Sample Category Title

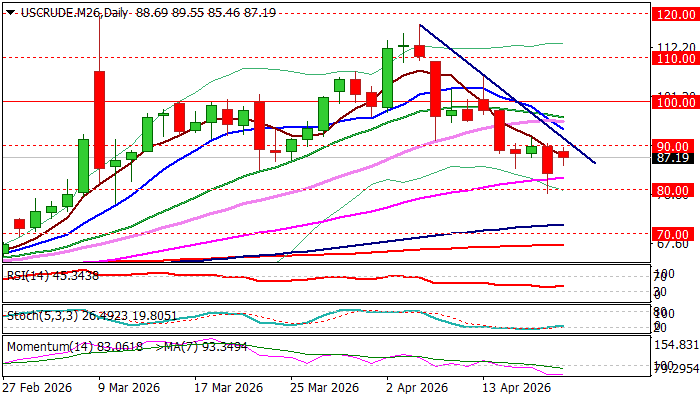

WTI Oil – Bearish Bias Below $90 Barrier

WTI oil opened $5 higher and gained over 6% at the start of the week, as “Trump Indicator” (one of key fundamental market drivers nowadays) changed direction during the weekend on fresh tensions over Strait of Hormuz, which was opened on Friday and closed again shortly after.

Today’s price jump partially offset optimism, sparked by Friday’s price drop of about 10% that hit the lowest since early March.

Although the overall picture has been darkened by the latest developments that raise fears of fresh escalation (that may have strong negative impact, not only on the region, but the global economy) technical picture on daily chart is expected to remain bearishly aligned while the price stays below $90 barrier (which caps upticks for the fourth consecutive session).

Negative momentum studies and the action weighed by two consecutive large bearish weekly candles, contribute to such scenario, but situation on the battlefield (extended ceasefire and peace talks or fresh escalation) is likely to have a key impact on crude oils’ price direction.

Repeated daily close below $90 to maintain slight bearish bias and risk retest of 55DMA ($82.63) guarding more significant $80/$79 zone, break of which to confirm signal of bearish continuation.

On the other hand, sustained break above $90 would provide relief, but extension above $94 will be needed to confirm the signal.

Res: 90.00; 91.80; 92.46; 93.71

Sup: 84.50; 82.63; 80.00; 79.00

Eco Data 4/21/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 22:00 | NZD | NZIER Business Confidence Q1 | -4 | 48 | ||

| 22:45 | NZD | CPI Q/Q Q1 | 0.90% | 0.80% | 0.60% | |

| 22:45 | NZD | CPI Y/Y Q1 | 3.10% | 2.90% | 3.10% | |

| 06:00 | GBP | Claimant Count Change Mar | 26.8K | 21.4K | 24.7K | 17.1K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | 4.90% | 5.20% | 5.20% | |

| 06:00 | GBP | Average Earnings Excl Bonus 3M/Y Feb | 3.60% | 3.50% | 3.80% | |

| 06:00 | GBP | Average Earnings Incl Bonus 3M/Y Feb | 3.80% | 3.60% | 3.90% | 4.10% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | -17.2 | -6.7 | -0.5 | |

| 09:00 | EUR | Germany ZEW Current Situation Apr | -73.7 | -69.5 | -62.9 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | -20.4 | -10.3 | -8.5 | |

| 12:30 | USD | Retail Sales M/M Mar | 1.70% | 1.30% | 0.60% | 0.70% |

| 12:30 | USD | Retail Sales ex Autos M/M Mar | 1.90% | 1.30% | 0.50% | 0.70% |

| 14:00 | USD | Pending Home Sales M/M Mar | 1.50% | 0.00% | 1.80% | 2.50% |

| 14:00 | USD | Business Inventories Feb | 0.40% | 0.10% | -0.10% | 0.00% |

| 22:00 | NZD |

| NZIER Business Confidence Q1 | |

| Actual | -4 |

| Consensus | |

| Previous | 48 |

| 22:45 | NZD |

| CPI Q/Q Q1 | |

| Actual | 0.90% |

| Consensus | 0.80% |

| Previous | 0.60% |

| 22:45 | NZD |

| CPI Y/Y Q1 | |

| Actual | 3.10% |

| Consensus | 2.90% |

| Previous | 3.10% |

| 06:00 | GBP |

| Claimant Count Change Mar | |

| Actual | 26.8K |

| Consensus | 21.4K |

| Previous | 24.7K |

| Revised | 17.1K |

| 06:00 | GBP |

| ILO Unemployment Rate (3M) Feb | |

| Actual | 4.90% |

| Consensus | 5.20% |

| Previous | 5.20% |

| 06:00 | GBP |

| Average Earnings Excl Bonus 3M/Y Feb | |

| Actual | 3.60% |

| Consensus | 3.50% |

| Previous | 3.80% |

| 06:00 | GBP |

| Average Earnings Incl Bonus 3M/Y Feb | |

| Actual | 3.80% |

| Consensus | 3.60% |

| Previous | 3.90% |

| Revised | 4.10% |

| 09:00 | EUR |

| Germany ZEW Economic Sentiment Apr | |

| Actual | -17.2 |

| Consensus | -6.7 |

| Previous | -0.5 |

| 09:00 | EUR |

| Germany ZEW Current Situation Apr | |

| Actual | -73.7 |

| Consensus | -69.5 |

| Previous | -62.9 |

| 09:00 | EUR |

| Eurozone ZEW Economic Sentiment Apr | |

| Actual | -20.4 |

| Consensus | -10.3 |

| Previous | -8.5 |

| 12:30 | USD |

| Retail Sales M/M Mar | |

| Actual | 1.70% |

| Consensus | 1.30% |

| Previous | 0.60% |

| Revised | 0.70% |

| 12:30 | USD |

| Retail Sales ex Autos M/M Mar | |

| Actual | 1.90% |

| Consensus | 1.30% |

| Previous | 0.50% |

| Revised | 0.70% |

| 14:00 | USD |

| Pending Home Sales M/M Mar | |

| Actual | 1.50% |

| Consensus | 0.00% |

| Previous | 1.80% |

| Revised | 2.50% |

| 14:00 | USD |

| Business Inventories Feb | |

| Actual | 0.40% |

| Consensus | 0.10% |

| Previous | -0.10% |

| Revised | 0.00% |

Sunset Market Commentary

Markets

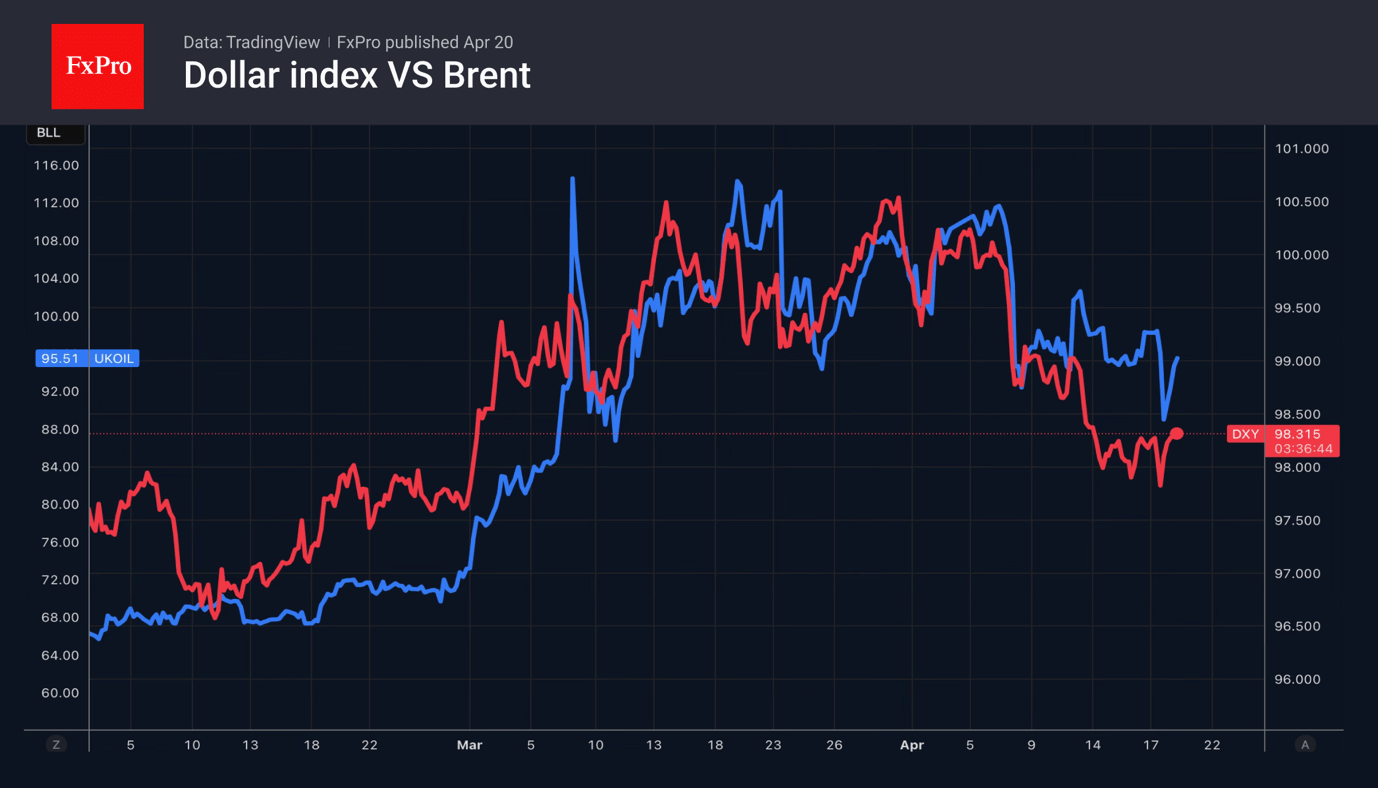

After the unjustified optimism on an ‘orderly’ end to the conflict between the US and Iran going into the weekend, markets at the start of the new week are facing again a lack of visibility on the next steps in the conflict. This a fortiori applies to the conditions and the nature of any reopening of the Strait of Hormuz. Economic analysts in this context also have to resort to guesstimates on the timing of any repair of energy and other supply chain disruptions that will determine the economic fall-out on the world economy. The end of a two-week ceasefire Tuesday evening is the next high profile deadline. New talks are expected to take place ahead of this deadline in Pakistan. However, Iran reclaiming an earlier promise to open de Strait of Hormuz and the US maintaining the blockade of Iran ports and seizing an Iranian ship illustrate the division/distrust between the parties involved. Markets today show the logic Pavol reaction that can be expected in case of such a U-turn in sentiment. Brent oil, still the most symbolic pointer on potential economic disruption due to the conflict, hovers near $95/b to be compared with levels below $90 at some point on Friday. Despite the substantial repositioning compared to Friday, intraday volatility remained rather low. Is this again some kind of agnosticism on yet another U-turn in the scenario of the conflict?. Or is it markets holding some complacency/hope that the bar for both sides to return to outright military hostilities has become high? Time will tell. European equites return part of Friday’s gain (Eurostoxx 50 -1% after a 2%+ gain on Friday). US indices open with losses of about 0.25%/0.5%. It’s all about assessing difficult to measure political probabilities, but also here, the damage/disappointment could have been more outspoken. Yields in the US and European opened higher, but momentum dwindled as the session continued. Markets are holding to the view that most central banks will take their time to assess the economic impact (both on inflation and growth) before adapting policy when deemed necessary later. Next week’s policy meetings of the Fed, the ECB and the BoE in this respect are seen as coming too already to trigger any preemptive action, especially with oil prices holding below $100/b. US yields today add between 0.5 bps (30-y) and 1.5. bps (2-y). EMU swap yields are rising between 4 bps (2-y) and 1.5 bps (30-y), only a fraction of Friday’s decline. On FX markets, the dollar failed to extend/hold gains at the open this morning. DXY trades near 98.2, with any bottoming out process still lacking any convincing follow-through price action. EUR/USD after an early session dip trades little changed near 1.1765. USD/JPY gains modestly (158.7), with underlying yen softness still keep the pair within reach of the 160 barrier. The US currency apparently ‘needs’ higher risk-aversion and/or higher oil prices to really regain momentum.

News & Views

Canadian inflation accelerated from 0.5% M/M to 0.9% in March with the annual number jumping from 1.8% to 2.4%. Markets feared an even bigger rise (1.1% M/M & 2.6%). Details showed gasoline prices rising by a record 21.2% M/M and oil prices by 2.6% M/M. Core inflation (ex-food and energy) rose a modest 0.1% M/M & 1.9% Y/Y, also printing below consensus (2.2% Y/Y). The Bank of Canada’s preferred trimmed mean slowed from 2.3% Y/Y to 2.2% Y/Y. There remained lingering base-year effects from the GST/HST break which ran from December 2024 to February 2025, resulting in downward pressure on headline inflation in March 2026. The Canadian central bank is expected to hold policy unchanged when it meets next week. Governor Macklem last week indicated that his main concern is longer-term inflation expectations. He sounded vigilant in not allowing the energy shock to spread.

Slovenia PM Golob admitted that his party was unable to form a government. Golob’s liberal party won last month’s national election by a razor-thin margin. The Freedom Movement won 29 out of 90 seats, beating outgoing PM Jansa’s (Orban ally, Trump adept, Russian sympathy) populist party which secured 28 seats. Jansa might now seek a return to office by setting up a centre-right coalition. He earlier indicated all options were comfortable for his party, forming a government, remaining in the opposition (ruled out now) or participating in new elections.

Another Week, Another Gap Down for EURUSD

- The escalation of the conflict in the Middle East has boosted demand for the US dollar.

- Washington and Tehran may be strengthening their positions ahead of negotiations.

The US dollar opened the week with a 0.2% gap upwards, driven by increased demand for safe-haven assets. EURUSD has opened with a downward gap for the second five-day period in a row due to signs of an escalating conflict in the Middle East. First, talks between the US and Iran broke down; now, reports suggest a second round may not take place. No sooner had Tehran announced the opening of the Strait of Hormuz to commercial vessels than the Americans seized one of its tankers. However, it should be noted that the initial fear is being washed out of the market rather quickly. It seems that major players are discerning positive dynamics amidst this chaos.

On Tuesday, 21 April, the ceasefire expires. Donald Trump is threatening further air strikes if Iran does not agree to a deal. Investors realise they have gone too far in their desire to jump onto the last carriage of the EURUSD train heading north. The markets, like the US president, have been mistaking wishful thinking for reality. It is time to shed these illusions. An escalation of the conflict in the Middle East risks triggering a renewed rally in oil and the USD index.

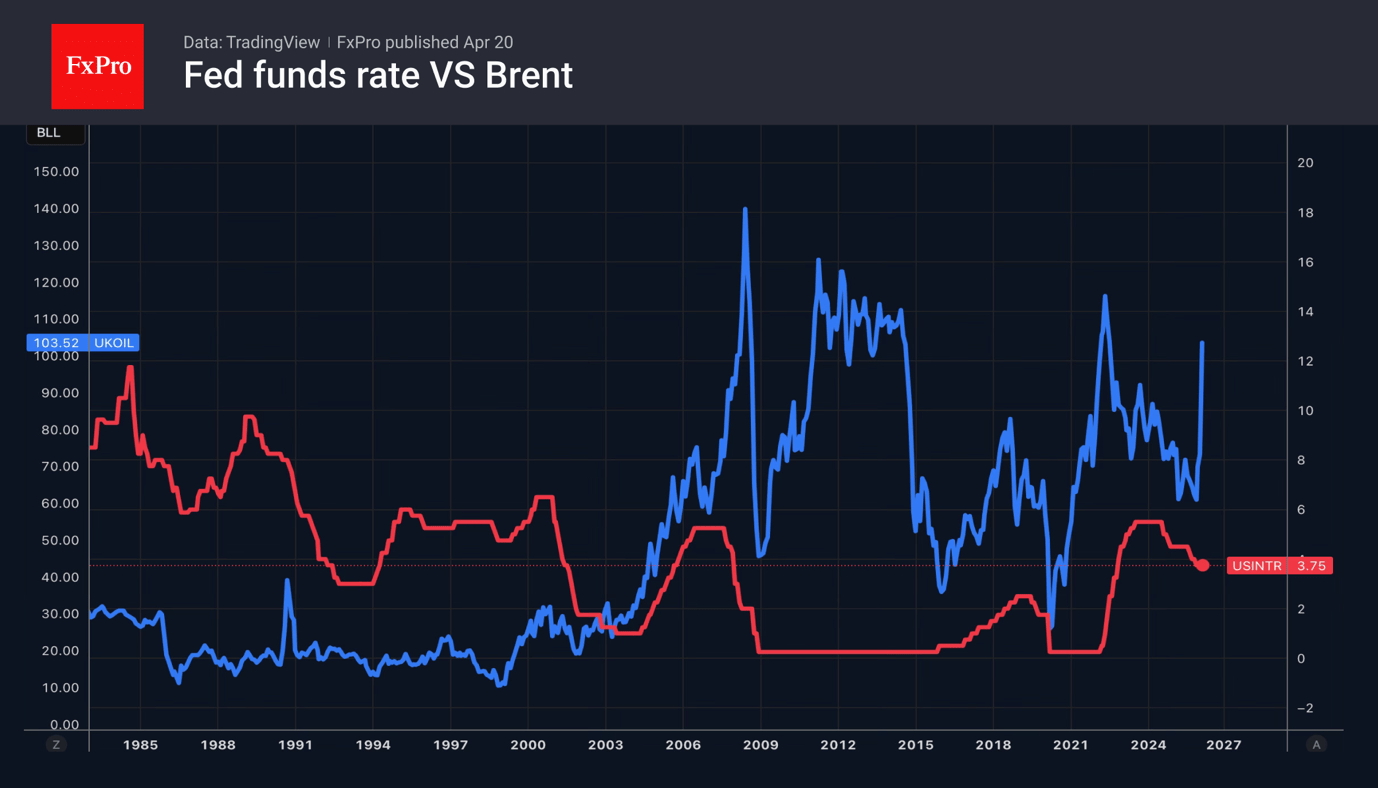

The longer the Strait of Hormuz remains blocked, the worse the consequences for the global economy will be. The threat of soaring consumer prices is becoming increasingly real. According to FOMC member Christopher Waller, if inflationary risks outweigh the risks of unemployment, the Fed will have to keep rates at their current level even if the labour market continues to cool. If one of the central bank’s key ‘doves’ says so, the others may start to consider tightening monetary policy. This would support the US dollar.

Signs of stagflation may emerge in the economic calendar. Data on business activity in the eurozone, the UK and the US could signal accelerating inflation and slowing economic growth. This would put central banks in an extremely difficult position. Given the ECB’s reluctance to raise its key rate in April, this could provide an opportunity for the bears to launch a counterattack on EURUSD.

The strengthening of the US dollar has caused gold to retreat on fears of accelerating inflation, which will force central banks, led by the Fed, to tighten monetary policy. However, traders are in no hurry to force the issue. The aggressive rhetoric from Washington and Tehran may be nothing more than a desire to strengthen their own positions ahead of the negotiations.

Oil Prices Boost Canadian Inflation in March

Headline CPI inflation jumped up to 2.4% year-on-year (y/y) in March, slightly less than consensus expectations. Higher energy prices were a big part of the story, with inflation ex-energy up a more modest 2.2% y/y.

Prices at the pump soared 21% in March – the largest increase on record. Energy prices as a whole were 3.9% higher versus a year ago, an about face from being down 9.3% y/y in February. But energy prices a year ago still included the consumer carbon levy, which was removed in April 2025. So the impact of energy on inflation is set to get much larger in next month's data.

Inflation for other key consumer essentials picked up. Grocery inflation picked up again to 4.4% y/y in March, up from 4.1% in February. Shelter inflation also picked up slightly, rising 1.7% y/y, up from 1.5% y/y in February. Despite this, overall services inflation cooled further to 2.5% y/y.

The Bank of Canada has focused on broader "underlying inflation" recently, but the official core inflation metrics (median and trim), cooled slightly in March to 2.3% y/y. Zeroing in on trends over the past three months, trim and median inflation continued to run well below the Bank of Canada's 2% target.

Key Implications

As expected, higher oil prices boosted Canadian inflation in March. Oil prices have fallen in recent days but remain nearly 40% higher than a year ago. That means energy prices are likely to keep headline inflation elevated for some time. April's inflation reading is likely to head much higher as the dampening effect of the removal of the consumer carbon levy falls out of the year-on-year inflation calculation.

Given a generally soft economic backdrop in Canada, we expect the effect on core prices should be more modest. Core inflation is expected to stay reasonably close to the 2% target on a year-on-year basis this year. The Bank of Canada is widely expected to leave its key policy rate unchanged at 2.25% at next week's announcement. We will be listening closely for the Bank's assessment of the impact of the spike in oil prices on Canada's economy.

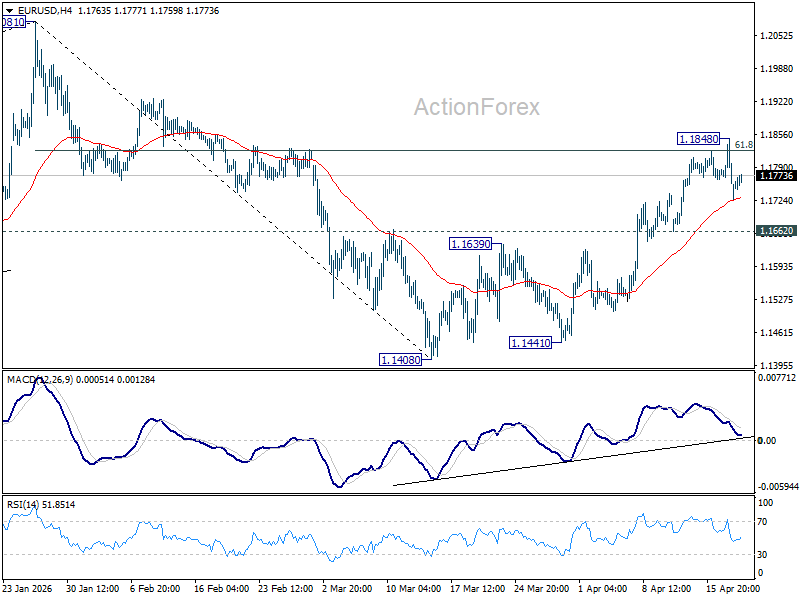

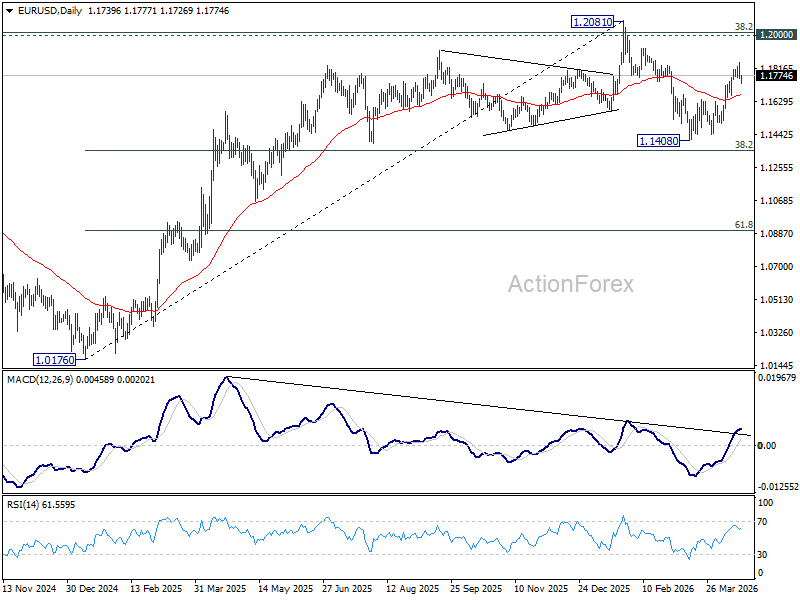

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1733; (P) 1.1792; (R1) 1.1823; More….

EUR/USD is still extending consolidations below 1.1848 and intraday bias remains neutral. Further rally is in favor as long as 1.1662 support holds. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will bring deeper decline back towards 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

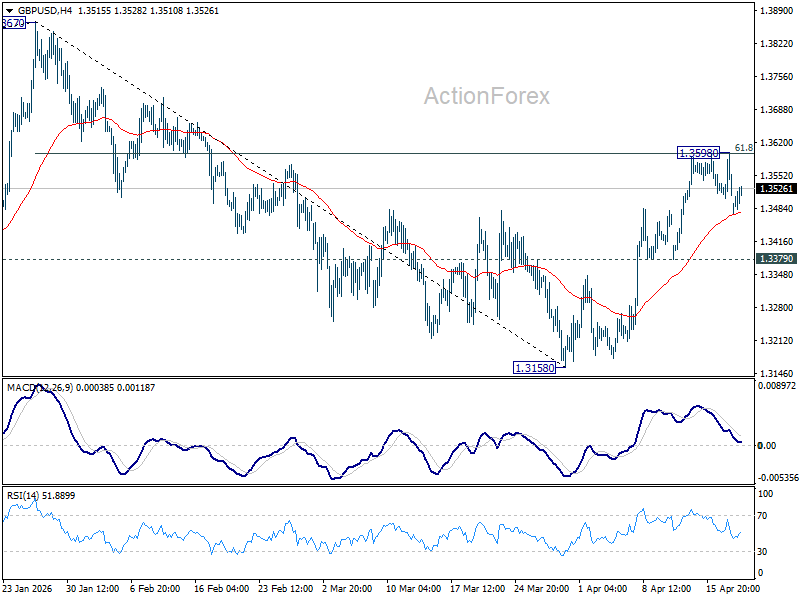

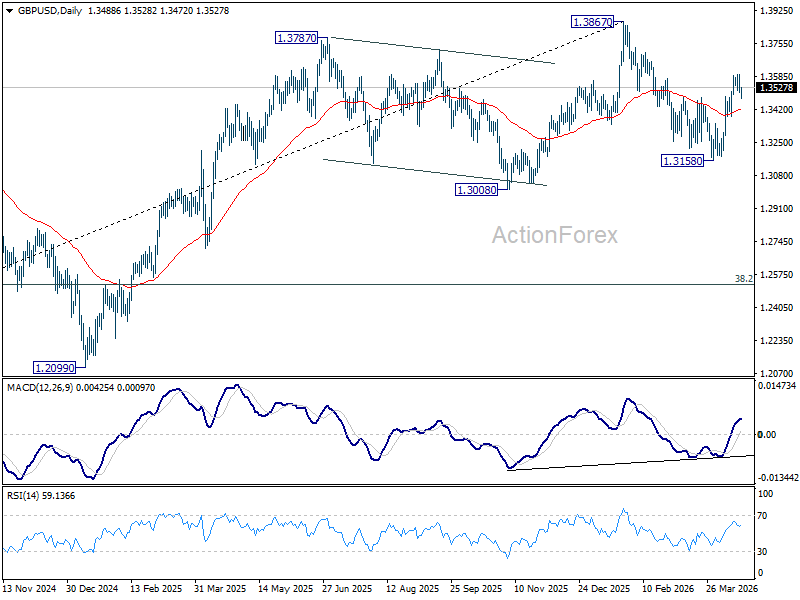

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3480; (P) 1.3540; (R1) 1.3575; More...

GBP/USD is still extending consolidations below 1.3598 and intraday bias remains neutral. Further rise is in favor as long as 1.3379 support holds. Sustained break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, firm break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

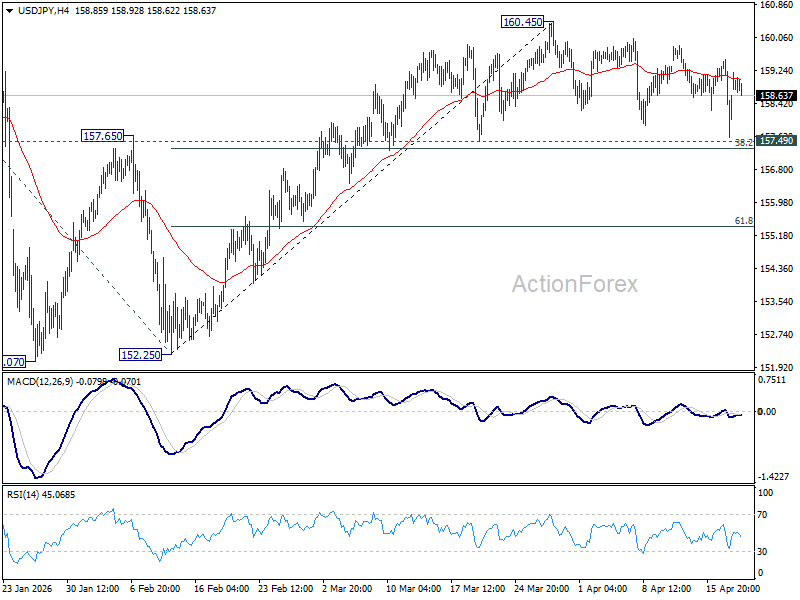

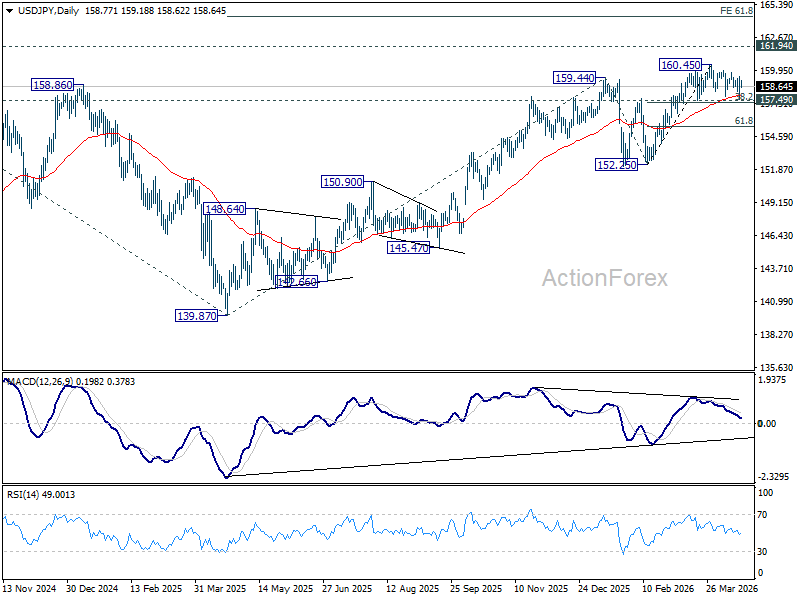

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.63; (P) 158.58; (R1) 159.56; More...

Intraday bias in USD/JPY remains neutral at this point, as consolidations continue below 160.45 short term top. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.80) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

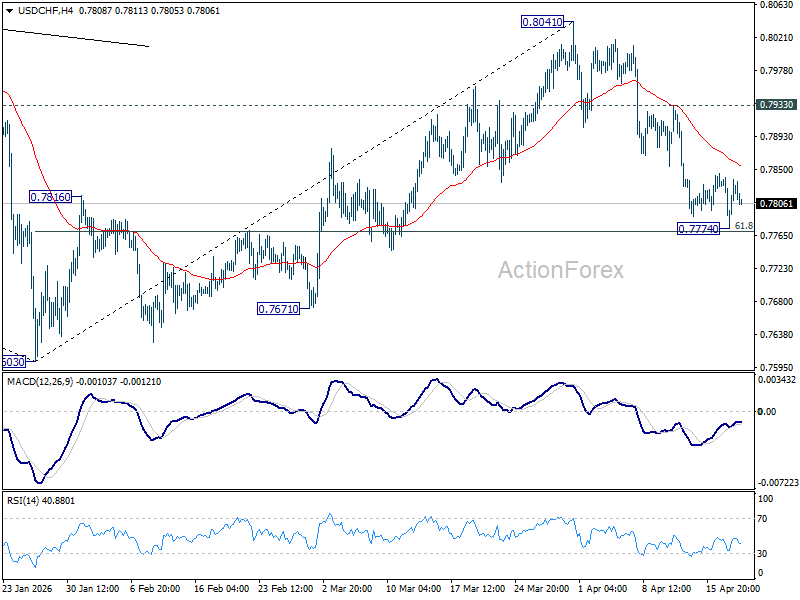

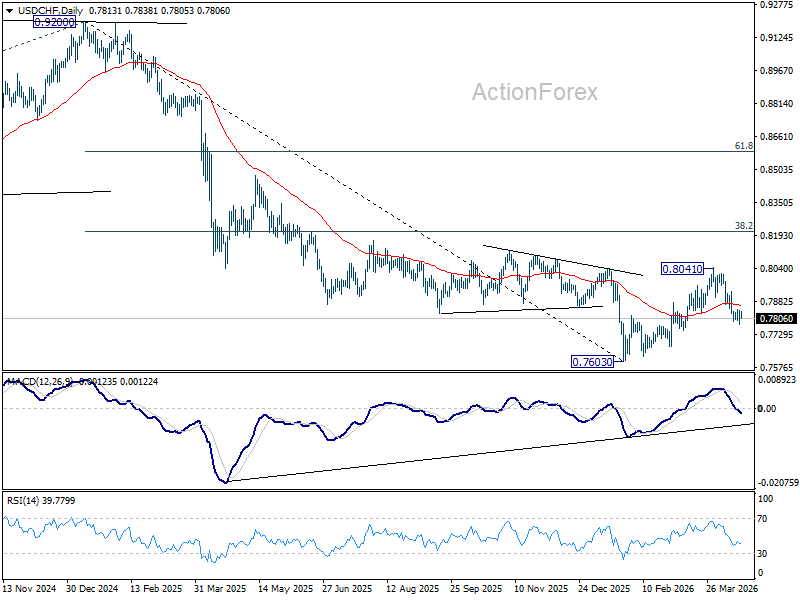

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7780; (P) 0.7811; (R1) 0.7847; More….

USD/CHF is staying consolidations above 0.7774 temporary low and intraday bias remains neutral. Upside of recovery should be limited below 0.7933 resistance to bring another fall. Sustained break of 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will resume the decline from 0.8041 to retest 0.7603 low.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8059) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

Markets on Hold Pending US–Iran Talks, Warsh Fed Chair Hearing Next Catalyst

Markets are broadly steady today as traders hold back from taking directional positions, waiting for clarity on whether a second round of US–Iran talks will take place in Islamabad before the April 22 ceasefire deadline. Despite rising geopolitical tension, price action across assets suggests a clear lack of conviction.

The ceasefire is visibly fraying, with multiple escalations in recent days, yet markets are not reacting decisively. The key reason is simple: there is still no confirmation on whether talks will proceed. Until there is a definitive “go” or “no-go” signal, the situation remains unresolved from a trading perspective.

This leaves markets stuck in a holding pattern. Dollar strength seen earlier on geopolitical headlines has faded without follow-through, reflecting hesitation rather than conviction. Traders are unwilling to chase moves that could quickly reverse depending on diplomatic developments.

Equities tell a similar story. Major European indices are trading lower and US futures are in the red, but losses remain limited. The absence of aggressive selling suggests that investors are adjusting to rising risks, rather than pricing in a full escalation scenario.

Oil remains the clearest signal—and it is not confirming escalation. Prices jumped as the “peace trade” receded, but remain below the critical $100 level. As long as that threshold holds, markets are reluctant to shift into full risk-off positioning.

In currency markets, positioning reflects caution rather than conviction. Swiss Franc leads gains, followed by Dollar, while risk-sensitive currencies like Aussie and Kiwi lag. The distribution suggests a mild defensive bias, but not a full shift into risk aversion.

While geopolitics dominates the immediate outlook, a second catalyst is approaching from the policy side. Kevin Warsh is set to appear before the Senate Banking Committee on April 21 for his nomination hearing to become the next Federal Reserve Chair, succeeding Jerome Powell when his term ends on May 15. The timing is tight, and the process is far from straightforward.

Warsh is widely seen as a credible candidate with deep ties to financial markets and the Republican establishment. However, his confirmation path is complicated by political dynamics that go beyond standard nomination procedures. The Senate Banking Committee remains narrowly divided, meaning even a single Republican defection could derail the process.

The most immediate obstacle is Thom Tillis, who has publicly stated he will block any Federal Reserve nominations until the Department of Justice investigation into Powell is dropped. In a 13–11 committee split, Tillis effectively holds a deciding vote. Without his support, Warsh’s nomination may not even reach the full Senate floor.

On the other side, Democrats led by Elizabeth Warren have called for a delay in the hearing, arguing it is inappropriate to confirm a successor while the sitting Chair is under active investigation. Combined with earlier procedural delays, the risk is that the confirmation timeline slips dangerously close to Powell’s May 15 exit, raising the prospect of leadership uncertainty at the Fed—an issue that markets are not yet pricing, but cannot ignore for long.

For now, markets are waiting. Without confirmation on US–Iran talks, there is little incentive to commit. But if geopolitical signals remain inconclusive, attention may quickly shift toward policy uncertainty as the next driver.

Canada Inflation Jumps to 2.4% yoy in March, Gasoline Prices Up Record 21.2% mom

Canada inflation jumped to 2.4% in March as gasoline prices surged a record 21.2% on the month. The spike highlights how energy shocks are pushing headline inflation higher—even as underlying pressures remain more contained. Read More.

NZD/USD Eyes CPI as RBNZ Assess Pre-Shock Inflation Pressures

NZ CPI may show cooling inflation—but the real question is whether it was already sticky before the oil shock. With core inflation in focus, the data could shift RBNZ rate expectations and drive the next move in NZD/USD. Read More.

China Holds LPR Steady for 11th Month, Signals Stability Amid Global Risks

China kept its benchmark lending rates unchanged for an 11th straight month, reinforcing a cautious stance as policymakers balance growth support against rising global risks. With the PBoC signaling a “moderately loose” policy bias but prioritizing currency stability, markets are watching how Beijing navigates geopolitical and trade tensions. Read More.

New Zealand Posts NZD 698M Trade Surplus as China, Australia Drive Export Growth

New Zealand’s trade surplus held at NZD 698M in March as exports climbed on strong demand from China and Australia, but a faster surge in imports signals rising domestic demand and cost pressures. Read More.

Gold Drops as Ceasefire Cracks, But Oil Says Markets Aren’t Pricing War Yet

Gold drops as US–Iran ceasefire cracks, but oil below $100 signals markets aren’t pricing war. Fading momentum leaves gold vulnerable to a deeper move toward the 4,000 level if tension turns into conflicts. Read More.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7780; (P) 0.7811; (R1) 0.7847; More….

USD/CHF is staying consolidations above 0.7774 temporary low and intraday bias remains neutral. Upside of recovery should be limited below 0.7933 resistance to bring another fall. Sustained break of 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will resume the decline from 0.8041 to retest 0.7603 low.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8059) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).