency is linked to negative reactions in stock markets to news about Iran, which has reduced risk appetite. BTC has lagged significantly behind equities in recent days, building up potential but not yet rushing to realise it.

News Background

According to SoSoValue, net inflows into spot BTC ETFs rose to $996.4 million. Net weekly inflows into US spot Ethereum ETFs totalled $275.8 million.

According to Glassnode, positioning in the options market remains uncertain. Nexo confirms the contradiction: the rally is gaining momentum, but the derivatives market does not believe in it.

Bitcoin’s return above $75,000 is met with scepticism: funding rates on perpetual futures have remained in negative territory for around 46 consecutive days, notes Bloomberg. This is one of the longest periods of bearish sentiment in the history of derivatives, comparable only to the aftermath of the FTX crypto exchange collapse in late 2022.

Traders are actively building up short positions, betting against a breakout. This creates conditions under which a short squeeze becomes more likely should the upward momentum persist, notes K33 Research. A break above $76,000 could send BTC towards $85,000, suggests Kaiko.

According to TheEnergyMag, public mining companies sold a record 32,000 BTC in the first quarter amid a record-low hash rate. This is more than in the whole of 2025. The figure also exceeds the second-quarter 2022 data, when miners liquidated 20,000 BTC following the collapse of the Terra (LUNA) ecosystem.

As a result of the latest adjustment, Bitcoin’s mining difficulty fell by 2.43% to 135.59 T. According to Glassnode, the BTC network’s hash rate, smoothed by a 7-day moving average, has recovered from ~978 EH/s to ~992 EH/s since the start of the month.

XAU/USD: Gold Price Drops on Renewed Geopolitical Tensions and Stronger Dollar

Gold opened with gap-lower on Monday, hitting levels around $150 lower from Friday’s high, as sentiment changed again on escalation over the weekend that resulted in closure of Hormuz strait.

Fresh negative developments on the ground faded optimism and revived fears about inflation and other factors surrounding war environment, with higher dollar and oil prices.

Technical picture, however, did not change significantly after Friday’s / today swings, as the price still holds above significant support at $4759 (broken Fibo 50% of $5419/$4099, reinforced by 10DMA), which marks the floor of near-term range (that extends into fifth consecutive session).

Near-term action is likely to remain in sideways mode while range boundaries ($4759 / $4891 -55DMA) hold, with conflicting indicators on daily chart (MAs in predominantly bullish configuration, countered by weaker momentum studies / price weighed by daily cloud).

Markets will be looking for a fresh catalyst from dynamics in geopolitical picture, with violation of current range boundaries to generate initial direction signals.

In the negative scenario, violation of $4759 pivot would weaken near-term structure and risk acceleration towards supports at $4700 (round-figure), $4663 (20DMA) and $4603 (broken Fibo 38.2%).

Conversely, break of $4891 and nearby $4915 (Fibo 61.8%) would unmask psychological $5000 barrier.

Res: 4871; 4891; 4915; 5000.

Sup: 4759; 4700; 4663; 4603.

Oil Surges 6% as Sentiment Sours, Nikkei Rises. US-Iran Developments in Focus

- Geopolitical tensions between the US and Iran escalated over the weekend, causing market sentiment to dive.

- The US dollar reclaimed its footing, hitting a one-week high as the optimistic "peace deal" narrative crumbled.

- The immediate market direction hinges on diplomatic efforts ahead of Tuesday’s ceasefire deadline.

- The overall outlook anticipates the DXY to maintain a defensive posture.

Market sentiment took a dive this morning after weekend tensions between Iran and the US reared its head once more.

The ceasefire remains fragile and will be tested at the start of the week after the US seized an Iranian cargo ship and traffic through the Strait of Hormuz remained largely halted. President Donald Trump struck a cautiously optimistic tone, suggesting that Iran has committed to keeping the Strait of Hormuz open.

Despite the "completely open" announcement made on Friday, market sentiment was quickly dampened by reports of the Islamic Revolutionary Guard Corps (IRGC) targeting tankers within 24 hours of the statement. This immediate escalation serves as a grim reminder that while political agreements provide a temporary reprieve, the operational risks in the region remain elevated.

The impact from these developments saw oil prices rise more than 6% in early Monday trade. Gold on the other hand opened around $40 down from its Friday close before dropping to a daily low around the 4737 mark. The precious metal ground its way back toward the $4800/oz mark which seems to be the immediate hurdle to cross and gain acceptance above for a move higher.

All in all risk assets are lower, one of the few exceptions being Japan's Nikkei share average which rose on the day. The benchmark Nikkei 225 Index rose 0.60% to close at 58,824.89 compared with its record intraday level of 59,688.10 touched on Thursday. The broader Topix climbed 0.43% to 3,777.02.

Dollar Finds Support on Safe-Haven Bid

The US dollar reclaimed its footing on Monday, hitting a one-week high against a basket of major peers as the optimistic "peace deal" narrative began to crumble.

The catalyst for the greenback's resurgence stems from Tehran’s refusal to participate in a second round of negotiations, casting significant doubt on the longevity of the two-week ceasefire set to expire this Tuesday.

The shift in sentiment was felt across the G10 space, with high-beta and risk-sensitive currencies bearing the brunt of the move:

Euro (EUR/USD): The single currency slipped 0.05% to $1.1754, having earlier touched a weekly low of $1.1729.

Sterling (GBP/USD): Cable followed suit, trading 0.15% lower at $1.3497 as the broader "risk-off" mood took hold.

Aussie (AUD/USD): The most sensitive to shifts in global stability, the Australian dollar dropped 0.3% to $0.7145.

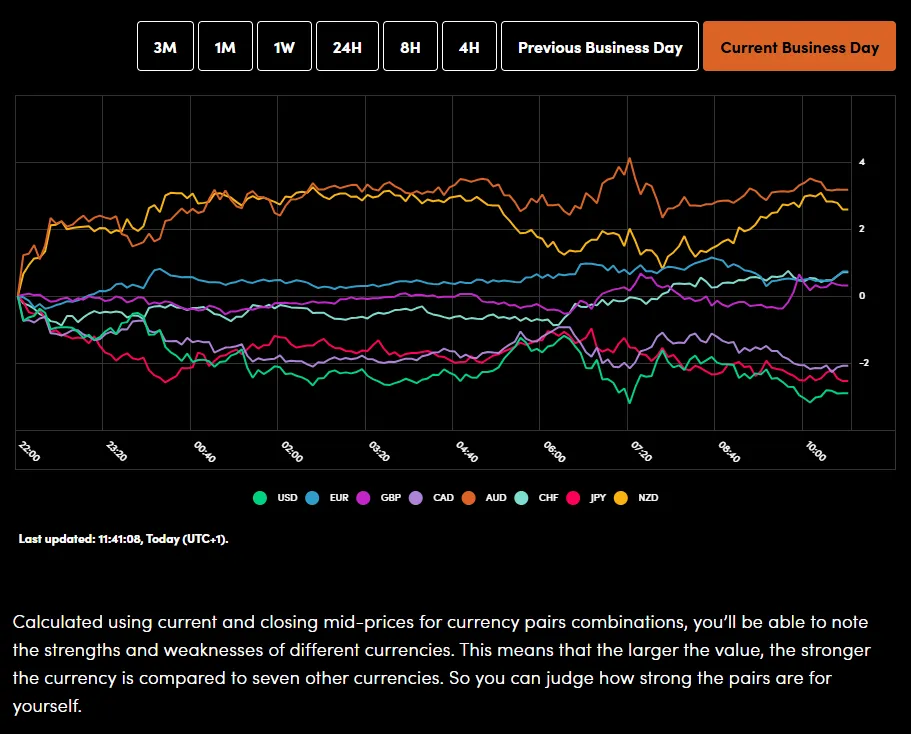

Currency Power Balance

Source: OANDA Labs

European Open: Geopolitical risk roils markets

European equities began the week on a negative note, with the STOXX 50 down 1.3% and the STOXX 600 falling 0.9%.

Travel and leisure stocks fell sharply, with Ryanair tumbling 3.5% while energy outperformed, including Shell (2.5%).

US stock index futures inched lower while the CBOE Volatility Index .VIX, known as Wall Street's "fear gauge", gained after falling for the last eight sessions and was last up 2.25 points at 19.73, a one-week high.

Looking Ahead

The immediate market direction hinges on whether the diplomatic efforts in Pakistan yield a breakthrough or if the "tough talk" escalates ahead of tomorrow’s ceasefire deadline. The key barometer for progress will be the physical presence of Iranian negotiators. While the current "market mood music" remains anxious, there is a subtle undercurrent of hope for a resolution that could spark a relief rally in risk assets.

Tuesday’s Triple Threat: Warsh, Ceasefires, and Retail Sales Tomorrow stands as the pivotal session for the week, defined by three key catalysts:

- The Ceasefire Deadline: Expiration without a deal could reignite a sharp flight to safety.

- Kevin Warsh’s Confirmation: His Senate hearing for the Fed Chair role will be scrutinized. Expect a "split personality" approach: dovish on interest rates but hawkish on shrinking the Fed's balance sheet.

- US Retail Sales (March): Expected to remain resilient despite the energy tax on consumers, reinforcing the "higher for longer" narrative.

Chart of the Day - DXY

The US Dollar Index (DXY) is currently attempting to claw back recent losses, trading near the 98.24 handle after a sharp decline earlier this month. On the H4 chart, the index has found strong structural support around the 97.70 level, where a series of "BULL" signals and RSI divergence suggest a near-term bottom may be in place.

Key Levels to Watch:

- Resistance: Immediate upside pressure faces a stern test at 98.73 (red horizontal). A break above this could see the index rally toward the 99.21 (100-SMA) and 99.35 (200-SMA) confluence zone.

- Support: The 97.70 area remains the critical floor. A daily close below this pivot would invalidate the current recovery and open the door for a move toward the 97.00 psychological mark.

With the RSI (14) rising from oversold territory and currently at 48.65, momentum is shifting back to the bulls. However, until the DXY reclaims its moving averages, the broader bias remains neutral to bearish.

USD Index Four-Hour Chart, April 20, 2026

Source: TradingView.com (click to enlarge)

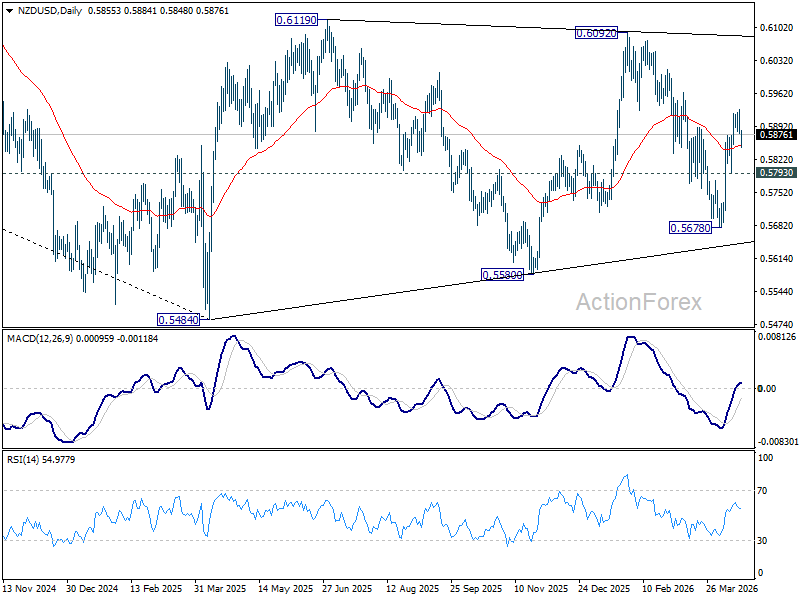

NZD/USD Eyes CPI as RBNZ Assess Pre-Shock Inflation Pressures

New Zealand inflation data will be a major focus in the upcoming Asian session. Q1 CPI may show modest cooling, but the real question is whether inflation was already sticky before the oil shock hit. With the Iran conflict only beginning to impact energy prices late in the quarter, Q1 data will offer a relatively clean read on underlying inflation dynamics before the full effect of recent supply shocks.

Forecasts are narrowly split. Headline CPI is expected to ease from 3.1% yoy to around 2.9–3.1% yoy, but that range masks uncertainty beneath the surface. Markets are less focused on the headline print and more on non-tradables inflation, which captures domestic price pressures tied to wages and services.

This is where the policy implications become more significant. The Reserve Bank of New Zealand has already shifted toward a more cautious, hawkish stance, signaling it will “look through” direct fuel price impacts but not tolerate "second-round effects". If underlying inflation is already proving sticky in Q1, it would raise the risk that the upcoming energy shock feeds more aggressively into broader pricing.

“Q1 is signal, Q2 is confirmation.” That framework is central to how markets are approaching this release. Q1 sets the baseline for underlying inflation, while Q2 will reveal how much of the energy-driven price pressure is transmitted through the economy. A firm Q1 print would therefore amplify concerns about inflation persistence rather than alleviate them.

If non-tradables inflation remains elevated, the RBNZ may be pushed closer to resuming tightening, potentially bringing forward expectations for a rate hike in Q3. Even without a headline surprise, underlying stickiness would be enough to shift the policy outlook.

For NZD/USD, the rebound from 0.5678 suggests the prior decline from 0.6092 has completed in the near term. Yet, the broader structure remains one of consolidation (from 0.5484) within a larger downtrend. While gains may extend as long as 0.5793 holds, resistance at 0.6092–0.6119 is likely to cap upside.

On the downside, break of 0.5793 will bring deeper fall to 0.5678 support first. Further break there will argue that the down trend from 0.7463 (2021 high) is ready to resume through 0.5484 (2025 low).

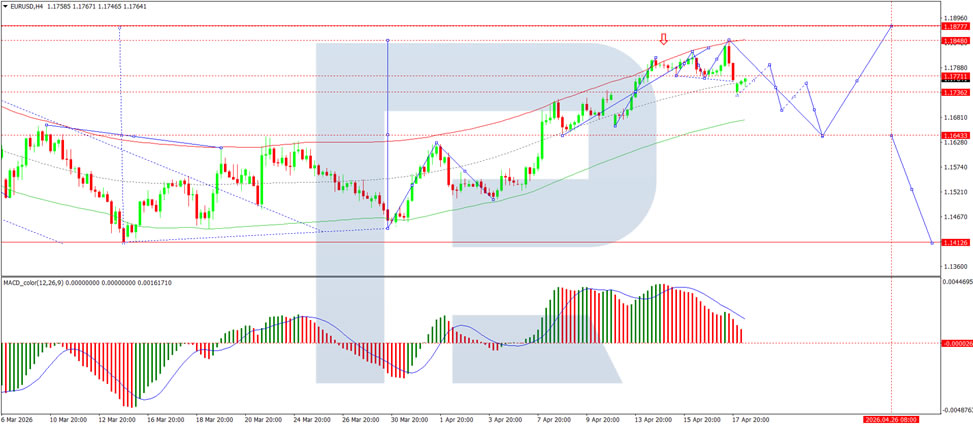

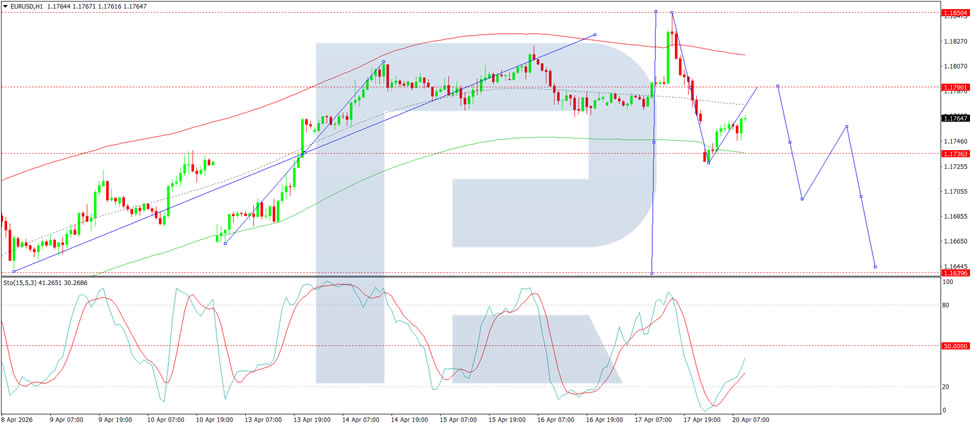

EUR/USD Starts the Week Higher, but the Outlook Remains Unstable

EUR/USD moved higher on Monday after a correction, trending towards 1.1759. Earlier, the US dollar had partially regained ground following last week's decline, supported by increased demand for safe-haven assets amid an escalation of the US-Iran conflict.

Donald Trump reported that the US Navy opened fire and detained an Iranian ship in the Gulf of Oman after it failed to comply with orders when leaving the Strait of Hormuz.

Tehran, in turn, abandoned plans to open the strait after Washington failed to lift the blockade of Iranian ports. Iran also signalled it would not participate in the second round of talks.

The protracted conflict is increasing risks to energy supplies, intensifying inflationary pressure, and reducing the likelihood of policy easing. Markets are revising their expectations, with the probability of a Fed rate cut diminishing this year.

The baseline scenario now assumes rates will remain unchanged in the coming months, likely through the end of 2026.

Technical Analysis

On the H4 chart of EUR/USD, the market is forming a consolidation range around the 1.1800 level, currently extending down to 1.1737. An upward wave to 1.1790 is likely. Subsequently, a downward wave to 1.1700 could develop. Technically, this scenario is confirmed by the MACD indicator, with its signal line above the zero level but pointing firmly downwards, reflecting continued bearish momentum with the potential for the downward trend to persist.

On the H1 chart, the market is forming the structure of the next upward wave to the 1.1790 level. After reaching this level, a correction to 1.1700 is likely, followed by a possible rise to 1.1745. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below 50 and pointing firmly upwards towards 80.

Conclusion

EUR/USD has opened the week on a positive note, but the outlook remains fragile following renewed escalation in the US-Iran conflict. Trump's announcement of a naval incident in the Gulf of Oman and Tehran's withdrawal from planned talks and efforts to reopen the Strait of Hormuz have revived geopolitical risks. Energy supply concerns are intensifying inflationary pressures, pushing Fed rate cut expectations further out, with rates now expected to remain on hold through 2026. While technical indicators suggest a short-term bounce towards 1.1790, the broader bearish momentum appears intact, and any sustained euro strength would likely require a genuine de-escalation of the conflict.

DAX Uptrend at Risk from Fundamentals

March proved to be one of the weakest months for the German index in recent years, though conditions stabilised by mid-April. At present, the DAX (Germany 40 mini on FXOpen) is showing a solid recovery, trading around 24,650. The rebound has been largely driven by gains in Rheinmetall and Infineon, highlighting investor preference for defence and technology stocks amid the current geopolitical backdrop.

The index remains highly sensitive to developments around the Strait of Hormuz. Ongoing reports of blockades and resumptions in shipping continue to fuel uncertainty in energy markets, directly affecting costs for German industry. At the same time, ECB policy remains a limiting factor: the central bank has kept rates at 2.0%, and despite inflation concerns, markets are not pricing in easing before the summer.

Technical picture

After reaching highs near 25,500 in January 2026, the index entered a sharp correction phase. A gap on 2 March signalled a shift in sentiment, prompting traders to close long positions. On 9 March, an extreme spike in vertical volume was recorded as the market attempted to break below 23,000. The index later tested strong support at 22,000, where heavy buying emerged and a base began to form.

Following the rebound, the price consolidated above the POC zone of 23,500–23,800, which has since turned into support. Volume levels have normalised after the March volatility, suggesting that panic selling has subsided. The RSI indicator confirms improving momentum, rising to 64.9 and holding above its moving averages, pointing to renewed bullish strength. The next key resistance for buyers stands at 25,000.

Summary

Holding above the POC zone has restored a bullish structure, returning control to buyers. The 23,000 level is now shaping up as a strong support area, while RSI with MA signals recovering demand. However, despite the current rebound, the broader fundamental backdrop remains mixed, with geopolitical risks and ECB policy expectations continuing to influence the index’s trajectory.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

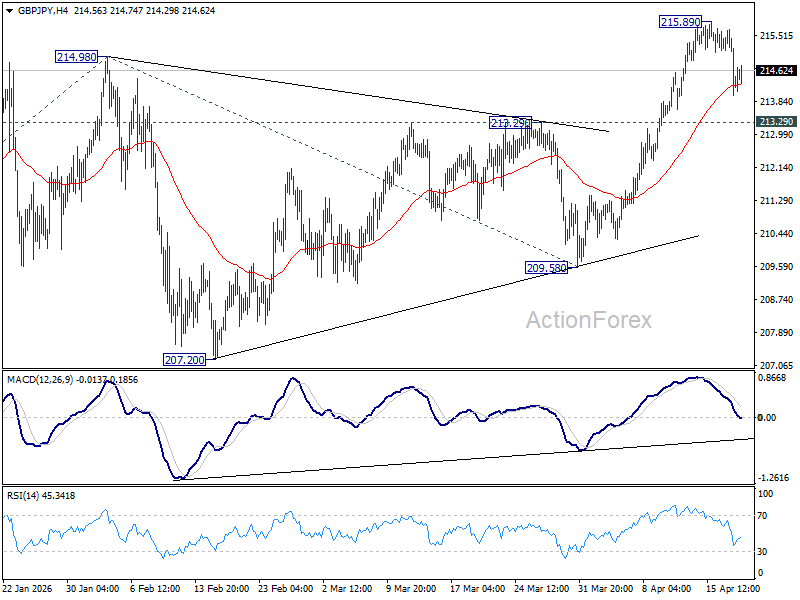

GBP/JPY Daily Outlook

Daily Pivots: (S1) 213.74; (P) 214.72; (R1) 215.43; More...

Intraday bias in GBP/JPY remains neutral for the moment, and more consolidations could be seen below 215.89. Further rise is expected as long as 213.29 resistance turned support holds. Firm break of 215.89 will resume larger up trend to 61.8% projection of 199.04 to 214.98 from 209.58 at 219.43.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 204.83) holds, even in case of another deep pullback.

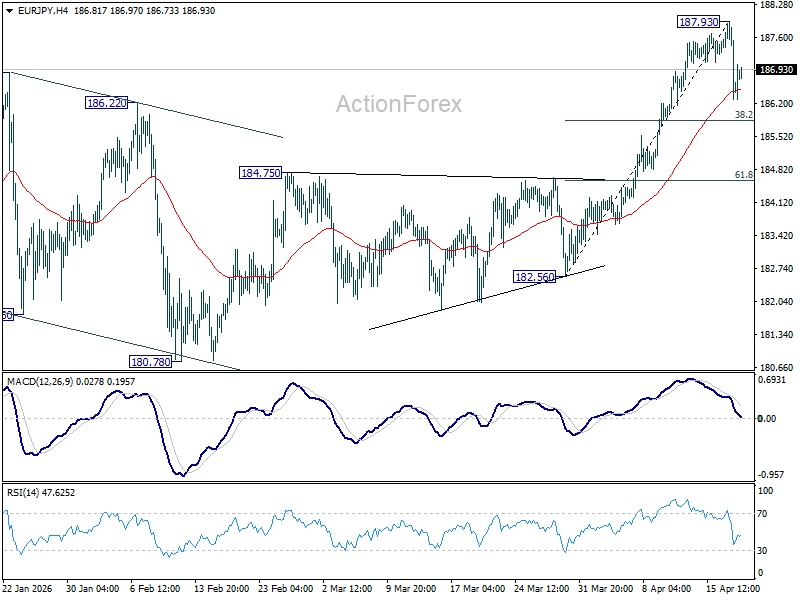

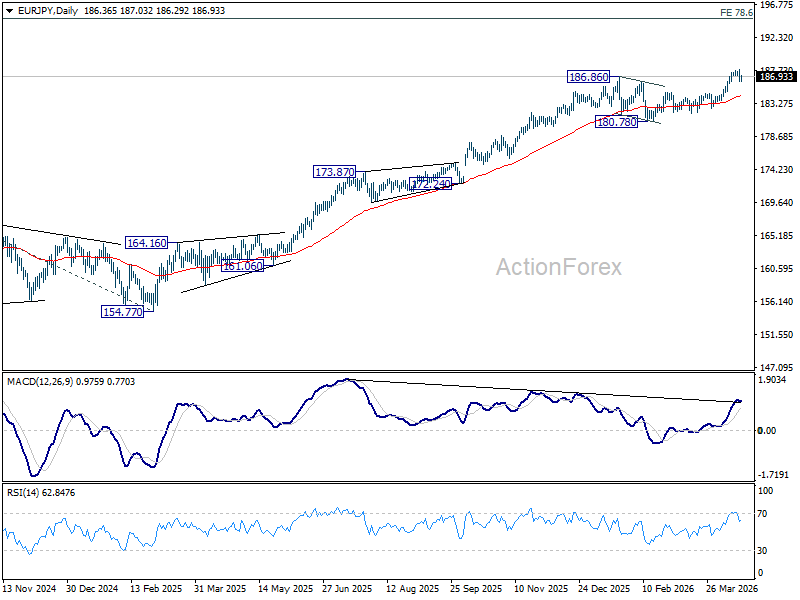

EUR/JPY Daily Outlook

Daily Pivots: (S1) 185.99; (P) 186.97; (R1) 187.63; More...

Intraday bias in EUR/JPY is turned neutral with current recovery. But more consolidations could be seen below 187.93 short term top. Another fall might be seen to 38.2% retracement of 182.56 to 187.93 at 185.87. On the upside, though, break of 187.93 will resume larger up trend.

In the bigger picture, up trend from 114.42 (2020 low) is in progress Next target is 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. For now, medium term outlook will stay bullish as long as 180.78 support holds, even in case of deeper pullback.

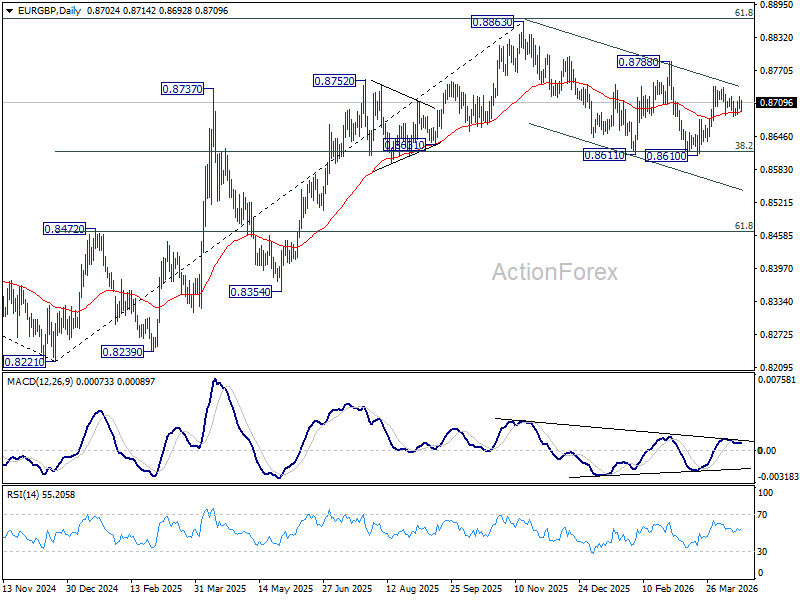

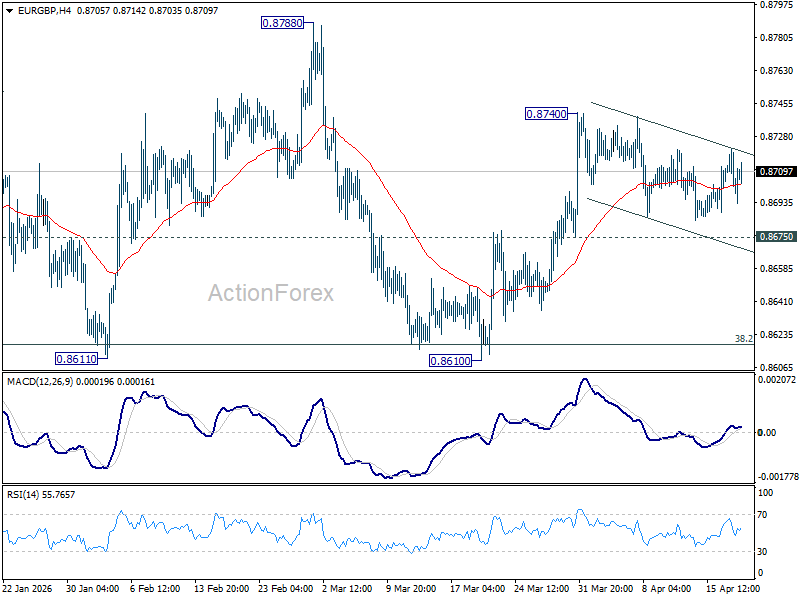

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8693; (P) 0.8710; (R1) 0.8719; More…

Intraday bias in EUR/GBP remains neutral and more consolidations could be seen below 0.8740. As long as 0.8675 support holds, further rise remains mildly in favor. On the upside, break of 0.8740 will resume the rally from 0.8610 to 0.8788 resistance. However, firm break of 0.8675 will turn bias back to the downside for retesting 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be ready to resume through 0.8863 (2025 high). Nevertheless, sustained trading below 0.8618 should confirm bearish reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.